Languages

Pages

Legal

Practical Implementation of

GASB 75 (OPEB)April 24, 2018

Webinar

Presented in association with

Presented by:

Stephen W. Blann, CPA, CGFM, CGMADirector of Governmental Audit QualityRehmann

2

Session Outline

• GASB 74 – OPEB Plans• GASB 75 – OPEB for Employers• Unique considerations for non-trusted plans• Implementation challenges by plan type• Initial journal entries• Alternate Measurement Method (small plans)

3

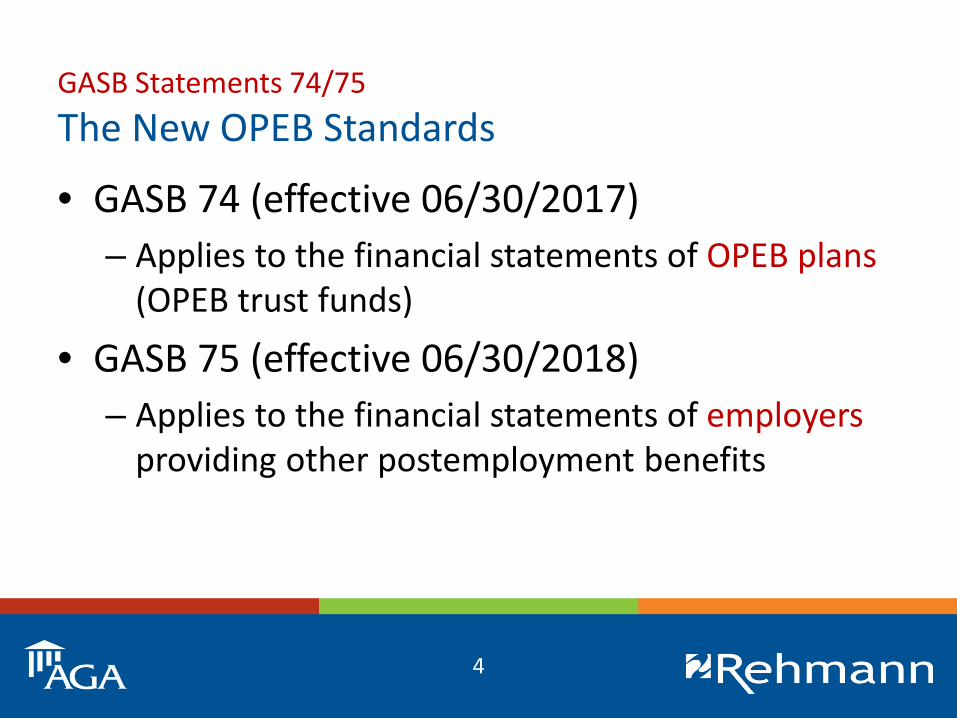

GASB Statements 74/75The New OPEB Standards

• GASB 74 (effective 06/30/2017)– Applies to the financial statements of OPEB plans

(OPEB trust funds)

• GASB 75 (effective 06/30/2018)– Applies to the financial statements of employers

providing other postemployment benefits

4

GASB Statements 74/75The New OPEB Standards

• OPEB Plans defined– Arrangements through which OPEB is determined,

assets dedicated for OPEB (if any) are accumulated and managed, and benefits are paid as they come due.

5

GASB Statements 74/75Defining Pension & OPEB

• Pensions– Retirement income and benefits (other than

healthcare) provided through a pension plan

6

GASB Statements 74/75Defining Pension & OPEB

• Other Postemployment Benefits (OPEB) defined– All postemployment healthcare benefits

• Medical, dental, vision, hearing, etc.• Regardless of whether provided by a pension plan

– Postemployment benefits other than retirement income not administered by a pension plan

• Death benefits, life insurance, disability, long-term care

– Excludes termination benefits

7

GASB Statements 74/75Defining Pension & OPEB

• Termination benefits (GASB 47):– An inducement to hasten the termination of

services (e.g., early retirement incentives)– May be voluntary or involuntary– Requires professional judgment to determine

employer’s intent and employee’s understanding– Recorded at the NPV of the benefits to be paid

when the agreement is made (not OPEB)

8

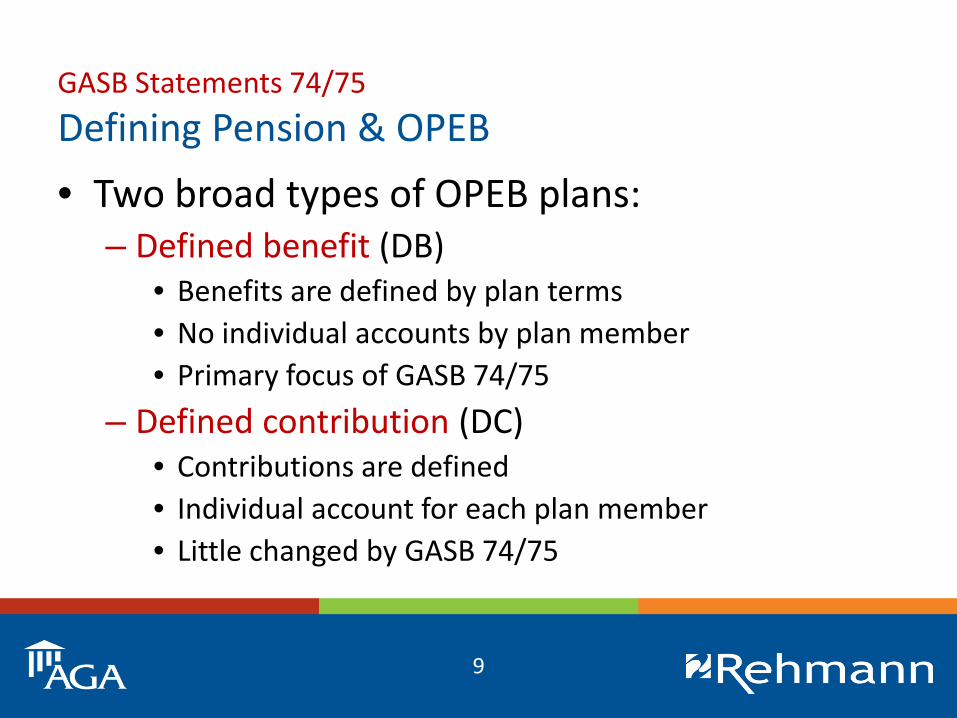

GASB Statements 74/75Defining Pension & OPEB• Two broad types of OPEB plans:

– Defined benefit (DB)• Benefits are defined by plan terms• No individual accounts by plan member• Primary focus of GASB 74/75

– Defined contribution (DC)• Contributions are defined • Individual account for each plan member• Little changed by GASB 74/75

9

GASB Statements 74/75Defining Pension & OPEB• Three types of defined benefit plans:

– Single-employer OPEB plan• A primary government and its component units may be

considered to be one employer– Agent multiple-employer OPEB plan

• Assets are pooled, but each employer’s share is legally available to pay the benefits of only its employees

– Cost-sharing multiple-employer OPEB plan• Assets are pooled, and may be used to pay benefits of

the employees of any participating employer

10

GASB Statements 74/75Defining Pension & OPEB

• GASB has determined that OPEB plans are conceptually similar to pensions, and has largely replicated the guidance from GASB 67/68 in GASB 74/75– Retains requirement for actuaries to consider the

implicit rate subsidy– Retains the option for small plans to use the

alternative measurement method

11

GASB Statements 74/75OPEB Plan Financial Statements

• Defined benefit or defined contribution plans administered through a qualifying trust or equivalent arrangement are reported in an OPEB trust fund– Resources accumulated for OPEB not in a

qualifying trust are reported in governmental / proprietary funds of the employer (or an agency fund if held for other governments)

12

GASB Statements 74/75OPEB Plan Financial Statements

• DB plans calculate and disclose the employer’s net OPEB liability, but do not record it in the OPEB trust fund, itself

• GASB 74 does not apply if there is not an “OPEB plan”

