Languages

Pages

Legal

South Carolina Public Charter School District

Performance Framework

Financial Performance

Organizational Performance

Academic Performance

Dana C. Reed, Assistant Superintendent of Performance StandardsCourtney Mills, Director of AccountabilityBobby Rykard, Fiscal Analyst

What is the Performance Framework?

• 3-part document (academic, fiscal, organizational) that sets forth expectations of performance and compliance.

• Basis for school evaluation, monitoring, and intervention that informs the SCPCSD Board’s high- stakes decision making.

Autonomy

Accountability

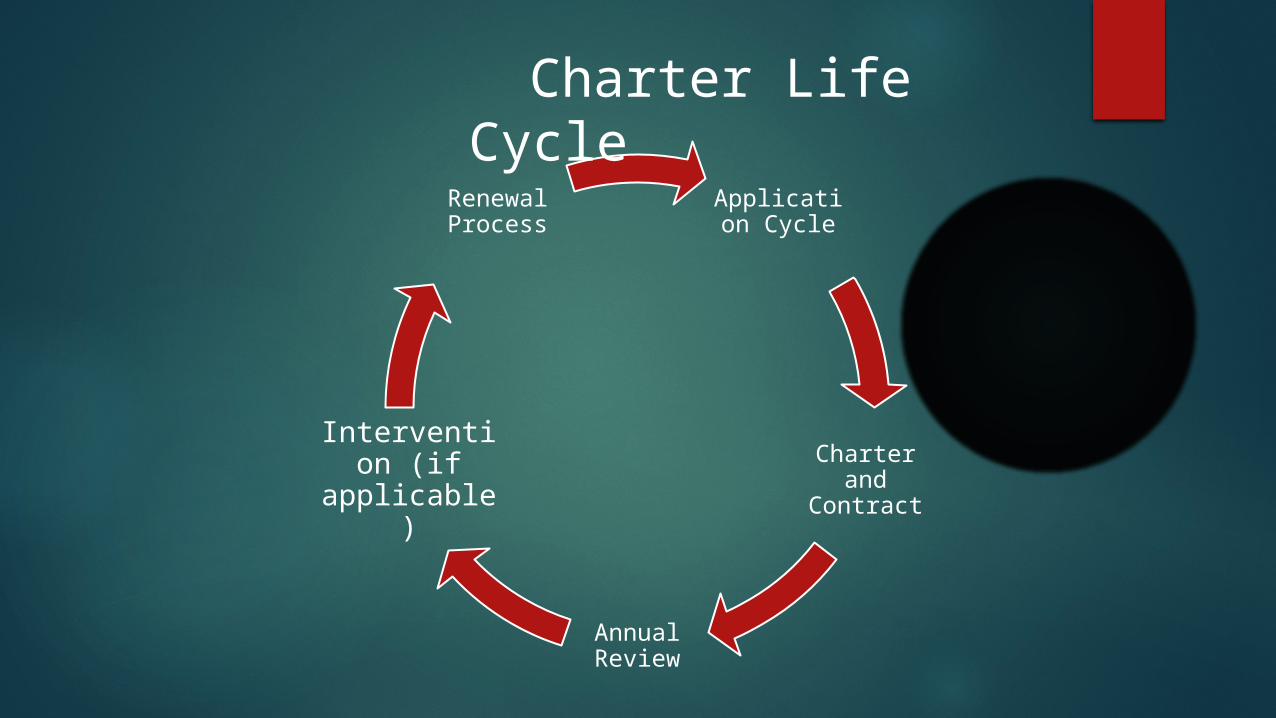

Application Cycle

Charter and

Contract

Annual Review

Intervention (if

applicable)

Renewal Process

Charter Life Cycle

Guiding Questions

Academic Financial Organizational

Is the academic program a success?

Is the school financially

viable?

Is the organization effective and

well run?

Performance Framework

Performance Framework Goals

• Focuses on outcome measures that align with the goal of providing a high-quality education for all students.

• Allows for greater transparency between the SCPCSD and the charter schools it authorizes by setting clear standards for charter school success.

• Provides continuity of charter cycle with consistent language from the application to renewal.

• Allows stakeholders, including SC families, to make informed decisions about charter school performance and quality.

Next Steps

SCPCSD Board approval (August)

TA session for school leaders/board chairs (September)

Development of data collection methods necessary for implementation (Fall)

Implementation year (2014/15)

Issue an annual report to each school (with the exception of first year schools) that reflects how many standards the school exceeded, met, did not meet, or fell far below, depending on the section of the framework (February 2015)

Note

There is a lot of fluidity surrounding academic accountability and that will necessitate revisions to the framework in the future.

For example, HSAP was administered for the last time this summer.

For the first year roll-out of the framework, we will have HSAP data to plug into the framework.

