Languages

Pages

Legal

April 24, 2017

IPO Review

ICICI Securities Ltd | Retail Equity Research

S Chand, incorporated in 1970, is India’s leading education content

company with a presence across the entire education lifecycle through K-

12 (73% of revenues), higher education (24% of revenues) and early

learning segments (3% of revenues). S Chand has a strong presence in

CBSE/ICSE affiliated schools. It offers 55 consumer brands across

knowledge products and services including ‘S Chand’, ‘Vikas’,

‘Madhubun’, ‘Saraswati’, ‘Destination Success’, and ‘Ingnitor’. Recently,

the company acquired 74% stake in Chhaya Prakashani to strengthen its

presence in Eastern India. Driven by a number of acquisitions, S Chand

posted revenue CAGR of 33% over FY12-16. In FY16, S Chand sold 35.5

million copies of a total of 11,144 titles.

Investment Rationale

Leading position in the K-12 market…

S Chand is India’s leading K-12 education content company in terms of

revenue, with a strong presence in CBSE/ICSE affiliated schools,

contributing 73% of consolidated revenues in FY16. From FY12-16, K-12

revenues grew at 46.83% CAGR. Initially, the company’s main foray was

into English grammar, science and maths subjects. In order to fill the

portfolio gaps with respect to individual subject strength, the company

acquired Madhubun and Vikas brands in FY13 (strong presence in Hindi

titles) and Saraswati brand (strength in French and arts & craft titles).

Through the Chhaya acquisition, S Chand expanded its presence in

eastern India. With a large number of students nowadays opting for CBSE

and ICSE boards, the company believes there is significant opportunity to

further increase market share in the K-12 segment.

Strong integrated in-housing printing and logistic capability…

S Chand has developed a robust supply chain ensuring optimisation of

back-end operations and processes. Over the last two years, the company

has spent ~| 45.3 crore capex to enhance its printing capacity from 15

tonnes of paper per day in FY14 to 55 tonnes of paper per day in FY16.

Captive requirements, to the extent of 85%, are fulfilled in-house.

Pan-India player…

S Chand has developed a strong distribution network consisting of 4932

distributors & dealers and an in-house sales team of 838 professionals

working from 52 branches and marketing offices. The company’s recent

acquisitions have helped it to diversify its geographical reach. Acquisition

of Saraswati (NSHPL) enhanced the distribution network in southern India

whereas acquisition of Vikas (VPHPL) added the distribution network in

north India. In addition, the Chhaya acquisition expanded its presence in

eastern India adding 771 more distributors.

Key risks and concerns

CBSE board advising schools to use only NCERT print content

High degree of seasonality in K-12 business

Obligation to acquire remaining 26% stake in Chhaya Prakashani

Priced at FY16 PE multiple of 50x (excluding Chhaya) on higher band

The standalone multiple on FY16 basis looks expensive at 50x. However,

accounting for the Chhaya merger, adjusted P/E appears at 34x FY16.

Completion of Chhaya acquisition would further strengthen S Chand’s

leadership position in the K-12 segment, which would enable it to post

15% revenue CAGR in the near term. We have a SUBSCRIBE

recommendation on the issue on the back of growth prospects.

S Chand Ltd

Price band | 660-670

Rating matrix

Rating : Subscribe

Issue Details

Issue Opens 26-Apr-17

Issue Closes 28-Apr-17

Issue Size (| Crore) 729

Fresh Issue 325

Offer for Sale 404

Price Band (|) 660-670

No of Shares on Offer (crore) 1.1

QIB (%) 50%

Non-Institutional (%) 15%

Retail (%) 35%

Minimum lot size (No. of shares) 22

Objects of issue

Amount

a) Repayment of loans availed by the company

and its subsidiaries, EPHL, which were utilized

towards funding the acquisition of Chhaya | 150.4 crore

b) Repayment/prepayment, in full or in part of

certain loans availed by the company and

certain of its subsidiaries, VPHL & NSHPL | 104.6 crore

c) General corporate purposes | 70 crore

20062006

Shareholding pattern (at upper price band: | 670)

Pre-Issue Post-Issue

Promoter & promoter group 58.3% 46.6%

Public 41.7% 53.4%

Financial Summary - EPS

| Crore FY14 FY15 FY16 9MFY17

Total Revenue 370.0 476.7 537.8 149.5

EBITDA 78.8 102.2 125.3 (84.9)

EBITDA Margin (%) 21.3 21.4 23.3 (56.8)

PAT 42.6 32.8 46.6 (88.5)

EPS* 12.3 9.4 13.4 (25.5)

* Considering post equity dilution

Valuation Summary (at upper price band: | 670)

