Languages

Pages

Legal

SMMT MOTOR INDUSTRY FACTS 2018

WHAT IS SMMT?

The Society of Motor Manufacturers and

Traders (SMMT) is one of the largest and most

influential trade associations in the UK. Its

resources, reputation and unrivalled automotive

data place it at the heart of the UK automotive

industry. It undertakes a variety of activities

to support and represent the interests of the

industry and has a long history of achievement.

Working closely with member companies,

SMMT acts as the voice of the UK motor

industry, supporting and promoting its

interests, at home and abroad, to government,

stakeholders and the media.

SMMT represents more than 800 automotive

companies in the UK, providing them with a

forum to voice their views on issues affecting the

automotive sector, helping to guide strategies

and build positive relationships with government

and regulatory authorities.

To find out how to join SMMT

and for more information, visit www.smmt.co.uk/memberservices or email [email protected]

For media enquires please visit www.smmt.co.uk/contact/media-team or email [email protected]

WH

AT IS SMM

T?

02

CONTENTS

UK AUTOMOTIVE AT A GLANCE 4-5

UK AUTOMOTIVE INDUSTRY 6UK automotive employment 6UK automotive: background 7

MANUFACTURING 8UK automotive manufacturing 8UK car manufacturing 9UK car exports 10Global automotive manufacturing 11Map: UK automotive manufacturing sites 12-14Commercial vehicle manufacturing 15Engine manufacturing 16Digitalisation of automotive manufacturing 17

UK AUTOMOTIVE SUPPLY CHAIN 18UK AUTOMOTIVE AND THE EU 19A DAY IN UK AUTOMOTIVE 20

REGISTRATIONS 21New car registrations 21Changing consumer tastes 22Registrations by sales type 23Registrations by segment 24-26Commercial vehicle registrations 27

VEHICLES ON THE ROAD 28-29

UK automotive aftermarket 30

ENVIRONMENT AND AIR QUALITY 31-33Environment – CO2 31Environment – Air Quality 32Environment – WLTP and RDE 33

CONNECTED CARS 34-35SMMT GROUP 37

CON

TENTS

03

UK AUTOMOTIVE AT A GLANCEU

K AUTO

MO

TIVE AT A GLAN

CE

Specialist car manufacturers 60+

Suppliers2,500

Commercial vehicle manufacturers

Cars built in 2017

1,671,166

Engines built in 2017

2,722,325

Commercial vehicles built in 2017

78,219

People employed across UK Auto

856,000

UK automotive turnover

£82 billion

Cars currently on UK roads

34.7 million

Cars exported in 2017

1,334,538

New cars registered in 2017

2,540,617

Countries importing UK-built vehicles

160+

Engine manufacturers

869 9

5

20

6

05

04

UK AUTOMOTIVE EMPLOYMENTU

K AU

TOM

OTIV

E EMPLO

YMEN

T

25,000new jobs to be

created in automotive manufacturing

41,000 people employed

in UK motorsport – 25,000 are engineers

(Motorsport Industry

Association)

186,000people directly

employed in manufacturing

856,000 people employed

across UK automotive

78,480 young people

began engineering and manufacturing

apprenticeships in 2016/7

(Semta)

06

UK A

UTO

MO

TIVE: B

ACKGR

OU

ND

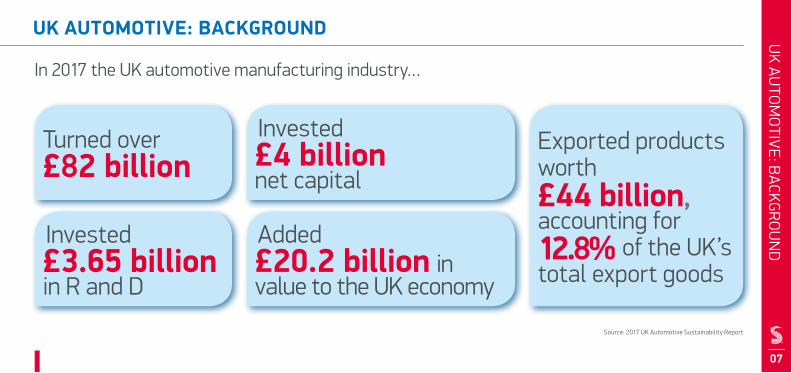

UK AUTOMOTIVE: BACKGROUND

In 2017 the UK automotive manufacturing industry…

Turned over £82 billion

Invested £3.65 billion in R and D

Exported products worth £44 billion, accounting for 12.8% of the UK’s total export goods

