Languages

Pages

Legal

Philip Alexander

8 December 2011

Reporting for insurers

Reporting for insurers

• Financial reporting

– 2011 year-ends – financial reporting issues

– Convergence and the transition from UK GAAP to IFRS

– Update on the insurance International Financial Reporting Standard

• Solvency II – reporting disclosures update

Financial Reporting Issues – UK GAAP

• Period of reduced activity for the ASB but some revisions to UK Standards:

– FRS 8 – Related party transactions

– FRS 25 – Rights issues in foreign currencies

– FRS 30 – Heritage Assets

• Additionally, some UITF pronouncements:

– UITF 47 – Extinguishing Financial Liabilities with equity instruments (only applies if FRS 26 has been adopted)

– UITF 48 – the accounting implications of moving from the RPI to CPI for retirement benefits under final salary pension scheme

Financial Reporting Issues – IFRS

• Sir David Tweedie stood down, along with a number of IASB Board Members

– Housekeeping and conclusion of ongoing projects

– For year ends 31 December 2012 and 2013 there are a number of new pronouncements which effect financial reporting

– For 31 December 2011 year ends, limited revisions

• Main changes:

– IFRIC 19 – Extinguishing Financial Liabilities with Equity Instruments

– IAS 24 – Related parties

Convergence – the move to IFRS• Current landscape –three accounting bases

– FRSSE – smallest entities– UK GAAP– IFRS

• Internationally a move to IFRS for large and medium companies

• New GAAP– Full IFRS– IFRS with limited disclosures (for subsidiaries?)– IFRS for medium sized companies – the FRSME– FRSSE

• Problems defining the FRSME

• Timetable for convergence slipping – 2014 or even 2015?

• But insurers are likely to have to go full IFRS model

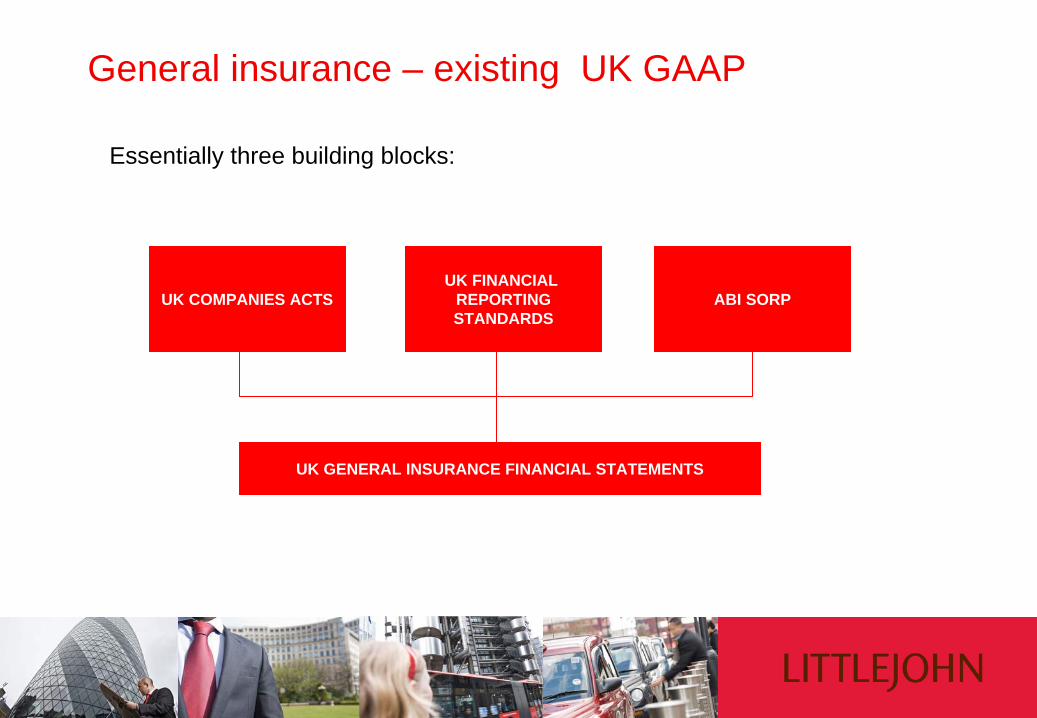

General insurance – existing UK GAAP

Essentially three building blocks:

UK COMPANIES ACTS ABI SORPUK FINANCIAL

REPORTINGSTANDARDS

UK GENERAL INSURANCE FINANCIAL STATEMENTS

General insurance – Under IFRSEssentially building blocks:

• No ABI Sorp

• IFRS 4 – Interim standard, does not deal with insurance liability measurement defaults to UK GAAP position, in most circumstances

UK COMPANIES ACTSIFRS 4 –

DisclosuresContract definition

INTERNATIONALFINANCIAL

REPORTINGSTANDARDS

UK GENERAL INSURANCE FINANCIAL STATEMENTS

But we have a ‘new’ IFRS 4• Not yet defined and different time lines suggested by the ASB

2012 – IASBissue IFRS 4

revised

2013 – EUAdoption

2014Solvency II & convergence?

