Languages

Pages

Legal

SSelected key 2016 and beyond business trends in the luxury industry

January 2016

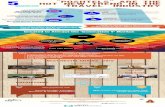

4 key trends in the Luxury industry4 key trends in the Luxury industry

A changing world:A changing world: new growth drivers

in the Luxury industry

1

• Strong reduction in retail expansion: 2/3 of the next decade's growth will be organic

• Opportunities in countries where luxury buying is long-established, with US consumers expected to be the main contributor of future growthy

Intro values still roaring & customers i i l l ki2

• Intro luxury values (quality, exclus., craftsmanship) still stronger than extro• Accelerating shift from “having” to “being”

consumers expected to be the main contributor of future growth

All r

ight

s re

serv

ed.

increasingly looking for experience

'W d f M th' k

• How to (i) diversify and (ii) deliver individual outstanding experiences along the purchase pathway ?

• Word of mouth/advocacy now the #1 influencer of luxury purchases

onsu

lting

Gro

up, I

nc. A'Word of Mouth' key

influencer for purchases

3

Word of mouth/advocacy now the #1 influencer of luxury purchases• And magazines are not dead (yet)

015

by T

he B

osto

n C

o

The rise of the digital world4

• Luxury sales are accelerating online• Beyond e-commerce, digital as a key lever to influence purchasing

behaviors of Luxury customers

Luxury Overview - 17Jan16- FINAL.pptx 1

Cop

yrig

ht ©

2

world behaviors of Luxury customers• Multichannel is a Must – What role for the stores in the future ?

4 key trends in the Luxury industry4 key trends in the Luxury industry

A changing world:A changing world: new growth drivers

in the Luxury industry

1

• Strong reduction in retail expansion: 2 / 3 of the next decade's growth will be organic

• Opportunities in countries where luxury buying is long-established, with US consumers expected to be the main contributor of future growthy

Intro values still roaring & customers i i l l ki2

• Intro luxury values (quality, exclus., craftsmanship) still stronger than extro• Accelerating shift from “having” to “being”

consumers expected to be the main contributor of future growth

All r

ight

s re

serv

ed.

increasingly looking for experience

'W d f M th' k

• How to (i) diversify and (ii) deliver individual outstanding experiences along the purchase pathway ?

• Word of mouth/advocacy now the #1 influencer of luxury purchases

onsu

lting

Gro

up, I

nc. A'Word of Mouth' key

influencer for purchases

3

Word of mouth/advocacy now the #1 influencer of luxury purchases• And magazines are not dead (yet)

015

by T

he B

osto

n C

o

The rise of the digital world4

• Luxury sales are accelerating online• Beyond e-commerce, digital as a key lever to influence purchasing

behaviors of Luxury customers

Luxury Overview - 17Jan16- FINAL.pptx 2

Cop

yrig

ht ©

2

world behaviors of Luxury customers• Multichannel is a Must – What role for the stores in the future ?

New growth drivers (1/3) : Recent switch from Retail expansion to Organic growth

1expansion to Organic growth

Last decade growth by component2 Upcoming decade growth by component2

10%

40%

100%

30%

100%

40%

20%

All r

ight

s re

serv

ed.35%

25%

20%

10%

onsu

lting

Gro

up, I

nc. A

Total growth

VolumeEmerging markets

Traditional Markets1

25%

Price - Mix Total growth

VolumePrice - MixEmerging markets

Traditional markets1

20%

015

by T

he B

osto

n C

o

60% 40%

Organic growth (LFL)

Retail expansion

30% 70%

Organic growth (LFL)

Retail expansion .

Luxury Overview - 17Jan16- FINAL.pptx 3

Cop

yrig

ht ©

260%

1. Europe (Italy, France, UK, Germany, Spain, Nordics), US and Japan; 2. Referrers to personal luxury (apparel, accessories, hard luxury, Perfume & Cosmetics)Note: Last decade Personal Luxury market CAGR growth ~5%; upcoming decade Personal Luxury market CAGR growth ~4%Source: Bernstein / BCG analysis

40% 30% 70%

New growth drivers (2/3) : Top Luxury consumers are back and are to make 40% of growth

1

Cluster 2014

# (M) $Bn1

2021

# (M) $Bn1

and are to make 40% of growth

# (M) $Bn # (M) $Bn

73122

4284

25

24Ultra

Beyond money$10 k

$20 k

135

330

94

220

11

18

9

15 220

Very high

Total Top Luxury

$5 k

All r

ight

s re

serv

ed.