13

GASB Statements 74/75OPEB Plan Financial Statements

• Statement of Fiduciary Net Position– Major categories of assets held– Principal components of investments and

receivables– Deferred outflows of resources, liabilities, and

deferred inflows of resources typically small or non-existent

– Balance is fiduciary net position

14

GASB Statements 74/75OPEB Plan Financial Statements

• Statement of Changes in Fiduciary Net Position– Additions (employer / employee contributions,

investment income by component)– Deductions (benefits, plan administrative

expenses)– Should report all benefits paid (even if initially

paid directly by the employer)

15

GASB Statements 74/75OPEB Plan Financial Statements

16

CPE Prompt 1 of 4

• What is the relationship between GASB Statements 74 and 75?A. You either implement one or the other,

depending on the existence of an OPEB trustB. GASB 74 applies to OPEB plans, while GASB 75

applies to employers who provide OPEBC. GASB 74 applies to single-employer plans, while

GASB 75 applies to multiple-employer plansD. All of the above

17

GASB Statements 74/75Net OPEB Liability

• Recorded by the employer (not the plan)• Equal to the actuarially determined total OPEB

liability, less the net position of the OPEB trust fund

• Recorded in full accrual financial statements (certain portions are offset by deferred inflows/outflows and amortized)

18

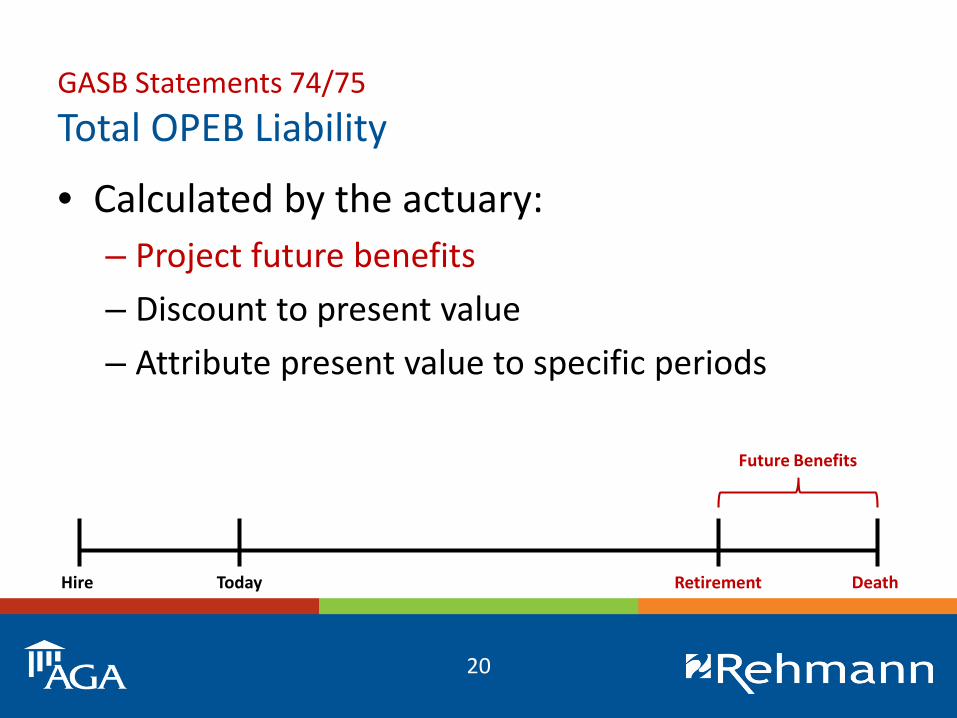

GASB Statements 74/75Total OPEB Liability

• Calculated by the actuary:– Project future benefits– Discount to present value– Attribute present value to specific periods

Hire Today DeathRetirement

19

GASB Statements 74/75Total OPEB Liability

• Calculated by the actuary:– Project future benefits– Discount to present value– Attribute present value to specific periods

Hire Today DeathRetirement

Future Benefits

20

GASB Statements 74/75Total OPEB Liability

• Calculated by the actuary:– Project future benefits– Discount to present value– Attribute present value to specific periods

Hire Today DeathRetirement

Future BenefitsDiscount Rate

21

GASB Statements 74/75Total OPEB Liability

• Calculated by the actuary:– Project future benefits– Discount to present value– Attribute present value to specific periods

Hire Today DeathRetirement

TOL

Service Cost

Future BenefitsDiscount Rate

22

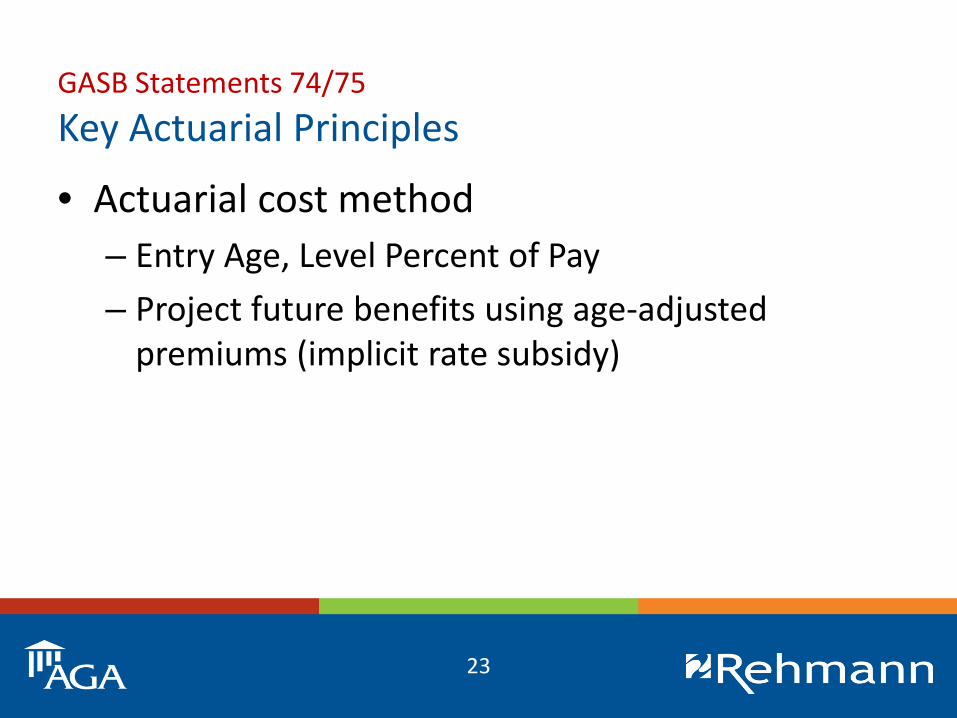

GASB Statements 74/75Key Actuarial Principles

• Actuarial cost method– Entry Age, Level Percent of Pay– Project future benefits using age-adjusted

premiums (implicit rate subsidy)

23

GASB Statements 74/75Key Actuarial Principles

• Expected return/discount rate– Single blended rate comprised of:

• Expected rate of return (years w/ sufficient assets)• AA 20-year muni bond rate (years w/ insufficient assets)

– A lower discount rate produces a higher liability and vice versa

24

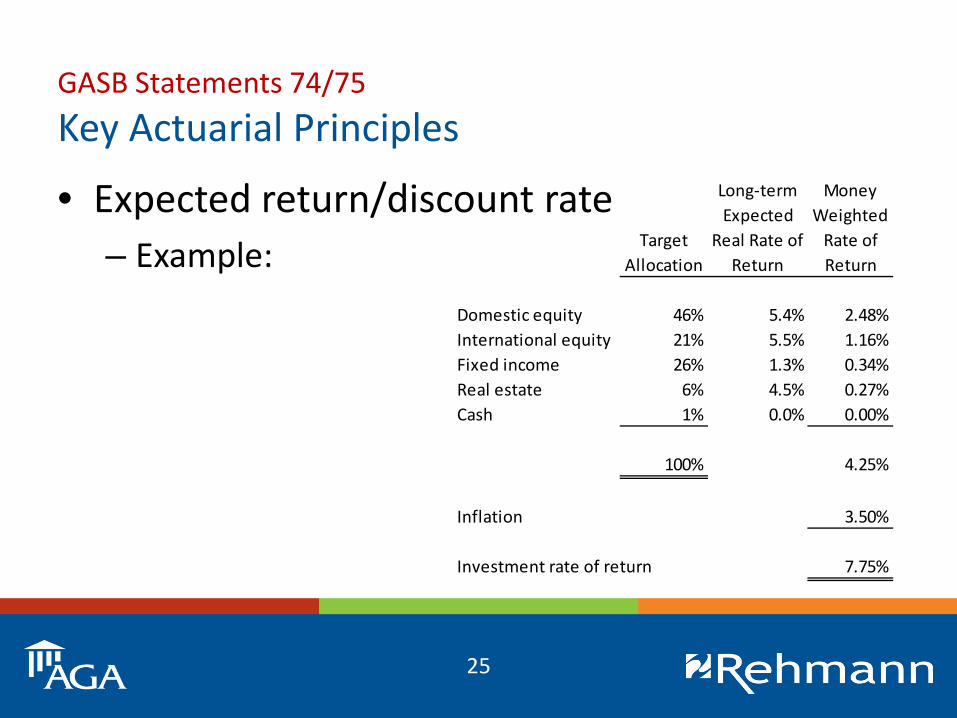

GASB Statements 74/75Key Actuarial Principles

• Expected return/discount rate– Example:

