Languages

Pages

Legal

Managerial Exposure to Losses

Aloke (Al) Ghosh Stan Ross Department of Accountancy

Baruch College, The City University of New York Box B12-225, One Bernard Baruch Way

New York, NY 10010 e-mail: [email protected]

and

Doocheol Moon School of Business Yonsei University

Seoul, Korea e-mail: [email protected]

November 2010

Managerial Exposure to Losses 1. Introduction

In a recent study, Roychowdhury (2006) provides persuasive evidence consistent with

the premise that managers manipulate operating (‘real’) activities to avoid reporting losses. By

deviating from normal operations, managers avoid reporting losses through cash flow from

operations. Similarly, the discontinuity in the frequency of firm-years around zero earnings (e.g.,

Hayn 1995, Burgstahler and Dichev 1997) is widely cited as evidence of earnings management

to avoid reporting losses.1 In a related survey, Graham et al. (2005) conclude that executives

prefer not to report losses by manipulating earnings even when such activities might erode firm

value. But why are Chief Executive Officers (CEOs) so keen to avoid reporting losses?

Some popular explanations for earnings management include bonus compensation and

capital market consequences (e.g., Hayn 1995, Dechow and Sloan 1991). However, changes in

bonus compensation are unlikely to be large because managers report small profits rather than

losses. Similarly, because stock market response to losses is muted (e.g., Joos and Plesko

2005, Hayn 1995), managers are unlikely to be concerned about capital market penalties from

reporting losses. In this study, we investigate an alternative explanation that is more directly

associated with the CEO’s personal exposure to losses, job security. In particular, we examine

whether losses lead to higher CEO turnover.

The decision to replace a CEO is probably one of the most important decisions made by

the board of directors with long-term implications for a firms’ investment, operating and financing

decisions (Huson et al. 2001). CEO turnover was around 10% per year during the 1970s and

1980s and 11% in the 1990s (Murphy and Zabonjik 2004). However, between 1992 and 2005,

annual CEO turnover jumped to 15%. In the more recent years since 1998, CEO turnover is

1The claims of earnings management based on observed discontinuities in firm-year distributions

are controversial. For instance, Durtschi and Easton (2005) attribute the discontinuities in firm-year distributions to deflation and sample selection criteria. Similarly, Dechow et al. (2003) are unable to document evidence consistent with firms using accounting accruals to report small profits.

2

around 16.5% implying that the average CEO tenure is just over six years (Kaplan and Minton

2006). More important, while prior studies find modest relationship between turnover and firm

performance (Murphy 1999, Murphy and Zimmerman 1993), Kaplan and Minton (2006) find that

the CEO turnover-performance relationship is much stronger for the recent years which

suggests that boards have become more sensitive to firm performance and are acting decisively

in response to poor performance. Overall, the results suggest that the CEO’s job is more

precarious than thought previously.

Prior studies examining the relationship between CEO turnover and firm performance

tend to use either accounting measures (e.g., operating income, income from continuing

operations, net income) or/and stock price measures (e.g., stock returns, industry adjusted

stock returns) of performance. Our fundamental hypothesis is that losses capture an

independent assessment of the CEO’s ability that is not fully captured in the traditional

accounting and market-based performance measures. In addition to reflecting poor or declining

performance, losses are one of the ultimate indicators of management failure. Therefore, boards

are more likely to closely scrutinize CEO tenure considerations for loss firms. Boards might also

be concerned that their reputation as the ultimate monitors of management might be tarnished if

they do not hold CEOs accountable for losses, which erodes shareholder equity. Finally,

because annual losses frequently trigger concurrent and future dividend omissions and

reductions (DeAngelo et al. 1992), which are important shareholder considerations, it might be

easier for boards to justify firing a CEO when firms report losses.

Based on a comprehensive sample of CEO turnovers between 1997 and 2005, we find a

statistically and economically significant relationship between CEO turnover and accounting

losses. Controlling for the other determinants of CEO turnover including market and accounting

measures of performance, volatility, industry concentration, firm size, growth, restructuring

activities, financial restatements, and CEO age, we find that CEOs reporting losses are more

likely to lose their jobs within the two-year period following losses, including the year of the loss,

3

compared to profit firms. The economic magnitude of the estimates is also large. Holding the

other variables at the mean values, we find that the probability of a CEO losing a job within two

years of reporting a loss is about 52% higher than firms reporting profits. Additionally, our

results suggest that boards typically tend to focus on the bottom line number; CEOs are held

accountable for losses when a loss includes core, non-core, and discontinued operations and

not just core operations.

Prior studies document that sustained earnings growth is rewarded by debt and equity

markets because of better performance and superior managerial ability (Elliott et al. 2010,

Ghosh et al. 2005, Barth et al. 1999). Similar to the studies examining the rewards from

sustained growth for positive earnings, we analyze whether sustained losses impact CEO

turnover by including five indicator variables measuring consecutive annual losses from years

one to five. We observe that the relationship between CEO turnover and losses is the strongest

when a firm reports a loss for the current year. Controlling for the current period loss, CEOs are

more likely to be dismissed when a firm reports two consecutive annual losses. However, losses

sustained over three or more years do not increase the chances of a CEO turnover. These

results suggest that boards play a proactive role in holding management responsible for poor

performance and that they do not allow matters to worsen before firing the incumbent CEO.

Our analyses assume that accounting loss is a pre-determined variable. However,

because prior research suggests that accounting loss might be endogenously determined (Klein

and Marquardt 2006, Joos and Plesko 2005), the regression estimates from a logistic

regression of CEO turnover on an indicator variable for accounting losses might be biased and

inconsistent. We overcome the endogeneity problem using a two-stage least squares estimation

procedure. Drawing on prior studies, in the first stage we model the likelihood of a firm reporting

an annual loss. In the second stage, we use the estimated value of the likelihood of a loss as an

instrumental variable in the CEO turnover regressions. After controlling for endogeneity of

4

accounting losses, we continue to find unusually high frequency of CEO turnover for firms

reporting losses.

Prior studies find that the stock market views the appointment of an outsider CEO more

favorably than the appointment of an insider CEO, especially when the incumbent CEO is

forced to resign because of performance related reasons (e.g., Borokhovich et al. 1996).

Therefore, we also examine whether losses increase the likelihood that the board hires an

outsider to replace the incumbent CEO to send a credible signal to investors. We find that

losses lead to more frequent appointments of CEOs from outside the firm.

The rest of the paper is organized as follows. Section 2 develops the hypotheses,

Section 3 outlines our research design to test our hypotheses, and Section 4 describes the

sample selection procedure and the data. Section 5 reports the empirical results, Section 6

discusses sensitivity analyses, and finally Section 7 concludes the paper.

2. Hypothesis Development

Annual reports, news releases and press coverages often reference the importance of

consistently making profits which suggests that management has incentives to avoid reporting

losses. In a survey and interview of 400 key executives directly involved in the financial

reporting process, Graham et al. (2005) find that 65% of the executives prefer to report a profit

rather than a loss. Consistent with the loss-avoidance conjecture, Burgstahler and Dichev

(1997) find evidence of earnings management to avoid reporting losses.2 In a subsequent

study, Roychowdhury (2006) provides direct evidence of management using real activities to

avoid reporting losses.

2Earnings management could include a broad range of actions that affect earnings through

operating, investing and financing decisions or through pure accounting choices. Roychowdhury (2006) finds that firms avoid losses by offering price discounts to temporarily increase sales, by increasing production temporarily to decrease the cost of goods sold, and by reducing discretionary expenditures aggressively to improve operating margins.

5

Why are CEOs so concerned about reporting accounting losses and why would they go

to such lengths to manage earnings so as not to report losses? In the subsequent sub-section,

we hypothesize that the primary reason for CEOs avoiding losses is related to career concerns.

Anecdotal evidence supports this conjecture. For example, Jacques Aigrain, the CEO of Swiss

Re, was dismissed following the announcement of an annual loss in 2009.

