Languages

Pages

Legal

Providing an Enabling Regulatory Environment to Enhance Access to

Finance for MSMEs.

A Joint Regional Symposium: "Best Practice Regulatory Principles A Joint Regional Symposium: "Best Practice Regulatory Principles Supporting MSME Access to Finance" 27-28 June 2011Supporting MSME Access to Finance" 27-28 June 2011

Mary Rose A. Contreras Core IT Specialist Group

Supervision and Examination Sector

AGENDA

Current Financial Landscape and Mobile Penetration

E-Money and Business Models

E-money: Enhancing MSMEs access to finance

Creating an Enabling Environment with Proportionate Regulations

Tasks Ahead

99% mobile phone coverage

KBs, TBs, RBs and 9000 ATMS are located in cities and big towns

26% of Filipinos have access to formal financial channels

More than 75% of the population have mobile phones

610 out of 1635 municipalitiesdo not have banks

2B text messages/day

90M Population

Financial Landscape & Mobile Penetration

CIRCULAR 649 – Guidelines on E-Money Issuance and Operations of E-Money Issuers

Monetary value Monetary value as represented by a claim on its issuer, that is –

a. Electronically stored in an instrument or device;

b. Issued against receipt of funds of an amount not lesser in value than the monetary value issued;

c. Accepted as a means of payment by persons other than the issuer;

d. Withdrawable in cash or cash equivalent; and

e. Issued in accordance with BSP Circular No. 649 dated 9 March 2009

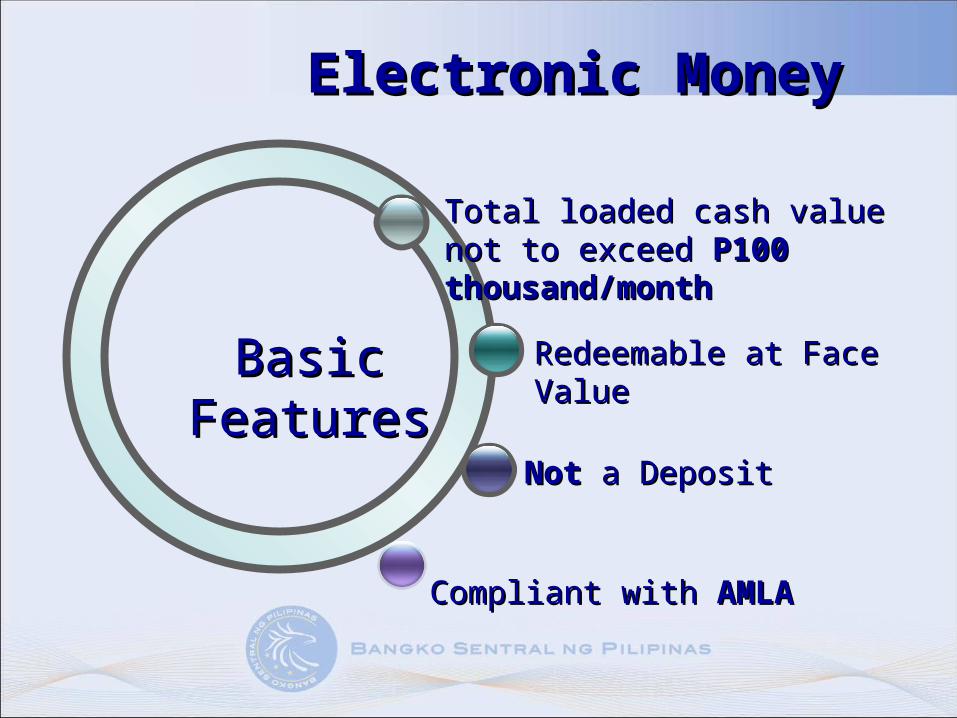

Redeemable at Face Redeemable at Face ValueValue

NotNot a Deposit a Deposit

Total loaded cash value not to Total loaded cash value not to exceed exceed P100 thousand/monthP100 thousand/month