Invested £4 billion net capital

Added £20.2 billion in value to the UK economy

07

Source: 2017 UK Automotive Sustainability Report

UK A

UTO

MO

TIVE M

AN

UFA

CTURIN

GUK AUTOMOTIVE MANUFACTURING

Commercial vehicles by brandMake Volume

Vauxhall 59,795

Leyland Trucks 15,323

Alexander Dennis 1,734

Dennis Eagle 890

Wrightbus 303

Cars by brandMake Volume

Jaguar Land Rover 532,107

Nissan 495,206

BMW 218,885

Honda 164,160

Toyota 144,077

Cars by modelModel Volume

Nissan Qashqai 346,771

MINI 218,885

Honda Civic 122,885

Toyota Auris 119,020

Nissan Juke 104,770

Top fives in production – 2017

08

UK CA

R MA

NU

FACTU

RING

UK CAR MANUFACTURING

09

UK car manufacturing

UK car manufacturing – 2017 vs 2016YTD 2016 YTD 2017 % Change

Total 1,722,698 1,671,166 -3.0%

Home 373,255 336,628 -9.8%

Export 1,349,443 1,334,538 -1.1%

% export 78.3% 79.9%

2,000,000

1972 2009 2013 2014 2015 2016 20170

1,000,000

500,000

1,500,000

RECO

RD H

IGH

1,671,166

1.67M cars built in the UK in 2017, the

SECOND BIGGEST OUTPUT since the turn of the century

UK CA

R EXPORTS

UK CAR EXPORTS

1.33m cars manufactured for export in 2017

8 out of 10 cars made in the UK are exported

The UK exports to over 160 markets worldwide

10

TOP EXPORT DESTINATIONS FOR UK CARS

EU 53.9%

US 15.7%

CHINA 7.5%

AUSTRALIA 2.9%

TURKEY 2.6%

JAPAN 2.4%

CANADA 2.1%

SOUTH KOREA 1.6%

RUSSIA 1.2%

ISRAEL 0.9%

Germany

Italy

France

Belgium

Spain

Worldwide EU

THE UK EXPORTS TO 160 COUNTRIES WORLDWIDE

GLOB

AL A

UTO

MO

TIVE M

AN

UFA

CTURIN

GGLOBAL AUTOMOTIVE MANUFACTURING

Top 10 European automotive manufacturers in 2017Rank Country Cars Commercial

Vehicles Total % change

1 Germany 5,645,581 0 5,645,581 -1.76%

2 Spain 2,291,492 556,843 2,848,335 -1.30%

3 France 1,748,000 479,000 2,227,000 6.54%

4 UK 1,671,166 78,219 1,749,385 -3.70%

5 Czech Rep. 1,413,881 6,112 1,419,993 0.00%

6 Italy 742,642 399,568 1,142,210 3.53%

7 Slovakia 1,001,520 0 1,001,520 -3.70%

8 Poland 514,700 175,029 689,729 1.16%

9 Hungary 502,000 3,400 505,400 -4.01%

10 Belgium 336,000 43,140 379,140 -5.08%

Top 15 global automotive manufacturers in 2017Rank Country Cars Commercial

vehicles Total % change

1 China 24,806,687 4,208,747 29,015,434 3.19%

2 USA 3,033,216 8,156,769 11,189,985 -8.13%

3 Japan 8,347,836 1,345,910 9,693,746 5.31%

4 Germany 5,645,581 0 5,645,581 -1.76%

5 India 3,952,550 830,346 4,782,896 5.83%

6 South Korea 3,735,399 379,514 4,114,913 -2.69%

