Languages

Pages

Legal

s o a r i n g t o n ew h e i g ht s

17th Floor, Menara AFFIN80 Jalan Raja Chulan50200 Kuala LumpurMALAYSIA.

T +603 2055 9000F +603 2026 1415

www.affinbank.com.my

A n n u A l R e p o R t 2 0 0 8

HOW TO USE THE CD-ROM

this Financial Statements is a pDF document and works on all pC and Mac computers.

You will need Acrobat Reader to view the Statements.

If you don’t have Acrobat Reader, a copy of Acrobat Reader is included in this CD.

Double click the installer and follow the simple steps on screen.

Should you encounter any difficulties in operating this CD-RoM, please contact:

Head, Corporate Communications DepartmentAffin Bank Berhad

Tel: +603 2055 9000

contents

1 Corporate Profile

2 Corporate Information

3 Corporate Structure

4 Financial Highlights

6 Board of Directors

10 Management Team

12 Shariah Committee Members

13 Shariah Committee’s Report

16 Balance Sheet

17 Income Statements

18 Cash Flow Statements

�

corporateprofile

AFFIN Islamic Bank Berhad (AFFIN Islamic) is a wholly-owned subsidiary of

AFFIN Bank Berhad (AFFINBANK). Headquartered in the heart of Kuala Lumpur,

AFFIN Islamic traces back to 1993 when it began its business as the Islamic

banking arm of AFFINBANK. On 13 September 2005, the Islamic Banking

Division of AFFINBANK was incorporated as a separate entity and effective

1 April 2006, AFFIN Islamic operates as a standalone Islamic bank with an

authorised and paid up capital of RM1 billion and RM160 million respectively.

In line with Malaysia’s Financial Sector Masterplan that aspires to transform

the country into a global hub for Islamic Financial Services, AFFIN Islamic

continuously conducts research and development into new financial products

and services that are capable of competing in the global financial arena.

Despite its youth, AFFIN Islamic has successfully achieved key milestones.

In April 2008, AFFIN Islamic became the first domestic Islamic bank in

Malaysia to enter into a Musharakah agreement with a notable developer in

Pulau Pinang. In May 2008, AFFIN Islamic successfully launched its Islamic

debit MasterCard, the first in the Asia Pacific region.

As a pioneer in Islamic banking for both traditional Islamic consumer and

business financing products, AFFIN Islamic also offers a wide array of consumer

products and services to cater for the different needs of individual clients.

AFFIN Islamic Business Banking meanwhile offers Shariah compliant business

products and services from short to long term financing requirements including

syndicated financing, project financing, trade finance and treasury products

to all business enterprises ranging from small businesses to large corporates.

AFFIN Islamic has the structuring expertise to provide innovative financing

solutions to its clients. Clients of AFFIN Islamic comprise government bodies,

corporations, financial institutions and both local and international investors.

Going forward, through innovation, AFFIN Islamic will also move into distinct

Islamic banking areas such as wealth and asset management products to

create a more diverse Islamic asset portfolio.

�

affin islamic bankannualreport2008

Corporate Profile

�

corporateinformation

affin islamic bankannualreport2008Corporate Information

nameAFFIN Islamic Bank Berhad (709506-V)

Dateofincorporation13 September 2005

principalactiVitiesAFFIN Islamic Bank Berhad is principally involved in the carrying

out of Islamic banking and finance related services.

BoarDofDirectorschairmanYBhg. Jen Tan Sri Dato’ Seri Ismail bin Haji Omar (Bersara)

DirectorsYBhg. Dato’ Sri Abdul Hamidy bin Abdul Hafiz

YBhg. Tan Sri Dato’ Lodin bin Wok Kamaruddin

(Directorship from 1 January 2008 to 1 April 2008)

YBhg. Laksamana Madya Tan Sri Dato’ Seri Ahmad Ramli

bin Mohd Nor (Bersara)

YBhg. Tan Sri Mohamed Jawhar

Encik Mohd Suffian bin Haji Haron

Encik Zulkiflee Abbas bin Abdul Hamid

chiefexecutiveofficerEncik Kamarul Ariffin bin Mohd Jamil

companYsecretarYNimma Safira Khalid

reGistereDoffice17th Floor, Menara AFFIN,

80, Jalan Raja Chulan,

50200 Kuala Lumpur.

Tel : 03-2055 9000

Fax : 03-2026 1415

aUtHoriseDsHarecapitalNo. of shares 1,000,000,000

Par value RM1.00

Total RM1,000,000,000

issUeDanDpaiD-UpsHarecapitalNo. of shares 160,000,002

Par value RM1.00

Total RM160,000,002

sUBstantialsHareHolDer No. of shares

AFFIN Bank Berhad 160,000,002

eXternalaUDitorsPricewaterhouseCoopers (AF 1146)

�

corporatestrUctUre

affin islamic bankannualreport2008Corporate Structure

affinHolDinGsBerHaD

lemBaGataBUnGanGkatantentera*

BoUsteaDHolDinGsBHD*

BankofeastasialimiteD*

100%

affinBankBerHaD

100%

affinislamicBankBerHaD

* more than 20% shareholdings as at 27.2.2009

�

financialHiGHliGHts

affin islamic bankannualreport2008Financial Highlights

profit/(loss)beforetaxation(million)

08

07

06

41.4

57.9

50.1

financing(Gross)(billion)

08

07

06 1.2

1.7

2.5

earningspershare(sen)

08

07

06

17.5

24.7

22.9

Depositsfromcustomers(billion)

08

07

06

4.3

3.7

2.8

shareholders’funds(million)

08

07

06

262.7

235.6

196.7

totalassets(billion)

08

07

06

6.1

6.3

3.9

�

Year Ended 31 December 2008 2007 2006

RM’000 RM’000 RM’000

Bank

Profit Before Taxation 41,361 57,885 50,091

Profit After Taxation 28,002 39,440 36,568

assets

Total Assets 6,069,603 6,267,026 3,902,886

Financing and Advances 2,449,939 1,734,155 1,227,293

liabilities&shareholders’funds

Deposits from Customers 4,252,119 3,708,613 2,823,420

Share Capital 160,000 160,000 160,000

Shareholders’ Funds 262,671 235,607 196,696

financialratios(%)

Return on Equity (ROE) 16.80 26.69 27.47

Earnings Per Share (EPS) 17.5 sen 24.7 sen 22.9 sen

affin islamic bankannualreport2008

Financial Highlights

��

affin islamic bankannualreport2008Board of Directors

BoarDofDirectors

YBHG.Dato’sriaBDUlHamiDYBinaBDUlHafizNon-Independent Non-Executive Director

YBHG.JentansriDato’seriismailBinHaJiomar(Bersara)Chairman/Non-Independent Non-Executive Director

Jen Tan Sri Dato’ Seri Ismail bin Haji Omar (Bersara), aged 68, was appointed as a Director and as Chairman of AFFIN Islamic on 1 April 2006.

He graduated from Royal Military Academy, Sandhurst, United Kingdom in 1961 and attended military training and management development courses from several international institutions such as The Land Forces Command and Staff College, Canada in 1972, the UN International Peace Academy, Vienna in 1981 and the National Defence College, India in 1988.

He was appointed Chief of Defence Forces in 1995 and retired on 31 December 1998, after 38 years of service as a professional soldier. His military service included various Command and Service appointments at the Army, Armed Forces and Government Ministerial levels.

He currently holds directorships in several public and private companies including AFFINBANK, EP Engineering Sdn Bhd and ABB Trustee Berhad. He is also the Chairman of Global Medical Alliance Sdn Bhd.

His strength is his high quality leadership. As the Chairman, his leadership strength ensures the smooth functioning and effectiveness of the Board. He leads the Board in setting positive values and standards in the Bank.

He attended all 11 Board Meetings held during the financial year ending 31 December 2008.

Dato’ Sri Abdul Hamidy bin Abdul Hafiz, aged 52, was appointed as a Director of AFFIN Islamic on 1 April 2006 and Managing Director/CEO of AFFINBANK on 1 June 2003.

He is also the Chairman of the Association of Banks in Malaysia (ABM) from 2006, an industry trade group representing local financial institutions.

Prior to his appointment at AFFIN Islamic and AFFINBANK, he was the Managing Director of Pengurusan Danaharta Nasional Berhad. His directorships in several public and private companies include AFFINBANK, AFFIN Investment Bank Berhad, AFFIN Capital Sdn Bhd, Financial Mediation Bureau, ABM-MCD Holdings Sdn Bhd, AFC Holdings (Malaysia) Sdn Bhd, BCF Holdings Sdn Bhd, Credit Guarantee Corporation Malaysia Berhad, Cagamas Berhad and Asean Finance Corporation Limited.

His extensive banking experience and knowledge has served him well in improving the Bank. His expertise ensures the success of the Bank’s governance and management functions.

He attended all 11 Board Meetings held during the financial year ending 31 December 2008.

��

Tan Sri Dato’ Lodin bin Wok Kamaruddin, aged 59, was appointed to the Board of Directors of AFFIN Islamic on 1 April 2006. He is presently the Chief Executive of Lembaga Tabung Angkatan Tentera, Deputy Chairman of AFFIN Holdings Berhad and Group Managing Director of Boustead Holdings Berhad.

He graduated with a Bachelor of Business Administration in 1972 and Masters in Business Administration from the University of Toledo, Ohio, USA in 1973. He has extensive experience in general management and fund management.

He currently holds directorships in several public companies including AFFINBANK, AFFIN Investment Bank Berhad, AXA AFFIN Life Insurance Berhad, Johan Ceramics Berhad, Boustead Plantations Berhad, Boustead Properties Berhad, Boustead Heavy Industries Corporation Berhad and UAC Berhad.

