Languages

Pages

Legal

National & Regional Economic Outlook

The Alliance Bank Business Outreach Center 2014 Economic Outlook Conference

November 6, 2014

Ronald J. GundersonProfessor of EconomicsNorthern Arizona University

A Few Bright Spots

Gasoline prices have dropped sharplyRetail sales should improve as a resultNew job creation is better this year than in

several yearsConsumer Confidence is up!

2

Consumer Confidence Index

Date IndexOctober 2014 94.5

September 2014 89.0

October 2013 72.4

Most Recent Low

February 2009 25.3

Most Recent High

October 2007 95.2

3

Source: The Conference Board, October 2014 (90.0 represents healthy conditions)

The Current Picture

Wages are not keeping up so income hasn’t rebounded

Millions of persons are working part-time even though they would like to be full-time

It is taking longer to find jobs (structural unemployment)

People are still struggling with mortgage debt

Source: Boak & Rugaber, AP Economics Writers. August 1, 2014.

4

Wealth Without Workers; Workers Without Wealth

We are in the midst of an economic revolution, but this is not our first experience with a revolutionary environment.

Source: The Economist, October 4, 2014

5

The 19th century industrial revolution transformed the human condition, but for the typical wage-earner, this meant hard labor in crowded, disease-ridden cities.

It was nearly 100 years before the typical worker benefited from the revolution.Source: The Economist, October 4, 2014

6

Industrial Revolution

Digital Revolution

Today’s digital revolution is creating a similar situation worldwide, but we don’t have 100 years to find a solution.

Source: The Economist, October 4, 2014

7

Technology Changes

Technology has destroyed a large number of medium-skilled jobs

Increased the number of persons competing for lower-skilled jobs, while expanding the range of tasks that can be automated

Workers are competing against each other and against machines!

Source: The Economist, October 4, 2014

8

A Bold Response

Raise the productivity and employability of the less-skilled.

Revamp education, not just for the young, but adults need lifetime learning to keep up.

This will increase employability, but further advances in technology will keep wages low.

Source: The Economist, October 4, 2014

9

The Future

The market system thrives on finding new ways to do old things!

Joseph Schumpeter called this: Creative Destruction

Unless a market society continues to provide solutions to the downsides that accompany the benefits of new technology, Schumpeter felt capitalism will disappear.