7 Mexico 1,900,029 2,168,386 4,068,415 13.00%

8 Spain 2,291,492 556,843 2,848,335 -1.30%

9 Brazil 2,269,468 430,204 2,699,672 25.20%

10 France 1,748,000 479,000 2,227,000 6.54%

11 Canada 749,458 1,450,331 2,199,789 -7.21%

12 Thailand 818,440 1,170,383 1,988,823 2.28%

13 UK 1,671,166 78,219 1,749,385 -3.70%14 Turkey 1,142,906 552,825 1,695,731 14.12%

15 Russia 1,348,029 203,264 1,551,293 19.01%

11

1

2 30 31

7

12

22

8

99 10

20

5

4

3

14

26

12

13

27

32

2928

15

2311

6

24

25

21

1617

1

18

11

19

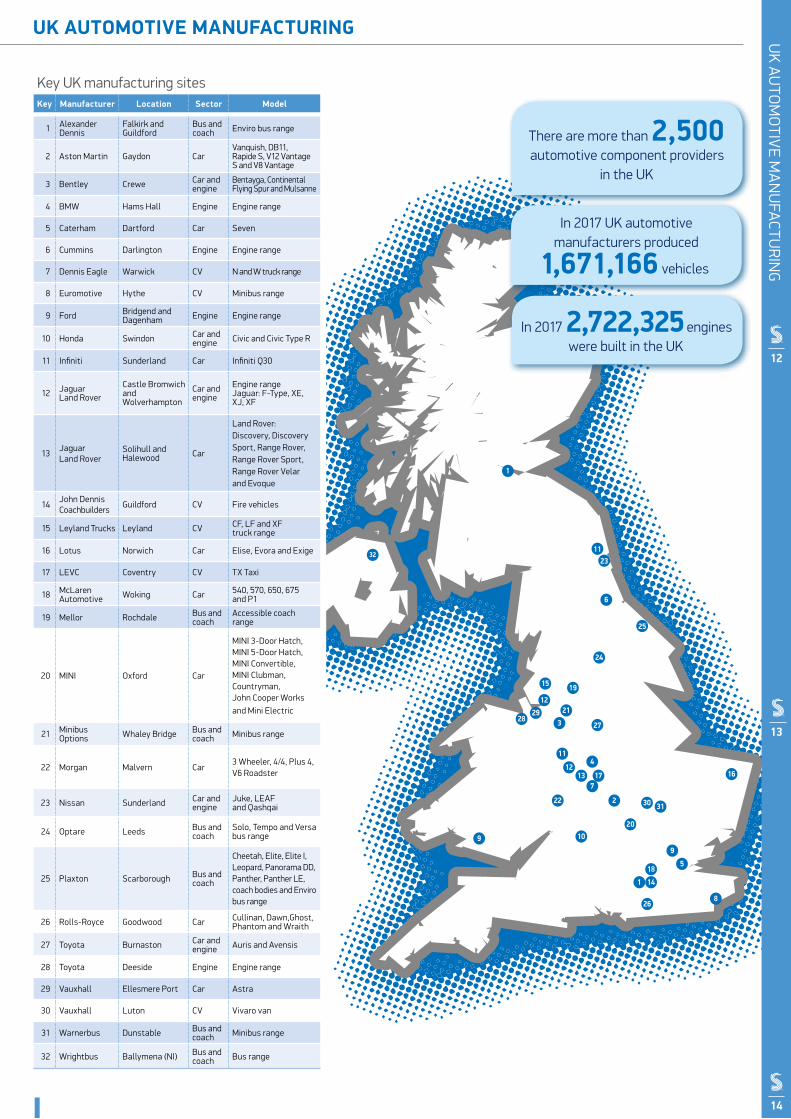

In 2017 UK automotive manufacturers produced

1,671,166 vehicles

In 2017 2,722,325 engines were built in the UK

There are more than 2,500 automotive component providers

in the UK

Key UK manufacturing sitesKey Manufacturer Location Sector Model

1 Alexander Dennis

Falkirk and Guildford

Bus and coach Enviro bus range

2 Aston Martin Gaydon CarVanquish, DB11, Rapide S, V12 Vantage S and V8 Vantage

3 Bentley Crewe Car and engine

Bentayga, Continental Flying Spur and Mulsanne

4 BMW Hams Hall Engine Engine range

5 Caterham Dartford Car Seven

6 Cummins Darlington Engine Engine range

7 Dennis Eagle Warwick CV N and W truck range

8 Euromotive Hythe CV Minibus range

9 Ford Bridgend and Dagenham Engine Engine range

10 Honda Swindon Car and engine Civic and Civic Type R

11 Infiniti Sunderland Car Infiniti Q30

12 Jaguar Land Rover

Castle Bromwich and Wolver hampton

Car and engine

Engine range Jaguar: F-Type, XE, XJ, XF

13Jaguar Land Rover

Solihull and Halewood Car

Land Rover: Discovery, Discovery Sport, Range Rover, Range Rover Sport, Range Rover Velar and Evoque

14John Dennis Coachbuilders

Guildford CV Fire vehicles

15 Leyland Trucks Leyland CV CF, LF and XF truck range

16 Lotus Norwich Car Elise, Evora and Exige

17 LEVC Coventry CV TX Taxi

18 McLaren Automotive Woking Car 540, 570, 650, 675

and P1

19 Mellor Rochdale Bus and coach

Accessible coach range

20 MINI Oxford Car

MINI 3-Door Hatch, MINI 5-Door Hatch, MINI Convertible, MINI Clubman, Countryman, John Cooper Works and Mini Electric

21 Minibus Options Whaley Bridge Bus and

coach Minibus range

22 Morgan Malvern Car3 Wheeler, 4/4, Plus 4, V6 Roadster

23 Nissan Sunderland Car and engine

Juke, LEAF and Qashqai

24 Optare Leeds Bus and coach

Solo, Tempo and Versa bus range

25 Plaxton Scarborough Bus and coach

Cheetah, Elite, Elite I, Leopard, Panorama DD, Panther, Panther LE, coach bodies and Enviro bus range