(x) FY13 FY14 FY15 FY16

P/E 72.7 54.6 71.0 49.8

EV/EBITDA 43.5 31.6 24.4 19.9

Research Analyst

Bharat Chhoda

Ankit Panchmatia

Cheragh Sidhwa

Page 2 ICICI Securities Ltd | Retail Equity Research

Company Background

Incorporated in 1970, S Chand is India’s leading education content

company with a presence across the entire education lifecycle through K-

12 (73% of revenues), higher education (24% of revenues) and early

learning segments (3% of revenues). The company has a strong presence

in the CBSE/ICSE affiliated schools and increasing presence in state board

affiliated schools as well. S Chand offers 55 consumer brands across

knowledge products and services including ‘S Chand’, ‘Vikas’,

‘Madhubun’, ‘Saraswati’, ‘Destination Success’, and ‘Ingnitor’. Recently,

the company acquired a 74% stake in Chhaya Prakashani to strengthen in

presence in eastern India. In FY16, S Chand sold 35.47 million copies of a

total of 11,144 titles. Additionally Chhaya sold 9.88 million copies of 433

titles in FY16. The company has a contractual relationship with at least

1958 authors for over five years.

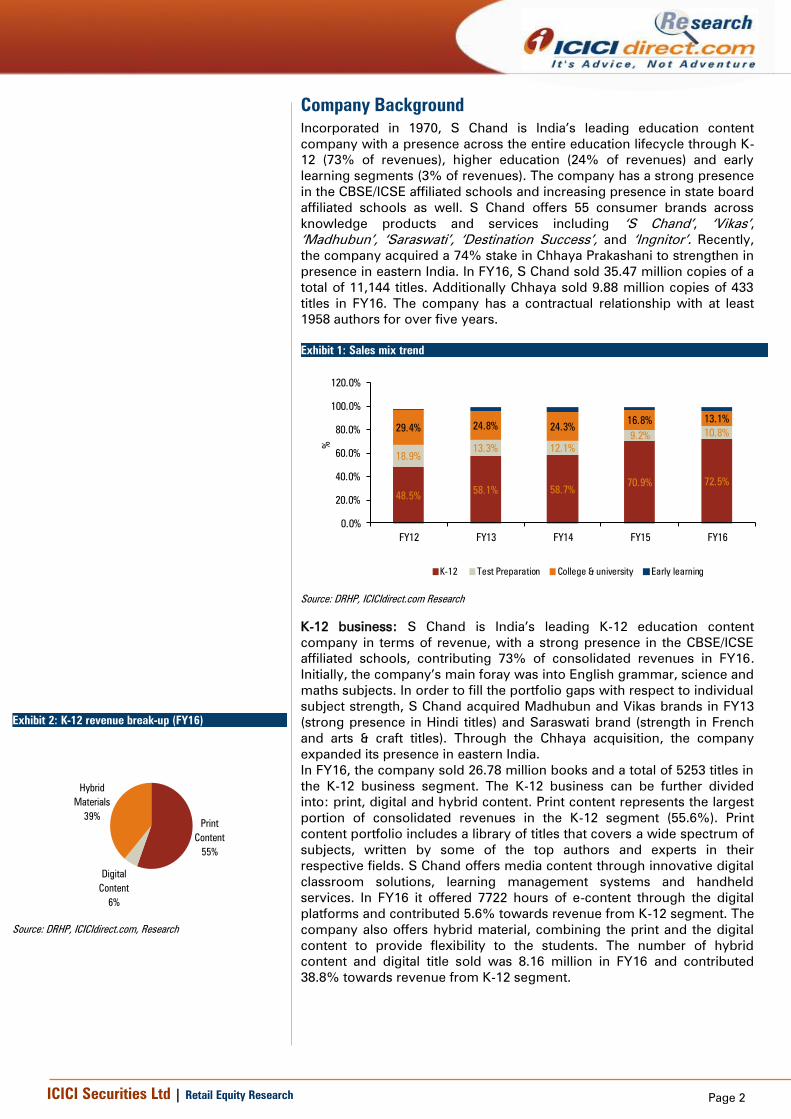

Exhibit 1: Sales mix trend

48.5%58.1% 58.7%

70.9% 72.5%

18.9%

13.3% 12.1%

9.2% 10.8%29.4% 24.8% 24.3%

16.8% 13.1%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

FY12 FY13 FY14 FY15 FY16

%

K-12 Test Preparation College & university Early learning

Source: DRHP, ICICIdirect.com Research

K-12 business: S Chand is India’s leading K-12 education content

company in terms of revenue, with a strong presence in the CBSE/ICSE

affiliated schools, contributing 73% of consolidated revenues in FY16.

Initially, the company’s main foray was into English grammar, science and

maths subjects. In order to fill the portfolio gaps with respect to individual

subject strength, S Chand acquired Madhubun and Vikas brands in FY13

(strong presence in Hindi titles) and Saraswati brand (strength in French

and arts & craft titles). Through the Chhaya acquisition, the company

expanded its presence in eastern India.

