Languages

Pages

Legal

1

Presentation for investors and shareholders

for Q2 2016

August, 10 2016 Belgrade

Anton Fyodorov

2

NIS in Q2 2016

Exploration and Production

• Testing ended with a positive outcome at two exploratory wells, one is in the testing phase.

• Estimated reserves increment in 2016 – 3.7%.

• Kumane – Investment Project upheld by NIS IB (drilling in August 2016)

• RAG Kiha-004 – drilled, oil recovery during testing

• Blocks Ex-7 and Ex-8 - Phase 3 of seismic operations ended, data processing is in progress

• Testing of Jimbolia-6 well is finished – resulted in gas flow.

• Turija II – 3D seismic data processing completed. The acquisition is in progress on the Južni Banat I polygon

• Drilling Plan for the entire year was fulfilled (19 wells)

3

NIS in Q2 2016

Refining

• Deconservation and start-up of the «Small» Atmospheric Distillation Unit and the Kerosene Merox Unit for the purpose of increasing the scope of refining and production efficiency.

• The Gasoline In-Line Blending project has been completed.

• The final version has been obtained for the extended Basic Design (FEED) of the Delayed Coking Unit.

• The tender procedure is on-going for the selection of the EPCm contractors, and also the tender activities have started for the selection of the suppliers for long lead items (LLI).

• The Certificate of Conformity of the quality management system to the requirements of ISO 9001:2008 standard has been awarded

• The procedure of legalization of the facilities in the Pančevo Refinery has been successfully completed.

4

NIS in Q2 2016

Sales and Distribution

• Beginning of sale of branded fuel G-Drive diesel in the Serbian market

• Beginning of sale of branded fuel G-Drive 100 in the Romanian market

• The supply of fuel for intercontinental flights has started

• The beginning of the implementation of the program of PS operational activities optimization

• 2 new tank trucks for transportation of jet fuel

5

NIS in Q2 2016

Energy

• Small power plant Majdan (2.4 MW)

- Works in final stage • Small power plant Miloševo (9.8 MW)

- Agreement reached with the Exploration and Production Block that the complete design activities will be carried out by the NTC

• CNG station at PS Čačak 1 - construction activities finished - obtaining the approval for the type of measuring device

from the Directorate of Measures and Precious Metals - exploitation by the end of July.

• CNG Station “Ostrovo” - Gas exploitation approved - The main mining project completed - Access road from the village of Ostrovo built - Ground-leveling works in progress

• CPP Pančevo - Tender closed; evaluation of bids underway

• Windpark Plandište - obtained PPA (feed in).

