Languages

Pages

Legal

1

Smart Beta 2.0: A Disruptive Innovation

By Steven Vannelli, CFA, Eric Bush, CFA, Bryce Coward, CFA, and Jennifer Thomson

At the beginning of ever major disruptive innovation, fear, uncertainty and doubt reign supreme. Consumers are fearful of the

unknown, uncertain of the benefits and doubt the durability of the innovation. But, in the end, fear, uncertainty and doubt give

way to confidence, understanding and acceptance. The fund management industry is on the cusp of a major disruptive

innovation.

In “Smart Beta 2.0: The Next Battleground for Asset Management Dollars Heats Up,” Moody’s describes how “asset

managers are accelerating their expansion in the smart beta space, as alternative index strategies become more

sophisticated and gain broader acceptance.”

The report continues: “This accelerating activity has coincided with a shift in the evolution of smart beta products from the

basic – simple and static security selection and weighting schemes – towards the development of more sophisticated

products that are based on multiple factors and timing of exposures. Smart beta’s next phase – call it ‘smart beta 2.0’ – will

be more research intensive.

“This next phase will likely place smart beta funds in direct competition with traditional mutual funds … In a sense, smart

beta 2.0 will evolve into a more disciplined and cheaper form of active management – that is, it will attempt to achieve the

goals of traditional active managers, but at a lower cost and with more consistency in terms of adhering to a set of investing

rules.

“Those most at risk are traditional mutual funds with highly diversified portfolios whose performance closely tracks, and

typically lags, the index – e.g., closet indexers with over 100 securities in their portfolios. The AUM loss from these firms

could directly accrue to asset managers well-positioned to offer the next iteration of smart beta funds.”

Smart beta is a disruptive innovation for investors. The promise of smart beta is excess returns in a cheaper, simpler and

more predictable way. Before now, only mutual funds managed by humans could boast the potential for excess returns—

and, if and when they did generate alpha, it was not necessarily repeatable: there were more unknowns, higher fees and

higher taxes. Smart beta aims to capture these same excess returns in a cheaper, transparent and predictable, rules-based

way.

Passive vs. Active vs. Index Realities

The emergence of ETFs in the 1990s allowed investors to invest mechanically in broad equity market segments for the first

time. Previously, most assets in the United States were actively managed by investment managers. Over time, investors

began to view the decision to invest in an index fund as a “passive” investment, and the decision to hire a portfolio manager

via a mutual fund as an “active” investment. The emergence of smart beta funds has blurred the lines.

Today many view a fund following an index as a “passive” investment, which doesn’t quite tell the whole story. In “Indexes

Can Be Passive, Active Can be Indexes, but Passive Can’t Be Active,” John Rekenthaler describes Morningstar’s approach:

“Historically, active and index investing have been viewed as binary events. A fund is either one or the other… It is fine to

place exchange traded funds and indexed mutual funds into the same index group, and put all remaining mutual funds into

2

Smart Beta 2.0: A Disruptive Innovation

the active group… Although even then, a third set is helpful. There’s a difference between indexes that weight securities

according to market capitalization… and indexes that incorporate viewpoints… By our reckoning, the active/index duo

should expand to three: 1) actively managed funds, 2) index funds weighted by market cap, and 3) strategic beta index

funds.

“Let’s switch from discussing active vs. passive to active vs. index. Those are not the same things because passive is not a

synonym for indexing. A passive fund is a fund that does not express a viewpoint. An index fund is a fund that mimics a list

of securities. Those are two different things. Thus a strategic beta fund is an index fund, but it is not a passive fund.”

Let’s start by decomposing the terms passive and active management. A passively managed fund is designed not to take a

viewpoint, as Rekenthaler put it, which means that passive funds follow benchmark indexes like the S&P 500 or MSCI World

Index. When he says that passive funds don’t have a viewpoint, what he means is that they simply own all the stocks in a

benchmark index, in the exact same weight. No human decisions are made in a passive fund. As the index changes, the fund

is similarly adjusted. The fund performs almost identically to the underlying index, minus fees.

Traditionally, an actively managed fund is managed on a discretionary basis by a portfolio manager to achieve results relative

to some benchmark. Portfolios usually represent a small fraction of the companies in the reference benchmark. Changes to

the composition of the portfolio occur continuously as the portfolio manager adjusts the portfolio to pursue opportunities. For

actively managed funds, performance tends to deviate from the benchmark, sometimes better and sometimes worse, minus

fees.

A new form of active management has emerged, called smart beta. Smart beta ETFs are designed to follow an index, but

that index is different than a benchmark index. Smart beta indexes do take a viewpoint on markets and express that

viewpoint by a selection and/or weighting scheme that differs from a benchmark index. If we consider the true “activeness”

of a fund—as we will discuss in the next section—rather as the extent to which a portfolio differs from a broad benchmark,

then we can much more effectively analyze a fund’s true contribution to an overall portfolio.

Morningstar’s Rekenthaler goes on to describe the evolution of the fund management industry since 1994: “Active

management dominated for the first 10 years … market indexes took control after the 2008 market crash and has never

looked back; and … strategic beta, the newest member of the troika, is rapidly becoming a major force.”