Long-term MoneyExpected Weighted

Target Real Rate of Rate ofAllocation Return Return

Domestic equity 46% 5.4% 2.48%International equity 21% 5.5% 1.16%Fixed income 26% 1.3% 0.34%Real estate 6% 4.5% 0.27%Cash 1% 0.0% 0.00%

100% 4.25%

Inflation 3.50%

Investment rate of return 7.75%

25

GASB Statements 74/75Key Actuarial Principles

• AA 20-year muni bond rate– Examples (12/31/17):

• Bond Buyer - 3.44%• S&P - 3.16%• Fidelity - 3.31%

Source: www.bartel-associates.com

26

GASB Statements 74/75Key Actuarial Principles

• Expected return/discount rate– Single blended rate calculation (example):

• Expected rate of return = 7.75% for 36 years• AA 20-year muni bond rate = 3.44% for 24 years• Blended rate = 6.03% (applied to all years)

27

GASB Statements 74/75Key Actuarial Principles

• Asset method– Fiduciary net position is calculated based on GAAP

(i.e., fair value of plan assets)

28

GASB Statements 74/75Key Actuarial Principles

• Annual Cost– OPEB Expense equal to the benefits earned during

the period with adjustments for deferred recognition of some gains/losses

– Net OPEB Liability is not smoothed– OPEB Expense (and impact on employer net

position) is smoothed through offsetting deferred inflows/outflows

29

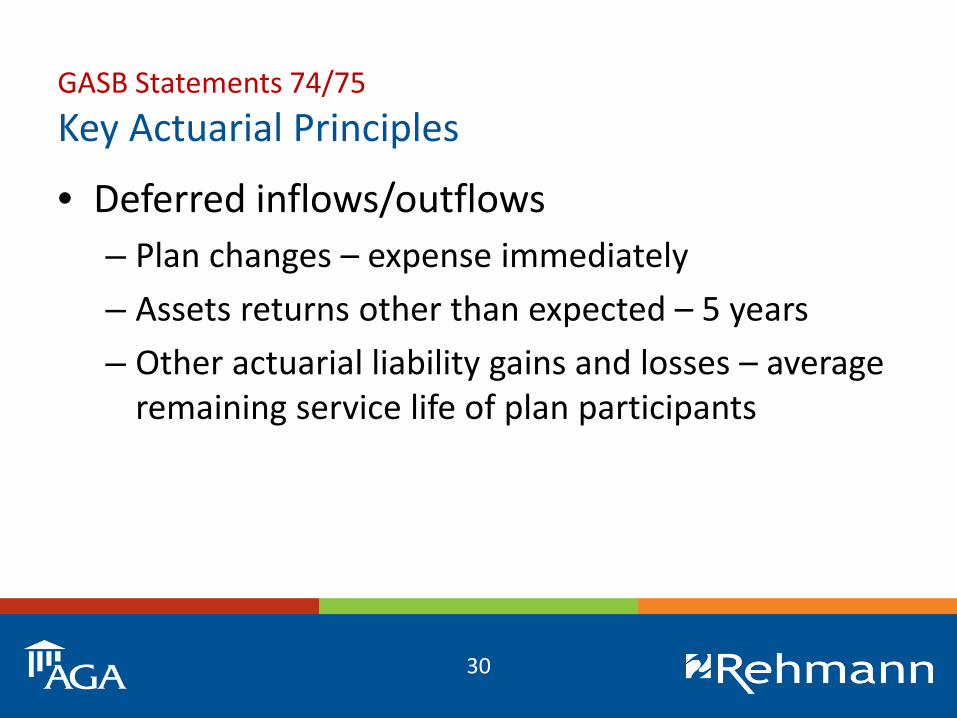

GASB Statements 74/75Key Actuarial Principles

• Deferred inflows/outflows– Plan changes – expense immediately– Assets returns other than expected – 5 years– Other actuarial liability gains and losses – average

remaining service life of plan participants

30

GASB Statements 74/75Key Actuarial Principles

• Sensitivity analyses– Changes in the discount rate

– Changes in the healthcare cost trend rate

31

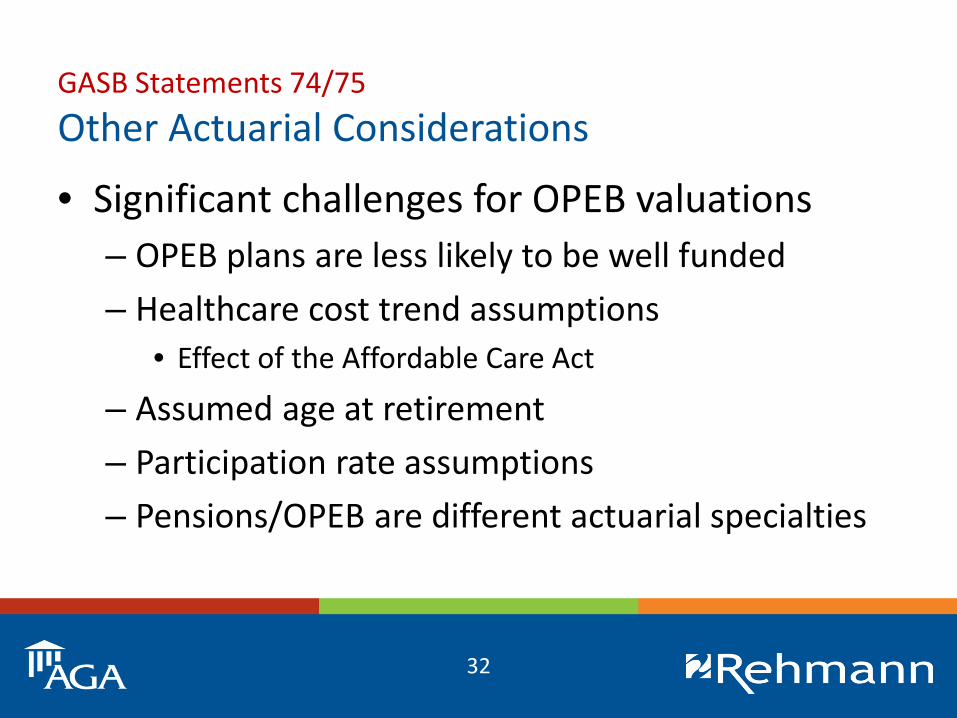

GASB Statements 74/75Other Actuarial Considerations

• Significant challenges for OPEB valuations– OPEB plans are less likely to be well funded– Healthcare cost trend assumptions

• Effect of the Affordable Care Act

– Assumed age at retirement– Participation rate assumptions– Pensions/OPEB are different actuarial specialties

32

CPE Prompt 2 of 4

• How should the actuary discount future projected benefits?A. Using the long-term expected real rate of return

on plan assetsB. Using a risk-free rate of returnC. Using a single blended rate based on A and BD. It’s a mystery

33

GASB Statements 74/75What to Expect from Your Actuary

• GASB 75-specific valuation– Valuation date & measurement date– Plan membership– Total OPEB Liability– Plan Fiduciary Net Position (may be separate)– Development of the single discount rate– Sensitivity analysis - discount rate

(cont.)

