Languages

Pages

Legal

April, 2009

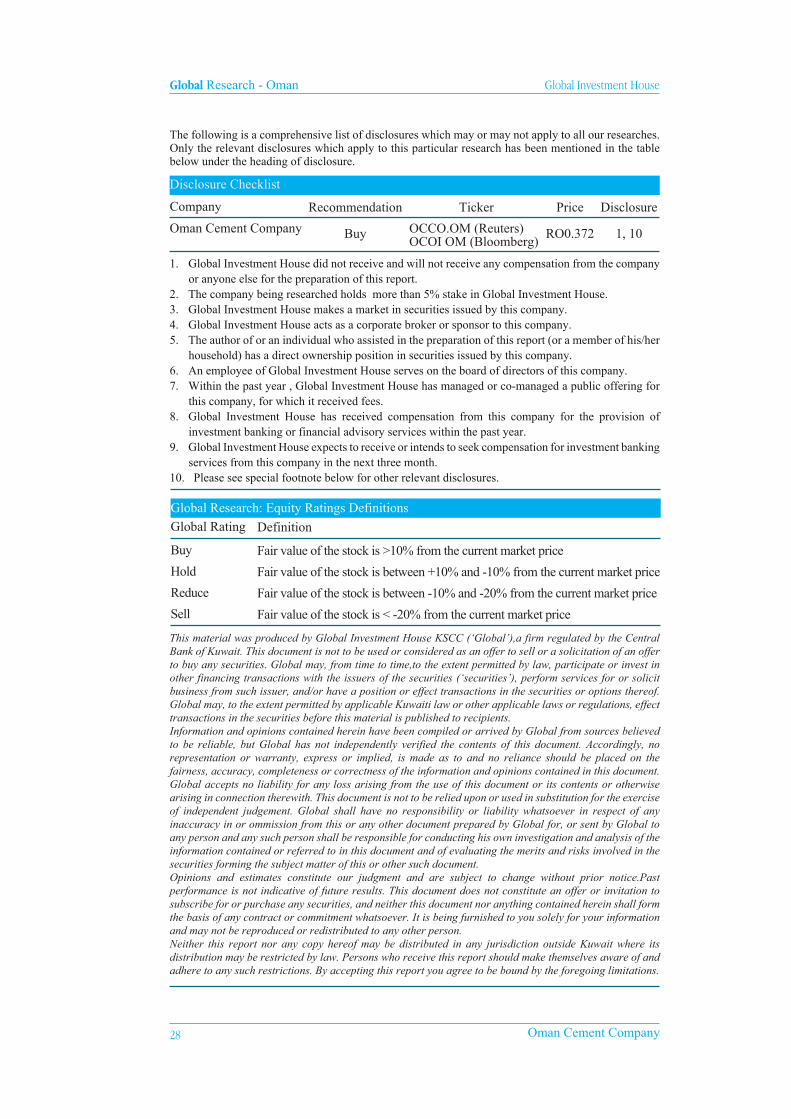

Buy

Oman Cement Company

Oman Cement Company 1

Global Research - Oman

Om

an

Faisal Hasan, CFAHead of [email protected] No:(965) 22951270

Hettish KumarFinancial [email protected] No:(965) 22951281

Tickers:OCCO.OM (Reuters)OCOI OM (Bloomberg)

Listing:Muscat Securities Market

Current Price:RO0.372 (As on April 13th, 2009)

Investment Update

Investment Summary

• Oman Cement Company (OCC) posted revenue of RO63.5mn which was higher by 9% as per our estimates of RO58.3mn for 2008. Difference in the forecasted and actual revenue was because of the increase in the price cap during the year as well as import of higher amount of clinker and cement. Company sales volume increased by 14.6% to 2.1mn tons as compared to 1.87mn tons in 2007. On the other hand local sales price increased by 12.2% to RO29.7/ton whereas the export price rose by 11.6% to RO36.5/ton.

• OCC’s cost of sales increased by 69% to RO49.65mn in 2008. The increase in cost was due to high purchase cost of cement and clinker imported under instructions from the government in order to meet the local demand. The company imported 0.92mn tons of clinker during the year to meet the demand, which is 42% higher as against 0.53mn tons during the previous year.

• OCC’s other income increased by 68% to RO3.2mn in 2008 as against RO1.91mn in 2007. This other income portion has over the years added significant amount to the bottom line.

• OCC reported profit before tax of RO14.1mn in 2008 which was subject to 12% income tax resulting in a profit after tax of RO12.5mn as compared to RO17.6mn in 2007. In 2008, the company managed to report net margins of 19.74% as against 35.3% in 2007.

• In terms of quarterly performance of 2008, 1Q-2008 was the most favorable quarter as the company report profit after tax of RO3.9mn and net margins of 34%. Although in the last quarter the company report highest ever revenue but was not able to full transfer it to the bottom line as the net margins were merely 9% in 4Q-2008.

• OCC’s assets declined marginally to RO133mn in 2008 as compared to RO134.3mn in 2007. The major reason for the fall in assets in 2008 was because of decline in the investment available for sale. Investment available for sale dropped to RO15.2mn as compared to RO21.0mn in 2007.

• OCC announced an expansion of 1.2mn tons in clinker capacity for which a contract has been signed. The duration for construction and erection of the project is 25 months as per the contract and the project is expected to be completed in December 2009- 1st Quarter

Global Research - Oman Global Investment House

� Oman Cement Company

of 2010. In order to finance the project, OCC will be partly utilizing loan funds. The total contract value for the Expansion Project is RO62.7mn (US$162mn) and RO20mn of the project cost is to be met from loans.

• Sohar Praton Concrete Products Company SAOC, a 58.4% subsidiary of OCC went into liquidation and consequently, the parent company’s control of the subsidiary passed to the liquidator. Accordingly, the subsidiary is deconsolidated with effect from 12 March 2008. On the other hand, Oman Mondi Shuaiba Packaging (OMSP) reported an improved performance during the year 2008. Revenue earned by OMSP increased from RO3.5mn to RO6.5mn in 2008.

• As per MEED, over US$105bn worth of projects have been announced by Oman. Keeping in view the liquidity crunch and the cash constraints, even if we discount the projects by more than a half, still there would be ample demand which would be catering to sales growth of the cement companies in Oman. According to OCC, the expected demand for cement in Oman is estimated at 4.63mtpa during 2009.

• The value of OCC’s shares derived from the weighted average of the DCF and relative valuation methods is RO0.676 per share. The stock closed at RO0.372 on the Muscat Securities Market at the end of trading on 13th April 2009, which implies that the weighted average value of OCC’s shares is at a premium of 82% to the share’s current market price. At their current price, OCC’s shares have a P/E multiple of 10.6x and 7.2x for 2009 and 2010 respectively. We therefore reiterate our BUY recommendation on the scrip.

Table 01: Investment Indicators CMP (13th April 2009) Shares in Issue (mn) M-Cap (RO mn) 52-Week Hi/Lo (RO)

RO0.372 330.9 123.1 1.025 / 0.232

Year

Gross Profit

(RO mn)

Net Profit

(RO mn)

EPS

(RO)

BVPS

(RO)

ROAE

(%)

P/E

(x)

P/BV

(x) 2010 F 19.8 17.0 0.05 0.36 14.79 7.2 1.0 2009 F 13.4 11.6 0.04 0.34 10.42 10.6 1.1 2008 A 13.9 12.5 0.04 0.33 11.32 7.9 0.9 2007 A 20.5 17.6 0.05 0.33 17.07 12.5 2.0

Source : Company’s Annual Reports, Reuters & ’Global’ Research.Historical P/E & P/BV multiples based on respective year-end prices, while those for future years are based on current market price in the Muscat Securities Market as on April 13, 2009.

Chart 01: Share Price Performance Chart

Source: Zawya

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

13-A

pr-0

8

13-M

ay-0

8

13-J

un-0

8

13-J

ul-0

8

13-A

ug-0

8

13-S

ep-0

8

13-O

ct-0

8

13-N

ov-0

8

13-D

ec-0

8

13-J

an-0

9

13-F

eb-0

9

13-M

ar-0

9

13-A

pr-0

9

0.00

0.20

0.40

0.60

0.80

1.00

1.20

(RO

)

Index - LHS OCC - RHS

Global Research - Oman Global Investment House

Oman Cement Company �

Oman Cement Sector

The cement industry in Oman dates back to 1977, when Oman Cement Company (OCC) was set up, followed by Raysut Cement Company (RCC), which started in 1981. OCC is situated in the Muscat Governorate in Northern Oman, while RCC’s plant is located in the Dhofar Governorate in Southern Oman. Most of the consumption is concentrated in the northern part of the country as the southern part is less developed and demand for cement is lower. As a consequence of that RCC has established a cement receiving facility at Port Sultan Qaboos in Muscat with a capacity of 15,000 tons cement to cater to the Northern part of the Country. RCC being present in the southern part of the country serves the deficit markets of Yemen and East Africa for which it has established cement receiving facilities at the Ports of Mukalla and Aden.

In Oman, construction activity has been in heightened mode since 2003, with cement demand surpassing supply, resulting in cement shortages and price hikes. Consequently, the Omani government decided to impose a ban on cement exports in mid 2004, a move that forced local producers to focus on opportunities at home. Since then the country’s cement deficit declined as the demand supply gap reversed into surplus. In nominal terms Oman’s building and construction sector value has increased from RO159mn in 2000 to RO762mn at the end of 2007, growing at a CAGR of 25%. Which is further expected to rise to RO838mn in 2008. The building and construction sector contribution to the nominal GDP of the country is 4.8% as of 2007 which is expected to touch 5% at the end of 2008. Oman ranks below in terms of country’s building and construction sector contribution to the GDP when compared with its regional players. UAE ranks at the top at 8% followed by Qatar and Bahrain at 5.7% and 5% respectively.