10

Regional Economic Trends

Flagstaff & Northern Arizona

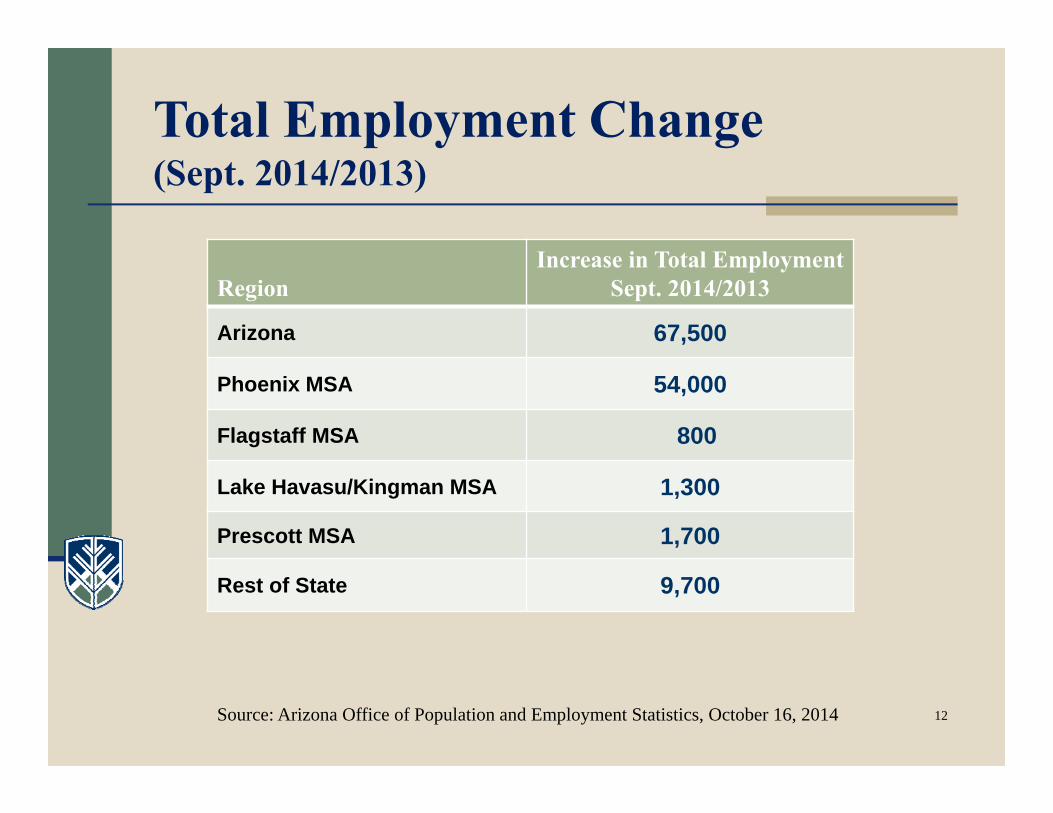

RegionIncrease in Total Employment

Sept. 2014/2013

Arizona 67,500

Phoenix MSA 54,000

Flagstaff MSA 800

Lake Havasu/Kingman MSA 1,300

Prescott MSA 1,700

Rest of State 9,700

Total Employment Change(Sept. 2014/2013)

Source: Arizona Office of Population and Employment Statistics, October 16, 2014 12

