Languages

Pages

Legal

Welcome To

#oilgasict

Mark StephenBBC Scotland

Conference Chair

#oilgasict

Conference Apphttps://app.bizvento.com/oilgasict15

URL on all badges#oilgasict

Drinks ReceptionExhibition Room

Sponsored by

#oilgasict

Angus MurrayTAQA

@taqa

#oilgasict

The role of ICT as an enabler in a low oil price world

How did we all get here….

……and where is “here”

Chasing the barrels not the bucks

The law of supply and demand…

- Which direction of change reacts quickest?

Sustainable Business is key.

The Levers for Change…

• The Basics… more oil and/or lower cost

• How can IT help with these challenges

• Working with our supply chain

• Need to challenge the statics

• ‘Upgrade or Die!’

Opportunity or Threat?

Kotter’s model…

A driver for change… a common cause

Re-baseline to a sustainable industry.

Enabling Technologies

Collaboration

Consolidation…

Total Cost of Ownership is king…

- Bandwidth/Riverbed, Cloud vs infrastructure, MI, ERP..(sharpen the pencil and

get good business cases)

Management…

- Applications sprawl – homebrew vs ‘off the shelf’

- ‘Upgrade or Die’

- Business need/challenge

- Chasing the dollar not the barrel

- DO LESS BETTER

Answers ?

Global consolidation & collaboration

Change in business activity

Collaboration….

- Technology

- Supply Chain

- Peer companies

Give them the tools to manage the business

- Cost management, process reviews

Still spending a lot of money, its not going away, just need to rebaseline.

Conclusions…. The future?

Change can be our friend,

Do Less Better… ValueMax

Collaboration…

- offshore/suppliers/like minded companies

Get on the boat!

Richard Higgsbrightsolid@brightsolid

#oilgasict

Information Classification: Restricted 16

Richard Higgs, CEO brightsolid

Investing £5 million into the $50 barrel

17Information Classification: Restricted

Plan for the next 20 minutes

Our Mission, Values and strategy Connecting Aberdeen to the North Sea and beyond What we’ve seen in other sectors Our cloud philosophy Data driven decision making and collaboration Moving to the utility cloud

18Information Classification: Restricted

brightsolid today

Mission: Technical Innovation with Personal Service (TIPS)

The oil and gas virtual and regional systems integrator –providing a platform for collaboration

Globally connected data centre and cloud specialists

A values driven organisation

19Information Classification: Restricted

The £5 million investment generates ?

20Information Classification: Restricted

What are we building?

Uptime Accredited Tier III, Fault Tolerant power & cooling

200 rack positions Day 1. Total capacity 400 racks, 25kW max power density.

Power Efficiency of 1.2. (80% less than national average)

21Information Classification: Restricted

Communications

22Information Classification: Restricted

Our VisionExtends

Work place recovery suite

Project working space for the energy community

Digital and innovation resources for all organisations across Aberdeen

Innovation, digital hub

23Information Classification: Restricted

What is on our minds right now?

“Usually, we disrupt markets……..Aberdeen has been disrupted enough.”

24Information Classification: Restricted

Transformations

We helped the Scottish Government in their journey to secure shared resources, the cloud and operationally excellent IT

“The solution is now hosted in a private cloud for less than half the price that IS were currently paying”

The Improvement Service solution is hosted by brightsolid

The reason for starting the journey

25Information Classification: Restricted

Journey to the cloud

“Spending on cloud computing infrastructure and platforms is expected to grow at a 30% compound annual rate from 2013 through 2018 compared with 5% growth for the overall enterprise IT market” Source Goldman Sachs

Operational excellence in infrastructure

26Information Classification: Restricted

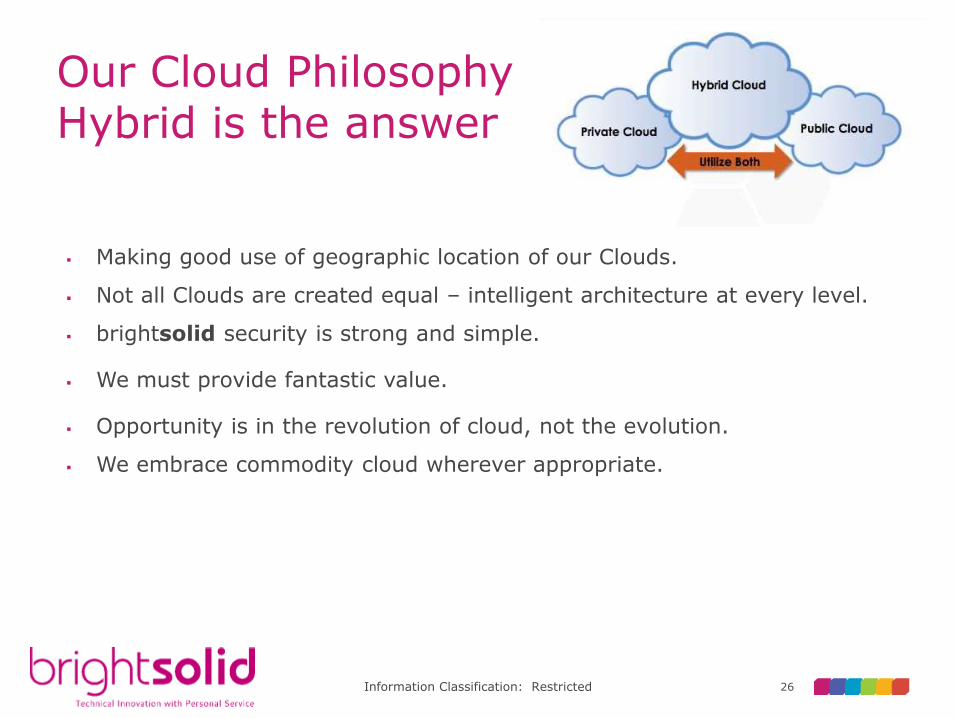

Our Cloud PhilosophyHybrid is the answer

Making good use of geographic location of our Clouds.

Not all Clouds are created equal – intelligent architecture at every level.

brightsolid security is strong and simple.

We must provide fantastic value.

Opportunity is in the revolution of cloud, not the evolution.

We embrace commodity cloud wherever appropriate.

27Information Classification: Restricted

Launching in Aberdeen

Cisco Cloud Interconnect

Microsoft Storage Spaces

Millions of IOPs, significantly cheaper than traditional SAN

Linear, predictable scaling

Built in Storage Quality of Service

AA (Aberdeen Azure)

Currently in test

28Information Classification: Restricted

Development in the brightsolid CloudDevOps Toolset

… or your own preferred toolset

29Information Classification: Restricted

Disaster Recovery in the brightsolid Cloud

Multiple Scenarios Catered ForPhysical and Virtual Services ProtectedSelf-Service Management of Disaster Recovery Invocation

30Information Classification: Restricted

Collaborative platform cloudsA portfolio built on capacity for operational excellence & innovative drive

Platform and App. Clouds that are architected for operation, security and reliability

brightsolid

Cloud Recovery

31Information Classification: Restricted

Data driven collaborationLocal Council case study

The challenge:

Siloed departments & data sets Too much data but no valuable information Limited proactive intervention

Finding what’s valuable:

Joined up data, useful information pulled from multiple data sets Inter-agency collaboration that creates a proactive intervention