Losses and Career Concerns

Management in publicly held corporations is entrusted with the task of running a

business to generate profits for shareholders. Graham et al. (2005) find that three-fourths of the

survey respondents believe that their inability to avoid losses is seen as a “managerial failure”

by the executive labor market and by corporate boards. According to one of the surveyed

executives, “if I miss the target, I am out of a job.” One such target includes avoiding losses;

failure to report a profit may be seen as a sign of an incompetent executive. Similarly, Watts

(2003) claims that “managers have incentives to hide losses to avoid being fired before their

tenure is over” because admitting to losses could indicate that they invested in negative net

present value projects.

The board of directors is primarily charged with the responsibility of monitoring,

evaluating, and rewarding management and ultimately firing a CEO for poor performance.

Board members asses the ability of the CEO based on reported numbers and inside

information. When a firm reports a loss rather than a profit, it acts as a heuristic for ultimate

failure (Pinnuck and Lillis 2007). Accounting losses are a signal that the underlying business

model has failed under the present leadership.

When firms report losses, the board is expected to become more proactive in finding out

the reasons for losses and ultimately taking the decision to dismiss the CEO for several

reasons. First, shareholders might expect the board to dismiss the CEO when a firm reports a

loss because of erosion in equity value and the board might be acting to placate shareholders

(Watts 2003). Second, boards have no assurance that CEOs would change their business

6

strategy following losses, which suggests that current losses might persist into the future. For

instance, instead of abandoning loss-making projects, CEOs may continue to operate their pet

projects by subsidizing the losses with the profits from other segments. Similarly, entrenched

and powerful CEOs may be unwilling to discontinue projects with losses either because they are

reluctant to acknowledge their mistakes or because of some personal benefits from managing a

larger firm. Third, a newly appointed CEO is more likely to perform an objective and critical

review of the firm’s business operations, to shut down poorly performing divisions, and to

consider new strategies that allow the firm to become profitable again than an incumbent CEO

who might have strong preferences about his/her prior investments. In summary, a testable

hypothesis is that CEO turnover is higher following accounting losses.

Our hypothesis has broader implications. Several valuation studies find that the relation

between returns and earnings is weaker for loss firms than for profit firms (Collins et al. 1999,

Burgstahler and Dichev 1997, Hayn 1995). The “liquidation/abandonment option” to redeploy

existing assets is often used as an explanation for the differential results between firm values

and earnings for profit and loss firms. Assuming that CEOs are willing to liquidate a firm or to

discontinue a segment, when losses are expected to perpetuate, investors perceive losses as

being temporary. Therefore, the stock market reaction to losses is muted.

However, in the presence of agency problems, it is less clear why CEOs might be willing

to exercise the liquidation/abandonment option when losses are expected to continue. For

example, Ofek (1993) finds that entrenched managers are reluctant to discontinue operations

even when a firm is distressed. In general, prior studies do not directly address or specify what

mechanisms ensure that even entrenched CEOs, or CEOs keen to build empires through value

reducing acquisitions would liquidate or abandon a loss-making operation if losses are expected

to continue.

Our study suggests that personal career concerns and higher frequency of CEO

turnover following reporting of accounting losses ensure that the liquidation or abandonment

7

option is not delayed. If the incumbent CEO is dismissed by the board because the firm reported

a loss, the successor CEO has no reasons to delay liquidating a division or reversing a strategy

implemented by his/her predecessor. When a CEO is retained by the board despite reporting a

loss, the incumbent CEO is as keen as a new CEO to exercise the liquidation/abandonment

option because he/she is conscious that not doing so is likely to result in a dismissal by the

board.

3. Research Design

We test the relationship between CEO turnover and accounting losses using the

following logistic regression.

Turnover = β0+ β1Loss + β2Market-return + β3Asset-return + β4ΔEarnings + β5Stock-volatility + β6Earnings-volatility + β7Concentration + β8Size + β9Growth + β10Restructure + β11Restatement + β12Age + Industry/Year Fixed effects + ε (1)

Where Turnover is an indicator variable that equals 1 when there is a change in the CEO in the

current or subsequent year and 0 otherwise. Our main independent variable is Loss, which is

also an indicator variable with a value of 1 when net income is negative for the current year and

0 otherwise. The predicted sign of the coefficient on Loss is positive; CEO turnover for firms with

losses is expected to be higher than firms with profits.

We include the following control variables which are measured one year prior to the year

of the CEO turnover. Market-return is the difference between the raw returns and the value-

weighted CRSP market returns over a twelve-month fiscal period. Asset-return is industry-

adjusted return on assets measured as the difference between the firm-specific and the

industry-median income before extraordinary items deflated by total assets at the beginning of

the year. ΔEarnings is the difference between current period earnings before extraordinary

items and the corresponding number in the prior year deflated by market value of equity at the

beginning of the year. Stock-volatility is the standard deviation of Market-return based on prior

twenty-four monthly returns. Earnings-volatility is the standard deviation of Asset-return over the

8

previous five years. Concentration is the industry level Herfindahl index. Size is the logarithmic

transformation of the fiscal year-end market value of equity. Growth is the sum of the market

value of equity and the book value of debt scaled by the book value of total assets. Restructure

is an indicator variable that equals 1 if special items as a percentage of total assets is less than

or equal to -5 percent and 0 otherwise. Restatement is an indicator variable equal to 1 when a

firm restates its financial statement in the current or prior year and 0 otherwise. Age is an

indicator variable equal to 1 when the CEO is over the age of 60 years and 0 otherwise.

We include one market and two accounting measures of performance (Market-return,

Asset-return, ΔEarnings) because prior studies find that CEO turnover is related poor

performance (e.g., Farrell and Whidbee 2003, DeFond and Park 1999, Murphy and Zimmerman

1993, Weisbach 1988). We include two measures of volatility, one market (Stock-volatility) and

another accounting (Earnings-volatility) because firms with higher volatility are more prone to

severe shocks that lead to more frequent CEO turnovers (Engel et al. 2003, DeFond and Park

1999). We control for industry concentration because CEO turnover is greater in highly

concentrated industries than in less concentrated industries (DeFond and Park 1999). We

control for firm size (Size) and investment opportunity (Growth) because larger firms and

growing firms have a greater demand for high quality CEOs (Smith and Watts 1992). We

include indicator variables for restructuring activities (Restructure) and financial restatements

(Restatement) because firms with structural or reporting problems are more likely to be

associated with CEO turnovers (Desai et al. 2006, Pourciau 1993). Because not all CEO

turnovers are performance related, as in DeFond and Park (1999), we include an indicator

variable for CEOs who are 60 years or older (Age). Finally, we include fixed effects for years

and industry to control for variations in CEO turnover over time and across industries.

We also estimate an augmented equation that includes several governance variables in

addition to those control variables already included in Equation (1) because prior studies find

9

that CEO turnover is associated with board characteristics (e.g., Weisbach 1988, Goyal and

Park 2002). Specially, we include the number of directors on the board (Board-size), the

percentage of independent directors on the board (Board-independence), indicator variables

when the CEO is also the board chair (CEO-duality) and when a firm has separate audit,

nominating, and compensation committees (Separate-committees), and the percentage of

common stock held by the five top executives (Ownership).

4. Data and Descriptive Statistics

4.1. Data and sample selection

Our sample consists of Standard and Poor’s (S&P) 1500 firms from Compustat’s

ExecuComp files during the period 1997 to 2006. Included in the ExecuComp files are the

names of the top five executives in the firm, a CEOANN variable indicating which of the five

executives has the title of a CEO, and the starting date of the CEO. Our CEO turnover indicator

variable is constructed from the information contained in ExecuComp files. If the name of the

executive listed as a firm’s CEO for the current year is different from the one listed as the CEO

for the prior year, we conclude that there was a change in the CEO, or a new CEO was hired,

for the current year. Because we define Turnover as one when there is a change in a CEO for

the current or subsequent year, and our sample period ends with 2006, we consider accounting

loss from 1997 to 2005. We also obtain the five top executive stock ownership and CEO age

data from the ExecuComp files.