He also sits on the Boards of The University of Nottingham in Malaysia Sdn Bhd, Boustead Petroleum Marketing Sdn Bhd, Boustead REIT Managers Sdn Bhd, Boustead Naval Shipyard Sdn Bhd, Boustead Petroleum Sdn Bhd, AFFIN Capital Sdn Bhd and Badan Pengawas Pemegang Saham Minoriti Berhad.

He brings a broad range of business management expertise to the Board which contributes positively to the Board’s decision-making.

He attended 3 out of 3 Board Meetings held during the financial year ending 31 December 2008.

Laksamana Madya Tan Sri Dato’ Seri Ahmad Ramli bin Mohd Nor (Bersara), aged 65, was appointed as a Director of AFFIN Islamic on 1 July 2006.

He graduated from the Brittania Royal Naval College Dartmouth, United Kingdom in 1996, the Indonesia Naval Staff College in 1976, the United States Naval War College and Naval Post-Graduate School in 1981. He also holds a Masters Degree in Public Administration from Harvard University, USA.

He retired as Chief of Royal Malaysian Navy in 1999. He currently holds directorships in AFFINBANK, Muhibbah Engineering (M) Berhad, Comintel Corporation Berhad and Favelle Favco Berhad.

Presently, he is the Executive Deputy Chairman/Group Managing Director of Boustead Heavy Industries Corporation Berhad. His appropriate leadership skills and vast experience are beneficial to the Board to gain a wider and forward looking perspective on strategic business decisions.

He attended all 11 Board Meetings held during the financial year ending 31 December 2008.

affin islamic bankannualreport2008

Board of Directors

YBHG.tansriDato’loDinBinWokkamarUDDinNon-Independent Non-Executive DirectorDirectorship from 1 January 2008 - 1 April 2008

YBHG.laksamanamaDYatansriDato’seriaHmaDramliBinmoHDnor(Bersara)Non-Independent Non-Executive Director

BoarDofDirectors(Cont.)

affin islamic bankannualreport2008Board of Directors

�

YBHG.tansrimoHameDJaWHar Independent Non-Executive Director

moHDsUffianBinHaJiHaronIndependent Non-Executive Director

En. Mohd Suffian bin Haji Haron, aged 64, was appointed as a Director of AFFIN Islamic on 1 July 2006.

He graduated with a Bachelor of Economics from University of Malaya in 1970 and holds a Master of Business Administration from University of Oregon, USA in 1976.

His current directorships in public companies include L.K. & Associates Sdn Bhd, Idaman Pharma Manufacturing Sdn Bhd and Polmag Sdn Bhd.

Prior to AFFIN Islamic, he was Director of Integrated Petroleum Services Sdn Bhd from 1992 to 2007 and Chairman of ASM Asset Management Sdn Bhd from 2001-2007.

He brings a diverse professional experience to the Board. His background provides the necessary independence to the Board and adds value by drawing on his experience and contributing to the Board’s decision-making process.

He attended all 11 Board Meetings held during the financial year ending 31 December 2008.

Tan Sri Mohamed Jawhar, aged 65, was appointed as a Director of AFFIN Islamic on 1 July 2006.

His other positions include Member, National Unity Advisory Panel, Malaysia; Non-Executive Chairman, New Straits Times; Co-Chair, Network of East Asia Think-tanks (NEAT) 2005-2006; Chairman, Malaysian National Committee, Pacific Economic Cooperation Council (PECC); Co-Chair, Council for Security Cooperation in the Asia Pacific (CSCAP) for a period of two years; Chair, ASEAN-ISIS (2007-2008); Expert and Eminent Person, for the purposes of the ASEAN Regional Forum (ARF) Register; Member of the Board of Directors, International Institute of Advanced Islamic Studies; and Distinguished Fellow, Institute of Diplomacy and Foreign Relations, Ministry of Foreign Affairs, Malaysia.

He served with the government before he joined ISIS Malaysia as Deputy Director-General in 1990, Director-General in March 1997 and Chairman and CEO in 2006.

His positions in government included Director-General, Department of National Unity; Under-Secretary, Ministry of Home Affairs; Director (Analysis) Research Division, Prime Minister’s Department and Principal Assistant Secretary, National Security Council. He also served as Counselor in the Malaysian Embassies in Indonesia and Thailand.

His appropriate leadership skills and vast experience are valuable to the Board to gain a wider and forward looking perspective on decision making.

He attended 10 of the 11 Board Meetings held during the financial year ending 31 December 2008.

affin islamic bankannualreport2008

Board of Directors

�

En. Zulkiflee Abbas Abdul Hamid, aged 52, was appointed as a Director of AFFIN Islamic on 1 April 2006.

He graduated with a Masters in Business Administration from the Southern Illinois University.

He joined AFFINBANK in March 2005 as Director, Enterprise Banking and was later made the Director of Business before assuming the position of Executive Director, Banking.

Prior to joining AFFIN Islamic and AFFINBANK, he was the Chief Credit Officer in one of Malaysia’s leading banks. He also served in various positions there including as board member of its subsidiaries.

His extensive banking experience and knowledge contribute to the Board’s decision-making process.

He attended 10 out of 11 Board Meetings held during the financial year ending 31 December 2008.

En. Kamarul Ariffin bin Mohd Jamil, aged 40, was appointed as CEO and Director on 3 January 2007 and 1 April 2006 respectively.

He graduated from the University of Cambridge in 1992 with a Bachelor of Arts (Economics).

He joined AFFINBANK in 2003 as Head, Corporate Strategy Division. In 2005, he was appointed as Head, Islamic Banking Division.

Prior to AFFIN Islamic and AFFINBANK, he held various positions at Pengurusan Danaharta Nasional Berhad namely Head of Managing Director’s Office and Special Assistant to Managing Director between 1999 and 2003. Kamarul also did a stint in Trenergy Malaysia Berhad and Shell Malaysia Trading Sdn Bhd in various capacities including business development, planning and Special Assistant to the Managing Director of Trenergy Malaysia Berhad.

He brings a broad range of business management expertise to the Board.

He attended all 11 Board Meetings held during the financial year ending 31 December 2008.

kamarUlariffinBinmoHDJamilChief Executive Officer/ Non-Independent Executive Director

zUlkifleeaBBasBinaBDUlHamiDNon-Independent Non-Executive Director

�0

manaGementteam

affin islamic bankannualreport2008Management team

kamarUlariffinBinmoHDJamilChief Executive Officer

HaJiaBDraniBinleBaiJaafarDeputy Chief Executive Officer

ferDaUstoHBinaBDUllaHHead, Islamic Banking Services

lokmanBinsHamsUDDinHead, Business Banking Support

mUHizanBinYaHYaHead, Business Financing

��

affin islamic bankannualreport2008

Management team

faUziaHBintiYUsofHead, Zakat Management

norizaHBintiDarUsManager, Islamic Treasury

zaBeDaHBintiaBUBakarHead, Mortgage Business

pUziaHBintiaBUBakarHead, Premier Corporate

raDziaHBintiaHmaDHead, Hire Purchase-i

��

associateprof.Dato’Dr.HailaniBinmUJitaHir Chairman

Associate Prof. Dato’ Dr. Hailani bin Muji Tahir, aged 63, obtained his PhD (1988) from University of Aberdeen, United Kingdom. He pursues his career as Professor at Universiti Kebangsaan Malaysia in Muamalah and Islamic Economics. Currently, he is also one of the Shariah Advisors for Takaful Nasional Berhad, Ampro Holding Co. Ltd. Singapore and Dana Putra Unit Trust. He has written a number of books and working papers on Muamalah and Islamic economics, such as Islamic Budgetary Policy; Islam and Muamalah: An introduction to Business Economics System; Islamic Economics System; and Discipline of Islamic Economic: In Theory and Practice, and the co-writer of ‘Zakat-Pensyariatan, Perekonomian dan Perundangan’. He was awarded by Selangor State Government ‘Tokoh Zakat Negeri Selangor’ in 1997. Recently, he was conferred ‘Datukship’ by the Selangor State Government in conjunction with Hari Keputeraan Sultan Selangor.

maJGenDato’HaJiJamilkHirBinBaHarom

Maj Gen Dato’ Hj Jamil Khir bin Baharom, aged 47, is currently the Pengarah Kor Agama Angkatan Tentera (KAGAT), who has served the military since November 1986. He received his degree in Islamic Studies (Shariah) from University of Malaya (1986) and Master of Islamic Studies from School of Islamic and Social Science Virginia USA.

associateprof.Dr.mDkHalilBinrUslan

Associate Prof. Dr. Md Khalil bin Ruslan, aged 47, is a law lecturer at University of Malaya at the Law Faculty for more than 16 years. He specializes in Islamic law, Islamic criminal law and Islamic commercial transactions. He has written a few working papers on Muamalah such as ‘Managing the risks in Islamic Project Financing’, ‘Quranic Guidance on Financial Planning’ and also the editor of manuscript on the Paradox of Faith: Is Islam a Hindrance to Business Success. He is also Shariah Committee Chairman of MAA Takaful.

