Languages

Pages

Legal

139

Scenarios:shooting therapids

How medium-term analysisilluminated thepower of scenarios forShell management

Pierre Wack

One of the most constant variables of to-day's management practices is the notion of change, adap-tation, and innovation. Executives willingly embracechange when solutions can be found for and applied to par-ticular problems. Losing salesf Improve product quality.Taking too long to get your product to the distributor^Shake up inventory. Threatened by a takeover^ Make yourmanagement and corporation more lean, mean, and re-sponsive to the shareholders.

In a way, .such change is easy because itdoesn 't challenge the assumptions of good managers.Faced with a problem, they simply apply yet another for-mulaic solution. In the end, such easy change won't workagainst the kind of economic upheaval that has occurredin the last 15 years. Some fundamental modifications havebeen made in the way we do business. Shouldn't the corpo-rate response be equally fundamentals

In the last issue of HBR, the author de-scribed how he and a group of strategic planners at RoyalDutch/Shell began to put in place a most innovative way toprepare managers to think more clearly about the future-scenario analysis. What was required was not the applica-tion of a new formula for planning but rather a new v/ayofthinking. Tb show how difficult the transformation, the au-thor described how the company came up with the ideaand developed it in the early 1970s. In this sequel, he car-ries the story forward to describe the medium-term scenar-ios constructed in 1975. At a time when management'sattention suddenly became fixed on the next quarter asopposed to the next decade, effective medium-term analysisproved vital in translating scenario theory into practice.The author patiently walks the reader through the develop-ment of the 1975 scenarios and then discusses the implica-tions of scenario analysis on the practice of management.

Mr Wack is retired head of the business environment division of the Royal Dutch/Shell Group plan-ning department. Wack, an economist, developed withEdward Newland the Shell system of scenario planning. Henow consults and participates in scenario developmentvi/ith management teams around the world. In 1983 and1984, he was senior lecturer in scenario planning at theHarvard Business School.

I recently discussed scenario analysiswith a well-known futurist. After I had listened to hispresentation of a set of six scenarios, he asked me whatI thought. "It was beautifully written, if complex,"I repUed. When pressed, I admitted that it was "impen-etrable." I added^ "The managers who hear it won'tknow what to do with it." To which the consultant re-sponded, "That is not really my concem. I simply layout the possibilities for them. It is up to the managersto know what they should do. I can't possibly tellthem."

This small illustration points up thekey problem with scenario planning: the interface ofscenarios and decision makers is ignored or neglected.By interface, I mean the point at which the scenarioreally touches a chord in the manager's mind-the mo-ment at which it has real meaning for him or her. Thefact that those with the responsibility for preparingthe scenario do not feel any responsibility for the inter-face is the main reason that-despite the logical appealscenarios should have for managers disenchantedwith forecasts - scenario planning has been scarcelydeveloped.

Scenarios that merely quantify alterna-tive outcomes of obvious uncertainties never inspire amanagement team's enthusiasm, even if all the alter-natives are plausible. Most executives do not like toface such alternatives. They yeam for some kind of"definiteness" when dealing with the uncertainty thatis the business environment, even if they have hadtheir fingers burned for relying on past forecasts.

The same managers who can easily de-cide between different courses of action when theyare in control often become unstuck when confrontedwitb alternative futures they can't control and don'treally understand. The reason is partly historical: manymanagers developed their skills in the 1950s and 1960s,an era characterized by an unusually high level of eco-nomic predictabihty. Being competent then meant

140 Harvard Business Review November-December 1985

knowing the right answer; it was considered incompe-tent or unprofessional to say, "Things could go this way-or that."

In truth, scenarios are often popularwith middle managers who do not have to make awe-some, final decisions. It is really top managers - whohave ultimate responsibility for a company's long-termstrategy-who find scenarios unhelpful. Most haverisen to the top of large organizations based on theirgood judgment. They are proud of that judgment andtrust it; their faith in it is one of their key motivations.The usual scenario analysis confronts them with rawuncertainties on which they cannot exercise theirjudgment. Because they cannot use what they considerto be their best quality, they often say, "Why botherwith all that scenario stuff? We'll go on as before." Topmanagement's desire for a framework In which to exer-cise good judgment is so strong that many executivescontinue to rely on forecasts, even though they knowthat forecasts often miss critical tuming points in thebusiness environment and even when they have beenhurt by poor forecasts before.

What distinguishes Shell's decision sce-narios from the first-generation analyses delineated inmy earlier article is not primarily technical; it is a dif-ferent philosophy, having to do with management per-ceptions and judgment.' The technicalities of decisionscenarios derive from that philosophy. Almost by defi-nition, scanning tbe business environment and crystal-lizing the findings in a set of scenarios means dealingwith a world outside the corporation: for example, theevolution of demand, supply, prices, technology, com-petition, business cycle changes, and so forth. But thisis only a half-truth and dangerous because there is an-t)ther half. Because the raw materials of scenarios aremade from this stuff of "outer space," it is not realizedthat more is needed: scenarios must come alive in "in-ner space," the manager's microcosm where choicesare played out and judgment exercised.

Scenarios deal with two worlds: theworld of facts and the world of perceptions. Theyexplore for facts but they aim at perceptions inside theheads of decision makers. Their purpose is to gatherand transform information of strategic significanceinto fresh perceptions. This transformation process isnot trivial- more often than not it does not happen.When it works, it is a creative experience that gener-ates a heartfelt "Aha!" from your managers and leadsto strategic insights beyond the mind's previous reach.

I have found that getting to that man-agement "Aha!" is the real challenge of scenario analy-sis. It does not simply leap at you when you've pre-sented all the possible alternatives, no matter howeloquent your expression or how beautifully drawnyour charts. It happens when your message reaches themicrocosms of decision makers, obliges them to ques-tion their assumptions about how their business world

works, and leads them to change and reorganize theirinner models of reality.