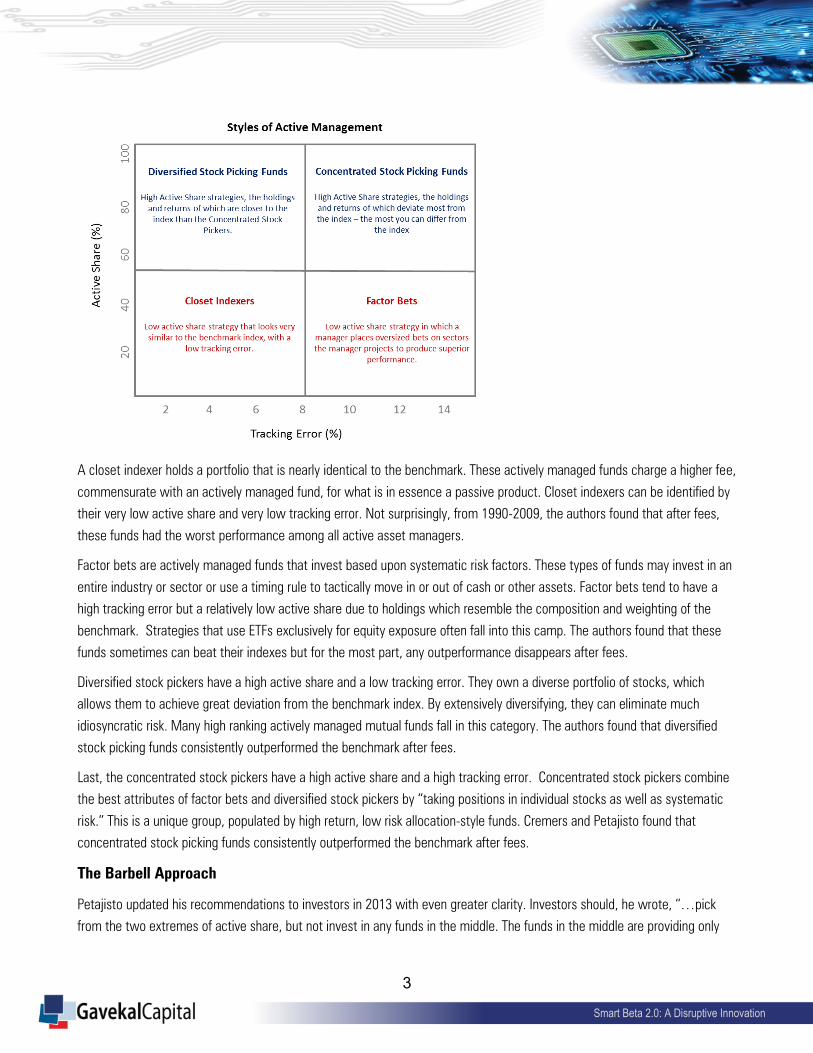

Understanding Active Share

Thanks to the work done by Martijn Cremers and Antti Petajisto, investors now have a tool to measure how “active” a fund

really is. Active share is a percentage (ranging from 0% to 100%) for long-only funds that measures how different a fund’s

holdings are from the benchmark holdings. Cremers and Petajisto combine active share with tracking error to devise four

types of active management styles: 1) closet indexer, 2) factor bet, 3) diversified stock picker, and 4) concentrated stock

picker. Many actively managed funds, it turns out, tend to hold a portfolio of stocks that look very similar to the reference

benchmark.

3

Smart Beta 2.0: A Disruptive Innovation

A closet indexer holds a portfolio that is nearly identical to the benchmark. These actively managed funds charge a higher fee,

commensurate with an actively managed fund, for what is in essence a passive product. Closet indexers can be identified by

their very low active share and very low tracking error. Not surprisingly, from 1990-2009, the authors found that after fees,

these funds had the worst performance among all active asset managers.

Factor bets are actively managed funds that invest based upon systematic risk factors. These types of funds may invest in an

entire industry or sector or use a timing rule to tactically move in or out of cash or other assets. Factor bets tend to have a

high tracking error but a relatively low active share due to holdings which resemble the composition and weighting of the

benchmark. Strategies that use ETFs exclusively for equity exposure often fall into this camp. The authors found that these

funds sometimes can beat their indexes but for the most part, any outperformance disappears after fees.

Diversified stock pickers have a high active share and a low tracking error. They own a diverse portfolio of stocks, which

allows them to achieve great deviation from the benchmark index. By extensively diversifying, they can eliminate much

idiosyncratic risk. Many high ranking actively managed mutual funds fall in this category. The authors found that diversified

stock picking funds consistently outperformed the benchmark after fees.

Last, the concentrated stock pickers have a high active share and a high tracking error. Concentrated stock pickers combine

the best attributes of factor bets and diversified stock pickers by “taking positions in individual stocks as well as systematic

risk.” This is a unique group, populated by high return, low risk allocation-style funds. Cremers and Petajisto found that

concentrated stock picking funds consistently outperformed the benchmark after fees.

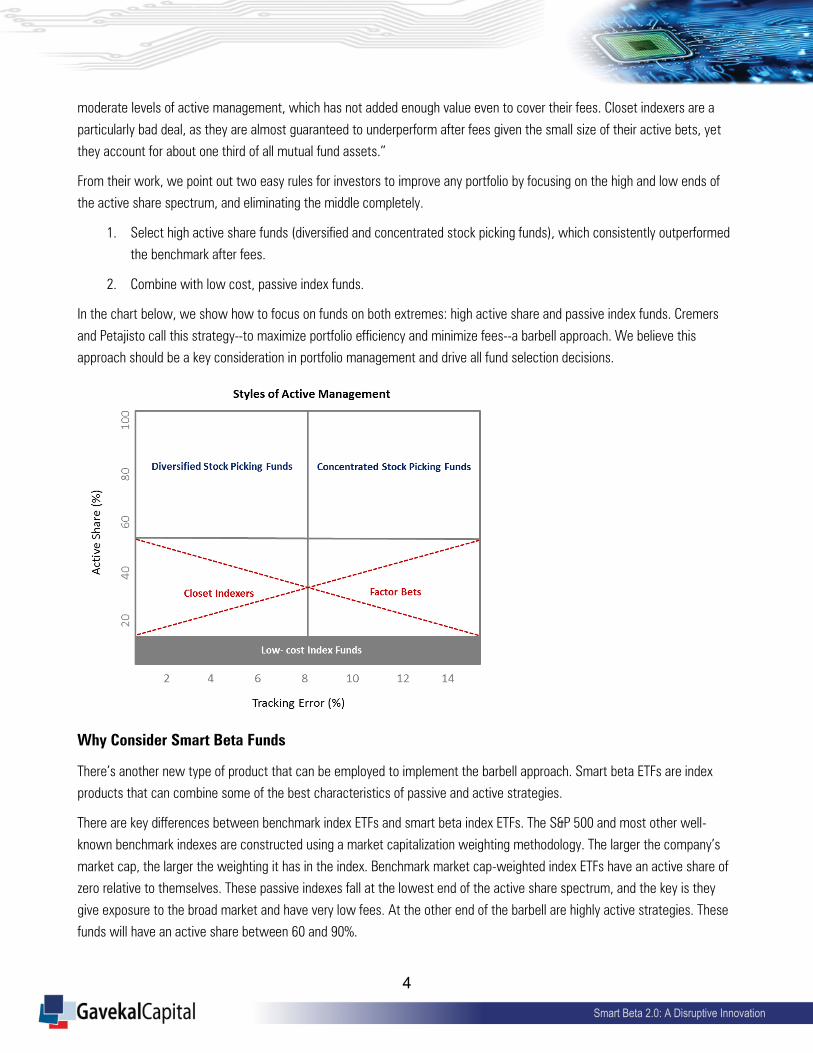

The Barbell Approach

Petajisto updated his recommendations to investors in 2013 with even greater clarity. Investors should, he wrote, “…pick

from the two extremes of active share, but not invest in any funds in the middle. The funds in the middle are providing only

4

Smart Beta 2.0: A Disruptive Innovation

moderate levels of active management, which has not added enough value even to cover their fees. Closet indexers are a

particularly bad deal, as they are almost guaranteed to underperform after fees given the small size of their active bets, yet

they account for about one third of all mutual fund assets.”

From their work, we point out two easy rules for investors to improve any portfolio by focusing on the high and low ends of

the active share spectrum, and eliminating the middle completely.

1. Select high active share funds (diversified and concentrated stock picking funds), which consistently outperformed

the benchmark after fees.

2. Combine with low cost, passive index funds.

In the chart below, we show how to focus on funds on both extremes: high active share and passive index funds. Cremers

and Petajisto call this strategy--to maximize portfolio efficiency and minimize fees--a barbell approach. We believe this

approach should be a key consideration in portfolio management and drive all fund selection decisions.