Chart 02: Building & Construction Sector (BCS) as % GDP

Source: Ministry of National Economy, Oman

On the other hand in real terms, country building and construction material sector contribution to the GDP has increased from 2.1% in 2000 to 6.7% in 2007. The difference between the nominal and real terms is because of the decline in the oil production from 299mn barrels in 2003 to 259mn barrels in 2007. Nevertheless in the same period nominal GDP continued to increase as the oil price surged from US$27.8/barrel in 2003 to US$65.2/barrel in 2007. Going forward we believe that building and construction material contribution to GDP will continue to increased (1) ongoing construction and expansion activities in the real estate and construction sector and (2) decline in the oil production in the country because of depleting reserves.

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008BCS as % of Nominal GDP BCS as % of Real GDP

The increasing difference is because of lower production of oil as

compared to BCS sector.

Global Research - Oman Global Investment House

� Oman Cement Company

Oman’s Cement Capacity Enhancements to Continue

Over the years with the increasing oil prices and higher budgetary revenues, the country continued to focus on the diversification and developmental activities which in turn required contribution from the cement sector as well for the construction activities. In view of that, both the cement companies has continued to increase their cement capacities which at the end of 2008 are 4.6mtpa as compared to 2.2mtpa in 2003.

Chart 03: Oman Cement Sector Capacity

Source: Oman & Raysut Cement

Oman Cement increased its capacity from 1.26mtpa in 2003 to 1.87mtpa in 2008. The heightened demand prompted OCC to announce a further expansion which will double its clinker capacity to 2.4mtpa. This expanded capacity would help in achieving high local market share and to reduce the company’s reliance on imported clinker which incurs lots of cost and reduces the margins. OCC is planning to bring the additional capacity on-stream in 2010.

On the other hand Raysut Cement also followed the footsteps of Oman Cement. It increased its cement capacity from 0.98mtpa in 2003 to 2.75mtpa in 2008. In the meanwhile it has surpassed the capacity of OCC, but with the expansion of OCC both would be able to produce almost equal amounts of cement.

Cement capacity of Oman has continued and have tracked the pace of capacity enhancements in the region. Overall in GCC, the cement capacity is expected to increase from 43mtpa in 2003 to 85.9mtpa and 116.3mtpa in 2008 and 2012 respectively. Hence, Oman’s contribution to the overall cement capacity of GCC is to decline from the current levels of 5.4% in 2008 to 4.6% in 2012.

Demand Supply Scenario

Country’s demand and supply situation has in 2008 almost broke even as the total supply of cement was 4.12mn tons while consumption in the country rose from 3.07mn tons to 4.06mn tons. Cement demand in the country is driven by:

• Tourism: In 2006, tourism accounted for 0.75% of the GDP with a value of RO103mn, but the government hopes this figure can be increased to 1.4%of GDP in 2010 and 3% by 2020. Hence more of the focus would be on developing the infrastructure which in turn would result in favorable situation for the cement industry. Many tourism related projects are expected to come online in the coming 3-4 years.

2.2 2.2 2.2 3.2 4.2 4.6 4.6 5.4 5.4 5.4

42.9 47.7 53.058.8

68.7

85.9

107.4 112.9 116.3

91.2

-

20

40

60

80

100

120

140

2003 2004 2005 2006 2007 2008 2009F 2010F 2011F 2012F

(mn

Tons

)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Oman Capacity GCC Capacity Oman as % of GCC

Global Research - Oman Global Investment House

Oman Cement Company �

Table 02: Tourism Projects in Oman Project Name Value (US$mn) Project End

Majan Gulf Properties - Khasab Resort 780 Q1 2012

Yenkit Tourism Devp - Integrated Tourism Complex 2,000 Q4 2011

Muriya - Resorts 850 Q4 2012

Alfa - Journey of Light Beach Resort 950 Q2 2011

Ministry of Tourism - Seeb Complex 100 Q3 2009

Omran - Asian Beach Games Project 180 Q2 2010

Omran - Duqm Hotel 80 Q1 2010

Omran - Fort Hotel Resort 300 Q4 2010

Omran - Jabal Al Akhdar Resort Hotel 150 Q2 2011

Omran - Oman Convention and Exhibition Centre 400 Q2 2011

Omran - Ras Al Hamra Resort & Retreat 700 Q1 2011

Omran / Qatari Diar Real Estate Inv. Co - Ras Al-Hadd Resort 220 Q2 2012

Sama Dubai - Yiti Resort & Spa (Yiti) 1,400 Q4 2010

Swiss-Belhotel International / HBG Holdings Ltd 200 Q4 2010

The Wave Tourism Development 2,000 Q1 2015

World In / Bolici Group - Hayoot Beach Resort 350 Q4 2010

10,660

Source: MEED

The total cost of these tourism related projects only is worth US$11bn which when translated into cement demand would result in cement demand of 6.5mn tons in the four year period. Overall, the outlook for tourism sector is very bright in the coming years and the Sultanate is leaving no stones unturned to realize exponential growth in this sector.

• Foreign Freehold Ownership: Earlier, only GCC nationals were the only foreigners allowed to buy land in Oman which extend land ownership rights to GCC national and GCC corporate entities. However, the Royal decree 12/2006, expands foreign ownership rights to include non-GCC nationals as well.

• Real Estate Investments: Despite the upsurge in property prices till September 2008 the Omani market remained competitive in terms of prices as compared to other GCC countries. Omani land is cheaper than the other GCC countries. This gives the country an advantage in attracting investments from other prosperous GCC countries.

As per MEED, at the end of 2008 US$105bn worth of projects has been announced by Oman. On a conservative note even if 50% of the projects go as per schedule atleast US$52.5bn worth of projects would continue as per schedule.

Table 03: Oman Cement Demand Expectations

Overall Project Announcements in Oman (2008-2015) (US$mn) 105,000.0

Assumed Actual Implementation 50% 52,500.0

Expected Building & Construction Related Projects 40% 21,000.0

Cement Revenue as % of Build & Cons Sector in GCC 12% 2,520.0

Cement Price per Ton as of 2008 in Oman (US$/Ton) 81.5

Resulting Cement Demand (2008-2015) (mn Tons) 30.9

Annual Cement Demand (mn Tons) 4.4

Source: MEED & Global Research

Global Research - Oman Global Investment House

� Oman Cement Company

These projects include various civil, industrial, infrastructure, real estate and construction related projects. Hence of the total if we assume 40% are related to infrastructure, building and real estate related construction projects the total amount of the project would be US$21bn. In the past, cement sector revenues of the GCC have averaged around 12% of the total building and construction sector contribution in the nominal GDP. Hence by calculating the total value of cement in the coming 7 years till 2015, it reveals that Oman would have a minimum cement demand of atleast 4.4mn tons per annum.

Cement production of Oman has increased from 2.51mn tons in 2003 to 4.12mn tons in 2008. On the other hand cement sold by Omani companies in the country was 4.05mn tons in 2008, which means that the demand and supply situation is running neck to neck.

Chart 04: Oman Demand Supply Scenario (mn tons)

Source: Global Research

Going forward, with the economic slowdown and lower oil prices we expect Oman cement sector to continue this stiff competition between supply and demand and later on would turn in to a surplus as one of the cement players capacity is expected to come online in 2010.

Per Capita Cement Consumption in Oman

The cement consumption in Oman is directly linked to the scope of infrastructure developments undertaken by the government in recent years. Cement consumption and prices have therefore been highly sensitive to the volume of government-backed construction work in the Sultanate, as supply constraints on locally produced clinker has persisted throughout the past few years. Omani per capita cement consumption is relatively lower than its regional players. UAE takes the lead with per capita cement consumption of more than 3,800kg. Qatar ranks 2nd with per capita cement consumption of more than 2,200kg.

In 2006, per capita consumption of Oman surpassed 1000kg mark and is currently standing at 1,499kg at the end of 2008. Looking at the pace of development in the country and expected future demand, it is expected that per capita consumption would reach 1,662kg by 2012.

-

1.0

2.0

3.0

4.0

5.0

6.0

2005 2006 2007 2008 2009F 2010F 2011F-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Supply Demand Surplus / (Gap)

Global Research - Oman Global Investment House

Oman Cement Company �

Chart 05: Per Capita Cement Consumption & Growth per Capita

Source: Company Reports & Global Research

Majority of the export share has been taken up by Raysut Cement. Oman Cement exports has increased from mere 641ktons in 2003 to as high as 1.2mn tons in 2006 and back to 807ktons in 2008.

Local and Export Cement Prices

Cement prices in Oman continued to increase despite government intervention over the prices. Average realizations for both the companies rose during 2008. On an average (local and export price) cement prices for Oman rose from US$71.5/ton to US$81.5/ton. Local cement price on average rose from RO27.5/ton in 2007 to RO31.5/ton in 2008.

Chart 06: Local & Export Prices (RO/Ton)

Source: Company Reports & Global Research * Amount of export revenue not available before 2006 for OCC

RCC which exports majority of its produce realized higher local prices of RO33/ton as compared to that of OCC at 29.7/ton. On the other hand average export rose from RO30.5/ton in to RO34.5/ton in 2008. RCC which exports majority of its produce realized lower export prices of RO32.3/ton as compared to that of OCC at 36.5/ton.

Local and export cement prices has reported a CAGR of 6.8% and 7.3% respectively during 2003-08. Government has put certain restrictions on the selling prices of cement. However, the rising cost of inputs in the form of clinker and other important inputs such as services and manpower, may have adverse impact on the future performance of the cement industry in general and OCC in particular. Going forward in 2009 alone we expect the cement price to remain relatively lesser as compared to that of 2008 mainly because of economic slowdown. In the medium to long term we expect prices to recover 2010 onwards.

