Languages

Pages

Legal

Ross Pruitt

Extension Livestock Economist

Summary

Recap of Overall Meat Complex in 2009 Beef Situation and Outlook Poultry Situation and Outlook Dairy Outlook Aquaculture Outlook

2009 Recap

Lower production in 2009First time ever that red meat and poultry

production declined in the same year

Lower production costs didn’t come soon enough

Slack demandH1N1 flu virusExports remained “strong”

U S BEEF AND VEAL EXPORTSCarcass Weight, Monthly

70

90

110

130

150

170

190

210

230

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Mil. Pounds

Avg.2003-07

2008

2009

I-N-1601/13/10Livestock Marketing Information Center

TOTAL RED MEAT IN COLD STORAGEEnd of the Month

800

850

900

950

1,000

1,050

1,100

1,150

JAN MAR MAY JUL SEP NOV

Mil. Pounds

Avg.2003-07

2008

2009

M-S-1112/23/09

Livestock Marketing Information Center

Data Source: USDA/NASS

CHICKEN IN COLD STORAGEEnd of the Month

625

645

665

685

705

725

745

765

785

805

825

JAN MAR MAY JUL SEP NOV

Mil. Pounds

Avg.2003-07

2008

2009

P-S-0512/23/09

Livestock Marketing Information Center

Data Source: USDA/NASS

Livestock Marketing Information Center

COMMERCIAL MEAT & POULTRY PRODUCTION

By Type of Meat, Annual

0

10

20

30

40

50

60

70

80

90

100

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Bil. Pounds

Turkey

Chicken

Lamb &Veal

Pork

Beef

M-S-03A01/07/10

Livestock Marketing Information Center

U S RED MEAT & POULTRY CONSUMPTIONPer Capita, Retail Weight, Annual

0

50

100

150

200

1986 1989 1992 1995 1998 2001 2004 2007 2010

Pounds

Red Meat

TotalPoultry

M-C-0701/07/10

2009 Beef Review Continued reduction in national beef

herd numbers Ideal growing conditions for forage in

2009Hay production affected in LA due to dry

summer and wet fall Increased carcass weights Lower byproduct values Continued feedlot losses of $90/head

Winter Grazing Costs

Louisiana Steer Prices

Louisiana Steer Prices

Price Slides Remain Highly Variable

BOXED BEEF CUTOUT VALUEChoice 600-900 Lbs. Carcass, Weekly

130

135

140

145

150

155

160

165

170

175

180

JAN APR JUL OCT

$ Per Cwt.

Avg.2003-07

2008

2009

C-P-6201/04/10

Livestock Marketing Information Center

Data Source: USDA/AMS

CHOICE MINUS SELECT BEEF PRICESCarcass Cutout Value 600-900 Lbs., Weekly

-2

0

2

4

6

8

10

12

14

16

18

20

JAN APR JUL OCT

$ Per Cwt.

Avg.2003-07

2008

2009

C-P-6801/04/10Livestock Marketing Information Center

2010 Outlook

Stronger prices across the boardFed cattle: $86-89 (2009 Avg: $83.25)Feeder cattle: $98-104 (2009 Avg: $97.28)LA 500 lb steers: $100 (2009 Avg: $94.60)Cull cows: $40-50 (2009 Avg: $41.97)

Expect prices to remain volatileNarrowing of price slides againEconomical grass-fed gains