Why Consider Smart Beta Funds

There’s another new type of product that can be employed to implement the barbell approach. Smart beta ETFs are index

products that can combine some of the best characteristics of passive and active strategies.

There are key differences between benchmark index ETFs and smart beta index ETFs. The S&P 500 and most other well-

known benchmark indexes are constructed using a market capitalization weighting methodology. The larger the company’s

market cap, the larger the weighting it has in the index. Benchmark market cap-weighted index ETFs have an active share of

zero relative to themselves. These passive indexes fall at the lowest end of the active share spectrum, and the key is they

give exposure to the broad market and have very low fees. At the other end of the barbell are highly active strategies. These

funds will have an active share between 60 and 90%.

5

Smart Beta 2.0: A Disruptive Innovation

Smart beta indexes are defined by their adherence to a rules-based, quantitative approach. Smart beta indexes use non-

capitalization weighted, rules-based methodologies to construct an index. A smart beta strategy could be a based on a

fundamental characteristic (such as growth or dividend yield) or it could be based on a factor (such as size or knowledge

intensity). What is most interesting about smart beta indexes is that they can exhibit active characteristics as a result of

intentional deviations from traditional capitalization weighted benchmark indexes. This means smart beta indexes can have a

high active share, offering investors an important additional tool which can be used alongside both passive and actively

managed investments to create efficient portfolios that seek to combine the best of passive and active investment

approaches while reducing fees. In the graphic below, we illustrate the three fund types.

In this paper, we’ll use two smart beta-style indexes, the Gavekal Knowledge Leaders Indexes, to illustrate the application of

smart beta in the barbell approach. You can see in the graphic below dividing Cremers and Petajisto’s styles of active

management, the Gavekal Knowledge Leaders Indexes are diversified stock picking strategies. This quadrant is one in which

many best-in-class actively managed mutual funds fall because of their very high active share and low tracking error. The high

active share of the Gavekal Knowledge Leaders Indexes results from selection criteria (stocks are selected using a risk factor,

the Knowledge Factor) and weighting criteria (equal weighted), resulting in a high active share compared to the benchmark.

We’ll simulate an optimization later in this paper that reveals the results and fee impact smart beta can make on a portfolio.

6

Smart Beta 2.0: A Disruptive Innovation

Gavekal Knowledge Leaders Developed World Index has an active share of 72% and a tracking error of 4.0%. Gavekal

Knowledge Leaders Emerging Markets Index has an active share of 85% and a tracking error of 6.9%. Calculations by Gavekal

Capital.

Tax Considerations

One more significant reason to consider employing smart beta ETFs is tax impact. When evaluating the contributions that

mutual funds and ETFs will make to the overall portfolio, it is also important to understand issues of intra-day liquidity and tax

efficiency. Mutual fund trades are settled once per day, at the end of the market close, and all trades are settled at the end-

of-the-day net asset value (NAV). Mutual funds generally hold limited amounts of cash, so a big redemption may necessitate

a fund to sell a portion of its holdings to raise cash. These transactions can impact fund holdings and lead to realized capital

gains for the remaining investors. ETFs, on the other hand, are traded intra-day and liquidity is provided by market makers,

also called authorized participants.

ETFs generally are a more tax efficient investment vehicle than mutual funds due to the internal operating mechanics. When a

mutual fund changes the composition of its portfolio, buying and selling stocks, it engages in cash transactions. These cash

transactions can result in short and/or long-term capital gains. These gains are distributed annually to mutual fund

shareholders. Shareholders generally have no way to anticipate when the mutual fund will realize capital gains or control

whether the gains are short or long-term. When evaluating a mutual fund for prospective investment, it is almost impossible

to determine the amount of unrealized gains in the fund and when they could be realized. In addition to annually distributed

gains, mutual fund shareholders also are liable for capital gains taxes when they sell shares of the fund itself. There are two

layers of taxes on most mutual fund investments.

An ETF, by contrast, modifies its portfolio by making what are known as in-kind transactions. On an ongoing basis, an ETF

exchanges units in the fund with authorized participants for the basket of stocks comprising the fund’s holdings. When an

7

Smart Beta 2.0: A Disruptive Innovation

ETF’s holdings change, for example at an index rebalancing, the ETF simply receives a basket of stocks reflecting the new

index holdings from the authorized participant and exchanges units of the fund. In this way, where the ETF does not engage

in cash transactions for securities, there is generally no tax liability generated within an ETF. ETF investors are liable for

capital gains taxes when they sell the fund, but they can control whether the gain is short-term or long-term by their decision

when to sell. Because ETFs do not distribute gains annually, ETF investors sidestep one layer of taxation, and this is why ETFs

are typically more tax efficient for taxable investors.

One of the most underappreciated facts of mutual fund investing—especially six years into a bull market—is that, unless a

mutual fund is brand new (or the NAV has been declining for some time), investors are buying into a portfolio that likely has

embedded unrealized gains. For ETFs, this is generally not a concern. The operating mechanics of ETFs are such that they

don’t generate taxes at the fund level, so there are no embedded unrealized gains to worry about. ETFs are a superior

investment vehicle in taxable accounts because they sidestep one layer of taxation and allow an investor to decide when and

what type of capital gain to incur.

Six years into an equity bull market, this complete absence of embedded gains makes it a very opportune time for an investor

to consider the merits of an ETF to achieve equity exposure. Once investors make the switch from mutual funds to ETFs for

core equity exposure, they will never have to worry about buying or receiving distributed capital gains again. This is partly

why Goldman Sachs is expecting ETF assets to double over the next five years (http://www.etftrends.com/2015/06/etfs-3-

trillion-is-nice-but-6-trillion-is-better/).

This is one of the key reasons why investors may want to consider using ETFs instead of mutual funds whenever possible. By

filling up the lower and middle sections of the barbell with benchmark index ETFs, investors will find themselves having

lowered overall fees significantly per basis point of alpha, and they will have fee budget left over to choose a few strategic,

high active share mutual funds and/or ETFs that bring unique attributes to a portfolio (attributes that are not available in any

benchmark index ETF).

How to Use Smart Beta Funds in a Portfolio

As described earlier, some smart beta index-based ETFs, depending on the construction methodology, have a very high active

share. Some smart beta index-based ETFs offer a fusion of the rules-based, lower-fee benefit of index investing with the

outperformance associated with higher active share strategies. A high active share should be a prerequisite for any smart

beta strategy under consideration, as it has been linked to outperformance relative to a benchmark before and after fees. We

offer an example in the Gavekal Knowledge Leaders Indexes.

Data as of August 31, 2015. Source: Gavekal Capital.

High active strategies, like those of our smart beta indexes, are ideal for use in the barbell alongside passive index ETFs which

keep fees low. Both of the above indexes have an active share in excess of 70%, making them highly active strategies. The

proprietary selection methodology and an equal weighting scheme create that difference from the benchmark. The Gavekal

Knowledge Leaders Developed World and Emerging Markets Indexes are equal-weighted and rebalance twice a year, in April

and October. Both of the indexes are diversified indexes, meaning there is no industry concentration greater than 25%. This

Index Active Share Tracking Error Benchmark

Gavekal Knowledge Leaders Developed World Index 72% 4.0% MSCI World Index

Gavekal Knowledge Leaders Emerging Markets Index 85% 6.9% MSCI Emerging Markets Index

8

Smart Beta 2.0: A Disruptive Innovation

is an important point since many smart beta indexes—especially many of the new smart beta indexes representing solar,

robotics or genomics—are concentrated indexes, with most of the holdings falling in just one or a couple of industries.