After the first year of implementation, we will need to revise the framework to reflect the assessment that will be secured by the SCDE.

Academic Performance

COURTNEY MILLS

DIRECTOR OF ACCOUNTABILITY

Academic

Perform

ance

“Authorizers are charged with holding schools accountable for high standards of academic performance. This framework focuses purposefully on quantitative academic outcomes as a basis for analysis to be used in high-stakes decisions.”

NACSA Core Performance Framework and Guidance, page 8

“Each authorizer and charter school must enter into a contractual agreement stating that student performance of all students . . . is the most important factor when determining to renew or revoke a school's charter.”

SC Board of Education Regulations 43-601.VII.(B)(2)

Academic Performance

Assessment Data (August) ESEA Grades (October) State Report Cards (November) Annual Report (December) Quarterly Reporting

Academic Data Sources

Student Achievement (Absolute) Student Achievement (Growth) Comparative Performance Post-Secondary Readiness State and Federal Accountability Charter-Specific Academic Performance Goals

Academic Performance Indicators

Financial Performance

ROBERT (BOBBY) RYKARD

FINANCIAL ANALYST Financial

Perform

ance

Bobby Who???

Purpose of Financial Framework

To annually assess the financial health and viability of schools

To provide interventions and on-going monitoring and technical assistance where appropriate based on risk factors

To ensure a sound financial foundation in support of academic achievement

Financial Performance Review Process

Preliminary Review and Preliminary Rating Annually Existing Schools

Quarterly Follow-Up Schools Where Standards Not Met

New Schools as Technical Assistance in First Year

Final Rating – Upon Completion of Follow-Up Analysis

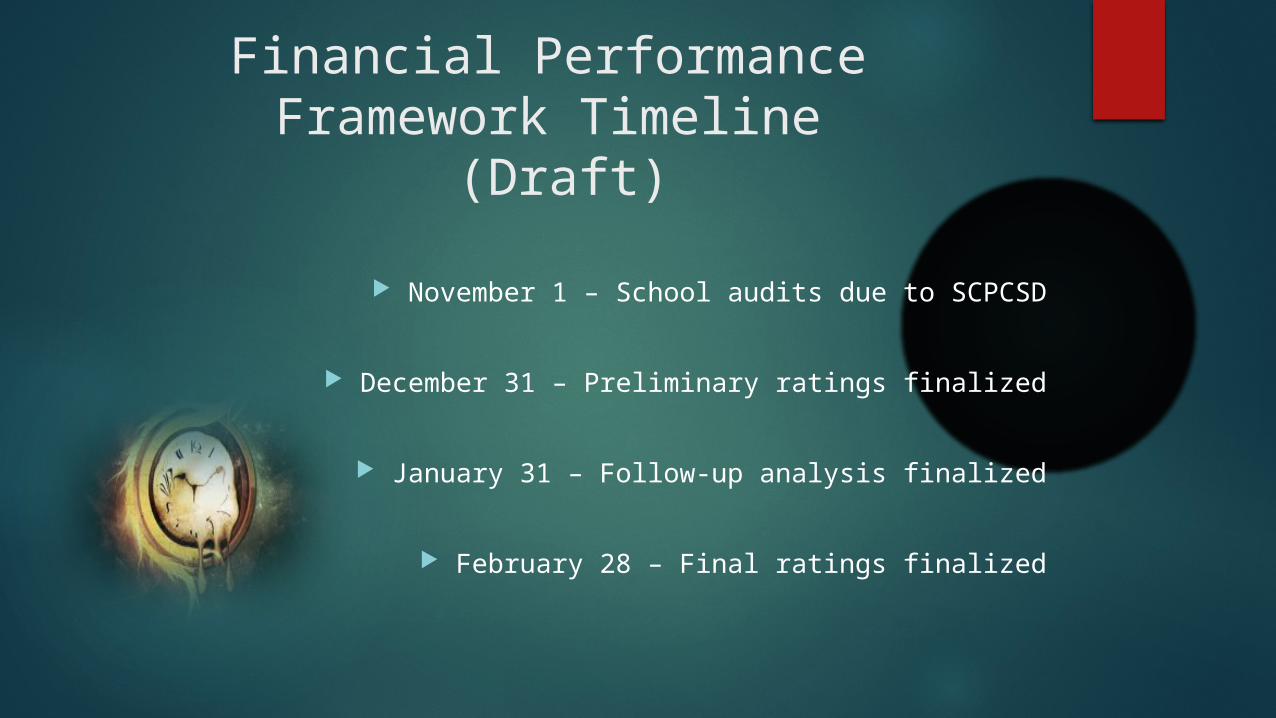

Financial Performance Framework Timeline

(Draft)

