Languages

Pages

Legal

Proprietary & Confidential – E-LOAN, Inc. ©2005

Page 2

This presentation contains forward-looking statements based on

current expectations that involve risks and uncertainties. E-LOAN

actual results may differ from the results described here. Factors

that could cause actual results to differ include, but are not limited

to, general conditions in the lending industry, interest rate

fluctuations, and the impact of competitive products. These and

other risk factors are detailed in reports E-LOAN files with the

Securities and Exchange Commission.

Safe Harbor

Page 3

Refinance

Purchase

Auto

Home Equity

$1,174 B

$692 B$431 B

$1,479 B

* MBAA (Mortgage), SMR Research (Home Equity), Company Estimate (Auto)** Revenue estimate assumes the market revenue basis points is equal to E-LOAN Q4 2004 levels.

• 2004 Originations of $3.8 Trillion

• $80 Billion Revenue Market

Consumer Lending Market

Page 4

• Unnecessary Costs and ConflictsHighly compensated sales people

Pricing based on negotiation not creditworthiness

Recommendations based on salesperson’s commission structure

• Confusing and Mistrusted ProcessLack of pricing transparency – “junk fees”

Complex terminology – “points, index rate, impounds”

Lack of control – distrust of process and profession, “black box”

• Slow ProcessMany intermediaries – time demand on customer

Too much paperwork – disclosures, documentation

Problem: Getting a Loan is a Pain

Page 5

• Leverage the InternetCreate Customer Loyalty Through Transparency

Reduce Customer Acquisition Costs

Reduce Loan Processing Costs – Offshore & Paperless Process

• Apply a Manufacturer Mentality to Lower Costs

• Eliminate the Middleman

E-LOAN Solution: Streamline the Process

Page 6

Shop

Apply

Underwrite

Document

Fund

Monitor

$

Brokers/Auto Dlrs.

WholesaleLenders

RetailLenders E-LOAN

LeadCompanies

End-to-End Solution

Page 7

Fast ProcessGreat Rates

Internet = Enormous Operating Leverage

Low Cost Producer

Low Rates

Market Share

Scale

Page 8

927 25

43

8098

122

7

13

9

43

60

73 37

43

$0

$20

$40

$60

$80

$100

$120

$140

$160

1998 1999 2000 2001 2002 2003 2004 2005Est*

$ M

illio

ns

Refinance

Diversified

* Guidance as of February 17, 2005 (Q4’04 Earnings Conference Call)

153

103

68

36

22

135

165

Our Revenue has Grown…

Page 9

RefinanceMortgagePurchaseMortgageNon-PrimeMortgage (1)Auto

Home Equity (2)

Q1 2003

Total Revenue $36 M

Diversified Revenue $15 M

Q1 2005

Total Revenue $38 M

Diversified Revenue $27 M

(1) Non-Prime originations, similar to purchase mortgages, have proven to be stable in various interest rate environments. (2) Q1 2005 includes revenue from E-LOAN Closing Services, Inc.

58%

30%16%

8%12%

16%

34%

14%

6%

6%

… and Diversified for Greater Predictability

Page 10

2002($ in billions)

2003

($ in billions)

2004($ in billions)

Total US Home Equity Originations (1) 257 327 431

Total Value of US Homes (2) 14,900 16,000 17,100

Total US mortgage debt outstanding (2) 6,900 7,600 8,300

Total US home equity available (2) 8,000 8,400 8,800

• Significant home equity available to borrowers

• Lower rates & tax advantages compared to credit card debt

Source: (1) SMR Research: Home Equity Loans: 2005 Outlook (exclusive of any home equity securitizations done by non-federally regulated institutions (2) Federal Reserve, NYSE and NASDAQ

Home Equity Finance Market

Page 11

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

$ M

illio

ns

* Source: Mortgage Bankers’ Association of America

Large, Stable, Growing Market

Purchase Mortgage Market

Page 12

2002 2003 2004 Target

% Diversified Revenue 42% 53% 72% 85%

Revenue 100% 100% 100% 100%

Expenses:

Operations 51% 46% 49% 40%

Marketing 25% 27% 35% 27%

Technology 6% 6% 7% 7%

G&A 7% 6% 9% 6%

Pre-tax Income 11% 16% 1% 20%

E-LOAN Financial Model

Page 13

• Gain on sale of loansFirst Mortgages, Home Equity, & Subprime Auto = cash gain on sale

Prime Auto Loans = discounted cash flow gain on sale

• Interest spread on loans held prior to saleMortgage & Home Equity = typically held approx. 30 days

Auto Loans = typically held under 10 days

Loan Average Loan Size Gain On Sale - Basis Points Gain On Sale - Dollars

Mortgage $ 215,000 207 bps $ 4,500

Home Equity $ 54,000 305 bps $ 1,630

Auto * $ 16,000 220 bps $ 300

Q1 2005

How We Make Money

* Excludes the $2.65 benefit from the QSPE Auto loan sale

Page 14

Expense MortgageHome Equity

Auto

Headcount & Related 50% 63% 66%

Commissions 21% 13% ---

Processing Costs 18% 15% 20%

Facilities & Other 11% 9% 14%

• Majority of cost is headcount & commission related (66% - 71%)