34

GASB Statements 74/75What to Expect from Your Actuary

• GASB 75-specific valuation– Sensitivity analysis - healthcare cost trend rate– List of actuarial assumptions used– Calculation of OPEB expense– Deferred inflows/outflows (may be separate)– Allocation by division (optional)– Sample footnotes and RSI (optional)

35

GASB Statements 74/75Timing Implications

• In an ideal world, everything would be measured in real time at the employer’s fiscal year end

• In reality, plans and employers don’t always have the same year end, and actuarial valuations take time to complete

36

GASB Statements 74/75Timing Implications• Actuarial valuations

– GASB 74 allows up to 24 months prior to the FYE of the OPEB plan

• Use update procedures to roll forward to the OPEB plan’s FYE (i.e., the “measurement date”)

– GASB 75 allows up to 30 months prior to the FYE of the employer

• Use update procedures to roll forward to the OPEB plan’s FYE (i.e., the “measurement date”)

37

GASB Statements 74/75Timing Implications

• “Measurement date”– Date at which the NOL is measured– Based on the plan’s FYE– May be up to one year prior to the employer’s FYE– OPEB contributions (including direct benefit

payments) made after the measurement date are reported as deferred outflows of resources

38

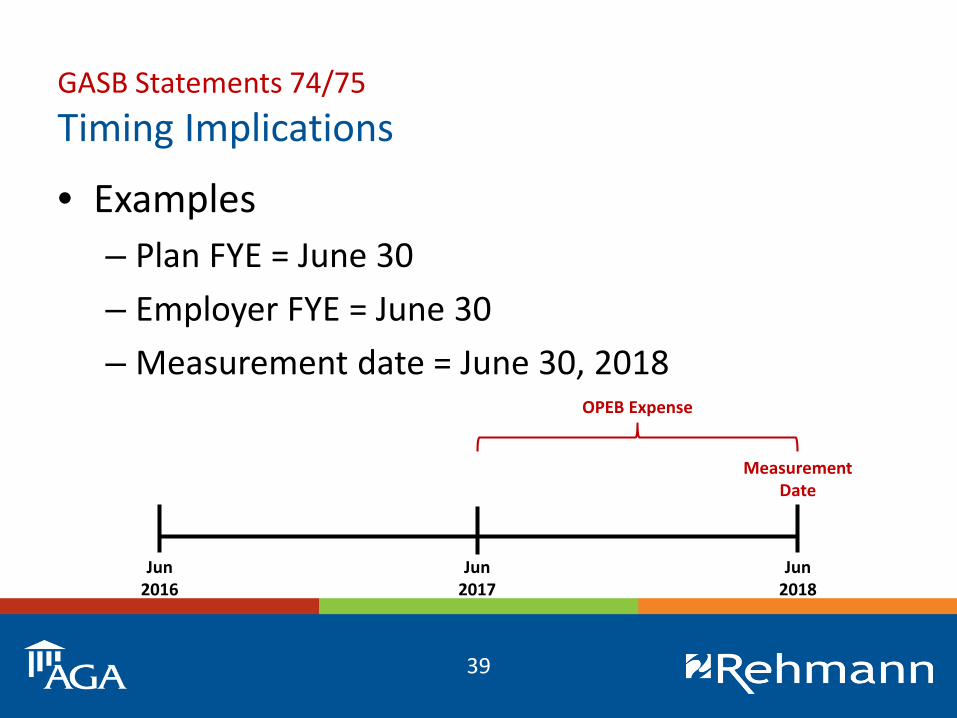

GASB Statements 74/75Timing Implications

• Examples– Plan FYE = June 30– Employer FYE = June 30– Measurement date = June 30, 2018

MeasurementDate

OPEB Expense

Jun2016

Jun2018

Jun2017

39

GASB Statements 74/75Timing Implications

• Examples– Plan FYE = June 30– Employer FYE = June 30– Measurement date = June 30, 2017

MeasurementDate

Deferred OutflowsOPEB Expense

Jun2016

Jun2018

Jun2017

40

GASB Statements 74/75Timing Implications

• Examples (MERS)– Plan FYE = December 31– Employer FYE = June 30– Measurement date = December 31, 2017

Jun2016

Jun2018

MeasurementDate

Deferred Outflows

Jun2017

OPEB Expense

Dec2017

Dec2016

41

GASB Statements 74/75Timing Implications

• Examples (MSPERS)– Plan FYE = September 30– Employer FYE = June 30– Measurement date = September 30, 2017

Sep2017

Jun2018

MeasurementDate

Deferred Outflows

Jun2017

Pension Expense

Dec2017

Dec2016

Sep2016

Mar2017

Jun2016

Mar2018

42

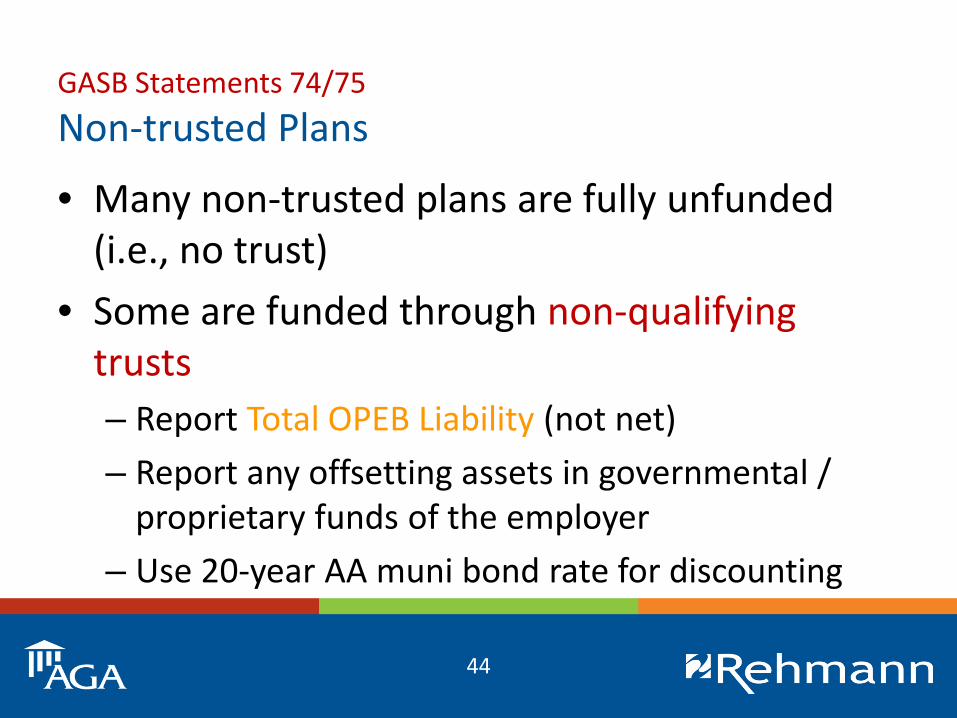

GASB Statements 74/75Non-trusted Plans

• Not all OPEB plans are administered through a qualifying trust or equivalent arrangement– Contributions/earnings are irrevocable– Plan assets are dedicated to providing OPEB– Plan assets are legally protected from creditors

43

GASB Statements 74/75Non-trusted Plans

• Many non-trusted plans are fully unfunded (i.e., no trust)