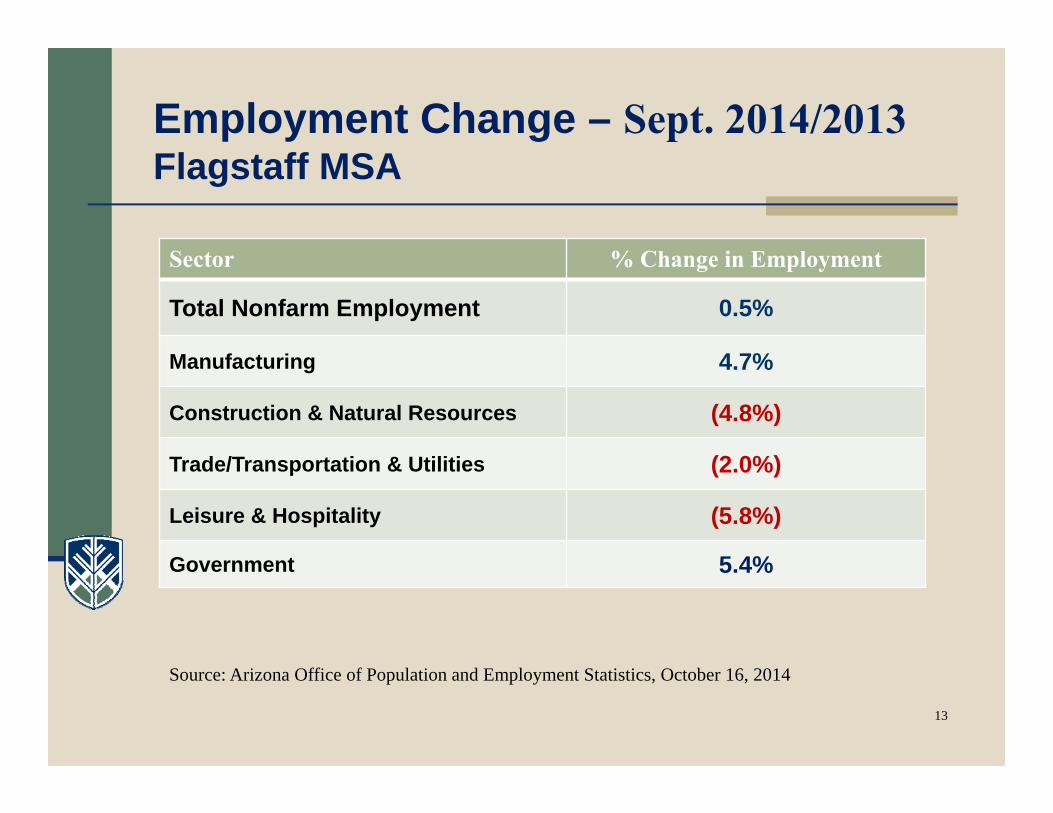

Sector % Change in Employment

Total Nonfarm Employment 0.5%

Manufacturing 4.7%

Construction & Natural Resources (4.8%)

Trade/Transportation & Utilities (2.0%)

Leisure & Hospitality (5.8%)

Government 5.4%

Employment Change – Sept. 2014/2013Flagstaff MSA

Source: Arizona Office of Population and Employment Statistics, October 16, 2014

13

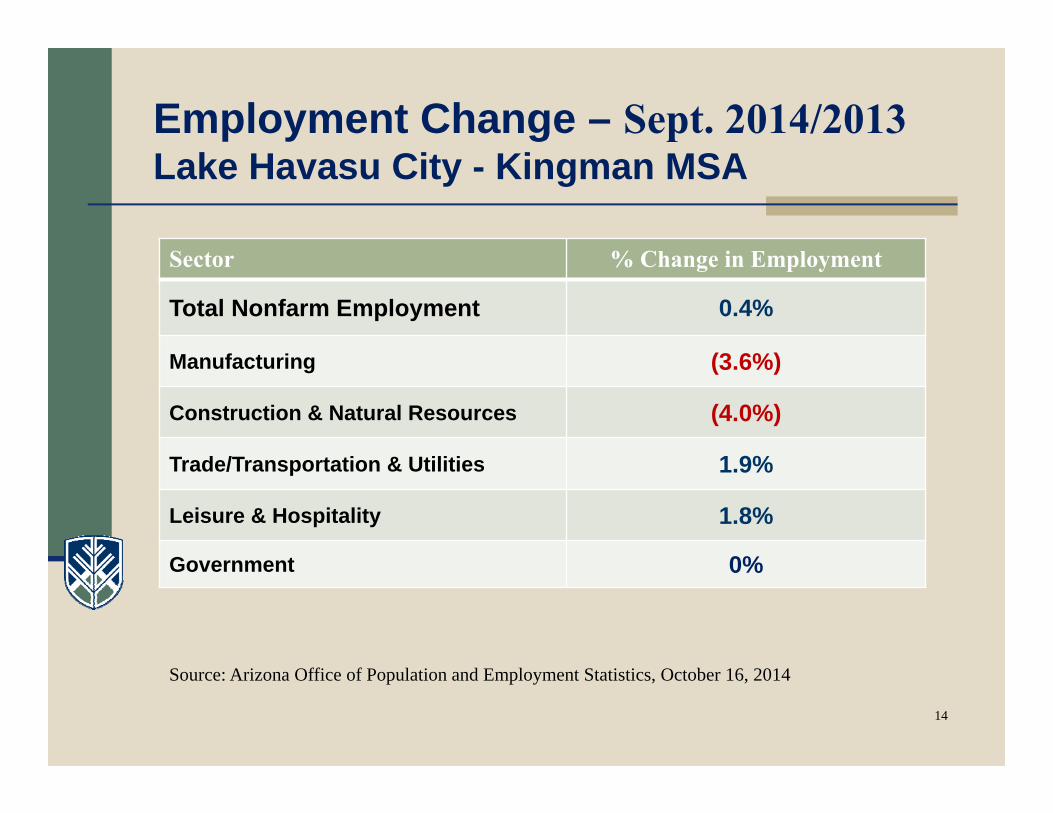

Sector % Change in Employment

Total Nonfarm Employment 0.4%

Manufacturing (3.6%)

Construction & Natural Resources (4.0%)

