Languages

Pages

Legal

October 3, 2007 Version “B2”

Financial Services Industry Landscape

Regulation Going Forward

James C. Allen, CFAHead, Capital Markets PolicyCFA Institute

February 17, 2010

2

Rethinking Regulation

Page 2

Investors’ Working Group Report

July 2009

A Roadmap for a more comprehensive, effective and responsive regulatory

environment for investors, consumers and the broader financial system.

3

Short-Term Reforms

Page 3

• Strengthening existing federal agencies responsible for policing financial institutions and markets and protecting investors and consumers.

• Filling the gaps in the regulatory architecture and authority over certain investment firms, institutions and products.

• Improving corporate governance.

• Creating a Systemic Risk Oversight Board.

4

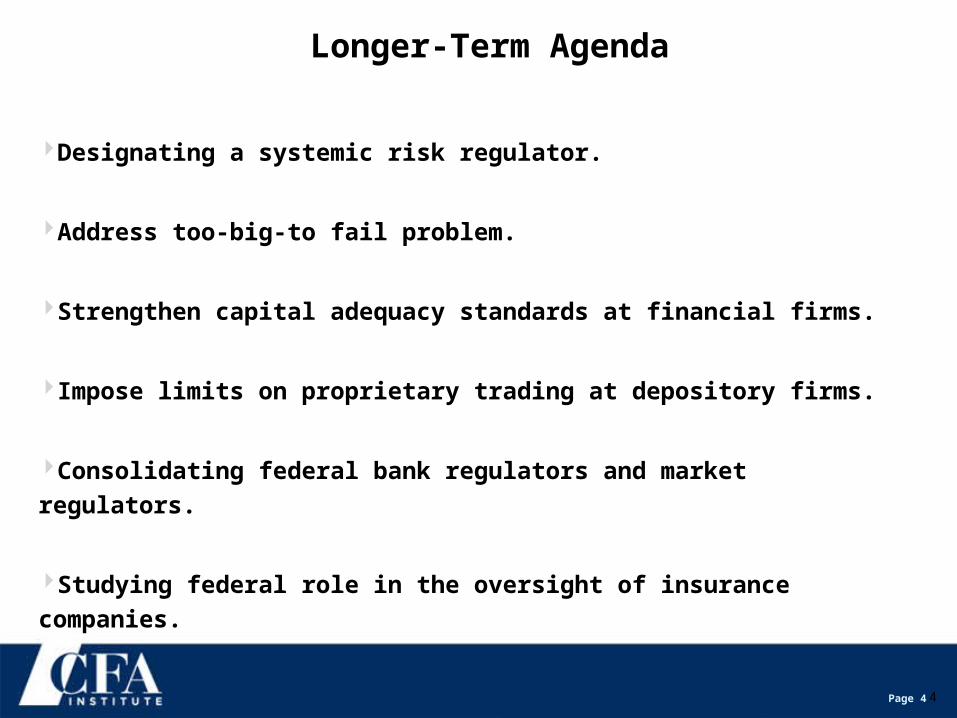

Longer-Term Agenda

Designating a systemic risk regulator.

Address too-big-to fail problem.

Strengthen capital adequacy standards at financial firms.

Impose limits on proprietary trading at depository firms.

Consolidating federal bank regulators and market regulators.

Studying federal role in the oversight of insurance companies.

Page 4

5

Strengthening Existing Regulators

• Regulators should have enhanced independence through stable, long-term funding that meets their needs.

• Regulators should acquire deeper knowledge and expertise.

• Staff should have a wide range of backgrounds.

• Compensation should be sufficient to attract top professionals.

• Promoting policies that are good for consumers, investors.