26 Rolls-Royce Goodwood Car Cullinan, Dawn,Ghost, Phantom and Wraith

27 Toyota Burnaston Car and engine Auris and Avensis

28 Toyota Deeside Engine Engine range

29 Vauxhall Ellesmere Port Car Astra

30 Vauxhall Luton CV Vivaro van

31 Warnerbus Dunstable Bus and coach Minibus range

32 Wrightbus Ballymena (NI) Bus and coach Bus range

UK AUTOMOTIVE MANUFACTURINGU

K AU

TOM

OTIV

E MA

NU

FACTU

RING

14

13

12

2016 2017 % Change

Total 93,924 78,219 -16.7%

Home 39,102 29,320 -25.0%

Export 54,842 48,899 -10.8%

% export 58.4% 62.5%

201470,869

201594,479

201693,924

201778,219

COM

MERCIA

L VEHICLE M

AN

UFACTU

RING

COMMERCIAL VEHICLE MANUFACTURING

UK Commercial Vehicle manufacturing volumes:2014 to 2017

UK Commercial Vehicle manufacturing – 2016 vs 2017

15

Proportion of British-built CVs exported to global markets rose to

62.5% in 2017 – the largest proportion in eight years

94.1% of CVs produced for international

markets, the majority bound for the EU

16

UK EN

GINE PR

OD

UCTIO

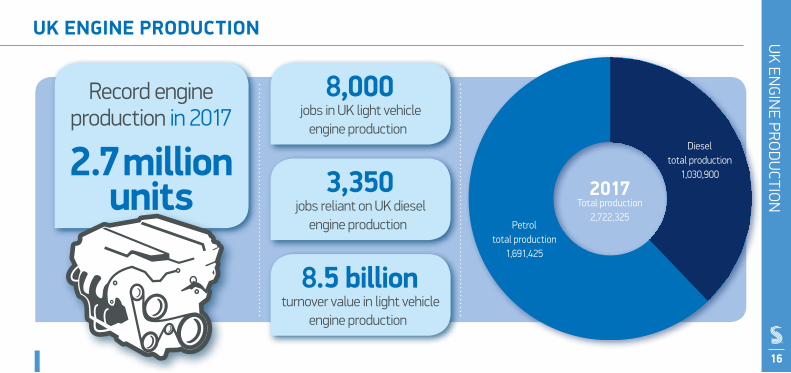

NUK ENGINE PRODUCTION

2017

Record engine production in 2017

2.7 million units

8,000jobs in UK light vehicle

engine production

3,350jobs reliant on UK diesel

engine production

8.5 billionturnover value in light vehicle

engine production

16

Total production2,722,325

Dieseltotal production

1,030,900

Petroltotal production

1,691,425

DIGITA

LISATION

OF M

AN

UFA

CTURIN

GDIGITALISATION OF AUTOMOTIVE MANUFACTURING

17

MACHINE DOWNTIMEREDUCED BY UP TO

40%

TIME TO MARKETREDUCED BY UP TO

25%

REDUCED PARTS INVENTORY BY UP TO

20%

INCREASED PRODUCTIVITY BY UP TO

5%

TOTAL CUMULATIVE ECONOMIC BENEFIT BY 2035

£74 billion

BENEFIT TO WIDER ECONOMY

£1.7 billion

BENEFIT TO VEHICLE MANUFACTURERS

£4.3 billion

BENEFIT TO SUPPLIERS

£2.6 billion

Source: SMMT and KPMG report The Digitalisation of the UK Automotive Industry (2016)

The digital revolution of the automotive industry is already underway. Vehicle manufacturers and suppliers are benefitting from increased productivity, greater flexibility and shorter times to market.

UK A

UTO

MO

TIVE SU

PPLY CHA

INUK AUTOMOTIVE SUPPLY CHAIN

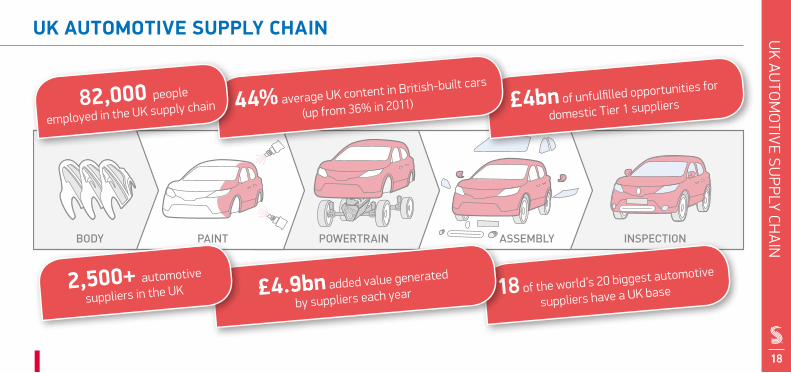

BODY PAINT POWERTRAIN ASSEMBLY INSPECTION

£4bn of unfulfilled opportunities for

domestic Tier 1 suppliers

18 of the world’s 20 biggest automotive

suppliers have a UK base

44% average UK content in British-built cars

(up from 36% in 2011) 82,000 people

employed in the UK supply chain

£4.9bn added value generated

by suppliers each year

18

2,500+ automotive

suppliers in the UK

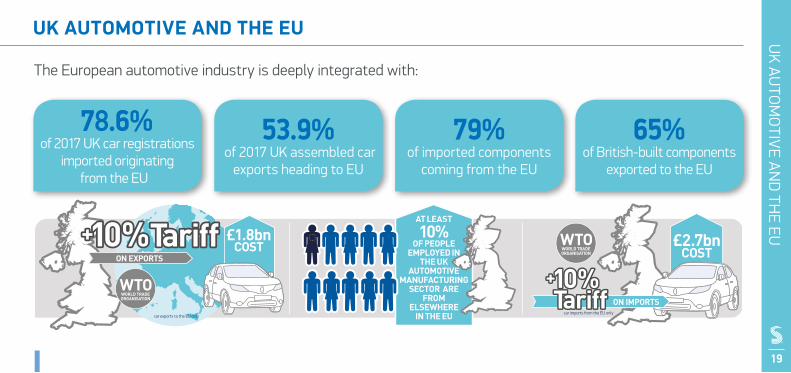

UK AUTOMOTIVE AND THE EUU

K AU

TOM

OTIV

E AN

D TH

E EU

19

AT LEAST

10% OF PEOPLE

EMPLOYED IN THE UK

AUTOMOTIVE MANUFACTURING

SECTOR ARE FROM

ELSEWHERE IN THE EU

£2.7bnCOST

ON IMPORTScar imports from the EU only

WTOWORLD TRADE ORGANISATION

ON EXPORTS

£1.8bnCOST

car exports to the EU only

WTOWORLD TRADE ORGANISATION

The European automotive industry is deeply integrated with:

78.6% of 2017 UK car registrations

imported originating from the EU

53.9% of 2017 UK assembled car

exports heading to EU

79% of imported components

coming from the EU

65% of British-built components

exported to the EU

1100 EU TRUCKS

deliver to UK car and engine

plants

6400 CARS

manufactured

10500 ENGINES manufactured

1300 CARS

distributed to UK dealers

4700 ENGINES

delivered to UKfactories

5100 CARS

exported worldwide

5700 ENGINES

exported worldwide

Import figures based on SMMT estimates;

output figures: SMMT from production

and export international exchange data

ComponentsWORTH£35m

delivered just in time

from EU

A D

AY IN U

K AU

TOM

OTIV

E

20

A DAY IN UK AUTOMOTIVE

REGISTRATIO

NS

NEW CAR REGISTRATIONS

Model Volume

1 Ford Fiesta 94,533

2 Volkswagen Golf 74,605

3 Ford Focus 69,903

4 Nissan Qashqai 64,216

5 Vauxhall Corsa 52,772

6 Vauxhall Astra 49,370

7 Volkswagen Polo 47,855

8 MINI 47,669

9 Mercedes-Benz C Class 45,912

10 Mercedes-Benz A Class 43,717

3,000,000

’01 ’02 ’03 ’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 ’14 ’150

2,000,000

1,500,000

1,000,000

500,000

2,500,000

’16 ’17

2,540,617

Annual New Car Registrations – 2001 to 2017

Top 10 UK sellers in 2017

21

New car registrations by fuel type – 2017 vs 2007

2007

2017

1,065,879

1,354,917

119,821

16,641

DIES

ELPE

TROL

AFV

DIES

ELPE

TROL

AFV

967,413

1,419,953

CHA

NGIN

G CON

SUM

ER TASTES

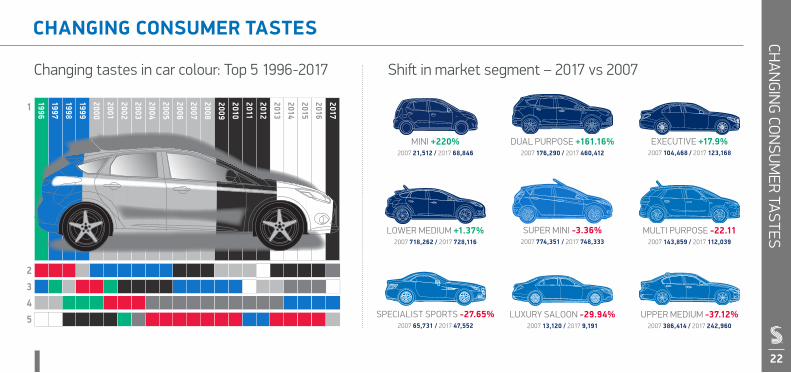

CHANGING CONSUMER TASTES

Changing tastes in car colour: Top 5 1996-2017

22

Shift in market segment – 2017 vs 2007

MINI +220%2007 21,512 / 2017 68,846

SPECIALIST SPORTS -27.65%2007 65,731 / 2017 47,552

LOWER MEDIUM +1.37%2007 718,262 / 2017 728,116

SUPER MINI -3.36%2007 774,351 / 2017 748,333

DUAL PURPOSE +161.16%2007 176,290 / 2017 460,412

LUXURY SALOON -29.94%2007 13,120 / 2017 9,191

UPPER MEDIUM -37.12%2007 386,414 / 2017 242,960

EXECUTIVE +17.9%2007 104,468 / 2017 123,168

MULTI PURPOSE -22.112007 143,859 / 2017 112,039

1

2

34

5

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

REGISTR

ATION

S BY SA

LES TYPEREGISTRATIONS BY SALES TYPE

FleetModel Volume

Volkswagen Golf 47,865

Ford Focus 42,130

Nissan Qashqai 41,685

Ford Fiesta 38,132

Vauxhall Astra 37,510

PrivateModel Volume

Ford Fiesta 56,400

Volkswagen Polo 30,487

MINI 28,188

Ford Focus 27,771

Volkswagen Golf 25,380

Top five new car registrations in 2017 by sales type

BusinessModel Volume

Vauxhall Corsa 13,857

Vauxhall Viva 6,940

Vauxhall Astra 3,615

Vauxhall Mokka X 3,436

Mitsubishi Outlander 2,901Business

3.8%

51.9%

44.2%

2017 registrations by sales type

Business If the vehicle is being registered by a company that operates up to 24 vehicles, it is designated a business sale. This includes dealer demonstrators.

Fleet If the vehicle is being registered by a company that operates a fleet of 25 or more vehicles, it is designated a fleet sale. This includes dealer demonstrators and Motability-leased vehicles. Private If the vehicle is being registered primarily for the personal use of a private individual, it is designated a private sale.