6

Dividend payment for 2015

16,1

Total dividens, bn RSD Dividend yield, %*

16.1

4.0

Net profit Dividends

25%

24.69 RSD gross

per share

0.00%

4.93%

4.02%

3.83%

4.12%

*Shares’ prices on December 31st, 2015

7

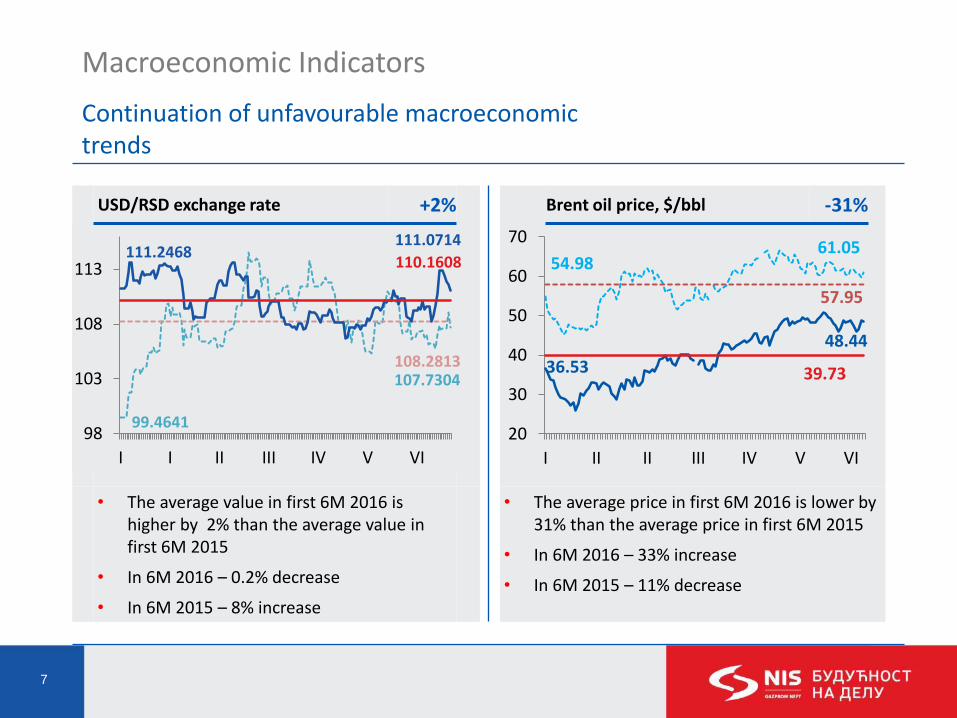

Macroeconomic Indicators

Continuation of unfavourable macroeconomic trends

USD/RSD exchange rate +2% Brent oil price, $/bbl -31%

• The average value in first 6M 2016 is higher by 2% than the average value in first 6M 2015

• In 6М 2016 – 0.2% decrease

• In 6М 2015 – 8% increase

• The average price in first 6M 2016 is lower by 31% than the average price in first 6M 2015

• In 6М 2016 – 33% increase

• In 6М 2015 – 11% decrease

99.4641

107.7304 108.2813

111.2468 111.0714

110.1608

98

103

108

113

I I II III IV V VI

36.53

48.44

39.73

54.98 61.05

57.95

20

30

40

50

60

70

I II II III IV V VI

8

HSE Indicators

Positive trend

Increase in transparency LTIF RAR

LTIF – Rate of Injuries (fatalities with injuries that caused lost work days , multiplied by 1 million and divided by the number of working hours. RAR - the number of road accidents per kilometers travelled , multiplied by 1 million

2.2

1.67

3.41

Plan2016

6М 2016

6М 2015

0.32

0.21

0.43

Plan2016

6М 2016

6М 2015

Major events

Medium events

Minor events

Pot.

events

51%

24%

51%

6М 2015. 6М 2016.

8,233 26,043

572 452

67 44

7 4

34%

9

Q2 2016 Key Indicators

NIS Group

Q2

2016. Q2

2015. ∆

𝐐𝟐 𝟐𝟎𝟏𝟔.

𝐐𝟐 𝟐𝟎𝟏𝟓.

(%) Key Indicators

Јединица мере

6M 2016.

6M 2015.

∆𝟔𝐌 𝟐𝟎𝟏𝟔.

𝟔𝑴 𝟐𝟎𝟏𝟓.

(%)

43.88 61.46 -29% Urals $/bbl 38.1 57.2 -33%

2.9 9.6 -70% Net income bn RSD 3.1 5.0 -36%

9.4 13.8 -32% EBITDA bn RSD 13.2 21.0 -37%

46.0 57.0 -19% Sales revenues bn RSD 81.4 103.4 -21%

5.0 19.9 -75% OCF bn RSD 8.6 24.3 -65%

43.5 37.7 +15% Calculated liabilities from taxes and other public revenues

bn RSD 76.3 67.2 +13%

366.4 398.1 -8% Crude oil and gas production thou. t.o.e. 743 795 -7%

243 267 -9% Domestic crude oil production thou. tons 493 536 -8%

974 828 +18% Oil and semi-finished products refining volumes thou. tons 1,750 1,512 +16%

850 782 +9% Total sales of petroleum products thou. tons 1,553 1,463 +6%

67 48 +40% Sales – foreign assets thou. tons 123 89 +38

655 611 +7% Sales of petroleum products in the domestic market thou. tons 1,217 1,160 +5%