Information Classification: Restricted 32

33Information Classification: Restricted

Chris DavisIT4IT Forum

@it4it

#oilgasict

Copyright © The Open Group 2015

Copyright © The Open Group 2015 36

Achieving value from standardisation

Chris DavisUniversity of South Florida

Copyright © The Open Group 2015

Goals and overview

• A collaborative approach to improving IT efficiency

• Creating standardised, vendor-neutral IT

architecture

• Driving cost reduction and value optimisation

37

• The Open Group

• The IT4IT™ Forum

• Value propositions

Copyright © The Open Group 2015

The Open Group

• A global consortium that enables the achievement of business

objectives through the development of open, vendor-neutral IT

standards and certifications

• More than 480 member organisations: a diverse membership that spans

all sectors of the IT community — customers, systems and solutions

suppliers, tool vendors, integrators and consultants, as well as

academics and researchers

• Vision: Boundaryless Information Flow™ achieved through global

interoperability in a secure, reliable and timely manner

Copyright © The Open Group 2015

43,283 people in 131 countries

488 memberships

HQs in 40 countries

6 continents

PakistanPhilippines

PolandQatar

Saudi ArabiaSingapore

South AfricaSpain

SwedenSwitzerland

TaiwanTurkey

UKUnited Arab

EmiratesUSA

The Open Group membership

AustraliaBelgiumBrazilCanadaChinaColombiaCzech RepublicDenmarkFinlandFranceGermanyHong KongIndiaIrelandItaly

JapanKoreaLuxembourgMalaysia

MexicoNetherlandsNew ZealandNigeriaNorway

Copyright © The Open Group 2015

The Open Group

• Enables all organisations that use information technology to do things

better, faster and cheaper

• Enables all suppliers of information technology products and services to

gain business benefit

• Enable every individual to develop their skills and capabilities…

• Establish work groups and forums to develop standards, guides, best

practices and white papers

• Openly publish the output of those work groups and forums and

acknowledge the contributors

• Operate certification and accreditation programs to recognise the

individuals, products, services or processes that meet our members’

standards

Copyright © The Open Group 2015

What is the problem?

• Lack of cooperation across all IT

leads to sub-optimisation

• Insufficiently integrated IT

management toolsets, lack of

prescriptive guidance

• Inability to gain true insight in order to

make good decisions

• Immaturity makes it virtually

impossible to tackle disruptive

innovations like cloud, agility,

mobility, BYOD, …41

Copyright © The Open Group 2015

Who and where are we?

Original Consortium

• Shell

• Hewlett-Packard

• Achmea

• MunichRe

• Accenture

• PricewaterhouseCoopers

• University of South Florida

• AT&T

Forum Members now include

• IBM

• Microsoft

• ServiceNow

• Oracle

• Logicalis

• Capgemini

• ExxonMobil

• BP

• Origin Energy

42

Value Chain

RA 0.5 (level

1)

RA 1.0 (level

2)

RA 1.2 (level

3)

RA 1.3 (level

3)

… …

9/2011 1/2013 10/20148/2012 3/2014

Copyright © The Open Group 2015 43

Val Sribar, Group Vice President

Gartner Enterprise Software Research Group

Copyright © The Open Group 2015

What is IT4IT™?

• IT4IT™, an evolving Open Group standard, provides a

reference architecture for managing the Business of IT,

enabling insight for continuous improvement;

• IT4IT™ will enable IT execution across the entire Value

Chain in a better, faster, cheaper way with less risk;

• IT4IT™ is fundamentally vendor neutral, technology

agnostic and industry agnostic.

44

Copyright © The Open Group 2015

Value Chain, Reference Architecture

45

From Why to What

From What to How(uses TOGAF®, specified in ArchiMate™)

This is all about data!

Embracing existing process and agile frameworks.

Copyright © The Open Group 2015

IT Operating Model: Value Chains &

Reference Architecture

Deploy

• Release plan

• Deployment assets

• Change and

configuration process

• Knowledge

management

• App monitoring

Develop

• Technical policy

• Development (Agile,

iterative, waterfall…)

• Source & set up dev

environment

Requirements

• Business process

model

• User experience

• Functional &

technical

• Functional: desktop,

web, mobile

• Performance:

desktop, web, mobile

• Security: static,

dynamic

Test

Requirement to Deploy

KPIs:

• Cycle Time

• Requirements ‘Churn’

• Production Defects

Copyright © The Open Group 2015

Positioning IT4IT™ in the ‘landscape’

Copyright © The Open Group 2015

IT4IT™ and ITIL®ITIL IT4IT

Positioning Framework describing functions/capabilities/disciplines.

Information model driven reference architecture, supportive of multiple process frameworks.

Origins “Best” or “good” practice origins intended for broad

audience of executives, managers, and individual contributors.

Originated out of needs identified by enterprise

architects and IT managers for clearer implementation and integration guidance

Methodology Primarily unstructured narrative. “Process” (similar

to what enterprise architects would term function) is the primary unit of analysis.

Structured consistently with TOGAF and

Archimate. Value stream, capability, data, system views.

Orientation Oriented to practitioner education rather than solution

Solution orientation

Value approach Oriented to deep discussion of individual silo

functions/processes. Beyond overall service

lifecycle, does not emphasize longer lived value flows.

Focused on the end to end flow of four high level

IT value streams (Strategy to Portfolio,

Requirement to Deploy, Request to Fulfill, Detect to Correct) across IT capabilities.

Internal consistency Ambiguous and overlapping terminology in places Mutually exclusive and comprehensive, rigorously

avoiding ambiguity and overlap in its architectural catalogs

Level of detail Not sufficiently detailed to be of utility to planners

and architects attempting to integrate IT management infrastructure.

Precise representation of data and integration patterns in complex IT management domain

Agile Implicit waterfall, top-down planning orientation. Explicit coverage of Agile and DevOps trends.

Maintenance process

Long term history of proprietary ownership. Multi-year revision cycle

Open development process

Copyright © The Open Group 2015

IT4IT™ Value Propositions

For ‘consuming IT organisations’ e.g. ExxonMobil,

Shell, Origin Energy

• Helps to plan and implement IT4IT solutions

For software vendors e.g. IBM, HP, Microsoft,

ServiceNow, Oracle

• Helps to determine current tools capability vs.

Reference Architecture

Copyright © The Open Group 2015

IT4IT™ Value Propositions

For software integrators e.g. Accenture, Capgemini,

Logicalis, Tata Consultancy Services

• Prescriptive guidance to help consuming

companies plan for implementation of IT4IT journey

For individuals (‘within’ each of the organisation

types)

• personal professional development opportunity.

Copyright © The Open Group 2015 60

Questions & Discussion

#oilgasict

Refreshments &Exhibition

Please check badges for workshop location

#oilgasict

Welcome Back

#oilgasict

Prof John McCallSmart Data

Technologies Centre

@rgucomputing#oilgasict

Smart Data Technologies

John McCall

Robert Gordon University

Data Explosion

• The world's per-capita capacity to store information has roughly doubled every 40 months since the 1980s