In FY16, the company sold 26.78 million books and a total of 5253 titles in

the K-12 business segment. The K-12 business can be further divided

into: print, digital and hybrid content. Print content represents the largest

portion of consolidated revenues in the K-12 segment (55.6%). Print

content portfolio includes a library of titles that covers a wide spectrum of

subjects, written by some of the top authors and experts in their

respective fields. S Chand offers media content through innovative digital

classroom solutions, learning management systems and handheld

services. In FY16 it offered 7722 hours of e-content through the digital

platforms and contributed 5.6% towards revenue from K-12 segment. The

company also offers hybrid material, combining the print and the digital

content to provide flexibility to the students. The number of hybrid

content and digital title sold was 8.16 million in FY16 and contributed

38.8% towards revenue from K-12 segment.

Exhibit 2: K-12 revenue break-up (FY16)

Hybrid

Materials

39%

Digital

Content

6%

Content

55%

Source: DRHP, ICICIdirect.com, Research

Page 3 ICICI Securities Ltd | Retail Equity Research

In FY12-16, K-12 consolidated revenues (excluding Chhaya) grew at

46.8% CAGR, which includes organic growth of 20.5%.

Exhibit 4: S Chand growth anchored by K-12 growth

83.9

162.0217.3

337.8389.8

123.1

0.0

100.0

200.0

300.0

400.0

500.0

600.0

FY12 FY13 FY14 FY15 FY16

| c

rore

K-12 Chhaya

Revenue contribution from

Chhaya acquired in

Dec,2016

Source: DRHP, ICICIdirect.com Research

Higher education business: This is the second largest segment by

consolidate revenues and comprises two components:

Test preparation

College & university/technical and professional

Test preparation: S Chand publishes niche test preparation titles in print

for popular professionals and entrance examinations in India, including

competitive and reference books for government and public sector

entrance examinations. The company has also started offering online test

preparation and assessment as well. In FY16, the company sold 1.98

million copies of 109 titles in test preparation and contributed 10.8%

towards consolidated revenues.

College & university/technical and professional: The company provides

content from graduation level to post graduation level in subjects such as

accounting, economics, physics, etc. The sales team works directly with

higher education institutions, from which they receive content

development requests. In FY16, the company sold 2.86 million copies and

contributed 13.1% towards consolidated revenues.

Early learning business: The early learning business caters to the

youngest customer market (0-4 years age), contributing 3.2% of

consolidated revenues.

