Languages

Pages

Legal

PwC’s Non-Banking Financial Company Insights Analysis of regulatory changes and impact assessment January–April 2017

2 PwC PwC’s Non-Banking Financial Company Insights

PwC’s Non-Banking Financial Company Insights

Preface Disbursal of loan amount in cash Review of guidelines on ‘Pricing of Credit’ Other notifications issued by RBI from January–April 2017 Contacts

The non-banking financial companies (NBFC) industry experienced significant growth in December 2016. The Finance Minister Arun Jaitley, in his 2017–18 Union Budget speech on 1 February 2017, announced a host of measures and incentives to boost the NBFC sector and fuel economic growth. Some of the highlights are listed below:

• NBFCs with high net worth will now be able to access capital markets to raise funds as the government has allowed them to list their stocks with different stock exchanges. High net worth NBFCs can also participate in initial public offerings (IPOs) like banks and insurance companies do. This will help NBFCs grow and bring them at par with other banks and financial institutions.

• Systemically important NBFCs (asset size of 500 crore INR and above) regulated by RBI may be categorised as qualified institutional buyers (QIBs) by SEBI. This will help strengthen the IPO market and increase its money supply.1

• NBFCs are set to benefit from the Credit Guarantee Scheme and the interest subsidy on affordable housing loans. This move could benefit housing finance companies/mortgage firms. Two new middle-income categories have been created under the Pradhan Mantri Awas Yojana (PMAY) in urban areas, under which loans of up to 9 lakh INR will receive interest subvention of 4% and loans up to 12 lakh INR will get a 3% benefit.

• Indirect tax proposals: NBFCs are required to consider interest/discount on the value of exempt income while opting for a proportionate reversal scheme.2

RBI has notified NBFCs of the following:

• NBFCs cannot lend more than 25,000 INR in cash against gold as directed by RBI.

• High-value loans against gold of 1 lakh INR and above must only be disbursed by cheque.

1 PTI. (2017). Budget 2017: High net worth NBFCs can access capital markets via IPOs. Retrieved from http://www.livemint.com/Politics/vJoQu2jpI3bazZFadaRPJM/Budget-2017-High-net-worth-NBFCs-can-access-capital-markets.html (last accessed on 12 May 2017)

2 PwC. (2017). Budget 2017: Key proposals for Financial Services Sector. Retrieved from https://www.pwc.in/assets/pdfs/budget/2017/budget_2017_key_proposals_for_financial_services_sector.pdf (last accessed on 12 May 2017)