Diversified indexes are appropriate for the implementation of core portfolio allocations, while concentrated indexes are more

appropriate as satellite assets. As such, both of the Gavekal Knowledge Leaders Indexes are designed to be used in core

portfolio allocations to the developed and emerging markets. For more information on how we construct the Gavekal

Knowledge Leaders Indexes and how they performed over 10 and 15 years, see our white paper, “The Knowledge Leader

Indexes: Capturing Abnormal Returns of Highly Innovative Companies.”

Smart Beta Comparative Analysis

Now let’s bring together our smart beta indexes and actively managed funds in a comparative analysis. First, it’s important

to set up a few analysis guidelines. In order to ensure that any comparisons we make are based on valid, apples-to-apples

observations, we make a few simple adjustments.

1. For the Gavekal Knowledge Leaders Developed World Index, we deducted a fee of 75bps, which represents the

average fee for actively managed funds in Morningstar’s World Stock category minus 25bps.

2. For the Gavekal Knowledge Leaders Emerging Markets Index, we deducted a fee of 95bps, which represents the

average fee for actively managed funds in Morningstar’s Diversified Emerging Markets equity category minus

25bps.

3. We only will consider actively managed mutual funds that have at least a 10 year history. For actively managed

mutual funds, we used the fee stated in the prospectus.

4. We will use the MSCI All Country World Index as our benchmark. The MSCI ACWI is the most comprehensive

single global equity benchmark for investors representing over 85% of the investable worldwide universe of stocks.

To carry on our fee adjustment to indexes, we will adjust the performance of the MSCI All Country World Index by

33bps, which is the actual fee of the iShares ACWI ETF.

Now we have a 10 year history of our smart beta indexes, actively managed mutual funds and a benchmark index, that are all

adjusted for fees. This data treatment gives us a set of standardized data on all assets with which to make comparisons.

Analysis of Gavekal Knowledge Leaders Developed World Index Results vs. World Stock Mutual

Funds

Investors can learn a lot about how a smart beta index can contribute to overall results by comparing it actively mutual funds.

We evaluate how the fee-adjusted Gavekal Knowledge Leaders Developed World Index stacks up when compared to every

mutual fund in the Morningstar World Stock category with a 10 year history, using low-cost I and Y shares.

1. Performance: The Gavekal Knowledge Leaders Developed World Index comes in second out of 39 funds for

cumulative 10 year performance, recording a 120% cumulative gain, or 8.2% per year.

2. Volatility: The Gavekal Knowledge Leaders Developed World Index has one of the lowest standard deviations

among all 39 funds. Only three funds have a lower standard deviation.

3. Alpha: The Gavekal Knowledge Leaders Developed World Index generated an annualized 3.2% alpha over the last

10 years, second out of 39 funds.

9

Smart Beta 2.0: A Disruptive Innovation

4. Correlation: With a 97.4% correlation to the MSCI World benchmark index, the Gavekal Knowledge Leaders

Developed World Index has among the highest correlation of all funds.

5. Risk-Adjusted Performance: The Gavekal Knowledge Leaders Developed World Index generated the fourth highest

Sharpe Ratio of all 39 funds and the fourth highest Treynor Ratio of all 39 funds.

Data as of August 31, 2015. Sorted by Performance (10 Years – Annualized).

Source: Gavekal Capital, Factset; Monthly data; Index Publisher: Solactive

An investor cannot invest directly in an index.

Analysis of Gavekal Knowledge Leaders Emerging Markets Index Results vs. Diversified Emerging

Markets Mutual Funds

Next we look at how the fee-adjusted Gavekal Knowledge Leaders Emerging Markets Index compares to all Morningstar

Diversified Emerging Markets category mutual funds with 10-year data available, using I and Y shares only.

1. Performance: The Gavekal Knowledge Leaders Emerging Markets Index comes in first out of 32 funds for

cumulative 10 year performance, recording a 185.1% cumulative gain, or 11% per year.

2. Volatility: At 21.6%, the Gavekal Knowledge Leaders Emerging Markets Index has the lowest standard deviations

among all 32 funds.

Performance

Name

Actual/Imputed

Fee

Performance -

10 Years

Annualized

Performance -

10 Years

Cumulative

Standard

Deviation Beta Alpha

Treynor

Ratio Correlation

Sharpe

Ratio

Morgan Stanley Institutional Funds, Global Franchise Ptf Cl I 0.97% 8.7% 129.8% 13.6% 0.72 5.1% 11.85 88.8% 0.63

Gavekal Knowledge Leaders Developed World Index (TR) 0.75% 8.2% 120.0% 15.0% 0.87 3.6% 9.27 97.4% 0.54

Oppenheimer Global Opportunities Fund Class Y 0.92% 8.0% 116.9% 20.2% 1.06 2.8% 7.46 87.8% 0.39

MFS Global Equity Fund - Class I 0.98% 7.9% 113.9% 16.0% 0.93 3.3% 8.34 97.4% 0.49

Hartford Global Capital Appreciation Fund Class Y 0.83% 7.8% 112.2% 17.8% 1.03 2.7% 7.44 96.9% 0.43

BlackRock Glbl Sm Cap I 1.03% 7.5% 106.6% 17.8% 1.01 2.5% 7.31 95.3% 0.42

WFA Global Opportunities Fund Admin Class 1.40% 7.5% 106.0% 18.7% 1.06 2.2% 6.97 94.8% 0.40

American Century Global Growth - Institutional Class 0.88% 7.2% 99.6% 16.9% 0.98 2.3% 7.19 96.9% 0.42

AllianzGI Global Small Cap Fund Class Institutional 1.26% 7.1% 99.1% 20.4% 1.16 1.4% 6.04 95.1% 0.34

Mutual Global Discovery Fund Class Z 0.96% 7.1% 98.5% 11.0% 0.60 4.1% 11.56 91.9% 0.64

VY Oppenheimer Global Portfolio Initial 0.75% 7.0% 96.8% 17.7% 1.04 1.8% 6.64 97.8% 0.39

Oppenheimer Global Fund Class Y 0.89% 6.8% 93.1% 17.8% 1.04 1.6% 6.43 97.8% 0.38

Dreyfus Worldwide Growth Fund Class I 0.91% 6.5% 86.9% 14.4% 0.81 2.4% 7.84 93.9% 0.44

MassMutual Premier Global Fund Service Class 1.03% 6.4% 86.1% 17.7% 1.03 1.3% 6.09 97.7% 0.36

MFS Series Trust VIII, MFS Global Growth Fd Cl I 1.20% 6.3% 83.7% 16.8% 0.99 1.4% 6.22 98.5% 0.37