Exhibit 3: K-12 book shelf…

Source: Company, ICICIdirect.com, Research

Source: DRHP, ICICIdirect.com, Research

Exhibit 5: Higher education book shelf…

Source: Company, ICICIdirect.com, Research

Exhibit 6: Higher education revenue break-up

50.969.2

89.979.9

70.4

32.7

37.1

44.6

43.9 57.9

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

FY12 FY13 FY14 FY15 FY16

| c

rore

College & university Test Preparation

Source: DRHP, ICICIdirect.com Research

Exhibit 7: Early learning book shelf…

Source: Company, ICICIdirect.com, Research

Page 4 ICICI Securities Ltd | Retail Equity Research

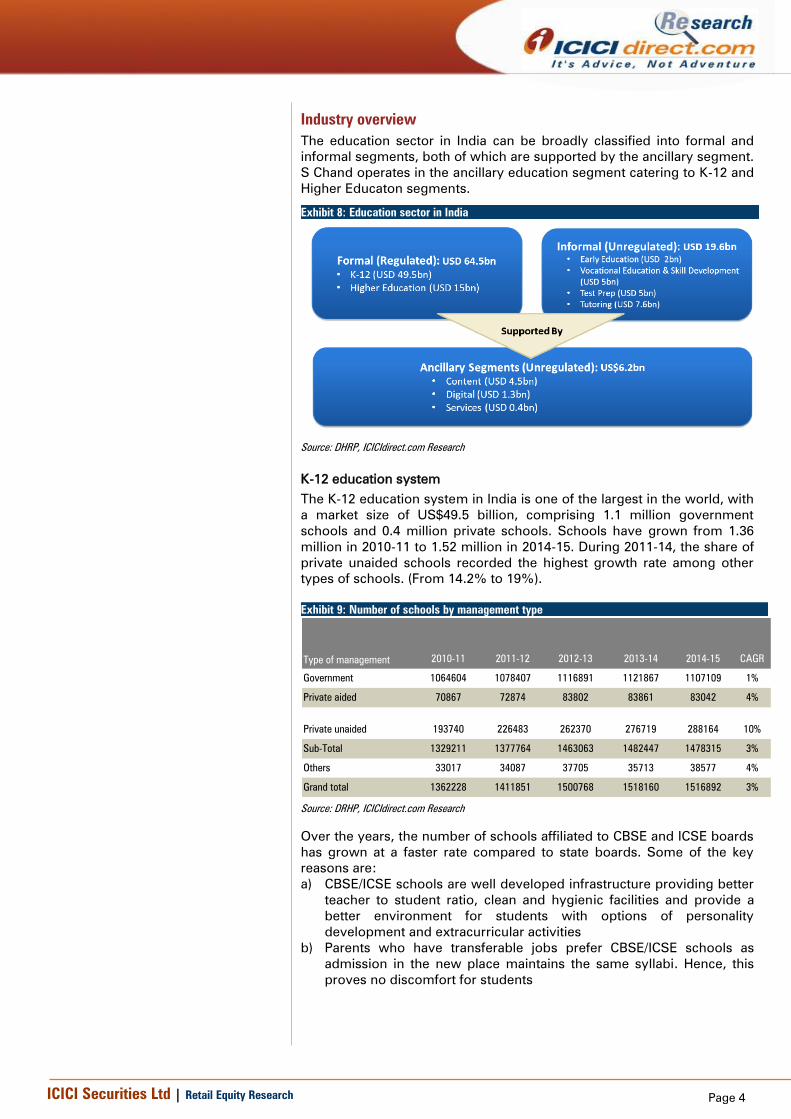

Industry overview

The education sector in India can be broadly classified into formal and

informal segments, both of which are supported by the ancillary segment.

S Chand operates in the ancillary education segment catering to K-12 and

Higher Educaton segments.

Exhibit 8: Education sector in India

Source: DHRP, ICICIdirect.com Research

K-12 education system

The K-12 education system in India is one of the largest in the world, with

a market size of US$49.5 billion, comprising 1.1 million government

schools and 0.4 million private schools. Schools have grown from 1.36

million in 2010-11 to 1.52 million in 2014-15. During 2011-14, the share of

private unaided schools recorded the highest growth rate among other

types of schools. (From 14.2% to 19%).

Exhibit 9: Number of schools by management type

2010-11 2011-12 2012-13 2013-14 2014-15 CAGR

Government 1064604 1078407 1116891 1121867 1107109 1%

Private aided 70867 72874 83802 83861 83042 4%

Private unaided 193740 226483 262370 276719 288164 10%

Sub-Total 1329211 1377764 1463063 1482447 1478315 3%

Others 33017 34087 37705 35713 38577 4%

Grand total 1362228 1411851 1500768 1518160 1516892 3%

Type of management

Source: DRHP, ICICIdirect.com Research

Over the years, the number of schools affiliated to CBSE and ICSE boards

has grown at a faster rate compared to state boards. Some of the key

reasons are:

a) CBSE/ICSE schools are well developed infrastructure providing better

teacher to student ratio, clean and hygienic facilities and provide a

better environment for students with options of personality

development and extracurricular activities

b) Parents who have transferable jobs prefer CBSE/ICSE schools as

admission in the new place maintains the same syllabi. Hence, this

proves no discomfort for students

Page 5 ICICI Securities Ltd | Retail Equity Research

The gradual shift of students from state board schools to CBSE/ICSE

school augurs well for the company, since it has a strong presence in

CBSE/ICSE affiliated schools.

Exhibit 10: Number of schools by affiliated boards

CAGR

2010-11 2011-12 2012-13 2013-14 2014-15

2010-11 to

2014-15 2015-16

CBSE 11349 12337 13898 14778 15933 8.9% 17474

ICSE 1461 1565 1678 1798 1927 7.2% 2181

State board 1316401 1363862 1447487 1465871 1460455 2.6% NA

Total 1329211 1377764 1463063 1482447 1478315 2.7% -

Boards

Source: DRHP, ICICIdirect.com Research

Ancillary segment

The ancillary segment of India’s education sector is estimated to be worth

~ US$6.2 billion in 2015, and is expected to grow at 21% CAGR up to

US$15.4 billion by 2020. The ancillary segment comprises the industries

related and supplementary to both formal and informal education

segments. Therefore, it is a direct beneficiary of growth in both education

segments. The K-12 education content market is estimated at US$3,366.2

million and has grown at 19.3% CAGR in 2011-15. With a large market

share, the state board affiliated school content market presents a large

opportunity for a pan-India content provider. Central board affiliated

schools (i.e. CBSE/ICSE schools) exhibited faster growth at 21.7% CAGR

in 2011-15, aided by participation of the private sector.

Exhibit 11: K-12 education content market (US$ million)

2010-11 2011-12 2012-13 2013-14 2014-15 CAGR

CBSE 203.1 251.5 304.6 371.8 445.2 21.7%

ICSE 28.1 34.4 40.6 50 59.4 20.5%

State board 1433.9 1718.2 2046.2 2477.7 2861.6 18.9%

Total 1665.1 2004.1 2391.4 2869.5 3366.2 19.3%

Total K-12

Source: DRHP, ICICIdirect.com Research

The school market segment is very fragmented. There are big national

content providers with a pan-India presence and several small national

content providers in addition to regional providers who are very strong in

their respective markets. There appears to be a consolidation opportunity

for large content providers who can acquire smaller providers with both a

national and, particularly, a regional presence. Such consolidation activity

would enable a better reach/brand equity and market share in Tier II cities

and towns where such regional content providers are already established

in their respective markets.