506 481 +5% Motor fuels thou. tons 919 870 +6%

180 172 +5% Retail thou. tons 331 313 +6%

4.5 5.5 -18% CAPEX bn RSD 9.1 12.5 -27%

680 571 +19% Total indebtedness to banks mn USD 680 571 +19%

10

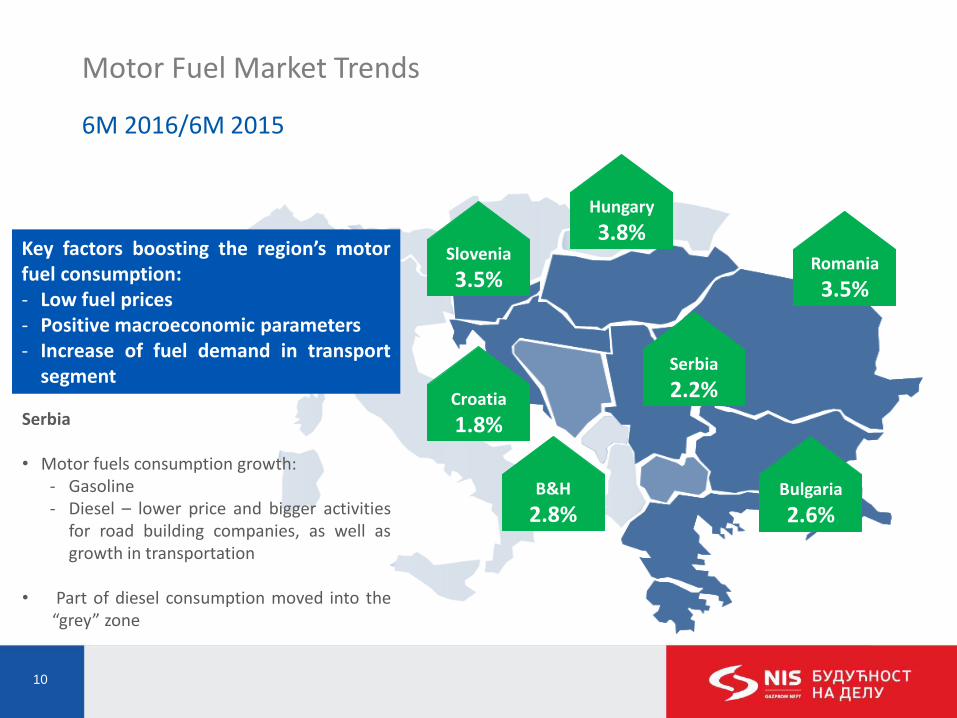

Motor Fuel Market Trends

6М 2016/6M 2015

Key factors boosting the region’s motor fuel consumption: - Low fuel prices - Positive macroeconomic parameters - Increase of fuel demand in transport

segment

Slovenia

3.5%

Croatia

1.8%

B&H

2.8%

Hungary

3.8% Romania

3.5%

Bulgaria

2.6%

Serbia

2.2% Serbia • Motor fuels consumption growth:

- Gasoline - Diesel – lower price and bigger activities

for road building companies, as well as growth in transportation

• Part of diesel consumption moved into the

“grey” zone

11

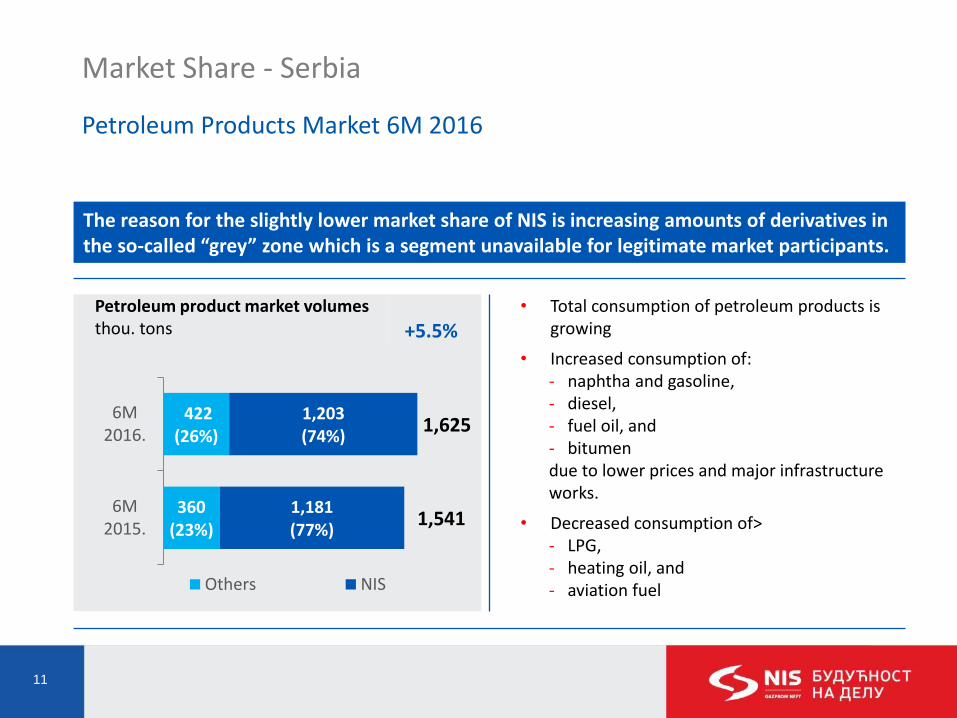

Market Share - Serbia

Petroleum Products Market 6М 2016

Petroleum product market volumes thou. tons +5.5%

• Total consumption of petroleum products is growing

• Increased consumption of: - naphtha and gasoline, - diesel, - fuel oil, and - bitumen due to lower prices and major infrastructure works.