MFS Aggressive Growth Allocation Fund - Class I 0.13% 6.2% 82.1% 15.9% 0.94 1.5% 6.47 98.2% 0.38

Dimensional Investment Grp Global Eq Portf Cl I 0.31% 6.2% 81.9% 17.6% 1.04 1.0% 5.84 98.2% 0.34

Mutual Quest Fund Class Z 0.77% 6.0% 78.5% 10.0% 0.55 3.2% 10.67 91.4% 0.58

Oppenheimer Portfolio Series: Equity Investor Fund Cl Y 0.23% 5.9% 78.1% 17.0% 1.00 1.0% 5.85 98.1% 0.34

Hartford Global Growth HLS Fund, Class IA 0.81% 5.9% 76.7% 19.5% 1.12 0.3% 5.13 95.8% 0.29

Cohen & Steers Global Infrastructure Fund Inc Class I 1.10% 5.8% 75.3% 14.7% 0.75 2.0% 7.52 85.6% 0.39

Hartford Global Growth HLS Fund Class IB 1.06% 5.6% 72.3% 19.5% 1.12 0.0% 4.89 95.8% 0.28

Janus Aspen Global Research Portfolio Institutional Shs 0.61% 5.5% 70.4% 17.8% 1.01 0.4% 5.29 95.3% 0.30

Putnam Global Equity Fund Class Y 1.02% 5.3% 66.9% 18.3% 1.07 -0.1% 4.78 97.8% 0.28

AB Global Thematic Growth Fund, Inc. - Class I 0.96% 4.9% 61.4% 20.8% 1.15 -0.8% 4.14 92.5% 0.23

Fidelity Advisor Global Capital Appreciation Fund: Class I 1.20% 4.9% 60.7% 18.9% 1.08 -0.5% 4.40 95.1% 0.25

Goldman Sachs Trust Equity Growth Strategy Portfolio Institutional Sh 0.20% 4.7% 58.9% 17.2% 1.02 -0.3% 4.52 99.1% 0.27

Delaware Global Value Fund Class I 1.30% 4.3% 52.4% 17.9% 1.04 -0.9% 4.03 97.0% 0.23

The AB Portfolios - AB Wealth Appreciation Strategy - Class I 0.79% 4.1% 49.9% 17.2% 1.02 -0.9% 3.95 98.5% 0.23

Aberdeen Global Equity Fund Institutional Class 1.19% 4.1% 49.5% 18.6% 1.01 -0.9% 3.93 90.8% 0.21

UBS Global Sustainable Equity Fund Class P 1.00% 4.0% 48.6% 19.1% 1.11 -1.5% 3.54 97.3% 0.21

Aberdeen Global Equity Fund Insti Service Class 1.19% 3.6% 42.1% 21.2% 0.66 0.3% 5.26 51.7% 0.16

QS Batterymarch Global Equity Fund I 1.14% 3.5% 40.8% 16.9% 0.95 -1.2% 3.55 93.8% 0.20

Deutsche World Dividend Fund Institutional Class 0.95% 3.3% 38.4% 18.3% 1.04 -1.9% 3.06 95.2% 0.17

Ivy Cundill Global Value Fund Class Y 1.38% 3.3% 38.4% 16.0% 0.85 -0.9% 3.74 88.8% 0.20

Third Avenue Value Fund Insti Class 1.07% 2.7% 31.1% 19.3% 1.08 -2.6% 2.44 93.1% 0.14

ClearBridge Global Growth Trust Cl I 0.90% 2.4% 27.1% 19.6% 1.09 -3.0% 2.12 92.6% 0.12

Alpine Dynamic Dividend Fund 1.35% 1.2% 12.8% 17.3% 0.99 -3.7% 1.11 95.2% 0.06

Deutsche Global Equity Fund Institutional Class 1.22% -2.5% -22.3% 23.5% 1.03 -7.6% (2.54) 73.1% (0.11)

Risk Stats (Relative to MSCI ACWI)

Comparisons Relative to All World Stock Mutual Funds (I & Y Share Classes) with 10 Year Track Record

10

Smart Beta 2.0: A Disruptive Innovation

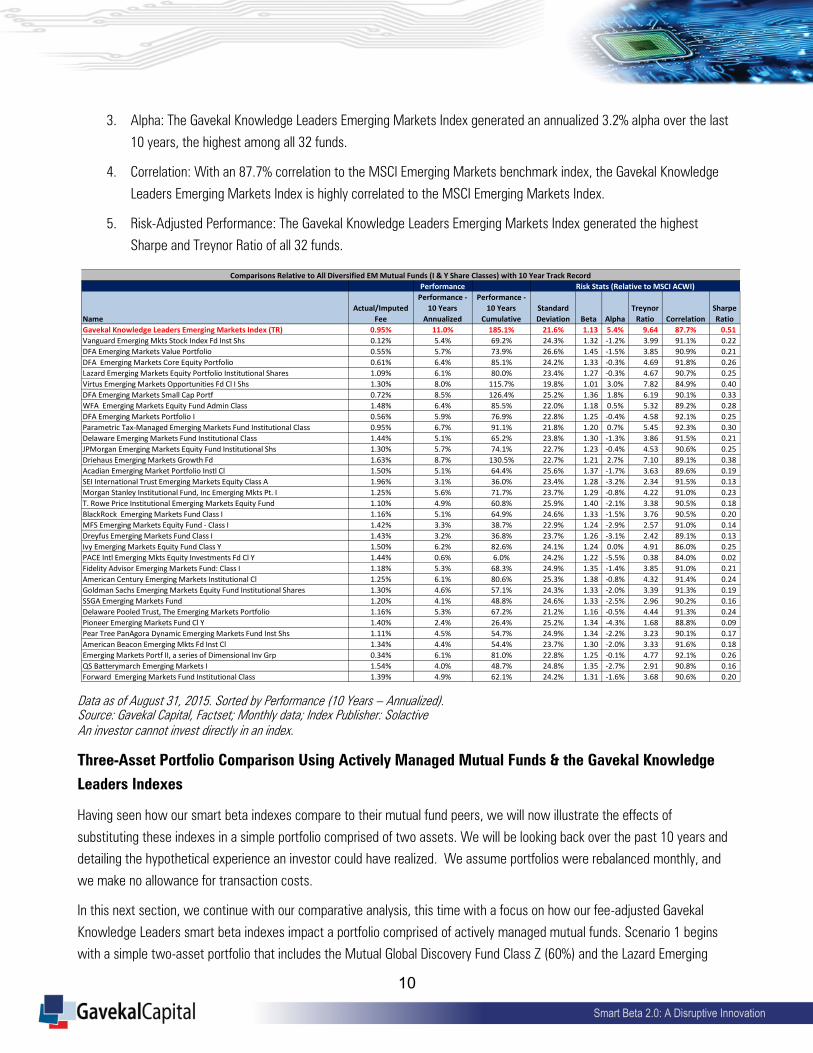

3. Alpha: The Gavekal Knowledge Leaders Emerging Markets Index generated an annualized 3.2% alpha over the last

10 years, the highest among all 32 funds.