23

Fleet

Private

REGISTR

ATION

S BY SEGM

ENT

REGISTRATIONS BY SEGMENT

Supermini

Lower M

edium

Model Volume Segment share

Hyundai i10 25,224 36.7%

Volkswagen up! 13,555 19.7%

Vauxhall Viva 9,963 14.5%

Suzuki Celerio 6,755 9.9%

Skoda Citigo 6,527 9.5%

Segment total: 68,846

Model Volume Segment share

Ford Fiesta 94,533 12.6%

Vauxhall Corsa 52,772 7.0%

Volkswagen Polo 47,855 6.4%

MINI 47,669 6.4%

Nissan Juke 38,912 5.2%

Segment total: 748,333

Model Volume Segment share

Volkswagen Golf 74605 10.2%

Ford Focus 69903 9.6%

Nissan Qashqai 64216 8.8%

Vauxhall Astra 49370 6.8%

Mercedes A-Class 43717 6.0%

Segment total: 728,116

Mini

Top cars registered by segment

24

REGISTRATIONS BY SEGMENTR

EGISTRATIO

NS B

Y SEGMEN

T

Top cars registered by segment

Model Volume Segment share

Mercedes-Benz C Class 45,912 10.4%

Mercedes-Benz E Class 26,733 21.7%

BMW 5 Series 19,477 15.8%

Audi A6 12,768 10.4%

Jaguar XF 7,710 6.3%

Segment total: 123,168

Executive

Model Volume Segment share

BMW 3 Series 35,904 14.8%

Audi A4 25,294 10.4%

BMW 4 Series 22,050 9.0%

Skoda Octavia 20,493 8.4%

Vauxhall Insignia 16,884 6.9%

Segment total: 242,960

Upper M

edium

Model Volume Segment share

Mercedes-Benz S Class 2,939 32.0%

BMW 7 Series 2,274 24.7%

Jaguar XJ 970 10.6%

Bentley Continental 770 8.4%

Audi A8 749 8.2%

Segment total: 9,191

Luxury

25

REGISTR

ATION

S BY SEGM

ENT

REGISTRATIONS BY SEGMENT

Top cars registered by segment

Specialist Sports

Dual Purpose

MPV

26

Model Volume Segment share

Audi TT 7,762 16.3%

Volkswagen Scirocco 4,935 10.4%

Mazda MX-5 4,698 9.9%

Mercedes SLC 3,664 7.7%

Porsche 718 2,556 5.4%

Segment total: 47,552

Model Volume Segment share

Kia Sportage 39,683 8.6%

Ford Kuga 39,212 8.5%

Hyundai Tucson 29,430 6.4%

Volkswagen Tiguan 29,121 6.3%

Range Rover Evoque 24,906 5.4%

Segment total: 460,412

Model Volume Segment share

Ford C-MAX 12,655 11.3%

Vauxhall Zafira Tourer 12,219 10.9%

Citroen C4 Picasso 11,017 9.8%

Ford S-MAX 5,977 5.3%

Ford B-MAX 5,930 5.3%

Segment total: 112,039

COM

MER

CIAL V

EHICLE R

EGISTRATIO

NS

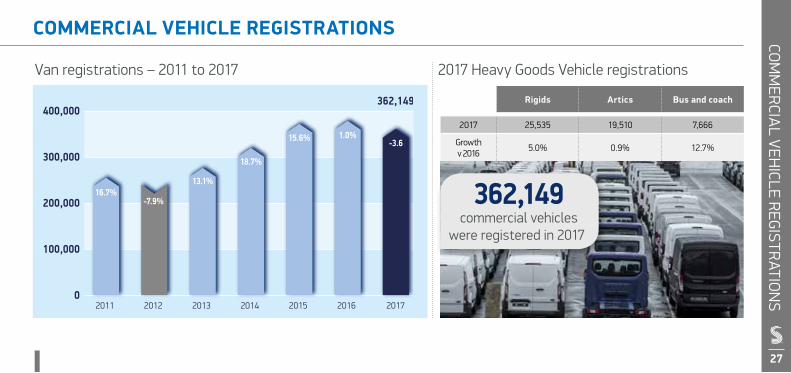

COMMERCIAL VEHICLE REGISTRATIONS

Van registrations – 2011 to 2017

Rigids Artics Bus and coach

2017 25,535 19,510 7,666

Growth v 2016

5.0% 0.9% 12.7%

0

100,000

200,000

300,000

400,000362,149

2014201320122011 20172015 2016

16.7%-7.9%

13.1%

18.7%

15.6% 1.0%-3.6