• Decreased consumption of> - LPG, - heating oil, and - aviation fuel

The reason for the slightly lower market share of NIS is increasing amounts of derivatives in the so-called “grey” zone which is a segment unavailable for legitimate market participants.

360 (23%)

422 (26%)

1,181 (77%)

1,203 (74%)

1,541

1,625

6M2015.

6M2016.

Others NIS

12

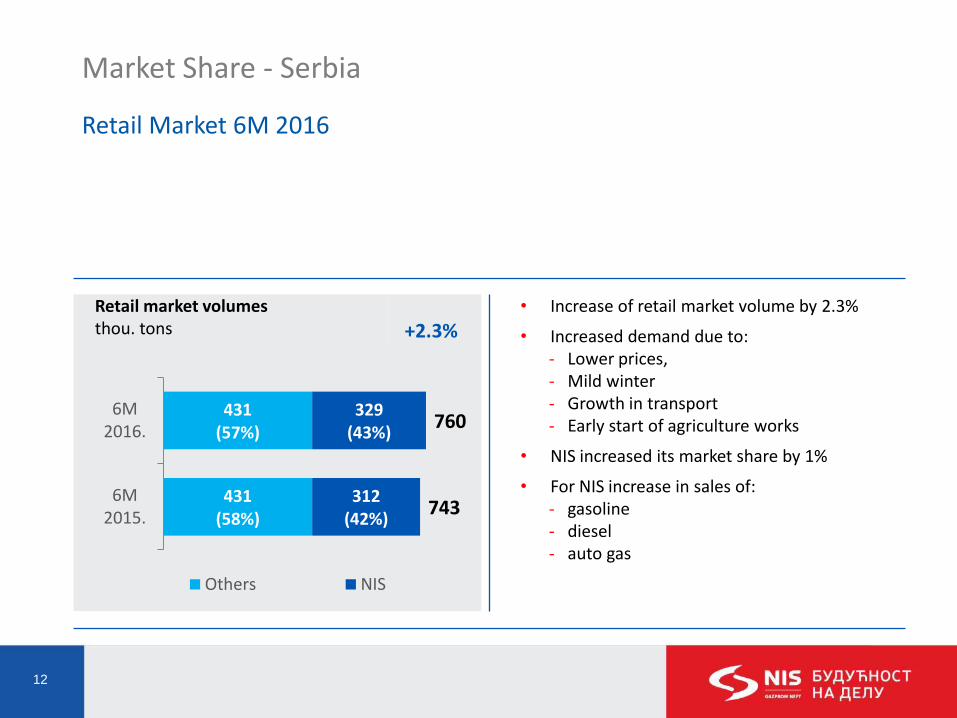

Market Share - Serbia

Retail Market 6М 2016

Retail market volumes thou. tons +2.3%

• Increase of retail market volume by 2.3%

• Increased demand due to: - Lower prices, - Mild winter - Growth in transport - Early start of agriculture works

• NIS increased its market share by 1%

• For NIS increase in sales of: - gasoline - diesel - auto gas

431 (58%)

431 (57%)

312 (42%)

329 (43%)

743

760

6M2015.

6M2016.

Others NIS

13

Market Share - Region

6М 2016*

Bosnia and Herzegovina

No. Of PSs: 35 % entire mark.: 11.7% % retail mark.: 10.7%

Romania

No. Of PSs: 18 % entire mark.: 0.6% % retail mark.: 0.9%

Bulgaria

No. Of PSs: 35 % entire mark.: 4.5% % retail mark.: 4.3%

*Compared with market share for 6М 2015

14

Operating Indicators

Exploration and Production

Oil and gas output thou. of oil equivalent

-7% -8%

• Above the plan: - Production of domestic oil - + 7.8 thousand tons - Production of domestic gas - +2% - Implementation of GTA - Production resulting from new drilling activities

267

265

257

251

243

116

115

116

112

111

15

15

14

14

13

398

395

387

377

366

Q2 2015.