Page 6 ICICI Securities Ltd | Retail Equity Research

S Chand Strategies

Increasing share of the content spend in CBSE/ICSE schools

To compliment and diversify the home-grown product portfolio and S

Chand brand, over the years, the company has acquired various

education players to strengthen its offerings. As a result of such

acquisitions, the company has an expansive product range and strong

brands across multiple subject offerings. Going forward, S Chand is open

to further brand acquisitions, which would help it to provide

complementary content targeted at CBSE/ICSE affiliated schools. With the

growing middle class and emphasis on education, the company believes

there is significant opportunity to further increase the market share in

both volume and percentage.

Increasing presence in state board markets

According to Nielsen, the state board content is | 18320 crore and is the

largest part of the Indian K-12 market. To increase the market share in the

state board segment, the company intends to acquire leading regional

content houses in attractive markets. The company believes the regional

acquisitions would enable them to increase market share and acquire

distribution networks catering to state board affiliated schools.

Expanding presence in test preparation market

The company believes the test preparation market will continue to

expand as more government jobs become available that require

examinations at the national and state levels. In addition, many

examinations are now moving to the online format. The company intends

to build the online solution by investing in education technology

companies to leverage their innovative technologies and gain from the

company’s content and industry experience.

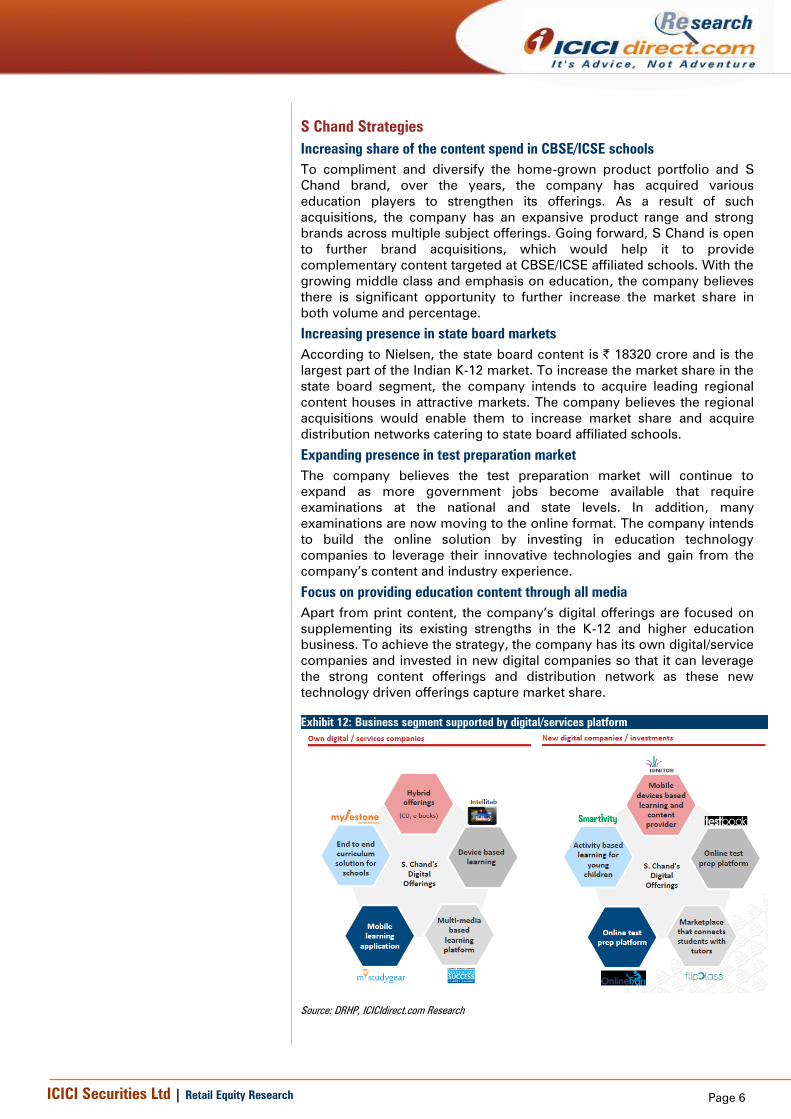

Focus on providing education content through all media

Apart from print content, the company’s digital offerings are focused on

supplementing its existing strengths in the K-12 and higher education

business. To achieve the strategy, the company has its own digital/service

companies and invested in new digital companies so that it can leverage

the strong content offerings and distribution network as these new

technology driven offerings capture market share.