Compliant with Compliant with AMLAAMLA

Electronic MoneyElectronic Money

BasicBasicFeaturesFeatures

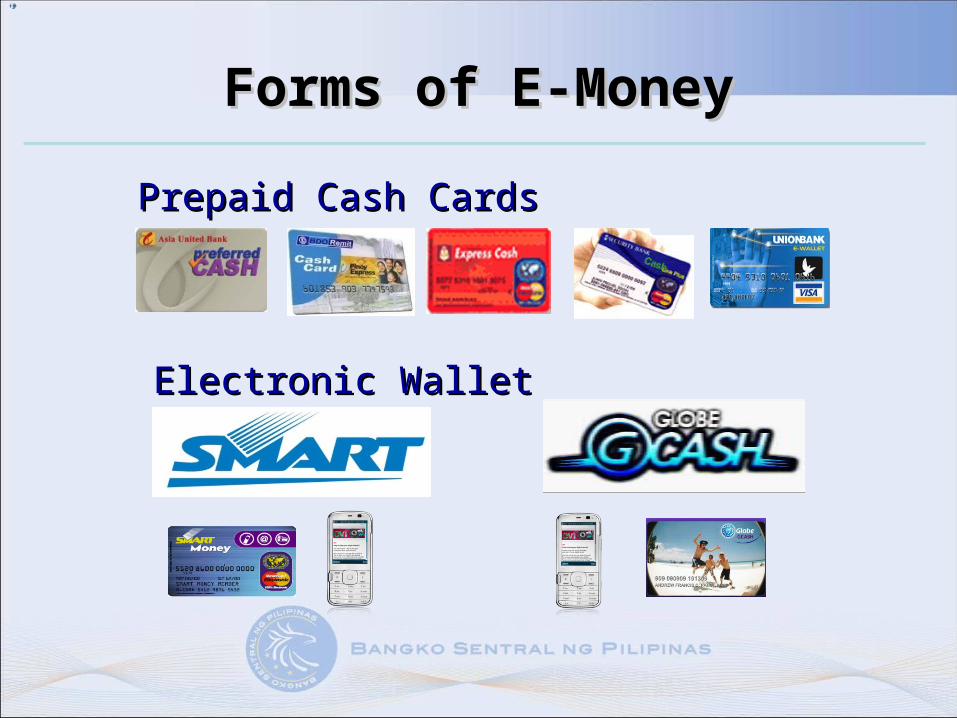

Forms of E-MoneyForms of E-Money

Prepaid Cash CardsPrepaid Cash Cards

Electronic WalletElectronic Wallet

ACCREDITED REMCO

OUTLET

Remittance

-11h -10h -09h -08h -07h -06h -05h -04h -03h -02h -01h00h

+01h +02h +03h +04h +05h +06h +07h +08h +09h +10h+11h

Expanding Financial Access Through Innovative Technology

Purchase of Goods

Payment of Fare

Banking Products- Deposits- Loans- Bills Payment

Utility Bills Payment

Payment of School Fees

Payment of Taxes and

Licenses

Person-to-Person

Transfer

E-money: Enhancing Access to Finance for MSMEs

• Loan Release• Loan Payment• Deposit Build-up

Loan Release

1 Upon loan application, client already indicates his e-money/e-wallet account number

2 Upon loan release, client shall receive an SMS notification on the credited loan proceeds to e-wallet

3 Client can go to any Cash Out center to convert electronic money to actual cash

Loan amount has been credited to

XXXXXXXXXX0005. Thank you for using this

service

Loan Payment

1 Client chooses loan payment from menu, enters the amount to be paid, enters his PIN to authorize the transaction

2 Client and the lending bank shall receive an SMS notification upon fund transfer from client’s e-wallet to lending bank’s e-wallet

3 Lending bank records the loan payment made in step 2

Amount of P100 has been transferred

to/from XXXXXXXXXX03452.

Thank you for using this service

Deposit build-up

1 Client chooses text-a-deposit from menu, enters the amount, enters his PIN to authorize the transfer of e-money value from his wallet to bank’s wallet

2 Client and the depositary bank shall receive an SMS notification upon fund transfer from client’s e-wallet to depositary bank’s e-wallet

3 Depositary bank records the amount to the client’s deposit account.

Amount of P100 has been transferred

to/from XXXXXXXXXX03452.

Thank you for using this service

Benefits to UsersBenefits to Users

Reduced travel time & costReduced travel time & cost

Reduced riskReduced risk

ConvenientConvenient

AvailabilityAvailability

Time savingTime saving

1.1. Allow non-banks to offer e-moneyAllow non-banks to offer e-money2.2. Remittance Agents allowed to perform Remittance Agents allowed to perform

Cash-In/Cash-OutCash-In/Cash-Out3.3. Simplification of requirements for KYCSimplification of requirements for KYC4.4. Formalized guidelines on issuance of Formalized guidelines on issuance of

electronic moneyelectronic money5.5. Allowed microfinance-oriented OBO Allowed microfinance-oriented OBO

limited transactional banking activitieslimited transactional banking activities

Creating an Enabling Environment with Creating an Enabling Environment with Proportionate RegulationsProportionate Regulations

Latest BSP Regulatory Initiatives• Circular 649 (January 2009)- Regulating the issuance

of electronic money – Definition of e-money and EMIs– EMI as the supervised entity of Bangko Sentral– Qualification standards of both bank/ non bank

issuers such as Capital, Risk Management and Liquidity Cover

– Compliance to AML rules– Consumer protection standards including Adequate

Disclosure

Latest BSP Regulatory Initiatives• Circular 704 (December 2010)- Electronic Money Network

Service Providers (EMNSP)– Smaller banks aiming to be EMIs can engage services of EMNSP – Stressed Due Diligence and Continuing Operational Review

• Circular No. 706 (January 2011) – Updated AML rules and regulations– Reduced due diligence for low risk clients– Reliance on third-party KYC

• Circular 694 (October 2010)- Microfinance-oriented other banking offices (MF-OBO)– MF-OBO can perform limited transactional banking

activities: micro-deposits, release micro-loans, etc.

TASKS AHEADTASKS AHEAD

Success breeds new challenges and risks.

Steady advocacy for responsible financePrice transparency Consumer Protection

Close monitoring of market practices and developments

Financial literacy promotion

Top Related