• Some are funded through non-qualifying trusts– Report Total OPEB Liability (not net)– Report any offsetting assets in governmental /

proprietary funds of the employer– Use 20-year AA muni bond rate for discounting

44

GASB Statements 74/75Non-trusted Plans

• GASB Implementation Guide 2017-3– Trust agreement calls for a return of amounts

remaining in trust once all obligations have been fulfilled

• Qualifying trust

45

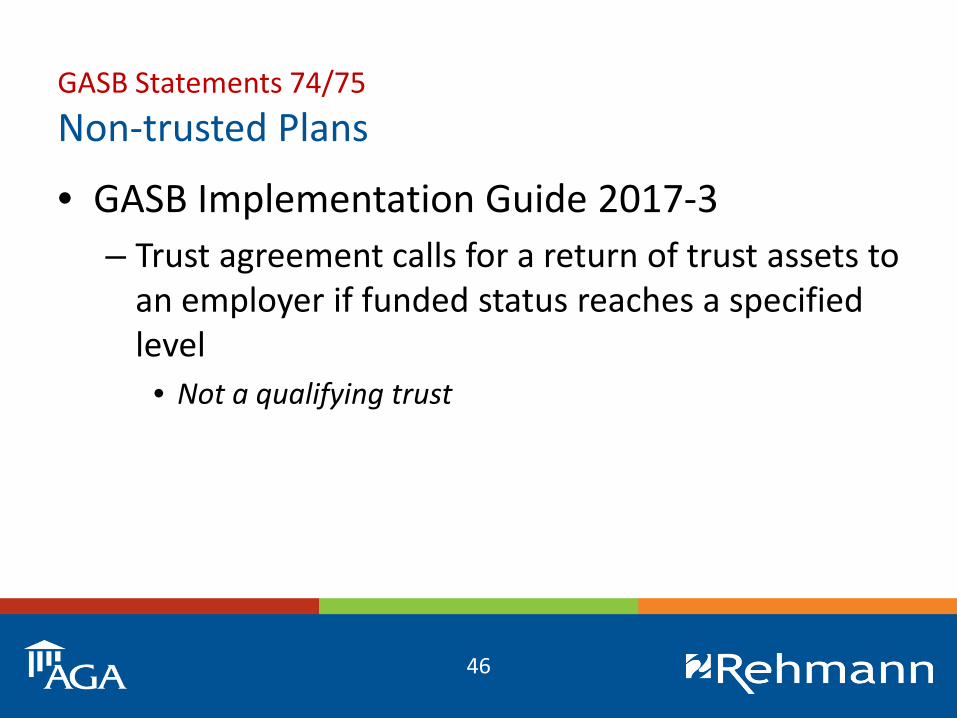

GASB Statements 74/75Non-trusted Plans

• GASB Implementation Guide 2017-3– Trust agreement calls for a return of trust assets to

an employer if funded status reaches a specified level

• Not a qualifying trust

46

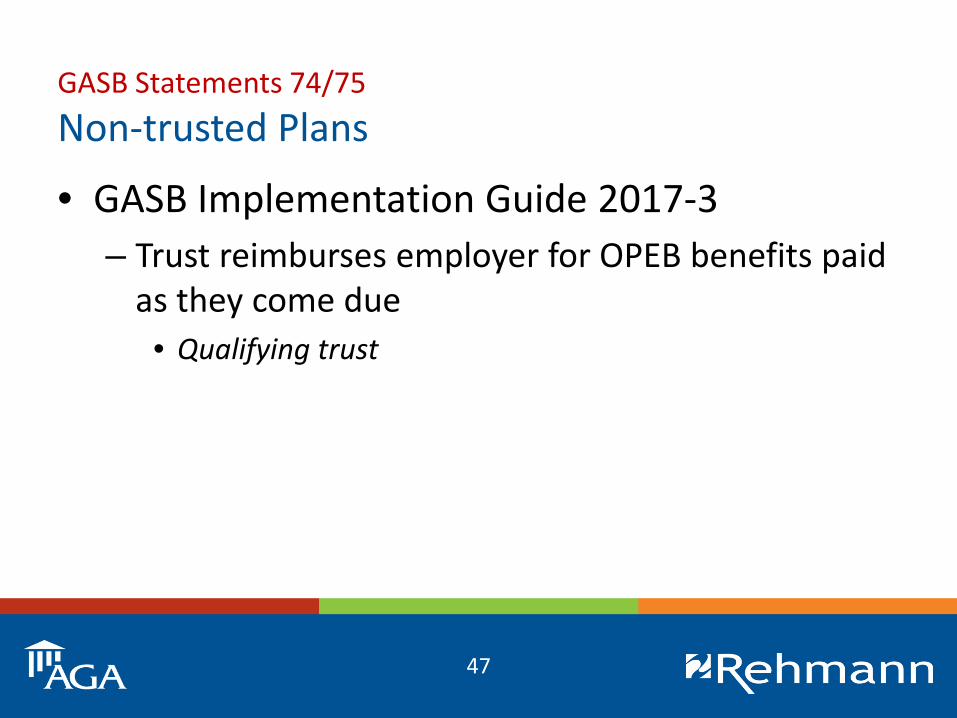

GASB Statements 74/75Non-trusted Plans

• GASB Implementation Guide 2017-3– Trust reimburses employer for OPEB benefits paid

as they come due• Qualifying trust

47

GASB Statements 74/75Non-trusted Plans

• GASB Implementation Guide 2017-3– A single trust is used for both OPEB and some

other benefit that is not OPEB (e.g., pensions or active employee healthcare)

• Not a qualifying trust, unless the “OPEB partition” of the trust is dedicated solely to providing OPEB

48

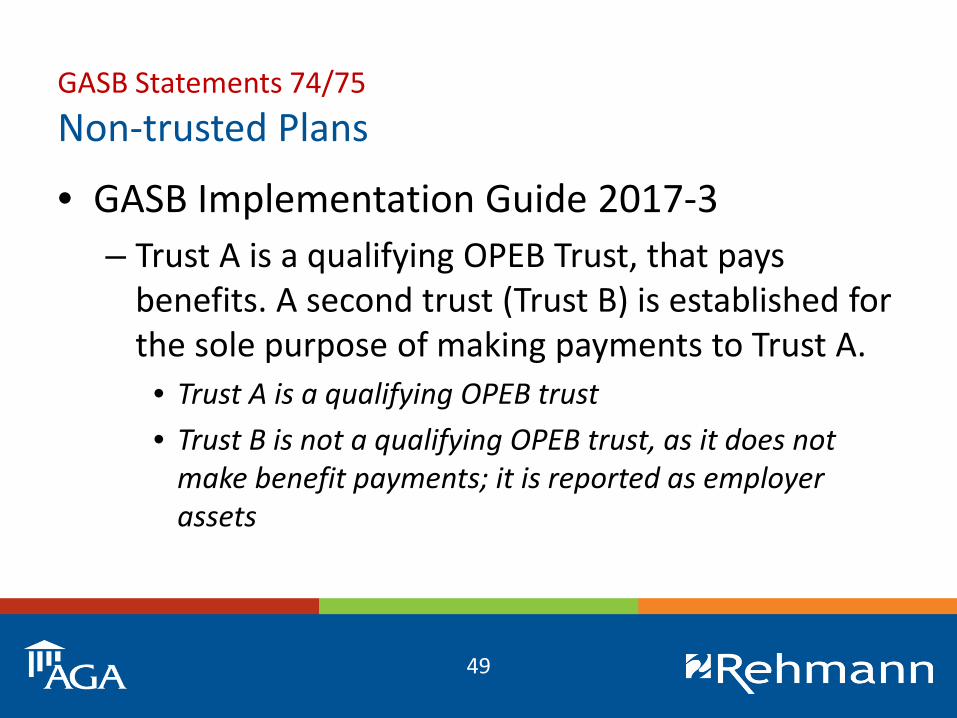

GASB Statements 74/75Non-trusted Plans

• GASB Implementation Guide 2017-3– Trust A is a qualifying OPEB Trust, that pays

benefits. A second trust (Trust B) is established for the sole purpose of making payments to Trust A.

• Trust A is a qualifying OPEB trust• Trust B is not a qualifying OPEB trust, as it does not

make benefit payments; it is reported as employer assets

49

GASB Statements 74/75Non-trusted Plans - Recap

Description Trust meeting par. 4 Non-Trust1 Recognize in Statement

of Net PositionNet OPEB Liability (NOL) Total OPEB Liability (TOL)

2 Present Value for TOL determined using

Long term rate of return (LTROR) or single blended rate of LTROR and AA 20 year Municipal Bond Index

AA 20-year municipal bond index

3 Recognize in Statementof Net Position

Deferred O/I for both TOL and Investments

Deferred O/I for TOL only

4 Recognize in Statementof Net Position

Deferred outflow for contributions after Measurement Date (MD)