Q3 2015.

Q4 2015.

Q1 2016.

Q2 2016.

Domestic oil Domestic gas Angola

Estimated increase of hydrocarbon reserves for 2016 is

3.7%

536

493

229

223

30

27

795

743

6M2015

6M2016

Domestic oil Domestic gas Angola

15

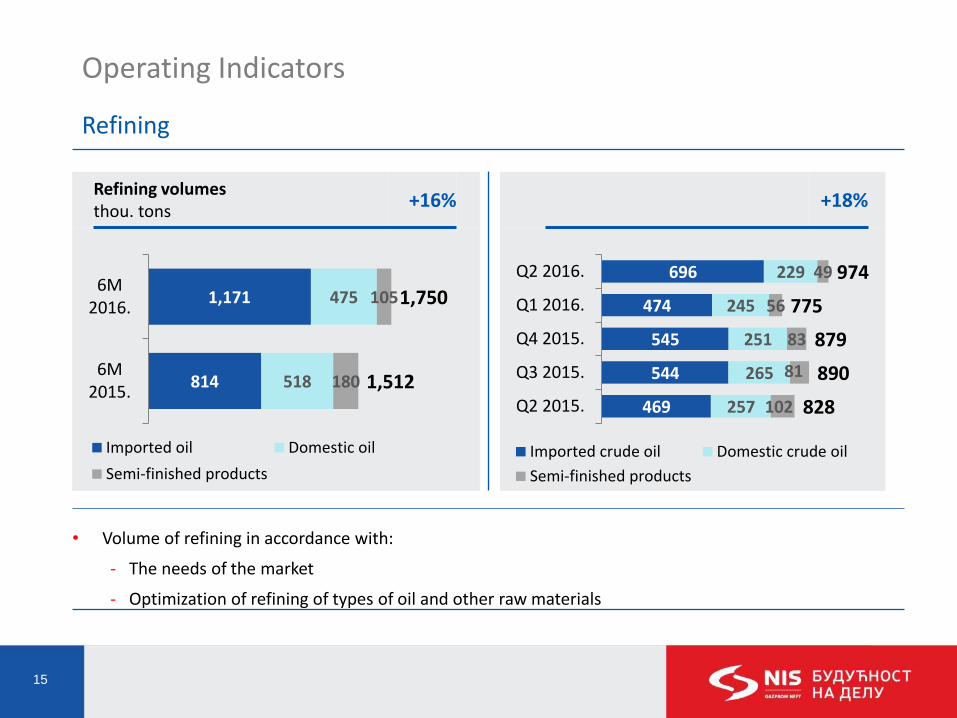

Operating Indicators

Refining

Refining volumes thou. tons

+16% +18%

• Volume of refining in accordance with:

- The needs of the market

- Optimization of refining of types of oil and other raw materials

814

1,171

518

475

180

105

1,512

1,750

6M2015.

6M2016.

Imported oil Domestic oil

Semi-finished products

469

544

545

474

696

257

265

251

245

229

102

81

83

56

49

828

890

879

775

974

Q2 2015.

Q3 2015.

Q4 2015.

Q1 2016.

Q2 2016.

Imported crude oil Domestic crude oil

Semi-finished products

16

Operating Indicators

Sales and Distribution

Sales volumes* thou. tons

+6% +9%

• Retail - Serbia - volume growth by 6%

• Wholesale - Serbia - volume growth by 5%

• Export - at the same level • Foreign assets - volume growth by 38%

313

331

89

123

847

886

214

214

1,463

1,553

6M2015.

6M2016.

Retail - Serbia Foreign assetsWholesale - Serbia Export

172

183

185

151

180

48

54

52

56

67

439

501

555

411

476

123

134

127

86

128

782

872

920

703

850

Q2 2015.

Q3 2015.

Q4 2015.

Q1 2016.

Q2 2016.

Retail - Serbia Foreign assetsWholesale - Serbia Export

*internal sale included (6M 2016: app. 6 thousand tons; 6M 2015: app. 7 thousand tons)

17

Financial Indicators

Net income bn RSD

-36% -70%

• Prices of oil and oil products

9.6

6.0

3.7

0.3

2.9

Q2 2015.

Q3 2015.

Q4 2015.

Q1 2016.

Q2 2016.

5.0

3.1

6M2015.

6M2016.