-

200

400

600

800

1,000

1,200

1,400

1,600

2003 2004 2005 2006 2007 2008-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Per Capita Cement Consumption Growth

10

16

22

28

34

40

2003 2004 2005 2006 2007 2008 2003 2004 2005 2006 2007 2008

OCC - Local Price RCC - Local PriceOCC - Export Price RCC - Export Price

Global Research - Oman Global Investment House

� Oman Cement Company

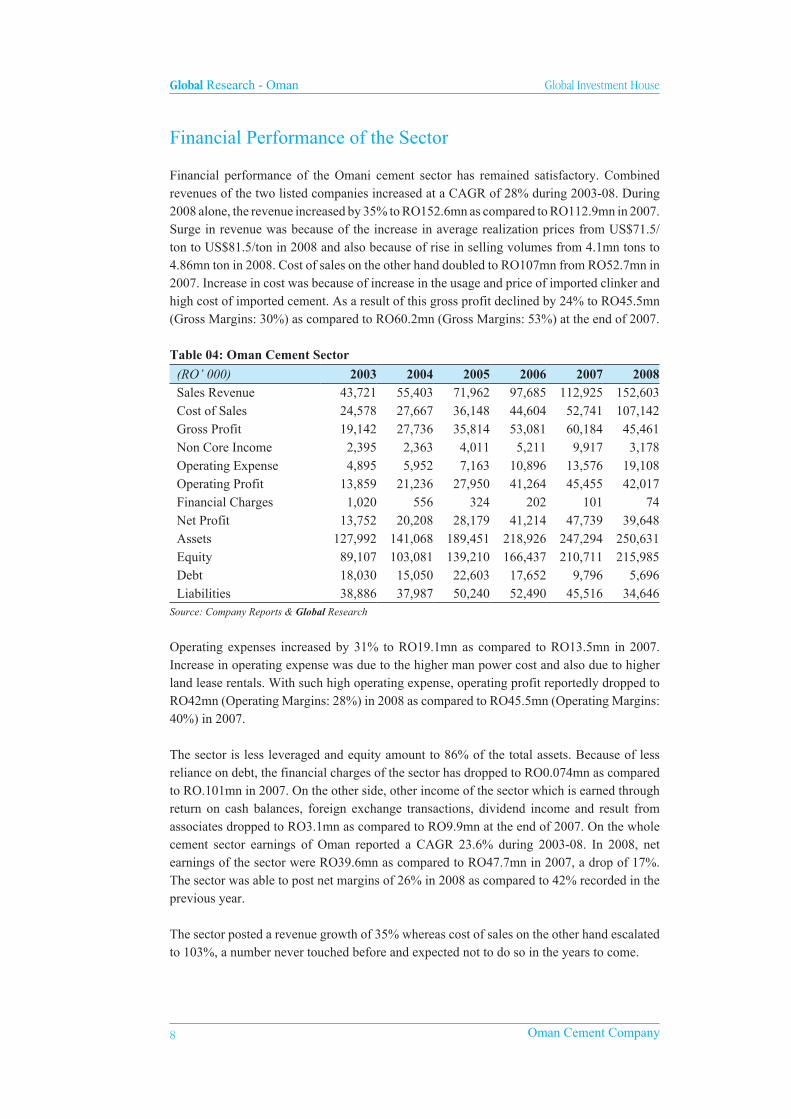

Financial Performance of the Sector

Financial performance of the Omani cement sector has remained satisfactory. Combined revenues of the two listed companies increased at a CAGR of 28% during 2003-08. During 2008 alone, the revenue increased by 35% to RO152.6mn as compared to RO112.9mn in 2007. Surge in revenue was because of the increase in average realization prices from US$71.5/ton to US$81.5/ton in 2008 and also because of rise in selling volumes from 4.1mn tons to 4.86mn ton in 2008. Cost of sales on the other hand doubled to RO107mn from RO52.7mn in 2007. Increase in cost was because of increase in the usage and price of imported clinker and high cost of imported cement. As a result of this gross profit declined by 24% to RO45.5mn (Gross Margins: 30%) as compared to RO60.2mn (Gross Margins: 53%) at the end of 2007.

Table 04: Oman Cement Sector

(RO’ 000) 2003 2004 2005 2006 2007 2008 Sales Revenue 43,721 55,403 71,962 97,685 112,925 152,603 Cost of Sales 24,578 27,667 36,148 44,604 52,741 107,142 Gross Profit 19,142 27,736 35,814 53,081 60,184 45,461 Non Core Income 2,395 2,363 4,011 5,211 9,917 3,178 Operating Expense 4,895 5,952 7,163 10,896 13,576 19,108 Operating Profit 13,859 21,236 27,950 41,264 45,455 42,017 Financial Charges 1,020 556 324 202 101 74 Net Profit 13,752 20,208 28,179 41,214 47,739 39,648 Assets 127,992 141,068 189,451 218,926 247,294 250,631 Equity 89,107 103,081 139,210 166,437 210,711 215,985 Debt 18,030 15,050 22,603 17,652 9,796 5,696 Liabilities 38,886 37,987 50,240 52,490 45,516 34,646

Source: Company Reports & Global Research

Operating expenses increased by 31% to RO19.1mn as compared to RO13.5mn in 2007. Increase in operating expense was due to the higher man power cost and also due to higher land lease rentals. With such high operating expense, operating profit reportedly dropped to RO42mn (Operating Margins: 28%) in 2008 as compared to RO45.5mn (Operating Margins: 40%) in 2007.

The sector is less leveraged and equity amount to 86% of the total assets. Because of less reliance on debt, the financial charges of the sector has dropped to RO0.074mn as compared to RO.101mn in 2007. On the other side, other income of the sector which is earned through return on cash balances, foreign exchange transactions, dividend income and result from associates dropped to RO3.1mn as compared to RO9.9mn at the end of 2007. On the whole cement sector earnings of Oman reported a CAGR 23.6% during 2003-08. In 2008, net earnings of the sector were RO39.6mn as compared to RO47.7mn in 2007, a drop of 17%. The sector was able to post net margins of 26% in 2008 as compared to 42% recorded in the previous year.

The sector posted a revenue growth of 35% whereas cost of sales on the other hand escalated to 103%, a number never touched before and expected not to do so in the years to come.

Global Research - Oman Global Investment House

Oman Cement Company �

Table 05: Oman Cement Sector Ratios2003 2004 2005 2006 2007 2008

Revenue Growth (%) N/A 27% 30% 36% 16% 35%

Cost Growth (%) N/A 13% 31% 23% 18% 103%

Asset Growth (%) N/A 10% 34% 16% 13% 1%

Gross Margins (%) 44% 50% 50% 54% 53% 30%

Non Core Income as % of PAT 17% 12% 14% 13% 21% 8%

Operating Margins (%) 32% 38% 39% 42% 40% 28%

Net Margins (%) 31% 36% 39% 42% 42% 26%

Debt as % of Assets (%) 14% 11% 12% 8% 4% 2%

Liabilities as % of Assets (%) 30% 27% 27% 24% 18% 14%

Equity as % of Assets (%) 70% 73% 73% 76% 85% 86%

Return on Equity (%) 15% 20% 20% 25% 23% 18%

Return on Assets (%) 11% 14% 15% 19% 19% 16%

Source: Company Reports & Global Research

Other income earned by the sector contributed 8% to the overall profits of the sector in 2008 as compared to 21% in 2007. Drop in the contribution was because of lesser amounts earned through investment portfolio and share of profit from associates. With assets and equity of RO250.5mn and RO216mn, the sector with net income of RO39.6mn was able to give return on assets and return on equity of 16% and 18% respectively.

Table 06: Oman Cement Sector Statistics2003 2004 2005 2006 2007 2008

Cement Produced in Oman (000 Tons) 2,515 2,621 2,686 3,609 3,875 4,121

Cement Sold in Oman (000 Tons) 1,889 1,847 2,173 2,589 3,072 4,057

Cement Exports from Oman (000 Tons) 641 824 821 1,210 1,032 807

Price per Ton in Oman (US$) 44.9 53.9 62.4 66.8 71.5 81.5

Cost per Ton in Oman (US$) 25.2 26.9 31.4 30.5 33.4 57.2

EV/Ton (US$) 169.5 249.9 468.8 356.9 373.6 169.8

Per Capita Cement Consumption (Kg) 807 765 866 1,005 1,157 1,499

Source: Company Reports & Industry Sources

Enterprise value per ton of the companies rose at a CAGR of 21.8% during 2003-07. However with the decline in the equity markets, the enterprise values declined for both the companies by over 50%. Enterprise value per ton of Oman Cement dropped to US$133 in 2008 as compared to US$305 in 2007. While the same for Raysut Cement dropped to US$207 in 2008 as compared to US$442 in 2007.

Global Research - Oman Global Investment House

10 Oman Cement Company

Oman Cement Sector in Charts

Source: Company Reports & Global Research

25%

31%

37%

43%

49%

55%

61%

2003 2004 2005 2006 2007 2008

Gross Margins (%)

5%

9%

13%

17%

21%

25%

2003 2004 2005 2006 2007 2008

Non Core Income as % of PAT

20%

25%

30%

35%

40%

45%

2003 2004 2005 2006 2007 2008

Operating Margins (%)

20%

25%

30%

35%

40%

45%

2003 2004 2005 2006 2007 2008

Net Margins (%)

0%

1%

2%

3%

4%

5%

6%

2003 2004 2005 2006 2007 2008

Financial Charges as % of Loan

0%

3%

6%

9%

12%

15%

2003 2004 2005 2006 2007 2008

Debt as % of Assets

-

100

200

300

400

500

2003 2004 2005 2006 2007 2008

EV/Ton (US$)

66%

70%

74%

78%

82%

86%

90%

2003 2004 2005 2006 2007 2008

Equity as % of Assets

15%

17%

19%

21%

23%

25%

2003 2004 2005 2006 2007 2008

Return on Equity (%)

10%

12%

14%

16%

18%

20%

2003 2004 2005 2006 2007 2008

Return on Assets (%)

Global Research - Oman Global Investment House

Oman Cement Company 11

Sector Outlook

Oman’s 2008 budget surplus soared to RO1.58bn (US$4.1bn) in 2008 compared to RO40.2mn a year earlier as the country’s oil revenues jumped up on record-high oil prices. Total state 2008 revenues stood at RO7.9bn compared to RO5.9bn a year earlier while expenditure rose to RO6.4bn in 2008 compared to RO5.9bn a year earlier, according to Ministry of National Economy. Such high revenues would give room to the country for further development and project announcements.

