Languages

Pages

Legal

ScalingupcleancookinginurbanKenyawithLPG&Bio-ethanol

AmarketandpolicyanalysisJune2018

2

Acknowledgment

ThisdocumentisanoutputfromtheMobilisingInvestmentproject,aninitiativeoftheClimateandDevelopmentKnowledgeNetwork (CDKN) and Low Emission Development Strategies Global Partnership (LEDS GP) contracted throughSouthSouthNorth (SSN). The Mobilising Investment project is funded by the International Climate Initiative (IKI) of theGermanFederalMinistry for theEnvironment,NatureConservationandNuclear Safety (BMU),on thebasisofadecisionadoptedbytheGermanBundestag.

3

Disclaimer

The views expressed are not necessarily those of, or endorsed by, BMU or any of the entities delivering theMobilisingInvestmentproject,whocanacceptnoresponsibilityorliabilityforsuchviewsorinformation,orforanyrelianceplacedonthem. This publication has been prepared for general guidance on matters of interest only, and does not constituteprofessional advice. You should not act upon the information contained in this publication without obtaining specificprofessionaladvice.Norepresentationorwarranty(expressor implied) isgivenastotheaccuracyorcompletenessoftheinformation contained in this publication, and, to the extent permitted by law, the entitiesmanaging the delivery of theMobilising Investmentprojectdonotacceptorassumeany liability,responsibilityordutyofcareforanyconsequencesofyouoranyoneelseacting,orrefrainingtoact,inrelianceontheinformationcontainedinthispublicationorforanydecisionbasedonit.

4

Executivesummary

Note:(1)ThisassumesastandardhouseholdconsumptionandisbasedonassumptionsofstoveefficiencyofexistingtechnologiesandcurrentfuelpricingSources:(2)StandardMedia,“ToughTimesAheadasStateIntroducesonKerosenetoFundSpendingPlan”,June92016

MajorityofKenyansstillcookwithdirtyfuelsthatcausesignificanthealthandenvironmentaldamage,despitecleaneroptions

LPGhaspenetratedNairobiandhigher-incomehouseholds;

Bio-ethanolcanbeanattractivecleanfuelforlower

incomehouseholds

EliminatingVATandimporttariffscanmakeBio-ethanolamongthecheapest1cooking

fueloptionsinKenya

Unlikeothercleanfuels,Bio-ethanolcanbeproduceddomesticallyovertime,whichwouldspurindustrialgrowthwhiledeliveringpositivesocialandeconomicbenefits

• Charcoal,kerosene,andfirewoodstilldominatetheKenyanmarket

• Thesefuelsaremajorcontributorstorespiratorydiseases,carbonemissions,anddeforestation

• TheGovernmentofKenya(GoK)hasstateditsambitiontotransitionKenyatomodern,cleanfuels

• TheurbanmarketpresentsthemostimmediateopportunitytotransitionKenyanstocleanerfuels,suchasLPGandBio-ethanol

• Whilemodern,cleanfuelsarenowmoreavailable,therearechallengeswithconsumerawareness,affordabilityandaccessibility

• LPGpenetrationhasincreasedrapidlyoverthepastfiveyears,especiallyinNairobi–thebenefitsarewell-publicized

• Whilelessknownabout,liquidBio-ethanolisnowincreasinglyviableasanurbancookingsolution,drivenbyinnovationsintechnologyanddistribution

• DespitehavingequivalentbenefitstoLPG,thecostofBio-ethanolisinflatedby25%importtariffsand16%VATtreatment

• ThistreatmentisinstarkcontrasttoLPG–whichenjoyseffectivetaxrateofzero–andkerosene,at9%importdutiesandzero-ratedVAT2

• IfGoKmade(denaturedtechnical)Bio-ethanolzero-ratedforVATandeliminatedtariffs,itwouldbeamongthecheapestcookingfueloptionsinKenyaandcoulddisplacecharcoalandkerosene

5

TableofContents

SectionI:Introduction

SectionII:KenyanCookingFuelMarketOptionsandSnapshot

SectionIII:PotentialofBio-ethanolforCookinginKenya

SectionIV:Bio-ethanolPolicyAnalysis

SectionV:ConclusionsandRecommendations

Appendices

6

SECTIONI:INTRODUCTION

Thisstudywasdevelopedto:

1. PositionthecookingfuelmarketwithinthewidercontextoftheGovernmentofKenya’sandothers’effortstoimprovethewelfareofKenyansacrossavarietyofdimensionso Vision2030aimstotransformKenyaintoanewly-industrializing,middle-incomecountryprovidingahighqualityoflifetoallits

citizensby2030inacleanandsecureenvironment;muchprogresshasbeenmade(e.g.,intheareasofhealthcare,education,andhousing)

o However,despitethecontinuedadvocacyeffortsofvariousstakeholders,additionalstridesareneededtoensurethatallKenyanshaveaccesstoaffordablecleancookingoptions

2. EvaluateKenya’surbanhouseholdcookingfuelsectorandunderstandthewaysinwhichcustomersareunder-servedbytraditionalfuels,whichcontinuetodominateovermoremodern,cleanfuelalternativeso TraditionaldirtyfuelsdominatefueluseinKenya:~85%1ofKenyansrelyontheseforcookingo Continueddependenceonthesefuelshasnegativeimpactsonhealth,environmental,andothersocialoutcomes

3. Profiletheavailablemoderncookingfueloptionsbasedonemergingtechnologiesandtrends

4. HighlightBio-ethanolcookingfuelasaviableandscalablemoderncookingfuelwiththepotentialtobesoldatpricesaffordabletothemajorityofurbanKenyanscurrentlyrelyingonkeroseneandcharcoalo Bio-ethanolandLPGarethemostfeasiblealternativestotraditionalfuels,offeringKenyansacleanandefficientcookingexperienceo WhileLPGisgenerallywell-understoodandisbeingactivelypromotedbythegovernment,Bio-ethanolrequiresfurtherexploration

andcanbecomplementarytoLPGasamoderncookingfuelforKenyans

5. Recommendstrategiesforenablingprivatesector-ledmodernizationofthecookingfuelsector–withafocusonBio-ethanol–todelivermaximumsocial,environmentalandeconomicbenefitsforthepublic

Source:(1)KenyaIntegratedHouseholdBudgetSurvey(2018),NationalBureauofStatistics

SectionI:introd

uctio

n

7

TheurbanKenyancookingfuelmarketisestimatedatUSD600m–USD800mperannum,andremainsdominatedbydirtyfuels

*Thismarketsizeestimateisbasedoncurrenturbanpopulationsize,fuelusepatterns,estimatedhouseholdconsumption/spend(basedonaverageefficienciesofcookstoves/fuelsinthemarket),andmarketpricedataforurbanKenyaSource:KenyaIntegratedHouseholdBudgetSurvey(2018),NationalBureauofStatistics

PrimaryCookingFuelUsedinKenyanHouseholdsin2017(households,millions)

SectionI:introd

uctio

n

Firewood -5.7

1.4

Charcoal

-0.2

-0.2Kerosene

LPG

Electricity 0.0 0.1

1.1-0.6

1.5

0.8

PrimaryCookingFuelUsedinKenyanHouseholdsin2017(%ofpopulation)

5584

15

22

14

29

28

16

313 252

Kenya Rural

9 2

Urban

Otherfuels

Charcoal

Kerosene

LPG

Firewood

ThisreportfocusesontheopportunityforBio-ethanoltoservetheurbanKenyanpopulation(marketestimatedat~$600-800mn*perannumwithfullfueltransition).ThemajorityofKenyanscurrentlypayingforcookingfuelsliveinurbanKenya• Mostfuelusedinruralareasisgatheredandnot

purchased(e.g.,84%ofhouseholdsusefirewoodastheirprimaryfuel)

• Market-drivenapproachesforexpandingtheuseofmodernfuelsareunlikelytotakeholdintheseareasintheshortterm

• Inurbanareas,ontheotherhand,over80%ofhouseholdsarealreadypurchasingcookingfuelandareprimetargetsformodernfueluse

Withinmodernfueloptions,Bio-ethanolandLPGarethemostfeasibletoday;Bio-ethanolistheleastunderstood• LPGiswell-understood,alreadypromotedbythe

Government,andenjoysstrongconsumerrecognition• Bio-ethanolisrelativelyunexploredandhasachieved

lowerpenetrationthusfar• Electricitywillbecomeincreasinglyimportanttothe

overallcookingmix;however,fornow,onlyhigherincomeconsumerscanaffordtheexpensivebutefficientelectricstovesthatareneededtomakeelectriccookingviable

InurbanKenya,themajoritystillusecharcoalandkerosene;thisnumberismuchhigherwhenfuel‘stacking’isincluded

Kenyanurbanhouseholdsarenowreadyforrapiduptakeofclean,modernfuels

Urban

Rural

8

SECTIONII:KENYANCOOKINGFUELMARKETOPTIONSANDSNAPSHOTThemajorityofurbanKenyansrelyoncharcoalfuelsandharmfulkerosenefortheircookingneeds• Charcoal(22%),kerosene(29%),andLPG(28%)arethedominant“primary”cookingfuelsinurbanKenyaasof2017• Stacking,i.e.,theuseofmultiplefuels/stoves,isawidespreadphenomenoninKenya;charcoalandkeroseneuseisthusmuchmorecommon

thanprimarycookingfueldataindicates–e.g.,2-3xurbanhouseholdsusingcharcoalvs.numberthatusecharcoalaprimarycookingfuel• NairobiisdistinctfromurbanKenya,withfarhighershareofhouseholdsusingLPG(44%)andkerosene(47%)asprimarycookingfuels(2017).

KeroseneisthedominantfueloftheNairobipoor1

Continueddependenceondirtyfuelsposesserioushealth,environmental,andsocio-economiccostsforKenya• 8-10%ofearlydeathsareattributabletoindoorairpollutionfromcharcoalandwoodcookinginKenya;thisexcludestheunquantifiedbutlikely

substantialnegativeeffectsofkerosenecookingonlungfunction,infectiousillnessandcancerrisks,aswellasburnsandpoisonings• Kenyaloses10.3millionm3ofwoodfromitsforestseveryyearfromunsustainablecharcoalandwoodfueluse• Householdbiomassfuelusecontributes>22milliontonnesofCO2eqeachyear(ashighas35MTCO2eqincludingfuelproductionemissions),

whichisequivalentto30-40%oftotalKenyaGHGemissions1

KeroseneandcharcoalremaindominantinurbanKenyaduetotherelativeaffordabilityandavailabilityofthesefuelsandaccompanyingstoves• KeroseneiscurrentlythelowestcostmainstreamcookingfuelinurbanKenya;charcoalboughtinsmallamounts(i.e.,tins)isthemostexpensive

cookingfuel,butcharcoalboughtinbulkbymiddleclassconsumers,i.e.,in40kgbags,canbeafairlyaffordableoption• Intermsofaccessibility,keroseneandcharcoalarecurrentlyomnipresentinurbanKenya–thereareover1,500kerosenedispensingpointsin

NairobialoneandanecdotalevidencesuggeststhatmostpeopleinNairobilivewithina50-150meterwalkfromacharcoalseller

CleanmoderncookingfuelsareavailableinKenya,buttheyhavenotyetovercomeconsumerawareness,affordabilityandaccessibilitybarriersinordertobecomescalableandsignificantlyreduceuseoftraditionalfuels• LPGiswellunderstoodandincreasinglycommoninurbanKenya,butdespitecontinuedinvestmentsincapacity,LPGisasolutionthatisunlikely

tobecometheprimaryfuelforthemajorityofurbanpopulationduetohighcostsandlimitedavailabilityoutsideofNairobi.LPGalsohasaweakperceptionofsafetyasafuelresultingfrompoorsafetypracticesoftheillegalgreymarketLPGre-fillers(estimatedat30-50%ofmarket)

• ElectricityforcookingisnotviabletodayinKenyaandhasminimalpenetration(~2%inurbanKenya)duetothehighcostsofefficientelectriccookstoves($200+)ofthetypethatcouldmakethecostsofelectriccookingcomparabletoalternatives

• LiquidBio-ethanolisanemergingoption,buthaslowawareness,isonlyavailableinselectgeographiesviaearlystageenterprises,andisrelativelyhighcostduetounfavorabletaxandtarifftreatmentrelativetocookingfuelalternativeslikecharcoal,kerosene,andLPG