Setting out

Scenario analysis demands first tbatmanagers understand tbe forces driving their businesssystems rather than rely on forecasts or alternativesIthat is, someone else's understanding and judgmentcrystallized in a figure that then becomes a substitutefor thinking). Using scenarios is as different from rely-ing OB forecasts as judo is from boxing: you want to useoutside forces to your competitive advantage andmake them work for you so that two plus two equalsfive or even more. You will find little or no power bymerely accepting expert information about an out-come like tbe future price of oil or the future level ofdemand; power comes with an understanding of theforces behind the outcome. Scenarios must help deci-sion makers develop tbeir own feel for the nature ofthe system, the forces at work within it, the uncertain-ties that underlie the alternative scenarios, and theconcepts useful for interpreting key data.

Scenarios structure the future into pre-determined and uncertain elements (see Exhibit /). Thefoundation of decision scenarios lies in exploration andexpansion of the predetermined elements: events al-ready in the pipeline whose consequences have yet tounfold, interdependencies within the system (surprisesoften arise from interconnectedness), breaks in trends,or the "impossible." Decision scenarios rule out im-possible developments; they deny much more thanthey affirm.

T will now take a risk and describe a ten-year-old scenario analysis. It is a risk because the sce-nario's subject is the business cycle, and no subjectthreatens to bore the reader in quite the same way as abusiness cycle that has passed. Even so, the discussionis important because:

1 We may be near the top of the businesscycle, and a recession with serious implications couldbegin, given the fragility of the world economy. Ittroubles me that so few companies have analyzed tbeimplications for them of economic developments out-side the range of surprise-free possibility Macroecono-mists may discuss contingencies but managers do not.

2 The scenario analysis I presented in thefirst article was somewhat atypical. It dealt with an

I "Scettarios:Uncharced Waters Ahead,"HBR Septembcr-Ocioher 1985,p. 72.

Scenario planning 141

The exhibits in Parts I and II are reprinted with thekind permission of Shell Intemational PetroleumCompany. I would like to acknowledge the originalcontributions of my former Shell colleagues andthe members of Group Planning. G.A. Wagner,A. Benard, K. Swart, and J.C. Davidson get specialthanks because they were instrumental in launch-ing the concept. My conceptualization of scenarioanalysis has benefited greatly from discussion withmy former Harvard Business School colleagues, inparticular Bruce Scott and David Bell. This articlewould not have been written without Norman Dun-can and Peggy Evans. It expresses one or twothings I have learned: it does not necessarily repre-sent Shell's current planning views or practices.

economic disruption of a magnitude we do not oftenencounter. Moreover, we believed the disruption wasa predetermined factor; uncertain were the reactionsto it.

The following example deals with moretypical cychcal fluctuations. We presented it in May1975, when the world was nearly at the hottom of theworst recession since World War II.

Analyzing the predeterminedelements

When the oil shock of 1973-1974 madethe dreams—and nightmares-described in the sce-narios discussed in my first article come true, manag-ers at Shell (like managers everywhere) redirected theirattention to the short term, focusing on economicgrowth, oil demand, inflation, interest rates, and theirsensitive relationship with OPEC supphers. In 1975,we addressed their concerns hy developing medium-term scenarios for the rapids. The predetermined ele-ments of these scenarios were:

The first wave-inflation. Like a largerock dropped in a lake, the 1973 oil price increase gener-ated a series of waves, beginning with inflation, whichwas higher than simple cost-through-the-systemarithmetic would indicate (on average, only 3% or 4%).Booming world economies were already out of balanceprior to the oil shock and affected hy high inflation.Furthermore, the enormous publicity surrounding theoil price increase (coming as it did with productioncuts and selective embargoes} caused major economicactors-trade unions, entrepreneurs, and consumers-to overanticipate the actual inflationary impact. Suchoverreaction added fuel to the fire, accelerating therate of inflation.

The second wave-deflation. Frommid-1974, a contraction in demand to well below pro-duction capacity followed. The extra cash outflow toOPEC acted like an extemal excise tax on consumerdemand of some $60 billion each year-or 2.5% ofOECD economies. Govemment anti-inflation policiescontributed toward pushing demand far below produc-tion potential. Economic dominoes fell one by one as:

D The automohile industry, always on themargin of discretionary spending and vulnerable toboth the real increase in gasohne prices and the "oillink" in the consumer's mind, suffered an immediatedecline, with extensive multipher effects through thebalance of the economy

n Building and construction, also a power-ful engine of economic activity, fell some six monthslater as govemment anti-inflation policies caused acredit crunch.

D The world iron and steel industry re-mained an island of continuing high activity for ninemonths after the oil shock. It was propped up by abacklog of orders (from shipyards, for instance) plussome stock building. Large orders from the communistworld contributed toward keeping it buoyant longerthan other sectors. Eventually, however, the decline inthe automobile and construction industries had adomino effect on the iron and steel industry.

Two other actions deepened the reces-sion. First, companies drastically ran down invento-ries. The imposition of credit controls in the face ofshrinking demand and the expectation of a fall inprices guaranteed a drastic drop in inventories. Wheninventories are reduced by eight days, it is equivalentto forgoing six months of 5% economic growth; inven-tories in many segments were reduced by more thaneight days. Next, consumer spending, long the stableengine of OECD economies, took a nosedive. For thefirst time since recovery started in the early 1950s, con-sumers stopped buying, increased savings, and began toworry about what the future might hold. The resultingrecession was the most severe since World War II (seeExhibit II].

Electoral rendezvous. The governmentsof fapan, Cermany, and the United States would eachface the electorate in 1976. If the truism applies tliatpeople vote their pocketbooks, then presiding over a re-cession is an invitation to defeat at the polls. The in-centives for incumbent governments to go for growthwere thus overwhelming.

Reflation in the pipeline. Not onlywere politicians anticipating the 1976 elections, butthey were also keenly aware that much of the hardshipborne in 1975 was unnecessary and self-infllcted-the

142 Harvard Business Review November-December 1985

Exhibit I 1975 global framework

Predetermined elements

Recordeconomicgrowth

Oil crisis

Highinflation

1973

First wave:Inflation

Overanticipalion

Second wave:deflation

Automobile

Building andconstruction

Iron and steel

Inventories

Consumerspending

Investment *

Credtlimplosion

1976electoralrendezvous

\

fc. Most severe^ ^ ^ postwar

recession

Fundamentalsocial andpoiiticai change

Reflation =most effectiveanti-infiationpolicy

1974 1975

deflation was too harsh. With excess capacity so wide-spread, govemments could safely reflate and expand-ijig output could reduce unit prices and further curbinflation. Such reflation would largely he self-financ-ing through taxation on increasing income, sales, andprofits, and lowered costs for unemployment benefits.

