Languages

Pages

Legal

Second Quarter 2014 ReviewAugust 14, 2014

2

Cautionary StatementsThis presentation contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of

the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements, other than statements of historical fact included in this presentation, regarding Eclipse

Resources’ strategy, future operations, financial position, estimated revenues and income/losses, projected costs and capital expenditures, prospects, plans and objectives of

management are forward-looking statements. When used in this presentation, the words “will,” “would,” “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,”

“project” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These

forward-looking statements are based on Eclipse Resources’ current expectations and assumptions about future events and are based on currently available information as to the

outcome and timing of future events. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements described under

the heading “Risk Factors” in Eclipse Resources’ final prospectus dated June 19, 2014 and filed with the Securities Exchange Commission pursuant to Rule 424(b) of the

Securities Act on June 23, 2014 (the “IPO Prospectus”), and in “Item 1A. Risk Factors” of Eclipse Resources’ Quarterly Report on Form 10-Q.

Forward-looking statements may include statements about Eclipse Resources’ business strategy; reserves; general economic conditions; financial strategy, liquidity and capital

required for developing its properties and timing related thereto; realized natural gas, NGLs and oil prices; timing and amount of future production of natural gas, NGLs and oil;

its hedging strategy and results; future drilling plans; competition and government regulations, including those related to hydraulic fracturing; the anticipated benefits under its

commercial agreements; pending legal matters relating to its leases; marketing of natural gas, NGLs and oil; leasehold and business acquisitions; the costs, terms and

availability of gathering, processing, fractionation and other midstream services; general economic conditions; credit markets; uncertainty regarding its future operating results,

including initial production rates and liquid yields in its type curve areas; and plans, objectives, expectations and intentions contained in this presentation that are not historical.

Eclipse Resources cautions you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which

are beyond its control, incident to the exploration for and development, production, gathering and sale of natural gas, NGLs and oil. These risks include, but are not limited to;

legal and environmental risks, drilling and other operating risks, regulatory changes, commodity price volatility, inflation, lack of availability of drilling, production and

processing equipment and services, counterparty credit risk, the uncertainty inherent in estimating natural gas, NGLs and oil reserves and in projecting future rates of

production, cash flow and access to capital, the timing of development expenditures, and the other risks described under the heading “Item 1A. Risk Factors” in Eclipse

Resources’ Final Prospectus of Form S-1 and in “Item 1A. Risk Factors” of this the Company’s Quarterly Report on Form 10-Q.

Reserve engineering is a process of estimating underground accumulations of natural gas, NGLs and oil that cannot be measured in an exact way. The accuracy of any reserve

estimate depends on the quality of available data, the interpretation of such data and price and cost assumptions made by reserve engineers. In addition, the results of drilling,

testing and production activities may justify revisions of estimates that were made previously. If significant, such revisions could change the schedule of any further production

and development drilling. Accordingly, reserve estimates may differ significantly from the quantities of natural gas, NGLs and oil that are ultimately recovered.

Should one or more of the risks or uncertainties described in Eclipse Resources’ Quarterly Report on Form 10-Q occur, or should underlying assumptions prove incorrect, the

Company’s actual results and plans could differ materially from those expressed in any forward-looking statements.

All forward-looking statements, expressed or implied, included in this presentation are expressly qualified in their entirety by this cautionary statement. This cautionary

statement should also be considered in connection with any subsequent written or oral forward-looking statements that Eclipse Resources or persons acting on the Company’s

behalf may issue.

Except as otherwise required by applicable law, Eclipse Resources disclaims any duty to update any forward-looking statements, all of which are expressly qualified by the

statements in this section, to reflect events or circumstances after the date of this presentation.