• As of 2012, 2.5 exabytes(2.5×1018) of data are being created each day

• Problem is very big and growing fast

• Opportunity is very big and growing fast

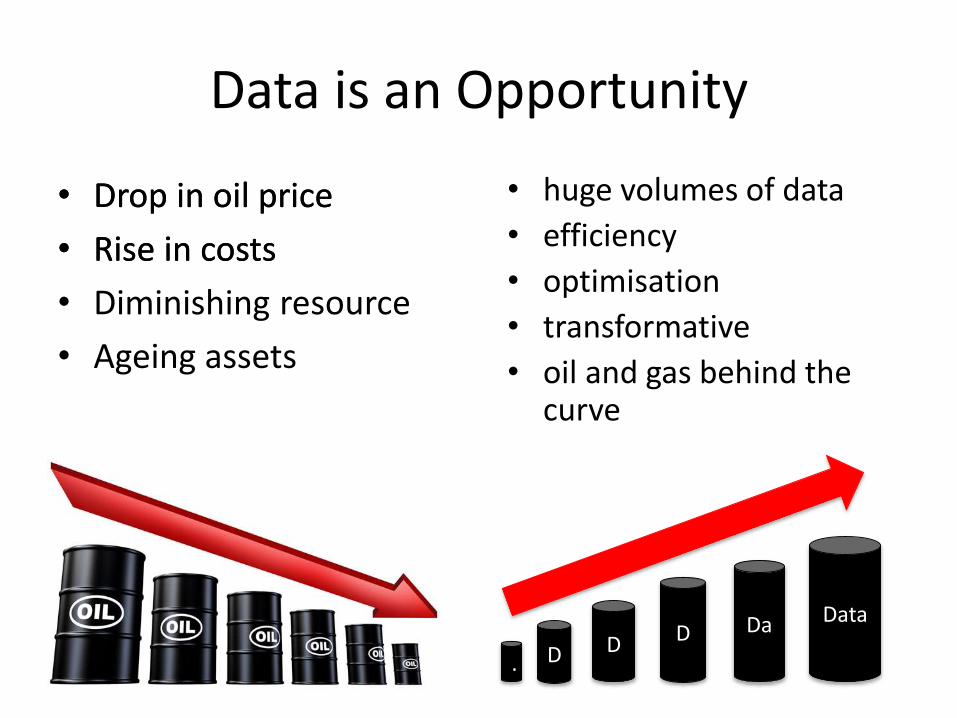

Data is an Opportunity

• Drop in oil price

• Rise in costs

• Diminishing resource

• Ageing assets

. D D D Da Data

• huge volumes of data

• efficiency

• optimisation

• transformative

• oil and gas behind the curve

• Drop in oil price

• Rise in costs

Key Industry Challenges

Bravo et al. (2013) SPE Journal

Bravo et al. (2013) SPE Journal

Key Questions

How can you use data to improve the bottom line?

What can you do with captured data?

Sensors and Data Models

Gas Turbine Power Plant

• Data model of 21 temperature sensors in a gas turbine power plant

• Model from 15 mins of normal operations data (870 measurements per sensor)

• Used to compare actual values with those inferred from neighbours

• 0.4% severe missed alarms

• 6.5% mild false alarms

• Controllable precision

Data Model for Sensor Validation

C4

AX

AE

C2

C5

C3

C1

Extract from the sensor model

Prof. John McCall, RGUIbargüengoytia et al. 2008)

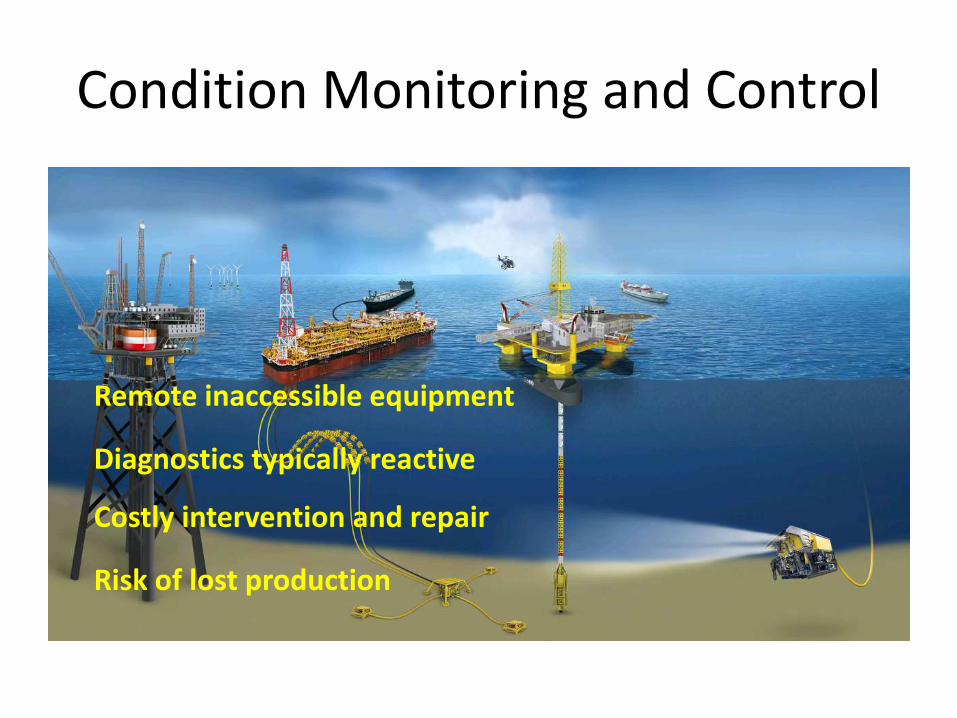

Condition Monitoring and Control

Remote inaccessible equipment

Diagnostics typically reactive

Costly intervention and repair

Risk of lost production

Control Systems Data Model

• V-Sentinel™ – pressure sensors data model

– no mathematical modelling

– no fixed alarm thresholds

– self-adapts to new installations

• Detects:

– accumulator gas loss, insulation resistance dropping, standby pump anomaly,hydraulic fluid leakage

• predicts valve failure

V-Sentinel™

• provides 24/7 condition monitoring

• allows early fault detection

• enables predictive maintenance

• Benefits for the industry– increased production

availability

– customisable fault-detection to fit specific needs

http://www.vipersubsea.com/products/v_sentinel/

Logistics and Supply Chain Optimisation

• Resource intensive– high opex– affects production

• Dynamic– demand and supply

changes

• Unpredictable– delays and events affect

plans

• Complexity– complex chain of decision

and implication– tendency to over-resource

Solving Logistics Problems

• Modern algorithms can solve hard logistical problems effectively

– genetic algorithms, ant colonies, …

• Need to be data driven

• Need to capture important constraints

• Computationally Intensive

77

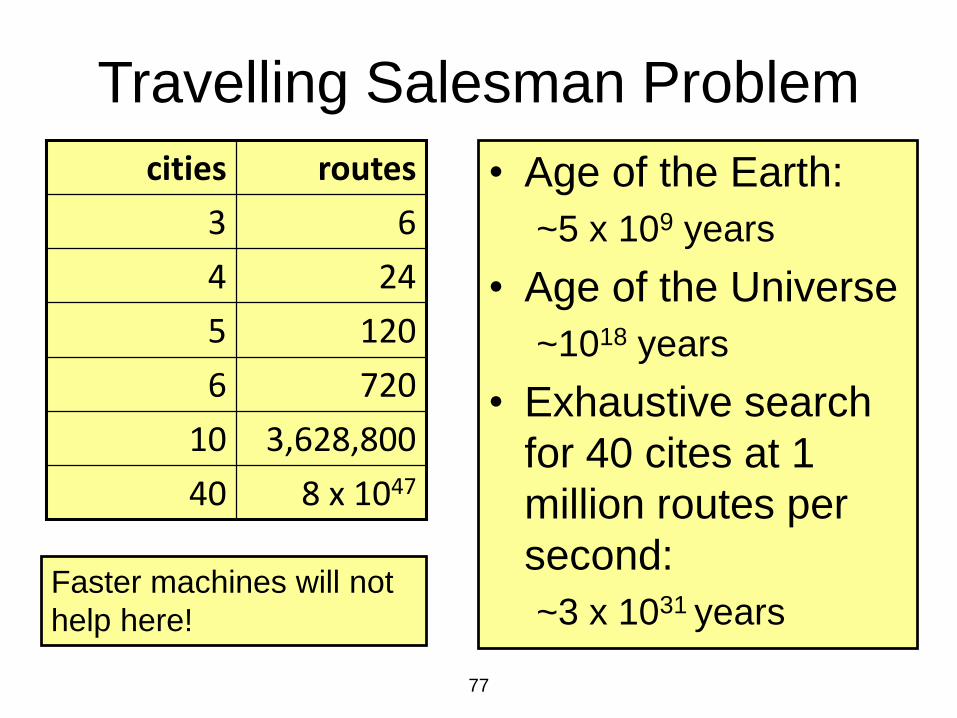

Travelling Salesman Problem

• Age of the Earth:

~5 x 109 years

• Age of the Universe

~1018 years

• Exhaustive search

for 40 cites at 1

million routes per

second:

~3 x 1031 years

63

244

8 x 104740

3,628,80010

7206

1205

routescities

Faster machines will not

help here!