The data on earnings and other firm characteristics are obtained from Compustat annual

files. Stock return data are obtained from CRSP files. We obtain board characteristics (size,

composition, and structure) from the RiskMetrics database (also previously known as IRRC).

We construct one combined sample by merging the CEO, accounting, stock return, and

governance data. To remove the effect of outliers, we winsorize the top or bottom 1 percent of

the observations for Market-return, Asset-return, ΔEarnings, Earnings-volatility, Concentration,

10

and Growth.3 This sample selection procedure results in 11,738 firm-year observations over

fiscal years 1997 through 2005 with information about CEO turnover included up to 2006.

4.2. Descriptive statistics

Panel A of Table 1 reports the descriptive statistics for the variables included in Equation

(1). CEO turnover levels are higher than those typically reported by prior studies; the frequency

of CEO turnover is 23.6% over the entire sample period. The difference in turnover levels

between our study and prior studies is attributable to the measurement of our CEO turnover

variable. CEO turnover is generally measured for any given year while we measure turnover for

the current and subsequent year. Losses are fairly common; of all the firm years, 17.5% report

negative net income. The mean (median) cumulative market-adjusted stock returns (Market-

return) are 0.085 (0.017). The mean (median) industry-adjusted return on assets (Asset-return)

and changes in earnings before extraordinary items deflated by market value of equity

(ΔEarnings) are 0.050 (0.029) and 0.011 (0.006), respectively. The mean (median) return

volatility (Stock-volatility) is 0.116 (0.104), whereas the mean (median) earnings volatility

(Earnings-volatility) is 0.057 (0.030). The Herfindahl index (Concentration) has a median of

0.041. The mean fiscal-year end market value of equity (Market-equity) is $7.2 billion, while the

median number is much smaller ($1.36 billion). The mean (median) market-to-book ratio

(Growth) is 1.70 (1.20). 8.5% of firm years report special items less than or equal to -5 percent

of total assets and 8.9% of firm years are involved with restatements in the current or prior year.

The mean and median values of CEO age are very close; the median CEO age is 56.

Panel B of Table 1 reports the summary statistics for the CEO turnover and non-turnover

samples and the significance of the difference in means between the two samples. We find that

losses are more frequent for CEO turnover firms. 25.5% of the CEO turnover sample has losses,

while the corresponding number for the non-turnover sample is 15.1%. The difference in Loss

3Our results are not sensitive to other outlier identification methods and they remain qualitatively unchanged when we remove the top and/or bottom 0.5 or 1 percent of observations or even retain all the outliers.

11

(10.4%) is statistically significant at the 1 percent level. As in prior studies, we also find that,

compared to non-turnover firms, CEO turnover firms have lower stock market and accounting

performance, are riskier, have lower growth opportunities, restate their financial statements

more frequently, and have older CEOs. The mean difference of two other variables,

Concentration and Market-equity, is not significant.

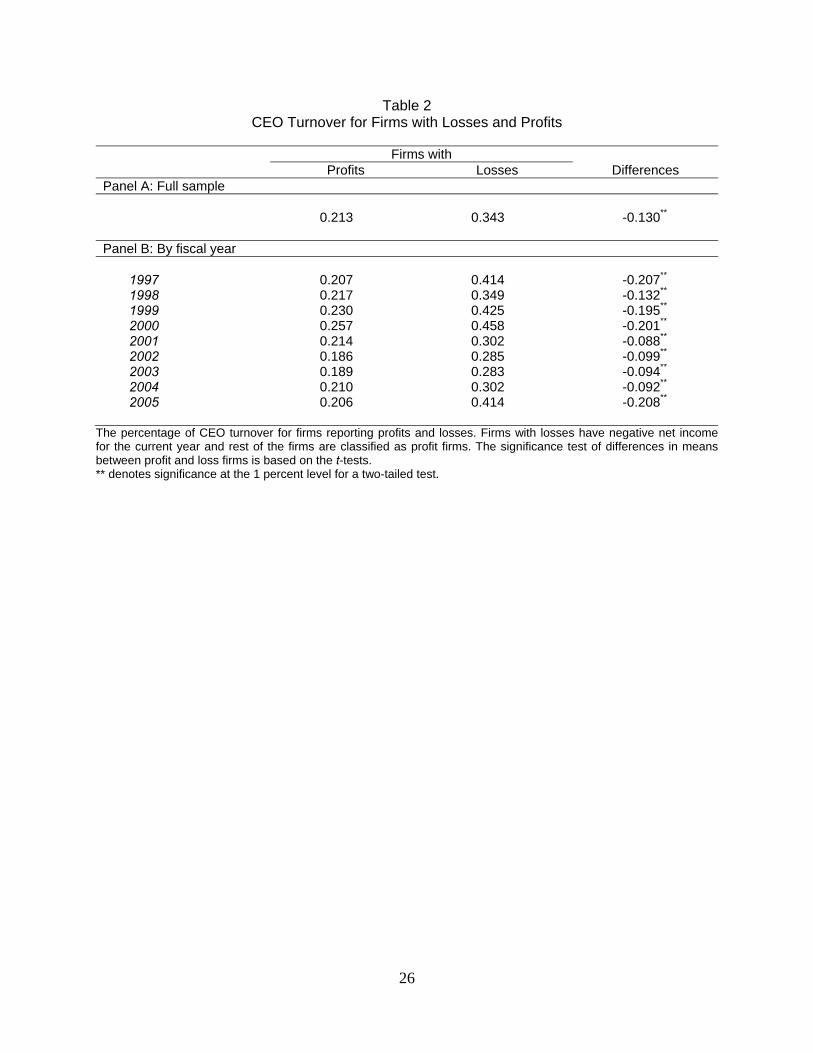

Table 2 presents the relative frequency of CEO turnover for firms reporting losses and

firms reporting profits. Consistent with our expectations that accounting losses are more likely to

lead to a CEO turnover, Turnover in Panel A is higher among loss firms than among profit firms.

More specifically, the frequency of a CEO turnover for the current or subsequent year is 34%

when firms report negative net income while the corresponding number is 21% when firms

report a non-negative number as net income. The difference in frequency in turnover between

the two groups of firms is statistically significant at the 1 percent level. Thus, our preliminary

results indicate that firms with losses have a higher chance of being associated with current or

future CEO turnover than firms with profits.

Panel B of Table 2 reports the frequency of CEO turnover for loss and profit firms from

1997 to 2005. The frequency of CEO turnover for firms reporting profits appears to be constant

around 20% over the sample years. On the other hand, the frequency of CEO turnover for firms

reporting losses fluctuates over time. However, the difference in the frequency of CEO turnover

between loss and profit firms is statistically significant for each of the sample years indicating

that our hypothesis that losses lead to higher CEO turnover is statistically reliable across each

of the years.

5. Empirical Results

5.1. CEO turnover and accounting losses

Table 3 presents the logistic regression results for Equation (1) that predicts the

probability of top executive turnover following losses. The dependent variable Turnover is an

indicator variable that equals 1 when there is a change in the CEO in the current or subsequent

12

year and 0 otherwise. Our interest is in the sign and magnitude of the coefficient on Loss.

Consistent with our expectations and with our univariate results, we find a statistically and

economically significant relationship between CEO turnover and accounting losses. The

coefficient on Loss is 0.655 (χ2=155.48) in the first regression without the control variables. The

coefficient on Loss remains positive and significant (0.586; χ2=86.09) in the second regression

when we include other variables such as the market and accounting measures of firm

performance. The economic magnitude of the coefficient is large. Holding the control variables

at their mean values, the probability of a CEO losing his/her job within two years of reporting a

loss is 32 percent, while the corresponding number for profit firms is 21 percent. Thus, the

likelihood of CEO turnover for loss firms is about 52 percent larger than that for profit firms.