Long-term unemployment was becom-ing evident as a social prohlem. Unemployment fallsmost heavily on the young. Few govemments could af-ford to do nothing ahout the prospect of a third gradu-ating class moving from the classroom to the welfarerolls.

All these predetermined elements com-bined to make it virtually certain that govemmentswould attempt to reflate.

Reaching the rapids

We spent much time developing thepredetermined elements and imderstanding the recentpast. To recapitulate, managers will only accept sce-narios when their common, predetermined elements

enter and unfold in their minds. We call this process"rooting" hecause scenarios on their own-that is, asmere description of altemative courses of events-would he effective and alive in the minds of managersas long as a tree without roots. I have seen many sce-narios suffer this fate.

That economies would reflate waslargely predetermined. What was unknown in thespring of 1975 was the timing and nature of the recov-ery. To illuminate the forees driving the further devel-opment of the system and its critical uncertainties, wedesigned two scenarios of recovery:

The "Boom and Bust" scenario foresawa vigorous recovery that contained theseeds of its own destruction.

The "Constrained Growth" scenarioprojected a kind of "muddling-through"recovery that would differ fundamental-ly from earlier business cycle recoveries.

We also considered the possihility thatreflation would not happen; our "Depression Contin-gency" scenario seemed so improbable, however, thatwe did not think it relevant for planning. The threepossihilities are arrayed in Exhibit 1.

Scenario planning 143

Uncertainties

Boom andBustIncreasinglikelihood

ConstrainedGrowthDecreasinglikelihood

Boom

Foursurprises

Springeffect

uonsumer-

recovery

Hyper-inflation

^ ^

Highrate

Shock

Cost push

Rne tuning Need forinternational

Muddling cooperationalong

Depression— Contingency " ^

Unlikely^—

The worldknows how

^ ^ k to reflate^ ^ ^ butaccidenta

shocks deferrecovery.

Recession Inventories

Deflation

ft^onitorzigzageconomy

1976

Boom & Bust: a series ofsurprises

Boom and Bust described an economicworld more characteristic of the 1950s than the 1960s.Cycles of greater amplitude and shorter durationwould develop. We believed that the longer the recov-ery was deferred, the more likely this scenario—as gov-emments tumed to panic measures to reflate theireconomies.

First surprise-rapid recovery. Ratherthan tepid, the recovery would be swift, strong, andforceful, as some economies like that of the UnitedStates would grow by 11% or 12% in 18 months. Suchgrowth would be as if an economy the size of Britain'swere to appear all at once on the world map. Such a re-bound would not imply spectacular achievements,- itwould only reflect the depth of the 1973-1975 dent inthe economy-a coiled-spring effect.

Second surprise-oil-intensive recovery.Reports of OPEC's death, we beheved, were premature.Even though news of energy savings might persuadegovemments that Westem conservation measurescould negate OPEC's negotiating strength, such a boastcould not stand up to analysis. Reduced oil consump-

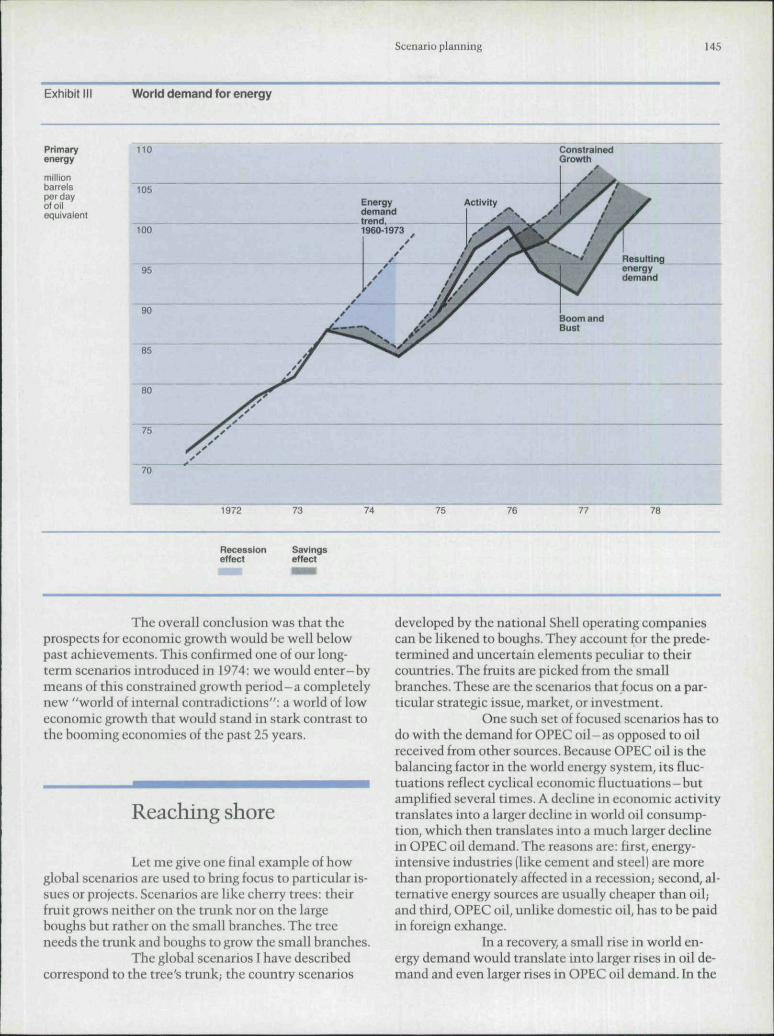

tion resulted not from a fundamental change in behav-ior but mainly from the recession, which had cut bothindustrial and consumer demand. A boom in 1976 or1977 would allow most consumers to revert to previ-ous patterns of behavior and consumption. Economicgrowth in 1976-1977 would have to be fueled by arisein energy demand, particularly for oil (see Exhibit 111).