Deferred outflow for OPEB payments after MD

5 OPEB related assets Recorded in Plan FS and used to determine Plan Fiduciary Net Position

Recorded in appropriate governmental or proprietary fund

6 OPEB expense Change in the NOL with appropriate deferrals and amortization

Change in TOL with appropriate deferrals and amortization

50

CPE Prompt 3 of 4

• If an employer provides OPEB, but has not established a qualifying trust:A. It should report its total OPEB liability, rather than

its net OPEB liabilityB. It should use the risk-free rate of return to discountC. It should report any assets accumulated for OPEB

as employer assetsD. All of the above

51

GASB Statements 74/75Unique Challenges by Plan Type

• Single-Employer– May be administered by pension, but must be

accounted for separately– May be in a multiple-employer pension but single-

employer OPEB (different actuaries/processes)– More frequently pay-as-you-go– May share some assumptions with pension, and

differ in others

52

GASB Statements 74/75Unique Challenges by Plan Type

• Agent Multiple-Employer– Actuarial valuations are conducted separately for

each participating employer, but may not allow for unique assumptions for each

– Need to ensure that the actuarial certification (cover letter) is addressed to the employer

– Will need employer-specific info provided by plan for fiduciary net position

53

GASB Statements 74/75Unique Challenges by Plan Type

• Cost-Sharing Multiple-Employer– Actuarial valuation is conducted for the plan as a

whole, with each employer having a proportionate share to record

– Will need employer-specific info provided by plan– Pension and OPEB portions may be comingled

internally, and need to be separated for GAAP reporting

54

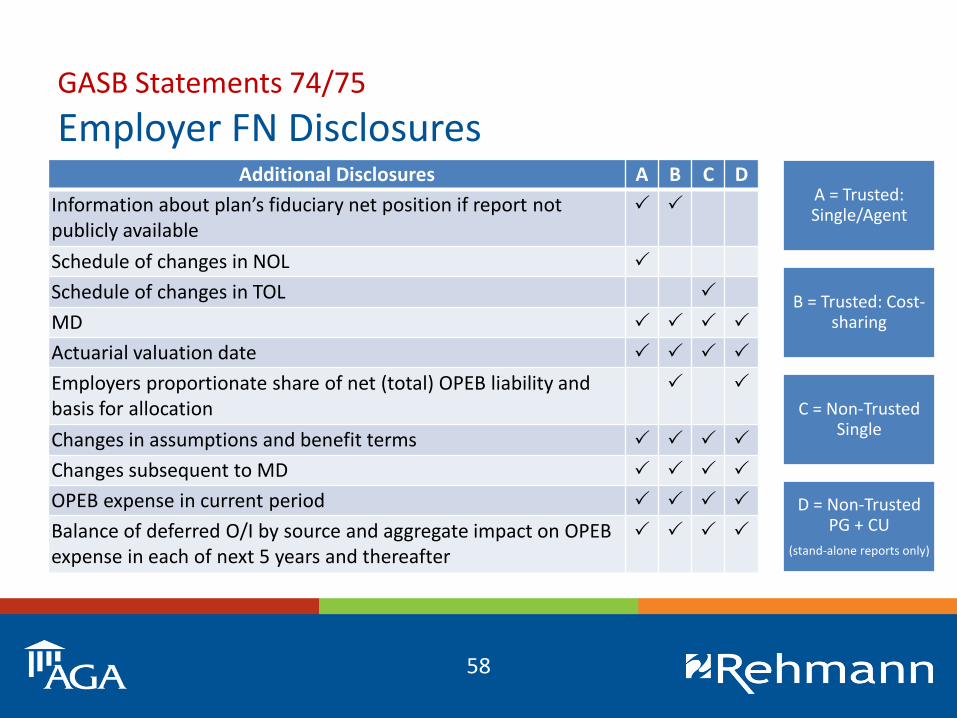

GASB Statements 74/75Employer FN Disclosures

Plan Description A B C DName of plan, administrator of plan, and type of plan

Benefit terms, including (1) classes of employees covered, (2) types of benefits, (3) key elements of OPEB formula, (4) terms or policies with respect to automatic benefit changes, including ad hoc cost of living adjustments (COLAs), (5) legal authority

Number of employees covered

Fact that no assets accumulated in a trust

Contribution requirements, including (1) authority under which contributions made, (2) legal or maximum contributions rates, (3) contribution rates, and (4) contributions made

Authority under which to pay OPEB benefits as they come due and amount

Availability of audited plan financial statements

A = Trusted: Single/Agent

B = Trusted: Cost-sharing

C = Non-Trusted Single

D = Non-Trusted PG + CU

(stand-alone reports only)

55

GASB Statements 74/75Employer FN Disclosures

A = Trusted: Single/Agent

B = Trusted: Cost-sharing

C = Non-Trusted Single

D = Non-Trusted PG + CU

(stand-alone reports only)

Assumptions and Other Inputs A B C D

Significant assumptions, including inflation, healthcare cost trend rates, salary changes, postemployment benefit changes

Source of mortality assumptions

Dates of experience studies

Fact that projections of sharing of benefit costs based on established pattern of practice

NOL sensitivity to healthcare cost trend rate (±1%)

TOL sensitivity to healthcare cost trend rate (±1%)

56

GASB Statements 74/75Employer FN Disclosures

A = Trusted: Single/Agent

B = Trusted: Cost-sharing

C = Non-Trusted Single

D = Non-Trusted PG + CU

(stand-alone reports only)

Discount Rate A B C D

Discount rate used

Assumptions about projected cash flows

Long-term expected rate of return on plan investments and how determined

Municipal bond rate used

Periods of projected benefit payments applied to long-term rate of return and municipal bond rate, if applicable

Assumed asset allocation and long-term expected real rate of return for each major asset class

NOL sensitivity to discount rate (±1%)

TOL sensitivity to municipal bond rate (±1%)

57

GASB Statements 74/75Employer FN Disclosures

A = Trusted: Single/Agent

B = Trusted: Cost-sharing

C = Non-Trusted Single

D = Non-Trusted PG + CU

(stand-alone reports only)

Additional Disclosures A B C DInformation about plan’s fiduciary net position if report not publicly available

Schedule of changes in NOL

Schedule of changes in TOL

MD

Actuarial valuation date

Employers proportionate share of net (total) OPEB liability and basis for allocation

Changes in assumptions and benefit terms

Changes subsequent to MD

OPEB expense in current period

Balance of deferred O/I by source and aggregate impact on OPEB expense in each of next 5 years and thereafter

58

GASB Statements 74/75Employer RSI

A = Trusted: Single/Agent

B = Trusted: Cost-sharing

C = Non-Trusted Single

D = Non-Trusted PG + CU

(stand-alone reports only)

10-Year Schedules A B C D

Changes in NOL by source

Components of NOL and related ratios

Proportionate share of NOL

Employer contributions

Changes in TOL by source

TOL as a percentage of covered employee payroll

Proportionate share of TOL

59

GASB Statements 74/75Transition• Restate beginning equity

– Remove any Net OPEB Obligation (GASB 45)– Add beginning Net OPEB Liability (GASB 75)– Add any beginning deferred outflow for contributions

subsequent to the measurement date (all other deferrals are prospective only)

• RSI schedules– Prospective only (if information is not available)– Contributions history will generally be available

60

GASB Statements 74/75Transition – Initial Journal Entries• Sample City, a 06/30 FYE has the following

facts related to its 12/31 OPEB Plan:– Sample City uses a third-party to collect and invest

OPEB assets in a qualifying trust– The amounts on the next slide occurred related to

