Languages

Pages

Legal

Building on Terra FirmaOur Experience with Infill Development

Tuesday, October 3, 2017 | 10:45 am to 12 pm

Omni Hotel | Providence

Kevin Walker | Acting Executive Director

Northcountry Cooperative FoundationPhoto, Fargo Forum

August 29, 2009.

ZUMBRO RIDGE ESTATES

ROCHESTER, 90 UNITS, 2017

20

BENNETT PARK COOPERATIVE

MOORHEAD, 70 UNITS, 2007

SUNRISE VILLA COOPERATIVE

CANNON FALLS, 47 UNITS

PRAIRIE LAKE ESTATES HOMEOWNERS

COOPERATIVE

KENOSHA, WI, 70 UNITS, 2013PARK PLAZA COOPERATIVE

FRIDLEY, 88 UNITS, 2011

FIVE LAKES COOPERATIVE

FAIRMONT, 94 UNITS, 2014

MADELIA MOBILE VILLAGE COOPERATIVE

MADELIA, 57 UNITS, 2008

STONEGATE COOPERATIVE

LINDSTROM, 50 UNITS, 2012

HILLCREST COMMUNITY COOPERATIVE

CLARKS GROVE, 90 UNITS, 2015

Track record

PAMMEL CREEK ESTATES, INC.

LA CROSSE, WI 51 UNITS

750 households

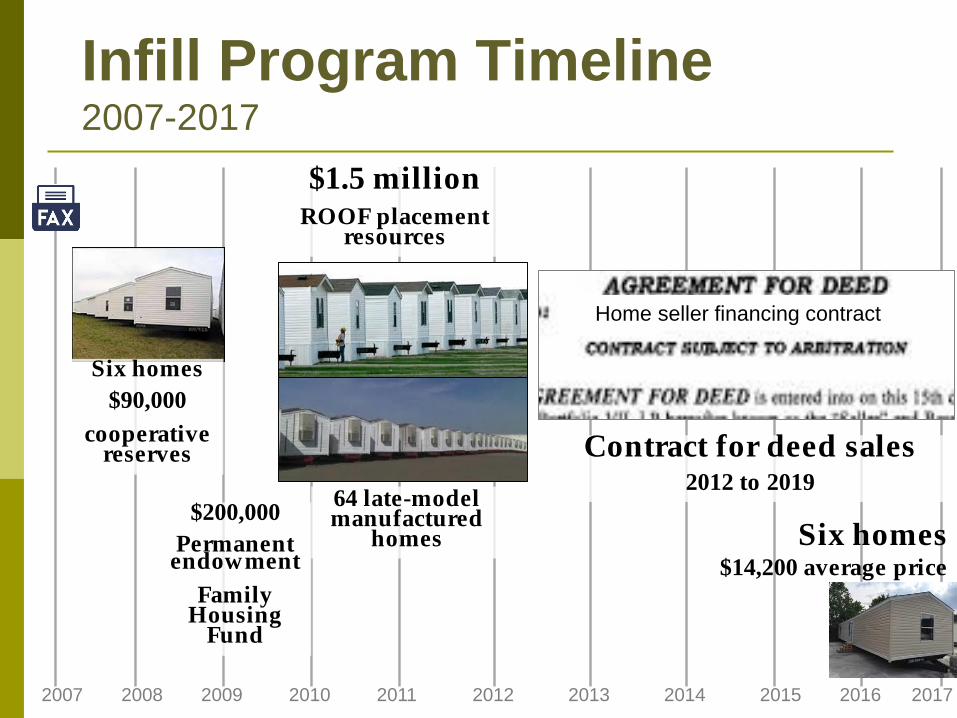

Infill Program Timeline2007-2017

21

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Six homes

$90,000

cooperative reserves

$200,000

Permanent endowment

Family Housing

Fund

$1.5 millionROOF placement

resources

64 late-model manufactured

homes

Home seller financing contract

Contract for deed sales2012 to 2019

Six homes$14,200 average price

NCF Infill ProgramTwo models

22

FEMA Surplus – 70 homes (2007 – 2019)

• 18-month mandatory stewardship period ($195 to $250 mtce fee)

• NCF provided credit toward purchase at end of 18 months

• Average sales price: $26,000

• Down payment: $1K to $2K;

• Monthly housing payments: $210 to $425 (5- to 7-year term)

FEMA Auction – 6 homes (2017)