2016 – IFRS 4revised adopted

in the EU

Optimistic

Potential 2 Year Gap

2014Solvency II &convergence?

2016 – IASBissue IFRS 4

revised

2017 – IFRS 4revised adopted

In the EU

2018 – IFRS 4revised early

implementation

Pessimistic

Potential 4 Year Gap

What to do in the gap periods

Simplifies the accountingrequirements

Some consistency across the market

BUT

Preparers to consider changesin accounting policies arising from insurance

contract definitions

Inconsistencies in accounting for insurance

liabilities

Further change with newstandard

Incorporate the currentversion of IFRS 4

into UK GAAP

Single platform forRegulatory and Financial

Reporting

Good quality financialinformation

Consistency

BUT

Short implementation

Further change with newstandard

Incorporate SolvencyII Rules intoUK GAAP

Only one change required

Better quality financialinformation

Consistency

BUT

Short implementation

Will the ED become the Standard

Incorporate IFRS 4revised intoUK GAAP

What will revised IFRS 4 look like? (Possibly!)

• Liabilities measured as the amount required to fulfil the contractual obligations over the lifetime of a contract

• Measured at discounted fulfilment cash flows plus a risk adjustment

• Maximum amount an insurer would rationally pay to be relieved of the risk that the ultimate fulfilment cash flows exceed those expected

• Additional component – the residual margin to eliminate day 1 profits

IFRS Balance Sheet

Risk allowance

Residual margin

Equity

Discounted probabilityweighted

estimate offulfilmentcash flows

Developments since the Exposure Draft

• General positive movements, recognition that general business is different to life

– Concern over long term policies e.g. construction– Materiality– Disclosure if material amounts of ‘longer term’ business

• No day one profits– Sounds similar to existing accounting – UPR

• Contract boundary– Now starts when policy incepts – ED as soon as risk taken on to the books– Exception for onerous contracts

• Disclosure

Areas of debate

• Consistency with FASB residual margin is the key sticking point – FASB want a single risk margin / acquisition costs

• Presentation – what level of disaggregation should be on the face of the accounts

• Short term contracts – should these be accounted for using building block approach

• How to present changes in insurance liabilities through SOCI • Transition

2010 2011 2012 2015

IASB Exposure Draft –

Insurance Contracts

Major pieces of the model put

together

IASB issue review draft or

re-expose

Sometime after 1 January – new IFRS for

insurance contracts

Presentation by Neil Coulson

December 2011

Solvency II reporting - update

Solvency II reporting

• Solvency and Financial Condition Report (SFCR)– Narrative public disclosure

• Regular Supervisory Reporting (RSR)– Narrative reporting to supervisor

• Quantitative Reporting Templates (QRT)– Quarterly / Annually

• Not ORSA

Reporting timetable

• Public consultations potentially ongoing through 2012 – (Potentially through to 2016 for refinements)

• Reporting to supervisor to demonstrate preparation at mid 2013– First reporting 31 March 2014 quarterly QRTs

• First reporting 31 December 2014 annual SFCR, RSR, QRTs– Potential 2 year transition for SFCR where systems cannot provide all

information

Consultation on reporting

See consultations under www.eiopa.eu• Originally CP58 in July 2009 – QRT detail only provisional

• Since then changes to level 2 requirements not formally consulted upon– Most requirements are at level 2 for SFCR & RSR

• New level 3 consultation issued 8 November 2011 closes 20 January 2012– Details & instructions for QRTs– No additional requirements to level 2 for SFCR & RSR– Only guidance on some items

• Valuation of assets & liabilities / intergroup transactions• SFCR policy on disclosure / RSR policy on reporting

Application to Lloyd’s?

Lloyd’s is the regulated and reporting entity

• Lloyd’s will therefore produce an aggregate SFCR & RSR

• Will collate template information by extending quarterly reporting from syndicates

– Primarily quantitative but also some qualitative data including ORSA

• Reduced timelines for syndicates to permit Lloyd’s to collate within deadlines

• Lloyd’s will issue an update in December to explain latest proposals & give guidance of collation of qualitative information

Solvency & Financial Condition Report (SFCR)

• Annual report to the public

• Posted on website

• Prescribed format

• Single Group SFCR – supervisor approval – must cover all subsidiaries

• References to other documents must be to specific item – not general hyperlink

• Also a small number of annual QRTs to public

• Undertaking’s disclosure policy– Seek permission of supervisor not to disclose– Not disclose confidential information from supervisor– Supervisor can require additional disclosure

Regular Supervisory Reporting (RSR)

• Annual report to supervisor– Or up to every 3 years with annual summary of material change

• Stand alone document – no reference to other documents

• Similar format to SFCR with additional detail

• Supported by larger number of QRTs– Small number of quarterly QRTs

• Undertaking’s reporting policy - approval

SFCR layout

• Summary

• Business & performance (5 sub-headings) – Including – business written, underwriting & investment performance

• System of governance (8) – Including – structure, fit & proper, ORSA, risk management, controls,

internal audit, actuary, outsourcing

• Risk profile (7)– Including underwriting, market, credit, liquidity, operational.