Page 5

6

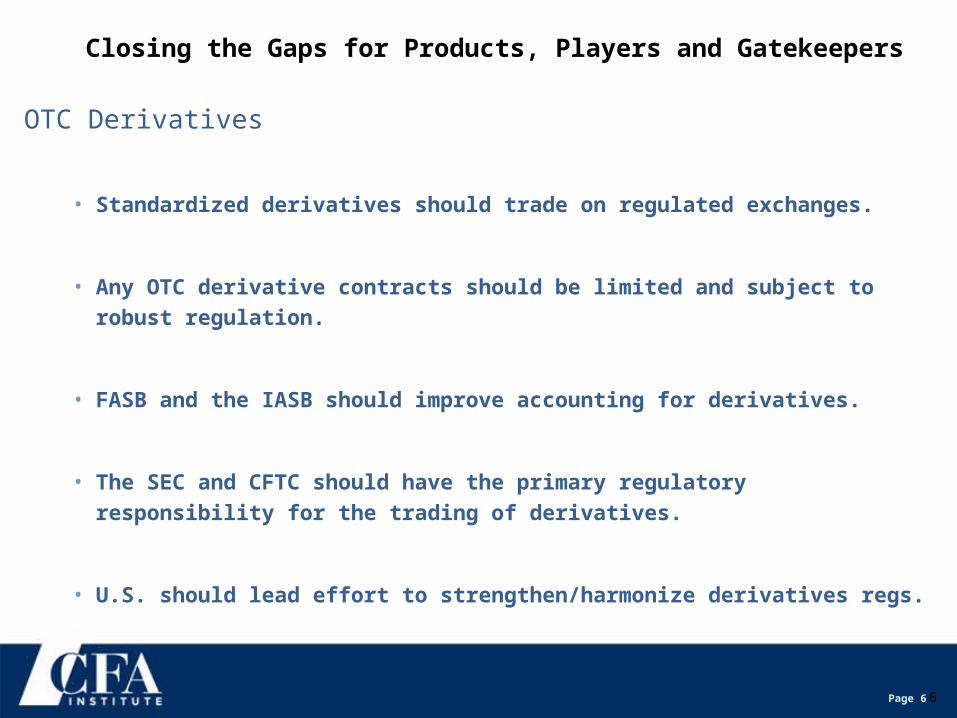

Closing the Gaps for Products, Players and Gatekeepers

OTC Derivatives

• Standardized derivatives should trade on regulated exchanges.

• Any OTC derivative contracts should be limited and subject to robust regulation.

• FASB and the IASB should improve accounting for derivatives.

• The SEC and CFTC should have the primary regulatory responsibility for the trading of derivatives.

• U.S. should lead effort to strengthen/harmonize derivatives regs.

Page 6

7

Closing the Gaps for Products, Players and Gatekeepers

Securitized Products

• New accounting standards for off-balance sheet treatment of securitizations should be implemented without delay.

• Sponsors should fully disclose their maximum potential loss from exposure to off-balance sheet asset-backed securities.

• The SEC should require ABS sponsors to improve the timeliness and quality of disclosures to investors in these instruments and other structured products.

• ABS sponsors should be required to retain a meaningful residual interest in their securities products, also known as “having skin in the game.”

Page 7

8

Closing the Gaps for Products, Players and Gatekeepers

Hedge Funds, Private Equity and Investment Companies

• All investment managers of funds that are available to U.S. investors should be required to register with the SEC as investment advisers, subject to its oversight.

• Existing regulations for investment managers should be reviewed to see if they are appropriate for the variety of funds and advisers.

• Investment managers should make regular disclosures about their holdings to regulators on a real-time basis and to their investors on a delayed basis.

Page 8

9

Closing the Gaps for Products, Players and Gatekeepers

Hedge Funds, Private Equity and Investment Companies (cont’d)

• Investment advisers and brokers who provide investment advice to their customers should adhere to a fiduciary standard. In addition, their compensation practices should be reformed and their disclosures should be improved.

• Finally, institutional investors – including pension funds, hedge funds and private equity firms – should make timely, public disclosures about their proxy voting guidelines, proxy votes cast, investment guidelines and members of their governing bodies, and report annually on holdings and performance.

Page 9

10

Closing the Gaps for Products, Players and Gatekeepers

Non-Bank Financial Institutions

• Congress should give regulators resolution authority, analogous to the FDIC’s authority for failed banks, to wind down or restructure troubled, systemically significant non banks.

Page 10

11

Closing the Gaps for Products, Players and Gatekeepers

Mortgage Originators

• Congress should create a new agency to regulate consumer financial products, including mortgages.

• Banks and other mortgage originators should comply with minimum underwriting standards, and documentation and verification requirements.

• Mortgage regulators should develop suitability standards and require lenders to comply with them.

• Finally, mortgage originators should be required to retain a meaningful residual interest in all loans and outstanding credit lines.