18

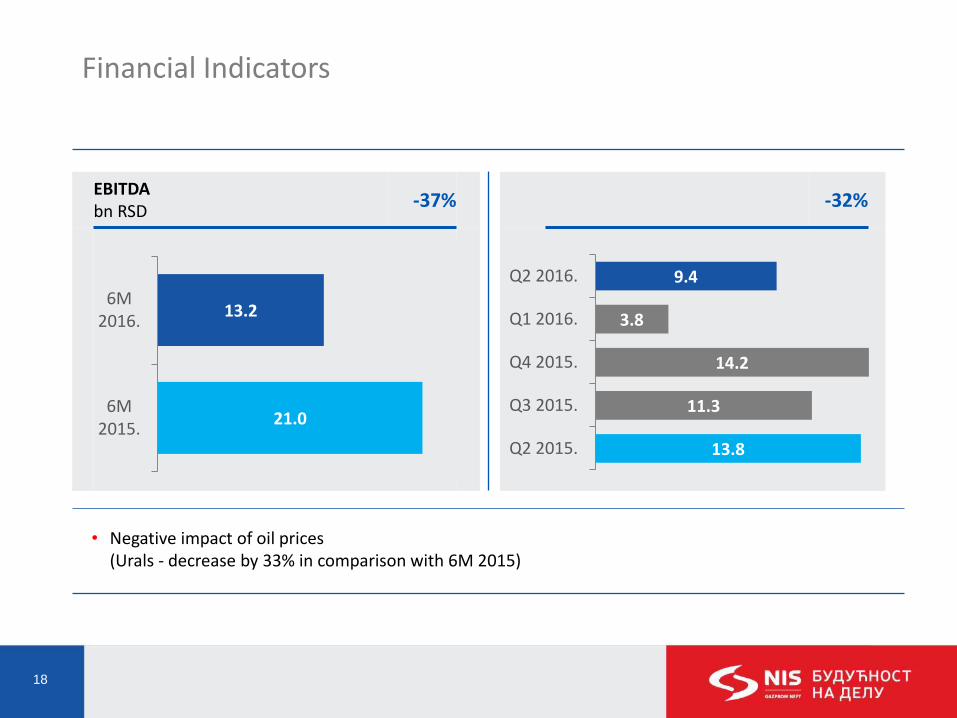

Financial Indicators

EBITDA bn RSD

-37% -32%

• Negative impact of oil prices (Urals - decrease by 33% in comparison with 6M 2015)

13.8

11.3

14.2

3.8

9.4

Q2 2015.

Q3 2015.

Q4 2015.

Q1 2016.

Q2 2016.

21.0

13.2

6M2015.

6M2016.

19

Financial Indicators

OCF bn RSD

-65% -75%

• Inflow lower by RSD 14.4 billion - Low prices of oil products

• Outflow higher by RSD 1.4 billion - Higher commitments to the state and higher commitments to suppliers

19.9

11.7

15.0

3.6

5.0

Q2 2015.

Q3 2015.

Q4 2015.

Q1 2016.

Q2 2016.

24.3

8.6

6M2015.

6M2016.

20

Financial Indicators

CAPEX bn RSD

-27% Investments by segments bn RSD

• The biggest investments in the Exploration and Production • Prioritization of investment portfolio

82%

2% 8%

2%

4%

2% Exploration andproduction

Services

Refining

Sales anddistribution

Energy

Corporate centre30.3

28.0

12.5

9.1

2015.actual

2016.forecast

6M 2015.

6M 2016.

21

Improvement of Operational Efficiency

Effect of operational efficiency improvement measures on EBITDA indicator bn RSD

1.3

0.4

2.8

0.4 0.5

0.4

5.9 5.9

3.2 0.3

0.1

0.0 0.1

0.2

0.4

1.0

0.0

1.0

0.5

1.1

1.1

0.7

0.3

0.2

0.0 0.2

0.0

0.5 1.2

0.0

1.2

1.9

0.7

2.8 0.7

0.7

1.3 8.1

1.2 9.3

4.4

Explorationand

production

Services Refining Sales anddistribution

Energy Corp. centre(Functions)

NISestimate

2016

Preventeddamage

Total NISestimate

2016

6M 2016

Measures (BP, QPR1, QPR2) Additional measures (QPR2) Prevented damage Potential

59%

55%

3.7 bn RSD

22

Indebtedness to Banks The withdrawal of favuorable loans based on import from EU

Total debt to banks mn USD

+2% Total indebtedness to banks mn USD

+1%

201

25

41

4

86

32

52

86

392

430

330

264

358

430

560

499

518

200

155

116

99

94

82

72

73

71

793 611

446 403

455 598

664 623

676

31.12.'09.