Third surprise-booming U.S. oil im-ports. The upsurge in U.S. oil imports would easily putto rest talk about "Project Independence," PresidentGerald Ford's import-reduction targets, and alternativeenergy projects. Our estimates indicated that in such ascenario U.S. imports would rise by 2.5 million barrelsper day in 1976 (more than Britain's total imports orKuwait's current exports), with a further increase of 2million barrels per day in 1977 (in aggregate, more thanBritain's total energy consumption).

Because we believed that a normal re-covery would be equivalent to the sudden creation of anew economic nation, we could now add that the newnation would be almost totally dependent on MiddleEast oil. Consumer countries would once again betrapped.

Fourth surprise-stagnant alternativeenergies. Countries would find that alternative energy

144 Harvard Business Review November-December 1985

Exhibit II Decline in industrial productionmeasured from previous cyclical peak

USA Europe Japan

Recessionfirst quarter,1975

14% - 9 %

Previouspostwarr8(;essions

7% - 2 %

programs consisted largely of empty words and papertigers. Most nuclear plants operated well below designcapacity, and many had been deferred or canceled.Little had been done in the coal sector. The OECD na-tions were not meeting their target forecasts for coalproduction. The world had come far from the crashprograms of the dark days of the oil embargo. Alterna-tive energies could do little to relieve consumer coun-tries' continued dependence on Middle East oil.

The bust-a second recession. Highinflation-approaching hyperinflation in many of theweaker OECD nations-threatened a sustained recov-ery. Rates that would exceed the highest levels of 1974-1975 by a further 5% would hecome politically andsocially intolerable, signaling to governments that thehoom was getting out of control. Their reaction wouldbe to reapply deflationary measures, including creditrestrictions, higher interest rates, oil import controls,and limits on oil consumption. Just as the recoverywould be surprisingly rapid, so the downturn could besharp. Inventories would play an important role: stockbuilding, starting from the depths of the current reces-sion, would promote growth in production during theupswing. But as liquidity disappeared in the face ofstrong deflationary measures, stocks would be rundown rapidly, making the downturn that much sharper.

How probable was the Boom and Bustscenario? Because it held out dramatic implications forall sectors of the world economy and oil in particular,we found it hard to give equal attention to the otherscenario. Even so, in 1975, we still considered it lessprobable than its alternative. Constrained Growth.While we made no forecasts about the start of a boom,we were willing to assume that the longer the recoverytook to get under way the more likely the Boom andBust scenario would occur.

Constrained Growth: a neweconomic world

Everything in the Boom and Bust sce-nario was normal; the "surprises" were typical of busi-ness cycles. The Constrained Growth scenario wasbuilt on a more genuine surprise: recovery would beslower and more halting than any upturn of the post-World War n era.

The intemal logic of this scenario wasthat the high-growth trend of the past 25 years hadcome to an end-not only because of the oil shock andthe eclipse of the Bretton Woods monetary order, butalso because the very success of the postwar economiesbrought with it limitations on continued vigorousgrowth. Along with unprecedented economic growthhad come unprecedented expectations for higher stan-dards of living and more impressive social welfare pro-grams. High expectations produced a new economicrigidity as govemments were locked into a continualround of tax increases to pay for these social programs.Moreover, industrialized countries now were slower tochange and adjust to surprises-whether an oil crisis ornew competitors like lapan and the industrializingcountries of Southeast Asia.

Constrained growth would characterizethe first years of this new economic world in which allthe engines of growth - consumption, internationaltrade, govemment spending, and investment-wouldwork with less power.

Investment was emphasized as a changethat we called a lasting "technological recession."From the end of World War II until the early 1970s, thebest new technology in basic industries could, on itsown merit, outcompete existing technology A newsteel plant, for example, was more economical than anexisting one per ton of capacity,- new cement and paperplants, new refineries and tankers, and new power gen-eration plants were regularly more efficient than theprevious technology. Beginning in the early 1970s, how-ever, such technological progress could not beat risingcosts. It was now cheaper to acquire existing capacitythan it was to order new capacity.

For perhaps 10 to 15 years, the unit capi-tal and operating costs of almost all new plants in basicindustries would exceed the costs of existing equip-ment. That would obviously discourage new invest-ment in industries that had been the engine of postwareconomic growth and accentuate inflationary pressure.We analyzed the other engines of growth: governmentspending would result in budget deficits and morerigidity; consumer spending would be changed by thematuration in the life cycle of a large range of consum-er durables; and intemational trade would be character-ized by accumulating imbalances and frictions.

Scenario planning 145

Exhibit Iti World demand for energy

Primaryenergy

millionbarrelsper dayof oilequivalent

1972 73 74 75 76 77 76

Recession Savingseffect effect

The overall conclusion was that theprospects for economic growth would be well helowpast achievements. This confirmed one of our long-term scenarios introduced in 1974: we would enter-bymeans of this constrained growth period-a completelynew "world of intemal contradictions": a world of loweconomic growth that would stand in stark contrast tothe booming economies of the past 25 years.

Reaching shore

Let me give one final example of howglobal scenarios are used to bring focus to particular is-sues or projects. Scenarios are like cherry trees: theirfruit grows neither on the trunk nor on the largebouglis but rather on the small hranches. The treeneeds the trunk and boughs to grow the small branches.

The global scenarios I have describedcorrespond to the tree's trunk; the country scenarios

developed by the national Shell operating companiescan he likened to boughs. They account for the prede-termined and uncertain elements peculiar to theircountries. The fruits are picked from the smallbranches. These are the scenarios that focus on a par-ticular strategic issue, market, or investment.

One such set of focused scenarios has todo with the demand for OPEC oil-as opposed to oilreceived from other sources. Because OPEC oil is thehalancing factor in the world energy system, its fluc-tuations reflect cyclical economic fluctuations-butamplified several times. A decline in economic activitytranslates into a larger decline in world oil consump-tion, which then translates into a much larger declinein OPEC oil demand. The reasons are: first, energy-intensive industries (like cement and steel) are morethan proportionately affected in a recession; second, al-temative energy sources are usually cheaper than oil;and third, OPEC oil, unlike domestic oil, has to be paidin foreign exhange.