Trade/Transportation & Utilities 1.9%

Leisure & Hospitality 1.8%

Government 0%

Employment Change – Sept. 2014/2013Lake Havasu City - Kingman MSA

Source: Arizona Office of Population and Employment Statistics, October 16, 2014

14

Sector % Change in Employment

Total Nonfarm Employment 1.2%

Manufacturing 3.1%

Construction & Natural Resources 2.3%

Trade/Transportation & Utilities 5.2%

Leisure & Hospitality (4.9%)

Government 1.9%

Employment Change – Sept. 2014/2013Prescott MSA

Source: Arizona Office of Population and Employment Statistics, October 16, 2014

15

Flagstaff Real Estate (Overall market)

Median Single Family Home Price* September 2014 ---- $359,900

September 2013 ---- $305,000

September 2012 ---- $274,700

May 2007 ---- $399,750 (peak median price)

*The median price is often not the best measure because it largely reflects which part of the market is moving.

Source: Flagstaff Real Estate News, Ann Heitland, Remax Peak Properties, Various Issues.

16

Flagstaff Single Family Homes Median Sales Price

17

392,500 387,900

323,000338,950

297,000281,500 274,700

305,000

359,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Median Price ($) (September)

Flagstaff Real Estate (Overall Flagstaff Regional market)

Supply of Homes (Sept. 2014/2013) $0 – $200,000 fell from 2.1 months to 2.0 months

$200,000 – $300,000 rose from 2.8 months to 3.4 months

$300,000 – $400,000 stayed the same at 4.4 months

Flagstaff is still a sellers’ market up to $400,000.

The number of homes for sale in September rose 6.5% from a year ago.

18

Source: Flagstaff Real Estate News, Ann Heitland, Remax Peak Properties, Various Issues.