Domestic cement demand is expected to remain robust during 2009, fuelled in large part by planned investments in major infrastructure projects, integrated tourism and residential complexes, and general housing growth. The project line-up included the six domestic airports at Sohar, Ras al Hadd, Duqm, Shaleem, Adam and Haima; port developments at Sohar and Duqm; the tourism and residential developments in Ras al Hadd, Sifah, Yiti and Taqah; and the Batinah coastal road rehabilitation program. In fact, up to 10% of the estimated RO800mn in allocations towards infrastructure projects, announced by the government in its 2009 budget, would go towards cement purchases alone.

Significant cement demand will also be generated when many Omanis, keen to have their own homes, embark on the development of their government-allotted residential plots. Around 196,000 plots were distributed during the 2003-2007 period, against which only around 37,000 building permits have been issued so far. This leaves some 160,000 plots awaiting potential development, not counting the scores of allotments that authorities have began to make to a broader segment of Omani women.

Nevertheless, supply would outstrip demand and would create a surplus situation which would put pressure on the cement companies in the country. This surplus would increase the cement players reliance on exports which would be flooded with excess capacity from Pakistan, India and Saudi Arabia. India and Pakistan have relatively lesser room for cutting their prices which in turn can be taken up Omani companies as their gross margins are higher than those of Pakistani and Indian cement companies. Along with that, after the clinker expansion are carried out the cost would give more room for the Omani companies to breach the export market share of other cement companies.

Global Research - Oman Global Investment House

1� Oman Cement Company

Oman Cement Company

Revenue to Grow Post Expansion

In 2008, the revenue increased to RO63.5mn as compared to RO49.9mn at the end of 2007. Such a growth was possible because of higher production and sales volume as well as better realization prices.

The clinker produced during the year 2008 was 1.18mn tons as against 1.15mn tons produced during the corresponding period of 2007. This represents 98.5% (2007-96.17%) capacity utilization. While the cement produced during the year 2008 was 2.003mn tons which is 7.4% higher than 1.87mn tons produced during the previous year 2007. During the year 264,728ktons of cement was procured as per the instructions of Ministry of Commerce & Industry to meet the local market demand.

OCC sales volume increased by 14.6% to 2.1mn tons as compared to 1.87mn tons in 2007. Out of the total 2.1mn, local sales volume were 2.07mn tons whereas the exports were down from previous levels of 2007 at 91,251tons to 81,285tons. On the other hand local sales price increased by 12.2% to RO29.7/ton whereas the export price increased by 11.6% to RO36.5/ton.

Chart 07: Sales Revenue

Source: Company Reports & Global Research

In 2009, we expect the economic slowdown locally as well as regionally to impact the company which will result in lower sales revenue for the year. We expect a nominal drop in volumes with a 2-3% drop in the local as well as export price. Going forward, we expect OCC to report a CAGR growth of 7.2% during 2008-12. After 2009, we expect the things to come back on track and expect an increase in volume as well as price mainly because of expected economic recovery globally as well as regionally and initiation of delayed and halted projects. Along with that the company would have higher clinker and cement capacity which would enable it to roll out more volumes of cement.

Cost Pressure to Ease

Cost of the sales increased at a CAGR of 25.3% during 2003-08. In 2008, cost of sales increased by 69% to RO49.65mn. The increase in cost was due to high purchase cost of cement and clinker imported under instructions from the government in order to meet the local demand. The company imported 0.92mn tons of clinker during the year to meet the

-10.0

20.030.040.0

50.060.070.0

80.090.0

2003 2004 2005 2006 2007 2008 2009 (F) 2010 (F) 2011 (F) 2012 (F)-5%

0%

5%

10%

15%

20%

25%

30%

35%

Revenue (RO mn) Growth

Global Research - Oman Global Investment House

Oman Cement Company 1�

demand, which is 42% higher as against 0.53mn tons during the previous year. On the other hand in 2008 the company also imported 174k tons of cement to meet the shortfall locally.

Chart 08: Gross Profit & Margins

Source: Company Reports & Global Research

In 2009, we expect the company would follow the same trend and would continue to import significant amount of clinker at 0.6mn tons and 0.15mn tons of cement to meet their local requirements. Later on we expect the company cost pressure to ease off and anticipate it to increase at a CAGR of 5.4% during 2008-12. Lesser growth in the cost would be due to availability of new clinker capacity which would halt the import of high cost clinker.

As a result of availability of additional clinker capacity after 2009 we expect the company’s gross profit to increase at a CAGR of 12.9% during 2008-12 as compared to a CAGR growth of 5.8% during 2003-08. OCC enjoyed higher gross margins during 2003-07 averaging around 43%. Such margins would be harder to achieve in the coming years as the but nevertheless OCC’s margins would be significantly better than what were reported in 2008.

Loans & Financial Charges

In 2008, OCC financial charges increased to RO66.5k as compared to RO23.0k in 2007. While the loan balance declined to RO0.9mn in 2008 from RO2.2mn recorded in the previous year. With the announcement of the expansion by OCC and the need of financing the Company will be partly utilizing loan funds. The total contract value for the Expansion Project is RO62.7mn (US$162mn) out of which RO20mn of the project cost is to be met from loans.

Chart 09: Loans & Financial Charges (RO mn)

Source: Company Reports & Global Research

-

5.0

10.0

15.0

20.0

25.0

2003 2004 2005 2006 2007 2008 2009 (F) 2010 (F) 2011 (F) 2012 (F)18.0%

23.0%

28.0%

33.0%

38.0%

43.0%

48.0%

53.0%

Gross Profit (RO mn) Gross Margins

-

0.1

0.1

0.2

0.2

0.3

0.3

2003 2004 2005 2006 2007 2008 2009 (F) 2010 (F) 2011 (F) 2012 (F)0.18

1.18

2.18

3.18

4.18

5.18

6.18

7.18

Loans - RHS Financial Charges - LHS

Global Research - Oman Global Investment House

1� Oman Cement Company

Previously the company has acquired three loan facilities of which the first one from Government of the Sultanate of Oman is interest free and amounts to RO0.9mn. The loan is secured by a first mortgage over the assets of the parent company and the assignment of the insurance policy over plant and machinery as a first beneficiary and is being repaid in annual installments of RO 300,000 which commenced in December 2002.

Non-Core Income

In 2008, OCC non-core income increased by 68% to RO3.2mn as against RO1.91mn in 2007. This non-core income portion has over the years added significant amount to the bottom line. In 2008, non-core income as percentage of profit after tax was 26% as compared to 11% in 2007.

Chart 10: Non-Core Income

Source: Company Reports & Global Research

Going forward, we expect the non-core income portion to continue to cushion the bottom line of the Company and grow at a CAGR of 14.7% during 2008-12. OCC’s subsidiary Oman Mondi Shuaiba Packaging has also turned profitable in 2008 and would be adding good amounts to the total.

Net Profit

In 2008, OCC reported profit before tax of RO14.1mn which was subject to 12% income tax resulting in a profit after tax of RO12.5mn as compared to RO17.6mn in 2007. In 2008, the company managed to report net margins of 19.74% as against 35.3% recorded in the previous year. In terms of quarterly performance of 2008, 1Q-2008 was the most favorable quarter as the company report profit after tax of RO3.9mn and net margins of 34%. Although in the last quarter the company report highest ever revenue but was not able to full transfer it to the bottom line as the net margins were merely 9% in 4Q-2008.