Top Aspirational 7654 2519

+110$2 k

onsu

lting

Gro

up, I

nc. A

609481 422356Aspirational

015

by T

he B

osto

n C

o

Total LuxuryConsumers1 ~1015~755 ~465~390

Luxury Overview - 17Jan16- FINAL.pptx 4

Cop

yrig

ht ©

2+2601. Including Experiential and Personal luxury, excluding cars and YachtsNote: rounded numbersSource: BCG Analysis

New growth drivers (3/3) : US consumers expected to be the main contributor to future growth

1main contributor to future growth

P&E1 Luxury market growth by Nationality ($Bn)y g y y ($ )

Top Luxury

330496

450+$110B

y

All r

ight

s re

serv

ed.

672029220

150

300

~55%

onsu

lting

Gro

up, I

nc. A

0

150

015

by T

he B

osto

n C

o02021Others3Middle

EasternEuropean2ChineseAmericans2014

Luxury Overview - 17Jan16- FINAL.pptx 5

Cop

yrig

ht ©

2

1. Personal & Experiential Luxury market; 2. Italian, French, German, English 3. Including Japanese, S. Korean, Russian, Brazilian and RoWSource: BCG 2014 ad hoc study (10'000 respondents in 10 countries)

4 key trends in the Luxury industry4 key trends in the Luxury industry

A changing world:A changing world: new growth drivers

in the Luxury industry

1

• Strong reduction in retail expansion: 2 / 3 of the next decade's growth will be organic

• Opportunities in countries where luxury buying is long-established, with US consumers expected to be the main contributor of future growthy

Intro values still roaring & customers i i l l ki2

• Intro luxury values (quality, exclus., craftsmanship) still stronger than extro• Accelerating shift from “having” to “being”

consumers expected to be the main contributor of future growth

All r

ight

s re

serv

ed.

increasingly looking for experience

'W d f M th' k

• How to (i) diversify and (ii) deliver individual outstanding experiences along the purchase pathway ?

• Word of mouth/advocacy now the #1 influencer of luxury purchases

onsu

lting

Gro

up, I

nc. A'Word of Mouth' key

influencer for purchases

3

Word of mouth/advocacy now the #1 influencer of luxury purchases• And magazines are not dead (yet)

015

by T

he B

osto

n C

o

The rise of the digital world4

• Luxury sales are accelerating online• Beyond e-commerce, digital as a key lever to influence purchasing

behaviors of Luxury customers

Luxury Overview - 17Jan16- FINAL.pptx 6

Cop

yrig

ht ©

2

world behaviors of Luxury customers• Multichannel is a Must – What role for the stores in the future ?

Intro values still roaring2

Intro values still roaring

"What is luxury to you?"

• Adorned

Extrovalues% of respondents1

24% 24% 29% 30% 34% 38% 39% 40% 41% 44%

aesthetics• Brand visibility• Customization• Being Cool/Sexy

All r

ight

s re

serv

ed.

Introl

g y

onsu

lting

Gro

up, I

nc. A

76% 76% 71% 70% 66% 62% 61% 60% 59% 56%• Quality• Exclusivity• Craftsmanship

values

015

by T

he B

osto

n C

oCraftsmanship• Timeless

Luxury Overview - 17Jan16- FINAL.pptx 7

Cop

yrig

ht ©

2

1. Respondents were asked to rank the top 3 values: the graph represent the value ranked as the most importantSource: BCG 2014 ad hoc study (10'000 respondents in 10 countries)

Experiential Luxury market accounts for the largest part of the Luxury market

2the Luxury market

Luxury market ($B,2014 retail value)

541 500

Personal luxury ($290B)

Experiential luxury($465B)

Cars & Yachts($350B)

Others($280B)

5472154

350

1 500

1 000

1 385

P&E1 Market: $755B

All r

ight

s re

serv

ed.354

624941121500

$755B

onsu

lting

Gro

up, I

nc. A121

61670

TotalOther2Perfume &

Watches&

ApparelAcces- ArtTechno-Cars & Hotel & Food & Furniture

015

by T

he B

osto

n C

o& Cosmetics

&Jewelry

sories logyYachtsExclusive vacations

Wine

Covered by True-Luxury Global Consumer Insight

Luxury Overview - 17Jan16- FINAL.pptx 8

Cop

yrig

ht ©

2

1.Personal and Experiential luxury 2. Including Private Jets, Art de la table, etcNote: Some numbers are rounded.Source: BCG 2014 specific survey, BCG-IPSOS market research

Fundamental differences between personal Luxury goods and Luxury experiences

2and Luxury experiences

E i ti l lP l L d H b id Experiential luxuryPersonal Luxury goods

Having Being

Hybrid

For self only

Usually visible to

Often with others

Not always visibleCharacte-

-ristics

All r

ight

s re

serv

ed.other

For the mid-long term

Instant pleasure

onsu

lting

Gro

up, I

nc. A

Examples

• iPad• High-end kitchen• High end furniture• ....