SectionII:Ken

yancook

ingfuelm

arketo

ptionsand

snap

shot

(1)Dalbergestimatebasedonbottomupbuild-upofKenyacookingemissionsbasedonfuelmix,averagefuelvolumes,andstandardemissionfactorsincludingCH4andNO2,butexcludingBC.NotethatWRICAITtotalCO2emissionsforKenya(2013)areestimatedat60.53MTCO2eqtotal,whichwebelieveisanunderestimateasthenumberonlyincludes<8MTCO2eqofcookingrelatedemissions.OurrevisedmodelsuggeststhattheKenyatotalemissionsareactuallyinthe75-88MTCO2eqrangebasedonthemostuptodatecookingfuelmixandupcookingfuelcombustionandcharcoalproductionemissionfactorsthatarealignedwithCDMdefaultsforKenyaSource:Statisticsrepeatedandsourcedonfollowingpages

9

DespiteincreasedLPGuse,mosthouseholdsstillusemultiplefuelsanddirtyfuels–charcoal,kerosene,andwood–stilldominateurbanKenya

Source:(1)KenyaIntegratedHouseholdBudgetSurvey(2018),NationalBureauofStatistics;(2)DalbergproprietaryKenyaenergyaccesssurvey,N=300(2015)

SectionII:Ken

yancook

ingfuelm

arketo

ptionsand

snap

shot

UseofLPGhasincreasedsignificantlysinceitsintroduction,especiallyinNairobi;however,dirtyfuelsstilldominatecookinginurbanKenya• LPGsharehasincreased3-4Xsincetheearly2000s;dataacrossthistimeperiodshowsthat,eveninurbanarea,LPGuseis

concentratedamongstthoseearningahigherincome• ~70%ofKenyanhouseholdsinurbanareasusefirewood,charcoal,orkeroseneastheirprimaryfuel

Mosthouseholdsusemultiplefuelsinanygivenweekso,evenwhereLPGpenetrationishigh,householdsarestillcookingwithcharcoalandkerosene

HigheruseofLPGamonghigh-incomeKenyanssuggeststhatlower-incomeKenyansneedanalternativethatcandeliversimilarbenefitstoLPG,whilecompetingwithcharcoalandkeroseneonprice

Dirtyfuelsrepresent~70%and~55%ofprimaryfuelsuseinurbanKenyaandNairobi,respectively

Becausemostpeopleusemorethanonefuel,useofdirtyfuelsishigherthanprimarycookingfueldataindicate

Charcoal/keroseneareprimaryNairobicookingfuel(2016)1(%oftotalhouseholds(HH),N=24,000KenyaHHself-reportedprimaryfuel)

55

16

15

22

14

29

47

1328 44

AllKenya

3 5

1UrbanKenya Nairobi

3

5Charcoal

Kerosene

Other

Firewood

LPG

AllKenya–anyuseoffuelvs.primarycookingfuel2(%oftotalHH,N=300,Dalberg2015survey)

65%

Charcoal KeroseneFirewood

55%

LPG

69%

26%35%

8%15% 10%

Maincookingfuel

Anyfueluse

10

Continueddependenceonthesedirtyfuelsposesserioushealth,environmental,andfoodinsecurityrisksforKenya

Note:DALYisameasureofoveralldiseaseburden,expressedasthenumberofyearslostduetoill-health,disabilityorearlydeathSource:(1)2016GlobalBurdenofDiseasedata;(2)DalbergbottomupestimatetriangulatedwithWRICAIT(2013)KenyaGHGemissionsestimatesavailableathttps://www.climatelinks.org/sites/default/files/asset/document/2017_USAID_GHG%20Emissions%20Factsheet_Kenya.pdf;(3)UNEnvironment,“DeforestationcostingKenyaneconomymillionsofdollarseachyearandincreasingwatershortagerisk”,2016;Dalberganalysis

• Indoorairpollution:728kDisability-AdjustedLifeYears(DALYs)and16.6kdeathsannually,8-10%ofearlydeathsinKenya1,likelyasubstantialunderestimateofthefulldiseaseburdenasmanynegativecookinghealtheffectshavenotyetbeenquantified(e.g.,burns,eyediseases,physicalinjuriesfromcarryingfirewood,etc.)

• LowerrespiratorytractdiseaseisthethirdlargestcontributorofdeathsinKenyawhilepneumoniaisamajorcauseofdeathtochildrenundertheageoffive,largelyduetoindoorairpollution1

• Deforestationandforestdegradation:Kenyaloses10.3millionm3ofwoodfromitsforestseveryyearfromunsustainablecharcoalandwoodfueluse,amajorcontributortothe0.3%peryeardeforestationrate2

• GHGemissions:HouseholdfueluseinKenyacontributes22-35milliontonnesofCO2eqeachyear,whichisequivalentto30-40%oftotalKenyaGHGemissions2

• Foodinsecurity:deforestation,resultingfromtheuseofdirtyfuels,exacerbatesfoodinsecurityandharmstheagriculturesector.Kenya'sfiveforestwatertowersfeedfilteredrainwatertoriversandlakesandprovideover75percentofthecountry'srenewablesurfacewaterresources3

Impactofusingbiomassfuelforcooking

Health

Environment

Foodinsecurity

SectionII:Ken

yancook

ingfuelm

arketo

ptionsand

snap

shot

11

Charcoalisparticularlyharmfulasitcontributesmoretohouseholdairpollution,GHGemissions,anddeforestationthanotherfuels

Source:DalbergimpactsizingmodelforruralKenya,2018;HouseholdAirPollutionInterventionTool,withcustomizedinputsforNairobibasedrespectiveswitchingtoLPGandethanolconsumption.Note:morequalitativedetailprovidedinAppendixA

SectionII:Ken

yancook

ingfuelm

arketo

ptionsand

snap

shot

IMPACT Wood Charcoal Kerosene

Health(deathsandDALYsduetohouseholdairpollutionfromPM2.5)

~2kavoidabledeaths165kaDALYs

~3kavoidabledeaths~250kaDALYs

~2-3kavoidabledeaths~160kaDALYs

Environment&climate(GHGemissions)

2.5-4.4tonneCO2eq/urbanHHannually

3.6-5tonneCO2eq/urbanHHannually

1tonneCO2eq/urbanHHannually

Socialopportunitycosts(timeopportunitycoststofuelcollection,cookingandcleaning)

0.8-1.3avoidablehrsperdayperurbanHH

0.3-0.4avoidablehrsperdayperurbanHH Notimepovertyimpact

Householdandmacro-economics

• Foregoneincomesforavoidabletimespentcookingandcleaning

• Taxrevenuelossforgovernmentgiveninformalityofmarket

• Foregoneincomesforavoidabletimespentcookingandcleaning

• Avoidablespendingonexpensivefuel

• Taxrevenuelossforgovernmentgiveninformalityofmarket

• Costtoeconomyofillicitmixingofkerosenewithdiesel

• Negativebalanceofpaymentseffectsduetokeroseneimports

12

CharcoalandkeroseneremaindominantinurbanKenyabecauseofwideavailabilityandrelativeaffordability…

Note:Givencombinedaffordabilityandaccessibilityconstraints,electricityasacookingfuelnotexploredindetailinthisreport.Source:(1)Dalbergproprietaryresearch;(2)KokoandDalberg;(3)Dalbergfieldresearch;(4)Dalbergsurveyandproprietarycharcoalpricetracker;(5)DalbergandKokoresearch;(6)KokoNetworksestimate;(7)Yonemitsu(2014)forKiberaandK.Muindi(2016)forKorogochoandViwandanislums

SectionII:Ken

yancook

ingfuelm

arketo

ptionsand

snap

shot

Relatively low costs and wide availability for dirty fuels, but such fuels are increasingly expensive

FUEL Affordability&availabilityassessment

Wood

• Abundantandlargelyfreeinruralareasforcollectors,though20-30%ofruralHHsbuyingatleastsomeoftheirfirewood1

• FirewoodisincreasinglyscarceandexpensiveinurbanKenya,particularlyNairobi(e.g.,>$0.50/kg),butstillfairlylowcost(e.g.,$0.15/kginKisumu,$0.10-0.15/kginmostruralandperi-urbanKenya)2

• Traditionalandmoderatelyimprovedfirewoodstovesarefreeorverylowcost(<$10)

Charcoal

• WidelyavailableinurbanKenya(e.g.,charcoalavailablewithin50–150mofmosthomesinNairobi)3

• Increasinglyexpensiveasforestsrecede(pricesrosefrom$0.10/kgto$0.35-0.50/kginNairobiinpastdecade,doublinginjustpast3-5years)4

• Majorpovertypremium–20-30%highercostfrombuyingcharcoalin2kgtinsvs.40kgbags5

Kerosene

• Widelyavailablethroughoutmass-marketneighbourhoodsathyper-localdistributionpoints(e.g.,1500+pointsinNairobialone)6

• MostaffordableandlowestcostfuelinurbanKenyacurrently

• Oftenonlytrulyaffordableoptionforpooresturbanresidents(e.g.,keroseneisprimaryfuelfor70-80%ofslumhouseholdsinNairobi)7

13

…butadvantageoftraditionalfuelsvs.cleanfuelsisfasteroding

*Bio-Ethanolcookingfuelisaclearliquidmadefrom~95%ethylalcohol,5%water,violetdye,andanindustry-standardbitteringagent(Bitrex)whichirreversiblymakesthisfuelunfitforhumanconsumption;Excludesalcohol-based‘gels’,whicharetypicallyhigher-costandlower-powerfuels.Note:Givencombinedaffordabilityandaccessibilityconstraints,electricityasacookingfuelnotexploredindetailinthisreport.Source:(1)ChristianAid(2017)survey,(2)Dalbergfieldresearch,(3)KokoNetworks,(4)Dalberganalysis

SectionII:Ken

yancook

ingfuelm

arketo

ptionsand

snap

shot

Clean fuels face availability and affordability challenges, but both gaps are closing

FUEL Affordability&availabilityassessment

LPG

• FuelavailabilityisfairlywidespreadinNairobi(>40%useLPGasprimaryfueland>60%haveLPGstove)1;forurbanKenyaasawhole,availabilityisprojectedtoincrease–KenyaPipelineCompany(KPC)plantomorethandoubleLPGstoragecapacityby2020

• LPGislargelyunaffordableasaprimaryfuelforbottom50-70%acrossurbanKenyaandpriceshavebeenunstable($1.25to1.75/kgovercourseof2017)2

• Highupfrontstove/cylindercosts(>$100for2-burner)2

Electricity

• Notwidelyavailable:residentialgridprovisionedforlightingonly;majorcapexinvestmentrequired• Electricitycoststoohighformass-marketelectriccooking(uptake~5%inNairobi,~2%inurbanKenya)1

• Efficientelectricstovesarepriceduncompetitively(>$200)forstovesthatbringcostsofelectriccookingwithinrealmofotherfuelalternatives2

Bio-ethanol

• DenaturedBio-ethanol*forcookingcurrentlyonlyavailablefromahandfulofprovidersthatareallcurrentlyatnascentorpilotscale(i.e.,KOKONetworks,Leocome,SafiInternational),butabouttoscalequickly–e.g.,1000KOKOPointsgoingliveacrossNairobiinlate20183

• CookingwithlowestcostBio-ethanolonKenyamarketisslightlymoreexpensivethankerosene,onparwithLPG,andbelowcostof4kgtincharcoal--wouldbelowestcostoptioniftaxandtariffregimewasequaltootherfuels4

• Bio-ethanolstovesarefairlylowcost($45for2-burner)comparedtocleanalternativeslikeLPG4

14

ModerncookingfuelsareavailableinKenya,buttheyhavenotovercomeconsumerawareness,affordabilityandaccessibilityadoptionbarriersSectionII:Ken

yancook

ingfuelm

arketo

ptionsand

snap

shot

LPG Bio-ethanol

Appliances Mixof1-burner‘meko’and2-burnerstovekit(includinghose,pressureregulator,cylinder)

Mixof1-burnerand2-burnerBio-ethanolstovesfromKOKO,SAFI,CleanCook

Fuel • Imported• Availableincylindersof3kg,6kg,13kg

• Importedanddomesticallyproduced• Availablein1&5Lpre-packagedbottles(oraslittleas350mLinrefillable2.3Lcanister–KOKONetworks)

Players • Total(TotalGaz)• Hashi• KenolKobil(KGas)• KenyanPipelinecompany(infrastructure)• Pay-as-you-goLPGpilots–(e.g.,PayGoEnergy,

EnvirofitSmartGas,KopaGas)

• KOKONetworks• Leocome• SafiInternational• ProsolLimited• IR&DAfricaLimited

Keybarrierstoscale

• Highupfrontstoveandcylindercosts• Highongoingfuelcosts(especiallygivenLPG

notwidelyavailableinsmallerquantities)• Safetyconcernsbysomecustomers• Highcapitalexpendituresrequiredforscaling

necessaryinfrastructure

• RelativelyhighongoingfuelcostsduetoVATandtariffsvs.otherfuelalternativesthatdonotfacesuchduties

• Verylowlevelsofconsumerandmarketawareness

Source:Deskresearch,previousNairobisurveyandfocusgroups.