3

Successfully completed initial public offering of 30.3 million shares resulting in net

proceeds of $545.4 million

Revenues grew to $27.0 million, a 9% increase over the first quarter of 2014 while adjusted

EBITDAX (a non-GAAP measure) for the quarter was $11.3 million

Strong Financial

Results

Key Highlights

Record

Production &

Operating

Results

New Firm

Transportation

Agreements

Average Daily Production

41.9 Mmcfe/d, a 9% increase from the first quarter 2014

58.2 Mmcfe/d in June 2014, 52% increase from the first quarter 2014 average

Commenced drilling 24 gross (16 net) operated Utica Shale wells achieving an average time

from spud to rig release of 23 days for wells drilled to total depth during the quarter

Turned to sales 3 gross (2.5 net) operated Utica Shale dry gas wells

Average initial flowing pressure of 5,838 psi over the first five days

30-day sales rate of 34.9 Mmcf/d using the company’s restricted choke production method

Mid-year 2014 proved reserves increased by 70% from March 31, 2014 to 186.4 Bcfe (22%

liquids) with a pre-tax PV10 of $337.9 million

Increased Utica Shale leasehold to approximately 99,300 net acres and Marcellus Project Area

to approximately 26,400 net acres

205,000 Dth per day on Columbia Gas Transmission’s Utica Access project accessing the

Columbia Transmission (TCO) Pool

Up to 150,000 Dth per day on Energy Transfer’s “Rover” project going north to Dawn,

Ontario and south to the Gulf Coast

Up to 100,000 Dth per day on the TETCO “Team 2014” project, providing flexibility to

move gas to the northeastern M3 market, the Gulf Coast and Midwestern markets

4

Pipeline Start Date Term Volume (Dth/d) Market

Floating Basis Firm Sales Nov-14 5 months 80,000 Tied to Dominion South

Fixed Basis Firm Sales Apr-15 7 months 50,000 Henry Hub less $1.328

Fixed Basis Firm Sales Nov-15 5 months 20,000 Henry Hub less $0.900

TETCO Apr-15 9.5 years 100,000 Gulf Coast, Midwest & M3

TCO Nov-16 15 years 205,000 TCO Pool

Energy Transfer Dec-16 15 years 50,000 Canada

Energy Transfer Jun-17 15 years 100,000 Gulf Coast

Midstream/Marketing Update

1. Henry Hub Natural Gas Differentials

During the second quarter, several agreements totaling 455,000 dekatherms of firm transportation were executed and come on line as early as April 2015

Based on current market conditions, differential for operated natural gas production is expected to average

approximately $0.90 to $1.00 per MMBtu below NYMEX during 2015

All long term firm transportation agreements expected to beat 90 cent long term differential target

(including transportation costs)

Start Date Term Volume (Dth/d) Average Differential ($/Dth)1

Nov-14 5 months 25,000 ($1.067)

Apr-15 7 months 25,000 ($1.208)Natural Gas Basis Swaps

5

Daily Production & Pricing

Eclipse has achieved record revenue and production levels for the quarter

Change %

Production – Average Per Day

Gas (Mcf/d) 27,020 30,519 (3,499) -11% 28,760

Oil (Bbls/d) 1,244 1,198 46 4% 1,221

Natural Gas Liquids (Bbls/d) 1,243 103 1,140 1103% 676

Total Equivalent (Mcfe/d) 41,941 38,326 3,615 9% 40,143

Average Natural Gas Price per Mcf

Realized Price (Before Derivatives) $4.09 $5.08 ($0.99) -20% 4.62

Realized Impact From Cash Settled Derivatives ($0.38) ($0.52) $0.15 28% (0.46)