• Significant leverage to operations cost as we automate process

Operations Cost Mix

Page 15

• Labor Cost

Offshore – India & Philippines

Express / “No Commission” Products

Process automation / streamline efforts

• Technology Automation

Paperless loan processing

Upgraded loan origination system

Expand automated underwriting

Tools to improve application to fund conversion

Operations Cost Initiatives

Page 16

Product Q1 2005 Target % Change

Mortgage $ 1,830 $ 1,250 (32%)

Home Equity

$ 800 $ 500 (38%)

Auto $ 250 $ 125 (50%)

• Includes both fixed and variable costs to originate & sell loans

• Excludes interest expense

Operations Cost Per Loan

Page 17

• Shift to internet marketing – online advertising / search

Television

Direct Mail

Online/Search

Other

Overhead

Q1 2004

Total Marketing $11.1 M

Q1 2005

Total Marketing $13.4 M

54%45%

15%

1%

11%

1%

8%

5%

19%

41%

Marketing Mix is Evolving

Page 18

Early Uses

Simple Purchases

Books

Music

Financial Transactions

Pay Bills

Trade Stocks

Airline Tickets

Online Loans

Security

Privacy

More Experience

Complex Uses

Evolution of Internet Usage

Page 19

0.90%

3.60%

2.50%

6.10%

2001 2007

Purchase Refinance

Online % of Market

Source: Jupiter Research [Oct 2002]

Online Growth – Internet Home Mortgage

Page 20

• Lower Acquisition Costs Maximize advertising channel spend through use of application attribution model

Lower TV costs through fixed rate purchases, better station selection and enhanced focus on profitable local markets

Use recent trademark registration to lower search word costs

More aggressive approach to obtaining Internet partnerships

• Better Utilize Substantive Brand We’ve Developed 90% of customers say they are highly likely to use us again, another 6% say they are

likely – they cite our fast, easy, transparent and affordable approach

• Increase Realtor Partnerships

Marketing Initiatives

Page 21

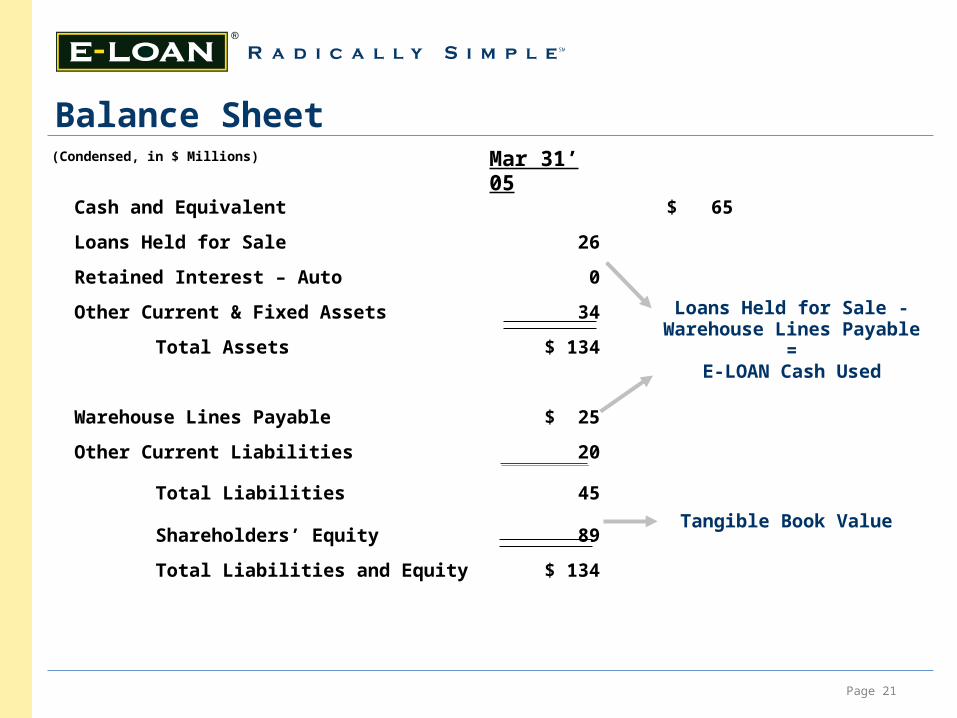

Cash and Equivalent $ 65

Loans Held for Sale 26

Retained Interest – Auto 0

Other Current & Fixed Assets 34

Total Assets $ 134

Warehouse Lines Payable $ 25

Other Current Liabilities 20

Total Liabilities 45

Shareholders’ Equity 89

Total Liabilities and Equity $ 134

(Condensed, in $ Millions) Mar 31’ 05

Tangible Book Value

Loans Held for Sale -Warehouse Lines Payable

=E-LOAN Cash Used

Balance Sheet

Proprietary & Confidential – E-LOAN, Inc. ©2005

Top Related