LPGiswell-understood.LiquidBio-ethanolisacomplementary,emergingcookingfuelsolutionthatisdescribedandanalyzedinmoredepthinthefollowingsectionofthisreport

15

Source:(1)CalculationsbasedonFAO,“LogisticsofCharcoalProduction”,2010;(2)bottomupbuildofHHemissionsatpointoffuelconsumptionandincludingfuelproductionw/averageemissionsfactors-charcoalstoveusedisKCJ;(3)assumesaverage50ug/m324hremissionsof50forbothLPGandEthanolbasedonlabdata,fielddatarangesare15-71ug/m3forLPG,30-100+forethanol,butfieldnumbersnotapplestoapplesgivenambientpollutionvariation;(4)KokodatatriangulatedwithProjectGaiareportsforCleanCookinMadagascarandTanzania;independentreportsforHaiti;SafiJikoinKenya;evidenceseemstopointtocomparableLPGandEthanolstovecookingtimes

SectionIII:A

nalysiso

fBio-ethan

olfo

rcoo

kingpoten

tialinKe

nya

ImpactofswitchingtoBio-ethanol ImpactofswitchingtoLPGCategory

• ~0.25DALYssavedperHHperthreeyearinterventionperiodfromswitchingfromcharcoalandkerosene

• Reductionof~50deathsper25,000householdsfromreducedindoorairpollution3

• Safetyrisksofstorage,handlingandusearelowerforaliquidthanpressurizedgas

• ~0.25DALYssavedperHHperthreeyearinterventionperiodfromswitchingfromcharcoalandkerosene

• Reductionof~50deathsper25,000householdsfromreducedindoorairpollution3Health

• Upto30treessavedperHHannuallyfromswitchingfromcharcoal1

• Slowsdownrateofdeforestationand,consequently,itsimpactonfoodinsecurity

• 0.7-3.3tonnereductioninGHGemissionsperHHperyearfromswitchingfromkeroseneandcharcoalrespectively2

• Upto30treessavedperHHannuallyfromswitchingfromcharcoal1

• Slowsdownrateofdeforestationand,consequently,itsimpactonfoodinsecurity

• 0.5-3.1tonnereductioninGHGemissionsperHHperyearfromswitchingfromkeroseneandcharcoalrespectively2

Environmental

• Distributedinsmallervolumes,makingitmoreaccessibletolower-incomeusers

• ExistingdomesticBio-ethanolsectorcouldbeexpanded,creatingformal,taxablejobsandboostingsmallholderfarmingincome

• 20-40minssavedperHHperdayfromswitchingawayfromcharcoal4

• Higherupfrontcostsandrequirespurchasinginlargerbundlesizes

• 20-40minssavedperHHperdayfromswitchingawayfromcharcoal4Economic/

opportunitycosts

Bio-ethanoldeliversenvironmentalimpactscomparabletoLPGwhilerequiringconsumerstopaylowerupfrontcostsandallowingsmallerpurchasesizes

16

TheGovernmentofKenyahasintervenedtopromoteLPG;policyactionisnowneededtoleveltheplayingfieldforBio-ethanol

Source:Stakeholderinterviews;StockholmEnvironmentInstitutediscussionbriefontheKenyancharcoalsector;Variousnewspaperarticles;Dalberganalysis

Thegovernmentisusingatwo-

prongedstrategytopromotecleancookinginKenyan

households

Curbuseofdirtyfuelsandstoves

Promotecleancookingfuelsandstoves

Todate,Bio-ethanolforcookinghasnotbeenasmuchatargetofgovernmentinterventiondespitebeingahigh-impactcleanfueloption,mainlyduetolimitedprivate

sectoractivitySectionII:Ken

yancook

ingfuelm

arketo

ptionsand

snap

shot

• ‘Kerosene-FreeKenya’campaignaimstophaseouttheuseofkeroseneforlightingandcooking,andreplaceitwithcleanenergysources,includingplanstoincreasetaxesonkerosene.Thiswouldalsoreducetheillicituseofkerosenetodilutediesel

• Effortstoregulatethecharcoalindustrybyprovidingsupportforsustainableproductionandcommunityforestmanagementareminimizingimpactofcharcoaluse

• GoKhasintroducedfiscalincentivestoreducecostsofcleancooking

• VATzero-ratingforLPGhasreducedpricesandMwananchiGasProjectsubsidizescostofcylinders

• RemainingdutiesandVATonBio-ethanolstovesandfueladdscosttocustomers

Policysupport LPG Ethanol

FUEL Removeimportduty

VATzero-rating

APPLIANCE

Reduceimportduty

RemoveVAT

Subsidizeappliance

ü

ü

ü

ü

ü

ü

17

SECTIONIII:POTENTIALOFBIO-ETHANOLFORCOOKINGINKENYA

Note:statisticsrepeatedandsourcedonfollowingpages.MoredetailedimpactanalysiscontainedinAppendixB

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

Thehealth,environmental,andothersocialimpactsoftransitioningfrommoretraditionalfuels(e.g.,firewood,charcoal,andkerosene)arewelldocumented;whileLPGhasenjoyedmorevisibilityandpromotioninKenya,thepotentialbenefitsoftransitioningtoBio-ethanolarealsosignificantataHHlevel• SwitchingfromcharcoaltoeitherBio-ethanolorLPGcouldsaveupto30treesandreduce3-5tonnesofGHGemissionsperhousehold• Bio-ethanolandLPGhaveaveragePM2.5emissionsmuchlowerthanthoseoftraditionalfuels• TransitioningallkeroseneandcharcoalusersinNairobitoBio-ethanolcouldresultinupto2mntonnesGHGsand200,000DALYsaverted

annually• ThistransitionwouldalsocounteractdeforestationanditsnegativeeffectsonagriculturalyieldsandfoodinsecurityBio-ethanolcanalsodeliveradditionaleconomicbenefits• Aslocaldemandisunlockedandthenecessaryinvestmentsaremade,theexistinglocaltechnicalalcoholindustrycouldbeexpandedtoserve

thisdemand,creatingjobsacrossthevaluechain• Whilethesewilldisplacejobsinthecharcoalvaluechain,theywillgenerallybeofhigher-qualityandbetterpaying,andpotentiallytaxable,

providingthegovernmentwithadditionalresourcestoinvestotherjobcreationactivitiesfordisplacedpersons

Bio-ethanolisbecomingcost-competitiveandscalableasacookingsolution,giveninnovationsthatleveragelocalizeddistributiontechnologyandexistingdownstreaminfrastructure• Bio-ethanolV2.0modelhasshrunklogisticscostsbetweenthelandedcostandfinalpricetocustomer,withtaxesnowdriving~25%offinal

price• Bio-ethanolV2.0canbescaledwithsignificantlylowercapitalexpendituresthanrequiredforscalingLPGThepartnershipbetweenVivoEnergy,adownstreamfueltradingcompany,andKOKONetworks,ahardwareandsoftwaretechnologycompanyenablingthelast-miledistributionofBio-ethanolfuel,istheleadingexampleofV2.0inKenya• Leveragingexistingfuelinfrastructure,salespoints,andmobileandcloudtechnology,KOKO’smodeldeliversfuelcloserandmorecheaplyto

customers• VivoEnergyusesKOKOtechnologiestosafelyandefficientlyaddanewlineofliquidfueltoitsexistingdownstreaminfrastructure• Withthismodel,Bio-ethanolissoldtocustomersat$0.85/L

18

Alcohol-basedcookinghasadecades-longhistory,butonlyinnichemarkets

Source:Expertinterviews.

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

WorldWarII:Soldiers&farmers

usedalcoholproducedonfarms

Late20thcentury:Usedforcamping,recreational

vehicles;distributedbyEuropeanandNorthAmericancompanies

Early21stcentury:Adaptedforusein

refugeecampsinEastAfrica;non-commercial

2013:FirstcommercialV1.0ventureforBio-ethanolcookingcaptured10%ofMaputoHHswithinayearofretaillaunch

Sugarfeedstocks(e.g.,sugarcane)

Starchfeedstocks(e.g,maize,grains)

Cellulosicfeedstocks(e.g.,wasteresidues)

Ediblesugar

Syrup

Bio-ethanolmadefrommolassesbyproductor

syrup

Denaturedtechnicalalcoholusedforcookingis

thecheapest

molasses

HistoryofBio-ethanol

Bio-ethanolproduction

2014-17:V1.0BioethanolcookingfuelcompanieslaunchedinmanyAfricancountries

2017:FirstV2.0ethanolcookingfuelsolutioncommerciallylaunchedinNairobi

19

Atransitionofallkerosene/charcoalusersinNairobitoBio-ethanolcouldresultin~2mntonnesGHGs,200KDALYs,and1,500deathsavertedp.a.

Note:(1)KyotoparticlesandblackcarbonCO2equivalents;Source:(2)Kenya’sIntendedNationallyDeterminedContribution,MinistryofEnvironmentandNaturalResources,2015.(3)HAPITmodel;(4)DalbergNairobiimpactmodel.SeeAppendixBformethodology.

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

AfulltransitionofkeroseneandcharcoaluserstoBio-ethanolinNairobialonewouldhelptowardsachievingtheSustainableDevelopmentGoals

~200,000DALYsand1,500deathsaverted34overathreeyear

interventionperiod

Difficulttoquantifygivenpoordata,butmosttimesavingsfromcollection,cooking,andcleaning

willaccruetowomen

USD60mninannualconsumersavings4

Reductionof2mntonnesofCO2eqemissions1

Thisrepresents2-3%ofKenya’sannualGHGemissionsand10%ofKenya’s2030GHGreductiongoal2

20

RecentinnovationsenableBio-ethanoltoundercutdirtyfuelsandquicklyscale

Source:KOKONetworks

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

“V2.0SmartFuelATM”approachleveragestechnologyanddownstreamfuelsinfrastructuretoremoveover50%ofsupplychaincostswithinthetraditional“V1.0CentralizedBottling”approach

V1.0CentralizedBottlingApproach

Urbanstorage Packaging Distribution Retail Userexperience

Paymentsandtracking

Cashandclipboards;stockon

consignment,leadingtostockouts

100%digitalpayments;automatedinventory

management

Safelydockreusable,valve-

controlledcanisterwithATM&stove

Nospillage,noplasticwaste

FuelATMsinsideshopswithlowfuels-

industrymarginsforshopkeepers

Smallretrofittedfueltankersforlast-mile,slashinglogisticscosts

Zerorecurringpackagingcosts

asfueldistributedinbulkform

Distributedstorageincustomisedtanksat

existingpetrolstations

Pourfrombottle;wipeupspillage;discard

bottle

Smallshops&highfast-moving

consumergoods(FMCG)

industrymargins

Low-capacitytrucks

transportingbottlesfromcentralfacilityandacross

longdistances

Expensive,thickplastic

disposablebottles

Large,centralized

bottlingfacility

V2.0SmartFuelATMNetworkApproach

21

V2.0approachenablesBio-ethanoltonowscalecompetitivelywithotherfuels

Source:(1)BusinessDailyAfrica,“MorepainforpoorascharcoalpriceitsSh2,500abag”,2018;(2)BusinessDaily,“GasPricesFallbyOverSh600in2015”;(3)TimetricLPGdata2018;(4)KOKONetworkspricingdata2018;(6)Basedon3,500MJperHHperyear–thisisatriangulatedfigurebasedon:WorldBankDevelopmentResearchGroup,“HouseholdCookingFuelChoiceandAdoptionofImprovedCookstovesinDevelopingCountries”,2014;UniversityofNairobiandPlankInstituteforChemistry,“BiofuelconsumptionratesandpatternsinKenya”,2002;O’SullivanandBarnes,“EnergyPoliciesandMultiptopicHouseholdSurveys,2007;DalbergNairobifuelhouseholdsurvey2018(7)StovepricesfromDalbergfieldresearch