3 PwC PwC’s Non-Banking Financial Company Insights

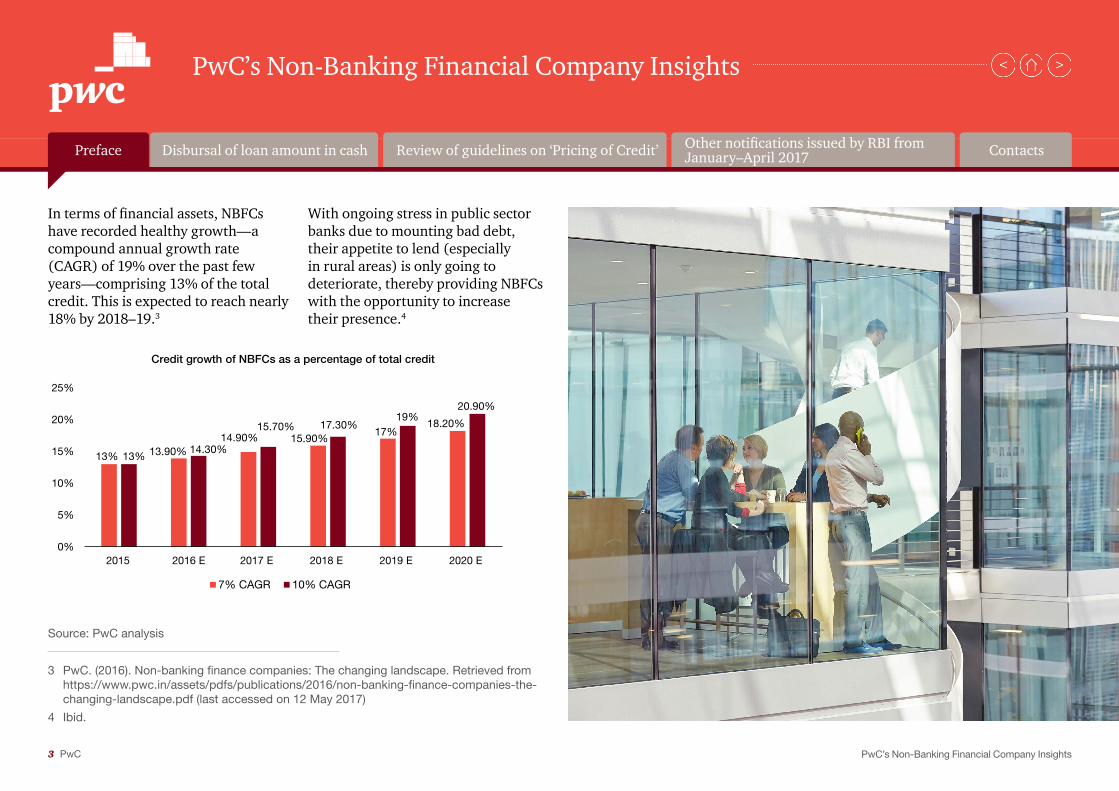

In terms of financial assets, NBFCs have recorded healthy growth—a compound annual growth rate (CAGR) of 19% over the past few years—comprising 13% of the total credit. This is expected to reach nearly 18% by 2018–19.3

With ongoing stress in public sector banks due to mounting bad debt, their appetite to lend (especially in rural areas) is only going to deteriorate, thereby providing NBFCs with the opportunity to increase their presence.4

3 PwC. (2016). Non-banking finance companies: The changing landscape. Retrieved from https://www.pwc.in/assets/pdfs/publications/2016/non-banking-finance-companies-the-changing-landscape.pdf (last accessed on 12 May 2017)

4 Ibid.

13% 13.90%14.90% 15.90%

17%18.20%

13%14.30%

15.70% 17.30%19%

20.90%

0%

5%

10%

15%

20%

25%

2015 2016 E 2017 E 2018 E 2019 E 2020 E

Credit growth of NBFCs as a percentage of total credit

7% CAGR 10% CAGR

Source: PwC analysis

PwC’s Non-Banking Financial Company Insights

Preface Disbursal of loan amount in cash Review of guidelines on ‘Pricing of Credit’ Other notifications issued by RBI from January–April 2017 Contacts

4 PwC PwC’s Non-Banking Financial Company Insights

Background and objective:

Ref:RBI/2016-17/245 DNBR (PD) CC.No.086/03.10.001/2016-17

Date of notification: 09 March 2017

Applicable entities: All NBFCs

RBI circular reference:

As per the directions given in Non-Banking Financial Company – Non-Systemically Important Non-Deposit taking Company (Reserve Bank) Directions, 2016, and Non-Banking Financial Company – Systemically Important Non-Deposit taking Company and Deposit taking Company (Reserve Bank) Directions, 2016, under para 37(iii)(b), high-value loans against gold of 1 lakh INR and above must only be disbursed by cheque.

However, to align with the requirements of the Income-tax Act, 1961, section 269SS and 269T are now applicable to all NBFCs with immediate effect.

Section 269SS states that a person shall not take or accept a loan/deposit from another person otherwise than

by the prescribed banking channels, i.e. a/c payee cheque or account payee bank draft or by use of an electronic clearing system, so that the aggregate from such a person is 20,000 INR or more.

Further, section 269T states that no repayment of any advance received in relation to a transfer of immovable property will be made except by the said prescribed banking channels if the aggregate is 20,000 INR or more—whether the transfer takes place or not is irrelevant.

RBI’s move is being seen as part of its ‘go digital’ drive post-demonetisation and a way to curb black money in the economy. However, the purpose of gold loans may be defeated since they are usually used during medical emergencies.

Implications for NBFCs• Due to this new threshold limit,

NBFCs will not be able to make part disbursements or accept part repayments in cash and cheque (section 269SS).

• In order to keep their businesses alive, NBFCs may want to guide farmers with opening a bank account to allow smooth disbursement of loans, keeping in mind that the average ticket size is 25,000 INR to 35,000 INR.

• NBFCs may need to set up procedures and strengthen them to speed up the process of disbursing loans to small marginal borrowers as these small borrowers are often in immediate need of cash to meet their liabilities.

• NBFCs will also need to track the repayment of loans in cheques for which disbursements were made in cash prior to the notification since

part repayment of loans in cash will be hampered.

• Non-compliance with the threshold limit as stated in the guideline will attract a penalty under section 271D.

Some points that NBFCs need to consider are:

• In order to obtain loans faster, will marginal borrowers turn to pawnbrokers despite extremely high interest rates?

• Will small-time borrowers help the economy transform into a ‘cashless economy’ by opening bank accounts?

• Will interest rates on loans charged by NBFCs be affected?

• If multiple loans are disbursed to a single borrower, will they be considered to exceed the threshold limit for marginal borrowers?