Page 11

12

Closing the Gaps

Nationally Recognized Statistical Rating Organizations (NRSROs)

• NRSROs compromised by conflicts of interest.

• Investors relied too heavily on ratings and ignored differences between structured

securities and traditional debt ratings..

• Encourage alternatives to the predominant issuer-pays NRSRO business model.

• Bolster the SEC’s position as an independent overseer of credit rating agencies.

• NRSROs should be held to a higher standard of accountability.

• Reliance on credit ratings should be greatly reduced by regulatory amendments.

Page 12

13

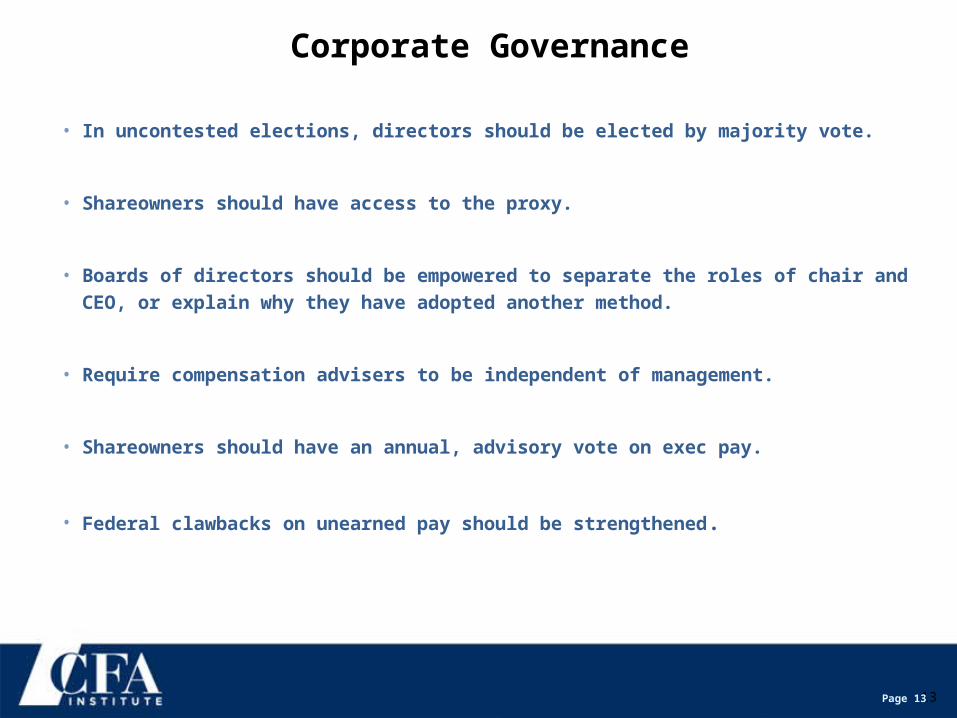

Corporate Governance

• In uncontested elections, directors should be elected by majority vote.

• Shareowners should have access to the proxy.

• Boards of directors should be empowered to separate the roles of chair and CEO, or explain why they have adopted another method.

• Require compensation advisers to be independent of management.

• Shareowners should have an annual, advisory vote on exec pay.

• Federal clawbacks on unearned pay should be strengthened.

Page 13

14

Systemic Risk Oversight Board

• Independent Systemic Risk Oversight Board that will supplement, not supplant, the functions of

existing federal financial regulators.

• Not a systemic risk regulator.

• The board’s budget should ensure its independence from financial firms and the entities setting

regulatory policy.

• All board members should be full-time and independent.

• The board should have a dedicated and highly skilled staff.

• This board should have the legal authority to gather all information that it deems is relevant to

systemic risk.

Page 14

15

Systemic Risk Oversight Board

The board would report to regulators any findings that require prompt action to relieve systemic pressures, and to make periodic reports to Congress and the public.

The board would offer regulators recommendations on appropriate action.

Regulators can implement the board's recommendations on a “comply or explain” basis.

Regulators in a better position to understand implications of regulatory action and when it might be appropriate to refine or modify a recommendation.

Under this approach, regulators could have the burden of either

(1) adopting and implementing the recommendation provided by the board,

(2) refining the recommendation as deemed necessary, or

(3) rejecting the recommendation.