sHariaHcommitteememBers

affin islamic bankannualreport2008Shariah Committee Members

Dr.asYrafWaJDiBinDato’DUsUki

Dr. Asyraf Wajdi bin Dato’ Dusuki is currently Head, Research Affairs of International Shariah Research Academy for Islamic Finance (ISRA), Shariah Panel of AFTAAS Shariah Advisory, Director of Islamic Financial Consultancy and Chairman of Darul Hanan Foundation. He successfully obtained his Bachelor of Accounting (Hons) International Islamic University Malaysia (IIUM) in 2000, Master of Science with Distinction in 2002 (Islamic Economics, Banking and Finance) and PhD in Islamic Banking and Finance in 2005, from Loughborough University United Kingdom. He was associate professor at the Kulliyyah of Economic and Management Science, IIUM since 2000-2008 before he resigned. He is actively engaging in a lot of research in Islamic banking and actively participates in international/national conferences, e.g. in Emirates, London, Tehran, Germany, Jakarta and Brunei, on Islamic banking and finance as speaker as well as presenter. His areas of specialization are Islamic Banking and Finance, Fiqh Muamalat, Corporate Governance of Islamic Financial Institutions, Accounting for Islamic Financial Institutions, Risk Management and Analysis of Islamic Banking, Islamic Accounting, Islamic Business Ethics and Corporate Social Responsibility.

associateprof.Dr.BoUHeraoUasaiD

Associate Prof. Dr. Bouheraoua Said obtained Bachelor in Fiqh and Usul Fiqh from National Higher Institute of Religion Foundations (University of Algiers) in 1991, Master of Quran and Sunnah in 1998 and PhD in Fiqh/Usul Fiqh (Shariah) from International Islamic University Malaysia (IIUM) in 2002 and he is currently an Associate Professor at Department of Islamic Law, Ahmad Ibrahim Kulliyyah of Law, at the university and Coordinator of Ahmad Ibrahim Kulliyyah of Laws Arabic Unit. He is an expert in research area of Usul Fiqh/Shariah in terms of providing Shariah ruling based on Islamic legal sources which particularly may contribute to the authentic innovation in Islamic Banking and Finance. He currently is an appointed referee for Journal of Islam in Asia, Member of Editorial Board of At-Tajdid International Refereed Journal and Consultant Editor in Al-Risalah Refereed Journal IIUM. He was also the Winner of the Lamya al-Faruqi award for academic excellence year 1999, organized by International Institute of Islamic Thought & IIUM.

��

affin islamic bankannualreport2008

Shariah Committee’s Report

sHariaHcommittee’sreport

We, DR. HAILANI MUJI TAHIR and DR. MD. KHALIL RUSLAN, two of the members of the Shariah Committee of AFFIN Islamic Bank Berhad, do hereby confirm on behalf of the Shariah Committee, that in our opinion, the operation of the Bank for the financial year ended 31 December 2008 have been conducted in conformity with the Shariah principles.

On behalf of the Shariah Committee,

Dr.HailanimUJitaHir Dr.mDkHalilrUslan

Kuala Lumpur23 February 2009

��

reportoftHecHairmanoftHeBoarD

affin islamic bankannualreport2008title“ Society is where the Bank draws its customer base from. The Bank believes that every organization should return to the community what it has been able to draw from it. The Bank aspires not only to paint an image of a caring Bank but to truly be a caring Bank.”

kamarulariffinmohdJamil Chief Executive Officer, AFFIN Islamic

��

affin islamic bankannualreport2008

title

��

BalancesHeetas at 31 December 2008

theBank/ The Bank economicentity 2008 2007 rm’000 RM’000

assetsCash and short-term funds 2,358,150 3,532,550Available-for-sale securities 1,071,326 774,250 Held-to-maturity securities 575 –Financing, advances and other loans 2,449,939 1,734,155 Other assets 52,585 135,676 Tax recoverable 5,187 – Statutory deposits with Bank Negara Malaysia 106,400 82,300 Investment in jointly controlled entity 500 – Amount due from jointly controlled entity 750 – Property and equipment 3,247 273 Land held for sale 15,000 – Intangible assets 1,392 1,610 Deferred tax assets 4,552 6,212

totalassets 6,069,603 6,267,026

liaBilitiesDeposits from customers 4,252,119 3,708,613 Deposits and placements of banks and other financial institutions 1,261,205 2,078,923 Other liabilities 39,234 32,674 Amount due to holding company 254,374 207,611Provision for tax – 3,598

totalliaBilities 5,806,932 6,031,419

eQUitYShare capital 160,000 160,000 Reserves 102,671 75,607

totaleQUitY 262,671 235,607

totalliaBilitiesanDeQUitY 6,069,603 6,267,026

commitmentsanDcontinGencies 6,994,462 3,917,054

affin islamic bankannualreport2008Balance Sheet

��

incomestatementsfor the financial year ended 31 December 2008

theBank/ The Bank economicentity 2008 2007 rm’000 RM’000

Income derived from investment of depositors’ funds and others 278,588 227,404 Income derived from investment of shareholders’ funds 12,062 11,240Allowance for losses on financing (27,113) (9,146)Transfer from profit equalisation reserve – 501

totaldistributableincome 263,537 229,999

Income attributable to the depositors (155,195) (124,618)

totalnetincome 108,342 105,381

Personnel expenses (9,501) (5,633)Other overheads and expenditures (57,480) (41,863)

profitbeforezakatandtaxation 41,361 57,885

Zakat (2,359) (2,240)Taxation (11,000) (16,205)

netprofitafterzakatandtaxation 28,002 39,440

attributableto: Equity holders of the Bank 28,002 39,440

earningspershare – basic/fully diluted (sen) 17.5 24.7

affin islamic bankannualreport2008

Income Statements

��

theBank/ The Bank economicentity 2008 2007 rm’000 RM’000

casHfloWsfromoperatinGactiVities

profitbeforezakatandtaxation 41,361 57,885

Adjustments for items not involving the movement of cash and cash equivalents: Income from securities – available-for-sale securities (13,259) (5,555)– held-to-maturity securities – (2,003)Amortisation of premium less accretion of discount– available-for-sale securities (18,570) (9,886)– held-to-maturity securities – 599Gain on sale from securities– held-for-trading securities (44) –– available-for-sale securities (57) –Gain on unrealised foreign exchange (18,361) (1,331)Depreciation of property and equipment 609 57 Amortisation of intangible asset 491 483 Net specific allowance for bad and doubtful financing 16,183 2,400 Income suspended 1,668 2,412 Charge of general allowances 10,824 6,600 Bad debt on financing written-off 220 146

operatinGprofitBeforecHanGesinWorkinGcapital 21,065 51,807

(Increase)/decrease in operating assets:Held-for-trading securities 43 –Foreign exchange transaction 15,761 1,960Financing, advances and other loans (744,678) (518,420)Other assets 83,091 (124,316) Statutory deposits with Bank Negara Malaysia (24,100) (40,300)Amount due from jointly controlled entity (750) –

casHfloWstatementsfor the financial year ended 31 December 2008

affin islamic bankannualreport2008Cash Flow Statements

��

casHfloWstatementsfor the financial year ended 31 December 2008

theBank/ The Bank economicentity 2008 2007 rm’000 RM’000

Increase/(decrease) in operating liabilities:Deposits from customers 543,506 885,194Deposits and placements of banks and other financial institutions (817,717) 1,778,473Bills and acceptances payable – (23,689)Amount due to holding company 46,763 (277,425)Other liabilities 5,502 (37,704)

Cash generated from operations (871,514) 1,695,580Tax paid (17,819) (19,966)Zakat paid (1,299) –

netcasH(UseDin)/GenerateDfromoperatinGactiVities (890,632) 1,675,614

casHfloWsfrominVestinGactiVities

Increase in investment in jointly controlled entity (500) –Income received from securities– available-for-sale securities 13,259 5,555– held-to-maturity securities – 2,003Net sale of available-for-sale securities (279,695) (383,792)Redemption of held-to-maturity securities net of purchase (575) 90,000Purchase of property and equipment (3,620) (142)Purchase of land held for sale (15,000) –Purchase of intangible assets (237) –

netcasHUseDinfrominVestinGactiVities (286,368) (286,376)

net(Decrease)/increaseincasHanDcasHeQUiValents (1,177,000) 1,389,238

netincrease/(Decrease)inforeiGneXcHanGe 2,600 (629)

casHanDcasHeQUiValentsatBeGinninGoftHefinancialYear 3,532,550 2,143,941

casHanDcasHeQUiValentsatenDoftHefinancialYear 2,358,150 3,532,550

analYsisofcasHanDcasHeQUiValentsCash and short-term funds 2,358,150 3,532,550

affin islamic bankannualreport2008

Cash Flow Statements

For full Financial Statements, please refer to the enclosed CD-ROM.

This page has been intentionally left blank.

s o a r i n g t o n ew h e i g ht s

17th Floor, Menara AFFIN80 Jalan Raja Chulan50200 Kuala LumpurMALAYSIA.

T +603 2055 9000F +603 2026 1415

www.affinbank.com.my

A n n u A l R e p o R t 2 0 0 8

HOW TO USE THE CD-ROM

this Financial Statements is a pDF document and works on all pC and Mac computers.

You will need Acrobat Reader to view the Statements.

If you don’t have Acrobat Reader, a copy of Acrobat Reader is included in this CD.

Double click the installer and follow the simple steps on screen.

Should you encounter any difficulties in operating this CD-RoM, please contact:

Head, Corporate Communications DepartmentAffin Bank Berhad

Tel: +603 2055 9000

�

affin iSLaMiC bankAnnual Report 2008Financial Statements

2 Directors’ Report

18 Balance Sheets

19 Income Statements

20 Statement of Changes in Equity

21 Cash Flow Statements

23 Summary of Significant Accounting Policies

35 Notes to the Financial Statements

85 Statement by Directors

85 Statutory Declaration

86 Independent Auditors’ Report

88 Shariah Committee’s Report

finAnciAl stAtements

�

affin iSLaMiC bankAnnual Report 2008

Directors’ Report

DiRectORs’ RePORtfor the financial year ended 31 December 2008

The Directors hereby submit their report together with the audited financial statements of the Bank for the financial year ended 31 December 2008.