Exhibit 12: Business segment supported by digital/services platform

Source: DRHP, ICICIdirect.com Research

Page 7 ICICI Securities Ltd | Retail Equity Research

Financial performance

S Chand clocked in a consolidated revenue growth of 33%CAGR in FY12-

16 to | 537.8 crore mainly anchored by growth in the K-12 segment. K-

12’s consolidated operating revenues grew at a CAGR of 47%, which

includes organic growth of 20%. In the same period, revenues from test

preparation and college/university segments grew at 15% and 8% to

| 57.9 crore and | 70.4 crore, respectively. Revenues from early learning

segment scaled up from | 10 lakh in FY12 to | 17.3 core in FY16. On a

consolidated basis, EBITDA during the period increased at 49% CAGR to

| 125.3 crore while PAT (after minority interest) grew at a CAGR of 33% to

| 46.6 crore.

The company’s business is linked to the academic cycle and is therefore,

seasonal. In the K-12 segment, the company’s sales season has

traditionally been the fourth quarter of the financial year, which

contributes ~75% of overall revenues and profitability. The first nine

months of the fiscal typically tend to be weak or have shown a loss.

Exhibit 13: Revenue trajectory- CAGR of 33% in FY12-16

173.0

279.0

370.0

476.7

537.8

149.5

0.0

100.0

200.0

300.0

400.0

500.0

600.0

FY12 FY13 FY14 FY15 FY16 9MFY17

| c

rore

Source: DRHP, ICICIdirect.com, Research

Exhibit 14: EBITDA growth- CAGR of 49% in FY12-16

25.5

57.3

78.8

102.2

125.3

-84.9

14.7

20.521.3 21.4

23.3

-100

-50

0

50

100

150

FY12 FY13 FY14 FY15 FY16 9MFY17

| cro

re

0

5

10

15

20

25

%

EBITDA EBITDA Margin

Source: DRHP, ICICIdirect.com, Research

Exhibit 15: Net profit- CAGR of 33% in FY12-16

14.7

32.0

42.6

32.8

46.6

-88.5

-100

-80

-60

-40

-20

0

20

40

60

FY12 FY13 FY14 FY15 FY16 9MFY17

| c

rore

Source: DRHP, ICICIdirect.com, Research

Exhibit 16: Return ratio trend

16.2

11.0 11.6

8.3 7.8

13.9

12.4

14.7

13.1 12.5

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY12 FY13 FY14 FY15 FY16

%

RoE RoCE

Source: DRHP, ICICIdirect.com, Research

Page 8 ICICI Securities Ltd | Retail Equity Research

Objects of issue

The offer consists of a fresh issue and an offer for sale (OFS) by selling

share holders with a total issue size ranging from | 722.5 crore to | 728.6

crore. The company intends to raise | 325 crore at a price band of | 660-

670 leading to a fresh issue of 48.5-49.2 lakh shares.

Objects of fresh issue:

The details of the proceeds of the fresh issue are summarised below:

a) The company intends to utilise | 150.4 crore of the net proceeds

towards repayment of loans availed by the company and one of its

subsidiaries, Eurasia (EPHL), which were utilised towards funding the

acquisition of Chhaya

b) The company intends to utilise | 104.6 crore of net proceeds towards

repayment/prepayment of loans availed by the company and certain

of its subsidiaries, VPHL and NSHPL

c) General corporate purpose, which includes payment of issue

expenses and other general expenses

Exhibit 17: Schedule of implementation and deployment of net proceeds

Total estimated costs

Amount to be funded from the net

proceeds FY18

Repayment of loans availed by the company, which was

utilised towards funding the acquisition of Chhaya | 100.0 | 100.0 | 100.0

Repayment of loans availed by Eurasia Publishing House Pvt

Ltd, one of the company's subsidiaries, which was utilised

towards funding the acquisition of Chhaya| 50.4 | 50.4 | 50.4

Repayment/prepayment in full or in part, of certain loans

availed by the company | 55.0 | 55.0 | 55.0

Repayment/prepayment in full or in part, of certain loans

availed by certain of the company's subsidiaries, VPHPL &

NSHPL | 49.6 | 49.6 | 49.6

General corporate purpose | 70.0 | 70.0 | 70.0

TOTAL | 325 crore

Particulars (|cr)

Estimated utilisation of net proceeds

Source: DRHP, ICICIdirect.com, Research

Offer for sale:

The OFS consists of to 60 lakh equity shares amounting to | 404 crore

from Everstone Capital, IFC and promoters. Post IPO, the stake dilution

will be as follows:

a) Promoters (From 58.3% to 46.7%)

b) Everstone Capital (From 32.3% to 13.9%)

c) IFC (From 9.4% to 8.1%)

Page 9 ICICI Securities Ltd | Retail Equity Research

Key risks and concerns

CBSE board advising schools to use only NCERT print content for all classes

The CBSE has issued circulars, dated April 12, 2016 and July 20, 2015,

recommending that schools affiliated to CBSE use only NCERT print

content for all classes, since all schools affiliated to the CBSE follow the

syllabi prescribed by NCERT up to K-8 and syllabi prescribed by the CBSE

from ninth grade to 12th grade. Further, the CBSE circulars also

recommended that schools affiliated to the CBSE should avoid insisting

that students purchase additional print content from private content

providers. These circulars may reduce demand for educational content

among CBSE affiliated schools and, accordingly, may adversely impact

the business, results of operations, cash flows and financial condition.