31.12.'10.

31.12.'11.

31.12.'12.

31.12.'13.

31.12.'14.

31.12.'15.

31.03.'16.

30.06.'16.

Short-term Medium-term Long-term

233

33

13

14

34

28

12

10

4

793

611

446

403

455

598

664

623

676

1.026 644

458 418

489 626

675 633 680

31.12.'09.

31.12.'10.

31.12.'11.

31.12.'12.

31.12.'13.

31.12.'14.

31.12.'15.

31.03.'16.

30.06.'16.

L/C Debt to banks

Debt structure : USD 61% EUR 38% Other 1%

GPN loan as of 30.06.2016. – 326 mn EUR (-7%)

23

Comparative Analysis

EBITDA margin (%) EBITDA/FTE (thou. USD) Daily sales(t/day)

Share of light products (%) OPEX ($/boe)

33

18.2

16.3

14.6

3.7

17.2

27.0

18.4

17.9

6.2

1.3

14.2

7.8 6.6 6.6

5.5 5.3

4.9

6.1

4.9 1.5

12.3

12.2

6.3

6.4

Н/Д

9.3 87.4

75.4

75.0

73.1

71.0

76.2

3. 4.

4.

2.

2. 1.

24

∆ The average price of Urals oil is lower than the macro assumptions in the Business plan

∆ Limited opportunities for long term loans

∆ Positive net result

∆ Oil and gas production is above the plan even with the lower volume of investments

∆ Growth of sales

∆ Progress of Energy projects

25

Disclaimer

This presentation has been prepared by NIS a.d. Novi Sad (the “Company”), and comprises the slides for a presentation to investors concerning NIS

Group. Presentation does not constitute or form part of any offer or invitation, or any solicitation of any offer to sell or purchase or subscribe for, any

shares or other securities representing shares in the Company, nor shall it or any part of it nor the fact of its presentation or distribution form the basis

of, or be relied on in connection with, any contract or investment decision.

Any viewer of this presentation considering a purchase of such securities is hereby reminded that any such sale or purchase should be made solely on

the basis of the information contained in other publicly available documents and will be subject to the restrictions set out therein. No reliance may be

placed for any purposes whatsoever on the information contained in this presentation, or any other material discussed at any presentation or on its

completeness, accuracy or fairness. The information in this presentation should not be treated as giving investment advice or recommendation. All

reasonable measures are taken to ensure that the facts stated in this presentation are accurate, and that the opinions expressed are fair and

reasonable. However, the contents of this presentation have not been adopted by the corporate body’s of Company. Accordingly, no representation or

warranty, express or implied, is made or given by or on behalf of the Company or any of its members, directors, officers or employees or any other

person as to the accuracy, completeness or fairness of the information or opinions contained in or discussed at this presentation. None of the Company

or any of their respective members, directors, officers or employees nor any other person accepts any liability whatsoever for any loss howsoever

arising from any use of this presentation or its contents or otherwise arising in connection therewith.

The information in this presentation includes forward-looking statements. These forward-looking statements include all matters that are not historical

facts, statements regarding the Company’s and NIS Group’s intentions, beliefs or current expectations concerning, among other things, the NIS Group’s

results of operations, financial condition, liquidity, prospects, growth, strategies, and the industry in which the Company and NIS Group operate. By their

nature, forward-looking statements involve risks and uncertainties, including, without limitation, the risks and uncertainties to be set in other publicly

available documents, because they relate to events and depend on circumstances that may or may not occur in the future. The Company cautions you

that forward looking statements are not guarantees of future performance and that its actual results of operations, financial condition and liquidity and

the development of the industry in which the Company operates may differ materially from those made in or suggested by the forward-looking

statements contained in this presentation. In addition, even if the NIS Group’s results of operations, financial condition and liquidity and the

development of the industry in which the Company and NIS Group operate are consistent with the forward-looking statements contained in this

presentation, those results or developments may not be indicative of results or developments in future periods. The information and opinions contained

in this presentation are provided as at the date of this presentation and are subject to change without notice.

No person is under any obligation to update or keep current the information contained herein.

By attending the presentation you confirm that you have read and understood foregoing limitations.

Top Related