• Luxury hotel or resorts

• High-end restaurants

• Watches with diamonds

• Jewelry• Bags, apparel

015

by T

he B

osto

n C

oExamples• Spas...

g , pp• ...

Luxury Overview - 17Jan16- FINAL.pptx 9

Cop

yrig

ht ©

2

Source: Internet research

4 key trends in the Luxury industry4 key trends in the Luxury industry

A changing world:A changing world: new growth drivers

in the Luxury industry

1

• Strong reduction in retail expansion: 2 / 3 of the next decade's growth will be organic

• Opportunities in countries where luxury buying is long-established, with US consumers expected to be the main contributor of future growthy

Intro values still roaring & customers i i l l ki2

• Intro luxury values (quality, exclus., craftsmanship) still stronger than extro• Accelerating shift from “having” to “being”

consumers expected to be the main contributor of future growth

All r

ight

s re

serv

ed.

increasingly looking for experience

'W d f M th' k

• How to (i) diversify and (ii) deliver individual outstanding experiences along the purchase pathway ?

• Word of mouth/advocacy now the #1 influencer of luxury purchases

onsu

lting

Gro

up, I

nc. A'Word of Mouth' key

influencer for purchases

3

Word of mouth/advocacy now the #1 influencer of luxury purchases• And magazines are not dead (yet)

015

by T

he B

osto

n C

o

The rise of the digital world4

• Luxury sales are accelerating online• Beyond e-commerce, digital as a key lever to influence purchasing

behaviors of Luxury customers

Luxury Overview - 17Jan16- FINAL.pptx 10

Cop

yrig

ht ©

2

world behaviors of Luxury customers• Multichannel is a Must – What role for the stores in the future ?

Word of Mouth: 1st influence lever, overcoming magazines3

Word of Mouth: 1 influence lever, overcoming magazines

"Which of the following has an impact on your purchase decision?"

% of respondents2013 Different WoM influence across nationalities

Social Media & Blogs Physical

2014

39%

32%Events

Magazines2

WoM 49%29% 20%

Store 39%

WoM1 43%32%11%

Magazines 50%

46%47%49%52%52%53%55%

58%

17% Avg. 49%

Social Media & Blogs Physical

All r

ight

s re

serv

ed.

31%

32%

32%

Tailoredoffers

Storewindows

Events

TV &Movies 24%

Brandwebsites 34%

windows 39%

34%

10%

41%

19%

17%14%24%

21%26%18%

33%

49%

onsu

lting

Gro

up, I

nc. A

TV &Movies

Brandwebsites

26%

30%

offers

Events 20%

Tailoredoffers 22%

Movies

23%

10%

22%30%33%

25%30%26%

35%

22%

41%

015

by T

he B

osto

n C

o

SeenWore

Celebrities

19%

23%

SeenWorn 13%

Celebrities 20%23%22%22%

Luxury Overview - 17Jan16- FINAL.pptx 11

Cop

yrig

ht ©

2

1 Includes WoM, Social Media and Other Social blogs 2. Editorials and Commercial in MagazinesNote: multiple choices possible, out of top 3 ranksSource: BCG 2014 ad hoc study (10'000 respondents in 10 countries)

Social media and blogs the real engine of WoM growth3

Social media and blogs the real engine of WoM growth

"Which of the following has an impact on your purchase decision?"

+6pp

ǻpp '13-'14

5%8% Blogs

S

49%

43% +3pp

All r

ight

s re

serv

ed.6% Social

Media12% +6pp

onsu

lting

Gro

up, I

nc. A

Physical29%32% (3pp)

015

by T

he B

osto

n C

o

20142013

WoMdigitalization 0.3 0.7

Luxury Overview - 17Jan16- FINAL.pptx 12

Cop

yrig

ht ©

2

1. WoM Digitalization index: calculated as Social Media & Blogs influence vs. WoM physical influenceNote: multiple choices possible, out of top 3 ranksSource: BCG 2014 ad hoc study (10'000 respondents in 10 countries)

gindex1

Impact of blogger collaboration in luxury3

Impact of blogger collaboration in luxury

Enlisted nine bloggers to help drive online and brick• Enlisted nine bloggers to help drive online and brick-and-mortar sales

• Hosted a series of in-store events across the U.S., resulting in 147 000 social interactionsresulting in 147,000 social interactions

• Blogger Christine Andrew of Hello Fashion fueled a 107% uptick in “likes” and 465% increase in comments to Neiman Marcus’ Instagram page after