High degree of seasonality in K-12 business…

The company’s business is linked to the academic cycle and is therefore,

seasonal. In the K-12 segment, company’s sales season has traditionally

been the fourth quarter of the financial year. The first nine months of the

fiscal typically tends to be weak or have shown a loss. In addition, the

working capital cycle for print content in the CBSE/ICSE K-12 education

industry tends to be unduly high at the fiscal year end on account of high

sales in the last quarter, which then tapers down in subsequent quarters.

The company’s sales seasonality in its K-12 segment materially affects

operating revenue, margins and cash flows from quarter to quarter.

Heavy dependence on top authors to generate revenues…

A significant portion of the company’s revenues are derived from the top

20 authors. This concentration of revenues could potentially be a threat

with respect to negotiations regarding payment of royalties and other

terms. In FY16, the top 20 authors (in terms of revenue) contributed to

~48.94% of its total consolidated revenues from operations. The loss of

such authors could adversely affect the business, results of operation,

cash flows and financial condition.

Obligation to acquire remaining 26% stake in Chhaya Prakashani…

S Chand is obligated to acquire the remaining 26% outstanding share

capital of Chhaya Prakashani on or after November 15, 2018. The

company cannot assure that the business will generate sufficient cash

flow and may need to fund the remaining stake through additional debt.