the self-insured OPEB Plan

61

GASB Statements 74/75Transition – Initial Journal Entries

GASB 45 OPEB Obligation-6/30/17 A $ 800,000

Net OPEB Liability-12/31/16 B 3,500,000

Net OPEB Liability-12/31/17 C 4,200,000

Net OPEB Claims & Expense 01/01/17-6/30/17 D 1,000,000

Contributions to the Trust 01/01/17-6/30/17 E 600,000

Net OPEB Claims & Expense 01/01/18-6/30/18 F 1,100,000

Contributions to the Trust 01/01/18-6/30/18 G 600,000

Net OPEB Claims & Expense FY 6/30/18 H 2,200,000

Annual Contributions to the Trust 6/30/18 I 1,200,000

Investment return over expectation CY 2017 J 200,000

Actuarial losses on liability assumption for CY 2017 K 210,000

62

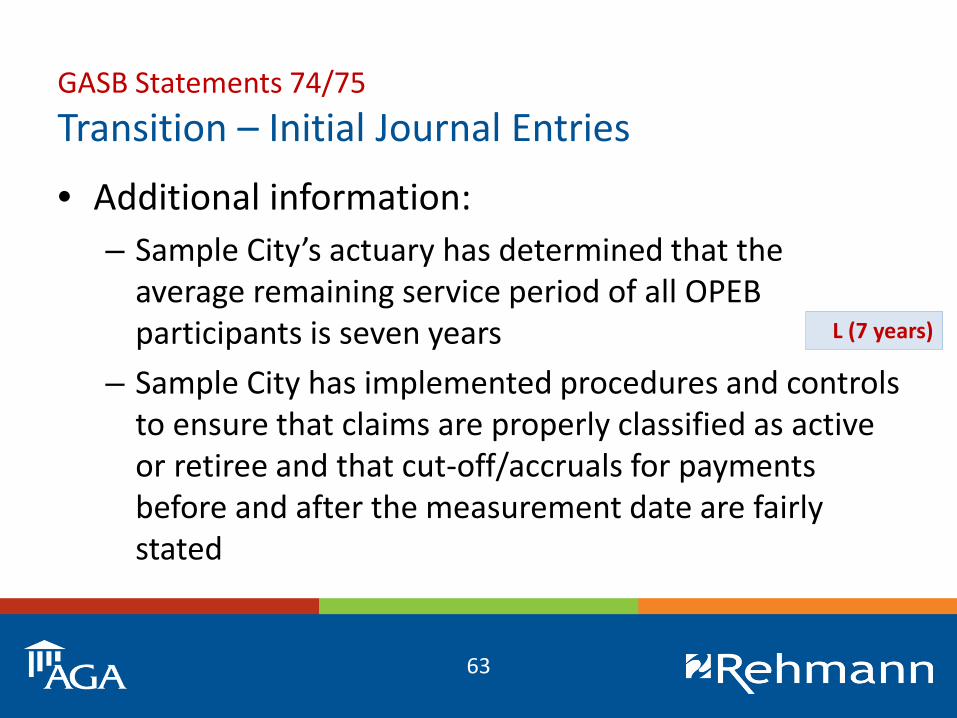

GASB Statements 74/75Transition – Initial Journal Entries

• Additional information:– Sample City’s actuary has determined that the

average remaining service period of all OPEB participants is seven years

– Sample City has implemented procedures and controls to ensure that claims are properly classified as active or retiree and that cut-off/accruals for payments before and after the measurement date are fairly stated

L (7 years)

63

GASB Statements 74/75Transition – Initial Journal EntriesEliminate the Net OPEB Obligation from GASB 45

Net OPEB Obligation A 800,000

Net Position 800,000

Book Beginning Net OPEB Liability per GASB 75

Net Position B 3,500,000

Net OPEB Liability 3,500,000

Book Beginning Deferred Outflows for Contributions Subsequent to the MD

Deferred Outflow-OPEB Payments/Contributions (1/1/17-6/30/17)

D+E 1,600,000

Net Position 1,600,000

64

GASB Statements 74/75Transition – Initial Journal EntriesRecord 2018 Amounts

OPEB expense (next slide) 3,980,000

Deferred outflow - contributions after MD F+G-D-E 100,000

Deferred outflow - assumption losses K-(K/L) 180,000

Deferred inflow - excess investment return J-(J/5) 160,000

Payments / contributions to trust * H+I 3,400,000

Net OPEB Liability C-B 700,000

* Assumes these were expensed as paid

65

GASB Statements 74/75Transition – Reconciliation of OPEB Expense

Change in the Net OPEB Liability C-B 700,000

Current fiscal year OPEB payments H 2,200,000

Current fiscal year contributions I 1,200,000

Flow through of BOY deferred OPEB payments after MD D 1,000,000

Flow through of BOY deferred contributions to the Trust E 600,000

EOY deferral for OPEB Payments between MD & FYE F (1,100,000)

EOY deferral for OPEB Payments between MD & FYE G (600,000)

Deferred outflow - actuarial losses [K-(K/L)] (180,000)

Deferred inflow - excess investment earnings [J-(J/5)] 160,000

Total = OPEB Expense $3,980,000

66

GASB Statements 74/75Transition – Allocations by Fund

• GASB does not specify how to allocate by fund– General rule: fund that is expected to pay the

liability– No JE in modified-accrual funds– Allocate to enterprise and internal service funds

on a rational basis (preferably contributions)– Use cost-sharing methodology for significant

changes in proportion from year to year

67

CPE Prompt 4 of 4

• When recording adjustments for GASB 75, an employer should:A. Book a liability in the general fundB. Book a liability in the government-wide financial

statements, split between governmental and business-type activities

C. Book a liability in the government-wide financial statements and any proprietary funds that are expected to pay for the cost of OPEB

D. Any of these approaches are permitted

68

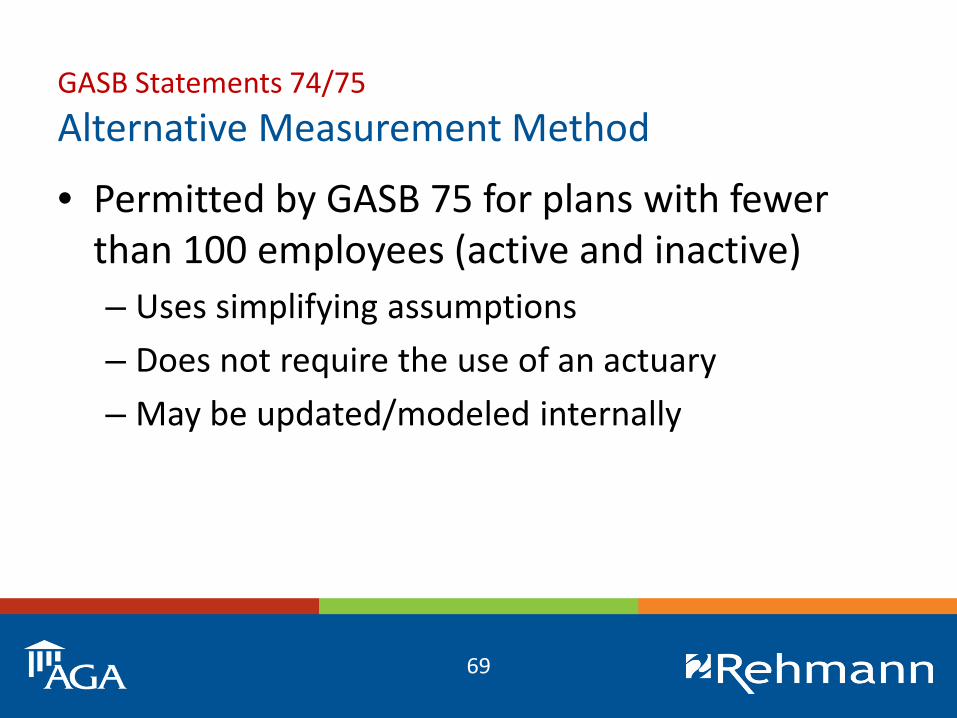

GASB Statements 74/75Alternative Measurement Method

• Permitted by GASB 75 for plans with fewer than 100 employees (active and inactive)– Uses simplifying assumptions– Does not require the use of an actuary– May be updated/modeled internally