• Median sales price: $37,000

• Down payment: $3,700

• Monthly housing payments: $370 (10-year term)

NCF Home Placement ProgramOutcomes

23

1. Performance. Default rate: 7.1%. All defaults have resulted in buyer advancing title

and keys to NCF (“repossession by mutual consent”)

2. Populations served.

1. Race/ethnicity: 71%: white; 16% Latino; 11%: American Indian; 2% Asian.

2. Income: 28% at 50% AMI, 42% at 60% AMI, 56% at 80% AMI.

3. Credit score: over half without a credit score.

3. Increase in net revenue to host cooperatives.

1. Cooperatives served: six communities.

2. Average of 12% contributions to cooperatives’ net revenue.

3. Earned income strategy.

1. Home placement fee (two to three months’ lot rent) from co-op after co-op has

realized two to three months of occupancy.

2. Developer fee (charged to buyer)

24

ImpactHappy homeowners!

ImpactResident-owned communities

25

Participating

Cooperatives (7 of 9)

NCF infill

Total lot

rent

Infill Revenue as

Share of Overall Revenue

71%

16%

11%

2%

White

Latino

American Indian

Southeast Asian

26

ImpactPopulations served

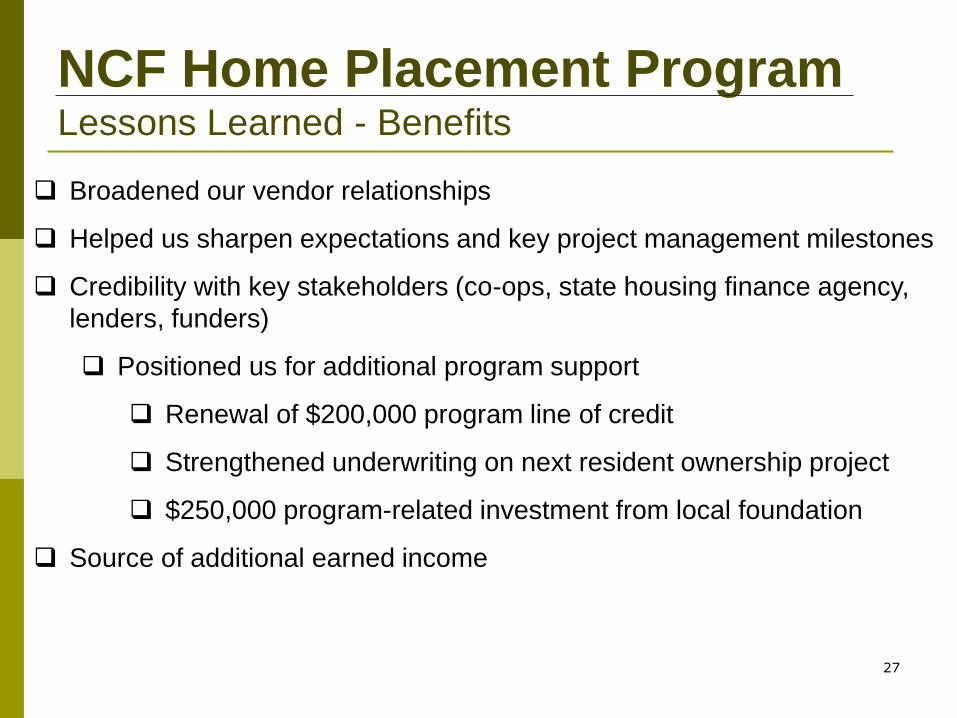

NCF Home Placement ProgramLessons Learned - Benefits

27

Broadened our vendor relationships

Helped us sharpen expectations and key project management milestones

Credibility with key stakeholders (co-ops, state housing finance agency,

lenders, funders)