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

Charcoal Kerosene LPG Bio-ethanolV1.0 Bio-ethanolV2.0

Fuelretailprice

$0.30-$0.45/kg1

$0.75-$0.85/L2

$1.70-1.75/kgfor6kg,13kgcylinders,

>$3.00/kgforPAYGLPG3

$0.90-$1.10/LwithsmallvolumesofKenyanfuel>$1.48atlarge

scalewithimportedBio-ethanol4

$0.85/LsustainableatscalewithimportedBio-ethanol,including$0.21/LofVATand

importtariffs4

AnnualcookingcostforaverageNairobiHH6 $207-249 $224 $233

$234–297(withlocally-producedBio-ethanol)

$385(atscalew/importedBio-ethanol*)

$220-230

Stoveretailprice7

$7KCJ,$25-35Burn/

Envirofit

$6-$20

$40-50for1-burner,$100-120for2-burner(incl.hose,regulator,cylinderdeposit)

$50-$70for2burnerstove(SAFI,Dometic)

$45for2burnerand$30for1-burner

(KOKO)

“V1.0CentralizedBottling”approachhasdifficultycompetingatscale,oncelimitedvolumesofKenyanBio-ethanolareabsorbedandimportsarerequired“V2.0SmartFuelATM”approachdeliverscostsavingsthatareacriticalenablerofscale.

22

V2.0CaseStudy:VivoEnergyKenyausesKOKOtechnologiestosafelyadda4thlineofliquidfuelstoitsexistinginfrastructureandincreaseitsreach

Source:KOKONetworks

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

VivosourcesandstoresbothdomesticBio-ethanolandforeignimports,usingKOKOtechnologiestoensurevisibilityoffuelflows§ Bio-ethanolisstoredindedicated

undergroundtanksaturbanpetrolstations

§ StationsinstallKOKO’sSmartDepotSystemtocontrolandmanagefuelflows

VivoMicroTankersequippedwithKOKO’sSmartTankerSystemperformlast-miledeliverytoKOKOpointFuelATMslocatedinneighbourhoodshops§ KOKOpointsarerefueledviaasecure

externalrefillingbox,locatedontheoutsideoftheshop

§ Avaporrecoverylineensuresnoescapeofvaporatanypoint–allvaporissafelytransferredbacktotheVivoservicestation

KOKOtechnologiescapturedataacrossthefuelsupplychainandfacilitatepayments

§ KOKO’sNetworkOperationsCentreensurescompletevisibilityandcontrolacrossthefuelsupplychain

§ KOKOpointsensorstransmittechnicalhealth,safety,inventoryandtransactioninformationinreal-time

§ KOKOSettlement&PaymentsSystemautomatesandde-riskspaymentflowsbetweenVivoandretailers

23

V2.0CaseStudy:Leveragingsalespoints,andmobile/cloudtech,KOKO’smodeldeliversfuelcloserandmorecheaplytocustomers

Source:KOKONetworks

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

KOKOpointsaredeployeddenselyacrossthecity,insideneighbourhoodshopsandconveniencestores§ KOKOpointsarelocatedwithina

shortwalkoftargethouseholds.§ ShopkeepersbecomeKOKOAgents,

withKOKOpointinstalledinshopunderfranchiseagreement.

AtaKOKOpoint,customersorderstovesandusetheirreusable“smart-valve”canistertosafelypurchasefuel§ NewcustomerordersanBio-ethanol

stove(1-or2-burner)fromlocalKOKOpointorviamobile

§ Stoveandcanisterarereadyforcustomercollectionthenextday

§ Customerspre-payandtop-upKOKOaccountusingmobilemoney–entiresystemiscashless

§ Vapor-tight“smart-valve”systemensuresthatfuelcanonlybeobtainedfromaKOKOpointoraddedtoastovewiththecanister

KOKOpointsyncstocustomer’sKOKOaccountandallowspurchasesofaslittleas~350mL§ Chipinsidecanisterinstantly

recognisescustomerdetails,synchingwithcustomer’sKOKOaccount

§ KOKO’sdispenser-baseddistributionmodelallowscustomerstobuyfuelfromaslittleasKES30/bundle(~350ml)

§ Customerselectsfuelvolumetobuy;nopenaltyforbuyingsmalleramount

24

V2.0innovationsmeanthatBio-ethanolcanbedeliveredatscaletothecustomeratapriceupto~40%lessthantheV1.0approach

Source:KOKOnetworks,expertinterviews.

SupplychainmarginsforBio-ethanol(%oftotalcost)

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

0.35 0.35

0.29

0.210.84

0.29

1.48

V1.0CentralizedBottling

V2.0SmartFuelATMs

0.85

-43%

LandedSupplyCostLogistics,Distribution,andRetailTaxes

Bio-ethanolV2.0costsaresignificantlylowerthanthoseofBio-ethanolV1.0

• Leveragingexistingdownstreaminfrastructurecancutdownbulkstorageandtransportcostsby~90%

• Technology-enableddistributioncanreducecombineddistributionandretailcostsby~45%

• Asidefromlandedsupplycost,taxesdrivetheretailpriceofBio-ethanolV2.0

25

Bio-ethanolV2.0canbescaledwithsignificantlylowercapitalexpenditurethanrequiredforscalingLPG

Note:Terminalincludes:LPG:terminalcapacityincrease,Bio-ethanol:fuelslinesfromshiptoport.Source:(1)KOKONetworksbusinessmodelassumptions,expertinterviews;(2)GLPGKenyaMarketAssessment,2013.

Incrementalinvestmentrequiredtoextendsupplyto2millionadditionalHHsinurbanKenya,(USDmillion)

SectionIII:P

oten

tialofB

io-ethan

olfo

rcoo

kinginKen

ya

Terminal Bulkstorageandtransport

Trucks

Tankers

Depotsandfillingplants

Cylinders

Lastmiledistribution

Total

27

98

164 290

Retailpoints

Terminal Bulkstorageandtransport

Lastmiledistribution

Micro-tankers

Total

0.05 0.08

1616

LPG2

CapexrequirementforscalingLPGinKenyais18xthatofBio-ethanolV2.0model

Bio-ethanol1

26

SectionIV:Bio-ethanolpolicyanalysisBio-ethanolisascalablecleanfueloption–especiallyusinglatesttechnologies–buttaxationisaffectingcustomers’abilitytoaccessfuelatlowestpossiblecost• GiventhelimitedlocalproductionoftechnicalBio-ethanol,importswillbenecessarytomeetthepotentialdemandintheshort-tomedium-term

• Only1.8mLofviabletechnicalBio-ethanolareproducedKenyaversusapotentialdemandof~120mnLinNairobialone• TechnicalBio-ethanolfaces16%inVATand25%indutiescomparedto0%formostotherfuels,withtheexceptionofkerosene,whichfacesa9%exciseduty;thisinflatesthecostatwhichBio-ethanolcookingfuelcanbesoldtocustomers

• Infact,Kenyaranksbelowothersub-SaharanAfricancountriesintermsofBio-ethanol-friendlypolicy,withcombineddutiesandVATof41%forBio-ethanol,vs.anaverageof33%for21sub-SaharanAfricancountriesforwhichdatawasavailable

• Thesetaxesandtariffsnowdrive~25%ofBio-ethanolretailpriceInthelongrun,Bio-ethanolcouldbeproducedlocallyafterfirstprovingdemandusingimports• Scalingthelocalindustrywillrequireaphasedapproachaspotentialinvestors(i.e.,thoselikelytoprovidetheprojectfinancetobuildmorededicatedBio-ethanolplantsinKenya)willwanttoseeatrack-recordofdemand

• Oncethisdemandisunlockedwithareliablesupplyofimports,domesticproductionwillfollowtoserveit

TaxconcessionswouldaccelerateunlockingtheBio-ethanolcookingfuelopportunitybylevellingtheplayingfieldandmakingpricesmorecompetitive• LevellingtheplayingfieldbygrantingdenaturedtechnicalalcoholaVAT-zeroratingandeliminatingrelatedtariffswouldmakeBio-ethanolfuelthecheapestoption,providingKenyanswithanaffordablealternativetotraditionalfuelsanddeliveringuptoaUSD60mnsavingtocustomersannually

• PlanstoincreasetaxesonkeroseneandrecentspikesinlocalKenyancharcoalpricesduetolocalloggingbansreinforcetheneedforcheaperalternativesforthelowestincomeusers

Note:statisticsrepeatedandsourcedonfollowingpages.MoredetailedimpactanalysiscontainedinAppendixB

SectionIV:B

io-ethan

olpolicyan

alysis

27

GiventhelimitedlocalproductionoftechnicalBio-ethanol,importswillbenecessarytomeetthepotentialdemandintheshort-tomedium-term

(1)Accountsfor3-5%oftotalethanolproductionfromthetopthreeethanolplantsinKenya(2)AssumesfulltransitionawayfromcharcoalandkerosenetoBio-ethanolasaprimarycookingfuelforthetop50%householdsbyincomeSource:KOKONetworks;Dalberganalysis

Bio-ethanolvolumesinKenya(millionlitersperyear)

BuildingupthelocalindustryforindustrialBio-ethanolwouldrequirefirstunlockingdemand;taxconcessionscouldfacilitatethisbyallowingKenyancustomersto

purchaseBio-ethanolatpriceslowerthancharcoalandkerosene

114.8

53.2

116.6

Totalethanolproduction

High-gradeethanol

production

1.8

55

Supplygapforproducingcookingfuel

Addressablemarketforethanol

cookingfuel(Nairobi)

Technicalethanol

production

Currently,mostoftheBio-ethanolproducedlocallyishigh-gradeBio-ethanolusedbythebeverageindustry,andnotforcooking;at1.8million1litersoflocaltechnicalBio-ethanolproduction,only~1.5%ofjustNairobi’spotentialaddressablemarket2wouldbeserved

SectionIV:B

io-ethan

olpolicyan

alysis

28Note:(1)MostcharcoalconsumedinNairobiissuppliedthroughinformalmarketshencevirtuallynotariffortaxesarecollected(2)Basedon7.25KESexcisedutychargedonaliterofkerosene(3)KOKONetworksretailanalysisSource:PetroleumInstituteofEastAfrica;WorldIntegratedTradeSolution;PwC,OverviewofVATinAfrica

FUEL Effectiveduty EffectiveVAT

Charcoal N/A N/A1

LPG 0% 0%

Kerosene 9%2 0%

DenaturedtechnicalBio-ethanol 25% 16%

KenyandutyandVATratesforcookingfuels

Bio-ethanolisatamajordisadvantagecomparedtotherestofthefuelsector;duty+VATrepresents25%oftheretailpricetothecustomer3

DutyandVATfordenaturedtechnicalBio-ethanolimportsaremuchhigherthanthoseappliedtoothercookingfuels

SectionIV:B

io-ethan

olpolicyan

alysis

29

Infact,KenyaranksbelowotherSub-SaharanAfricancountriesintermsofBio-ethanol-friendlypolicy

Source:WTO,mostrecentdataasofApril,2018forproduct220720-ethylalcoholandotherspirits,denatured,anystrength;PwCOverviewofVATinAfrica

DutyandtaxburdenonimporteddenaturedBio-ethanolSubsetof21SSAnations,reflectingduties+taxes,%