November 1 – School audits due to SCPCSD

December 31 – Preliminary ratings finalized

January 31 – Follow-up analysis finalized

February 28 – Final ratings finalized

Preliminary Ratings

Meets Standard Sound Financial Viability

Not Meeting Standard Indicates Some Financial Risk(s)

Far Below Standard Identifies Significant Financial Risk(s)

Requires Further Analysis Potential Financial Risk or Insufficient Information Requiring Additional Review

for Determination

Source Documentation

Audited Financial Statements

Due November 1st to SCPCSD

Using Accrual-Based Accounting

Following Generally Accepted Accounting Principles (GAAP)

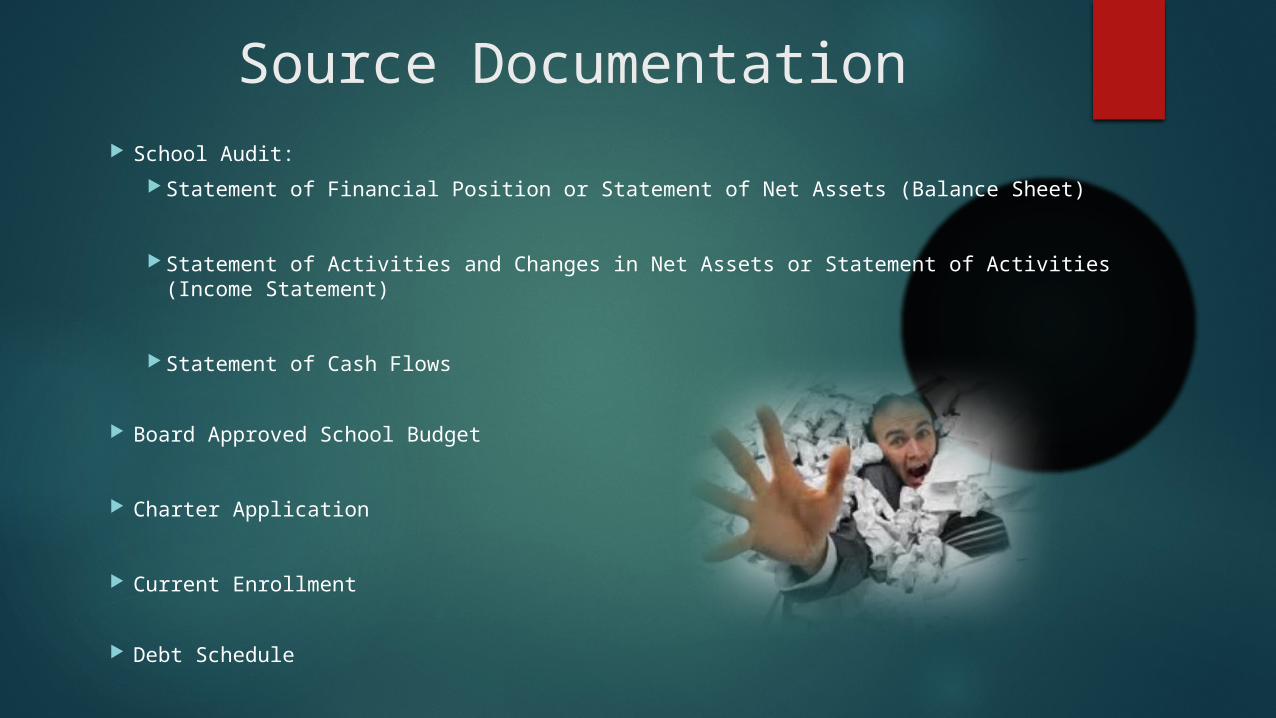

Source Documentation School Audit:

Statement of Financial Position or Statement of Net Assets (Balance Sheet)

Statement of Activities and Changes in Net Assets or Statement of Activities (Income Statement)