Large Scale Complexity

13,509 US cities Pop. > 500

Modern algorithms are routinely solving world tours in a few hours

Supply Vessel Scheduling

Internet

Server

Data Gathering

Hosted Service

/ SAP interface

Reporting, Analysis,

Control, Decision

Support

Operations

Modelling,

Simulation,

Optimisation

for Fleet

Planning &

Scheduling

AHTS

PSV

DSV

http://www.plansea.co.uk

Potential Benefits of Optimisation

• Increase utilisation, decrease resource requirement

• typical resources savings 10% -30% – supply vessel @£15K/day hire

– reduce 5 vessel fleet to 4 saves £4.5M per year on hire costs alone

• similar savings can be realisedthroughout the supply chain.

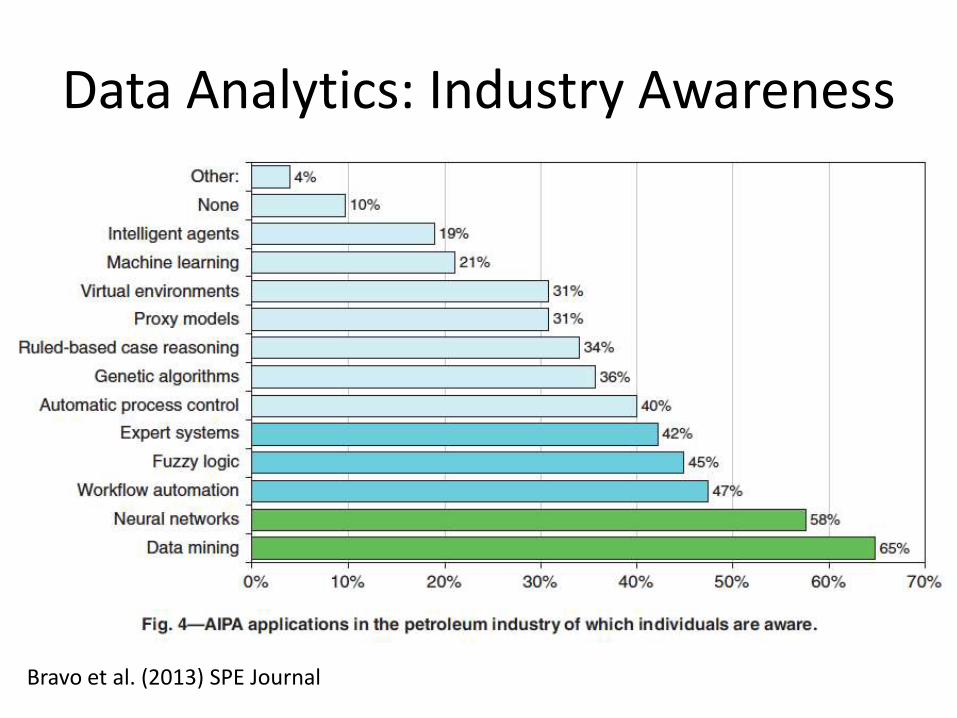

Data Analytics: Industry Awareness

Bravo et al. (2013) SPE Journal

Bravo et al. (2013) SPE Journal

Conclusion

• Smart Data offers huge benefits• Much potential remains to be explored• Economics favours new approaches• Aberdeen has leading industry

expertise and a strong supporting environment– DataLab – data science– CENSIS – sensors technology– OGIC – oil and gas innovation– Robert Gordon and Aberdeen Universities

Dr Vidar HepsoStatoil

@statoilasa

#oilgasict

Using technology to minimise the environmental impact of drilling and exploration--Integrated environmental monitoring

Vidar Hepsø (PhD), Statoil RDI, Trondheim, Norway

A shift in environmental monitoring

From expeditions and

offline samples

To continuous environmental

monitoring based on real-time data

Licence to operate demonstrating prudent operations

Integrated Environmental Monitoring; the total concept

Knowledge Sharing &

Analytics

Learning

Analysis

Sense making

Intelligent

Infrastructure

Planning

Decision making

Workflow

Business

Operations

Information &

Collaboration

Virtual interaction

Coordination

Shared awareness

Access

Connect

Sense

Emergency response

Sensors

& sensor

platforms

MobileExisting sensors & sources Stationary

ocean

observatory

Information & work processesExternal

organisations

Central support functionsAsset control room

Domain experts

Emergency responseEmergency response

Sensors

& sensor

platforms

MobileExisting sensors & sources Stationary

ocean

observatory

Sensors

& sensor

platforms

MobileExisting sensors & sources Stationary

ocean

observatory

Information & work processesInformation & work processesExternal

organisations

External

organisations

Central support functionsCentral support functionsAsset control roomAsset control room