In a recovery, a small rise in world en-ergy demand would translate into larger rises in oil de-mand and even larger rises in OPEC oil demand. In the

146 Harvard Business Review November-December 1985

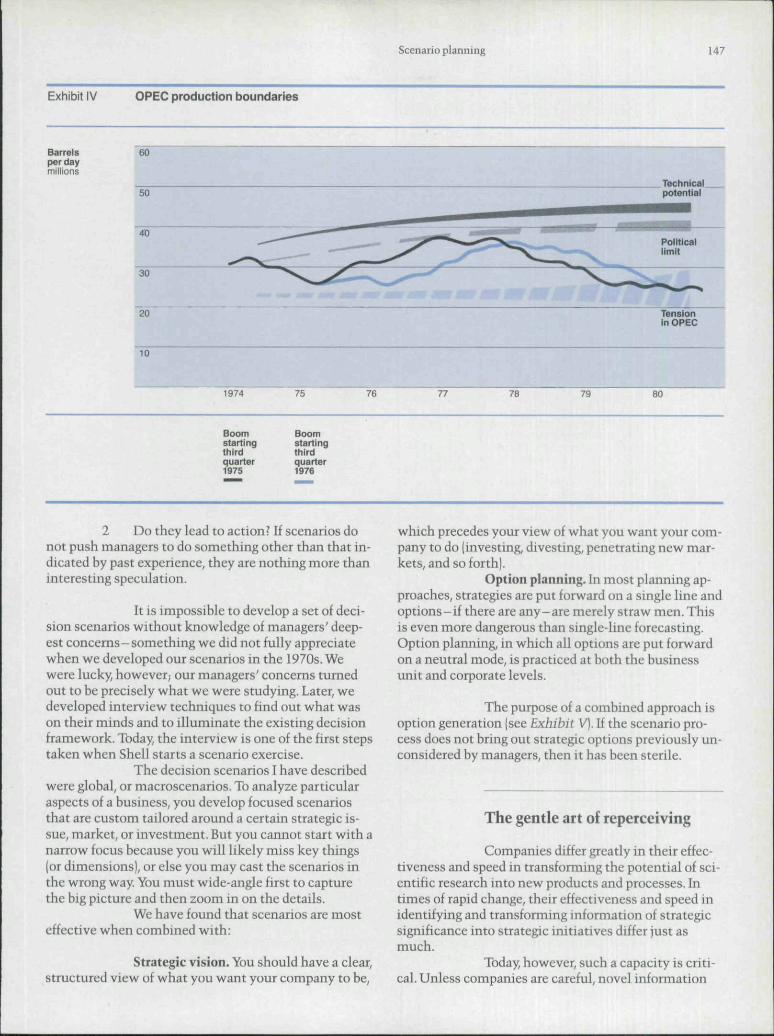

Boom and Bust scenario, for example, a 13% increase inworld energy demand in the first two years of a recov-ery would translate into a 23% increase in world oildemand and a 34% increase in OPEC oil demand. Howwould this demand match available supply? OPEC'soil production fluctuates in a narrow hand hetweentwo danger zones (see Exhibit IV]. Technical produc-tion capahilities and political willingness to producedetermine the upper band, which is dangerous for oil-consuming countries; the threshold of "OPEC dissatis-faction" is shown in the lower band, which is danger-ous for oil-producing countries hecause the solidarityand discipline of OPEC come under severe stress.

As an illustration, we made two simula-tions [shown in Exhibit IV]. The demand changes im-plicit in a normal hoom starting in late 1975 wouldbecome manifest in the winter oi 1976-1977, when sup-ply would he tight and prices under severe pressure.A hoom starting in late 1976 would he less dangerous.

Looking back at the trip

In the recovery of 1976-1978, economiesdeveloped mainly along the lines foreseen in the Con-strained Growth scenario. We were indeed introducedto the world of intemal contradictions. What had heenthe floor for long-term economic growth expectationshefore 1973 now hecame the ceiling. Many Shell man-agers recognized they were entering an era of slowergrowth and hedged their business plans accordingly.When the 1980s demanded leanness and restructuring.Shell was ready because it had begun the regimen early.That Shell saw this new world earher than most couldbe seen by comparing the various energy forecastsmade at the time. Shell consistently projected one ofthe lowest energy growth paths for the 1980s.

Scenarios serve two main purposes. Thefirst is protective: anticipating and understanding risk.The second is entrepreneurial: discovering strategicoptions of which you were previously unaware. Thislatter purpose is in the long run more important. Butwhile the more dramatic and (for Shell) dangerous ofthe two scenarios-Boom and Bust-did not occur, theexercise proved useful enough to our managers thatmedium-term scenarios were prepared every yearthereafter while in the rapids. As C. W. MacMalion ofthe Bank of England has succinctly ohserved: "Notime is as usefully wasted as that spent guardingagainst disasters that do not in the event occur."

Reflections in twilight

I have found that scenarios can effec-tively organize a variety of seemingly unrelated eco-nomic, technological, competitive, political, atid soci-etal information and translate it into a framework forjudgment-in a way that no model could do.

Decision scenarios acknowledge uncer-tainty and aim at structuring and understanding i t -hut not by merely crisscrossing variables and produc-ing dozens or hundreds of outcomes. Instead, theycreate a few altemative and internally consistent path-ways into the future. They are not a group of quasi-forecasts, one of which may he right. Decision scenar-ios describe different worlds, not just different out-comes in the same world. Never more than four (or itbecomes unmanageable for most decision makers), theideal number is one plus two; that is, first the surprise-free view (showing explicitly why and where it is frag-ile) and then two other worlds or different ways of see-ing the world that focus on the critical uncertainties.

The point, to repeat, is not so much tohave one scenario that "gets it right" as to have a set ofscenarios that illuminates the major forces driving thesystem, their interrelationships, and the critical uncer-tainties. The users can then sharpen their focus on keyenvironmental questions, aided by new concepts and aricher language system through which they exchangeideas and data.