PRinciPAl ActiVities

The principal activities of the Bank are Islamic banking business and related financial services. There were no significant changes in these activities during the financial year.

finAnciAl ResUlts

the Bank/ economic entity Rm’000

Profit before zakat and taxation 41,361

Taxation and zakat (13,359)

net profit for the financial year 28,002

DiViDenDs

No dividends have been paid by the Bank in respect of the financial period ended 31 December 2008.

The Directors do not recommend the payment of any dividend in respect of the current financial year.

ReseRVes AnD PROVisiOns

There were no material transfers to or from reserves or provisions during the financial year other than those disclosed in the financial statements.

BAD AnD DOUBtfUl finAncinG

Before the financial statements of the Bank were made out, the Directors took reasonable steps to ascertain that actions had been taken in relation to the writing off of bad financing and the making of allowances for doubtful financing, and have satisfied themselves that all known bad financing had been written off and adequate allowances had been made for bad and doubtful financing.

At the date of this report, the Directors are not aware of any circumstances which would render the amount written off for bad financing, or the amount of the allowance for doubtful financing in the financial statements of the Bank, inadequate to any substantial extent.

�

cURRent Assets

Before the income statement and balance sheet of the Bank were made out, the Directors took reasonable steps to ascertain that any current assets, other than financing, which were unlikely to be realised in the ordinary course of business, their values as shown in the accounting records of the Bank have been written down to their estimated realisable value.

At the date of this report, the Directors are not aware of any circumstances which would render the values attributed to the current assets in the financial statements of the Bank misleading.

VAlUAtiOn metHODs

At the date of this report, the Directors are not aware of any circumstances which have arisen which render adherence to the existing methods of valuation of assets or liabilities in the Bank’s accounts misleading or inappropriate.

cOntinGent AnD OtHeR liABilities

At the date of this report there does not exist:

(a) any charge on the assets of the Bank which has arisen since the end of the financial year which secures the liabilities of any other person; or

(b) any contingent liability in respect of the Bank that has arisen since the end of the financial year.

No contingent or other liability of the Bank has become enforceable, or is likely to become enforceable within the period of twelve months after the end of the financial period which, in the opinion of the Directors, will or may substantially affect the ability of the Bank to meet its obligations as and when they fall due.

cHAnGe Of ciRcUmstAnces

At the date of this report, the Directors are not aware of any circumstances, not otherwise dealt with in this report or the financial statements of the Bank, that would render any amount stated in the financial statements misleading.

items Of An UnUsUAl nAtURe

The results of the operations of the Bank during the financial year were not, in the opinion of the Directors, substantially affected by any item, transaction or event of a material and unusual nature.

There has not arisen in the interval between the end of the financial year and the date of this report any item, transaction or event of a material and unusual nature likely, in the opinion of the Directors, to affect substantially the results of the operations of the Bank for the current financial year in which this report is made.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Directors’ Report

�

affin iSLaMiC bankAnnual Report 2008

Directors’ Report

siGnificAnt eVents DURinG tHe finAnciAl YeAR

Significant events during the financial year are as disclosed in Note 37 to the financial statements.

sUBseQUent eVents

There were no material events subsequent to the balance sheet date that require disclosure or adjustments to the financial statements.

DiRectORs

The Directors of the Bank who have held office during the period since the date of the last report are:

Gen Tan Sri Dato’ Seri Ismail bin Haji Omar (Rtd) Chairman/Non-Independent Non-Executive Director

En. Kamarul Ariffin bin Mohd Jamil Chief Executive Officer Non-Independent Executive Director

Dato’ Sri Abdul Hamidy bin Abdul Hafiz Non-Independent Non-Executive Director

Tan Sri Dato’ Lodin bin Wok Kamaruddin Non-Independent Non-Executive Director (Directorship from 1 January 2008 to 1 April 2008)

Vice Admiral Dato’ Seri Ahmad Ramli bin Mohd Nor (Rtd) Non-Independent Non-Executive Director

Tan Sri Mohamed Jawhar Independent Non-Executive Director

En. Mohd Suffian bin Haji Haron Independent Non-Executive Director

En. Zulkiflee Abbas bin Abdul Hamid Non-Independent Non-Executive Director

DiRectORs’ RePORtfor the financial year ended 31 December 2008

�

DiRectORs’ inteRests

According to the register of Directors’ shareholdings, the interest of Directors in office at end of the financial year in shares, warrants and options of related corporations are as follows:

Ordinary shares of Rm1 each

As at As at 1.1.2008 Bought sold 31.12.2008

Affin Holdings BerhadTan Sri Dato’ Lodin bin Wok Kamaruddin 8,714* 800,000 – 808,714*Dato’ Sri Abdul Hamidy bin Abdul Hafiz – 200,000 – 200,000

Boustead Heavy industries corporation BerhadTan Sri Dato’ Lodin bin Wok Kamaruddin 2,000,000 – – 2,000,000

Boustead Petroleum sdn BerhadTan Sri Dato’ Lodin bin Wok Kamaruddin 5,466,465 – – 5,466,465

Al-Hadharah Boustead ReitTan Sri Dato’ Lodin bin Wok Kamaruddin 200,000 – – 200,000

*Shares held in trust by nominee company

number of warrants 2000/2010

As at As at 1.1.2008 Bought sold 31.12.2008

Affin Holdings BerhadTan Sri Dato’ Lodin bin Wok Kamaruddin 1,500 – – 1,500

Each warrant of the holding company (‘AFFIN Warrants 2000/2005’) entitles the registered holder to subscribe one new ordinary share of RM1.00 each in AFFIN Holdings Berhad at any time from the date of issue of 8 July 2000 at the exercise price of RM3.10 per share. The original exercise period of the AFFIN Warrants 2000/2005 was to expire on 7 July 2005. During the financial year 2005, the AFFIN Warrants 2000/2005 was extended for another five years and will expire on 7 July 2010 (‘AFFIN Warrants 2000/2010’).

DiRectORs’ RePORtfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Directors’ Report

�

affin iSLaMiC bankAnnual Report 2008

Directors’ Report

DiRectORs’ inteRests (continued)

Options over ordinary shares of Rm1 each

As at As at 1.1.2008 Granted exercised 31.12.2008

Affin Holdings BerhadTan Sri Dato’ Lodin bin Wok Kamaruddin 800,000** – 800,000 –

** This option was granted by the holding company, AFFIN Holdings Berhad under its Employees’ Share Option Scheme at the option price of RM1.41 per share and has expired in full before the expiry date (i.e.13 February 2008).

Ordinary shares of Rm10 each; Rm5 uncalled

As at As at 1.1.2008 Bought transfer 31.12.2008

ABB trustee Berhad***Gen Tan Sri Dato’ Seri Ismail bin Haji Omar (Rtd) 20,000 – – 20,000 Vice Admiral Dato’ Seri Ahmad Ramli bin Mohd Nor (Rtd) 20,000 – – 20,000

***Shares held in trust for the Bank

Ordinary shares of 50 sen each

As at As at 1.1.2008 Bought sold 31.12.2008

Boustead Holdings BerhadTan Sri Dato’ Lodin bin Wok Kamaruddin 21,695,000 – 1,879,000 19,816,000

Other than the above, the Directors in office at the end of the financial year did not have any other interest in shares, warrants and options over shares in the Bank or its related corporations during the financial year.

Options over ordinary shares of 50 sen each

As at As at 1.1.2008 Granted expired 31.12.2008

Boustead Holdings BerhadTan Sri Dato’ Lodin bin Wok Kamaruddin 5,912,699* – 5,912,699 –

* This is an option granted by Lembaga Tabung Angkatan Tentera (‘LTAT’) to acquire 29,912,699 Boustead Holdings Berhad shares from LTAT at RM1.70 per share, expiring on 14 November 2008.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

�

DiRectORs’ Benefits

Neither at the end of the financial period, nor at any time during the financial year, did there subsist any arrangement to which the Bank is a party with the object or objects of enabling Directors of the Bank to acquire benefits by means of the acquisition of shares in, or debenture of, the Bank or any other body corporate.

Since the date of incorporation, no Director of the Bank has received or become entitled to receive a benefit (other than the fees and other emoluments shown in Note 27 to the financial statements) by reason of a contract made by the Bank or a related corporation with the Director or with a firm of which he is a member or with a company in which he has a substantial financial interest except that certain Directors received remuneration as directors/executives of related corporations, share options granted to Directors of the Bank pursuant to the holding company’s Employee Share Option Scheme and share options granted by the ultimate holding corporate body and Boustead Holdings Berhad.

cORPORAte GOVeRnAnce

The Board of Directors is committed to ensure the highest standards of corporate governance throughout the organisation with the objectives of safeguarding the interests of all stakeholders and enhancing the shareholders’ value and financial performance of the Bank. The Board considers that it has applied the Best Practices as set out in the Malaysian Code of Corporate Governance throughout the financial year. The Bank is also required to comply with BNM’s Guidelines on Directorship in the Islamic Banks (‘BNM/GP1-i’).

(i) Board of Directors Responsibility and Oversight

the Board of Directors The direction and control of the Bank rest firmly with the Board as it effectively assumes the overall responsibility for corporate

governance, strategic direction, formulation of policies and overseeing the investments and operations of the Bank. The Board exercises independent oversight on the management and bears the overall accountability for the performance of the Bank and compliance with the principle of good governance.