4. Correlation: With an 87.7% correlation to the MSCI Emerging Markets benchmark index, the Gavekal Knowledge

Leaders Emerging Markets Index is highly correlated to the MSCI Emerging Markets Index.

5. Risk-Adjusted Performance: The Gavekal Knowledge Leaders Emerging Markets Index generated the highest

Sharpe and Treynor Ratio of all 32 funds.

Data as of August 31, 2015. Sorted by Performance (10 Years – Annualized).

Source: Gavekal Capital, Factset; Monthly data; Index Publisher: Solactive

An investor cannot invest directly in an index.

Three-Asset Portfolio Comparison Using Actively Managed Mutual Funds & the Gavekal Knowledge

Leaders Indexes

Having seen how our smart beta indexes compare to their mutual fund peers, we will now illustrate the effects of

substituting these indexes in a simple portfolio comprised of two assets. We will be looking back over the past 10 years and

detailing the hypothetical experience an investor could have realized. We assume portfolios were rebalanced monthly, and

we make no allowance for transaction costs.

In this next section, we continue with our comparative analysis, this time with a focus on how our fee-adjusted Gavekal

Knowledge Leaders smart beta indexes impact a portfolio comprised of actively managed mutual funds. Scenario 1 begins

with a simple two-asset portfolio that includes the Mutual Global Discovery Fund Class Z (60%) and the Lazard Emerging

Performance

Name

Actual/Imputed

Fee

Performance -

10 Years

Annualized

Performance -

10 Years

Cumulative

Standard

Deviation Beta Alpha

Treynor

Ratio Correlation

Sharpe

Ratio

Gavekal Knowledge Leaders Emerging Markets Index (TR) 0.95% 11.0% 185.1% 21.6% 1.13 5.4% 9.64 87.7% 0.51

Vanguard Emerging Mkts Stock Index Fd Inst Shs 0.12% 5.4% 69.2% 24.3% 1.32 -1.2% 3.99 91.1% 0.22

DFA Emerging Markets Value Portfolio 0.55% 5.7% 73.9% 26.6% 1.45 -1.5% 3.85 90.9% 0.21

DFA Emerging Markets Core Equity Portfolio 0.61% 6.4% 85.1% 24.2% 1.33 -0.3% 4.69 91.8% 0.26

Lazard Emerging Markets Equity Portfolio Institutional Shares 1.09% 6.1% 80.0% 23.4% 1.27 -0.3% 4.67 90.7% 0.25

Virtus Emerging Markets Opportunities Fd Cl I Shs 1.30% 8.0% 115.7% 19.8% 1.01 3.0% 7.82 84.9% 0.40

DFA Emerging Markets Small Cap Portf 0.72% 8.5% 126.4% 25.2% 1.36 1.8% 6.19 90.1% 0.33

WFA Emerging Markets Equity Fund Admin Class 1.48% 6.4% 85.5% 22.0% 1.18 0.5% 5.32 89.2% 0.28

DFA Emerging Markets Portfolio I 0.56% 5.9% 76.9% 22.8% 1.25 -0.4% 4.58 92.1% 0.25

Parametric Tax-Managed Emerging Markets Fund Institutional Class 0.95% 6.7% 91.1% 21.8% 1.20 0.7% 5.45 92.3% 0.30

Delaware Emerging Markets Fund Institutional Class 1.44% 5.1% 65.2% 23.8% 1.30 -1.3% 3.86 91.5% 0.21

JPMorgan Emerging Markets Equity Fund Institutional Shs 1.30% 5.7% 74.1% 22.7% 1.23 -0.4% 4.53 90.6% 0.25

Driehaus Emerging Markets Growth Fd 1.63% 8.7% 130.5% 22.7% 1.21 2.7% 7.10 89.1% 0.38

Acadian Emerging Market Portfolio Instl Cl 1.50% 5.1% 64.4% 25.6% 1.37 -1.7% 3.63 89.6% 0.19

SEI International Trust Emerging Markets Equity Class A 1.96% 3.1% 36.0% 23.4% 1.28 -3.2% 2.34 91.5% 0.13

Morgan Stanley Institutional Fund, Inc Emerging Mkts Pt. I 1.25% 5.6% 71.7% 23.7% 1.29 -0.8% 4.22 91.0% 0.23

T. Rowe Price Institutional Emerging Markets Equity Fund 1.10% 4.9% 60.8% 25.9% 1.40 -2.1% 3.38 90.5% 0.18

BlackRock Emerging Markets Fund Class I 1.16% 5.1% 64.9% 24.6% 1.33 -1.5% 3.76 90.5% 0.20

MFS Emerging Markets Equity Fund - Class I 1.42% 3.3% 38.7% 22.9% 1.24 -2.9% 2.57 91.0% 0.14

Dreyfus Emerging Markets Fund Class I 1.43% 3.2% 36.8% 23.7% 1.26 -3.1% 2.42 89.1% 0.13

Ivy Emerging Markets Equity Fund Class Y 1.50% 6.2% 82.6% 24.1% 1.24 0.0% 4.91 86.0% 0.25

PACE Intl Emerging Mkts Equity Investments Fd Cl Y 1.44% 0.6% 6.0% 24.2% 1.22 -5.5% 0.38 84.0% 0.02

Fidelity Advisor Emerging Markets Fund: Class I 1.18% 5.3% 68.3% 24.9% 1.35 -1.4% 3.85 91.0% 0.21

American Century Emerging Markets Institutional Cl 1.25% 6.1% 80.6% 25.3% 1.38 -0.8% 4.32 91.4% 0.24

Goldman Sachs Emerging Markets Equity Fund Institutional Shares 1.30% 4.6% 57.1% 24.3% 1.33 -2.0% 3.39 91.3% 0.19

SSGA Emerging Markets Fund 1.20% 4.1% 48.8% 24.6% 1.33 -2.5% 2.96 90.2% 0.16

Delaware Pooled Trust, The Emerging Markets Portfolio 1.16% 5.3% 67.2% 21.2% 1.16 -0.5% 4.44 91.3% 0.24

Pioneer Emerging Markets Fund Cl Y 1.40% 2.4% 26.4% 25.2% 1.34 -4.3% 1.68 88.8% 0.09

Pear Tree PanAgora Dynamic Emerging Markets Fund Inst Shs 1.11% 4.5% 54.7% 24.9% 1.34 -2.2% 3.23 90.1% 0.17

American Beacon Emerging Mkts Fd Inst Cl 1.34% 4.4% 54.4% 23.7% 1.30 -2.0% 3.33 91.6% 0.18

Emerging Markets Portf II, a series of Dimensional Inv Grp 0.34% 6.1% 81.0% 22.8% 1.25 -0.1% 4.77 92.1% 0.26

QS Batterymarch Emerging Markets I 1.54% 4.0% 48.7% 24.8% 1.35 -2.7% 2.91 90.8% 0.16

Forward Emerging Markets Fund Institutional Class 1.39% 4.9% 62.1% 24.2% 1.31 -1.6% 3.68 90.6% 0.20

Risk Stats (Relative to MSCI ACWI)

Comparisons Relative to All Diversified EM Mutual Funds (I & Y Share Classes) with 10 Year Track Record

11

Smart Beta 2.0: A Disruptive Innovation

Markets Equity Portfolio Institutional Shares (40%). Each fund is the largest actively managed fund by AUM with a 10-year

track record in its respective category.