Effective Realized Price $3.71 $4.56 ($0.85) -19% 4.16

Average Crude Oil Price per Bbl

Realized Price (No Derivatives) $93.30 $95.12 ($1.82) -2% 94.19

Average Natural Gas Liquid Price per Bbl

Realized Price (No Derivatives) $55.95 $61.83 ($5.88) -10% 56.41

Quarter to Quarter1H20142Q14 1Q14

6

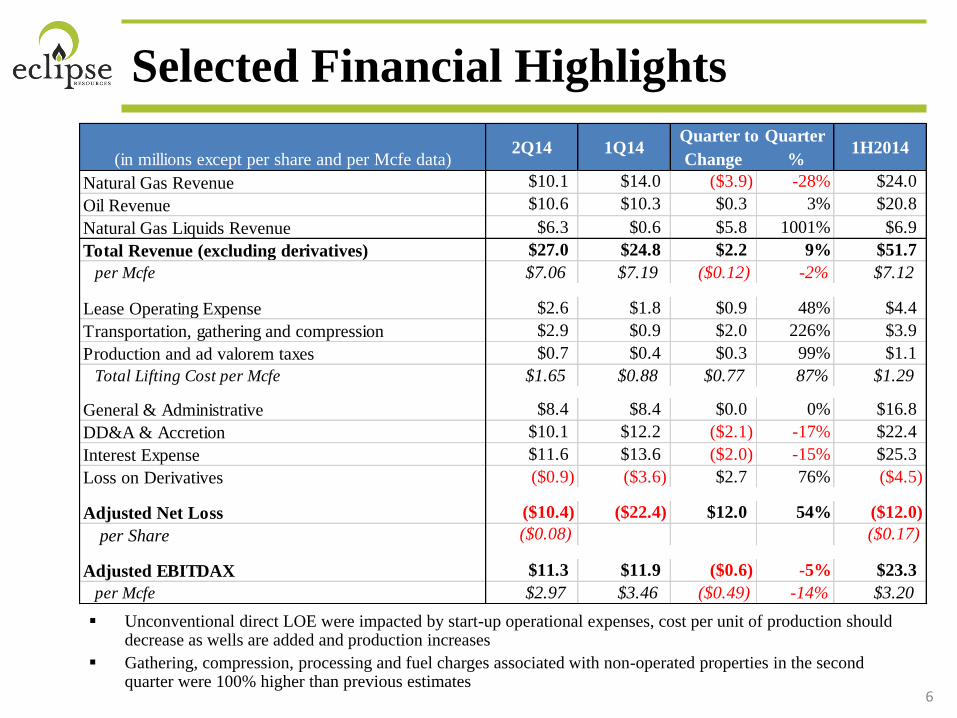

Selected Financial Highlights

Unconventional direct LOE were impacted by start-up operational expenses, cost per unit of production should decrease as wells are added and production increases

Gathering, compression, processing and fuel charges associated with non-operated properties in the second quarter were 100% higher than previous estimates

Change %

Natural Gas Revenue $10.1 $14.0 ($3.9) -28% $24.0

Oil Revenue $10.6 $10.3 $0.3 3% $20.8

Natural Gas Liquids Revenue $6.3 $0.6 $5.8 1001% $6.9

Total Revenue (excluding derivatives) $27.0 $24.8 $2.2 9% $51.7

per Mcfe $7.06 $7.19 ($0.12) -2% $7.12

Lease Operating Expense $2.6 $1.8 $0.9 48% $4.4

Transportation, gathering and compression $2.9 $0.9 $2.0 226% $3.9

Production and ad valorem taxes $0.7 $0.4 $0.3 99% $1.1

Total Lifting Cost per Mcfe $1.65 $0.88 $0.77 87% $1.29

General & Administrative $8.4 $8.4 $0.0 0% $16.8

DD&A & Accretion $10.1 $12.2 ($2.1) -17% $22.4

Interest Expense $11.6 $13.6 ($2.0) -15% $25.3

Loss on Derivatives ($0.9) ($3.6) $2.7 76% ($4.5)

Adjusted Net Loss ($10.4) ($22.4) $12.0 54% ($12.0)

per Share ($0.08) ($0.17)