SectionIV:B

io-ethan

olpolicyan

alysis

Ghana

Benin

SierraLeone

35

Nigeria

Zambia

Uganda

Burundi

DRC

BurkinaFasoCoteD’Ivoire

Algeria

Kenya

MaliSenegalAngola

MozambiqueCongo

10

Cameroon

20

Madagascar

43RwandaTanzania 43

2126

2828282828

30

3739394041

43

4349

ImporttariffVAT

30

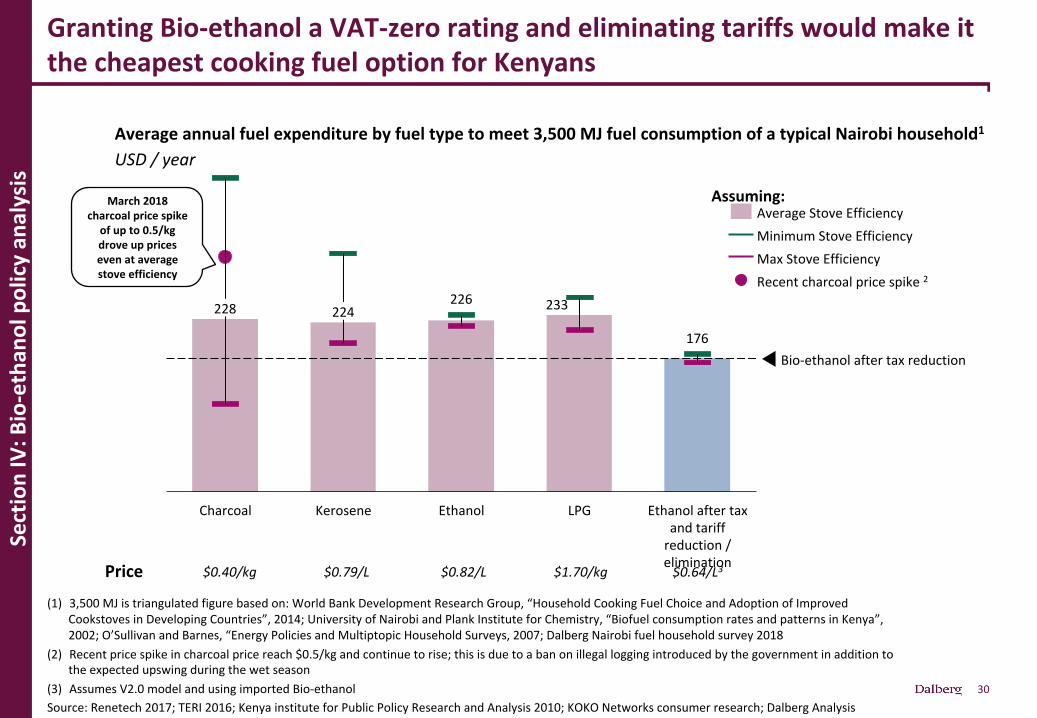

GrantingBio-ethanolaVAT-zeroratingandeliminatingtariffswouldmakeitthecheapestcookingfueloptionforKenyans

(1) 3,500MJistriangulatedfigurebasedon:WorldBankDevelopmentResearchGroup,“HouseholdCookingFuelChoiceandAdoptionofImprovedCookstovesinDevelopingCountries”,2014;UniversityofNairobiandPlankInstituteforChemistry,“BiofuelconsumptionratesandpatternsinKenya”,2002;O’SullivanandBarnes,“EnergyPoliciesandMultiptopicHouseholdSurveys,2007;DalbergNairobifuelhouseholdsurvey2018

(2) Recentpricespikeincharcoalpricereach$0.5/kgandcontinuetorise;thisisduetoabanonillegalloggingintroducedbythegovernmentinadditiontotheexpectedupswingduringthewetseason

(3) AssumesV2.0modelandusingimportedBio-ethanolSource:Renetech2017;TERI2016;KenyainstituteforPublicPolicyResearchandAnalysis2010;KOKONetworksconsumerresearch;DalbergAnalysis

Averageannualfuelexpenditurebyfueltypetomeet3,500MJfuelconsumptionofatypicalNairobihousehold1

USD/year

$0.64/L3

Charcoal

226

LPGKerosene

224228

176

233

Ethanol

Bio-ethanolaftertaxreduction

Ethanolaftertaxandtariffreduction/elimination

MinimumStoveEfficiency

Recentcharcoalpricespike2MaxStoveEfficiency

AverageStoveEfficiencyAssuming:

$1.70/kg$0.82/L$0.79/L$0.40/kgPrice

March2018charcoalpricespikeofupto0.5/kgdroveuppricesevenataveragestoveefficiency

SectionIV:B

io-ethan

olpolicyan

alysis

31

ThisreductionintaxesandtariffscouldleadtosavingsofuptoUSD60mnperyearforconsumersinNairobi,iftheyswitchtoBio-ethanol

Assumptions:100%ofpoorest,middleandupperincomecharcoalandkeroseneusersswitchtoBio-ethanol;noLPGusersswitchtoBio-ethanolinlower,middleorwealthiest–theseestimatesarethereforetheupperlimittosavingsSource:(1)Householdsegmentationbasedonatriangulationof:KenyaPopulationandHousingCensus2009;KenyaNationalBureauofStatistics,“FinAccessHouseholdSurvey”and“KenyaIntegratedHouseholdBudgetSurvey,2016;KenyaDalbergNairobihouseholdsurvey2016;KOKOhouseholdsurvey2017

3mn

Poorest50% Middle30% Upper20% Total

60mn

40mn17mn

Aggregatehouseholdsavingsbyincomesegmentwith100%charcoalandkerosenehouseholdsswitchingtoBio-ethanol1USDperyear NewBio-ethanolprice:USD0.64/L

<$200/month $200–500/month >$500/month

PoorestincomeHHcouldsaveupto$60peryearbyswitchingcompletely

toBio-ethanol

MiddleincomeHHcouldsaveupto$50peryearbyswitchingcompletely

toBio-ethanol

SectionIV:B

io-ethan

olpolicyan

alysis

32

ProvingthestrengthofurbanmarketswillunlocktheconditionstogrowadomesticBio-ethanolindustryovermediumtolongtermtomeetdemand

Source:Expertinterviews

• Proofofdomesticmarketestablishedthroughloweringoftradebarriers

• FulldemandforBio-ethanolsatisfiedthroughimports(e.g.fromSudan,Mauritius,Pakistan)

• Governmentidentifyinglandfordomesticproduction

• Growthoflocalfarmersandprocessingplants

• GovernmenttoincentivizingprivatesectorinvestmentinsmallholderfarmsfornewBio-ethanolcrops,andencourageefficientuseofwastedmolasses

• Public/privatedevelopmentoflogisticsnetworksfordistribution

• EstablishedKenyanBio-ethanolproduction

• FarmersgrowingBio-ethanolcropsandnetworkoffactoriesprocessingcrops

• GovernmentcreatesregionalBio-ethanolexportstrategy,afterprovingdomesticsuccessandscalability

Activ

ities

FullimportsofBio-et

hanolModerate

domestic

production;stil

lheavy

relianceonimports

Fulldomesticp

roduction

withexcessex

ported

SectionIV:B

io-ethan

olpolicyan

alysis

TheKenyanbeveragealcoholmarketisagoodexampleofhowimportswereusedtoprovelatentdemand;oncethiswasclear,localmolassesproducersbuiltBio-ethanolplantsinordertoservethebeveragemarket.NowtherearethreeBio-ethanolproducersinKenya,producing

50mnlitersannuallyandexportingtoUgandaandTanzania

33

RisksoftenassociatedwithBio-ethanolareoverstated;infact,thecookingBio-ethanolindustrycandriveeconomicgrowthinKenya

Source:(1)LightingAfrica,“Kerosene-freeKenya”,2012;(2)Ndegwaetal,“PotentialforBiofuelFeedstockinKenya”,2011;(3)ExpertinterviewsandDalberganalysis

NegativeimpactofBio-ethanolproductiononfoodsecurityhasnotbeenobservedinothercases;inKenya,<1%ofarablelandwouldberequiredforBio-ethanolproduction2

Foodsecurity Charcoalproductiondepletesnon-renewableforests,leadingtolanddegradation;reducingcharcoalusecouldactuallyenhancefoodsecurity

Jobs Jobslostinthecharcoalindustryarelowquality,lowpaying,andhighlyseasonalandlikelytobelostanyway,givengovernment’sgoalstocurbcharcoalproduction

AdomesticBio-ethanolindustryserving500,000customerscouldcreate40-70Knewjobs,generatingUSD17-35mninincrementalincomes2

Tradebalance InitialnegativeimpactofimportedBio-ethanolwilldecreaseasdomesticproductiondevelops

Inthefuture,domesticallyproducedBio-ethanolcouldreplaceimportedkerosene,improvingthetradebalance;KenyacouldonedaybearegionalnetexporterofBio-ethanol

Taxrevenue Largestpotentialnegativetaximpact–revenueslostfromkeroseneimports–willhappenregardless,sincegovernmentadvocatingaKeroseneFreeKenya1

DomesticBio-ethanolproductionwillcreateformal,incometax-payingjobs

PotentialrisksassociatedwithBio-ethanolareoftenoverstatedandlargelyaddressable

Infact,Bio-ethanolusepresentsopportunitiestostrengthentheKenyaneconomy

SectionIV:B

io-ethan

olpolicyan

alysis

34

SectionV:Conclusions

SectionV:Con

clusions

1. Ultimately,thedesiredoutcomeunderlyingthisreportisthatKenyanconsumershaveaccesstosafeandcleancookingfueloptionsatthelowestpossiblecost

2. Today,thereareviablecleancookingfueloptionsthatcanservetheKenyanpopulationcurrentlypayingfortheirfuel–theseusersareconcentratedinurbanKenya

3. Bio-ethanolandLPGareindisputablycleanerandsaferoptionsthancharcoal,kerosene,andfirewood–betterforKenyansandbetterfortheenvironmentasawhole

4. UseofLPGhassuccessfullyexpandedanditremainsakeysolution;now,Bio-ethanoltooiswell-positionedtobeamass-marketsolutionforurbanKenya

5. TheGoKandotherstakeholdershavebeenproactiveinpromotingcleanfuels;thereremainopportunitiestofurthereliminatebarrierstodriveadoptionofcleanfuels

6. Bio-ethanoldeliversequivalenthealthandenvironmentalbenefitsasLPG,anditcannowbedistributedatpricesaffordabletolowerandmiddleincomeKenyans

7. InorderfortheBio-ethanolopportunitytobefullyrealized,thereneedstobealevelplayingfieldtocompetewithothercookingfuels;specifically,VATandimporttariffsneedtobeeliminatedtoreducetheendcosttoKenyanconsumers

35

ComparisonofprimarycookingfueloptionsinUrbanKenya

Note:PM2.5exposureandGHGemissionsfiguresdependoncombinationoffuelandstoveused;however,conclusionsheartakeintoconsiderationtherangeoflikelycombinations.Source:Expertinterviews

SectionV:Con

clusionsand

Recom

men

datio

ns

Impa

cts

Affo

rdab

ility

/ ac

cess

ibili

ty

Pote

ntia

l fo

r sca

le

Charcoal Kerosene Bio-ethanol

• HighestPM2.5exposureandGHGemissions

• Keydriverofdeforestationand,consequently,foodinsecurity

• HighPM2.5exposure• LowerGHGemissions

thancharcoal,butstillhigher

• Safetyconcerns(firesandburns)

• Negativeimpactontradebalancegivenimports

• LowPM2.5exposure• LowestGHGemissions• Domesticproductionand

jobcreationopportunity• Shorter-termnegative

impactontradebalancegivenimports(untildomesticindustrygrows)

• LowestPM2.5exposure• LowGHGemissions• Negativeimpactontrade

balance

• Cheapestperunitprice• Annualcostofcooking

variesbasedonstoveefficiency;historicallylowonaveragethoughnowathighpoint

• Relativelylowupfrontstovecost

• Widelyavailablethroughoutmass-marketneighborhoodsathyper-localdistributionpoints

• Lowestannualcostofcooking

• Lowupfrontstovecost

• Notwell-understood;lowconsumerawareness

• Comparableannualcostofcookingtocharcoal;pricesinflatedbydisproportionatetaxes

• Relativelyhighupfrontstovecostvs.baselinecharcoal(competitivevs.cleanfuelalternatives)

• Highconsumerawareness• Availabilityconstrained

outsideofNairobi,butaccesshighincapital

• Highestpriceandannualcostofcooking

• Highestupfrontstovecost

• Alreadyavailableatscale • Alreadyavailableatscale • Recentinnovationshavereducedcapitalrequiredtoscale