A design that includes three scenariosdescribing altemative outcomes along a single dimen-sion is dangerous because many managers cannot re-sist the temptation to identify the middle scenario as abaseline. A scheme hased on two scenarios raises asimilar risk if one is easily seen as optimistic and theother pessimistic. Managers then intuitively believethat reality must be somewhere in hetween. They"split the difference" to arrive at an answer not verydifferent from a single-line forecast.

Experience shows that decision scenar-ios focus on critical uncertainties that are often verydifferent from those that seemed ohvious to managersat the beginning of the process. Despite this focus onuncertainty, decision scenarios do not paralyze manag-ers. Rather, the deeper understanding of the risks thatis gained often makes the decision maker capable ofconfronting apparently greater risk.

You can test the value of scenarios hyasking two questions:

1 What do they leave out? In five to tenyears, managers must not be able to say that the sce-narios did not warn them of important events that sub-sequently happened.

Scenario planning 147

Exhibit IV OPEC production boundaries

Barrelsper daymillions

60

Technical.potential

30

20 Tensiontn OPEC

10

1974 75 76 77 76 79 80

Boomstartingthirdquarter1975

Boomstartingthirdquarter1976

2 Do they lead to action ? If scenarios donot push managers to do something other than that in-dicated hy past experience, they are nothing more thaninteresting speculation.

It is impossible to develop a set of deci-sion scenarios without knowledge of managers' deep-est concems - something we did not fully appreciatewhen we developed our scenarios in the 1970s. Wewere lucky, however,- our managers' concerns tumedout to be precisely what we were studying. Later, wedeveloped interview techniques to find out what wason their minds and to illuminate the existing decisionframework. Today the interview is one of the first stepstaken when Shell starts a scenario exercise.

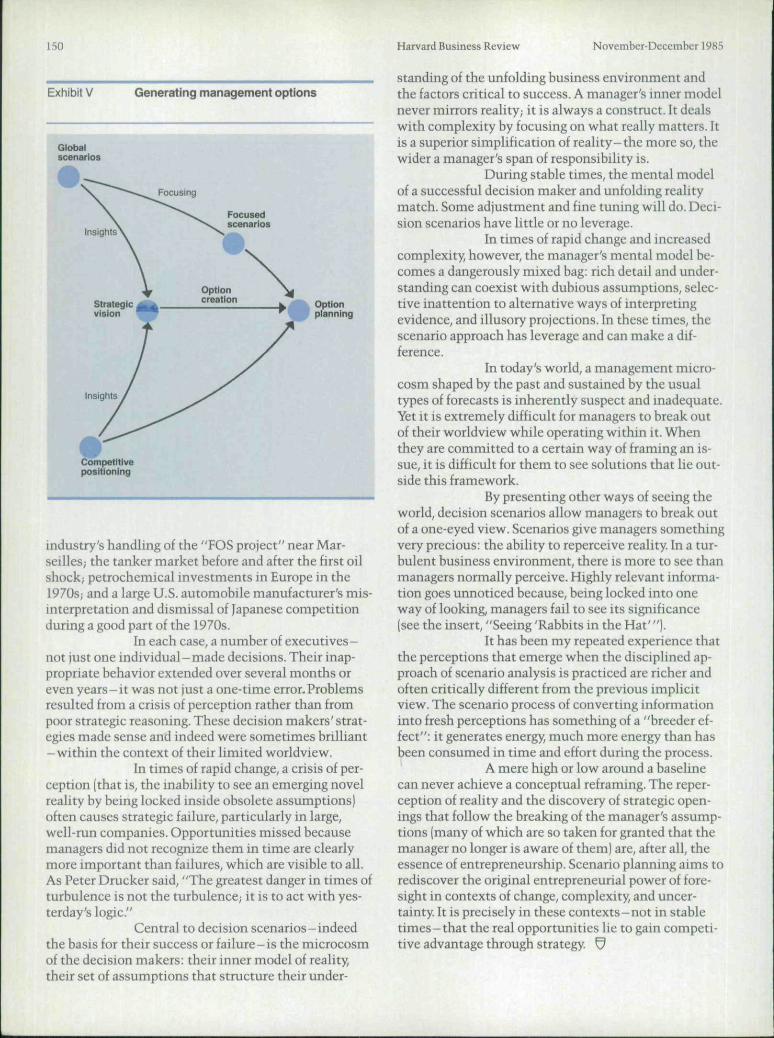

The decision scenarios 1 have describedwere glohal, or macroscenarios. To analyze particularaspects of a business, you develop focused scenariosthat are custom tailored around a certain strategic is-sue, market, or investment. But you cannot start with anarrow focus because you will likely miss key things(or dimensions), or else you may cast the scenarios inthe wrong way. You must wide-angle first to capturethe big picture and then zoom in on the details.

We have found that scenarios are mosteffective when combined with:

Strategic vision. You should have a clear,structured view of what you want your company to be.

which precedes your view of what you want your com-pany to do (investing, divesting, penetrating new mar-kets, and so forth).

Option planning. In most planning ap-proaches, strategies are put forward on a single line andoptions-if there are any-are merely straw men. Thisis even more dangerous than single-line forecasting.Option planning, in which all options are put forwardon a neutral mode, is practiced at both the husinessunit and corporate levels.

The purpose of a comhined approach isoption generation (see Exhibit V). If the scenario pro-cess does not hring out strategic options previously un-considered by managers, then it has heen sterile.

The gentle art of reperceiving

Companies differ greatly in their effec-tiveness and speed in transforming the potential of sci-entific research into new products and processes. Intimes of rapid change, their effectiveness and speed inidentifying and transforming information of strategicsignificance into strategic initiatives differ just asmuch.

Today, however, such a capacity is criti-cal. Unless companies are careful, novel information

148 Harvard Business Review November-December 1985

Seeing "rabbits in the hat"As any adult knows, a magician cannot producea rabbit unless it is already in (or very near) hishat. In the same way. surprises in the business envi-ronment almost never emerge without warning. Tounderstand the warnings, managers must be ableto look at available evidence in alternative ways.Otherwise, they can be badly misled by apparentlyvalid (acts if that is all they see, or they do not Inter-pret them in different ways.