There is a clear division of responsibility between the Chairman and the Chief Executive Officer to ensure that there is a balance of power and authority. The Board is responsible for reviewing and approving the longer-term strategic plans of the Bank as well as the business strategies. It is also responsible for identifying the principal risks and implementation of appropriate systems to manage those risks as well as reviewing the adequacy and integrity of the Bank’s internal control systems, management information systems, including systems for compliance with applicable laws, regulations and guidelines.

Whilst the Management Committee, headed by the Chief Executive Officer, is responsible for the implementation of the strategies and internal control as well as monitoring performance, the Committee is also a forum to deliberate issues pertaining to the Bank’s business, strategic initiatives, risk management, manpower development, supporting technology platform and business processes.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Directors’ Report

�

affin iSLaMiC bankAnnual Report 2008

Directors’ Report

cORPORAte GOVeRnAnce (continued)

(i) Board of Directors Responsibility and Oversight (continued)

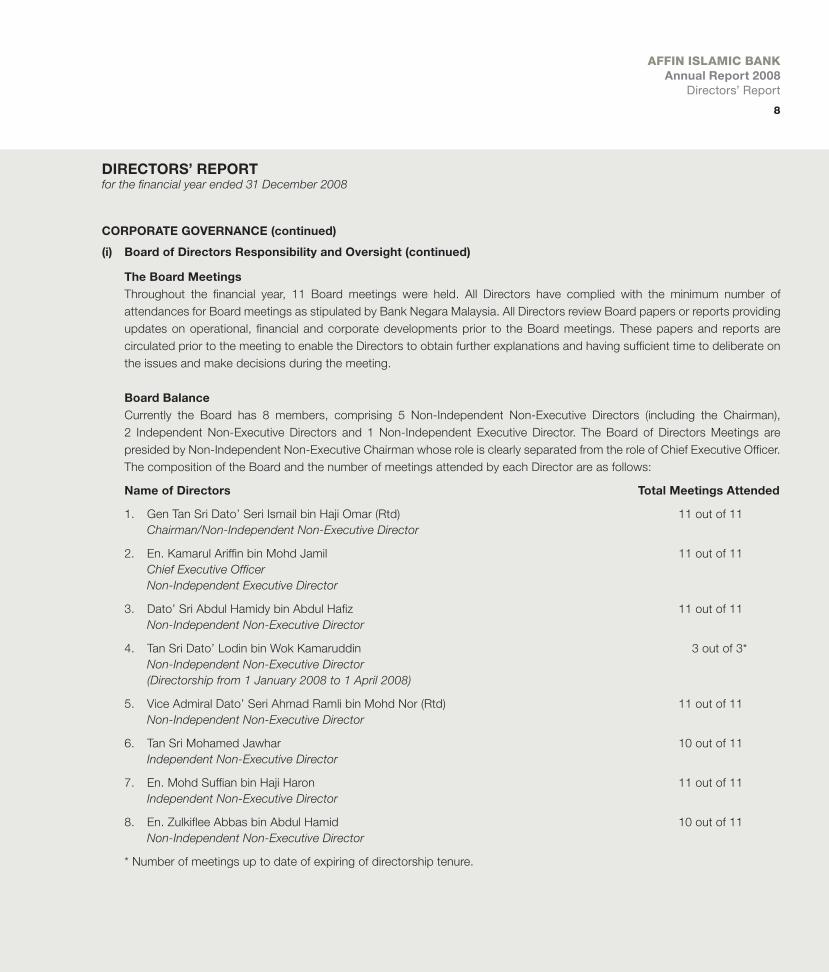

the Board meetings Throughout the financial year, 11 Board meetings were held. All Directors have complied with the minimum number of

attendances for Board meetings as stipulated by Bank Negara Malaysia. All Directors review Board papers or reports providing updates on operational, financial and corporate developments prior to the Board meetings. These papers and reports are circulated prior to the meeting to enable the Directors to obtain further explanations and having sufficient time to deliberate on the issues and make decisions during the meeting.

Board Balance Currently the Board has 8 members, comprising 5 Non-Independent Non-Executive Directors (including the Chairman),

2 Independent Non-Executive Directors and 1 Non-Independent Executive Director. The Board of Directors Meetings are presided by Non-Independent Non-Executive Chairman whose role is clearly separated from the role of Chief Executive Officer. The composition of the Board and the number of meetings attended by each Director are as follows:

name of Directors total meetings Attended

1. Gen Tan Sri Dato’ Seri Ismail bin Haji Omar (Rtd) 11 out of 11 Chairman/Non-Independent Non-Executive Director

2. En. Kamarul Ariffin bin Mohd Jamil 11 out of 11 Chief Executive Officer Non-Independent Executive Director

3. Dato’ Sri Abdul Hamidy bin Abdul Hafiz 11 out of 11 Non-Independent Non-Executive Director

4. Tan Sri Dato’ Lodin bin Wok Kamaruddin 3 out of 3* Non-Independent Non-Executive Director (Directorship from 1 January 2008 to 1 April 2008)

5. Vice Admiral Dato’ Seri Ahmad Ramli bin Mohd Nor (Rtd) 11 out of 11 Non-Independent Non-Executive Director

6. Tan Sri Mohamed Jawhar 10 out of 11 Independent Non-Executive Director

7. En. Mohd Suffian bin Haji Haron 11 out of 11 Independent Non-Executive Director

8. En. Zulkiflee Abbas bin Abdul Hamid 10 out of 11 Non-Independent Non-Executive Director

* Number of meetings up to date of expiring of directorship tenure.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

�

cORPORAte GOVeRnAnce (continued)

(i) Board of Directors Responsibility and Oversight (continued)

Board committees The Board is assisted by four committees with specific terms of reference. This enables the committees to focus on areas or

issues of critical importance to the operations of the Bank. Compositions, functions and terms of reference of these committees are highlighted below:

(i) NominationCommittee The Nomination Committee was established to provide a formal and transparent procedure for the appointment of Directors

and Chief Executive Officer. The Committee also assesses the effectiveness of the Board as a whole, contribution of each director, contribution of the board’s various committees and the performance of Chief Executive Officer and key senior management officers.

There were 2 meetings held during the financial year ended 31 December 2008. The Nomination Committee comprises the following members:

composition of the nomination committee total meetings Attended

1. En. Mohd Suffian bin Haji Haron 2 out of 2 Chairman/Independent Non-Executive Director

2. Dato’ Sri Abdul Hamidy bin Abdul Hafiz 2 out of 2 Non-Independent Non-Executive Director

3. Tan Sri Dato’ Lodin bin Wok Kamaruddin 1 out of 1* Non-Independent Non-Executive Director (Directorship from 1 January 2008 to 1 April 2008)

4. Vice Admiral Dato’ Seri Ahmad Ramli bin Mohd Nor (Rtd) 2 out of 2 Non-Independent Non-Executive Director

5. Tan Sri Mohamed Jawhar 2 out of 2 Independent Non-Executive Director

* Number of meetings up to date of expiring of directorship tenure.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Directors’ Report

�0

affin iSLaMiC bankAnnual Report 2008

Directors’ Report

cORPORAte GOVeRnAnce (continued)

(i) Board of Directors Responsibility and Oversight (continued)

Board committees (continued)

(ii) RemunerationCommittee The Remuneration Committee was established to evaluate and recommend to the Board the framework of remuneration

and the remuneration package for Directors, Chief Executive Officer and key senior management officers. The Board is ultimately responsible for the approval of the remuneration package. The Committee is guided by the need to ‘attract and retain’ and at the same time link the rewards to clearly articulate corporate and individual performance.

There were 4 meetings held during the financial year ended 31 December 2008. The Remuneration Committee comprises the following members:

composition of the Remuneration committee total meetings Attended

1. Tan Sri Mohamed Jawhar 4 out of 4 Chairman/Independent Non-Executive Director

2. Dato’ Sri Abdul Hamidy bin Abdul Hafiz 4 out of 4 Non-Independent Non-Executive Director

3. Tan Sri Dato’ Lodin bin Wok Kamaruddin 1 out of 1* Non-Independent Non-Executive Director (Directorship from 1 January 2008 to 1 April 2008)

4. Vice Admiral Dato’ Seri Ahmad Ramli bin Mohd Nor (Rtd) 4 out of 4 Non-Independent Non-Executive Director

* Number of meetings up to date of expiring of directorship tenure.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

��

cORPORAte GOVeRnAnce (continued)

(i) Board of Directors Responsibility and Oversight (continued)

Board committees (continued)

(iii) ShariahCommittee The Bank’s business activities are subject to Shariah compliance and conformation by the Shariah Committee. The Shariah

Committee is formed as legislated under Section 3(5)(b) of the Islamic Banking Act, 1983 and as per Guidelines on the Governance of Shariah Committee for the Islamic Financial Institutions (‘BNM/GPS-i’).

The duties and responsibility of the Shariah Committee are as follow: (i) To advise the Board on Shariah matters in order to ensure that the business operations of the Bank comply with the

Shariah principles at all times; (ii) To endorse and validate relevant documentations of the Bank’s products to ensure that the products comply with

Shariah principles; and (iii) To advice the Bank on matters to be referred to the Shariah Advisory Council.