• Highestcapitalexpendituresrequiredforscale

LPG

36

RecommendedpolicychangesforscalingupcleancookinginurbanKenya

GrantdenaturedBio-ethanolfuelaVAT-zerorating

Removeimportdutiesand

additionaltaxesonBio-ethanolfuelandappliances

Establishandenforcesafetyandqualitystandardsthroughregulatory

bodies

1 2 3

Themostcost-efficientandimpactfulwayforGoKtoscaleupcleancookingistoleveltheplayingfieldforemergingBio-ethanolwithLPG,increasingavailabilityandaffordabilityofcleancookingsolutionstoconsumers.Thespecificpolicyrecommendationsbasedonthisstudyare:

SectionV:Con

clusionsand

Recom

men

datio

ns

37

APPENDIXA:CookingFuelOptionsintheKenyanMarketB:PotentialofBio-ethanolforCookinginKenyaC:Bio-ethanolPolicyAssessmentD:RisksandOpportunities

38

Appendix

A:CookingFuelOptionsintheKenyanMarket

B:PotentialofBio-ethanolforCookinginKenya

C:Bio-ethanolPolicyAssessment

D:RisksandOpportunities

39

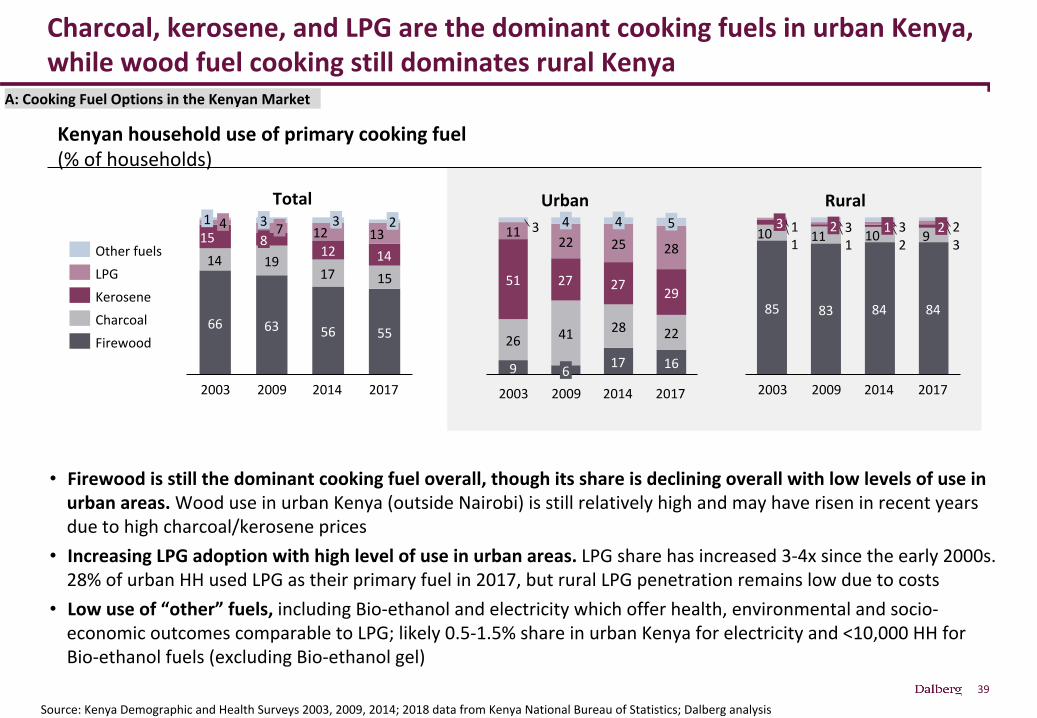

Charcoal,kerosene,andLPGarethedominantcookingfuelsinurbanKenya,whilewoodfuelcookingstilldominatesruralKenya

Source:KenyaDemographicandHealthSurveys2003,2009,2014;2018datafromKenyaNationalBureauofStatistics;Dalberganalysis

66 63 56 55

14 1917 15

1512 14

12 13841

2003

3 37

2009 2014

2

2017

LPGOtherfuels

CharcoalKerosene

Firewood

9 17 1626 41 28 22

51 27 27 29

1122 25 28

3

20142003

54

62009

4

2017

85 83 84 84

10 11 10 91 1 2 31 3 3 2

2003 20142009

23 1 2

2017

Urban RuralTotal

Kenyanhouseholduseofprimarycookingfuel(%ofhouseholds)

• Firewoodisstillthedominantcookingfueloverall,thoughitsshareisdecliningoverallwithlowlevelsofuseinurbanareas.WooduseinurbanKenya(outsideNairobi)isstillrelativelyhighandmayhaveriseninrecentyearsduetohighcharcoal/keroseneprices

• IncreasingLPGadoptionwithhighlevelofuseinurbanareas.LPGsharehasincreased3-4xsincetheearly2000s.28%ofurbanHHusedLPGastheirprimaryfuelin2017,butruralLPGpenetrationremainslowduetocosts

• Lowuseof“other”fuels,includingBio-ethanolandelectricitywhichofferhealth,environmentalandsocio-economicoutcomescomparabletoLPG;likely0.5-1.5%shareinurbanKenyaforelectricityand<10,000HHforBio-ethanolfuels(excludingBio-ethanolgel)

A:CookingFuelOptionsintheKenyanMarket

40

FuelstackingisawidespreadphenomenoninKenya;useofcharcoalandkerosenearemuchmorecommonthanprimarycookingfueldataindicate

Source:DalbergproprietaryKenyaenergyaccesssurvey,N=300(2015);smallsamplesizeleadtolowerconfidencelevelfordata,butinsightsdirectionallycorrectinthecaseofstove/fuelstackingpatterns

AllKenya–anyuseoffuelvs.primarycookingfuel(%oftotalHH,N=300,Dalberg2015survey)

UrbanKenya–anyuseoffuelvs.primarycookingfuel(%oftotalHH,N=~100,Dalberg2015survey)

KeroseneFirewoodCharcoal LPG

78%

24%

41%32%

47%

10%

29%23%

AnycookingfueluseMaincookingfuel

55%

Charcoal KeroseneFirewood

65%

LPG

26%

69%

35%

10%8%15%

A:CookingFuelOptionsintheKenyanMarket

41

LPGandkerosenedominateasprimarycookingfuelsinNairobi

Source:(1)KenyaNationalBureauofStatisticsfuelsurvey(2018,using2017data);(2)MundietalMPDI/Toxics,APHRC(2016);(3)DalbergandKokoNetworksfieldresearch;(4)https://www.ncbi.nlm.nih.gov/pubmed/29051417andhttps://www.researchgate.net/publication/279375156_A_Choice_Experiment_Study_on_Fuel_Preference_of_Kibera_Slum_Households_in_Kenya

• KeroseneandLPGaretheprimarycookingfuelinNairobioverall,withlowprimaryusageofcharcoal;useishighlydependentonincomelevelwithtop25-30%ofincomedistributionusingLPGalmostexclusivelyandnext20-30%usingamixofLPGwithcharcoalandkerosene;therestonlyuseLPGatlowlevelsduetoaffordability3

• ThelowermiddleoftheNairobiincomedistribution(30-40%ofHH)primarilyusekeroseneandmixwithcharcoalforthebulkoftheirday-to-daycookingneeds3

• Keroseneisthedominantfuelforthepoorest(15-20%)householdsinNairobiwhousekerosenealmostexclusivelyorinparallelwithalowlevelofcharcoalasasecondarycookingfuel4

• MajorityofHHengageinfuelstackingandcharcoalisthemostcommonsecondaryfuelacrossallincomelevelsasidefromthemostwealthygivenubiquityacrossNairobiandaculturalpreferenceforcharcoalcookingfordishes(e.g.,meatgrilling)

Charcoal/keroseneareprimaryNairobicookingfuel(2018)1(%oftotalHH,N=11,415KenyaHHself-reportedprimaryfuel)

Charcoal+KeroseneareprimarycookingfuelsforNairobipoor(%ofHH,n=1000inKorogocho&ViwandanislumsinNairobi,2016)2

55%

16%

14%

29%47%

15%

22%

13%28%

44%

5%

3%AllKenya UrbanKenya

5% 1%3%Nairobi

Kerosene Charcoal

72%

LPG

18%

94%76%

26%12%

Usestove/fuelCommonlyusestove/fuel

CharcoalLPG

FirewoodKerosene

Other

A:CookingFuelOptionsintheKenyanMarket

42

Charcoalisparticularlyharmfulasitcontributesmoretohouseholdairpollution,GHGemissions,anddeforestationthanotherfuels

Source:DalbergimpactsizingmodelforruralKenya,2018;HouseholdAirPollutionInterventionTool,withcustomizedinputsforNairobibasedrespectiveswitchingtoLPGandethanolconsumption.

Wood Charcoal Kerosene

Health • DeathsandDALYsduetohouseholdairpollutionfromPM2.5

• Qualityoflifediminutionduetootherhardtoquantifyhealtheffects(eyeirritation,cataracts,childmalnutrition)

~2kavoidabledeaths,165kaDALYs

• DeathsandDALYsduetohouseholdairpollutionfromPM2.5

• Qualityoflifediminutionduetootherhardtoquantifyhealtheffects(eyeirritation,cataracts,childmalnutrition)

~3kavoidabledeaths,~250kaDALYs

• DeathsandDALYsduetohouseholdairpollutionfromPM2.5

• Incrementalunquantifiedkerosenehealthharms(e.g.,cancersfrompolycyclicaromatichydrocarbons)

• Poisoningsandburns,particularlyforwomenandkids(e.g.,40-60%ofpediatricpoisoningcasesinKenyaduetokerosene)~2-3kavoidabledeaths,~160kaDALYs

Environment&Climatecosts

• GHG(CO2,BlackCarbon,otherglobalwarmingKyotoParticles)

• Contributortodeforestationand,consequently,foodinsecurity

2.5-4.4tCO2eq/urbanHHannually

• VeryhighGHGemissionsperhousehold(CO2,BlackCarbon,otherglobalwarmingKyotoParticlesfromcharcoalproductionanduse)

• Substantialdriverofdeforestationand,consequently,foodinsecurity

• Negativeimpactsonfoodsecurityduetoforestloss

3.6-5tCO2eq/urbanHHannually

• RelativelylowGHGemissionsperHHbutstill2-3xhigherthanfortrulycleanfuelslikeLPGandBio-ethanol

1tCO2eq/urbanHHannually

Socialopportunitycosts

• Timeopportunitycost(timepoverty)duetofuelcollection,slowercookingtimes,needtocleanupcharredcookingpotsandpans

0.8-1.3avoidablehrsperdayperurbanHH

• Timeopportunitycost(timepoverty)duetoslowercookingtimes,needtocleanupcharredcookingpots/pans,

0.3-0.4avoidablehrsperdayperurbanHH

• Notimepovertyeffectsvs.alternatives• Propertydamagefromurbanfiresdueto

kerosenecooking

Notimepovertyimpact

Householdeconomicsandmacro-economiceffects

• Foregoneincomesduetoavoidabletimespentcooking/cleaning

• Taxrevenuelossforgovernmentgiveninformalityofmarket

• Foregoneincomesduetoavoidabletimespentcookingandcleaning

• Avoidablespendingonrelativeinefficientandhigh-costcookingfuel

• Taxrevenuelossforgovernmentgiveninformalityofmarket

• Negativebalanceofpaymentseffectsduetokeroseneimports

A:CookingFuelOptionsintheKenyanMarket

43

Appendix

A:CookingFuelOptionsintheKenyanMarket

B:PotentialofBio-ethanolforCookinginKenya

C:Bio-ethanolPolicyAssessment

D:RisksandOpportunities

44

ThusfarlittleattentionhasbeenpaidtoBio-ethanolasacleanandeasy-to-usecookingfuelfortheKenyanpopulation

Source:KOKOcustomersurvey2017;Dalberganalysis

• Lowcosts:LowerupfrontcoststhanLPG,andsimilarongoingfuelcosttoLPGandkerosene,despiteVATandimporttariffsbeingleviedonBio-ethanolonly

• Affordablebundles:Bio-ethanolcanbesoldinsmall“refillbundles”,criticaltoservinglower-income“kidogoeconomy”segments

• Clean:Bio-ethanolburnscleanlywithlowparticulateemissions,likeLPG

• Sustainable:Unlikefirewoodandcharcoal,Bio-ethanolcanbeproducedsustainablyinKenya

Bio-ethanolisaviableandscalablealternativecookingfuel

B:PotentialofBio-ethanolforCookinginKenya

45

V2.0CaseStudy:Leveragingsalespoints,andmobile/cloudtech,KOKO’smodeldeliversfuelcloserandmorecheaplytocustomers

Source:KOKONetworks

§ Customersmakeupfrontpurchaseof1-or2-burnerBio-ethanolstove,alongwithreusable‘SmartCanister’.