After the second oil shock, a "scenario for the rap-ids" covering the medium term 1980-1985 intro-duced a notion at odds with prevailing wisdom.Called a "high savings case," it alerted manage-ment to "the possibility that consumers themselveswould produce a surprise in the form of a muchmore rapid decrease in energy and oil intensity thanthat assumed for the reference case." This wouldmean a further drop of 6 million barrels per day inthe demand for OPEC oil.

At the time, there was little hard evidence to supportthe case. There is always a lag in the impact ondemand of a price rise. Furthermore, there wasgreat uncertainty about the oil market and anxietyabout further supplies. The outbreak of the Iran-Iraqwar increased anxiety about supplies from theMiddle East. Both oil consumers and oil companiestried to increase their stocks of oil; customers'orders were strong: and industry forecasts as wellas the "feel of the market" all pointed toward sus-tained demand. The mood of the industry leanedtoward expansion: 1980-1981 saw an enormousincrease in drilling activity and feverish competitionto secure term contracts for the supply of crude.The problems of the oil industry were obviously onthe supply side, not on the demand side.

In March 1981, the new 1981-1985 scenarios forthe rapids stated that "last year's conservation sur-prise can no longer be regarded merely as a contin-gency." We also introduced a new scenario, 'HardTimes," that foresaw an economic recession deep-er than most observers expected, an oil conserva-tion surprise (drawn from the remarkable analysisby Aart Beijdorff), and societal change that wouldsignificantly affect both economic behavior and oildemand.

Under the Hard Times scenario, the combinedeffect of these three elements could lead to a totallydifferent~and much lower-level of oil demand (seeFigure A) than from the first oil shock-even though

Figure A OECD oil consumption

Millionbarrelsper dayof oilequivalent

40 Surprise-freereference

-''*"»,i case

Hard Timesscenafio

1960

AAI

AAD

65 70

^ Averageannualincrease

= Averageannualdecrease

75 80 85

7% AAi

- 4 % AAD

3% AAI

- 7 % AAD

-1 .6% AADSurprise- freereferencecase

- 4 % AADHard Timesscenario

outside the span of managerial expectations may notpenetrate the core of decision makers' minds, wherepossihle futures are rehearsed and judgment exercised.

Historical examples ahound. Alter con-cluding the nonaggression pact with Hitler in 1939,Stalin was so convinced the Germans would not attackas early as 1941 -and certainly not without an ultima-tum - that he ignored 84 warnings to the contrary.According to Barton Whaley, the warnings ahout

Operation Barharossa included communications fromRichard Sorge, a Soviet spy in the German embassy inTokyo, and Winston Churchill; the withdrawal of Ger-man merchant shipping from Soviet ports; and evacua-tion of German dependents from Moscow,-

Or consider the case of Pearl Harbor."Noise," the massive volume of signals, impeded un-derstanding of what was to come. As Roberta Wohl-stetter points out, "To discriminate significant sounds

Scenario planning 149

the immediate impact on GNP, balance of paymentof OECD, and so on was surprisingly similar.

We cailed the likelihood of there being a real con-servation surprise a "rabbit in the hat." Moreover,we were increasingly convinced that at least the twoears of our particular "rabbit" were already visible.First, less than one-sixth of the 1973-1974 crude oilprice increase had been passed on to final consum-ers because of the cushioning effect of refining andtransport costs and of various taxes in the sellingprice of the total products barrel. This time, how-ever, more than half of the crude price rise would befelt by final consumers, a change that suggestedconsumers' reactions would be nonlinear.

Second, a radical change in consumers' perceo-tions seemed likely to reinforce this growing p' '-eleverage. Few people had believed in the reality ofan oil crisis after 1973-1974; now fhe popular con-sensus seemed to be that the upward price trendwas irreversible. This change in attitude, combinedwith the normal effect of a large price increase,could reawaken previously dormant price elasticityfrom the first oil shock.

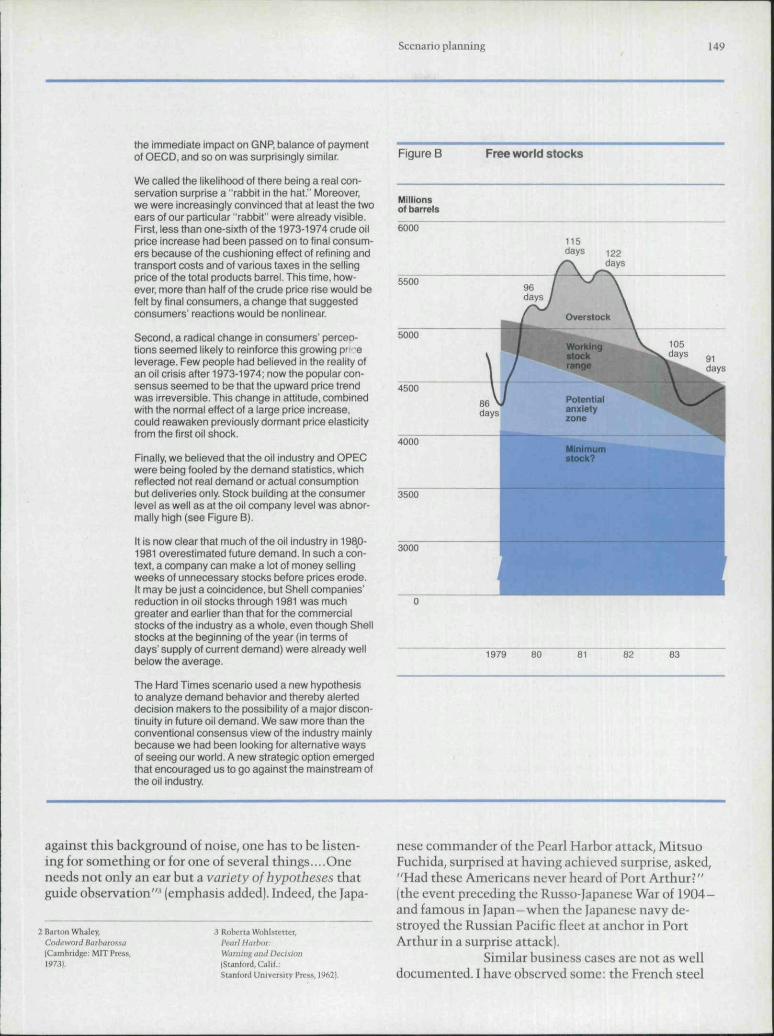

Finally, we believed that the oil industry and OPECwere being fooled by the demand statistics, whichreflected not real demand or actual consumptionbut deliveries only. Stock building at the consumerlevel as well as at the oil company level was abnor-mally high (see Figure B),

It is now clear that much of the oil industry in 198,0-1981 overestimated future demand. In such a con-text, a company can make a lot of money sellingweeks of unnecessary stocks before prices erode.It may be just a coincidence, but Shell companies'reduction in oil stocks through 1981 was muchgreater and earlier than that for the commercialstocks of the industry as a whole, even though Shellstocks at the beginning of the year (in terms ofdays' supply of current demand) were already wellbelow the average.