Adjusted EBITDAX $11.3 $11.9 ($0.6) -5% $23.3

per Mcfe $2.97 $3.46 ($0.49) -14% $3.20

(in millions except per share and per Mcfe data)2Q14 1Q14

Quarter to Quarter1H2014

7

Borrowing Base $100 million

Outstanding Borrowings $0 million

Letters of Credit Outstanding $25 million

Available Debt $75 million

Cash Balance $493 million

Total Liquidity (6/30/2014) $568 million

Liquidity Status

Balance Sheet and Liquidity Review

Eclipse has ample liquidity to execute its drilling program

Balance Sheet Summary

(in $ thousands)

Actual as of

6/30/14

Actual as of

12/31/13Change

Cash $493,420 $109,509 $383,911

AR and Other Current Assets 45,257 9,272 35,985

Oil and Gas Properties 1,345,318 1,018,084 327,234

Other Assets 6,882 6,658 224

Total Assets $1,890,877 $1,143,523 $747,354

AP and Accrued Liabilities $142,300 $55,459 $86,841

Accrued Interest Payable 23,243 20,294 2,949

Senior Notes 412,823 389,247 23,576

Deferred Taxes and Other Liabilities 106,721 10,552 96,169

Total Equity 1,205,790 667,971 537,819

Total Liabilities and Equity $1,890,877 $1,143,523 $747,354

8

Current Operations Activity

Eclipse continues to meet or exceed its drilling and completions goals

Operated Drilling Activity 4 Operated horizontal rigs

Spud 24 gross (16 net) wells in 2nd quarter, drilled 11 gross

( 6 net) to TD

Averaged 23 days spud to rig release

Drilled longest lateral to date on Duane Weisand well in Noble

County at 9,096’

Set spud to rig release company record on Mizer Farms 7H,

Harrison County in 17 days with total measured depth of 14,881’

Since company inception, have spud 47 wells with both big rig

and top hole with 32 wells TD’s thru 7/31/14

Operated Completions Activity

2 frac spreads working In discussion to dedicate second frac spread

6 completed wells in 2nd quarter with an average of 3.6 frac

stages per pad per day

Deliberate frac design testing program in progress Parameters under review include stage spacing, fluid type,

sand concentration, and cluster spacing

Non-Operated Activity

Participated in 16 gross (2.5 net) wells spuds

12 gross (2.6 net) wells turned-to-sales during the second quarter

As of July 31, 2014, interest in 62 gross (11.6 net) non-operated wells 9 gross (2.6 net) drilling

40 gross (8.1 net) producing

Operated Spuds in 1H14

9

2nd Half Planned Activity

Operated Non-Operated

Adding 2 rigs in the 4th quarter; exit the year running 6 horizontal rigs

Run 2 frac spreads

Commission Mizer and Hayes Central Gathering Facilities delivering

gas into Blue Racer System

Non-operating program active with up to 10 rigs running in

the play

Working acreage trades to consolidate positions

Eclipse will focus its drilling activity in the second half of the year primarily in the condensate and rich gas areas of the play

Spuds Completions TTS

Non-Op 10.4 11.2 5.8

Eclipse 31.5 19.6 16.5

Overall 41.9 30.8 22.3

2H14

Budgeted

(Net)

10

Guidance

Third Quarter 2014 Full Year 2014

Production

Total Production – MMcfe/d 70 – 85 73 – 79

% Natural Gas 80 – 85% 72 – 76%

% NGL 7 – 10% 8 – 11%

% Oil 8 – 10% 12 – 14%

% Operated 65 – 75% 65 – 75%

Natural Gas Basis Differential & Transportation / MMbtu $ (1.65) – (1.75) / MMBtu $ (1.15) – (1.25) / MMBtu

Expense

Lease Operating $ 0.40 – 0.50 / Mcfe $ 0.40 – 0.50 / Mcfe

Gathering, Transportation, Compression & Processing $ 0.75 – 0.95 / Mcfe $ 0.75 – 0.95 / Mcfe