§ KOKO'sproductofferingprovidesconsumerswithanaffordably-pricedmoderncleancookingsolution.

§ Stovescanbepurchasedwithfullamountpaidupfront,orvialayaway/savingsprogrammewherebysmallerdepositsmadeovertime(nodifferencetoprice).

§ Vapor-tight“smart-valve”systemensuresthatthecanisteristheonlywaytoobtainfuelfromaKOKOpoint,ortoaddfueltostove.

§ Dockingandvalvesystemensuresthatatnopointisthecustomerexposedtothefuelitself.

§ Optionalcustomersmartphoneappallowscustomerstomanageaccounts,shareKOKOcreditandearnmoneybysigningupfriendsandfamilymembers.

§ Referralprogrammeincentivisedthroughfuelcreditandsubsequentlythroughdirectmobilemoneypaymentsforbestcustomerpromoters.

B:PotentialofBio-ethanolforCookinginKenya

46

Impactmodellingmethodology

AnalysisconductedforNairobi

*Wehaveusedlabdatahere(despiteitsshortcomings)duetoabsenceofreliablereal-worlddatathatcontrolsforimpactofambientpollution**ThisretailpriceassumeszeroVATratingandnoimporttariffs

Changeinconsumptionofdifferentfuels

whenmovingfrombaselinetofuel

transitionscenario

Forenvironment:differenceinemissionsswitchingfromcharcoalorkerosenetoBio-

ethanol

Forhealth:HAPITmodelcalculationsofDALYsanddeathsavertedbasedon

PM2.5labdata

Forconsumersavings:differenceinspending

assumingthosewhoswitchpurchaseBio-ethanolat

$0.64/L**

Highlevelassumptionsoffuelusemixacrosslow,middle,andhighincome(basedonobservedstacking

behaviourinsurveys)

Perhouseholdassumptionsforper

HHannualfuelconsumption(basedonlabnetcalorific

value,stoveefficiency,and3,500MJperHHannualconsumption)

AnnualGHGemissionsreduced

DALYsanddeathsavertedoverathreeyearperiod

AnnualUSDsavings

B:PotentialofBio-ethanolforCookinginKenya

47

Fuelconsumptionandexpenditureatthehouseholdlevel:calculationandkeyassumptions

Source:LPG:JeulandFuelandStoveSurvey2012(50-60%),Jeuland2016(53%average),GLPGA(55%);KeroseneJeuland2012(25%-40%);Charcoal:GACCKenyacookstovesmarketassessment(12%and20%);BURN(40%);Bio-ethanol:ProjectGAIA2016;all:GACCCookstoveDatabase;Forpricing:KOKONetworksconsumersurveysNov2016toMarch2018,DalbergconsumersurveyFeb2018,expertinterviews

Fuel Netcalorificvalue(MJ/kg)*

Rangeofstoveefficienciesfromliterature

Stoveefficiencyusedforanalysis

Averageannualhouseholdfuelconsumption(assuming3,500MJ/HHannualconsumption)

Pricetoconsumer(USD)

Averageannualcostofcooking(USD)(assuming3,500MJ/HHannualconsumption)

LPG 46.6 50% 60% 55% 137kg 1.70/kg 233

Kerosene 43.1 25% 40% 35% 284L 0.79/L 224

Charcoal 28.2 12% 43% 21.9% 569kg 0.40/kg 228

Bio-ethanol 27.0 58% 62% 60% 275L 0.82/L 226

Annualcostofcooking=AnnualHHfuelconsumptionxunitpricetoconsumer

AnnualHHfuelconsumption=3500MJ/(netcalorificvaluexstoveefficiency)

B:PotentialofBio-ethanolforCookinginKenya

48

Baseline:high-levelfueluseassumptions

Intheabsenceofdetaileddataonprimaryandsecondaryfueluse,wehaveusedhigh-levelestimatesbasedonobservedstackingbehaviorandsimplifiedbyremovingnot

consideringfuelswithnegligibleuse

Note:theseareDalbergestimatesbasedonareviewofvarioussmallersurveys.Moregranularandvalidatedviewsofthisdataarenotpubliclyavailable

Lowincome Middleincome Highincome

Definition <$200/month

$200-500/month $500/month

ShareofHH 50% 20% 30%

#ofHH 687,500 412,500 275,000

LPGuse(%) 0% 20% 60%

Keroseneuse(%) 40% 50% 20%

Charcoal(%) 60% 30% 20%

Bio-ethanol(%) 0% 0% 0%

B:PotentialofBio-ethanolforCookinginKenya

49

Environmentimpact:fuel/stoveemissionsdataassumptions

Note:Charcoal(BasicICS)usedforcharcoalmodellingpurposes.AllKenyadatapointsSource:GACCCookstoveDatabase2017

5,1

3,6

1,9

1,00,5 0,3

LPGstoveKerosenewickstove

Charcoal(BasicICS)

Traditionalcharcoalstove

Charcoal(Intermediate

ICS)

Ethanolstove

TotalCO2eqemissions(Kyotoparticles+BCCO2eq)annuallyforfuel/stovecombinationsinurbanareastonnes/year

B:PotentialofBio-ethanolforCookinginKenya

50

Healthimpact:PM2.5emissionsassumptions

Note:Figuresareaveragesbasedonwiderliteratureandresearchsince,asofMarch2018,nopersonalexposuretestingforallfuelshasoccurredinNairobiSource:LPG:WHOIndoorAirQualityGuidelines;IPCBEEIndiaVolume10;Elsevier“Women’sPersonalandIndoorExposurestoPM2.5inMysore”.Kerosene:“WHOIndoorAirQualityGuidelines:HouseholdFuelCombustion”,2014;Charcoal:WHOIndoorAirQualityGuidelines;CleanCookstoves2015;BerkeleyAirMonitoring2015;GACC2015;ProjectGAIA2010;Firewood:CleanCookstovesTesting2015;Dalbergresearch

160 10050 47

500

LPGFirewood Charcoal Kerosene Ethanol

PM2.5EmissionsbyFuelAveragemicrograms/cubicmetre

B:PotentialofBio-ethanolforCookinginKenya

51

Healthimpact:HAPITcalculations

Note:inreality,personalexposurelevelsofPM2.5varywithe.g.ambientpollutionlevels,ventilationofcookingareainandconditionofstove.IngeneralstudiesfindLPGandBio-ethanoltobehighlycomparableintermsofbeneficialhealtheffectsSource:HAPITmodel–Inputstakethepre-interventionexposuretobebasedonaveragePM2.5databyfuel,andtakethecoutnerfactualexposuretobe10,inlinewiththeHAPITmodel'sdefaultassumptions.AnimportantcaveatforthisdataisthatpersonalexposuretestinginNairobiisminimal,particularlyforBio-ethanol;Data:LPG:WHOIndoorAirQualityGuidelines;IPCBEEIndiaVolume10;Elsevier“Women’sPersonalandIndoorExposurestoPM2.5inMysore”.Kerosene:“WHOIndoorAirQualityGuidelines:HouseholdFuelCombustion”,2014;Charcoal:WHOIndoorAirQualityGuidelines;CleanCookstoves2015;BerkeleyAirMonitoring2015;GACC2015;ProjectGAIA2010;Firewood:CleanCookstovesTesting2015

Impactofcharcoalusersswitching ToLPG ToBio-ethanolDALYsper25,000 6181 6050DALYsperHH 0.25 0.24Deathsavertedper25000 58 52

Impactofkeroseneusersswitchingto: ToLPG ToBio-ethanolDALYsper25,000 2651 2432DALYsperHH 0.11 0.10Deathsavertedper25000 15 12

B:PotentialofBio-ethanolforCookinginKenya

52

Appendix

A:CookingFuelOptionsintheKenyanMarket

B:PotentialofBio-ethanolforCookinginKenya

C:Bio-ethanolPolicyAssessment

D:RisksandOpportunities

53

Withouttaxes/tariffsthe10-yearaveragepriceofBio-ethanolislowerthanthoseofLPGandkerosene,and20%cheaperthancharcoal’stoday

*$198overpastyearassuming$0.40/kgaveragefortinof4kg;inrecentmonthpriceshavespikedupto0.46-.5/kg,0.46/kgyields$226cookingbudgetSource:Renetech2017;TERI2016;KenyainstituteforPublicPolicyResearchandAnalysis2010;KOKONetworksconsumerresearch2017;DalbergAnalysis

Averageannualfuelexpenditurebyfueltypetomeet3,500MJfuelconsumptionofatypicalNairobihousehold1

USD/year

228 224 233 224

176177

231

278 272

203

Ethanolaftertaxandtariffreduction

Charcoal* Kerosene LPG

10yearBio-ethanolavg.onparw/currentcharcoal,lowerthanotherfuels

Ethanol

Bio-ethanolw/otaxandtariffislowest-costoptiontoday

Pastyear10yraverage

310

March2018charcoalpricespike • Bio-ethanolisaglobalcommodity

withpricesthatfluctuateovertimeandinthepasthavebeenupto50%higherthantoday

• However,evenoverlongterm,tax/dutyfreeBio-ethanolwouldhavebeenalowercostfuelvs.LPGandkerosene

• Withtaxesandtariffsremoved,evenifglobalBio-ethanolpricesrevertedtohistoricalmean,Bio-ethanolwouldbecheaperthantoday’scharcoal

• Whilecharcoalhasbeencheaperinthepast,itspricescontinuetotrendupwardsinKenya

C:Bio-ethanolPolicyAssessment

54

RecentspikesinlocalKenyancharcoalpriceshavereinforcedtheneedforcheaperalternativesforthelowestincomeusers

Source:Charcoal(4Kg)pricesfrom2005to2013Q1obtainedfromTimetric,dataasofApr.2013;Dalberganalysis

200820062000

0.5

2002

0.3

0.2

2010

0.7

2004 20142012 2016 20180.0

0.1

0.4

0.6

0.8

Averageannualcharcoalprices2000-2018

2017USD/kg

• Thepriceofcharcoalhasbeentrendingupwardssincemid2005

• Recentincreaseshavebeenevenmoredramaticasaresultoflocalgovernmentcommitmentstocurbillegallogging

• Giventhelowest-incomeKenyans’disproportionatedependenceoncharcoal,theywillbetheonestosufferthemost

Whiletheseconditionsmaybetemporary,thesituationreinforcestheneedforacheaper,cleanerandreliablealternativetocharcoal

C:Bio-ethanolPolicyAssessment

55

Appendix

A:CookingFuelOptionsintheKenyanMarket

B:PotentialofBio-ethanolforCookinginKenya

C:Bio-ethanolPolicyAssessment

D:RisksandOpportunities

56

ThepotentialrisksofcookingBio-ethanoltransitionflaggedbygovernmentstakeholdersinourconsultationsareover-estimatedandlargelyaddressable

Taxrevenue

• ArgumentaroundimpactofBio-ethanolproductiononfoodsecurityisweakandhasnotbeenobservedinothercases

• Kenyahasabundantlandsuitableforsugarcaneproduction,ofwhichonlyasmallpercentage(~1%)wouldbeneededforBio-ethanolproduction3

• Thelandrequirementisevenlowerwhenproductionprocessesaremademoreefficient

Tradebalance

Jobs

Foodsecurity

• Short-termnegativeimpactoncharcoalindustryascharcoaluserssubstituteBio-ethanol• However,thesejobsarelowquality,lowpaying,andhighlyseasonal2• Furthermore,thegovernmentisalreadycurbingproductionofandencouraginguserstoswitchfromcharcoal,sohasalreadyacceptedtherisktothesejobs

• Potentialnegativeimpactof~USD60mnannuallyifallofNairobi’scookingBio-ethanolimported