During the financial year ended 31 December 2008, a total of 15 meetings were held. The Shariah Committee comprises the following members and the details of attendance of each member at the Shariah Committee meetings held during the financial year are as follows:

composition of the shariah committee total meetings Attended

1. Associate Professor Dr. Hailani bin Muji Tahir 12 out of 15 Chairman

2. Associate Professor Dr. Md Khalil bin Ruslan 13 out of 15 Member

3. Maj Gen Dato’ Haji Jamil Khir bin Baharom 11 out of 15 Member

4. Dr. Asyraf Wajdi bin Dato’ Dusuki 10 out of 11* Member (appointed on 25 April 2008)

5. Associate Professor Dr. Bouheraoua Said 10 out of 11* Member (appointed on 25 April 2008)

* Number of meetings since date of appointment.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Directors’ Report

��

affin iSLaMiC bankAnnual Report 2008

Directors’ Report

cORPORAte GOVeRnAnce (continued)

(ii) Risk management The Risk Management function, operating in an independent capacity, is part of the Bank’s senior management structure which

works closely as a team in managing risks to enhance stakeholders’ value.

The Risk Management function provides support to the Board Risk Management Committee (‘BRMC’). Committees namely Board Loan Recovery Committee (‘BLRC’), Management Loan Committee (‘MLC’), Asset and Liability Management Committee (‘ALCO’) and Operational Risk Management Committee assist the BRMC in managing credit, liquidity and operational risk respectively.

Responsibilities of these committees include: (i) risk identification (ii) risk assessment and measurement (iii) risk control and migration (iv) risk monitoring

BoardRiskManagementCommittee(‘BRMC’) The main function of Board Risk Management Committee is to assist the Board in its supervisory role in the management of

risk in the Bank. It has responsibility for approving and reviewing the credit risk strategy, credit risk framework and credit policies of the Bank.

BRMC was established to provide oversight and management of all risks in the Bank. The Committee also ensures that the procedures and framework in relation to identifying, measuring, monitoring and controlling risk are operating effectively. The Bank’s risk management framework is set out in Note 2 to the financial statements.

The BRMC meetings for the Bank were jointly held with AFFIN Bank Berhad and during the financial year ended 31 December 2008, a total of 5 meetings were held and the following Independent Non-Executive Director of the Bank sits in the meeting:

composition of the Board Risk management committee total meetings Attended

En. Mohd Suffian bin Haji Haron 5 out of 5 Member/Independent Non-Executive Director

DiRectORs’ RePORtfor the financial year ended 31 December 2008

��

cORPORAte GOVeRnAnce (continued)

(ii) Risk management (continued)

BoardLoanReviewandRecoveryCommittee(‘BLRC’) Board Loan Review Committee critically reviews loans and other credit facilities with higher risk implications, after due process

of checking, analysis, review and recommendation by the Credit Risk Management function, and if found necessary, exercise the power to veto loan applications that have been accepted by the Management Loan Committee. The Committee is also responsible to review on the non-performing loans presented by Management.

ManagementLoanCommittee(‘MLC’) Management Loan Committee approves complex and larger loans and workout/recovery proposals beyond the delegated

authority of the concerned individual senior management personnel of the Bank.

IndividualApprovers For the delegated authority, a dual sign-off approval system is in place, independent of business imperatives.

AssetandLiabilityManagementCommittee(‘ALCO’) Responsibilities of these committees include: (i) Manage the asset liability of the Bank through coordination of the Bank’s overall planning process including strategic

planning, budgeting and asset liability management process; (ii) Direct the Bank’s overall acquisition and allocation of Funds; (iii) Prudently manage the Bank’s interest rate exposure; (iv) Determine the overall Balance Sheet strategy and ensuring policy compliance; (v) Determine the type and scope of derivative activities, approve individual derivative transactions as well as control over the

level of exposure in derivatives; and (vi) Review of market risks in Bank’s trading portfolios.

OperationalRiskManagementCommittee Responsibilities of these committees include: (i) To evaluate operational risks issues on escalating importance/strategic risk exposure; (ii) To review and recommend on broad operational risks management policies best practices for adoption by the Bank’s

operating units; (iii) To review the effectiveness of broad internal controls and making recommendation on changes if necessary; (iv) To review/approve recommendation on operational risk management groups section up to address specific issue; (v) To take the lead in inculcating an operational risks awareness culture; (vi) To approve operational risk management methodologies/measurements tools; and (vii) To review and approve the strategic operational risk management initiatives/plans and to endorse for BRMC’s approval if

necessary.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Directors’ Report

��

affin iSLaMiC bankAnnual Report 2008

Directors’ Report

cORPORAte GOVeRnAnce (continued)

(iii) internal Audit and internal control Activities

RelationshipwiththeAuditors The Bank has established appropriate relationship with both internal and external auditors in conducting the audit function of

the Bank.

InternalControls The Board acknowledges its overall responsibility for maintaining a sound system of internal control to safeguard shareholders’

investments, Bank’s assets, and the need to review the adequacy and integrity of those systems regularly.

In accordance with BNM’s Guidelines on Minimum Audit Standards for Internal Auditors of Financial Institutions (‘BNM/GP10’), the Audit and Compliance Division (‘ACD’) conducts continuous reviews on auditable areas within the Bank. The continuous reviews by ACD are focused on areas of significant risks and effectiveness of internal control in accordance to the audit plan approved by the Audit and Examination Committee (‘AEC’). The risk highlighted on the respective auditable areas as well as recommendation made by the ACD are addressed at AEC and Management meetings on a monthly basis. The AEC also conduct annual reviews on the adequacy of internal audit function, scope of work, resources and budget of ACD.

At present, ACD consists of Operational Audit, IS Audit, Credit Review, Investigation and Compliance. Audit activities include these key components:

(a) Conduct audit on all auditable entities (Head Office, branches and subsidiaries) processes, services, products, system and provide an independent assessment to the Board of Directors, AEC and Management that appropriate control environment is maintained with clear authority and responsibility with sufficient staff and resources to carry out control responsibilities.

(b) Perform risk assessments to identify control risk and evaluate actions taken to provide reasonable assurance that procedures and controls exist to contain those risks.

(c) Maintain strong control activities including documented processes and system incorporating adequate controls to produce accurate financial data and provide for the safeguarding of assets, and a documented review of reported results.

(d) Ensure effective information flows and communication, including: (i) Training and the dissemination of standards and requirements; (ii) An information system to produce and convey complete, accurate and timely data including financial data; and (iii) The upward communication of trends, developments and emerging issues.

(e) Monitor controls, including procedures to verify that controls are in place and functioning, follow up on corrective action on control findings till its full resolution. Based on ACD’s review, identification and assessment of risk, testing and evaluation of controls, ACD will provide an opinion on the effectiveness of internal controls maintained by each entity.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

��

cORPORAte GOVeRnAnce (continued)

(iii) internal Audit and internal control Activities (continued)

The AEC comprises members of the Bank’s Board of Directors whose primary function is to assist the Board in its supervision over:

(i) The reliability and integrity of accounting policies and financial reporting and disclosure practise; (ii) The provision of advice to the Board with regards to the financial statements and business risks to enable the Board to

fulfill its fiduciary duties and obligations; and (iii) The establishment and maintenance of processes to ensure that they: – are in compliance with all applicable laws, regulations and company policies; and – have adequately addressed the risk relating to internal controls and system, management of inherent and business

risks, and ensuring that the assets are properly managed and safeguarded.

The AEC meetings for the Bank were jointly held with AFFIN Bank Berhad during the financial year ended 31 December 2008 and the following Independent Non-Executive Director of the Bank sits in the meeting:

composition of the Audit and examination committee total meetings Attended

Tan Sri Mohamed Jawhar 8 out of 10 Member/Independent Non-Executive Director (iv) management Reports Before each Board meeting, Directors are provided with a complete set of Board papers itemised in the agenda for Board’s

review/approval and/or notation.

The Board monitors the Bank’s performance by reviewing the monthly Management Report, which provides a comprehensive review and analysis of the Bank’s operations and financial issues. In addition, the minutes of the Board Committees and Management Committees meetings and other issues are also tabled and considered by the Board.

Procedures are in place for Directors to seek both independent professional advice at the Bank’s expense and the advice and services of the Company Secretary in order to fulfil their duties and specific responsibilities.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Directors’ Report

��

affin iSLaMiC bankAnnual Report 2008

Directors’ Report

BUsiness PlAn AnD stRAteGY fOR tHe finAnciAl YeAR enDeD 31 DecemBeR 2008 AnD fUtURe OUtlOOK

AFFIN Islamic Bank recorded a profit before tax of RM41.3 million for the financial year ended 31 December 2008, lower compared to year 2007 but it was mainly due to increase in allowances for financing growth and operating expenditures for business expansion. As at end 2008, total financing grew a remarkable 41% against the previous year while net non-performing financing improved to 1.34% from 1.74% recorded in 2007.

In year 2008, AFFIN Islamic has successfully achieved several key milestones, such as:

– In April 2008, AFFIN Islamic became the first domestic Islamic bank in Malaysia to enter into a Musharakah Agreement with a notable property developer in Pulau Pinang.

– In May 2008, AFFIN Islamic successfully launched its Islamic debit MasterCard, the first in the Asia Pacific region.

– In our continued effort to introduce various innovative products and services to our customers, AFFIN Islamic, together with the parent bank, has successfully launched the retail internet banking portal affinOnline.com in December 2008.

As for AFFIN Islamic future plans, the Bank will continue to grow beyond the traditional role of Islamic banks by providing more innovative Shariah-based products and services, in particular equity-based financing structures encompassing Musharakah and Mudharabah contracts within the retail and business banking sectors while expanding into new areas to generate new wealth.