Domain expertsDomain experts

Background photo: Harald Pettersen

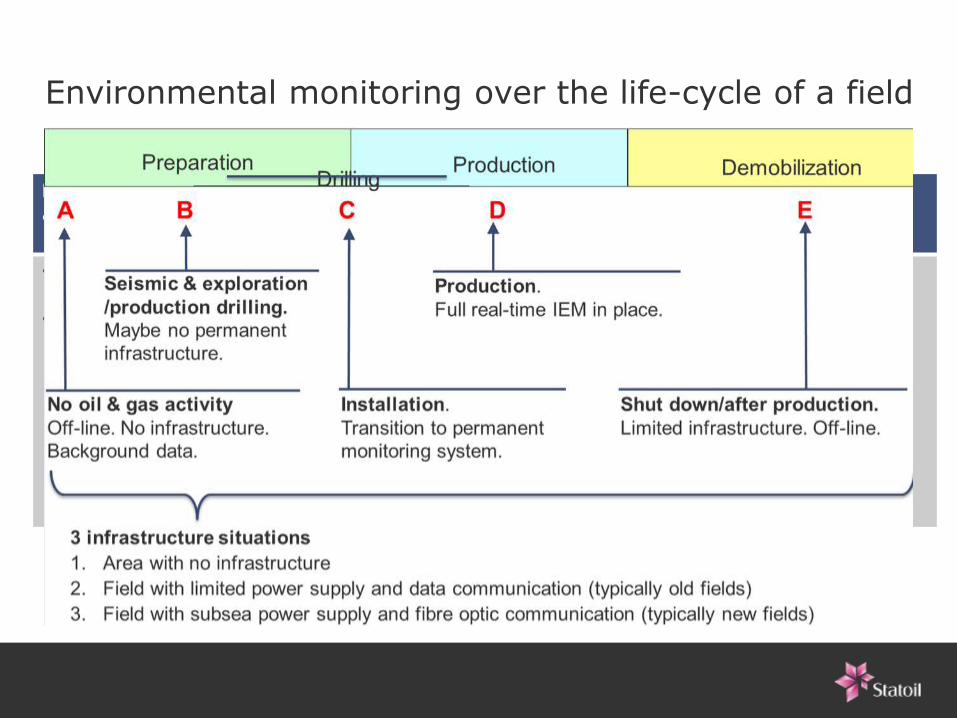

Environmental monitoring over the life-cycle of a field

Before development

& operations

During development

& operations

During production After

decommissioning

• Monitor and map

biological activity

• Analysis of data

and establishing

design basis

• Monitor and map

biological activity

• Analysis of

environmental

impact

• Leak detection by

acoustic & visual

monitoring for early

warning

• Monitor and map

biological activity

• Analysis of

environmental

impact

• Leak detection by

acoustic & visual

monitoring for early

warning

• Monitor and map

biological activity

• Analysis of

environmental

impact

The Norwegian Sea-the Morvin asset

• Area with cold water coral

structures

• On-line monitoring before, during

and after drilling

• Physical/chemical data

• Visual monitoring

• Real time monitoring proved no

harm to the corals

Drilling in areas with cold water corals

Planning phase

• Reduce environmental impact

• Obtain discharge permit

• Document & communicate

Operational phase

• Monitor & control exposure

• Take preventive actions

• Verify predicted risk & impact

Post drilling phase

• Document & evaluate operations

• Verify predicted risk & impact

Gather baseline data

• Environmental resources

• Species and conditions

• Critical levels / thresholds

• Met-ocean data

Perform analysis

• Simulate discharges

• Assess risk to environmental

resources

Create drilling plan, select drilling

& discharge locations

Visualize real-time environmental

and operational data

• Drill cuttings generated

• Key environmental parameters

Repeat simulation of discharges

Update risk evaluations

Decision support

Document risk evaluations and

any incidents

Document recommendations

and decisions made

Document and verify possible

environmental effects

Shared situation awareness & decision support

Field

23’ Oct21’ Nov

Conclusion

• Move to Integrated environmental monitoring covering the life-

cycle of an oil and gas asset

− Common operating pictures

− Real-time and operational understanding of risk and

environmental parameters

• Developing a capability platform/stack with a plug and play

sensor network that will enable us to test out new potential

environmental sensors

• Development of a platform with modules that can be adjusted to

various situations during the life-cycle of an oil and gas field

Classification: Internal 2013-09-1291

Presentation title:

Using technology to minimise the

environmental impact of drilling and

exploration

-Integrated environmental monitoring

Presenters name: Vidar Hepsø

Presenters title: Project Manager

E-mail: [email protected]

Tel: +4748034803

www.statoil.com

9

2

What do we want to measure? -Examples

Sensor Parameter Data type Location specific

Echo sounders Biological activity:

Fish

sea mammals

gas bubbles

Particles

Echogram, needs expert

interpretation

Large range

Camera with light Visual observation Video and/or still pictures Large range

Doppler recorder and

Current Profiler

Current speed and direction

Temperature

Conductivity

Pressure

Oxygen

Turbidity

Fluorescence

Time series, vector data

Point data

Point source

Sediment trap Samples to be analysed in the

laboratory

Point source

Hydrophone Biological activity Echogram, large data files that

needs expert interpretation

Large range

Hydrocarbon sniffers Presence of hydrocarbons Point data Point source

Martin OgdenExpro

@exprogroup

#oilgasict

Cloud Computing – The Truth

Martin Ogden – CIO

96

Expro employs over 5,400 people in over 50 countries, offering a truly global service solution.

With our head office in the UK, we have regional headquarters in Aberdeen, Accra (Ghana), Dubai, Houston, Kuala

Lumpur and Rio.

©Copyright Expro 2015

AmericasLocations: Texas, Los Angeles, Colarado, Oklahoma, North Dakota, Connecticut, Canada, Brazil, Argentina, Bolivia, Columbia, Mexico

More than 1,250 employees

Europe & CISLocations include: UK, Kazakhstan, Norway, Russia, Holland

More than 1,800 employees

Sub Saharan AfricaLocations include: Ghana, Nigeria, Angola, Congo, Gabon, South Africa, Equatorial Guinea, Cameroon, Ivory Coast

More than 1,000 employees

Asia, Middle East and North AfricaLocations include: Algeria, Egypt, Iraq, Saudi Arabia, UAE, Australia, India, Indonesia, Malaysia, Thailand, Vietnam, China

More than 1,400employees

100+ service locations

5,400+ employees

Extensive global presence

Introduction

/Martin Ogden – CIO

Joined Expro 2000

IT Team of 40

Global Remit

Support function working with:

Group HR,

Learning & Development,

Corporate Communications,

Global Supply Chain,

Business Process Improvement

Benefits of the cloud

SalesForce

Flexibility

Disaster recovery

Automatic software updates

Cap-Ex Free

Increased collaboration

Work from anywhere

Document control

Security

Competitiveness

Environmentally friendly

NTT

Achieve economies of scale

Reduce spending on

technology infrastructure

Globalize your workforce on

the cheap

Streamline processes

Reduce capital costs

Improve accessibility

Monitor projects more

effectively

Less personnel training is

needed

Minimize licensing new

software

Improve flexibility

Imperial College London

No wasted capacity

No in house maintenance

Fast deployment of new

services

No in-house maintenance of

infrastructure to support

application

Access to data anywhere

Synchronisation of data

across devices

Easy to share data

Data is backed up

Queensland Government

Reduced IT costs

Scalability

Business continuity

Collaboration efficiency

Flexibility of work practices

Access to automatic updates

Benefits of the cloud

SalesForce

Flexibility

Disaster recovery

Automatic software updates

Cap-Ex Free

Increased collaboration

Work from anywhere

Document control

Security

Competitiveness

Environmentally friendly

NTT

Achieve economies of scale

Reduce spending on

technology infrastructure

Globalize your workforce on

the cheap

Streamline processes

Reduce capital costs

Improve accessibility

Monitor projects more

effectively

Less personnel training is

needed

Minimize licensing new

software

Improve flexibility

Imperial College London

No wasted capacity

No in house maintenance

Fast deployment of new

services

No in-house maintenance of

infrastructure to support

application

Access to data anywhere

Synchronisation of data

across devices

Easy to share data

Data is backed up

Queensland Government

Reduced IT costs

Scalability

Business continuity

Collaboration efficiency

Flexibility of work practices

Access to automatic updates

FlexibilityFlexibility – Disaster recoveryFlexibility – Disaster recovery – Management Flexibility – Disaster recovery – Management – Cost

Is the cloud a myth?

Is the cloud a myth?

Conversation at a conference:

“I’ve been told it will take 6 months to migrate our data from system x to system

y, is that true?”

“That sounds reasonable, depending on how much data you have and how well

the two systems match”

“Why does it take so long, after all it’s all in the cloud”

Is the cloud a myth?

Reality is:

The cloud is a managed service

There are a myriad of providers

• Most do not interface/collaborate

• You will need other services:

– Single sign on/identity management

– Interfaces between on premise and cloud

– Interfaces between clouds

Its not a new concept – they used to be called Application Service

Providers (ASP)

The pitfalls of the Cloud

Service will only be as good as the service provider Over six in ten (63%) respondents are not 100% clear on what constitutes a failure or violation of their cloud service

provider’s SLA

Almost a quarter (22%) of respondents say that their cloud service provider didn’t deliver what they thought their

organisation had signed up to

Over one in ten (14%) had their job roles threatened because of SLA failure/violation

More than three quarters (77%) expect the pay-out received after an SLA violation to offset damage done to their company.