-

1.00

2.00

3.00

4.00

5.00

6.00

2003 2004 2005 2006 2007 2008 2009 (F)2010 (F)2011 (F)2012 (F)5%

10%

15%

20%

25%

30%

Non-Core Income (RO mn) Non-Core Income as % of PAT

Global Research - Oman Global Investment House

Oman Cement Company 1�

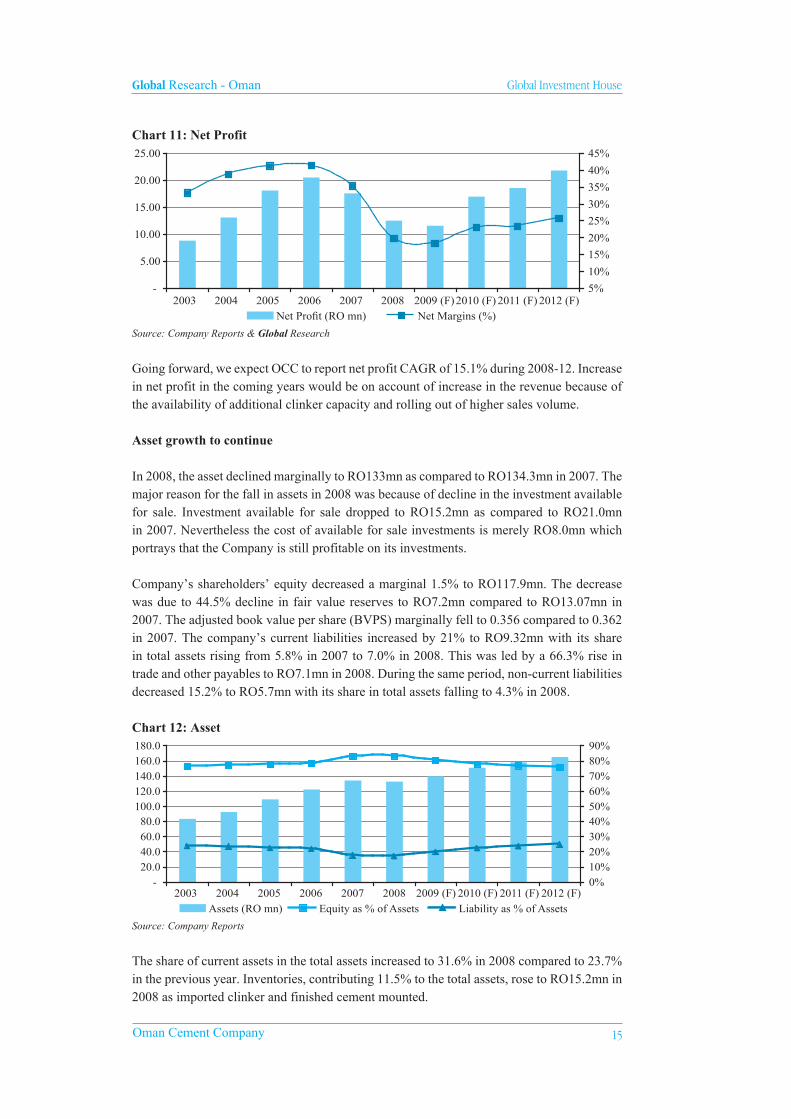

Chart 11: Net Profit

Source: Company Reports & Global Research

Going forward, we expect OCC to report net profit CAGR of 15.1% during 2008-12. Increase in net profit in the coming years would be on account of increase in the revenue because of the availability of additional clinker capacity and rolling out of higher sales volume.

Asset growth to continue

In 2008, the asset declined marginally to RO133mn as compared to RO134.3mn in 2007. The major reason for the fall in assets in 2008 was because of decline in the investment available for sale. Investment available for sale dropped to RO15.2mn as compared to RO21.0mn in 2007. Nevertheless the cost of available for sale investments is merely RO8.0mn which portrays that the Company is still profitable on its investments.

Company’s shareholders’ equity decreased a marginal 1.5% to RO117.9mn. The decrease was due to 44.5% decline in fair value reserves to RO7.2mn compared to RO13.07mn in 2007. The adjusted book value per share (BVPS) marginally fell to 0.356 compared to 0.362 in 2007. The company’s current liabilities increased by 21% to RO9.32mn with its share in total assets rising from 5.8% in 2007 to 7.0% in 2008. This was led by a 66.3% rise in trade and other payables to RO7.1mn in 2008. During the same period, non-current liabilities decreased 15.2% to RO5.7mn with its share in total assets falling to 4.3% in 2008.

Chart 12: Asset

Source: Company Reports

The share of current assets in the total assets increased to 31.6% in 2008 compared to 23.7% in the previous year. Inventories, contributing 11.5% to the total assets, rose to RO15.2mn in 2008 as imported clinker and finished cement mounted.

-

5.00

10.00

15.00

20.00

25.00

2003 2004 2005 2006 2007 2008 2009 (F)2010 (F) 2011 (F) 2012 (F)5%

10%

15%

20%

25%

30%

35%

40%

45%

Net Profit (RO mn) Net Margins (%)

-20.040.060.080.0

100.0120.0140.0160.0180.0

2003 2004 2005 2006 2007 2008 2009 (F) 2010 (F) 2011 (F) 2012 (F)0%10%20%30%40%50%60%70%80%90%

Assets (RO mn) Equity as % of Assets Liability as % of Assets

Global Research - Oman Global Investment House

1� Oman Cement Company

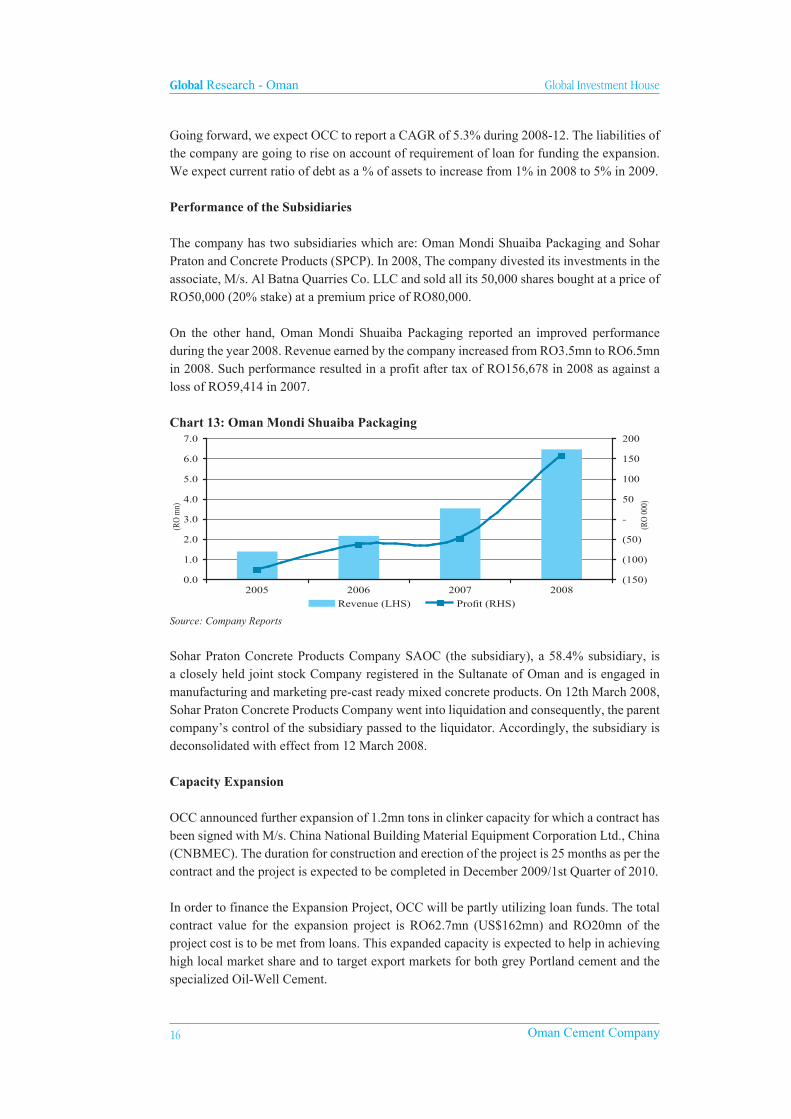

Going forward, we expect OCC to report a CAGR of 5.3% during 2008-12. The liabilities of the company are going to rise on account of requirement of loan for funding the expansion. We expect current ratio of debt as a % of assets to increase from 1% in 2008 to 5% in 2009.

Performance of the Subsidiaries

The company has two subsidiaries which are: Oman Mondi Shuaiba Packaging and Sohar Praton and Concrete Products (SPCP). In 2008, The company divested its investments in the associate, M/s. Al Batna Quarries Co. LLC and sold all its 50,000 shares bought at a price of RO50,000 (20% stake) at a premium price of RO80,000.

On the other hand, Oman Mondi Shuaiba Packaging reported an improved performance during the year 2008. Revenue earned by the company increased from RO3.5mn to RO6.5mn in 2008. Such performance resulted in a profit after tax of RO156,678 in 2008 as against a loss of RO59,414 in 2007.

Chart 13: Oman Mondi Shuaiba Packaging

Source: Company Reports

Sohar Praton Concrete Products Company SAOC (the subsidiary), a 58.4% subsidiary, is a closely held joint stock Company registered in the Sultanate of Oman and is engaged in manufacturing and marketing pre-cast ready mixed concrete products. On 12th March 2008, Sohar Praton Concrete Products Company went into liquidation and consequently, the parent company’s control of the subsidiary passed to the liquidator. Accordingly, the subsidiary is deconsolidated with effect from 12 March 2008.

Capacity Expansion

OCC announced further expansion of 1.2mn tons in clinker capacity for which a contract has been signed with M/s. China National Building Material Equipment Corporation Ltd., China (CNBMEC). The duration for construction and erection of the project is 25 months as per the contract and the project is expected to be completed in December 2009/1st Quarter of 2010.

In order to finance the Expansion Project, OCC will be partly utilizing loan funds. The total contract value for the expansion project is RO62.7mn (US$162mn) and RO20mn of the project cost is to be met from loans. This expanded capacity is expected to help in achieving high local market share and to target export markets for both grey Portland cement and the specialized Oil-Well Cement.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2005 2006 2007 2008

(RO

mn)

(150)

(100)

(50)

-

50

100

150

200

(RO

000

)

Revenue (LHS) Profit (RHS)

Global Research - Oman Global Investment House

Oman Cement Company 1�

Chart 14: Clinker Capacity Enhancement

Source: Company Reports

The company also signed contract for execution of civil works of the project for up gradation and modernization of Packing Plant has been signed with M/s. China National Building Material Equipment Corporation Ltd., China (CNBMEC) and the project is anticipated to be completed in the 2nd quarter of 2009.