362,149 commercial vehicles

were registered in 2017

27

2017 Heavy Goods Vehicle registrations

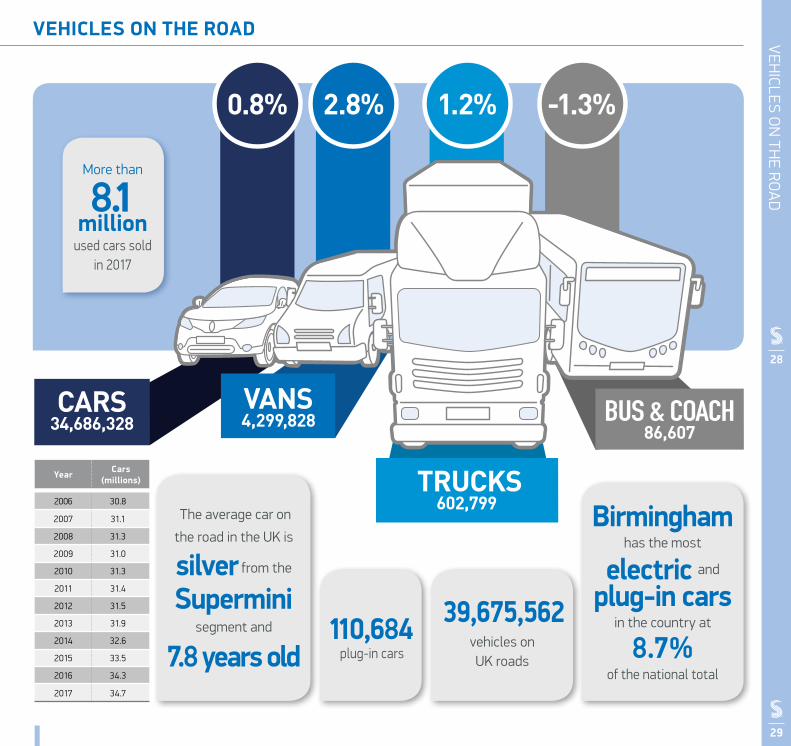

VEHICLES ON THE ROADV

EHICLES O

N TH

E RO

AD

0.8% 2.8% -1.3%1.2%

VANS4,299,828 BUS & COACH

86,607

TRUCKS602,799

CARS34,686,328

Year Cars (millions)

2006 30.8

2007 31.1

2008 31.3

2009 31.0

2010 31.3

2011 31.4

2012 31.5

2013 31.9

2014 32.6

2015 33.5

2016 34.3

2017 34.7

28

29

39,675,562 vehicles on UK roads

110,684 plug-in cars

More than

8.1 million

used cars sold in 2017

Birmingham has the most

electric and

plug-in cars in the country at

8.7% of the national total

The average car on

the road in the UK is

silver from the

Supermini segment and

7.8 years old

UK A

UTO

MO

TIVE A

FTERM

AR

KE

TUK AUTOMOTIVE AFTERMARKET

£12.2 billion contribution to UK economy

345,600 jobs supported

£695.39average annual spend per car

£21.1 billion revenue of UK a�ermarket

Services more than

30 millionvehicles a year

The Importance of the Aftermarket to the UK Economy

30Source: SMMT and Frost & Sullivan Reports: The Importance of the UK Aftermarket to the UK Economy (2017)

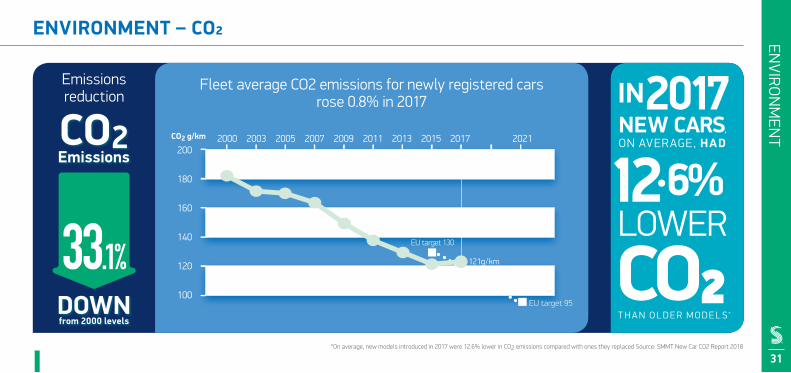

ENVIRONMENT – CO2EN

VIRO

NM

ENT

Emissions reduction

31

CO2 g/km

EU target 95

EU target 130

UK

140

120

100

160

180

200 2011 2009 2007 2005 2003 2000 2013 2015 2017 2021

121g/km

Fleet average CO2 emissions for newly registered cars rose 0.8% in 2017

*On average, new models introduced in 2017 were 12.6% lower in CO2 emissions compared with ones they replaced Source: SMMT New Car CO2 Report 2018

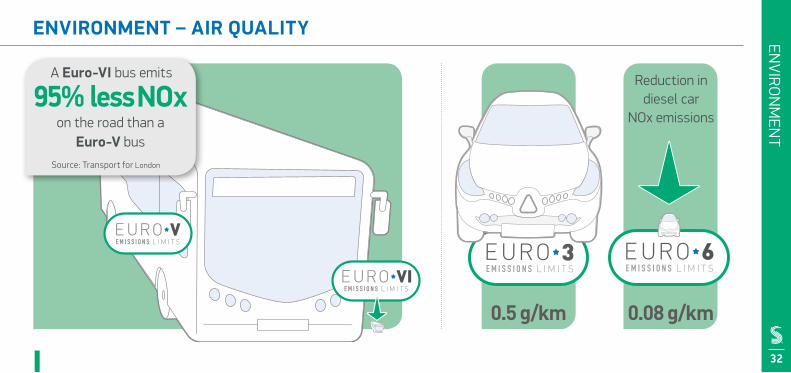

ENVIR

ON

MEN

TENVIRONMENT – AIR QUALITY

A Euro-VI bus emits

95% less NOx on the road than a

Euro-V busSource: Transport for London

0.5 g/km 0.08 g/km

Reduction in diesel car

NOx emissions

32

ENVIR

ON

MEN

T – WLTP

33

CAR EMISSIONS TESTING

Introduced in 2017, the WLTP (Worldwide Harmonised Light Vehicle Test Procedure) was introduced to replace the old NEDC lab test.

A lab test to measure fuel consumption, CO2 and pollutant emissions from cars:

■ Test cycle data based on real-driving data ■ Variety of driving phases tested■ Powertrain configuration of each car tested for the car’s lightest and heaviest version

New WLTP test from September 2017 RDEThe Real Driving Emissions (RDE) test measures pollutants while a car is driven on public roads, complementing the WLTP lab test.