Analysis of this baseline portfolio versus the MSCI ACWI benchmark reveals how actively managed funds can offer

benchmark beating performance. The 80/20 portfolio of the actively managed funds generated 1.3% per year better results,

after fees.

Data as of August 31, 2015.

MSCI ACWI Index adjusted by 33bps

Source: Gavekal Capital, Factset; Monthly data

In scenario 2, we replace only the Mutual Global Discovery Fund Class Z that was in the starting portfolio with the Gavekal

Knowledge Leaders Developed World Index, maintaining the 80/20 regional weighting scheme as we have in every other

case.

The effect of this substitution is a hypothetical portfolio that generates better returns than the benchmark, with a slightly

higher correlation and a lower fee. In this scenario performance is 2.1% per year better than the MSCI ACWI benchmark

after fees.

Data as of August 31, 2015.

MSCI ACWI Index adjusted by 33bps

Source: Gavekal Capital, Factset; Monthly data; Index Publisher: Solactive

An investor cannot invest directly in an index.

Holding Weight Assumed Fee

Mutual Global Discovery Fund Class Z 80% 0.98%

Lazard Emerging Markets Equity Portfolio Institutional Shares 20% 1.09%

Scenario 1 Portfolio Holdings

Total Return

Annualized

Cumulative

Return Correlation

Portfolio

Fee

MSCI ACWI (fee adjusted) 5.8% 75.7% 100.0% 0.33%

Scenario 1 Portfolio 7.1% 98.9% 95.2% 1.00%

Scenario 1 Portfolio Results - 10-Years Annualized - Monthly Rebalancing

Annualized Return & Risk Stats Relative to MSCI ACWI Index

Holding Weight Assumed Fee

Gavekal Knowledge Leaders Developed World Index (TR) 80% 0.75%

Lazard Emerging Markets Equity Portfolio Institutional Shares 20% 1.09%

Scenario 2 Portfolio Holdings

Total Return

Annualized

Cumulative

Return Correlation

Portfolio

Fee

MSCI ACWI (fee adjusted) 5.8% 75.7% 100.0% 0.33%

Scenario 2 Portfolio 7.9% 114.2% 96.4% 0.82%

Annualized Return & Risk Stats Relative to MSCI ACWI Index

Scenario 2 Portfolio Results - 10-Years Annualized - Monthly Rebalancing

12

Smart Beta 2.0: A Disruptive Innovation

Next, we swap out the Lazard Emerging Markets Equity Portfolio Institutional Shares and integrate the Gavekal Knowledge

Leaders Emerging Markets Index into the mix.

The effects of changing this one variable are fairly dramatic. The return of this portfolio is 2.3% higher than the MSCI ACWI

after fees.

Data as of August 31, 2015.

MSCI ACWI Index adjusted by 33bps

Source: Gavekal Capital, Factset; Monthly data; Index Publisher: Solactive

An investor cannot invest directly in an index.

In our final scenario, we examine the performance of a portfolio that includes both of the fee-adjusted Gavekal Knowledge

Leaders Indexes.

Relative to the MSCI ACWI performance is 3.1% per year better after fees.

Data as of August 31, 2015.

MSCI ACWI Index adjusted by 33bps

Source: Gavekal Capital, Factset; Monthly data; Index Publisher: Solactive

An investor cannot invest directly in an index.

Conclusion

As Moody’s suggests, there is a new battlefront in the money management business. New smart beta ETFs, so-called Smart

Beta 2.0 ETFs, are entering the market to compete against actively managed mutual funds. These funds will be formidable

competition for many actively managed mutual funds for a variety of reasons. In general, smart beta ETFs offer lower fees

than actively managed mutual funds, both directly via lower expense ratios, but also indirectly via the elimination of annually

Holding Weight Assumed Fee

Mutual Global Discovery Fund Class Z 80% 0.98%

Gavekal Knowledge Leaders Emerging Markets Index (TR) 20% 0.95%

Scenario 3 Portfolio Holdings

Total Return

Annualized

Cumulative

Return Correlation

Portfolio

Fee

MSCI ACWI (fee adjusted) 5.8% 75.7% 100.0% 0.33%

Scenario 3 Portfolio 8.1% 117.2% 95.1% 0.97%

Scenario 3 Portfolio Results - 10-Years Annualized - Monthly Rebalancing

Annualized Return & Risk Stats Relative to MSCI ACWI Index

Holding Weight Assumed Fee

Gavekal Knowledge Leaders Developed World Index (TR) 80% 0.75%

Gavekal Knowledge Leaders Emerging Markets Index (TR) 20% 0.95%

Scenario 4 Portfolio Holdings

Total Return

Annualized

Cumulative

Return Correlation

Portfolio

Fee

MSCI ACWI (fee adjusted) 5.8% 75.7% 100.0% 0.33%

Scenario 4 Portfolio 8.9% 134.2% 96.0% 0.79%

Scenario 4 Portfolio Results - 10-Years Annualized - Monthly Rebalancing

Annualized Return & Risk Stats Relative to MSCI ACWI Index

13

Smart Beta 2.0: A Disruptive Innovation

distributed capital gains. They offer improved trading liquidity and transparency compared to actively managed mutual funds.

And, smart beta indexes offer the possibility of superior performance, traditionally the province only of actively managed

funds.

On July 8, 2015, we launched two smart beta ETFs that follow the Gavekal Knowledge Leaders Developed World Index and

the Gavekal Knowledge Leaders Emerging Markets Index to compete directly with actively managed mutual funds. We

believe our smart beta ETFs offer investors a more efficient way to establish a core equity position in developed world and

emerging markets equities than traditional actively managed mutual funds.

The asset management battleground is taking shape, and while the winners won’t be known for years, we can confidently

predict investors will be the ultimate winner. In every disruptive innovation we have studied, from the telephone to the

internet, the consumer is the ultimate beneficiary. We have entered the smart beta marketplace to be a force of disruptive

innovation and help investors achieve their investment goals more efficiently. Smart beta 2.0 is here. Let the disruptive

innovation begin.

For more information about our investment products please click here.

We hope you find the content of this white paper useful. Please send questions, comments or feedback to

14

Smart Beta 2.0: A Disruptive Innovation

Sources

Agather, Rolf. “Smart Beta Indexes.” Journal of Indexes Europe: ‘Smart’ Beta Rising, December 2013.

Cremers, Martijn and Antti Petajisto. “How Active Is Your Fund Manager? A New Measure That Predicts Performance.”

Working Paper, August 2006. Last revised May 2009.

ETF.com. The Definitive Smart Beta ETF Guide. May 2015.