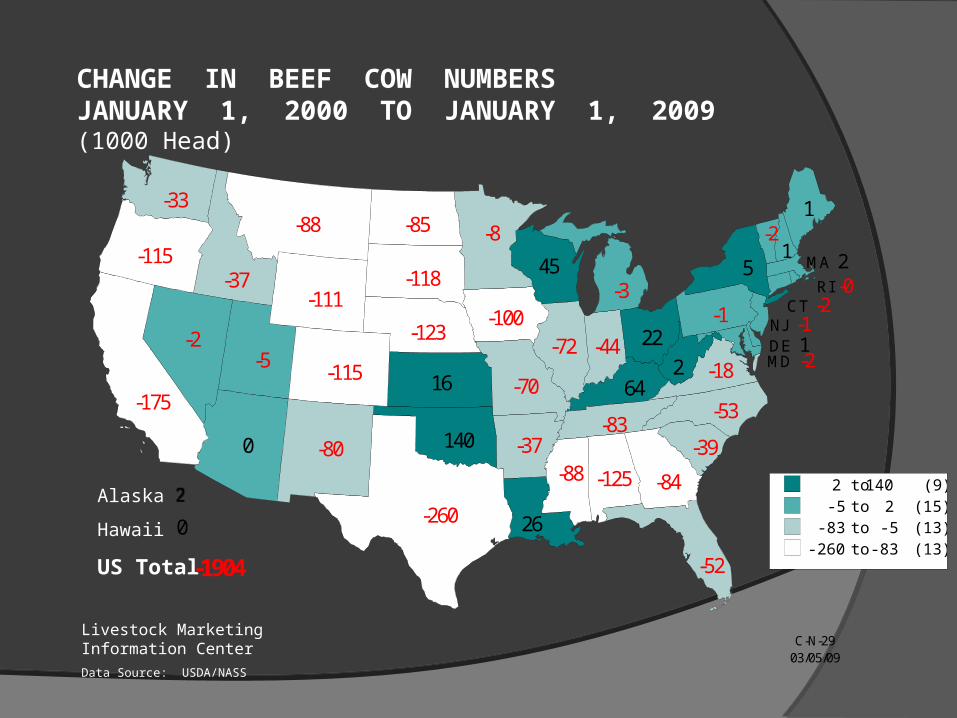

CHANGE IN BEEF COW NUMBERSJANUARY 1, 2000 TO JANUARY 1, 2009(1000 Head)

2 to 140 (9)-5 to 2 (15)

-83 to -5 (13)-260 to -83 (13)

C-N-2903/05/09

Alaska

Hawaii

US Total

-125

0 -37

-175-115

CT -2

DE 1

-52

-84

0

-37

-72 -44

16 64

26

1

MD -2

MA 2-3

-8

-88

-70

-88

-123-2

1

NJ -1

-80

5

-53

-85

22

140

-115

RI -0

-39

-118

-83

-260

-5

-2

-18

-33

2

45

-111

-1904

Livestock Marketing Information Center

Data Source: USDA/NASS

-100 -1

HEIFERS HELD AS BEEF COW REPLACEMENTS

July 1, U.S.

3

4

5

6

7

1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

Mil. Head

C-N-3707/24/09

-2.2 %

Livestock Marketing Information Center

Data Source: USDA/NASS

Livestock Marketing Information Center

BEEF COW SLAUGHTERFederally Inspected, Weekly

40

45

50

55

60

65

70

75

80

85

90Thou. Head

Avg.2003-07

2008

2009

C-S-3412/31/09

Longer Term Summary

Expansion in the beef herd unlikely till 2012

Prices still may recover quickly with a healthy economy

Rising input costs will negate some of the higher returns

Poultry on the Upswing

Returned to profitability after loss filled 2008Production even with year ago levels

Exports not as strong in 2009Production cutbacks restored profitabilityLowered feedstuff & energy prices improved

outlookByproduct values are higher than 2008

WHOLESALE CHICKEN BREAST PRICESSkinless/Boneless, Northeast, Truckload, Weekly

90

100

110

120

130

140

150

160

170

180Cents Per Pound

Avg.2003-07

2008

2009

P-P-0201/04/10

Livestock Marketing Information Center

Data Source: USDA/AMS

BROILER CHICKS PLACEDWeekly

150

155

160

165

170

175

180

185Mil. Birds

Avg.2003-07

2008

2009

Livestock Marketing Information Center

Data Source: USDA/NASS

P-S-1112/31/09

2010 Poultry Outlook

Projected 2% production increaseSlight increase in consumption

Trade issues with Russia Acquisition/merger impacts? Competition seminars Lending concerns?

Dairy Outlook

Demand is slowly starting to returnExport demand

Cold storage supplies need to decrease CWT buyouts provided positive

momentumSmaller dairy herds in the west

Livestock Marketing Information Center

DAIRY COW SLAUGHTERFederally Inspected, Weekly

30

35

40

45

50

55

60

65

70

75Thou. Head

Avg.2003-07

2008

2009

C-S-3512/31/09

CWT Buyouts

Livestock Marketing Information Center

MILK - FEED PRICE RATIOUS, Monthly

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

Jan Mar May Jul Sep Nov

Ratio

Avg.2003-07

2008

2009

12/31/09

Aquaculture

Aquaculture

Weaker dollar will not prevent increased imports

Consumer spending in 2010? Favorable supply conditions aid

productionSize of crawfish may be issue

○ Persistent cold weather ○ Overpopulation

Livestock Summary

Worst is likely behind the livestock industry2010 will not be a cakewalk however

Lower production will aid pricesEconomic recovery will increase impact of

lower productionChasing fewer consumer dollars?

How fast will input costs rise?

Email Newsletter

Sign up for twice a month marketing newsletter

Includes production tips, market news, and economic insight

Send email to [email protected] or contact your local extension agent

Questions?

Top Related