-

0.5

1.0

1.5

2.0

2.5

3.0

1983 1998 2010

Global Research - Oman Global Investment House

1� Oman Cement Company

Chart Gallery - Oman Cement Company

Source: Company Reports

Gross Margins (%)

15%

20%

25%

30%

35%

40%

45%

2007 2008 2009F 2010F 2011F 2012F

EV/EBITDA (x)

0.0

2.0

4.0

6.0

8.0

10.0

2007 2008 2009F 2010F 2011F 2012F

Net Margins (%)

15%

20%

25%

30%

35%

40%

2007 2008 2009F 2010F 2011F 2012F

EV/Revenues (x)

0.00

1.00

2.00

3.00

4.00

5.00

2007 2008 2009F 2010F 2011F 2012F

Return on Average Assets (%)

6%

8%

10%

12%

14%

16%

2007 2008 2009F 2010F 2011F 2012F

Return on Average Equity (%)

10%

12%

14%

16%

18%

20%

2007 2008 2009F 2010F 2011F 2012F

Non Core Income as % of PAT (%)

10%

14%

18%

22%

26%

30%

2007 2008 2009F 2010F 2011F 2012F

P/Bv Ratio (x)

0.5

0.8

1.1

1.4

1.7

2.0

2007 2008 2009F 2010F 2011F 2012F

P/E Ratio (x)

4.0

6.0

8.0

10.0

12.0

14.0

2007 2008 2009F 2010F 2011F 2012F

Debt as % of Assets (%)

0%

1%

2%

3%

4%

5%

2007 2008 2009F 2010F 2011F 2012F

Global Research - Oman Global Investment House

Oman Cement Company 1�

Outlook

In 2008 OCC imported clinker and cement to meet local demand under directions of the government, a claim for reimbursement of shortfall in profits below a base level of RO16.1mn after tax will be made during 2009 with the government. OCC has also entered into discretionary portfolio management agreements with two companies appointing them as portfolio managers to handle part of its investments in shares which as of 2008 amount to RO19.5mn.

Chart 15: OCC’s - FCF (RO mn) & FCF to Sales (%)

Source : Company Reports & ’Global’ Research

The company expanded its share of the Oil Well Cement market in the MENA region in 2008 as more and more drilling companies preferred to standardize on the company’s products because of high quality and consistent performance in cementing operations of oil wells. Considering the market demand of new types of cement, OCC has planned to introduce three new products in the year 2009.

According to OCC, the expected demand for cement in Oman is estimated at 4.63mtpa during 2009. In order maintain its market share, OCC installed an additional cement mill of 3,000tpd and is in the process of further expansion by installing new production line of 4,000tpd clinker capacity to meet the competition. With the neck to neck demand supply situation the expansion would pave the way towards a profitable future.

(20.0)

(15.0)

(10.0)

(5.0)

-

5.0

10.0

15.0

20.0

25.0

2003 2004 2005 2006 2007 2008 2009 (F) 2010 (F) 2011 (F) 2012 (F)-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

FCF FCF/Sales

Global Research - Oman Global Investment House

�0 Oman Cement Company

Valuation & Recommendation

DCF Method

In order to compute the cost of equity for the Discounted Cash Flow (DCF) method, we have used the Capital Asset Pricing Model (CAPM).

The following assumptions have been made in order to arrive at the DCF value of Oman Cement Company.

• A risk-free rate of 4.50% has been assumed.

• A market risk premium of 6.0% has been assumed.

• The beta of the company was quite low when computed on the basis of monthly returns over 5 years to end-March 2009, hence we have taken beta of 1.

• The cost of equity derived from the above assumptions using the Capital Asset Pricing Model (CAPM) is 10.51%.

• The cost of debt taken is 6%.

• Based on the above assumptions, the Weighted Average Cost of Capital (WACC) works out to be 9.61%.

• Terminal growth rate of 3.0% has been assumed.

Based on our future earnings projections and the above assumptions for DCF computations, the DCF value of Oman Cement is RO0.769 per share.

Table 07: Oman Cement - Equity Valuation by DCF (RO mn) 2009 (F) 2010 (F) 2011 (F) 2012 (F)

Free Cash Flow (3.61) 8.53 14.46 16.04

Discounted Cash Flow (3.38) 7.28 11.27 11.40

Terminal Value 249.9

WACC 9.6%

Terminal Growth Rate 3.00%

Primary Value 26.6

Discounted Terminal Value 177.6

Value of Investments 46.5 (As at December 2008)

Cash 4.7 (As at December 2008)

Debt 0.9 (As at December 2008)

Equity Value 254.5

No. of Equity Shares Outstanding (mn) 330.9

Per Share Value (RO) 0.769

Source : Global Research

Global Research - Oman Global Investment House

Oman Cement Company �1

Sensitivity Analysis

A sensitivity analysis for different estimated long-run future growth rates and weighted cost of capital (and, thereby, the underlying betas) is shown in table below. The table provides estimated fair values for OCC’s shares based on a range of varying inputs. The shaded area at the center shows the most probable range of alternatives.

Table 08 : Oman Cement - Sensitivity Analysis Terminal Growth Rate

WACC

1.0% 2.0% 3.0% 4.0% 5.0%7.6% 0.801 0.908 1.062 1.300 1.722 8.6% 0.708 0.785 0.889 1.039 1.272 9.6% 0.636 0.694 0.769 0.871 1.017

10.6% 0.580 0.625 0.681 0.754 0.854 11.6% 0.535 0.570 0.613 0.668 0.740

Source: Global Research

Relative Valuation Method

The peer group valuation is performed to compare the intrinsic value of Oman Cement arrived at using the DCF calculation. In order to value Oman Cement using this method, we have used the weighted average price-to-earnings (P/E) multiple for the Oman cement industry, comprising Oman Cement Company and Raysut Cement Company. The price-earnings multiple of a stock is a reflection of various factors, such as the expected profitability of the company, its growth potential as perceived by the market, predictability and sustainability of its revenues, the quality of its earnings and the quality of its management, among others.

To arrive at the peer-set P/E multiple, we have computed the average industry P/E of the two listed cement companies in Oman, based on their current market prices and projected earnings for 2008. The weighted average P/E for the GCC cement industry, thus arrived at, is 8x.

On the basis of the weighted average P/E for the industry and Oman Cement’s projected 2008 earnings, the company’s stock valuation comes to RO0.303per share. However, as the price-earnings multiple varies with time and is dependent on several factors, such as market sentiment and other qualitative factors, we have provided a lower weightage of 20% to the peer valuation method, and 80% weightage to the value arrived at using the DCF method.

Valuations

The value of OCC’s shares derived from the weighted average of the DCF and relative valuation methods is RO0.676 per share. The stock closed at RO0.372 on the Muscat Securities Market at the end of trading on 13th April 2009, which implies that the weighted average value of OCC’s shares is at a premium of 82% to the share’s current market price.

Table 09 : Weighted Average Share Value of Oman Cement (RO) Weightage Fair Value As per DCF Method 80% 0.769 As per Relative Valuation 20% 0.303 Weighted Average Share Value 0.676

Source: Global Research

At their current price, OCC’s shares have a P/E multiple of 10.6x and 7.2x for 2009 and 2010 respectively. We therefore reiterate our BUY recommendation on the scrip.

Global Research - Oman Global Investment House

�� Oman Cement Company

BA

LA

NC

E S

HE

ET

Om

an C

emen

t C

ompa

ny (

RO

) 20

0620

0720

0820

09 (

F)

2010

(F

)20

11 (

F)

2012

(F

) C

ash

& C

ash

Equ

ival

ents

1

,062

,128

2

,214

,961

4

,609

,866

4

,254

,620

5

,840

,876

6

,246

,713

6

,747

,207

B

ank

Bal

ance

s 7

7,57

9 7

7,57

9 1

01,1

73

101

,173

1

01,1

73

101

,173

1

01,1

73

Tra

de R

ecei

vabl

es

4,9

38,4

47

4,7

69,3

08

5,5

68,3

67

5,1

97,2

90

6,5

11,5

01

7,6

39,4

88

9,2

69,9

55

Oth

er R

ecei

vabl

es

1,6

81,0

87

1,3

11,8

76

1,5

41,0

38

1,7

32,4

30

2,0

34,8

44

2,4

00,9

82

3,2

44,4

84

Inv

ento

ries

5

,159

,343

4

,327

,600

1

5,24

3,49

8 1

3,64

3,83

6 1

1,93

8,05

3 1

4,32

7,32

5 1

6,77

7,50

5 S

hort

-ter

m D

epos

its

6,6

20,0

00

18,

085,

650

14,

570,

000

13,

113,

000

11,

801,

700

12,

745,

836

13,

765,

503

Hel

d to

Mat

urity

Inv

estm

ents

1

,131

,965

1

,050

,000

4

22,7

84

380

,506

4

18,5

56

460

,412

5

06,4

53

Tot

al C

urre

nt A

sset

s 2

0,67

0,54

9 3

1,83

6,97

4 4

2,05

6,72

6 3

8,42

2,85

5 3

8,64

6,70

4 43

,921

,929

50

,412

,281

H

eld

to M

atur

ity I

nves

tmen

ts

4,6

54,9

36

3,6

07,8

19

3,1

90,4

94

2,8

71,4

45

3,1

58,5

89

3,4

74,4

48

3,8

21,8

93

Lon

g-te

rm D

epos

its

34,

199,

661

19,

045,

080

12,

390,

075

11,

151,

068

12,

266,

174

13,

492,

792

14,

842,

071

Em

ploy

ee L

oans

5

4,01

2 1

3,46

4,54

3 -

-

-

-

-

I

nves

tmen

ts in

Ass

ocia

tes

283

,953

6

11,0

65

621

,272

6

52,3

36

717

,569

7

89,3

26

868

,259

I

nves

tmen

ts A

vaila

ble-

for-

Sale

1

3,43

4,08

9 2

1,06

6,19

2 1

5,28

6,51

4 1

3,75

7,86

3 1

5,13

3,64

9 1

6,64

7,01

4 1

8,31

1,71

5 G

ross

Fix

ed A

asse

ts

106

,606

,515

1

05,7

17,9

80

123

,942

,149

1

41,9

47,1

49

154

,947

,149

1

58,9

47,1

49

161

,947

,149

L

ess:

Acc

umul

ated

Dep

reci

atio

n 5

7,57

3,78

8 6

1,08

4,96

9 6

4,51

2,24

6 6

8,85

0,22

1 7

3,81

8,37

1 7

9,24

1,52

2 8

4,80

4,67

2 N

et F

ixed

Ass

ets

49,

032,

727

44,

633,

011

59,

429,

903

73,

096,

928

81,

128,

778

79,7

05,6

27

77,1

42,4

77

Tot

al A

sset

s 1

22,3

29,9

27

134

,264

,684

1

32,9

87,0

25

139

,952

,493

1

51,0

51,4

63

158,

031,

136

165,

398,

696

Lia

bilit

ies

Sho

rt-t

erm

Loa

n 4

77,4

29

698

,372

3

00,0

00

3,8

00,0

00

3,4

20,0

00

3,0

78,0

00

2,7

70,2

00

Ban

k B

orro

win

gs

77,

579

135

,330

-

-

-

-

-

T

rade

Pay

able

1

,836

,064

1

,776

,584

2

,592

,012

2

,728

,767

2

,984

,513

3

,183

,850

3

,355

,501

O

ther

Pay

able

s 1

,990

,150

2

,506

,350

4

,531

,318

4

,775

,342

5

,222

,898

5

,571

,738

5

,872

,127

P

rovi

sion

for

Tax

atio

n 3

,092

,798

2

,617

,511

1

,896

,380

1

,706

,742

1

,536

,068

1

,382

,461

1

,244

,215

T

otal

Cur

rent

Lia

bilit

ies

7,4

74,0

20

7,7

34,1

47

9,3

19,7

10

13,

010,

852

13,

163,

479

13,

216,

049

13,

242,

043

Def

erre

d T

axat

ion

4,3

95,2

96

4,2

02,6

84

3,8

73,7

40

2,3

51,1

69

3,4

47,6

78

3,7

68,5

03

4,4

26,5

35

Med

ium

-Ter

m L

oan

2,0

43,3

12

1,5

22,3

69

600

,000

2

,600

,000

2

,340

,000

2

,083

,735

1

,827

,470

E

mpl

oyee

Ind

emni

ty P

rovi

sion

8

78,2

86

1,0

40,4

94

1,2

62,3

27

1,3

12,8

20

1,4

04,7

17

1,5

03,0

48

1,6

08,2

61

Pro

pose

d D

ivid

end

1

1,58

0,54

5 8

,933

,563

7

,279

,200

8

,271

,818

1

3,23

4,90

8 1

6,54

3,63

6 1

9,85

2,36

3 P

aid-

up C

apita

l 3

3,08

7,27

1 3

3,08

7,27

1 3

3,08

7,27

1 3

3,08

7,27

1 3

3,08

7,27

1 3

3,08

7,27

1 3

3,08

7,27

1 S

hare

Pre

miu

m

6,7

24,1

45

6,7

24,1

45

6,7

24,1

45

6,7

24,1

45

6,7

24,1

45

6,7

24,1

45

6,7

24,1

45

Sta

tuto

ry R

eser

ve

11,

029,

090

11,

029,

090

11,

029,

090

11,

029,

090

11,

029,

090

11,

029,

090

11,

029,

090

Vol

unta

ry R

eser

ve

13,

633,

203

15,

434,

896

16,

543,

635

17,

705,

592

19,

406,

565

21,

265,

609

23,

449,

257

Fai

r V

alue

Res

erve

6

,528

,991

1

3,06

5,09

9 7

,250

,172

5

,721

,521

7

,097

,307

8

,610

,672

1

0,27

5,37

3 R

etai

ned

Ear

ning

s 2

4,55

3,58

0 3

1,43

7,04

6 3

5,98

5,91

5 3

8,17

1,70

7 4

0,24

5,56

0 4

0,43

3,31

9 4

0,23

3,78

8 R

eval

uatio

n Su

rplu

s 5

3,88

0 5

3,88

0 3

1,82

0 3

1,82

0 3

1,82

0 3

1,82

0 3

1,82

0 T

otal

Sha

reho

lder

’s E

quity

9

5,61

0,15

9 1

10,8

31,4

27

110

,652

,048

1

12,4

71,1

46

117

,621

,758

12

1,18

1,92

5 12

4,83

0,74

4 T

otal

Lia

bilit

ies

& E

quit

y 1

22,3

29,9

27

134

,264

,684

1

32,9

87,0

25

139

,952

,493

1

51,0

51,4

63

158,

031,

136

165,

398,

696

Sour

ce:

Com

pany

Rep

orts

& G

loba

l Res

earc

h

Global Research - Oman Global Investment House

Oman Cement Company ��

INC

OM

E S

TA

TE

ME

NT

Om

an C

emen

t C

ompa

ny

(R

O)

2006

2007

2008

2009

(F

)20

10 (

F)

2011

(F

)20

12 (

F)

Sal

es R

even

ue

49,

710,

230

49,

911,

507

63,

522,

594

63,

233,

698

74,

271,

809

79,

668,

943

84,

588,

343

Cos

t of

Sale

s (

26,7

57,3

79)

(29

,460

,849

) (

49,6

52,6

65)

(49

,800

,000

) (

54,4

67,3

68)

(58

,105

,263

) (

61,2

37,8

95)

Gro

ss P

rofi

t 2

2,95

2,85

1 2

0,45

0,65

8 1

3,86

9,92

9 1

3,43

3,69

8 1

9,80

4,44

1 2

1,56

3,68

0 2

3,35

0,44

9

Gen

eral

& A

dmin

istr

ativ

e E

xpen

ses

(2,

020,

866)

(2,

638,

844)

(2,

898,

425)

(2,

845,

516)

(3,

342,

231)

(3,

585,

102)

(3,

806,

475)

Ope

rati

ng P

rofi

t 2

0,93

1,98

5 1

7,81

1,81

4 1

0,97

1,50

4 1

0,58

8,18

2 1

6,46

2,21

0 1

7,97

8,57

8 1

9,54

3,97

3

Fin

ance

Cha

rges

(

74,7

78)

(23

,022

) (

66,5

17)

(23

3,50

1) (

230,

251)

(26

2,09

8) (

263,

684)

Oth

er I

ncom

e

38,

067

189

,691

5

81,4

44

523

,300

5

86,0

96

644

,705

7

09,1

76

Int

eres

t Inc

ome

1,6

82,9

53

2,2

59,0

10

1,6

26,1

76

1,4

63,5

58

1,6

09,9

14

1,7

70,9

06

3,7

18,9

02

Div

iden

d In

com

e 6

24,4

06

694

,764

9

48,4

24

726

,109

7

22,2

88

794

,517

8

73,9

68

Sha

re o

f R

esul

t of

Ass

ocia

tes

(27

,782

) (

16,6

16)

47,

003

54,

053

62,

161

71,

486

82,

209

Im

pair

men

t Los

s in

an

Ass

ocia

te/A

sset

-

(

1,21

9,29

9) -

-

-

-

-

Pro

fit

Bef

ore

Tax

atio

n 2

3,17

4,85

1 1

9,69

6,34

2 1

4,10

8,03

4 1

3,12

1,70

2 1

9,21

2,41

8 2

0,99

8,09

3 2

4,66

4,54

4

Tax

atio

n (

2,74

2,76

3) (

2,42

5,92

8) (

1,56

7,43

5) (

1,56

7,44

6) (

2,29

8,45

2) (

2,51

2,33

6) (

2,95

1,02

3)

Min

ority

Int

eres

t 1

23,8

32

348

,309

-

6

5,31

0 9

5,76

9 1

04,6

81

122

,959

Net

Pro

fit

20,

555,

920

17,

618,

723

12,

540,

599

11,

619,

566

17,

009,

735

18,

590,

438

21,

836,

480

P&

L A

ppro

pria

tion

Acc

ount

:

Op

Bal

ance

of

Ret

aine

d E

arni

ngs

17,

633,

797

24,

553,

580

31,

437,

046

35,

985,

915

38,

171,

707

40,

245,

560

40,

433,

319

Adj

ustm

ents

-

-

3

96,2

09

-

-

-

-

Net

Pro

fit f

or th

e ye

ar

20,

555,

920

17,

618,

723

12,

540,

599

11,

619,

566

17,

009,

735

18,

590,

438

21,

836,

480

Tra

nsfe

r to

Vol

unta

ry R

eser

ve

2,0

55,5

92

1,8

01,6

93

1,1

08,7

39

1,1

61,9

57

1,7

00,9

73

1,8

59,0

44

2,1

83,6

48

Pro

pose

d D

ivid

end

1

1,58

0,54

5 8

,933

,563

7

,279

,200

8

,271

,818

1

3,23

4,90

8 1

6,54

3,63

6 1

9,85

2,36

3

Clo

sing

Bal

ance

of

Ret

aine

d E

arni

ngs

24,

553,

580

31,

437,

046

35,

985,

915

38,

171,

707

40,

245,

560

40,

433,

319

40,

233,

788

Sour

ce:

Com

pany

Rep

orts

& G

loba

l Res

earc

h

Global Research - Oman Global Investment House

�� Oman Cement Company

CA

SH F

LO

W S

TA

TE

ME

NT

Om

an C

emen

t C

ompa

ny (

RO

) 20

0620

0720

0820

09 (

F)

2010

(F

)20

11 (

F)

2012

(F

) O

pera

ting

O

pera

ting

Act

iviti

es

25,

280,

514

21,

959,

295

16,

380,

673

12,

220,

294

20,

735,

736

21,

799,

646

23,

490,

274

Net

Pro

fit

20,

555,

920

17,

618,

723

12,

540,

599

11,

619,

566

17,

009,

735

18,

590,

438

21,

836,

480

Def

erre

d T

ax L

iabi

lity

2,7

42,7

63

2,4

25,9

28

-

(1,

522,

571)