Page 10 ICICI Securities Ltd | Retail Equity Research

Financial Summary

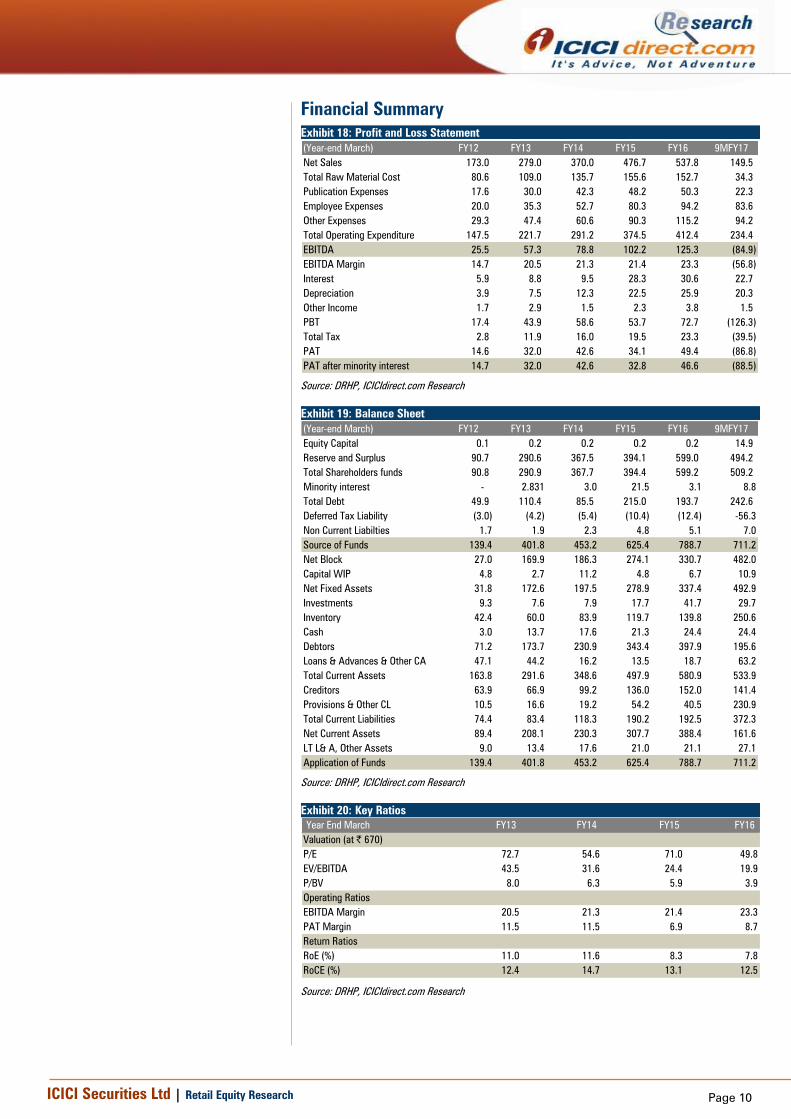

Exhibit 18: Profit and Loss Statement

(Year-end March) FY12 FY13 FY14 FY15 FY16 9MFY17

Net Sales 173.0 279.0 370.0 476.7 537.8 149.5

Total Raw Material Cost 80.6 109.0 135.7 155.6 152.7 34.3

Publication Expenses 17.6 30.0 42.3 48.2 50.3 22.3

Employee Expenses 20.0 35.3 52.7 80.3 94.2 83.6

Other Expenses 29.3 47.4 60.6 90.3 115.2 94.2

Total Operating Expenditure 147.5 221.7 291.2 374.5 412.4 234.4

EBITDA 25.5 57.3 78.8 102.2 125.3 (84.9)

EBITDA Margin 14.7 20.5 21.3 21.4 23.3 (56.8)

Interest 5.9 8.8 9.5 28.3 30.6 22.7

Depreciation 3.9 7.5 12.3 22.5 25.9 20.3

Other Income 1.7 2.9 1.5 2.3 3.8 1.5

PBT 17.4 43.9 58.6 53.7 72.7 (126.3)

Total Tax 2.8 11.9 16.0 19.5 23.3 (39.5)

PAT 14.6 32.0 42.6 34.1 49.4 (86.8)

PAT after minority interest 14.7 32.0 42.6 32.8 46.6 (88.5)

Source: DRHP, ICICIdirect.com Research

Exhibit 19: Balance Sheet

(Year-end March) FY12 FY13 FY14 FY15 FY16 9MFY17

Equity Capital 0.1 0.2 0.2 0.2 0.2 14.9

Reserve and Surplus 90.7 290.6 367.5 394.1 599.0 494.2

Total Shareholders funds 90.8 290.9 367.7 394.4 599.2 509.2

Minority interest - 2.831 3.0 21.5 3.1 8.8

Total Debt 49.9 110.4 85.5 215.0 193.7 242.6

Deferred Tax Liability (3.0) (4.2) (5.4) (10.4) (12.4) -56.3

Non Current Liabilties 1.7 1.9 2.3 4.8 5.1 7.0

Source of Funds 139.4 401.8 453.2 625.4 788.7 711.2

Net Block 27.0 169.9 186.3 274.1 330.7 482.0

Capital WIP 4.8 2.7 11.2 4.8 6.7 10.9

Net Fixed Assets 31.8 172.6 197.5 278.9 337.4 492.9

Investments 9.3 7.6 7.9 17.7 41.7 29.7

Inventory 42.4 60.0 83.9 119.7 139.8 250.6

Cash 3.0 13.7 17.6 21.3 24.4 24.4

Debtors 71.2 173.7 230.9 343.4 397.9 195.6

Loans & Advances & Other CA 47.1 44.2 16.2 13.5 18.7 63.2

Total Current Assets 163.8 291.6 348.6 497.9 580.9 533.9

Creditors 63.9 66.9 99.2 136.0 152.0 141.4

Provisions & Other CL 10.5 16.6 19.2 54.2 40.5 230.9

Total Current Liabilities 74.4 83.4 118.3 190.2 192.5 372.3

Net Current Assets 89.4 208.1 230.3 307.7 388.4 161.6

LT L& A, Other Assets 9.0 13.4 17.6 21.0 21.1 27.1

Application of Funds 139.4 401.8 453.2 625.4 788.7 711.2

Source: DRHP, ICICIdirect.com Research

Exhibit 20: Key Ratios

Year End March FY13 FY14 FY15 FY16

Valuation (at | 670)

P/E 72.7 54.6 71.0 49.8

EV/EBITDA 43.5 31.6 24.4 19.9

P/BV 8.0 6.3 5.9 3.9

Operating Ratios

EBITDA Margin 20.5 21.3 21.4 23.3

PAT Margin 11.5 11.5 6.9 8.7

Return Ratios

RoE (%) 11.0 11.6 8.3 7.8

RoCE (%) 12.4 14.7 13.1 12.5

Source: DRHP, ICICIdirect.com Research

Page 11 ICICI Securities Ltd | Retail Equity Research

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

Page 12 ICICI Securities Ltd | Retail Equity Research

Disclaimer

ANALYST CERTIFICATION

We /I, Bharat Chhoda, MBA, Ankit Panchmatia, MBA and Cheragh Sidhwa, MBA Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this

research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or wil l be directly or indirectly related to the specific

recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securitiesis under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Bharat Chhoda, MBA, Ankit Panchmatia, MBA and Cheragh Sidhwa, MBA Research Analysts of this report have not received any compensation from the companies mentioned in the

report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Bharat Chhoda, MBA, Ankit Panchmatia, MBA and Cheragh Sidhwa, MBA Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.