However, of those who have received a penalty payment from a cloud service provider after an SLA violation almost half of

these (46%) felt the pay-out was not comparable with the level of violation

(source Vanson Bourne Business Panel)

The pitfalls of the Cloud

You are no longer in control of the data

The data is sitting on the providers infrastructure

It is unlikely you will have full system access

You are no longer in control of the functionality

Upgrades can become onerous

Cloud sprawl

Application lock in – inflexibility

Cost

Conclusions

Cloud is not a silver bullet

It has its place

It is a useful deployment method

But it will bring problems and issues

My strategy

Cloud first unless:

• You lose functionality

• It is overly complex

• It costs more

Questions & Discussion

#oilgasict

Drinks ReceptionExhibition Room

Sponsored by

#oilgasict

30th April Edinburghwww.scot-secure.com

18th June Edinburghwww.scot-cloud.com

Day 2- Welcome To

#oilgasict

Mark StephenBBC Scotland

Conference Chair

#oilgasict

Cedric Levy-Bencheton

ENISA@enisa_eu

#oilgasict

European Union Agency for Network and Information Security www.enisa.europa.eu

Safeguarding the European energy market

Dr. Cédric LÉVY-BENCHETON

Network and Information Security Expert

European Union Agency for Network and Information Security

Oil & Gas ICT Leader, Aberdeen, 19 March 2015

European Union Agency for Network and Information Security www.enisa.europa.eu 116

Summary

• Presentation of ENISA

• Focus on protecting ICS / SCADA

– ICS/SCADA certification (2013)

– Window of exposure (2013)

– Certification of skills in ICS/SCADA (2015)

• Conclusion

European Union Agency for Network and Information Security www.enisa.europa.eu 117

EU Cyber Security Strategy

• The Five strategic objectives of the strategy:

– Achieving cyber resilience

– Drastically reducing cybercrime

– Developing cyberdefence policy and capabilities related to the Common Security and Defence Policy (CSDP)

– Developing the industrial and technological resources for cybersecurity

– Establishing a coherent international cyberspace policy for the European Union and promote core EU values

ENISA explicitly called upon

European Union Agency for Network and Information Security www.enisa.europa.eu 118

Presentation of ENISA

• The European Union Agency for Network and Information Security was formed in 2004. The original mandate was renewed and extended in 2013

• The Agency is a Centre of Expertise that supports the Commission and the EU Member States in the area of information security

• We facilitate the exchange of information between communities, with particular emphasis on the EU institutions, the public sector and the private sector

European Union Agency for Network and Information Security www.enisa.europa.eu 119

Hands on

Policy ImplementationRecommendations

Mobilising Communities

ENISA Activities

European Union Agency for Network and Information Security www.enisa.europa.eu 120

ENISA’s contributions to EU Initiatives and WG on SG and ICS/SCADA Security

• EuroSCSIE

• EU-US WG on smart grids security

– EU-US Working Group on Cyber Security and Cyber Crime (losing momentum)

• ERNCIP

– European Reference Network for Critical Infrastructure Protection

• TNCEIP

– Thematic Network on Critical Energy Infrastructure Protection

• DENSEK

– European Energy - ISAC

• NIS platform

• ENISA SISEC

– Smart Infrastructures Security Experts Community

• ENISA ICS Security Stakeholder Group

120

European Union Agency for Network and Information Security www.enisa.europa.eu 121

ICS/SCADA Security

• Key underlying infrastructure in all CIIs

• “Modernised” to be used via Internet

• Not business as usual for cyber security matters

• ENISA’s work– Certification of ICS/SCADA experts’ cyber security skills (2014)– Ex-post analysis of security incidents in ICS/SCADA environments

(2013)– ICS/SCADA Patching (2013)– ICS/SCADA Testing (2013)– ICS/SCADA Recommendations (2011)

European Union Agency for Network and Information Security www.enisa.europa.eu 122

Summary

• Presentation of ENISA

• Focus on protecting ICS/SCADA

– ICS/SCADA certification (2013)

– Window of exposure (2013)

– Certification of skills in ICS/SCADA (2015)

• Conclusion

European Union Agency for Network and Information Security www.enisa.europa.eu 123

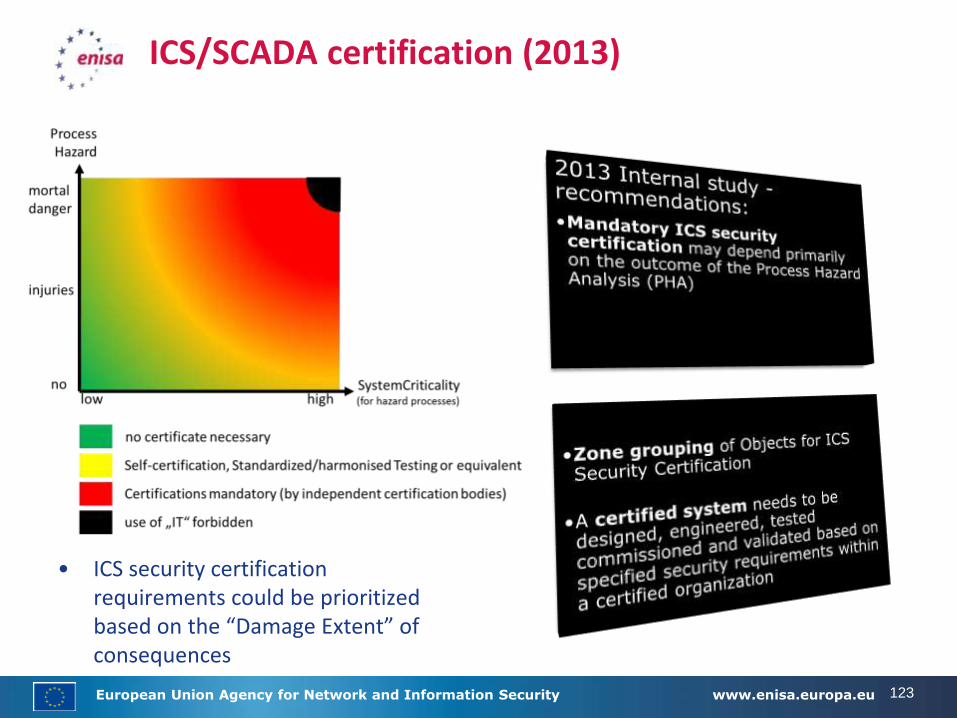

ICS/SCADA certification (2013)

• ICS security certification requirements could be prioritized based on the “Damage Extent” of consequences

European Union Agency for Network and Information Security www.enisa.europa.eu 124

Window of exposure (2013)

• Patching may not be possible for various reasons

• Patch management to enhance the security of ICS/SCADA

European Union Agency for Network and Information Security www.enisa.europa.eu 125

Certification of skills in ICS/SCADA (2015)

• Ensure security skills of all personals

– From operational to top management

– Importance in case of a crisis

• The report evaluates the needs of the sector

– List existing certification schemes

– Recommendations for a harmonised certification scheme

Certification is part of a global approach to enhanced cyber security

European Union Agency for Network and Information Security www.enisa.europa.eu 126

Summary

• Presentation of ENISA

• Focus on protecting ICS/SCADA

– ICS/SCADA certification (2013)

– Window of exposure (2013)

– Certification of skills in ICS/SCADA (2015)

• Conclusion

European Union Agency for Network and Information Security www.enisa.europa.eu 127

Conclusion

• ENISA’s work to enhance cyber security in ICS/SCADA

– A practical approach

– Targeted at different stakeholders

• Promote a multi-level approach

– Secure network architecture

– Patch management

– Certification of skills for every personal

Cyber Security for ICS/SCADA is a main concern for every actor

www.enisa.europa.euEuropean Union Agency for Network and Information Security

Follow ENISA:

Thank you

Dr. Cédric LÉ[email protected]

Phone: +30 2814 409 630Mobile: +30 6948 460 133

Matt GristSwire Oilfield Services

#oilgasict

Making Information Security Relevant and Real

Matt Grist – Group Information Security and Compliance Manager

Swire Oilfield Services

Swire Oilfield Services

The Americas:

USA & Brazil

Over 200 employees

Europe & Africa:

Head Office, UK, Norway,

West, Southern & East Africa

Over 600 employees

Asia Pacific:

SE Asia, Australia, India,

Sakhalin, Middle East

Over 50 employees

Global CCU Fleet Size:

Over 60,000

OverVu® - full service, track and trace solution

Assumptions

•The majority of the audience are not dedicated solely to information security

•Focus on costs

• IT is often seen as being responsible for security

• Information Security and IT Security are not (quite) the same thing

Confidentiality

Integrity

Availability

It comes down to risk (and reward?)•Make Information Security a business risk

•Do that by making it something that is relevant at the ‘C’ level

•Threat is real and it will happen. Is it ‘advanced’?