The Hard Times scenario used a new hypothesisto analyze demand behavior and thereby alerteddecision makers to the possibility of a major discon-tinuity in future oil demand. We saw more than theconventional consensus view of the industry mainlybecause we had been looking for alternative waysof seeing our world. A new strategic option emergedthat encouraged us to go against the mainstream ofthe oil industry.

Figure B Free world stocltt

Millionsol barrels

6000

1979 80 81 63

against this background of noise, one has to he listen-ing for something or for one of several things....Oneneeds not only an ear hut a variety of hypotheses thatguide ohservation"' (emphasis added). Indeed, the

2 Barton Whaley,Codeword BadtarossaICambritlge: MIT Press,1973).

3 Robena Wohlsterter,Peai] Harbor:Wariiitix "'id Oecisiim|Sianturd,Cali(.:StaniorJ University Press, 1962).

nese commander of the Pearl Harhor attack, MitsuoFuchida, surprised at having achieved surprise, asked,"Had these Americans never heard of Port Arthur?"(the event preceding the Russo-Japanese War of 1904-and famous in Japan—when the Japanese navy de-stroyed the Russian Pacific fleet at anchor in PortArthur in a surprise attack].

Similar husiness cases are not as welldocumented. I have ohserved some: the French steel

150 Harvard Business Review November-December 1985

Exhibit V Generating management options

Globaiscenarios

Optionplanning

Competitivepositioning

industry's handling of the "FOS project" near Mar-seilles; the tanker market before and after the first oilshock; petrochemical investments in Europe in the1970s; and a large U.S. automobile manufacturer's mis-interpretation and dismissal of Japanese competitionduring a good part of the 1970s.

In each case, a numher of executives-not just one individual-made decisions. Their inap-propriate behavior extended over several months oreven years-it was not just a one-time error. Problemsresulted from a crisis of perception rather than frompoor strategic reasoning. These decision makers' strat-egies made sense and indeed were sometimes brilliant-within the context of their limited worldview.

In times of rapid change, a crisis of per-ception (that is, the inability to see an emerging novelreality by being locked inside obsolete assumptions)often causes strategic failure, particularly in large,well-run companies. Opportunities missed becausemanagers did not recognize them in time are clearlymore important than failures, which are visible to all.As Peter Drucker said, "The greatest danger in times ofturbulence is not the turbulence; it is to act with yes-terday's logic."

Central to decision scenarios-Indeedthe basis for their success or failure—is the microcosmof the decision makers: their inner model of reality,their set of assumptions that structure their under-

standing of the unfolding business environment andthe factors critical to success. A manager's inner modelnever mirrors reality; it is always a construct. It dealswith complexity by focusing on what really matters. Itis a superior simplification of reality-the more so, thewider a manager's span of responsihility is.

During stable times, the mental modelof a successful decision maker and unfolding realitymatch. Some adjustment and fine tuning will do. Deci-sion scenarios have little or no leverage.

In times of rapid change and increasedcomplexity, however, the manager's mental model be-comes a dangerously mixed hag: rich detail and under-standing can coexist with dubious assumptions, selec-tive inattention to altemative ways of interpretingevidence, and illusory projections. In these times, thescenario approach has leverage and can make a dif-ference.

In today's world, a management micro-cosm shaped by the past and sustained by the usualtypes of forecasts is inherently suspect and inadequate.Yet it is extremely difficult for managers to break outof their worldview while operating within it. Whenthey are committed to a certain way of framing an is-sue, it is difficult for them to see solutions that lie out-side this framework.

By presenting other ways of seeing theworld, decision scenarios allow managers to break outof a one-eyed view. Scenarios give managers somethingvery precious; the ability to reperceive reality. In a tur-bulent business environment, there is more to see thanmanagers normally perceive. Highly relevant informa-tion goes unnoticed because, being locked into oneway of looking, managers fail to see its significance(see the insert, "Seeing 'Rabbits in the Hat'").

It has been my repeated experience thatthe perceptions that emerge when the disciplined ap-proach of scenario analysis is practiced are richer andoften critically different from the previous implicitview. The scenario process of converting informationinto fresh perceptions has something of a "breeder ef-fect": it generates energy, much more energy than hasbeen consumed in time and effort during the process.

A mere high or low around a baselinecan never achieve a conceptual reframing. The reper-ception of reality and the discovery of strategic open-ings that follow the breaking of the manager's assump-tions (many of which are so taken for granted that themanager no longer is aware of them) are, after ali, theessence of entrepreneurship. Scenario planning aims torediscover the original entrepreneurial power of fore-sight in contexts of change, complexity, and uncer-tainty. It is precisely in these contexts-not in stabletimes- that the real opportunities lie to gain competi-tive advantage through strategy. 0

Harvard Business Review Notice of Use Restrictions, May 2009

Harvard Business Review and Harvard Business Publishing Newsletter content on EBSCOhost is licensed for

the private individual use of authorized EBSCOhost users. It is not intended for use as assigned course material

in academic institutions nor as corporate learning or training materials in businesses. Academic licensees may

not use this content in electronic reserves, electronic course packs, persistent linking from syllabi or by any

other means of incorporating the content into course resources. Business licensees may not host this content on

learning management systems or use persistent linking or other means to incorporate the content into learning

management systems. Harvard Business Publishing will be pleased to grant permission to make this content

available through such means. For rates and permission, contact [email protected].

Top Related