The results of the control variables are generally consistent with our expectations and

similar to those reported in prior studies. The coefficient estimate on Market-return is negative

and significant, which indicates that poor stock performance significantly increases the

likelihood of CEO turnover. In contrast, the coefficient estimates on Stock-volatility, Size,

Restructure, Restatement, and Age are all positive and significant. The results suggest that the

likelihood of CEO turnover is higher for firms with higher volatility, larger firms with restructuring

activities and financial restatements, and firms with older CEOs. The coefficients on Asset-

return, ΔEarnings, Earnings-volatility, Concentration, and Growth are insignificant.

Our analysis in Table 3 relies on net income to partition firms into profit and loss groups

because net income is the bottom-line measure of accounting performance which includes core,

non-core, and discontinued operations, cumulative effect of accounting changes, and losses

attributable to minority interest. We additionally consider two other earnings measures: (1)

income before extraordinary items and (2) operating income. The first measure captures

earnings from core and non-core operations, while the second measure includes only earnings

from core operations.

13

Table 4 reports the regression results, using these alternative measures of reported

earnings to define Loss. Our results suggest that all the measures of reported earnings are

associated with a higher likelihood of a CEO turnover. Controlling for the other determinants of

CEO turnover−such as market and accounting measures of performance, volatility of market

and accounting performance, industry concentration, firm size, growth opportunities,

restructuring activities, financial restatements, and CEO age−the coefficient on Loss in Panel A

is 0.586 (χ2=86.09), 0.562 (χ2=74.16), and 0.305 (χ2=8.11), respectively, when Loss is defined

using net income, income before extraordinary items, and operating income as alternative

measures of reported earnings. As indicated in Panel B, the magnitude of the coefficient on

Loss is the largest when Loss is based on net income, but it is the smallest when Loss is based

on operating income. Our results suggest that boards tend to focus on the bottom line number

for holding CEOs accountable for losses.

One concern with Table 3 is that our regression specification excludes governance

measures for various agency problems which might impact CEO turnover and also be

associated with the likelihood of a firm reporting a loss. For instance, a CEO with a higher equity

ownership in the firm has more power because greater equity ownership might affect CEO

turnover decisions. Similarly, a more independent, effective and diligent board is more likely to

hold a CEO accountable for poor performance than one that is less effective. Accordingly, we

additionally include the size, composition, and structure of the board and managerial ownership

in Equation (1). Specifically, we include the number of members on the board (Board-size), the

percentage of independent directors on the board (Board-independence), the combination of

CEO and board chair positions (CEO-duality), the presence of separate standing sub-

committees (Separate-committees), and the percentage of common stock held by the top five

executives (Ownership). The additional data requirement reduces our sample to 7,516 firm-year

observations.

14

The results in Table 5 show that the inclusion of the additional board and ownership

variables does not alter the relation between CEO turnover and accounting losses. Consistent

with the results in Tables 3 and 4, the positive relation between CEO turnover and losses

continues to hold. The coefficient on Loss is 0.621 (χ2=77.92) and 0.552 (χ2=43.71),

respectively, without and with the control variables in the first and second regressions. The

parameter estimate in the second regression suggests that, based on the mean values of the

control variables, the probability of a CEO losing a job within two years of reporting a loss is 29

percent, while that of a CEO reporting a profit is 19 percent. We also find that, consistent with

the findings in prior studies (e.g., Goyal and Park 2002, Ghosh et al. 2010), the coefficient on

CEO-duality is negative and significant, suggesting that firms with combined CEO-Chair

positions have lower turnover than firms with separate positions. The coefficients on Board-size,

Board-independence, Separate-committees, and Ownership are all insignificant.

Overall, the results from Tables 3 to 5 suggest that CEOs reporting losses are more

likely to lose their jobs within the two-year period following losses including the year of the loss,

compared to CEOs reporting profits, which is consistent with our hypothesis.

5.2. CEO turnover and sustained accounting losses

Prior studies show that debt and equity markets reward firms with sustained earnings

growth because sustained earnings increases are indicative of the firms’ competitive

advantages and a higher probability of future earnings and cash flow growth (Elliott et al. 2010,

Ghosh et al. 2005, Barth et al. 1999). Similar to the studies on the information contents of

sustained earnings growth, we analyze whether sustained accounting losses affect the

likelihood of a CEO turnover. To measure sustained losses, we decompose Loss into 5 indicator

variables depending on the number of years of consecutive annual losses. Loss1 equals 1 for

firms with a loss in the current year but not in the prior year (i.e., NIt<0 and NIt-1≥0). Loss2 equals

1 for firms with two consecutive years of losses (i.e., NIt<0, NIt-1<0, and NIt-2≥0). Similarly, Loss3,

15

Loss4, and Loss5 equal 1 for firms with 3, 4, and 5 or more years of consecutive losses,

respectively.

Table 6 presents the regression results of CEO turnover on sustained losses. We find

evidence on the dampening effect of a sustained loss on the likelihood of CEO turnover. While

the coefficients on Loss1, Loss2, and Loss3 are all positive and significant in the first regression

with the control variables, the magnitude of the coefficients decreases as the length of sustained

loss period increases. The coefficients on Loss4 and Loss5 are insignificant.

In the second regression when we add the governance variables, the coefficients on

Loss1 and Loss2 remain positive and significant; they are 0.600 (χ2=35.33) and 0.565 (χ2=15.25),

respectively. Our results indicate that the effect of losses on CEO turnover is the strongest for

firms with a loss in the current year. Further, controlling for the current period loss, CEOs are

more likely to be dismissed when firms report losses over two consecutive years. However, the

coefficients on Loss3, Loss4, and Loss5 are insignificant, indicating that losses sustained over

three or more years do not increase the chances of a CEO turnover. These results may suggest

that boards of directors play a proactive role in replacing a poorly performing CEO before

matters even get worse which is one explanation why investors treat losses as being temporary.

5.3. Outside replacement and accounting losses

The decision to fire a poorly performing CEO benefits shareholders only when the board

appoints a more capable successor. CEOs who are appointed from outside the firm are more

likely to change pre-existing firm policies that resulted in losses. Borokhovich et al. (1996) find

that the stock market views the appointment of an outsider to the CEO position more favorably

than the appointment of an insider, especially when the incumbent CEO is forced to resign.

Therefore, we also examine whether accounting losses increase the likelihood of an outside

replacement to send a strong signal to investors that the CEO is committed turning around the

firm from a loss making firm to one making profits. We hand collect data to establish whether

16

the successor CEO is from outside the firm by reading press releases, 10-K reports, and

associated proxy statements. The sample to examine the impact of losses on outside

appointments consists of 1,483 CEO turnover observations.

Table 7 presents the regression results on the relationship between accounting losses

and the likelihood of outside succession, conditional on CEO turnover. We estimate Equation

(1) using a dichotomous dependent variable that equals 1 when the incumbent CEO is replaced

with a successor CEO from outside the firm and 0 if the replacement CEO is appointed from

within the firm. We find that the coefficient on Loss is positive and significant; it is 0.450

(χ2=7.96) and 0.488 (χ2=6.38), respectively, when we exclude and include the governance

variables in the first and second regressions. The parameter estimate in the second regression

suggests that, based on the mean values of the governance and control variables, the

probability of an outside appointment for firms reporting a loss is 29 percent, while that for firms

reporting a profit is 20 percent. Our results suggest that accounting losses lead to more frequent

appointments of CEOs from outside the firm.

We also find that the coefficient on Separate-committees is positive and significant,

which indicates that the likelihood of outside succession is higher for firms with specialized

committees on audit, appointment, and remuneration issues. Among the control variables, we

find that the coefficients on Market-return, Size, and Age are negative and significant, implying

that the boards of larger firms with higher stock performance and older CEOs tend to hire an

insider to replace the incumbent CEO.