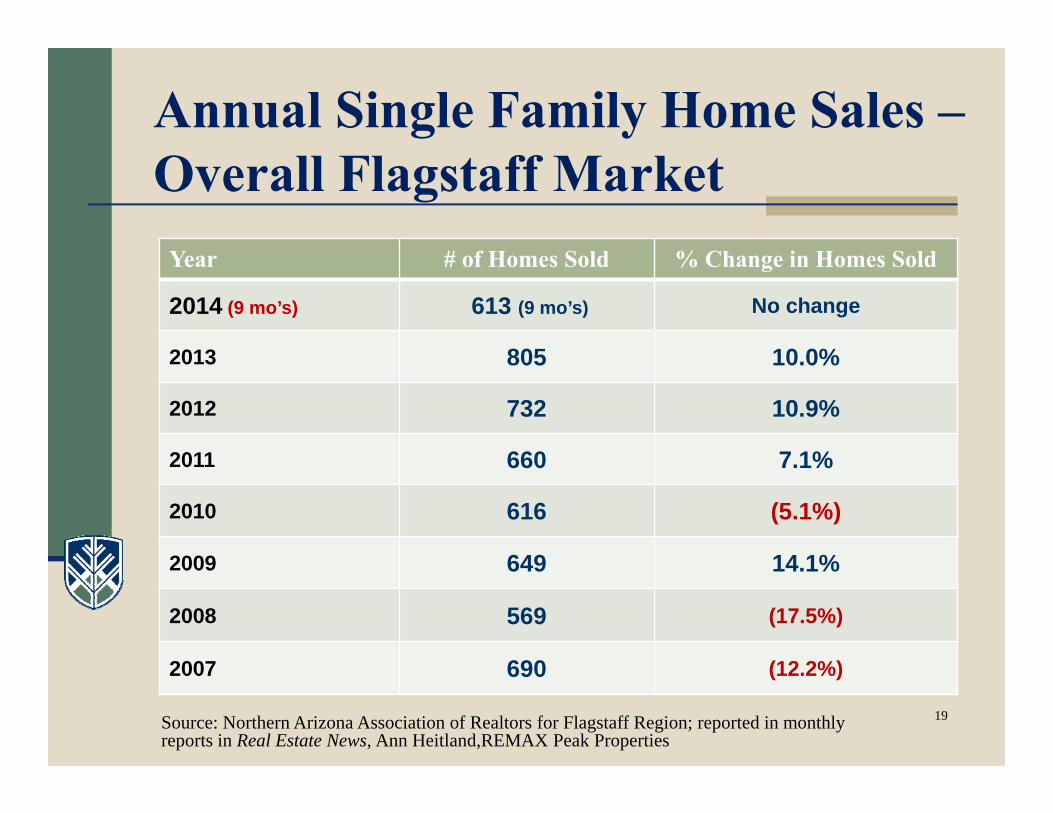

Year # of Homes Sold % Change in Homes Sold

2014 (9 mo’s) 613 (9 mo’s) No change

2013 805 10.0%

2012 732 10.9%

2011 660 7.1%

2010 616 (5.1%)

2009 649 14.1%

2008 569 (17.5%)

2007 690 (12.2%)

Annual Single Family Home Sales –Overall Flagstaff Market

Source: Northern Arizona Association of Realtors for Flagstaff Region; reported in monthly reports in Real Estate News, Ann Heitland,REMAX Peak Properties

19

Flagstaff Business Activity (FY 2015)Taxable Sales – July-September

Percent ChangeTaxable Business Activity from previous year

Total Business Activityw/o Utilities 6.6%

Auto Sales 11.3%

Construction 17.4%

BBB 7.2%

Other Retail 1.8%

Source: City of Flagstaff Sales Tax Division

Flagstaff Tax RevenuesTotal w/o Utilities

21

-6.32

3.29

2.04

6.84

3.51

6.62

FY 09-10 FY 10-11 FY 11-12 FY 12-13 FY 13-14 FY '15 (3 MO'S)