Cost of Breaches 2014

£600k -£1.15m is the average cost to a large organisation of its worst security breach of the year (up from £450 - £850k a year ago)*

£65k -£115k is the average cost to a small business of its worst security breach of the year (up from £35 -£65k a year ago)*

* Source - Department for Business, Innovation and Skills Information Security Breaches Survey 2014

Threat

• 1 Billion records breached in 2014

• “Chinese have penetrated every major corporation of consequence in the US and taken information”

• Saudi Aramco

• Attacks in Norway

• POC at Black Hat 2013 – Programmable Logic Controller

• What we don’t know

JP Morgan Chase

• May have been a set of stolen or compromised credentials

• Failure to use two factor authentication

• Used as step off to attack approximately 90 other servers

• 76 million household customers and 7 million businesses

It comes down to risk…. (and reward?)•Make Information Security a business risk

•Do that by making it something that is relevant at the ‘C’ level

•Threat is real and it will happen. Is it ‘advanced’?

•Not just about Confidentiality. Safety, availability, reputation etc.

Air Traffic Control Systems -Swanwick• Controls 200,000 square miles of airspace

• 5000 flights every 24hrs

• Ageing systems – and approximately 50 different systems

• Single line of code

• Challenge to upgrade

It comes down to risk…. (and reward?)• Make Information Security a business risk

• Do that by making it something that is relevant at the ‘C’ level

• Threat is real and it will happen. Is it ‘advanced’?

• Not just about Confidentiality. Safety, availability, reputation etc.

• Consider as part of the wider Risk Management process

• Risk owner – not IT

• Risk assessment informs investment

• Red lines (are there any?)

• Rewards – collaboration, efficiency. Enabled by security.

Not (just) about IT

• Information Management

• Risk

• Vendors - ‘compliance in a box’

• Policy

• Culture, convenience, employee expectation

• Cross function collaboration

• Business focussed and driven – support efficiency and collaboration

• Governance

Addressing the problem

• Management ownership

• Understand your environment and information

• The ‘basics’ will address much of the technical risk

• Focus on areas of risk or exception - legacy

• Monitor and report

• User education – make it not just about work

• Policy and Governance

• It will happen – have a plan (not just an IT plan)

Resources

• E&P Information Security Forum

• CISP and UK CERT

• Cyber Essentials

• ISO 27002

• Vendors

Making Information Security Relevant and Real

Matt Grist – Group Information Security and Compliance Manager

Swire Oilfield Services

Questions & Discussion

#oilgasict

Refreshments &Exhibition

Please check badges for workshop location

#oilgasict

Welcome Back

#oilgasict

Anders From & John Mullin

Subsea7@subsea7official

#oilgasict

Improving Collaborationand Performance with

Unified Communications

19 March 2015

Anders From and John Mullin

150Page 20-Mar-15

Subsea 7’s UC journey – so far

151Page 20-Mar-15

Islands of communication technology

IM & Presence

Telephony

Video Conferencing

Audio Conferencing

Mobile Telephony

152Page 20-Mar-15

Low hanging fruit

153Page 20-Mar-15

Third party conferencing services

>$50K/Month

154Page 20-Mar-15

Lync conferencing launch

• Deployment of Lync 2010 Conferencing Server

• Sonus SBC and contract with SIP Trunk Provider for dial in conferencing numbers

• Procurement and delivery of headsets to all land-based users globally - >6,500

155Page 20-Mar-15

Lync collaboration

• Collaboration with screen sharing and peer to peer audio

• Federation with clients and suppliers

• Federation now active with 35 external business partners allowing effectively free communication with them

156Page 20-Mar-15

High profile communication campaign

157Page 20-Mar-15

The result

158Page 20-Mar-15

Norway Enterprise Voice pilot

159Page 20-Mar-15

Next stop – Lync 2013

160Page 20-Mar-15

A single communications platform

161Page 20-Mar-15

UC Architecture

162Page 20-Mar-15

Hub and branch architecture

163Page 20-Mar-15

Next steps

• 50% targeted reduction in telephony costs globally

164Page 20-Mar-15

Pitfalls and Challenges

165Page 20-Mar-15

Steve HarrisonScottish Enterprise

@scotent

#oilgasict

So What Is Digital Offshore?

Is it seeking to

increase the

connectivity,

the

connections

and the

connectors ...?

For Oil &Gas,

OW, Sub Sea

Mining?

So What Is Digital Offshore?

Is it seeking to

encourage and

develop more

intelligent ,

safer and

smarter

devices in the

offshore

environment....

under ever

worsening

conditions?

So What Is Digital Offshore?

Is it seeking to

prove the value

that can come

from the data to

reduce costs,

improve

efficiencies and

increase

safety...for all

offshore

industries?

Digital Offshore

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

Objectives

1. Share with you our thinking about the Digital Offshore opportunity

2. Encourage you to volunteer your companies, data, resources to exploring these opportunities

3. Update you on our plans to consult with you about this opportunity and to seek your active involvement

What do we mean by Digital Offshore?

Working Definition

• Digital Offshore is the convergence

of the technologies, data sciences

and offshore industries and plays to

the strengths that Scotland has in

Sensors / Sub Sea electronics, Big

Data / Data Sciences / Data

analytics/ data visualisation and the

Offshore Industries of E&P,

Subsea, CCS, Decom, OW. ( And

future markets)

• Digital Offshore is an economic

development opportunity for

company growth, new venture

creation, innovation &

internationalisation.

What do we mean by Digital Offshore?

Working Definition

• Digital Offshore is the convergence

of the technologies, data sciences

and offshore industries and plays to

the strengths that Scotland has in

Sensors / Sub Sea electronics, Big

Data / Data Sciences / Data

analytics/ data visualisation and the

Offshore Industries of E&P,

Subsea, CCS, Decom, OW. ( And

future markets)

• Digital Offshore is an economic

development opportunity for

company growth, new venture

creation, innovation &

internationalisation.

Offshore Industries:Challenges, Realities & Visions

Technology:Machines/Plant Processing, Controlsystems

Data:Capture, Collecting, Transmission, Storage, Analysis

What do we mean by Digital Offshore?

Working Definition

• Digital Offshore is the convergence

of the technologies, data sciences

and offshore industries and plays to

the strengths that Scotland has in

Sensors / Sub Sea electronics, Big

Data / Data Sciences / Data

analytics/ data visualisation and the

Offshore Industries of E&P,

Subsea, CCS, Decom, OW. ( And

future markets)

• Digital Offshore is an economic

development opportunity for

company growth, new venture

creation, innovation &

internationalisation.

Offshore Industries:Challenges, Realities & Visions

Technology:Machines/Plant Processing, Controlsystems

Data:Capture, Collecting, Transmission, Storage, Analysis

Sorry it was a trick

question..its all of

them and more

Steve H & Scottish Enterprise

• An Engineer – 15 years in a Multinational – Oil & Gas Services

• A Business Professional - Strategy, M&A, Operations, HR, Business Development, Innovation.

• A coach, mentor & advisor

• A facilitator – helping to make things happen

Overview

1. SE Supports individual companies to grow ...grants/expertise/networks

2. SE develops, invests & manages projects to help sectors to grow

– Creating conditions to encourage growth

– Removing barriers / obstacles that prevent growth

– Identifying opportunities and investing in resources to realise them.

“We identify and exploit opportunities for Scotland's economic growth by supporting Scottish companies to compete, helping to build globally competitive sectors, attracting new investment and creating a world-class business environment.”

Digital Offshore

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

Opportunity

1. Can Digital Technologies increase uptime and improve efficiency?

2. Can Digital Technologies improve prediction and reservoir modelling accuracies?

3. Can Digital Technologies better inform capital investment decisions?

4. Can Digital Technologies reduce lift cost?

However “they” have been saying that for decades...