6. Sensitivity Analysis

6.1. Endogeneity

A potential concern with our prior results is that accounting losses are likely to be

endogenously determined (Klein and Marquardt 2006, Joos and Plesko 2005), which suggests

that the coefficient estimates from the regressions might be biased and inconsistent. We

17

address any endogeneity concerns using a two stage least squares (2SLS) estimation

procedure to obtain consistent and efficient estimates for losses. Specifically, drawing on prior

studies, we model losses in the first stage and then in the second stage we regress CEO

turnover on the probability of a firm reporting a loss obtained from the first stage regression.

The results for the first stage estimation are presented in the first column of Table 8. The

coefficients on Cash-flow, Accrual, Dividend, and Size are all negative and significant, which

suggests that firms with higher cash flow from operations, larger accruals, and larger firms

paying dividend are less likely to report accounting losses. In contrast, the coefficient on

lag(Loss) is positive and significant, indicating that firms with losses in the prior year are more

likely to incur losses in the current year.

In the second stage, we use the estimated values of losses from the first stage as an

instrumental variable and re-estimate Equation (1). After controlling for the endogeneity of

accounting losses, our results confirm the earlier findings on the positive relationship between

CEO turnover and losses. The coefficient on Pred-Loss is 0.648 (χ2=8.81) and 0.501 (χ2=4.15)

when we exclude and include the governance variables in the second and third columns,

respectively. Thus, our results once again confirm that the likelihood of CEO turnover is higher

for firms reporting accounting losses.

6.2. Magnitude of losses

Our analysis adopts the indicator variable Loss to examine the relation between

accounting losses and CEO turnover. Using the indicator variable to represent negative net

income, we presume that the impact of losses on CEO turnover does not depend on the

magnitude of accounting losses. Thus, as part of our sensitivity analyses, we examine whether

the strength of the relation between losses and turnover varies with the size of losses by adding

Magnitude which is the absolute value of net income deflated by book value of equity at the

beginning of the year.

18

Table 9 reports the results after including the interaction term between Magnitude and

Loss to estimate how Magnitude affects the sensitivity of top executive turnover to losses. Our

results on accounting losses continue to hold; the coefficient on Loss remains positive and

significant in the first and second regressions without and with Magnitude. Similarly, the

coefficient on Loss×Magnitude is positive and significant; it is 0.609 (χ2=12.30) and 0.700

(χ2=8.66) in the first and second regressions, indicating that the sensitivity of CEO turnover to

accounting losses becomes larger as the magnitude of accounting losses increases. Our results

suggest that boards take into account both incidence and size of accounting losses in removing

poorly-performing CEOs.

6.3. The effect of governance on the relationship between CEO turnover and losses

Goyal and Park (2002) examine how the leadership structure of the board affects the

sensitivity of CEO turnover to firm performance and find that the sensitivity of CEO turnover to

market-adjusted stock return is less for firms with CEO duality than for firms with separate

positions. Accordingly, we also examine whether governance characteristics affect the

sensitivity of turnover to losses by augmenting the logistic regressions reported in Table 5 after

additionally including interactions between accounting losses and the five governance variables

described earlier.

In unreported results, we find that the inclusion of interactions has no effect on our

results presented in Table 5. The coefficient on CEO-duality remains negative and significant,

while the coefficients on the other four governance variables also continue to remain

insignificant. Further, we find that the coefficients on Loss×CEO-duality and Loss×Separate-

committees are both positive and significant. These results suggest that the sensitivity of top

executive turnover to accounting losses is higher for firms with separate subcommittees and

firms with combined CEO and chairman positions. In the contrast to the results on CEO-duality

whose coefficient is negative, the coefficient on Loss×CEO-duality is positive. Because the

19

interaction term capture the marginal effect of CEO-duality on CEO turnover for loss firms

relative to profit firms, our results suggest that CEO-duality becomes less influential in affecting

CEO turnover for loss firms.

7. Conclusions

Several studies examine the importance of earnings and stock returns as measures of

firm performance on CEO turnover considerations (e.g., Weisbach 1988, Murphy and

Zimmerman 1993, Goyal and Park 2002). We suggest that accounting losses reflect managerial

effort and quality that are not fully captured in the traditional measures of firm performance. In

this paper, we investigate whether accounting losses provide information that can be used to

assess CEO retention/dismissal decision. Specifically, we examine whether accounting losses

lead to subsequent top executive turnover.

Based on a comprehensive sample of CEO turnover between 1997 and 2005, we find

that compared to profit firms, the likelihood of CEO turnover is significantly higher for loss firms.

Controlling for the other determinants of CEO turnover that include traditional market and

accounting measures of firm performance, the relative probability of a CEO losing a job within

two years is about 52 percent higher for firms reporting losses than firms reporting profits. Also,

when we use two other reported earnings measures (income before extraordinary items and

operating income) in addition to the bottom-line number (net income) to define accounting

losses, we find a positive relation between turnover and losses for all the three measures used

to define losses. However, the sensitivity of CEO turnover to losses is the strongest when

losses are defined using the bottom line net income number. Further, when we include the size,

composition, and structure of the board and managerial ownership in our regression

specifications, we find that inclusion of these additional governance variables does not alter the

effect of accounting losses on CEO turnover. Our results on the relation between turnover and

losses are also robust to the endogeneity of accounting losses and inclusion of magnitude of

accounting losses.

20

Moreover, we examine whether sustained accounting losses affect the likelihood of CEO

turnover and find that CEOs are more likely to be dismissed when firms report losses in the

current year or over two consecutive years but not when earnings are sustained over longer

periods which suggests that boards are more proactive in disciplining poorly performing

managers. We also examine whether accounting losses increase the likelihood of outside

replacement. We find that accounting losses lead to more frequent appointments of CEOs from

outside the firm. The probability of an outside appointment is 29 percent and 20 percent,

respectively, for loss firms and profit firms.

Our results suggest that while boards incorporate accounting and market measures of

performance in evaluating management, they view losses as an indicator of management failure

and consequently penalize CEOs for reporting losses. Additionally, prior studies often presume

that managers exercise the liquidation/abandonment option when losses are expected to persist

and, therefore, investors view negative earnings as having low information content relative to

positive earnings. However, the literature is silent why management will not continue to subside

their pet projects or invest in negative net present value projects when such projects benefit

their personal welfare. Our results suggest that CEO turnover or the threat of a higher turnover

following losses ensures that CEOs will exercise the liquidation/abandonment option. Finally,

our results also provide one explanation why firms manage earnings to avoid reporting losses.

21

References

Barth, M. E., J. A. Elliott, and M. A. Finn, 1999, Market rewards associated with patterns of increasing earnings, Journal of Accounting Research 37, 387-413.

Borokhovich, K. A., R. Parrino, and T. Trapani, 1996, Outside directors and CEO selection,

Journal of Financial and Quantitative Analysis 31, 337-355. Burgstahler, D., and I. Dichev, 1997, Earnings management to avoid earnings decreases and

losses, Journal of Accounting and Economics 24, 99-126. Collins, D. W., M. Pincus, and H. Xie, 1999, Equity valuation and negative earnings: The role of

book value of equity, The Accounting Review 74, 29-62. DeAngelo, H., L. DeAngelo, and D. J. Skinner, 1992, Dividends and losses, Journal of Finance

58, 1837-1863. Dechow, P., S. Richardson, and I. Tuna, 2003, Why are earnings kinky? An examination of the

earnings management explanation, Review of Accounting Studies 8, 355-384. Dechow, P., and R. Sloan, 1991, Executive incentives and the horizon problem, Journal of

Accounting and Economics 14, 51-89. DeFond, M. L., and C. W. Park, 1999, The effect of competition on CEO turnover, Journal of

Accounting and Economics 27, 35-56.

Desai, H., C. E. Hogan, and M. S. Wilkins, 2006, The reputational penalty for aggressive

accounting: Earnings restatements and management turnover, The Accounting Review 81, 83-112.

Durtschi, C., and P. Easton, 2005, Earnings management? The shapes of the frequency

distributions of earnings metrics are not evidence ipso facto, Journal of Accounting Research 43, 557-592.