PwC’s Non-Banking Financial Company Insights

Preface Disbursal of loan amount in cash Review of guidelines on ‘Pricing of Credit’ Other notifications issued by RBI from January–April 2017 Contacts

5 PwC PwC’s Non-Banking Financial Company Insights

Background and objective:The interest rate to be charged by NBFC-MFIs, as outlined by RBI, is the average of the base rates of the five largest commercial banks.

RBI has now notified NBFC-MFIs to ensure that the average interest rate on loans sanctioned during a quarter does not exceed the average borrowing cost during the preceding quarter plus the margin within the prescribed cap.

Earlier, the rate charged by NBFC-MFIs depended on the average borrowing cost during a financial year plus the margin.

Further, the average base rate is decided by RBI on the last working day of every quarter (9.75% for the quarter starting 1 April 2017).

Implications for MFIs• NBFCs need to streamline their

interest rate on a quarterly basis based on the rate provided by RBI.

• The top management of NBFCs may want to formulate and design internal principles for defining interest rates and review the average borrowing cost on a quarterly basis along with the average interest rate on loans sanctioned during a quarter.

• New procedures and processes need to be set in the company for comparing the interest rates and margins on a quarter-on-quarter basis.

• MFIs will also need to prepare quarterly reports showing compliance to the above-mentioned notification.

• Along with interest rates, NBFCs need to regularise processing fees and other charges.

• The number of complaints filed by customers regarding NBFCs charging high interest rates/penal charges has increased. NBFCs may want to formulate a plan to ensure that these complaints are reduced in the near future.

PwC’s Non-Banking Financial Company Insights

Ref:RBI/2016-2017/219 DNBR.CC.PD.No.084/22.10.038/2016-17

Date of notification: 02 February 2017

Applicable entities: All NBFC-MFI

RBI circular reference:

Preface Disbursal of loan amount in cash Review of guidelines on ‘Pricing of Credit’ Other notifications issued by RBI from January–April 2017 Contacts

6 PwC PwC’s Non-Banking Financial Company Insights

Circular reference number Name of the circular Brief impact/instructions

RBI/2016-17/242 DNBR.PD.CC.No.085/03.10.001/ 2016-17

Financing of Infrastructure – Definition of ‘Infrastructure Lending’

• RBI further updated the harmonised master list of infrastructure sub-sectors. In this regard, it is advised that with respect to the definition of ‘infrastructure lending’, NBFCs may henceforth be guided by the gazette notifications issued by the Department of Economic Affairs, Ministry of Finance, Government of India, from time to time.

• ‘Infrastructure lending’ means a credit facility extended by an NBFC to a borrower by way of a term loan/project loan/subscription to bonds/debentures/preference shares/equity shares in a project company acquired as a part of the project finance package such that the subscription amount is ‘in the nature of advance’ or any other form of long-term funding for exposure in infrastructure sub-sectors as notified by the Department of Economic Affairs, Ministry of Finance, Government of India, from time to time.

PwC’s Non-Banking Financial Company Insights

Preface Disbursal of loan amount in cash Review of guidelines on ‘Pricing of Credit’ Other notifications issued by RBI from January–April 2017 Contacts

7 PwC PwC’s Non-Banking Financial Company Insights

Vivek Iyer Partner [email protected] Mobile: +91 9167745318

Gaurav Mehta Manager [email protected] Mobile: +91 9820082799

Dnyanesh Pandit Director [email protected] Mobile: +91 9819446928

PwC’s Non-Banking Financial Company Insights

Preface Disbursal of loan amount in cash Review of guidelines on ‘Pricing of Credit’ Other notifications issued by RBI from January–April 2017 Contacts

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 157 countries with more than 2,23,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com

In India, PwC has offices in these cities: Ahmedabad, Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata, Mumbai and Pune. For more information about PwC India’s service offerings, visit www.pwc.com/in

PwC refers to the PwC International network and/or one or more of its member firms, each of which is a separate, independent and distinct legal entity in separate lines of service. Please see www.pwc.com/structure for further details.

©2017 PwC. All rights reserved.

About PwC

pwc.inData Classification: DC0

This document does not constitute professional advice. The information in this document has been obtained or derived from sources believed by PricewaterhouseCoopers Private Limited (PwCPL) to be reliable but PwCPL does not represent that this information is accurate or complete. Any opinions or estimates contained in this document represent the judgment of PwCPL at this time and are subject to change without notice. Readers of this publication are advised to seek their own professional advice before taking any course of action or decision, for which they are entirely responsible, based on the contents of this publication. PwCPL neither accepts or assumes any responsibility or liability to any reader of this publication in respect of the information contained within it or for any decisions readers may take or decide not to or fail to take.

© 2017 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Private Limited (a limited liability company in India having Corporate Identity Number or CIN : U74140WB1983PTC036093), which is a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of which is a separate legal entity.

AW/May2017-9641

Top Related