Statement of Cash Flows

Board Approved School Budget

Charter Application

Current Enrollment

Debt Schedule

Financial Performance Indicators

Near-Term Indicators Current Year

To Identify Immediate Risk

Sustainability Indicators Long-Term

On-going to Identify Risk to Financial Sustainability

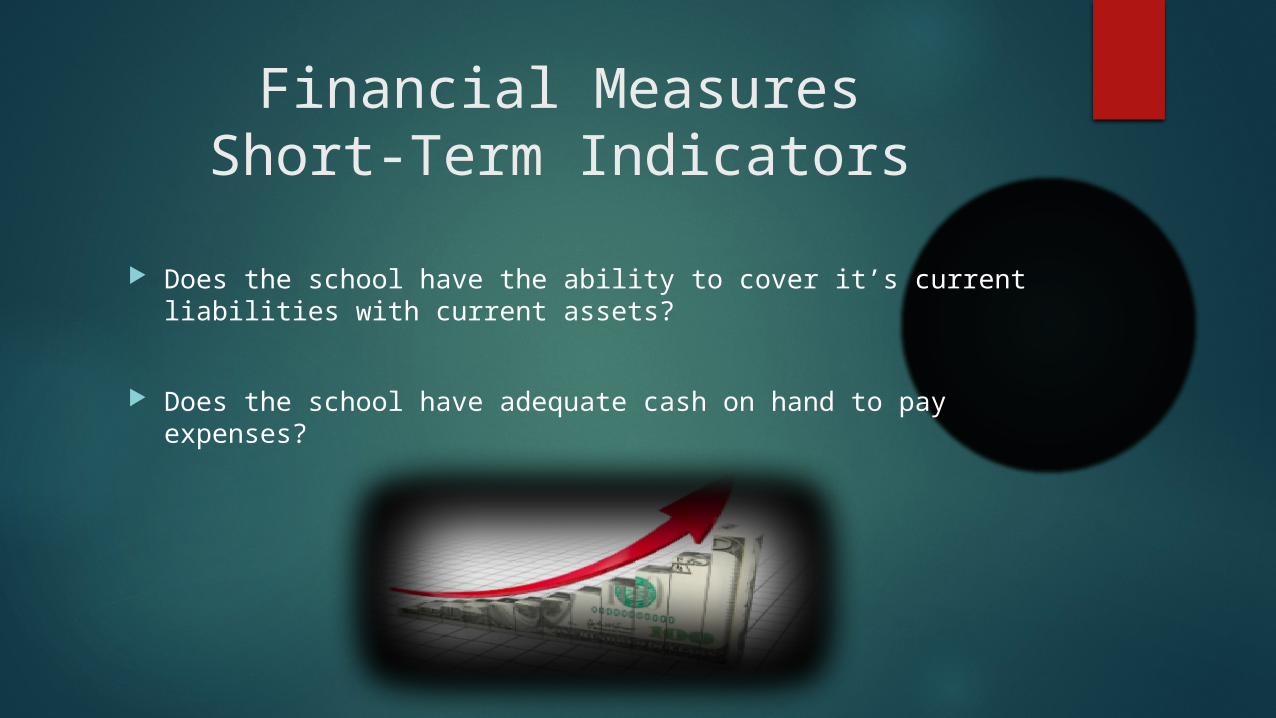

Financial MeasuresShort-Term Indicators

Does the school have the ability to cover it’s current liabilities with current assets?

Does the school have adequate cash on hand to pay expenses?

Financial MeasuresShort-Term Indicators

Is the school able to meet its enrollment projections?

Is the school able to meet its debt obligations or covenants?

Financial MeasuresSustainability Indicators

Is the school living within its available resources?

Is a reasonable proportion of the school’s assets financed through debt?

Financial MeasuresSustainability Indicators

Does the school have a positive change in cash balance from one period to another?

Does the school have the ability to cover its debt obligations in the current year?

Final Ratings

Meets Standard School overall financial record during preliminary review indicates sound

financial viability.

School meets requirements after follow-up analysis after previously being identified as “Not Meeting Standard” or “Far Below Standard”

Not Meeting Standard SCPCSD concludes there is a financial risk(s) requiring additional monitoring

and/or intervention.

Far Below Standard SCPCSD identifies significant financial risk(s) requiring additional monitoring

and/or intervention.

Financial PerformanceResults

Used for determining level and frequency of school monitoring

Used to target technical assistance and professional development

May be used in determinations for charter renewal

May be used in part for determination of probation or “Letters of Caution”

May be used as part of determination for school closure

SCPCSD Compliance Policy

Letters of Caution Issued when there is evidence that potential non-compliance may

occur

Letters of Non-Compliance Issued when non-compliance has occurred

Policy is not progressive!!! (Letters of Caution are not required prior to a Letter of Non-Compliance)

Questions/Concerns?

Organization

“A Quality Authorizer implements an accountability system that effectively streamlines federal, state, and local…compliance requirements while protecting schools’ legally entitled autonomy and minimizing schools’ administrative and reporting burdens.” NACSA Principles and Standards, page 16

• Expectations the charter school is required to meet through state and federal law, the Charter, or the Contract: • Spend public funds responsibly;• Practice sound governance; and • Adhere to laws and charter requirements

• Balance between appropriate oversight and infringement on autonomy

Organizational Framework

Organization Indicators

EDUCATION PROGRAM

ACCESS and EQUITY

GOVERNANCE (including accountability of management)

SCHOOL ENVIRONMENT (facilities, health, and safety)

STUDENTS/EMPLOYEES

FINANCIAL MANAGEMENT and OVERSIGHT

REPORTING

Top Related