Elliott, J. A., A. Ghosh, and D. Moon, 2010, Asymmetric valuation of sustained growth by bond-

and equity-holders, Review of Accounting Studies, Forthcoming. Engel, E., R. M. Hayes, and X. Wang, 2003, CEO turnover and properties of accounting

information, Journal of Accounting and Economics 36, 197-226. Farrell, K. A., and D. A. Whidbee, 2003, Impact of firm performance expectations on CEO

turnover and replacement decisions, Journal of Accounting and Economics 36, 165-196. Ghosh, A., Z. Gu, and P. Jain, 2005, Sustained earnings and revenue growth, earnings quality,

and earnings response coefficients, Review of Accounting Studies 10, 33-57. Ghosh, A., C. Karuna, and D. Moon, 2010, When the CEO is also the chair of the board,

Working paper, Baruch College, New York, NY.

22

Goyal, V., and C. Park, 2002, Board leadership structure and CEO turnover, Journal of Corporate Finance 8, 49-66.

Graham, J. R., C. R. Harvey, and S. Rajgopal, 2005, The economic implications of corporate

reporting, Journal of Accounting and Economics 40, 3-73. Hayn, C., 1995, The information content of losses, Journal of Accounting and Economics 20,

125-154.

Huson, M. R., R. Parrino, and L. T. Starks, 2001, Internal monitoring mechanisms and CEO

turnover: A long-term perspective, Journal of Finance 55, 2265-2297. Joos, P., and G. Plesko, 2005, Valuing loss firms, The Accounting Review 80, 847-870.

Kaplan, S., and B. A. Minton, 2006, How has CEO turnover changed? Increasingly performance

sensitive boards and increasingly uneasy CEOs, Working paper, University of Chicago, Chicago, IL.

Klein, A., and C. Marquardt, 2006, Fundamentals of accounting losses, The Accounting Review

81, 179-8206.

Murphy, K. J., 1999. Executive compensation, In O. Ashenfelter and D. Card (eds.), Handbook

of Labor Economics. Volume 3, North Holland, 2485-2525. Murphy, K. J., and J. Zabonjik, 2004, Managerial capital and the market for CEOs, Working

paper, University of Southern California, Los Angeles, CA. Murphy, K. J., and J. L. Zimmerman, 1993, Financial performance surrounding CEO turnover,

Journal of Accounting and Economics 16, 273-315. Ofek, E., 1993, Capital structure and firm response to poor performance, Journal of Financial

Economics 34, 3-30. Pinnuck, M., and A. Lillis, 2007, Profits versus losses: Does reporting an accounting loss act as

a heuristic trigger to exercise the abandonment option and divest employees?, The Accounting Review 82, 1031-1053.

Pourciau, S., 1993, Earnings management and nonroutine executive change, Journal of

Accounting and Economics 16, 317-336. Roychowdhury, S., 2006, Earnings management through real activities manipulation, Journal of

Accounting and Economics 42, 335-370. Smith, C. W., and R. L. Watts, 1992, The investment opportunity set and corporate financing,

dividend, and financing policies, Journal of Financial Economics 32, 262-292. Watts, R. L., 2003, Conservatism in accounting, Part I: Explanations and implications,

Accounting Horizons 17, 207-221.

23

Weisbach, M., 1988, Outside directors and CEO turnover, Journal of Financial Economics 20, 431- 460.

24

Table 1 Descriptive Statistics

Mean 1st Quartile Median 3rd Quartile Std. Dev. Panel A: Full Sample

Turnover 0.236 0.000 0.000 0.000 0.424 Loss 0.175 0.000 0.000 0.000 0.380 Market-return 0.085 -0.235 0.017 0.293 0.520 Asset-return 0.050 -0.002 0.029 0.096 0.115 ΔEarnings 0.011 -0.010 0.006 0.029 0.089 Stock-volatility 0.116 0.074 0.104 0.147 0.055 Earnings-volatility 0.057 0.013 0.030 0.065 0.080 Concentration 0.057 0.027 0.041 0.067 0.048 Market-equity 7.159 0.517 1.360 4.537 23.913 Growth 1.697 0.833 1.202 1.966 1.502 Restructure 0.085 0.000 0.000 0.000 0.279 Restatement 0.089 0.000 0.000 0.000 0.286 Age 56.204 51.000 56.000 61.000 7.491

CEO Turnover Yes No Differences Panel B: Firms with and without CEO Turnover

Loss 0.255 0.151 0.104** Market-return 0.006 0.110 -0.104** Asset-return 0.037 0.054 -0.017** ΔEarnings 0.003 0.013 -0.010** Stock-volatility 0.120 0.115 0.005**

Earnings-volatility 0.062 0.056 0.006**

Concentration 0.056 0.057 -0.001

Market-equity 7.870 6.939 0.931

Growth 1.638 1.716 -0.078*

Restructure 0.115 0.076 0.039** Restatement 0.111 0.083 0.028** Age 58.085 55.622 2.463**

Turnover is an indicator variable that equals 1 when there is a change in the CEO in the current or subsequent year and 0 otherwise. Loss is an indicator variable with a value of 1 when net income is negative for the current year and 0 otherwise. Market-return is the difference between the raw returns and the value-weighted CRSP market returns over a twelve-month fiscal period. Asset-return is the industry-adjusted return on assets measured as the difference between the firm-specific and the industry-median income before extraordinary items deflated by total assets at the beginning of the year. ΔEarnings is the difference between current period earnings before extraordinary items and the corresponding number in the prior year deflated by market value of equity at the beginning of the year. Stock-volatility is the standard deviation of Market-return based on prior twenty-four monthly returns. Earnings-volatility is the standard deviation of Asset-return over the previous five years. Concentration is the industry level Herfindahl index. Market-equity is the fiscal year-end market value of equity. Growth is the sum of the market value of equity and the book value of debt scaled by the book value of total assets. Restructure is an indicator variable that equals 1 if special items as a percentage of total assets is less than or equal to -5 percent and 0 otherwise. Restatement is an indicator variable equal to 1 when a firm restates its financial statement in the current or prior year and 0 otherwise. Age is the age of the CEO in years (for the outgoing CEO in turnover firms) as of the fiscal-year end. Panel A is based on the full sample with 11,738 firm-year observations between 1997 and 2005, while Panel B is based on the samples with and without CEO turnover (2,772 and 8,966 observations, respectively). The significance test of differences in means between firms with and without CEO turnover is based on the t-tests. ** and * denote significance at the 1 percent and 5 percent level, respectively, for a two-tailed test.

25

Table 2 CEO Turnover for Firms with Losses and Profits

Firms with Profits Losses Differences Panel A: Full sample

0.213 0.343 -0.130**

Panel B: By fiscal year

1997 0.207 0.414 -0.207**

1998 0.217 0.349 -0.132**

1999 0.230 0.425 -0.195**

2000 0.257 0.458 -0.201** 2001 0.214 0.302 -0.088** 2002 0.186 0.285 -0.099** 2003 0.189 0.283 -0.094** 2004 0.210 0.302 -0.092** 2005 0.206 0.414 -0.208**

The percentage of CEO turnover for firms reporting profits and losses. Firms with losses have negative net income for the current year and rest of the firms are classified as profit firms. The significance test of differences in means between profit and loss firms is based on the t-tests. ** denotes significance at the 1 percent level for a two-tailed test.