Portable Emission Measuring System (PEMS) measures data collected while car is driven in a variety of conditions:

Low speed (urban roads)Medium speed (rural roads)High speed (motorways)Low and high altitudesYear-round temperaturesAdditional vehicle payloadDifferent gradients

RDE provides a snapshot of a vehicle’s performance on the road

Why do we still need a lab test?The new WLTP test is much more representative and lab tests allow for a standardised, repeatable testing model which enables comparisons of one car’s emissions to the next.

6/10 people*with limited mobility will have

an improved quality of life

£51 BillionValue added annually by 2030

(at 2014 prices)

Top 5 benefits of CAVs

• Reduced stress of driving• Ability to rest on longer journeys• Fewer accidents• Lower insurance costs• Ability to travel at preferred times

320,000Additional jobs created,

25,000Jobs in automotive

manufacturing created by 2030

*when surveyed

CAVs could give

1 million UK people better access

to higher education

CONNECTED AND AUTONOMOUS VEHICLESCON

NECTED A

ND AU

TON

OM

OU

S VEHICLES

UK social and economic impact of connected and autonomous vehicles

34Sources:SMMT and KPMG report, 2014: Connected and Autonomous Vehicles: The UK Economic Opportunity and SMMT and PwC report, 2017: CAVs: Revolutionising Mobility in Society

CONN

ECTED AN

D AUTO

NO

MO

US VEH

ICLES

35

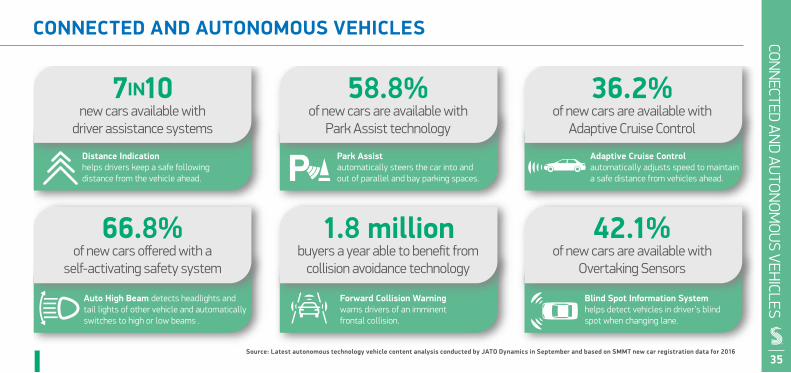

CONNECTED AND AUTONOMOUS VEHICLES

Forward Collision Warningwarns drivers of an imminent frontal collision.

Auto High Beam detects headlights and tail lights of other vehicle and automatically switches to high or low beams .

Blind Spot Information Systemhelps detect vehicles in driver’s blind spot when changing lane.

Park Assistautomatically steers the car into and out of parallel and bay parking spaces.

Adaptive Cruise Controlautomatically adjusts speed to maintain a safe distance from vehicles ahead.

7IN10 new cars available with

driver assistance systems

58.8% of new cars are available with

Park Assist technology

36.2% of new cars are available with

Adaptive Cruise Control

66.8% of new cars offered with a

self-activating safety system

1.8 million buyers a year able to benefit from

collision avoidance technology

42.1% of new cars are available with

Overtaking Sensors

Distance Indicationhelps drivers keep a safe following distance from the vehicle ahead.

Source: Latest autonomous technology vehicle content analysis conducted by JATO Dynamics in September and based on SMMT new car registration data for 2016

SMMT Industry ForumIndustry Forum was formed

in 1994, initially as a unique

collaboration between leading

vehicle manufacturers, SMMT

and government to improve the

performance and competitiveness of

the UK’s automotive supply chain.

Continued measurable success has led to

sustained growth into many other sectors including

aerospace, construction, domestic appliances,

electronics and food. Industry Forum now provides

support to blue chip organisations in more than 30

countries across five continents.

www.industryforum.co.uk

The Motor OmbudsmanThe Motor Ombudsman is the

automotive dispute resolution

body. Fully-impartial, it is the

first ombudsman to be focused

solely on the automotive

sector, and self-regulates

the UK’s motor industry through its comprehensive

Motor Industry Codes of Practice which have each

been approved by the Chartered Trading Standards

Institute’s Consumer Codes Approval Scheme (CCAS).

www.themotorombudsman.org

SMM

T GROU

PSMMT GROUP

37

DIS C L A IM E R

This publication contains general in for mat ion

a n d , a lt h o u g h S M M T endeavours to ensure

that the content is accurate and up-to-date

at the date of publication, no representation

or warranty, express or implied, is made as to

its accuracy or completeness and therefore

the infor mat ion in th is publ icat ion should

not be rel ied upon. Readers should always

s eek a p pr opr iate a d v ice f r o m a s u i t a bly

qualif ied expert before taking, or refraining

f rom tak ing, any ac t ion . T he content s of

th is publ icat ion should not be constr ued

as advice or guidance and SMMT disclaims

l iabil i t y for any loss, howsoever caused,

ar is ing d irec tly or indirec tly f rom rel iance

on the infor mat ion in th is publ icat ion. Any

use of data should be credited to SMMT.

THE SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED71 Great Peter Street, London, SW1P 2BNTel: +44 (0)20 7235 7000E-mail: [email protected]

:@SMMT :SMMT

www.smmt.co.uk

May 2018

Top Related