• Asdomesticproductiondevelops,thiswilldecrease

• LargestpotentialimpactistaxrevenuesfromkeroseneusedforcookingasusersshifttoBio-ethanol;however,thegovernmentisalreadyencouraginguserstoswitchfromkerosene

• TaxrevenuescollectedfromBio-ethanolusedforcookingarenegligibleandcharcoalisuntaxedandoftenproducedinformally1

1

2

3

4

Source:(1)KenyaForestryService,“CharcoalValueChainAnalysis”,2016;(2)ExpertinterviewsandDalberganalysis;(3)Ndegwaetal,“PotentialforBiofuelFeedstockinKenya”,2011;

D:RisksandOpportunities

57

Infact,formostpotentialrisksraised,therearepotentialopportunitiesforstrengtheningtheeconomy

Taxrevenue

• Reducingcharcoalusecouldenhancefoodsecurity• ~90%ofcharcoalforcookingisharvestedfromnon-renewableforests,drivingfoodinsecuritythroughnegativeimpactsonwatercyclesandlanddegradation

Tradebalance

Jobs

Foodsecurity

• DomesticBio-ethanolindustrywilldeliverbetter-paying,formaljobsalongtheBio-ethanolvaluechain,fromfarmerstodistributors

• Dependingonbusinessmodelsadopted,anindustryserving500,000customerscouldcreate40-70Knewjobs,generatingUSD17-35mninincrementalincomes

• Inthefuture,domesticallyproducedBio-ethanolcouldreplaceimportedkerosene,improvingthetradebalance

• Withenoughinvestmentintodomesticproduction,KenyacouldonedaybearegionalnetexporterofBio-ethanol(vs.importsfromSudan,Mauritius,andPakistan)

• DomesticBio-ethanolproductionhasthepotentialtoincreasestaxrevenuesinthelong-runasformal,incometax-payingjobsarecreatedinthedomesticBio-ethanolindustry

1

2

3

4

Source:Ndegwaetal,“PotentialforBiofuelFeedstockinKenya”,2011;PrajIndustries;Dalberganalysis

D:RisksandOpportunities

58

ThegovernmentstandstoloseuptoUSD4.5mnperyearfromforegonekerosenetaxrevenues–butthisisconsistentwiththekerosenecampaign

Source:WorldBankgovernmentdata2015;Kenyantaxandtariffschedule2017;Dalberganalysis

EstimatedyearlytaxrevenuefromfuelimportsMnUSD/year

Mainpotentiallossoftaxrevenuesisfromkeroseneimports;however,thegovernmentisalreadyworkingtocurbtheusekerosene

• Replacingallofthekeroseneestimatedtobeusedforcookingcouldresultinalossofupto$4.5mnperyear

• Lossofkerosenerevenuesisanexpectedoutcomeofthegovernment’sKeroseneFreeKenyacampaigninanycaseandwouldonlyrepresent<0.1%oftaxrevenues

• TaxrevenuescollectedfromBio-ethanolusedforcookingarenegligibleandcharcoalisuntaxedandoftenproducedinformally

4.5

4.5~0.0 ~0.0

CharcoaltaxrevenueEthanoltaxrevenueCookingkeroseneinNairobi

1

EstimatedimportedvolumesforNairobi:~60mnlitresofkeroseneperannum

Taxrevenue

D:RisksandOpportunities

59

Lossofkerosenerevenuesareminimal;whilstinitialbalanceoftradeeffectsofimportedBio-ethanolwillbenegative,adomesticindustrywilllessenthis

(1)Charcoalisnottaxedasislargelyinformal,andthereforenotincludedhereSource:WorldBankgovernmentdata2015;Kenyantaxandtariffschedule2017;Dalberganalysis

LPG

AllNairobiHHstransitiontoimportedLPG

AllNairobiHHstransitiontotax/tarifffreeethanol

Currentbalanceoftrade1

Kerosene-80mn

-30mn-50mn

-320mn

-240mn

EstimatedimportedvolumesforNairobi:125mnlitresofkeroseneand32,000tonnesofLPG/year

BalanceoftradefromNairobicookingfuelsMnUSD/year

2

Whileanegativeimpactonthetradebalanceislikelyintheshort-term,afulltransitiontoBio-ethanolwithouttaxesandtariffswouldhaveasmallerimpactonthetradedeficitthanonetoLPG• Basedonourmodeling,thecurrenttradebalanceforimportingkeroseneandLPGforcookinginNairobiwouldbe(-)~USD180mn/year

• AfulltransitionofNairobihouseholdstoLPGcouldexacerbatethisby~$180mn,whileafulltransitiontoBio-ethanolcouldexacerbatethisby~$240mn

• UnlikewithkeroseneorLPG,thereisacredibleopportunityfordevelopingadomesticBio-ethanolindustry

• Thiswouldimprovethetradebalanceinthelong-runandcouldeventransformKenyaintoanetexporterofBio-ethanol

Tradebalance

D:RisksandOpportunities

60

AnBio-ethanoltransitionwillsupport>70,000jobsandboostincomesacrossvaluechain,particularlyoncedemandfordomesticBio-ethanolisunlocked

39,0 40,0

31,0 33,1

0,2 0,6

Bulkstorageandtransport

0.8

Feedstockproduction

0.5

Lastmiledistribution

SalesEthanolproduction

1.0 0.3

Total

70.0 1.4 73.10.3

PotentialjobscreatedthroughdomesticBio-ethanolproduction000snumberofjobs

Whenmarketreaches500kBio-ethanolcookingcustomers,using54mnlitresoflocallyproducedBio-ethanolperyear,40-70Kjobswouldsupportcookingethanolvaluechain:

• LowerrangeofjobcreationexplainedbypotentialefficienciesinBio-ethanolproductionthatcoulddeliveranadditional30mnlitres1

• Jobswillbedisplacedincharcoalvaluechain,particularlyforcharcoalproducers,butthissamedisplacementwillresultfromthegovernment’sencouragementofatransitiontoLPG

• Furthermore,charcoaljobsarelowquality/incomeandeconomicallyandenvironmentallyunsustainableinthelong-term

Improvedprocesses1

NoimprovedprocessesIdenticalcapacityneeds

PotentialforadomesticindustrythatcreatesjobsisuniqueforBio-ethanolamongalternativefuels

Note:Lastmiledistributionandsalesareunaffectedbyimprovedupstreamproductionprocessesandthereforesameimpactonjobsexpected1MismanagementofBio-ethanolproductionprocessmeansfactoriesrunbelowcapacity;manyprocessingplantsrunatjust25%capacity.Improvedprocessescouldaddupto30mnlitresofdenaturedtechnicalBio-ethanolperyearusingexistingcapacityandinfrastructureSource:PrajIndustries;KOKONetworks;FoodandAgricultureData2017SugarcaneYieldbyCountry;Dalberganalysis

3

Jobs

D:RisksandOpportunities

61

Thiscouldresultinanadditional$35mnofadditionalincome,particularlyforsmallholderfarmersproducingsugarcane

Note:Lastmiledistributionandsalesareunaffectedbyimprovedupstreamproductionprocessesandthereforesameimpactonincomesexpected1MismanagementofBio-ethanolproductionprocessmeansfactoriesrunbelowcapacity;manyprocessingplantsrunatjust25%capacity.Improvedprocessescouldaddupto30mnlitresofdenaturedtechnicalBio-ethanolperyearusingexistingcapacityandinfrastructureSource:PrajIndustries;KOKONetworks;FoodandAgricultureData2017SugarcaneYieldbyCountry;Dalberganalysis

Whenmarketreaches500kBio-ethanolcookingcustomers,using54mnlitresoflocallyproducedBio-ethanolperyear,USD17-35mninincomesandprofitscouldbegenerated

• Thisestimationusesaconservativemedianpriceforsugarcane,asfeedstockincomeswillvarywithcommodityprices

• InthecaseoftheKOKOlastmiledistributionmodel,anadditionalUSD1,000–1,500taxableincomecouldbegeneratedperdistributionpoint,translatingintoatotalofUSD2mn–3mnperyear(assuming2,000distributionpoints)

0.9

Bulkstorageandtransport

17.5

Feedstockproduction

Ethanolproduction

Lastmiledistribution

13.0

3.4

Sales

0.8

Total

24.2

5.734.9

3.2

11.2

1.22.2

2.5

17.4

IdenticalcapacityneedsNoprocessesimprovedProcessesimproved1

PotentialincrementalincomesgeneratedthroughdomesticBio-ethanolproductionUSDmillions

3

Jobs

D:RisksandOpportunities

62

Foodsecurity:Upto30mmlitresofBio-ethanolcouldbeproducedthroughmoreefficientprocesses,whilstKenyahassurpluslandtomeetrequirements

Note:MismanagementofBio-ethanolproductionprocessmeansfactoriesrunbelowcapacity;manyprocessingplantsrunatjust25%capacity.Improvedprocessescouldaddupto30mnlitersofdenaturedtechnicalBio-ethanolperyearusingexistingcapacityandinfrastructureSource:(1)Ndegwaetal,“PotentialforBiofuelFeedstockinKenya”,2011;(2)ExpertinterviewsincludingPrajIndustries

15

12,000

6

Projectedhectaresassumingprocessesimproved2

Projectedhectares

assumingnoimprovementinprocess

Totalsuitablelandforsugarcane

AdditionalhectaresofsugarcanerequiredtomeetpotentialBio-ethanoldemand000shectares

1%oftotalsuitableland

0.5%oftotalsuitableland

DomesticproductionofBio-ethanolcouldevenimprovefoodsecuritybyreducingcharcoal-relateddeforestationandclimatechange,whichreducesagriculturalpotential

4

Atmost,~1%oflandsuitableforplantingsugarcanewouldbeneededtomeettheestimatedBio-ethanoldemandofNairobi1• Additionallandneededwouldnotencroachonlandforfoodorlivestock,asKenyahasabundantviablelandcurrentlynotinuse

• SugarcaneinKenyaisnotusedforfood,andthereforewouldnotredirectgrainsthatcouldbeusedforfood

Foodsecurity

D:RisksandOpportunities

63

Jobsimpactassumptions

Note:Basedonexpertinterviews,mismanagementofBio-ethanolproductionprocessmeansfactoriesrunbelowcapacity;manyprocessingplantsrunatjust25%capacity.Improvedprocessescouldaddupto30mnlitersofdenaturedtechnicalBio-ethanolperyearusingexistingcapacityandinfrastructureSource:(1)FAO,“Economiclivesofsmallholderfarmers”,2015;Humanosphere,“SouringSugarIndustryinKenya”,2017;(3)Calculationbasedonexpertinterviewsandsources(1)and(2)withlandtoproduce1Lofethanol;(4)KOKONetworksprocessingdata;expertinterviewsinclude:PrajIndustries,LakeOil

Item

FullProduction

needsImprovedProcesses

FeedstockproductionAveragesizeofSHF(Ha)1 0.47 0.47Tonnesofsugarcane/hectareofland(T/Ha) 65 65LofBio-ethanol/tonneofsugarcane(L/T)2 75 75LofBio-ethanol/hectareofland(L/Ha) 4875 4875Totalhectaresoflandneeded(Ha)3 11077 4923Average#ofadultsperfarm 3 3AverageSHFrevenue/tonneofsugarcane(USD/tonne) 35 35Averageannualyieldofsugarcane(Tonnes/hectare) 65 65

Bio-ethanolproductionAnnualcapacityoflargeprocessingplants(L) 12,000,000 12,000,000#ofstaff/plant 100 100Monthlyincomeforstaffinplants(USD) 400 400

Item

Fullproduction

needsImprovedprocesses

Bulkstorageandlogistics4

Sizeofstoragefacilities(L) 20,000 20,000Numberofstaffperstoragefacility 0.5 0.5Monthlyincomeforstaffinstoragefacilities(USD) 350 350

Lastmiledistribution4Capacityoftransporttankers(L)4 2000 2000#oftankers 65 65#ofpetrolstations 60 60#ofstaffperpetrolstation 2 2#ofstaffpertanker 2 2Monthlyincomefortransportstaff(USD) 250 250

Sales#ofKOKOpoints 2000 2000#ofagents/KOKOpoint 0.5 0.5IncomeperKP(USD) 150 150

D:RisksandOpportunities

Top Related