26

Table 3 CEO Turnover and Losses

Dependent variable: Turnover

(1) (2)

Intercept -1.304 (2764.95)** -2.286 (172.98)**

Loss 0.655 (155.48)** 0.586 (86.09)**

Control variables

Market-return -0.292 (31.99)**

Asset-return -0.463 (2.95)

ΔEarnings -0.209 (0.52)

Stock-volatility 1.735 (7.34)**

Earnings-volatility 0.020 (0.01)

Concentration -0.284 (0.25)

Size 0.078 (23.25)**

Growth -0.007 (0.13)

Restructure 0.183 (4.49)*

Restatement 0.334 (19.02)**

Age 0.639 (172.05)**

Fixed effects Industry and Year Observations 11,738 11,738 Nagelkerke R2 1.89% 6.11%

The probability estimates of a CEO Turnover when firms report a loss. The dependent variable Turnover is an indicator variable that equals 1 when there is a change in the CEO in the current or subsequent year and 0 otherwise. The independent variables are as follows. Loss is an indicator variable with a value of 1 when net income is negative for the current year and 0 otherwise. Market-return is the difference between the raw returns and the value-weighted CRSP market returns over a twelve-month fiscal period. Asset-return is the industry-adjusted return on assets measured as the difference between the firm-specific and the industry-median income before extraordinary items deflated by total assets at the beginning of the year. ΔEarnings is the difference between current period earnings before extraordinary items and the corresponding number in the prior year deflated by market value of equity at the beginning of the year. Stock-volatility is the standard deviation of Market-return based on prior twenty-four monthly returns. Earnings-volatility is the standard deviation of Asset-return over the previous five years. Concentration is the industry level Herfindahl index. Size is the logarithmic transformation of the fiscal year-end market value of equity. Growth is the sum of the market value of equity and the book value of debt scaled by the book value of total assets. Restructure is an indicator variable that equals 1 if special items as a percentage of total assets is less than or equal to -5 percent and 0 otherwise. Restatement is an indicator variable equal to 1 when a firm restates its financial statement in the current or prior year and 0 otherwise. Age is an indicator variable equal to 1 when the CEO is over the age of 60 years and 0 otherwise. All the variables except Restatement are measured one year prior to the year of the CEO turnover. We report the estimated coefficients from a logistic regression and the corresponding χ2–statistics in parenthesis. ** and * denote significance at the 1 percent and 5 percent level, respectively, for a two-tailed test.

27

Table 4 CEO Turnover and Losses: Alternative Earnings Measures

Dependent Variable: Turnover

Negative: Net Income Income before extraordinary items Operating incomePanel A: Firms with negative earnings

Loss 0.586 (86.09)** 0.562 (74.16)** 0.305 (8.11)**

Control variables Included Included Included Observations 11,738 11,738 11,738 Nagelkerke R2 6.11% 5.96% 5.15% Panel B: Differences in the estimated coefficients

Loss is negative net income 0.586 Loss is negative income before extraordinary items 0.562 Difference in estimated coefficients 0.024

Loss is negative net income 0.586 Loss is negative operating income 0.305 Difference in estimated coefficients 0.281

Loss is negative income before extraordinary items 0.562 Loss is negative operating income 0.305 Difference in estimated coefficients 0.257

The probability estimates of a CEO Turnover when firms report a loss. The dependent variable Turnover is an indicator variable that equals 1 when there is a change in the CEO in the current or subsequent year and 0 otherwise. Loss is an indicator variable with a value of 1 when earnings is negative for the current year and 0 otherwise. Earnings is defined as net income, income before extraordinary items, and operating income. The control variables are the same as those included in Table 3. We report the estimated coefficients from a logistic regression and the corresponding χ2–statistics in parenthesis. ** denotes significance at the 1 percent level for a two-tailed test.

28

Table 5 CEO Turnover and Losses: Including Governance Characteristics

Dependent Variable: Turnover

(1) (2)

Intercept -1.291 (63.52)** -2.261 (71.11)**

Loss 0.621 (77.92)** 0.552 (43.71)**

Governance variables

Board-size 0.040 (15.16)** 0.015 (1.36)

Board-independence -0.001 (1.06) -0.000 (0.02)

CEO-duality -0.456 (60.70)** -0.633 (102.36)**

Separate-committees 0.024 (0.10) 0.121 (2.11)

Ownership -0.003 (0.64) -0.005 (1.41)

Control variables Market-return -0.273 (14.68)**

Asset-return -0.367 (0.91)

ΔEarnings -0.172 (0.16)

Stock-volatility 1.496 (3.07)

Earnings-volatility -0.373 (0.46)

Concentration -0.399 (0.30)

Size 0.079 (10.47)**

Growth 0.012 (0.18)

Restructure 0.258 (4.97)*

Restatement 0.357 (15.89)**

Age 0.874 (194.20)**

Fixed effects Industry and Year Observations 7,516 7,516 Nagelkerke R2 2.98% 8.71%

The probability estimates of a CEO Turnover when firms report a loss. The dependent variable Turnover is an indicator variable that equals 1 when there is a change in the CEO in the current or subsequent year and 0 otherwise. The independent variables are as follows. Loss is an indicator variable with a value of 1 when net income is negative for the current year and 0 otherwise. Board-size is the number of directors on the board. Board-independence is the percentage of independent directors on the board. CEO-duality and Separate-committees are indicator variables set to 1 when the CEO is also the board chair and when a firm has separate audit, nominating, and compensation committees, respectively. Ownership is the percentage of common stock held by the five top executives. Market-return is the difference between the raw returns and the value-weighted CRSP market returns over a twelve-month fiscal period. Asset-return is the industry-adjusted return on assets measured as the difference between the firm-specific and the industry-median income before extraordinary items deflated by total assets at the beginning of the year. ΔEarnings is the difference between current period earnings before extraordinary items and the corresponding number in the prior year deflated by market value of equity at the beginning of the year. Stock-volatility is the standard deviation of Market-return based on prior twenty-four monthly returns. Earnings-volatility is the standard deviation of Asset-return over the previous five years. Concentration is the industry level Herfindahl index. Size is the logarithmic transformation of the fiscal year-end market value of equity. Growth is the sum of the market value of equity and the book value of debt scaled by the book value of total assets. Restructure is an indicator variable that equals 1 if special items as a percentage of total assets is less than or equal to -5 percent and 0 otherwise. Restatement is an indicator variable equal to 1 when a firm restates its financial statement in the current or prior year and 0 otherwise. Age is an indicator variable equal to 1 when the CEO is over the age of 60 years and 0 otherwise. All the variables except Restatement are measured one year prior to the year of the CEO turnover. We report the estimated coefficients from a logistic regression and the corresponding χ2–statistics in parenthesis. ** and * denote significance at the 1 percent and 5 percent level, respectively, for a two-tailed test.

29

Table 6 CEO Turnover and Sustained Losses

Dependent Variable: Turnover

(1) (2)

Intercept -2.189 (180.12)** -2.239 (69.64)**

Loss1 0.614 (64.78)** 0.600 (35.33)**

Loss2 0.608 (28.75)** 0.565 (15.25)**

Loss3 0.437 (8.56)** 0.382 (3.71)

Loss4 0.118 (0.32) 0.030 (0.01)

Loss5 0.281 (1.39) 0.367 (2.12)

Governance variables Not Included Included Control variables Included Included Observations 11,738 7,516 Nagelkerke R2 6.09% 8.77%

The probability estimates of a CEO Turnover when firms report a loss. The dependent variable Turnover is an indicator variable that equals 1 when there is a change in the CEO in the current or subsequent year and 0 otherwise. Loss is decomposed into 5 indicator variables depending on the number of years of consecutive annual losses. Loss1 equals 1 for firms with a loss in the current year but not in the prior year. Similarly, Loss2, Loss3, Loss4, and Loss5 equal 1 for firms with 2, 3, 4, and 5 or more years of consecutive losses, respectively. The governance and control variables are the same as those included in Table 5. We report the estimated coefficients from a logistic regression and the corresponding χ2–statistics in parenthesis. ** denotes significance at the 1 percent level for a two-tailed test.