Moving forward, AFFIN Islamic remains committed to continuously provide quality and innovative products and services to meet the needs and requirements of its customers and clients. As a full fledged Islamic bank, customers are assured that all banking transactions are free from the elements of interests (riba), uncertainty (gharar), gambling (maisir) and other un-Islamic fundamentals as these are monitored by the Bank’s Shariah Department and supervised by the Shariah Committee.

Although AFFIN Islamic expects Year 2009 to be challenging in the face of economic uncertainties, the banking sector remains robust and we are cautiously optimistic on the opportunities available. AFFIN Islamic shall take a ‘business as usual’ approach and remains committed to the needs of its customers. Nevertheless, AFFIN Islamic will continue to be vigilant and careful with its credit policies while at the same time, the Group continues with its strategy on sustaining business growth, improving asset quality, enhancing operational efficiency and raising the quality of its human capital.

As a wholly-owned subsidiary of AFFINBANK, AFFIN Islamic will continue to leverage on the parent bank’s infrastructure including the over 80 branches across the country for better cost efficiency and reap group synergy.

RAtinG BY eXteRnAl AGencies

The Bank was not rated by any external rating agencies during the financial year.

ZAKAt

The Bank did not pay zakat on behalf of its depositors or shareholders. The Bank only pays zakat on its business.

DiRectORs’ RePORtfor the financial year ended 31 December 2008

��

HOlDinG cOmPAnY AnD UltimAte HOlDinG cORPORAte BODY

The holding company of the Bank is AFFIN Bank Berhad and the ultimate holding company is AFFIN Holdings Berhad.

AUDitORs

The auditors, PricewaterhouseCoopers, have expressed their willingness to continue in office.

Signed on behalf of the Board of Directors in accordance with their resolution dated 23 February 2009.

Gen tan sri Dato’ seri ismail bin Haji Omar (Rtd)Chairman

Kamarul Ariffin bin mohd JamilChief Executive Officer

DiRectORs’ RePORtfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Directors’ Report

��

BAlAnce sHeetsas at 31 December 2008

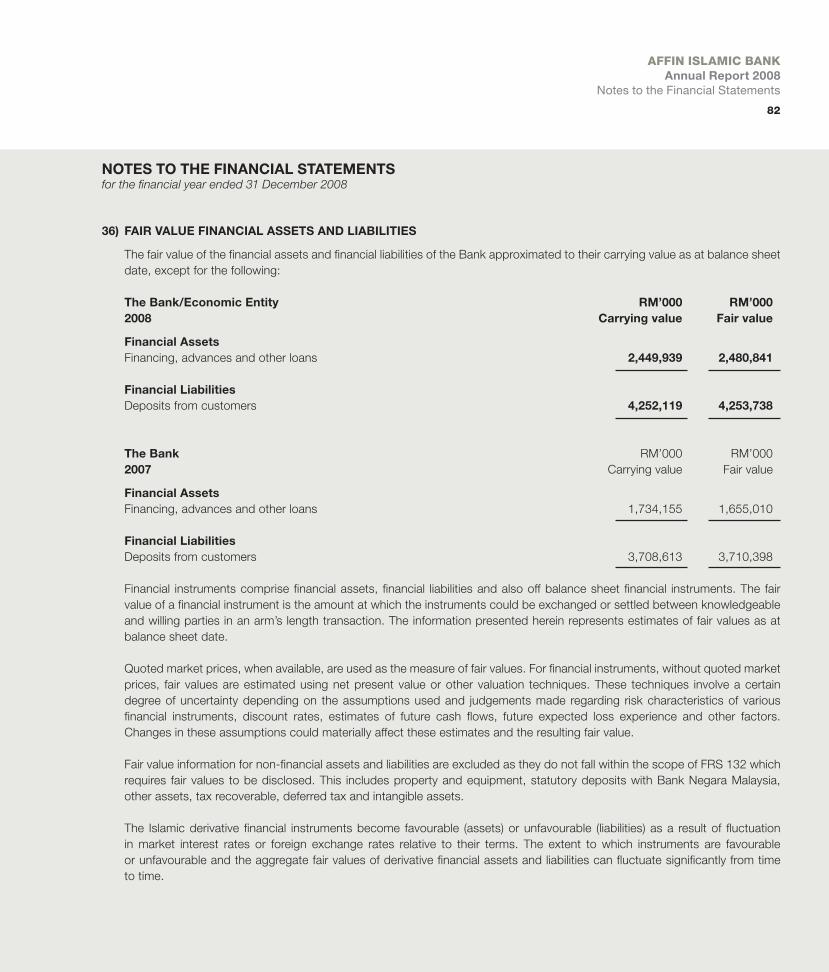

the Bank/ The Bank economic entity 2008 2007 note Rm’000 RM’000

AssetsCash and short-term funds 3 2,358,150 3,532,550Available-for-sale securities 4 1,071,326 774,250 Held-to-maturity securities 5 575 –Financing, advances and other loans 6 2,449,939 1,734,155 Other assets 8 52,585 135,676 Tax recoverable 5,187 – Statutory deposits with Bank Negara Malaysia 9 106,400 82,300 Investment in jointly controlled entity 10 500 – Amount due from jointly controlled entity 750 – Property and equipment 11 3,247 273 Land held for sale 12 15,000 – Intangible assets 13 1,392 1,610 Deferred tax assets 14 4,552 6,212

tOtAl Assets 6,069,603 6,267,026

liABilitiesDeposits from customers 15 4,252,119 3,708,613 Deposits and placements of banks and other financial institutions 16 1,261,205 2,078,923 Other liabilities 17 39,234 32,674 Amount due to holding company 18 254,374 207,611Provision for tax – 3,598

tOtAl liABilities 5,806,932 6,031,419

eQUitYShare capital 19 160,000 160,000 Reserves 20 102,671 75,607

tOtAl eQUitY 262,671 235,607

tOtAl liABilities AnD eQUitY 6,069,603 6,267,026

cOmmitments AnD cOntinGencies 31 6,994,462 3,917,054

The accounting policies on pages 23 to 34 and the notes on pages 35 to 84 form an integral part of these financial statements.

affin iSLaMiC bankAnnual Report 2008

Balance Sheets

��

incOme stAtementsfor the financial year ended 31 December 2008

the Bank/ The Bank economic entity 2008 2007 note Rm’000 RM’000

Income derived from investment of depositors’ funds and others 21 278,588 227,404 Income derived from investment of shareholders’ funds 22 12,062 11,240Allowance for losses on financing 23 (27,113) (9,146)Transfer from profit equalisation reserve 17 – 501

total distributable income 263,537 229,999

Income attributable to the depositors 24 (155,195) (124,618)

total net income 108,342 105,381

Personnel expenses 25 (9,501) (5,633)Other overheads and expenditures 26 (57,480) (41,863)

Profit before zakat and taxation 41,361 57,885

Zakat (2,359) (2,240)Taxation 28 (11,000) (16,205)

net profit after zakat and taxation 28,002 39,440

Attributable to: Equity holders of the Bank 28,002 39,440

earnings per share – basic/fully diluted (sen) 29 17.5 24.7

The accounting policies on pages 23 to 34 and the notes on pages 35 to 84 form an integral part of these financial statements.

affin iSLaMiC bankAnnual Report 2008Income Statements

stAtement Of cHAnGes in eQUitYfor the financial year ended 31 December 2008

non-Distributable Distributable

investment share statutory fluctuation Retained capital reserves reserves profits total Rm’000 Rm’000 Rm’000 Rm’000 Rm’000

the Bank/economic entity

At 1 January 2008 160,000 38,004 (401) 38,004 235,607

Net fair value change in available-for-sale securities – – (1,244) – (1,244)Deferred tax (Note 14) – – 306 – 306

Income and expenses recognised directly in equity – – (938) – (938)Net profit for the financial year – – – 28,002 28,002

Total recognised income and expense for financial year – – (938) 28,002 27,064Transfer to statutory reserves – 14,001 – (14,001) –

At 31 December 2008 160,000 52,005 (1,339) 52,005 262,671

the Bank

At 1 January 2007 160,000 18,284 128 18,284 196,696

Net fair value change in available-for-sale securities – – (717) – (717)Deferred tax (Note 14) – – 188 – 188

Income and expenses recognised directly in equity – – (529) – (529)Net profit for the financial year – – – 39,440 39,440Total recognised income and expense for financial year – – (529) 39,440 38,911

Transfer to statutory reserves – 19,720 – (19,720) –

At 31 December 2007 160,000 38,004 (401) 38,004 235,607

�0

affin iSLaMiC bankAnnual Report 2008

Statement of Changes in Equity

The accounting policies on pages 23 to 34 and the notes on pages 35 to 84 form an integral part of these financial statements.