Data2Text

Founded 2009,

3 scientist’s + 1

entrepreneur

Merged to form

Arria NLG in

2013

Floated on AIM

in 2014 for

£100M

Current trading

at £35M and 50

data scientists

Digital Offshore

The Value of Data

• As an ICT leader do you ever struggle to make the business case for improved & new technology?

• Is ICT seen as a value investment or a cost commodity?

• What if you could show that your systems, network and data can have a significant positive impact on performance?

Opportunity

1. Can Digital Technologies increase uptime and improve efficiency?

2. Can Digital Technologies improve prediction and reservoir modelling accuracies?

3. Can Digital Technologies better inform capital investment decisions?

4. Can Digital Technologies reduce lift cost?

However “they” have been saying that for decades...

Offshore Big Challenges

When to run and when

to not...

Prediction,

Prevention,

Production

Digital Offshore

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

(BIG) Vision’s

1. A vibrant and growing industry

cluster in Scotland & Aberdeen NOT

dependant upon proximity of

hydrocarbons and resilient to $oil

price.

2. A super cluster of high growth

companies to rival Silicon Valley as

the home for the Internet of (Energy )

Industry

3. Aberdeen regains and sustains its

reputation as the goto location of

choice for industry professionals and

companies. “Innovation City”

7 Years

From

zero to

$10Bn Val

and

$1.7Bn

Sales

Business

Model

Innovation

Can we

learn &

apply?

Digital Offshore

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

Challenges

1. Overcoming resistance and inertia

to change....

2. Gaining access to existing data

streams so that data scientists can

explore with domain experts to

interpret.

3. The reality of

operations...equipment not

configured correctly at first

installation and never corrected since

(22 regular inspections! GIGO)

4. Talking the same language and

having the same priorities

5. Misalignment and reward...

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

Overview

Digital Offshore

Joined Up Approach

1. A lot of activity is planned and

happening (calls & conferences)

2. Agreement to co-ordinate and

collaborate between different

organisations.

3. Working together on a 6 month

study consultation to baseline and

understand the opportunity.

4. Seeking ways to gain attention &

traction due to the current low oil

price

5. Developing a program of activity to

stimulate, encourage & support

Digital Offshore high growth

company start up’s.

Digital Offshore

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

Pathfinders Wanted

1. Do you have a datastream or data

set that you think might have hidden

value within it?

2. Do you have a problem where you

need a business case to validate

investment in technology?

3. Do you have a digital technology or

usage case that you would like us to

test and evaluate?

We are looking for bold pathfinders .

We have resources , we want your

problems so we can prove value.

Contact: [email protected]

to arrange a discussion.

Digital Offshore

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

Digital Entrepreneurs Wanted

1. Do you have an idea for a Digital

Offshore venture but unsure where

to start?

2. Would you like to be a Digital

Offshore millionaire, but don’t have

a killer idea?

3. Do you have an idea for a Digital

Offshore technology but not the

ability to develop it?

We are looking for bold entrepreneurs.

We have resources , we want to help

you build a venture of scale & value.

Contact: [email protected] to

arrange a discussion.

Digital Offshore

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

Investigation & Study

1. Establish the current realities about

the Digital Offshore sector in

Scotland

2. Investigate what is happening

elsewhere

3. Discuss and examine the critical

constraints, challenges and

handbrakes on growth

4. Develop suggestions for investment

to ensure Aberdeen continues to

lead

We need your voice in this. If you

want to take part or even help steer

then please :

Contact: [email protected]

to arrange a discussion

Digital Offshore

TopicsThursday 19th March

1. What do we mean by Digital Offshore?

2. The Digital Offshore opportunity

3. The Challenges

4. Finding Value

5. Consultative Study

6. FAMA

Freedom to Ask Me Anything!

(But I might not answer)

Objectives

1. Share with you our thinking about the Digital Offshore opportunity

2. Encourage you to volunteer your companies, data, resources to exploring these opportunities

3. Update you on our plans to consult with you about this opportunity and to seek your active involvement

Ernie LamzaOGIC

@ogicinnov8

#oilgasict

Collaborative Innovation

Ernie Lamza – Chief Operating Officer - OGIC

Collaborative Innovation

• Facilitating collaboration between academia and industry

• Delivering innovative solutions to the UKCS

• Ongoing IT Projects

The Innovation Centre Programme

OGIC – delivering demand-led innovation

• An oil & gas industry focussed broker and research funding organisation

• Aligned to industry agenda and ‘demand’ led

• Linking industry needs to university capabilities and ‘know-how’

• Funding £10.6m secured February 2014• Formal launch November 2014

• Targeting c. 100 projects over next 5 years• Funding of circa £1 million per year across 20 projects

OGIC Team

• Based at the Innovation Park in Aberdeen

• Broad oil & gas industry technical experience

• In house project management capability

Areas of demand – and of focusDefined by the oil & gas industry

Asset Integrity and Life Extension

Improving Exploration Outcomes

Subsea

Decommissioning

EnhancedOil Recovery

Production Optimisation

WellConstruction

Shale Gas Exploitation

OGIC – part of the oil & gas landscape

PILOT / ILGTechnologyLeadership

Board

IndustryCouncil

ResearchCouncilUK / SFC

Innovate UKSE / HIE

Sevenother

InnovationCentres

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

TRL 1 TRL 2 TRL 3 TRL 4 TRL 5 TRL 6 TRL 7 TRL 8 TRL 9

Basic Research Most Government Innovation Support

CommercialExploitation

Commercial Research Funding

UK Research Council Funding (NERC, ESPRC etc)

SFC Research Excellence Grants

SFC Research Postgraduate Grants

Pu

blic

Fu

nd

ing

Innovate UK funding

Innovation Centre funding

EU Project funding

Scottish GovernmentScottish Enterprise / HIE funding

Where Government funding is available

Technology Readiness levels – a useful language

Delivering innovative solutions

• Criteria• Oil & Gas• Innovative• Require academic input• Economic benefit for Scotland• OGIC funding typically £10-150k per project equating to 50% of project costs• Company contribution 50%

• Intellectual property• Held by company not university (or OGIC)• Non-competing license, deferred publication and use for teaching

Industry-led governance

Board

Chair

Paul de Leeuw

CEO

Ian Phillips

Enquest

Neil McCulloch

Proserv

David Lamont

Heriot Watt

Garry Pender

ETP

Barrie Shepherd

Oil & Gas UK Oonagh

Werngren

SFC - observer

Keith McDonald

SE / HIE -observer

David Rennie

Industry Advisory Panel

Project Review Panels

SubseaSeismic & Reservoir

Characterisation

Asset Integrity and Life

ExtensionDecom

Enhanced

Oil Recovery

Production

optimisation

Shale Gas Exploitation

Well

Construction

Delivering Innovative Solutions:Typical project application process

Initial company

approach to OGIC

Company agreed project

summary

University expressions of

interest

Project design evolves –

scope of work, schedule

Project Review Panel

approval

Contractual negotiation

Project delivery

Signpost to others Exit if criteria not met

Pre-project workshopsCompany approach OGIC with defined issue to be tackled

Initial problem definition, with NDA as appropriate

University expressions of interest – multiple participants

Collaborative workshop to generate potential solutions

R & D programme scoped

Projects executed

Project approval

Projects development

Initial University contacts

OGIC project hopper

~100 approaches

~18 in discussion

2 projects signed

Updated to 10 March 2015

Ongoing IT Projects

• Of the 20 projects in our hopper, 3 are IT based

• Topics include:• Artificial intelligence application for logistics

• Rapid data to knowledge conversion

• Advanced imaging

Get involvedVolunteer for our Project Review Panel

Get innovatingContact us

Jeanette ForbesPCL Group@pclgroup

#oilgasict

Questions & Discussion

#oilgasict

Oil & Gas ICT Leader2016

16th & 17th MarchAECC

#oilgasict

30th April Edinburghwww.scot-secure.com

18th June Edinburghwww.scot-cloud.com

Top Related