Percent ∆ From Previous Year

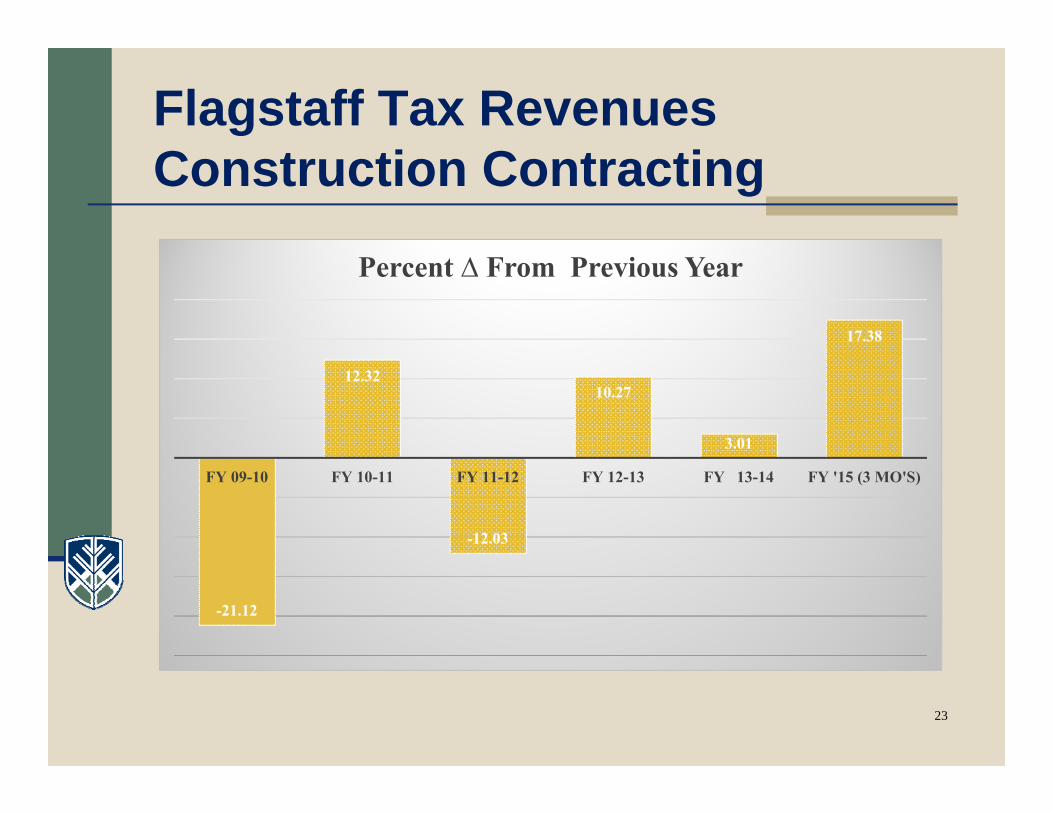

Flagstaff Tax RevenuesAuto Sales

22

3.38

18.3617.72

16.59

10.4211.28

FY 09-10 FY 10-11 FY 11-12 FY 12-13 FY 13-14 FY '15 (3 MO'S)

Percent ∆ From Previous Year

Flagstaff Tax RevenuesConstruction Contracting

23

-21.12

12.32

-12.03

10.27

3.01

17.38

FY 09-10 FY 10-11 FY 11-12 FY 12-13 FY 13-14 FY '15 (3 MO'S)

Percent ∆ From Previous Year

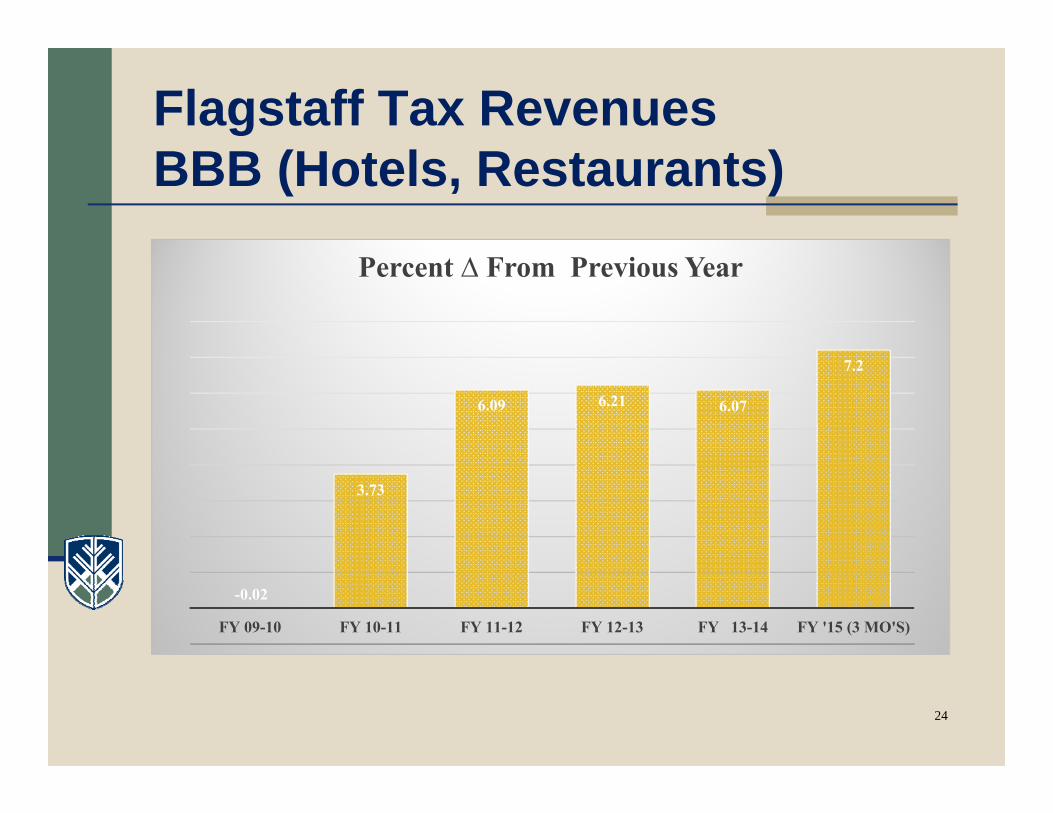

Flagstaff Tax RevenuesBBB (Hotels, Restaurants)