Page 15

16

SEC Funding

House Provides SEC with Increased Budget

Senate Original draft provided SEC with self-

funding mechanism

IWG Position SEC should have (1) more stable long-

term funding and a (2) self funding mechanism that maintains sufficient resources and maintains independence. Funding should be removed from the Congressional approval process.

Page 16

17

OTC Derivatives

House Large number of transactions remain exempt from exchange trading and central

clearing.

Senate Original draft was similar to House Bill.

IWG Position IWG expressed need for more transparent and regulated market with very limited

exemptions to requirement for standardized contracts to trade on exchange and clear centrally. IWG would like federal oversight of derivatives and capital requirements for derivative activities.

Page 17

18

Regulation of Investment Managers

House Requires single fiduciary standard for all

giving investment advice, but exempts hedge funds with less than $150M AUM.

Senate Original draft appears to support single

fiduciary standard; also asks for study on feasibility. Requires private funds to register and report positions.

IWG Position IWG urges a requirement for all investment

managers- to register and be subject to SEC oversight. Such a system leads to better transparency and better understanding of systemic risk.

Page 18

19

NRSRO Oversight

House Increased internal controls, greater

transparency of rating process and methods, greater SEC enforcement and examinations. Includes provision for enhanced NRSRO liability.

Senate Original draft is similar to House Bill, but

with no liability language.

IWG Position IWG supports House bill liability language

in order to make NRSROs more accountable, to penalize fraud, not simple mistakes.

Page 19

20

Corporate Governance

House Allows for Proxy Access.

No majority vote standard.

Senate Original draft allows for Proxy Access

AND majority vote standard.

IWG Position Supports Proxy Access and majority

vote standard.

Page 20

21

Systematic Risk Oversight

House Creates Financial Services Oversight

Council

Senate Original draft called for Agency of

Financial Stability

IWG Position In both cases, the Fed, Treasury and the

same regulators who failed to prevent systemic failure in recent years would

play significant roles. IWG proposes a Systemic Risk Oversight Board that

would be supported by an independent full-time staff and experts to help it provide

unbiased and informed look at market risk.

Page 21

22

CFA Centre Meetings with Lawmakers/Regulators

CFA Centre Staff ongoing meetings with regulators and lawmakers

Met recently with Senators Warner and Corker staff

Corker’s office is taking a new approach to Systemic Risk Regulator that is closer to the recommendations made by IWG.

Dodd has assigned different bi-partisan teams to each section of his Discussion Draft

Mixed feelings on whether Dodd’s resignation will help or hurt bill

• Mark up in February?

• Goes to floor Mid-spring?

• Bill done by mid-July / or wait until next year?

Fiduciary Standard may be Dodd’s legacy

Page 22

23

Upcoming Regulatory Milestones 2010

Mark-up Senate Financial Market Regulatory Overhaul Bill – Feb

Bill goes to Senate floor – Mid-Spring or Delayed

Financial Regulation Bill – Mid-July or Delayed

Report of Financial Crisis Inquiry Comm. – Dec.

Page 23

24

Member Views on IWG Proposal for Hedge Funds

Page 24

Hedge funds should report their investment positions on a delayed basis to the general public to put investors on notice of potential systemic risk conditions. (N=727)

Hedge funds should report real-time positions to regulators to help them monitor and control potential systemic risk. (N=727)

Requiring these disclosures will cause hedge fund managers to relocate to markets where such disclosures are not required. (N=720)

Please indicate whether you agree or disagree with the following statements relating to the IWG's recommendations on hedge funds:Agree Disagree

49% 51%

61% 39%

56% 44%

25

Member Perspectives – September 2009 Survey

Page 25

In efforts to close this regulatory "gap", all standardized (and standardizable) derivative contracts that currently trade over the counter should...

Agree Disagree Support in theory but do not consider to be a feasible option

12%

be required to trade on regulated exchange. (N=739)

be required to clear centrally. (N=725)

10%

12%

78%68%

20%

26

Member Perspectives – September 2009 Survey

“Investors as a group will do a better job than any small group of ‘regulators’ as long as there is transparency and disclosure. Leverage seemed to be the real culprit so better regulation of those ratios seems appropriate. SEC, Fed, Congress, etc, etc can't prevent the next bubble from forming or bursting but more prudent systemic leverage would dampen the adverse consequences.”

Page 26

Thank You

Top Related