All r

ight

s re

serv

ed.

comments to Neiman Marcus Instagram page after a Fall Trend event

onsu

lting

Gro

up, I

nc. A

• Rach Parcell of Pink Peonies reportedly drove $1 million in sales to nordstrom.com during the 2014

015

by T

he B

osto

n C

ogholiday season

Luxury Overview - 17Jan16- FINAL.pptx 13

Cop

yrig

ht ©

2

Source: WWD 'The Blogosphere Pays Off More Than Ever'. January 11, 2016

Vignette: Chanel targeting social media withimmersive pop-up perfume exhibit in NY

3immersive pop up perfume exhibit in NY

Immersive experience Social media promotion

Exhibit highlights key elements of Chanel No5 eau premiere from 'creation' to 'revelation'

Selfie walls• Visitors encouraged to post about their

experience online

Sensory experience• Coco Chanel whispers No5 anecdotes

directly to you

Twitter hashtag on perfume samples• Magically appears when sample paper is

spritzed with perfume to promote tweeting

All r

ight

s re

serv

ed.• Interactive video tables for each key

ingredient• 'Revelation' room scented with eau premiere

Virtual tickets

onsu

lting

Gro

up, I

nc. ACustomizable postcards

• Stamp-customizable eau premiere bottle cards mailed anywhere in the world for free

015

by T

he B

osto

n C

o

Luxury Overview - 17Jan16- FINAL.pptx 14

Cop

yrig

ht ©

2

Note: Chanel No5 eau premiere 'In a New Light' exhibit May 7-May17/15 in NYC

4 key trends in the Luxury industry4 key trends in the Luxury industry

A changing world:A changing world: new growth drivers

in the Luxury industry

1

• Strong reduction in retail expansion: 2 / 3 of the next decade's growth will be organic

• Opportunities in countries where luxury buying is long-established, with US consumers expected to be the main contributor of future growthy

Intro values still roaring & customers i i l l ki2

• Intro luxury values (quality, exclus., craftsmanship) still stronger than extro• Accelerating shift from “having” to “being”

consumers expected to be the main contributor of future growth

All r

ight

s re

serv

ed.

increasingly looking for experience

'W d f M th' k

• How to (i) diversify and (ii) deliver individual outstanding experiences along the purchase pathway ?

• Word of mouth/advocacy now the #1 influencer of luxury purchases

onsu

lting

Gro

up, I

nc. A'Word of Mouth' key

influencer for purchases

3

Word of mouth/advocacy now the #1 influencer of luxury purchases• And magazines are not dead (yet)

015

by T

he B

osto

n C

o

The rise of the digital world4

• Luxury sales are accelerating online• Beyond e-commerce, digital as a key lever to influence purchasing

behaviors of Luxury customers

Luxury Overview - 17Jan16- FINAL.pptx 15

Cop

yrig

ht ©

2

world behaviors of Luxury customers• Multichannel is a Must – What role for the stores in the future ?

The rise of online luxury continues : >25% growth every year since 2007

4year since 2007

Online luxury global market (personal luxury goods) (2007-2015, $B)(2007 2015, $B)

15.015.0

Online sales expected to

All r

ight

s re

serv

ed.9.0

5.6

expected to represent:

• ~10-15% of Luxury sales in 2020 ?

onsu

lting

Gro

up, I

nc. A

3.62.5

5 6 in 2020 ?• ~40-50% of

the growth 2015-2020 ?

015

by T

he B

osto

n C

o

2015F2011 201320092007

% on total l

5%+1.2%

Luxury Overview - 17Jan16- FINAL.pptx 16

Cop

yrig

ht ©

2

Note: Personal luxury includes apparel, leather and accessories, watch and jeweler, cosmetic sSource: Forrester research, BCG analysis

luxury

Digital: what's in beyond ecommerce?4

Digital: what s in beyond ecommerce?

Need to reorient Marketing Spend to Online (Social media, blogs etc)

Drive awareness with audiences through

Build deep consumer engagement and

A B

audiences through new platforms exploit advocacy

marketing

All r

ight

s re

serv

ed.

onsu

lting

Gro

up, I

nc. A

C

015

by T

he B

osto

n C

o

Enhance customer driven innovation:

• productsBuild a multichannel customer experience

D C

Luxury Overview - 17Jan16- FINAL.pptx 17

Cop

yrig

ht ©

2• retail,....customer experience

3 out of 4 consumers asking for omnichannel4

3 out of 4 consumers asking for omnichannel

"How important is for you that a brand can be reached through different channels?"