• Valuation for solvency purposes (4)– Including - assets, liabilities, technical provisions.

• Capital management (6)– Including – own funds, MCR, SCR, difference between model and standard

SFCR requirement changes

• Largely the same as CP58 – Still 32 headings and sub-headings• Some deletions and additions including:

– Comparatives required for business performance except for first year

– Transactions with shareholders & key people added

– Expenses by business line & geographic area deleted

– Details of amortisation/impairment of investments deleted

– Adequacy of system of governance deleted

– Less disclosure of internal audit & actuarial function

Quantitative reporting templates

• Cover solvency, balance sheet, underwriting, technical provisions, investments, reinsurance, future cash flows

– Up to 44 annual templates to supervisors if include life, health and non- marine

– If applicable up to 12 templates are also required at Ring Fenced Fund level

– Up to 10 additional templates for groups

• Up to 11 quarterly templates to supervisors

• The forms do not cover all areas of current FSA returns– Possible additional local returns – allowed for specific national

requirements

• Required to be submitted in XBRL

Quantitative reporting templatesForm Public disclosure Quarterly returnsBalance Sheet Y Y*Premium, claims, expenses Y YOwn funds Y YSCR YMCR Y YTechnical provisions Y YInvestment portfolio list Y*Derivatives Y*Outward reinsurance – next year Y*Group – entities in scope YGroup – counterparty risk concentration Y

*possible exemptions

QRTs key changes

• Detailed investment lists – Quarterly for insurers representing 90% of EU or 75% of country

insurance assets

• Reporting by underwriting or accident year– Not mandated by EU but may be by national supervisor

• Triangulations– Required by both E3 triangulations and E4 tabular claims movements

• Balance sheet– Only required quarterly if own fund & technical provision QRTs not

explain movement

• Variation analysis– Annual to supervisor to explain SII balance sheet movements

Audit

• Historically not required in Europe at present

• Audit requirement referred to in level 1 and 2 text but not specific

• EU informally indicating may leave to local supervisors

• If required unclear which QRT forms will require audit– More likely on the public returns– Unclear who opinion is addressed to & what form of opinion

• Lloyd’s will first require a review opinion from auditors on Solvency II balance sheet as at 30 June 2012

• Solvency II risk & solvency disclosures from SFCR & QRT likely to be included in future financial statements as a result of IFRS

Deadlines

• Annual SFCR & annual public QRTs– First year 20 weeks after year-end reducing by 2 weeks each year for

next 3 years to 14 weeks– For Lloyd’s syndicates 12 weeks reducing to 8 weeks

• Annual RSR & supervisor QRTs– As for SFCR

• Quarterly QRTs– First year 8 weeks after quarter-end reducing by 1 week for each of next

3 years to 5 weeks– For Lloyd’s syndicates 5 weeks reducing to 3 weeks

Supervisory reporting – pre-defined events

• Pre-defined event– Change in strategy– Mergers / Restructuring– Significant lawsuits / Emerging material internal/external risks– Material change in solvency position– Significant governance/operational failure / Fit & proper issues– SFCR/RSR not approved by AGM or auditors– Very significant intra-group transactions

• Update sections of RSR

• Consider additional ORSA

• Public disclosure of appropriate information – If non-compliance with MCR or significant non-compliance with SCR

Next steps

• Consultation response to EIOPA

• Plan improved timelines

• Gap analysis for QRTs

• Consider marketing importance of public reporting – long document

This seminar and the accompanying handouts cover topics only in general terms and are intended to give a wide audience an outline understanding of issues relating to accounting applicable to entities in the insurance sector, and therefore cannot be relied upon to cover specific situations; applications of the principles would depend on the particular circumstances involved. Furthermore, responses given in the seminar to questions are only based on an outline understanding of the facts and circumstances of the cases and therefore do not form an appropriate substitute for considered specific advice tailored to your circumstances. We recommend that you obtain professional advice before acting, or refraining from acting, on any of the contents. We would be pleased to advise you on the application of the principles demonstrated at the seminar, or on any other matters, to your specific circumstances, but in the absence of such specific advice, we cannot be responsible or held liable.

© Littlejohn

Top Related