1,0

96,5

10

320

,825

6

58,0

31

Tax

Pai

d -

-

1

,567

,435

(

189,

638)

(17

0,67

4) (

153,

607)

(13

8,24

6) D

epre

ciat

ion

3,6

89,0

29

3,8

62,7

87

3,9

50,0

36

4,3

37,9

75

4,9

68,1

50

5,4

23,1

50

5,5

63,1

50

Im

pair

men

t of

Ass

ets

-

784

,506

-

-

-

-

-

I

nter

est I

ncom

e (

1,68

2,95

3) (

2,44

8,70

1) (

2,15

3,15

1) (

1,46

3,55

8) (

1,60

9,91

4) (

1,77

0,90

6) (

3,71

8,90

2) D

ivid

end

Inco

me

(62

4,40

6) (

694,

764)

(94

8,42

4) (

726,

109)

(72

2,28

8) (

794,

517)

(87

3,96

8) F

inan

ce C

harg

es

12,

271

80,

825

66,

517

233

,501

2

30,2

51

262

,098

2

63,6

84

Pro

pose

d R

emun

erat

ion

to D

irec

tors

1

10,0

00

-

-

-

-

-

-

Am

ortiz

atio

n of

Bon

d Pr

emiu

m

(2,

090)

(2,

884)

(5,

457)

-

-

-

-

Oth

er A

mor

tizat

ions

-

2

70,8

19

-

-

-

-

-

Sha

re o

f R

esul

ts o

f A

ssoc

iate

Cos

. 2

7,78

2 1

6,61

6 (

47,0

03)

(54

,053

) (

62,1

61)

(71

,486

) (

82,2

09)

Gai

n on

Sal

e of

Pro

pert

y, P

lant

and

Equ

ip

-

-

(3,

820)

-

-

-

-

Gai

n fr

om S

ale

of I

nves

tmen

ts

-

-

(50

,649

) -

-

-

-

P

rovi

sion

s fo

r St

ores

, etc

. 4

86,3

89

171

,574

1

,204

,551

-

-

-

-

M

inor

ity I

nter

est

(12

3,83

2) (

348,

309)

-

(65

,310

) (

95,7

69)

(10

4,68

1) (

122,

959)

Ind

emni

ty

89,

641

222

,175

2

60,0

39

50,

493

91,

897

98,

330

105

,213

W

orki

ng C

apita

l 5

37,1

22

1,3

86,8

46

(10

,149

,386

) 2

,160

,127

7

92,4

59

(3,

335,

220)

(4,

452,

110)

Dec

/(in

c.)

in R

ecei

vabl

es

640

,132

-

(

1,11

9,47

9) 1

79,6

85

(1,

616,

625)

(1,

494,

124)

(2,

473,

970)

Dec

/ (i

nc)

in I

nven

tori

es

658

,969

6

60,1

69

(12

,120

,449

) 1

,599

,662

1

,705

,782

(

2,38

9,27

2) (

2,45

0,18

0) I

nc/(

dec)

in A

ccou

nts

Paya

ble

(1,

153,

875)

456

,720

3

,114

,136

1

36,7

55

255

,746

1

99,3

37

171

,651

I

nc/(

dec)

Oth

er C

urre

nt L

iabi

litie

s 3

91,8

96

-

-

244

,024

4

47,5

56

348

,839

3

00,3

89

Inc

/(de

c) O

ther

Cur

rent

Ass

ets

-

269

,957

(

23,5

94)

-

-

-

-

Inc

ome

Tax

Pai

d (

2,74

5,84

5) (

3,09

3,82

7) (

2,61

7,51

1) -

-

-

-

F

inan

cial

Cha

rges

Pai

d (

88,0

00)

(80

,825

) (

66,5

17)

-

-

-

-

Em

ploy

ee B

enef

its P

aid

(67

,990

) (

59,9

67)

(32

,803

) -

-

-

-

T

otal

Ope

rati

ng

22,

915,

801

20,

111,

522

3,5

14,4

56

14,

380,

421

21,

528,

195

18,

464,

426

19,

038,

164

Inv

esti

ng

Cap

ex

(23

6,10

5) (

518,

396)

(19

,807

,857

) (

18,0

05,0

00)

(13

,000

,000

) (

4,00

0,00

0) (

3,00

0,00

0) A

dvan

ce f

or P

urch

ase

of P

PE

(7,

078,

035)

-

-

12,

041

-

-

-

Div

iden

d In

com

e 1

,405

,834

-

-

7

26,1

09

722

,288

7

94,5

17

873

,968

M

atur

ity o

f L

ong-

Ter

m L

oans

4

,664

,981

1

,131

,966

1

,050

,000

-

-

-

-

I

nter

est I

ncom

e -

2

,714

,280

2

,215

,150

1

,463

,558

1

,609

,914

1

,770

,906

3

,718

,902

D

ivid

end

Rec

eive

d 6

22,3

06

694

,764

9

48,4

24

-

-

-

-

Loa

ns

-

-

-

361

,328

(

325,

195)

(35

7,71

5) (

393,

486)

Rec

all o

f Sh

ort-

term

Dep

osits

1

7,19

6,50

0 -

-

-

-

-

-

L

ong-

term

Dep

osits

(

9,61

7,32

0) 3

,688

,931

1

0,17

0,65

5 1

,239

,008

(

1,11

5,10

7) (

1,22

6,61

7) (

1,34

9,27

9) P

roce

eds

from

Dis

posa

l of

Prop

erty

-

-

3

,820

-

-

-

-

S

hort

-ter

m D

epos

its

(20

,815

,000

) (

13,4

07,7

17)

13,

489,

140

1,4

57,0

00

1,3

11,3

00

(94

4,13

6) (

1,01

9,66

7) I

nves

tmen

ts in

Ass

ocia

tes/

Subs

idia

ries

(

115,

624)

(34

3,72

8) 8

0,00

0 2

2,99

0 (

3,07

2) (

271)

3,2

76

Inv

estm

ents

Ava

ilabl

e fo

r Sa

le

-

(1,

095,

995)

(35

,249

) -

-

-

-

I

POs

& R

ight

s Is

sue

Subs

crip

tions

(

523,

007)

-

-

-

-

-

-

Cap

ital R

educ

tion

in A

FS I

nves

tmen

ts

2,0

00

-

-

-

-

-

-

Tot

al I

nves

ting

(

14,4

93,4

70)

(7,

135,

895)

8,1

14,0

83

(12

,722

,966

) (

10,7

99,8

72)

(3,

963,

317)

(1,

166,

286)

Fin

anci

ng

Cas

h Fl

ow f

rom

Dis

cont

inue

d O

pera

tions

-

5

7,75

1 -

-

-

-

-

R

ight

s Is

sue

of S

hare

s 1

81,2

50

-

-

-

-

-

-

Div

iden

d (

8,27

1,81

8) (

11,5

80,5

45)

(8,

933,

563)

(7,

279,

200)

(8,

271,

818)

(13

,234

,908

) (

16,5

43,6

36)

Ter

m-l

oan

Rep

aym

ents

(

259,

550)

(30

0,00

0) (

300,

000)

5,5

00,0

00

(64

0,00

0) (

598,

265)

(56

4,06

5) F

inan

ce C

harg

es

(12

,271

) -

-

(

233,

501)

(23

0,25

1) (

262,

098)

(26

3,68

4) T

otal

Fin

anci

ng

(8,

362,

389)

(11

,822

,794

) (

9,23

3,56

3) (

2,01

2,70

0) (

9,14

2,06

8) (

14,0

95,2

71)

(17

,371

,384

) N

et C

hang

e in

Cas

h 5

9,94

2 1

,152

,833

2

,394

,975

(

355,

245)

1,5

86,2

55

405

,837

5

00,4

94

Net

Cas

h at

Beg

inni

ng

1,0

02,1

86

1,0

62,1

28

2,2

14,9

61

4,6

09,8

66

4,2

54,6

20

5,8

40,8

76

6,2

46,7

13

Dis

cont

inue

d O

pera

tions

-

-

(

71)

-

-

-

-

Net

Cas

h at

End

1

,062

,128

2

,214

,961

4

,609

,866

4

,254

,620

5

,840

,876

6

,246

,713

6

,747

,207

So

urce

: C

ompa

ny R

epor

ts &

Glo

bal R

esea

rch

Global Research - Oman Global Investment House

Oman Cement Company ��

FACT SHEETOman Cement Company

2006 2007 2008 2009 (F) 2010 (F) 2011 (F) 2012 (F)

Liquidity Ratios

Current Ratio (x) 2.8 4.1 4.5 3.0 2.9 3.3 3.8

Quick Ratio (x) 2.1 3.6 2.9 1.9 2.0 2.2 2.5

Inventory Stock (Days) 78 59 72 106 86 82 93

Receivables Outstanding (Days) 33 35 30 31 29 32 36

Length of Operating Cycle (Days) 111 94 102 137 114 115 129

Payables Outstanding (Days) 32 22 16 19 19 19 19

Length of Cash Cycle (Days) 78 72 86 117 95 96 110

Profitability Ratios

Total Asset Turnover (x) 0.4 0.4 0.5 0.5 0.5 0.5 0.5

Total Net Fixed Asset Turnover (x) 1.0 1.1 1.1 0.9 0.9 1.0 1.1

Equity Turnover (x) 0.6 0.5 0.6 0.6 0.6 0.7 0.7

Gross Profit Margin (%) 46.2 41.0 21.8 21.2 26.7 27.1 27.6

Operating Margin (%) 42.1 35.7 17.3 16.7 22.2 22.6 23.1

Net Profit Margin (%) 41.4 35.3 19.7 18.4 22.9 23.3 25.8