��

the Bank/ The Bank economic entity 2008 2007 Rm’000 RM’000

cAsH flOWs fROm OPeRAtinG ActiVities

Profit before zakat and taxation 41,361 57,885

Adjustments for items not involving the movement of cash and cash equivalents: Income from securities – available-for-sale securities (13,259) (5,555)– held-to-maturity securities – (2,003)Amortisation of premium less accretion of discount– available-for-sale securities (18,570) (9,886)– held-to-maturity securities – 599Gain on sale from securities– held-for-trading securities (44) –– available-for-sale securities (57) –Gain on unrealised foreign exchange (18,361) (1,331)Depreciation of property and equipment 609 57 Amortisation of intangible asset 491 483 Net specific allowance for bad and doubtful financing 16,183 2,400 Income suspended 1,668 2,412 Charge of general allowances 10,824 6,600 Bad debt on financing written-off 220 146

OPeRAtinG PROfit BefORe cHAnGes in WORKinG cAPitAl 21,065 51,807

(Increase)/decreaseinoperatingassets:Held-for-trading securities 43 –Foreign exchange transaction 15,761 1,960Financing, advances and other loans (744,678) (518,420)Other assets 83,091 (124,316) Statutory deposits with Bank Negara Malaysia (24,100) (40,300)Amount due from jointly controlled entity (750) –

cAsH flOW stAtementsfor the financial year ended 31 December 2008

The accounting policies on pages 23 to 34 and the notes on pages 35 to 84 form an integral part of these financial statements.

affin iSLaMiC bankAnnual Report 2008Cash Flow Statements

cAsH flOW stAtementsfor the financial year ended 31 December 2008

the Bank/ The Bank economic entity 2008 2007 Rm’000 RM’000

Increase/(decrease)inoperatingliabilities:Deposits from customers 543,506 885,194Deposits and placements of banks and other financial institutions (817,717) 1,778,473Bills and acceptances payable – (23,689)Amount due to holding company 46,763 (277,425)Other liabilities 5,502 (37,704)

Cash generated from operations (871,514) 1,695,580Tax paid (17,819) (19,966)Zakat paid (1,299) –

net cAsH (UseD in)/GeneRAteD fROm OPeRAtinG ActiVities (890,632) 1,675,614

cAsH flOWs fROm inVestinG ActiVities

Increase in investment in jointly controlled entity (500) –Income received from securities– available-for-sale securities 13,259 5,555– held-to-maturity securities – 2,003Net sale of available-for-sale securities (279,695) (383,792)Redemption of held-to-maturity securities net of purchase (575) 90,000Purchase of property and equipment (3,620) (142)Purchase land held for sale (15,000) –Purchase of intangible assets (237) –

net cAsH UseD in fROm inVestinG ActiVities (286,368) (286,376)

net (DecReAse)/incReAse in cAsH AnD cAsH eQUiVAlents (1,177,000) 1,389,238

net incReAse/(DecReAse) in fOReiGn eXcHAnGe 2,600 (629)

cAsH AnD cAsH eQUiVAlents At BeGinninG Of tHe finAnciAl YeAR 3,532,550 2,143,941

cAsH AnD cAsH eQUiVAlents At enD Of tHe finAnciAl YeAR 2,358,150 3,532,550

AnAlYsis Of cAsH AnD cAsH eQUiVAlentsCash and short-term funds (Note 3) 2,358,150 3,532,550

��

affin iSLaMiC bankAnnual Report 2008

Cash Flow Statements

The accounting policies on pages 23 to 34 and the notes on pages 35 to 84 form an integral part of these financial statements.

��

sUmmARY Of siGnificAnt AccOUntinG POliciesfor the financial year ended 31 December 2008

A) BAsis Of PRePARAtiOn

The financial statements of the Bank have been prepared in accordance with Malaysian Accounting Standards Board (‘MASB’) Approved Accounting Standards in Malaysia for Entities Other Than Private Entities, Bank Negara Malaysia (‘BNM’) Guidelines, Shariah requirements and the provisions of the Companies Act, 1965. The Bank has adopted the revised Guidelines on Financial Reporting for Licensed Islamic Banks (‘BNM/GP8-i’) issued by BNM in June 2005.

The financial statements of the Bank have been prepared under the historical cost convention, unless otherwise indicated in this summary of significant accounting policies.

The preparation of financial statements in conformity with MASB Approved Accounting Standards in Malaysia for Entities Other Than Private Entities and BNM Guidelines requires the use of certain critical accounting estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenue and expenses during the reported period. It also requires Directors to exercise judgement in the process of applying the Bank’s accounting policies. Although these estimates are based on the Directors’ best knowledge of current events and actions, actual results may differ.

The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in Note (U).

(a) standards and amendments to the published standards that are applicable and effective to the Bank

The revisions to the published standards effective for the Bank’s financial period beginning 1 January 2008 are as follows:

– FRS 107 Cash Flow Statements

– FRS 112 Income Taxes

– FRS 118 Revenue

– FRS 134 Interim Financial Reporting

– FRS 137 Provisions, Contingent Liabilities and Contingent Assets

affin iSLaMiC bankAnnual Report 2008Summary of Significant Accounting Policies

A) BAsis Of PRePARAtiOn (continued)

(a) standards and amendments to the published standards that are applicable and effective to the Bank (continued)

The following describes the impact of new standards and amendments on financial statements of the Bank.

– The revised FRS 112 Income Taxes removes the requirements that prohibit recognition of deferred tax on unutilised reinvestment allowances or other allowances in excess of capital allowances. The adoption of this standard does not have any significant financial impact on the results of the Bank.

– Other revised standards have no significant changes compared to the original standards:

– FRS 107 Cash Flow Statements

– FRS 118 Revenue

– FRS 134 Interim Financial Reporting

– FRS 137 Provisions, Contingent Liabilities and Contingent Assets

The adoption of these revised standards did not have a material impact on the financial statements of the Bank.

(b) standards, amendments to the existing standards and interpretations that were effective in 2008 but not relevant to the Bank

The following standards, amendments and interpretations to published standards are mandatory for accounting periods beginning on or after 1 January 2008 but they are not relevant to the Bank’s operations:

– FRS 111 Construction Contracts

– FRS 120 Accounting for Government Grants and Disclosure of Government Assistant

– Amendments to FRS 121 The Effects of Changes in Foreign Exchange Rates – Net Investment in a Foreign Operations

– IC Interpretation 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities

– IC Interpretation 2 Members’ Shares in Co-operative Entities and Similar Instruments

– IC Interpretation 5 Rights to Interests Arising from Decommission, Restoration and Environmental Rehabilitation Funds

– IC Interpretation 6 Liabilities Arising from Participating in a Specific Market – Waste Electrical and Electronic Equipment

– IC Interpretation 7 Applying the Restatement Approach under FRS 129 Financial Reporting in Hyperinflationary Economies

– IC Interpretation 8 Scope of FRS 2

��

affin iSLaMiC bankAnnual Report 2008

Summary of Significant Accounting Policies

sUmmARY Of siGnificAnt AccOUntinG POliciesfor the financial year ended 31 December 2008

��

A) BAsis Of PRePARAtiOn (continued)

(c) standards, amendments to the published standards and interpretations to existing standards that are not yet effective and have not been early adopted

The new standards and IC Interpretations that are applicable to the Bank, but which the Bank has not early adopted, are as follows:

– FRS 8 Operating Segments (effective for accounting periods beginning on or after 1 July 2009). FRS 8 replaces FRS 114 2004 Segment Reporting. The new standard requires a ‘management approach’, under which segment information is presented on the same basis as that used for internal reporting purposes. The Group will apply this standard when effective.

– IC Interpretation 9 Reassessment of Embedded Derivatives (effective for accounting periods beginning on or after 1 January 2010). IC Interpretation 9 requires an entity to assess whether an embedded derivative is required to be separated from the host contract and accounted for as a derivative when the entity first becomes a party to the contract. Subsequent reassessment is prohibited unless there is a change in the terms of the contract that significantly modifies the cash flows that otherwise would be required under the contract, in which case reassessment is required. The Group will apply this standard when effective.

– IC Interpretation 10 Interim Financial Reporting and Impairment (effective for annual period beginning on or after 1 January 2010). IC Interpretation 10 prohibits the impairment losses recognised in an interim period on goodwill and investments in equity instruments and in financial assets carried at cost to be reversed at a subsequent balance sheet date. The Group will apply this standard when effective.

The following standards will be effective for annual period beginning on or after 1 January 2010. The Group will apply these standards when effective. The Group has applied the transitional provision in the respective standards which exempts entities from disclosing the possible impact arising from the initial application of the standard on the financial statements of the Group and Company.

– FRS 139 Financial Instruments: Recognition and Measurement

– FRS 7 Financial Instruments: Disclosures Nevertheless, the accounting policies of the Group incorporate revised BNM/GP8 which include selected principles of

FRS 139.

B) JOintlY cOntROlleD entities

Jointly controlled entities are corporations, partnerships or other entities over which there is contractually agreed sharing of control by the Bank with one or more parties where the strategic financial and operating decisions relating to the entities require unanimous consent of the parties sharing control.

Investment in jointly controlled entities are accounted for in the consolidated financial statements using the equity method of accounting and are initially recognised at cost.

sUmmARY Of siGnificAnt AccOUntinG POliciesfor the financial year ended 31 December 2008

affin iSLaMiC bankAnnual Report 2008Summary of Significant Accounting Policies

B) JOintlY cOntROlleD entities (continued)

The Bank’s share of the post-acquisition profits or losses of the jointly controlled entities are recognised in the income statement, and its share of the post-acquisition movements in reserves are recognised in reserves. The cumulative post-acquisition movements are adjusted against the carrying amount of the investment. When the Bank’s share of losses in a jointly controlled entity equals or exceeds its interest in the jointly controlled entity, including any other unsecured receivables, the Bank’s interest is reduced to nil and recognition of further losses is discontinued except to the extent that the Bank has incurred legal or constructive obligations or made payments on behalf of the jointly controlled entity.

Where necessary, adjustments have been made to the financial statements of jointly controlled entities to ensure consistency of accounting policies with those of the Bank.

Dilution gains and losses in jointly controlled entities are recognised in the income statement.

For incremental interest in a jointly controlled entity, the date of acquisition is purchase date at each stage and goodwill is calculated at each purchase date based on the fair value of assets and liabilities identified. There is no “step up to fair value” of net assets of previously acquired stake and the share of profits and equity movements for the previously acquired stake is recorded directly through equity.