Positioned us for additional program support

Renewal of $200,000 program line of credit

Strengthened underwriting on next resident ownership project

$250,000 program-related investment from local foundation

Source of additional earned income

NCF Home Placement ProgramLessons Learned – Challenges / Expectations

28

1. Maintenance/repairs (during/after 18 months)

2. Management services

3. Homebuyer support

Placement Replacement Strategy

What to Consider and Pilot Programs

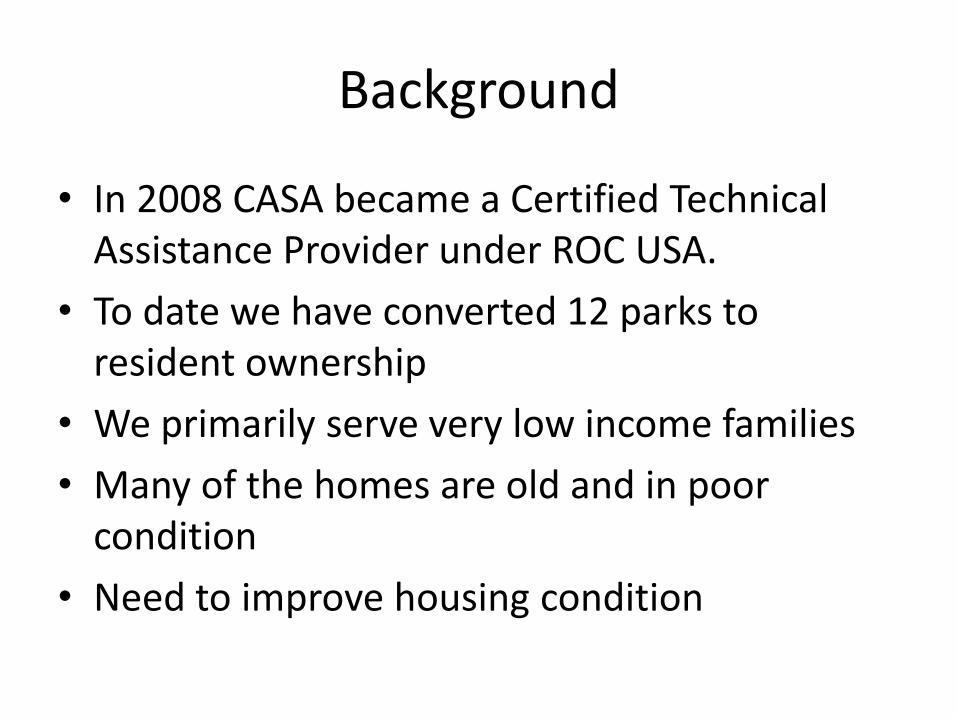

Background

• In 2008 CASA became a Certified Technical Assistance Provider under ROC USA.

• To date we have converted 12 parks to resident ownership

• We primarily serve very low income families

• Many of the homes are old and in poor condition

• Need to improve housing condition

What to Consider

• Program Development

• Financing Units

• Identifying Prospective Clients

• Coordination with Co-op’s

• Ordering and Placing Homes

• Counseling Buyers

• Marketing

Program Development

• Define the scope of the problem, create goals and objectives

• Analyze barriers

• Identify prospective clients

• Identify resources

• Close deals

• Collect data

• Determine how to fund ongoing operations of the program

Financing Units

• Identify potential resources for borrowers to purchase home

– For and Non Profit lenders with a single family loan product

– USDA RD 502 Program

– State Resources (AWHTC – lease program buys down cost by +/- $20K)

– IDA’s –DPA

– Energy Trust of Oregon - DPA

Identifying Prospective Clients

• Residents in Coop’s

– What is their appetite for a new home

– What aspects will improve that appetite (DPA, size, location, condition of existing home, etc)

– What is their ability to qualify for a loan

• Residents in NP Owned Parks

• Fee Simple

Working with the Co-op’s

• Identify which Coop’s have the most need and best opportunity

• Engage the Board for support of the program• Educate the Board on how the program works

– Meetings– Materials– FAQ’s– Contact info

• Have them spread the word to members of the Cooperative

• Coordinate on-site work with the Board building committee

Ordering and Placing Homes

• Working with either an intermediary or directly with the manufacturer

• Coordinating move

• Hiring a contractor to set the unit, to hook up utilities, and to install skirting, stairs and porches.

• Permits and inspections

Counseling Homebuyers

• Identify homebuyer barriers to buying a manufactured home (credit issues, limited income, size of family, etc.)

• Identify partners to counsel homebuyers

• Connecting homebuyer with partner

Marketing

• Co-op’s

• Employers

• Funders

• Partners

Pilots

• Bella Vista Estates Cooperative (Local and state resources)

• Umpqua Ranch Cooperative (USDA Rural Development 502 Program, Energy Trust of Oregon)

Contact Information

Lisa Rogers

(503) 687-3306

Sumiko Taylor-Hill

(503) 687-3319

Top Related