30

Table 7 Probability of an Outside CEO Appointment Conditional on CEO Turnover

Dependent Variable: Outsider Replacement (1) (2)

Intercept -0.006 (0.01) 0.248 (0.11)

Loss 0.450 (7.96)** 0.488 (6.38)*

Governance variables

Board-size -0.032 (0.69)

Board-independence 0.000 (0.01)

CEO-duality 0.262 (2.74)

Separate-committees 0.587 (5.71)*

Ownership -0.023 (3.02)

Control variables

Market-return -0.254 (3.11) -0.489 (5.55)*

Asset-return -0.008 (0.01) -0.123 (0.02)

ΔEarnings -0.441 (0.42) 0.395 (0.15)

Stock-volatility -0.261 (0.02) 1.282 (0.33)

Earnings-volatility 1.124 (1.34) -0.240 (0.02)

Concentration -1.296 (0.57) 0.048 (0.01)

Size -0.123 (7.31)** -0.153 (5.34)*

Growth 0.039 (0.47) 0.012 (0.02)

Restructure 0.180 (0.76) 0.246 (0.89)

Restatement -0.046 (0.07) -0.161 (0.60)

Age -0.537 (14.25)** -0.625 (13.60)**

Fixed effects Industry and Year Industry and Year

Observations 1,483 1,128 Nagelkerke R2 10.34% 14.01%

The dichotomous dependent variable Outsider Replacement equals 1 when the incumbent CEO is replaced with a successor CEO from outside the firm and 0 if the replacement CEO is appointed from within the firm. The independent variables are as follows. Loss is an indicator variable with a value of 1 when net income is negative for the current year and 0 otherwise. Board-size is the number of directors on the board. Board-independence is the percentage of independent directors on the board. CEO-duality and Separate-committees are indicator variables set to 1 when the CEO is also the board chair and when a firm has separate audit, nominating, and compensation committees, respectively. Ownership is the percentage of common stock held by the five top executives. Market-return is the difference between the raw returns and the value-weighted CRSP market returns over a twelve-month fiscal period. Asset-return is the industry-adjusted return on assets measured as the difference between the firm-specific and the industry-median income before extraordinary items deflated by total assets at the beginning of the year. ΔEarnings is the difference between current period earnings before extraordinary items and the corresponding number in the prior year deflated by market value of equity at the beginning of the year. Stock-volatility is the standard deviation of Market-return based on prior twenty-four monthly returns. Earnings-volatility is the standard deviation of Asset-return over the previous five years. Concentration is the industry level Herfindahl index. Size is the logarithmic transformation of the fiscal year-end market value of equity. Growth is the sum of the market value of equity and the book value of debt scaled by the book value of total assets. Restructure is an indicator variable that equals 1 if special items as a percentage of total assets is less than or equal to -5 percent and 0 otherwise. Restatement is an indicator variable equal to 1 when a firm restates its financial statement in the current or prior year and 0 otherwise. Age is an indicator variable equal to 1 when the CEO is over the age of 60 years and 0 otherwise. All the variables except Restatement are measured one year prior to the year of the CEO turnover. We report the estimated coefficients from a logistic regression and the corresponding χ2–statistics in parenthesis. ** and * denote significance at the 1 percent and 5 percent level, respectively, for a two-tailed test.

31

Table 8 CEO Turnover and Losses: Two Stage Least Squares

First-Stage Regression Second-Stage Regression

Dependent Variables = Loss Turnover Intercept -0.830 (38.42)** -2.343 (157.68)** -2.337 (68.81)**

Pred-Loss 0.648 (8.81)** 0.501 (4.15)*

Instruments Cash-flow -5.317 (354.37)** Accrual -2.726 (87.66)** Sales-growth -0.000 (0.05) lag(Loss) 1.330 (400.62)** Dividend -0.678 (180.26)** Dividend-stop 0.099 (0.52)

Governance variables Board-size 0.024 (2.70)Board-independence 0.000 (0.10)CEO-Duality -0.611 (92.21)**

Separate-committees 0.109 (1.64)Ownership -0.005 (1.66)

Control variables

Market-return -0.346 (43.92)** -0.340 (22.39)**

Asset-return -0.368 (1.22) -0.422 (0.89)ΔEarnings -0.113 (0.15) -0.094 (0.04)Stock-volatility 2.160 (10.76)** 1.836 (4.41)*

Earnings-volatility -0.027 (0.01) -0.310 (0.30)Concentration -0.572 (0.99) -0.694 (0.86)Size -0.104 (49.08)** 0.089 (26.78)** 0.074 (8.26)**

Growth -0.023 (1.30) 0.006 (0.04)Restructure 0.141 (2.59) 0.222 (3.58)Restatement 0.360 (21.88)** 0.398 (19.42)**

Age 0.629 (160.80)** 0.858 (180.25)**

Fixed effects Industry and Year Industry and Year Industry and Year

Observations 18,190 11,228 7,184 Nagelkerke R2 32.71% 5.19% 7.87%

In the first stage regression, the dichotomous dependent variable Loss equals 1 when reported net income is negative in the current year and 0 otherwise. The instruments which are measured in the prior year are: Cash-flow is cash flows from operations divided by beginning period total assets, Accrual is total accruals (net income – cash flows from operations) divided by beginning period total assets, Sales-growth is the percentage growth in sales, lag(Loss) is the one-year lagged value of Loss, Dividend equals 1 when the firm pays dividends and 0 otherwise, and Dividend-stop is an indicator variable equal to 1 if the firm stopped paying dividends and 0 otherwise. In the second stage, we regress the dichotomous dependent variable Turnover which equals 1 for firms with CEO turnover on the estimated value of loss from the first stage regression (Pred-Loss). The governance and control variables are as follows. Board-size is the number of directors on the board. Board-independence is the percentage of independent directors on the board. CEO-duality and Separate-committees are indicator variables set to 1 when the CEO is also the board chair and when a firm has separate audit, nominating, and compensation committees, respectively. Ownership is the percentage of common stock held by the five top executives. Market-return is the difference between the raw returns and the value-weighted CRSP market returns over a twelve-month fiscal period. Asset-return is the industry-adjusted return on assets measured as the difference between the firm-specific and the industry-median income before extraordinary items deflated by total assets at the beginning of the year. ΔEarnings is the difference between current period earnings before extraordinary items and the corresponding number in the prior year deflated by market value of equity at the beginning of the year. Stock-volatility is the standard deviation of Market-return based on prior twenty-four monthly returns. Earnings-volatility is the standard deviation of Asset-return over the previous five years. Concentration is the industry level Herfindahl index. Size is the logarithmic

32

transformation of the fiscal year-end market value of equity. Growth is the sum of the market value of equity and the book value of debt scaled by the book value of total assets. Restructure is an indicator variable that equals 1 if special items as a percentage of total assets is less than or equal to -5 percent and 0 otherwise. Restatement is an indicator variable equal to 1 when a firm restates its financial statement in the current or prior year and 0 otherwise. Age is an indicator variable equal to 1 when the CEO is over the age of 60 years and 0 otherwise. All the control variables except Restatement in the second stage regression are measured one year prior to the year of the CEO turnover. We report the estimated coefficients from a logistic regression and the corresponding χ2–statistics in parenthesis. ** and * denote significance at the 1 percent and 5 percent level, respectively, for a two-tailed test.

33

34

Table 9 CEO Turnover and Magnitude of Losses

Dependent variable: Turnover

(1) (2)

Intercept -2.281 (171.92)** -2.270 (168.25)**

Loss 0.459 (38.99)** 0.444 (32.30)**

Loss×Magnitude 0.609 (12.30)** 0.700 (8.66)**

Magnitude -0.091 (0.31)

Control variables Included Included Observations 11,738 11,738 Nagelkerke R2 6.26% 6.26%

The probability estimates of a CEO Turnover when firms report a loss. The dependent variable Turnover is an indicator variable that equals 1 when there is a change in the CEO in the current or subsequent year and 0 otherwise. Loss is an indicator variable with a value of 1 when net income is negative for the current year and 0 otherwise. Magnitude is the absolute value of net income deflated by book value of equity at the beginning of the year. The control variables are the same as those included in Table 3. We report the estimated coefficients from a logistic regression and the corresponding χ2–statistics in parenthesis. ** and * denote significance at the 1 percent and 5 percent level, respectively, for a two-tailed test.

Top Related