Production Tax 3.5% of Revenue 3.5% of Revenue

Cash G&A $ 11 – 12 million $ 39 – 42 million

Capital Expenditures $690 – 735 million

11

Sunday Monday Tuesday Wednesday Thursday Friday Saturday

1 2

3 4 5 6 7 8 9

10 11 12 13 14 15 16

17 18 19 20 21 22 23

2431

25 26 27 28 29 30

Sunday Monday Tuesday Wednesday Thursday Friday Saturday

1 2 3 4 5 6

7 8 9 10 11 12 13

14 15 16 17 18 19 20

21 22 23 24 25 26 27

28 29 30

August 2010

EnerCom’s 2010 Oil & Gas Conference

Presenting August 20

September 2010

Barclays CEO Energy Power Conference

Presenting September 4

Deutsche Bank Energy Conference

Presenting September 17

Morgan Stanley Marcellus-Utica Summit

Presenting September 17

Howard Weil Appalachian Bus Tour

Presenting September 30

Johnson Rice Energy Conference

Presenting September 30

Upcoming EventsA

ugu

stS

epte

mb

er

Appendix

Non-GAAP Reconciliation Tables

13

Adjusted EBITDAX

Change %

Net loss (112,648) (18,451) ($94,197) 511% (131,099)

Depreciation, depletion & amortization 9,957 12,027 ($2,070) -17% 21,984

Exploration Expense 9,295 4,545 $4,750 105% 13,840

Incentive unit compensation 27 29 ($2) -7% 56

Accretion of asset retirement obligations 191 186 $5 3% 377

Gain on reduction of pension liablilty 0 (2,208) $2,208 -100% (2,208)

Loss on derivative instruments 863 3,611 ($2,748) -76% 4,474

Net cash payment on derivative instruments (790) (1,441) $651 -45% (2,231)

Net cash paid for option premium (141) 0 (141)

Interest expense 11,618 13,636 ($2,018) -15% 25,254

Other income (1,585) 0 (1,585)

Income tax expense 94,541 0 94,541

Adjusted EBITDAX 11,328 11,934 ($606) -5% 23,262

per Mcfe $2.97 $3.46 ($0) -14% $2.81

1H2014(in thousands except per Mcfe data)

2Q14 1Q14Quarter to Quarter

14

Adjusted Net Loss

Change %

Loss Before Income Taxes, as reported (18,107) (18,451) $344 -2% (36,558)

Loss on derivative instruments 863 3,611 ($2,748) -76% 4,474

Net cash payment on derivative instruments (790) (1,441) $651 -45% (2,231)

Net cash paid for option premium (141) 0 (141)

Less Gain on Reduction of Pension Liability 0 (2,208) $2,208 -100% (2,208)

Add Impairment of Unproved Properties 3,666 0 3,666

Add Dry Hole Expense 102 27 $75 278% 129

Add Non-Cash Compensation Expense 27 29 ($2) -7% 56

Less Gain on Acquisition (1,586) 0 (1,586)

Loss Before Income Taxes, as adjusted (15,966) (18,433) $2,467 -13% (34,399)

Income Tax Benefit, adjusted (a)

5,588 6,452 ($863) -13% 12,040

Adjusted Net Loss (10,378) (11,981) $1,604 -13% (22,359)

Non-GAAP Adjusted Net Loss Per Share ($0.08) ($0.17)(a)

Income tax benefit represents the effect of company’s estimated annual tax rate 35% on Loss Before Income Taxes, adjusted

(in thousands except per share data)2Q14 1Q14

Quarter to Quarter1H2014

15

Hedging

DescriptionVolume

(MMbtu/d)Production Period

Weighted Average

Swap Price ($MMBtu)

Natural Gas Swaps

20,000 July - December 2014 $4.18

20,000 January - December 2015 $4.09

Natural Gas Put Spread

Purchased Put 20,000 June - December 2014 $4.50

Sold Put 20,000 June - December 2014 $4.00

Natural Gas Put - Sold

Sold Put 16,800 January - December 2015 $3.35

Natural Gas Basis Swaps

25,000 November - April 2015 ($1.067)

25,000 April - November 2015 ($1.208)

Top Related