Omnichannel importance across nationalities

% f d t25%Not

Important

78% 78%81%85% 81%%

90%

A

% of respondents

All r

ight

s re

serv

ed.

38%Somehowimportant

78% 78%

43% 57%

45%

71%

33%

75%41%

44% 27%42%34%

48%

Avg. 75%

onsu

lting

Gro

up, I

nc. A75% 45%

31%

33%49%38% 36%43% 49%

41% 37%

015

by T

he B

osto

n C

o

37%Not negotiable/Very Important

33%38% 36%

11%

41%26%

37%

Luxury Overview - 17Jan16- FINAL.pptx 18

Cop

yrig

ht ©

2

Source: BCG 2014 ad hoc study (10'000 respondents in 10 countries)

Total

"Pure store" no longer the first channel in terms of sales origination

4origination

"Where have you bought the last item purchased? Where have you researched it?"

53 Æ 62%% of last purchase for each respondent

1007 Æ8

8Æ 9

10060

80

38 Æ 45

8 Æ 9

All r

ight

s re

serv

ed.

100

20

40

47 Æ38

onsu

lting

Gro

up, I

nc. A

0

TotalShowrooming(viewed in store,

Pure OnlineResearched OnlinePurchased Offline

Pure in Store

015

by T

he B

osto

n C

o

purchased on line)Purchased Offline

Luxury Overview - 17Jan16- FINAL.pptx 19

Cop

yrig

ht ©

2

Source: BCG 2013 and 2014 ad hoc study (10'000 respondents in 10 countries)

2013 Æ 2014Omnichannel

Multi-channel Consumers spend more4

Multi channel Consumers spend more

Brand X: average consumer spend by channels (index=100)

267

156

All r

ight

s re

serv

ed.

100122

onsu

lting

Gro

up, I

nc. A111

015

by T

he B

osto

n C

o

Multichannel (on-line+store)

Store onlyOn-line only

Luxury Overview - 17Jan16- FINAL.pptx 20

Cop

yrig

ht ©

2

Source: BCG analysis, mix of Maisons (Europe, US)

As a consequence: - traffic in physical stores & + rent = decreasing store return

4decreasing store return

2008 2014

Traffic (#) ~ 70 K ~60 K

~ 9.1 K ~7.7 K

~ 13% ~ 12.8%Conversion rate (%)

Clients (#)

All r

ight

s re

serv

ed.

~$1.000 ~$1.300

9.1 K 7.7 K

Average yearly purchase ($)

Clients (#)

onsu

lting

Gro

up, I

nc. A~$9.1 M ~$10.0 MSales / store ($M)

015

by T

he B

osto

n C

o

~$6 K / sqm ~$9 K / sqm

$30 K / sqm $33 K / sqm

Rent / sqm

Sales / sqmx 5 x 3.7

Luxury Overview - 17Jan16- FINAL.pptx 21

Cop

yrig

ht ©

2

Note: Analysis performed on a subset of Personal Luxury BrandsSource: Public data, Interviews with experts, Cushman & Wakefield Valuation report, BCG analysis

Emerging Trends: New business modelsLuxury on-demandLuxury on demand

UberLUX• Tested in select markets on

Audi• Tested in SFO with plans to

Glamsquad• On-demand beauty app

All r

ight

s re

serv

ed.

Tested in select markets on New Year's and Valentine's Day 2015

• Car models: Mercedes Benz

Tested in SFO with plans to expand to more cities

• Vehicles available: A4 sedan & R8 supercar

y ppproviding hair, makeup or nail services from beauty professionals on-demand

onsu

lting

Gro

up, I

nc. ACar models: Mercedes Benz

S-Classes & BMW 7-Series

• Pickups from highest-rated drivers

sedan & R8 supercar

• Can use car for up to 28 days

• Currently in New York, LA, Miami and the Hamptons

• Founded by Gilt Groupe co-

015

by T

he B

osto

n C

odrivers• Also offers 'Audi at Home'

where residents in select condo complexes can share a fleet of Audi

y pfounder

Luxury Overview - 17Jan16- FINAL.pptx 22

Cop

yrig

ht ©

2share a fleet of Audi vehicles

Source: Company websites, Luxury Daily

Emerging Trends: New business modelsEmerging Trends: New business models

Luxury Travel Retail Wearable TechnologyLuxury Travel Retail Wearable Technology

All r

ight

s re

serv

ed.

onsu

lting

Gro

up, I

nc. A

015

by T

he B

osto

n C

o

Luxury Overview - 17Jan16- FINAL.pptx 23

Cop

yrig

ht ©

2

Thank you

bcg.com | bcgperspectives.com

Top Related