69

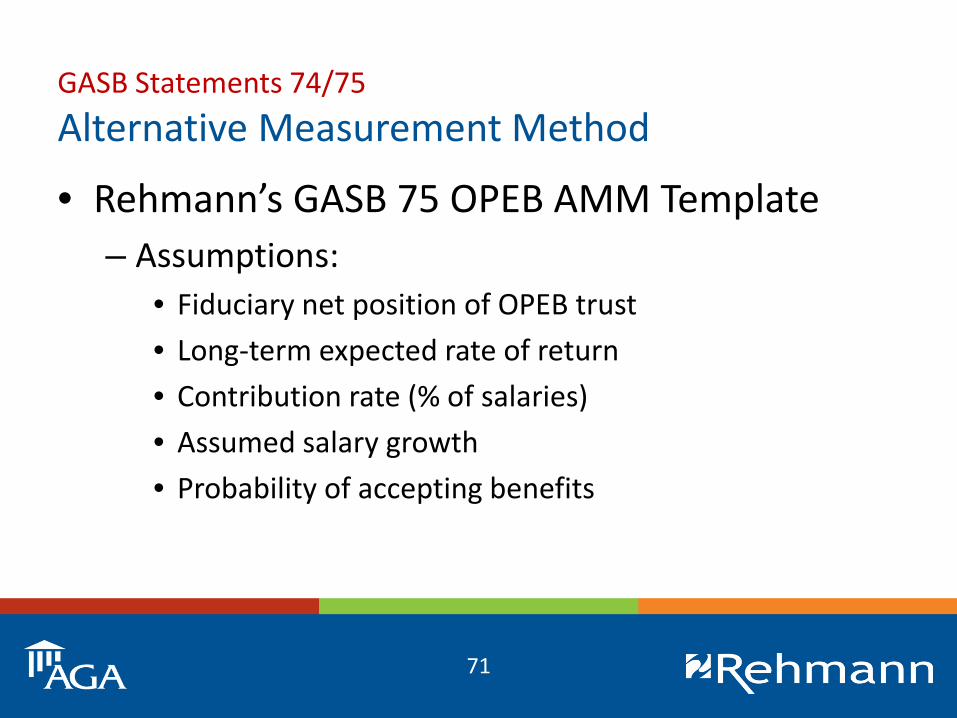

GASB Statements 74/75Alternative Measurement Method

• Rehmann’s GASB 75 OPEB AMM Template– Assumptions:

• Average retirement age• Benefits continue until (age/years/death)• Years to vest• Current cost of coverage (single/married, age-based)• Healthcare cost trend rate• AA 20-year muni bond rate

(cont.)

70

GASB Statements 74/75Alternative Measurement Method

• Rehmann’s GASB 75 OPEB AMM Template– Assumptions:

• Fiduciary net position of OPEB trust• Long-term expected rate of return• Contribution rate (% of salaries)• Assumed salary growth• Probability of accepting benefits

71

GASB Statements 74/75Alternative Measurement Method

• Rehmann’s GASB 75 OPEB AMM Template– Sample calculation:

• 30 employees (26 active, 4 inactive)• Average age at retirement = 62• Vest in 10 years, benefits provided until death• Plan is minimally funded ($12k), and pay-as-you-go• Rate of return = 5% investments; 3.31% AA 20-year

– Net OPEB Liability = $350,000

72

GASB Statements 74/75Alternative Measurement Method

• Rehmann’s GASB 75 OPEB AMM Template– Change in assumptions:

• Average age at retirement = 62 65

– Net OPEB Liability = $350,000 $110,000

73

GASB Statements 74/75Alternative Measurement Method

• Rehmann’s GASB 75 OPEB AMM Template– Change in assumptions:

• Rate of return = 5% 7%

– Net OPEB Liability = $350,000 $348,000

74

GASB Statements 74/75Alternative Measurement Method

• Rehmann’s GASB 75 OPEB AMM Template– Change in assumptions:

• Employer contributions = 0% 5%

– Net OPEB Liability = $350,000 $290,000

75

GASB Statements 74/75Alternative Measurement Method

• Rehmann’s GASB 75 OPEB AMM Template– Change in assumptions:

• Employer contributions = 0% 5%• Rate of return = 5% 7%

– Net OPEB Liability = $350,000 $235,000

76

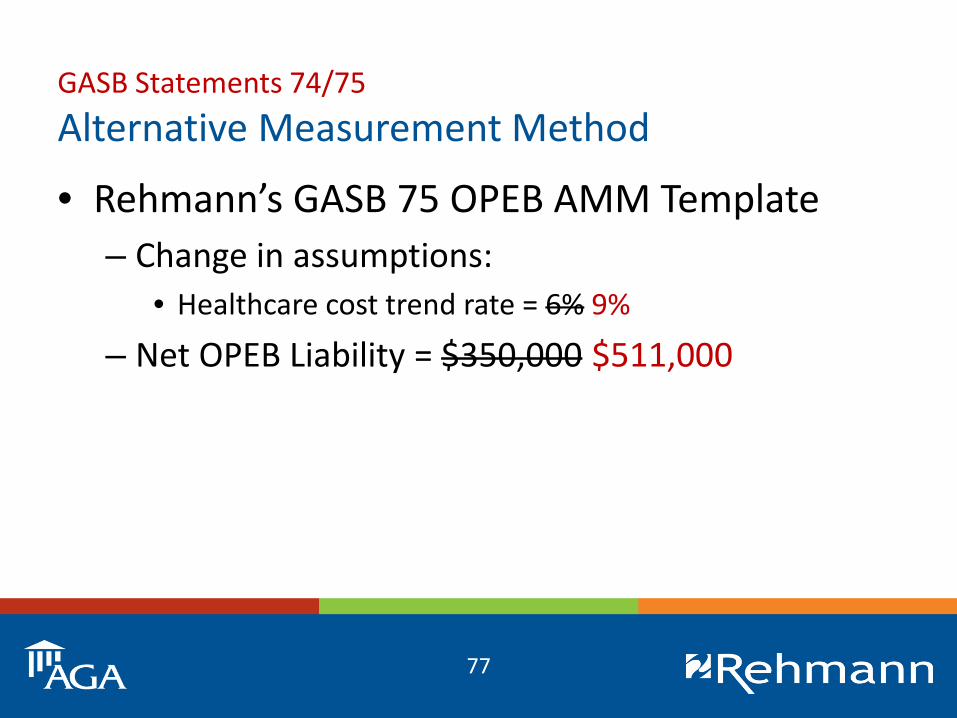

GASB Statements 74/75Alternative Measurement Method

• Rehmann’s GASB 75 OPEB AMM Template– Change in assumptions:

• Healthcare cost trend rate = 6% 9%

– Net OPEB Liability = $350,000 $511,000

77

GASB Statements 74/75Alternative Measurement Method

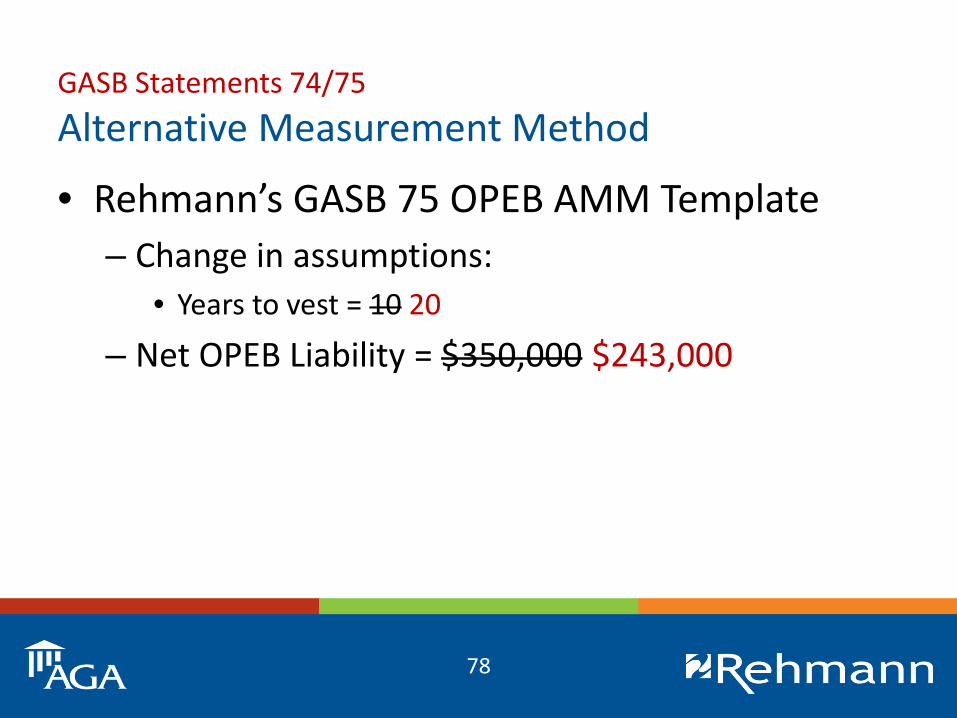

• Rehmann’s GASB 75 OPEB AMM Template– Change in assumptions:

• Years to vest = 10 20

– Net OPEB Liability = $350,000 $243,000

78

Questions?

79

For more information...

Stephen W. Blann, CPA, CGFM, CGMADirector of Governmental Audit [email protected]/government

80

Top Related