ETF Securities. ETPedia.

Invesco. Smart Beta ETF Strategies

Moody’s Investors Service. “Smart Beta 2.0: The Next Battleground for Asset Management Dollars Heats Up.” Sector

Comment. 10 September 2015.

Petajisto, Antti. “Active Share and Mutual Fund Performance.” Working Paper, January 2013.

Rekenthaler, John. “Indexes Can Be Passive, Active Can Be Indexes, but Passive Can’t Be Indexes.” Morningstar.com.

September 25, 2015.

Schriber, Todd. “ETFs: $3 Trillion is Nice, but $6 Trillion is Better.” ETFTrends.com. June 8, 2015.

Vanguard. What are the five ETF structures?

Definitions

Active Share is the percentage of stock holdings in a portfolio that differ from the benchmark index. Active Share determines

the extent of active management being employed by mutual fund managers: the higher the Active Share, the more likely a

fund is to outperform the benchmark index. Researchers in a 2006 Yale School of Management study determined that funds

with a higher Active Share will tend to be more consistent in generating high returns against the benchmark indexes.

Alpha is a measure of the portfolio’s risk adjusted performance. When compared to the portfolio’s beta, a positive alpha

indicates better-than-expected portfolio performance and a negative alpha worse-than-expected portfolio performance.

Beta is a measure of the funds sensitivity to market movements. A portfolio with a beta greater than 1 is more volatile than

the market and a portfolio with a beta less than 1 is less volatile than the market.

Correlation is the extent to which the returns of different types of investments move in tandem with one another in response

to changing economic and market conditions. Correlation is measured on a scale of -1 (negatively correlated) to +1

(completely correlated). Low correlation or negative correlation to traditional stocks and bonds may help reduce risk in a

portfolio and provide downside protection.

Upside/Downside Capture Ratio is used to show the relationship between the volumes of advancing and declining issues.

Information Ratio is a ratio of portfolio returns above the returns of a benchmark to the volatility of those returns.

Max Drawdown is the maximum single period loss incurred over the interval being measured.

The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity

15

Smart Beta 2.0: A Disruptive Innovation

market performance of developed markets.

Risk-adjusted Return is a concept that refines an investments return by measuring how much risk is involved in producing

that return.

Sharpe Ratio uses a fund’s standard deviation and its excess return (the difference between the fund’s return and the risk-

free return of 90-day Treasury Bills) to determine reward per unit of risk.

Standard deviation is a calculation used to measure variability of a portfolio’s performance.

Tracking Error is a measure of how closely a portfolio follows the index to which it is benchmarked.

Treynor Ratio is a risk-adjusted measure of return based on systematic risk. It is similar to the Sharpe ratio, with the

difference being that the Treynor ratio uses beta as the measurement of volatility.

Volatility is a statistical measure of the dispersion of returns for a given security or market index.

An investor cannot invest directly in an index.

Disclaimer

This document does not constitute an offer of services in jurisdictions where Gavekal Capital, LLC is not authorized to conduct

business. All information provided herein by Gavekal Capital is impersonal and not tailored to the needs of any person, entity

or group of persons. Past performance of an index is not a guarantee of future results. It is not possible to invest

directly in an index. Exposure to an asset class represented by an index is available through investable instruments based

on that index. Gavekal Capital makes no assurance that investment products based on the index will accurately track index

performance or provide positive investment returns. A decision to invest in any such investment fund or other investment

vehicle should not be made in reliance on any of the statements set forth in this document. Prospective investors are advised

to make an investment in any such fund or other vehicle only after carefully considering the risks associated with investing in

such funds, as detailed in an offering memorandum or similar document that is prepared by or on behalf of the issuer of the

investment fund or other vehicle. Inclusion of a security within an index is not a recommendation by Gavekal Capital to buy,

sell or hold such a security, nor is it considered to be investment advice. Closing prices for the Gavekal Knowledge Leaders

Indexes are calculated by Solactive AG based on the closing price of the individual constituents of the index as set by their

primary exchange.

Results from Gavekal Capital Optimization Tool may vary with each use and over time.

The entire equity mutual fund and ETF universes are considered in the analysis. The tool uses historic data from FactSet and

Morningstar to optimize allocation and calculate the impact of substituted mutual funds and ETFs. Where appropriate, the

tool will substitute Gavekal Knowledge Leaders Strategy products in its calculations to test for potential portfolio impact.

Other investments not considered may have characteristics similar or superior to those being analyzed.

IMPORTANT: The projections or other information generated by Gavekal Capital Optimization Tool regarding the likelihood of

various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of

future results. These materials have been prepared solely for informational purposes based upon information generally

available to the public from sources believed to be reliable. No content contained in these materials (including index data,

16

Smart Beta 2.0: A Disruptive Innovation

ratings, credit-related analyses and data, model, software or other application or output therefrom) or any part there of

(Content) may be modified, reverse-engineered, reproduced or distributed in any form by any means, or stored in a database

or retrieval system, without the prior written permission of Gavekal Capital. The Content shall not be used for any unlawful or

unauthorized purposes. Gavekal Capital and its third-party data providers and licensors do not guarantee the accuracy,

completeness, timeliness or availability of the Content. Gavekal Capital Parties are not responsible for any errors or omissions,

regardless of the cause, for the results obtained from the use of the Content. Content is provided on an “as is” basis.

The Gavekal Knowledge Leaders Developed World Index and the Gavekal Knowledge Leaders Emerging Markets Index

(Indexes) claim to be the longest running, real time test of the innovation leaders. This claim was determined via an internal

search of all indexes offered by the following list of index providers, which we believe to be comprehensive: S&P Dow Jones

Indices, MSCI, FTSE, FTSE/TMX Canada, Solactive, Research Affiliates, NASDAQ OMB Global Indices, Morningstar, Russell

Investments, Auspice eBeta Enhanced Indices, BNY Mellon Indices, CME Group/Dow Jones, Barclays Capital Indices, Zacks

Investment Research, Alphashares, Cohen & Steers and Sustainable Wealth Management. None of these providers offer

indexes compiling global innovation leader stocks nor do they offer indexes that have a quantitative process to measure a

company’s innovation. Gavekal will continue to monitor the above mentioned landscape with the goal of provide accurate and

non-misleading information.

The Indexes are calculated and published by Solactive AG. Solactive AG uses its best efforts to ensure that the Indexes are

calculated correctly. Irrespective of its obligations towards Gavekal Capital, Solactive AG has no obligation to point out errors

in the Indexes to third parties including but not limited to investors and/or financial intermediaries of the financial instrument.

Neither publication of the Indexes by Solactive AG nor the licensing of the Indexes or Indexes trademark for the purpose of

use in connection with the financial instrument constitutes a recommendation by Solactive AG to invest capital in said

financial instrument nor does it in any way represent an assurance or opinion of Solactive AG with regard to any investment

in any financial instrument.

For full information including any named holdings that may have been mentioned in the document as well as additional

policies and full disclosures on the Advisor, please visit our website gavekalcapital.com.

Top Related