24

-0.02

3.73

6.09 6.21 6.07

7.2

FY 09-10 FY 10-11 FY 11-12 FY 12-13 FY 13-14 FY '15 (3 MO'S)

Percent ∆ From Previous Year

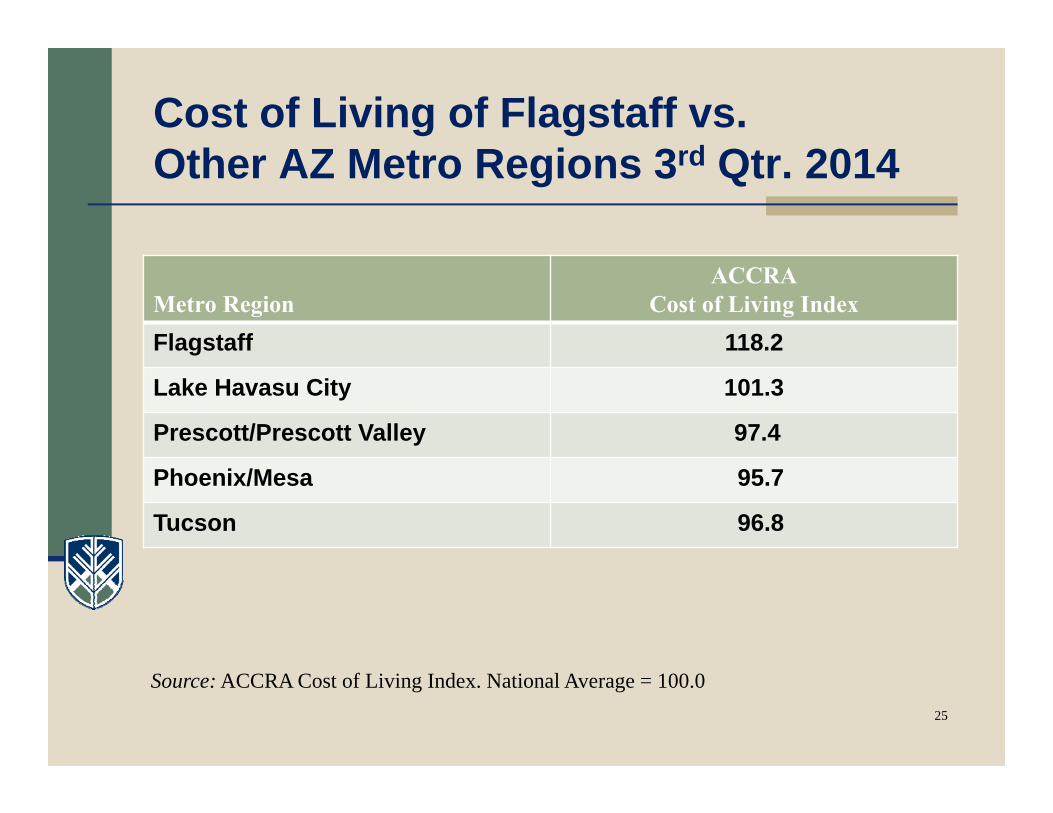

Cost of Living of Flagstaff vs.Other AZ Metro Regions 3rd Qtr. 2014

Metro RegionACCRA

Cost of Living IndexFlagstaff 118.2

Lake Havasu City 101.3

Prescott/Prescott Valley 97.4

Phoenix/Mesa 95.7

Tucson 96.8

Source: ACCRA Cost of Living Index. National Average = 100.025

Increased NAU Student Enrollment

NAU Enrollment – Mountain CampusFall 2014 20,134Fall 2013 19,320Fall 2012 18,431Fall 2011 17,761Fall 2010 17,529Fall 2009 16,032

Total increase since 2009: 4,102 students or >25%Source: NAU Office Planning and Institutional Research

Top Related