Languages

Pages

Legal

NASDAQ: MPET

October 2012

Building Shareholder Returns by

Maximizing the Potential of Currently Held Assets

1

Forward Looking Statements

Statements in this presentation which are not historical in nature are intended to be, and are hereby identified as, forward-looking statements for

purposes of the Private Securities Litigation Reform Act of 1995. These statements about Magellan and Magellan Petroleum Australia Limited

(“MPAL”) may relate to their businesses and prospects, revenues, expenses, operating cash flows, and other matters that involve a number of

uncertainties that may cause actual results to differ materially from expectations. Among these risks and uncertainties are the following: the future

outcome of the negotiations by Santos with its customers for gas sales contracts for the remaining uncontracted reserves in the Amadeus Basin; the

production volume at Mereenie and whether it will be sufficient to trigger the bonus amounts provided for in the Santos asset swap/sales agreement;

the ability of the Company to successfully develop its existing assets; the ability of the Company to secure gas sales contracts for the uncontracted

reserves at Dingo; the ability of the Company to implement a successful exploration program; pricing and production levels from the properties in

which Magellan and MPAL have interests; the extent of the recoverable reserves at those properties; the profitable integration of acquired businesses,

including Nautilus Poplar LLC; the likelihood of success of the drilling program at the Poplar Fields by the Company’s new farm-in partner, VAALCO

Energy; and the results of the ongoing production well tests in the U.K. In addition, MPAL has a large number of exploration permits and faces the risk

that any wells drilled may fail to encounter hydrocarbons in commercially recoverable quantities. Any forward-looking information provided in this

report should be considered with these factors in mind. Magellan assumes no obligation to update any forward-looking statements contained in this

report, whether as a result of new information, future events, or otherwise.

Oil and gas issuers are required to include disclosures regarding proved oil and gas reserves in certain filings made with the U.S. Securities and

Exchange Commission (“SEC”). Proved reserves are the estimated quantities of crude oil, natural gas, and natural gas liquids which geological and

engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and

operating conditions, i.e., prices and costs as of the date the estimate is made. The SEC also permits the disclosure of probable and possible

reserves which are additional reserves that are less certain to be recovered. Investors are urged to consider closely the disclosures in Magellan’s

periodic filings with the SEC available from us at the Company’s website, www.magellanpetroleum.com.

2

Magellan is…

…executing a turnaround strategy focused on maximizing the value of

existing oil and gas assets in the United States, Australia, and the

United Kingdom

3

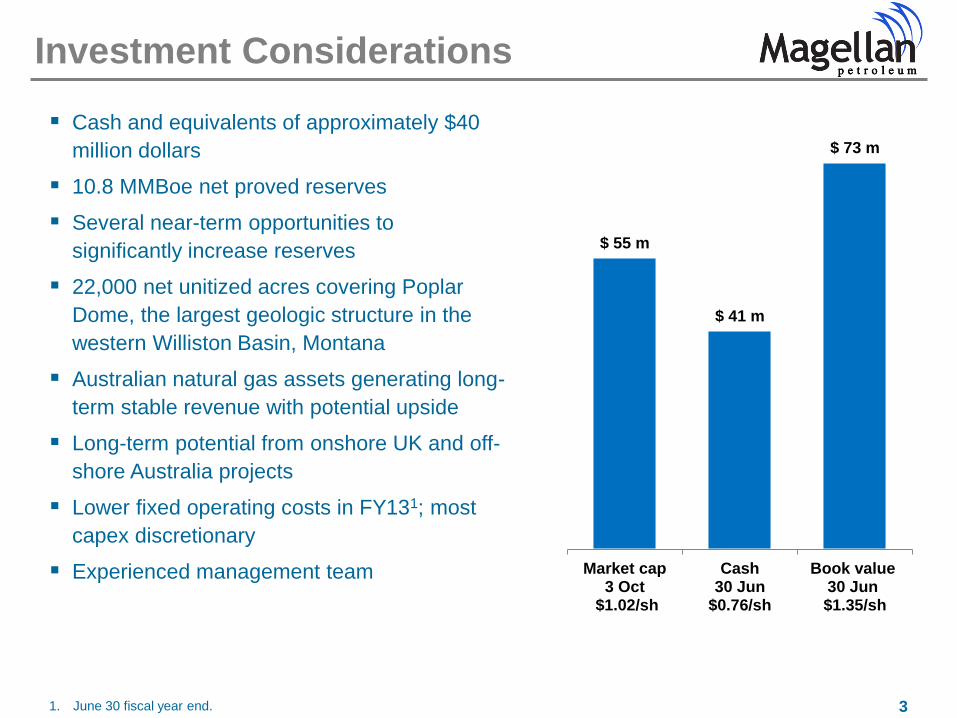

Investment Considerations

Cash and equivalents of approximately $40

million dollars

10.8 MMBoe net proved reserves

Several near-term opportunities to

significantly increase reserves

22,000 net unitized acres covering Poplar

Dome, the largest geologic structure in the

western Williston Basin, Montana

Australian natural gas assets generating long-

term stable revenue with potential upside

Long-term potential from onshore UK and off-

shore Australia projects

Lower fixed operating costs in FY131; most

capex discretionary

Experienced management team

1. June 30 fiscal year end.

$ 55 m

$ 41 m

$ 73 m

Market cap3 Oct

$1.02/sh

Cash30 Jun

$0.76/sh

Book value30 Jun

$1.35/sh

4

Turnaround Leadership

Robin West (66) – Chairman

Founder, CEO of PFC Energy

Former Reagan Administration Assistant

Secretary of the Interior (1981-83),

responsible for U.S. offshore oil policy

Member of National Petroleum Council and

Council on Foreign Relations

Director of Key Energy Services and

formerly of Cheniere Energy

Tom Wilson (60) – CEO

Former President of KMOC and Anderman

International

Former First Vice President and director of

Young Energy Prize

Previously, led new international strategy

for Apache and served as a Project

Manager for Shell Oil

Mark Brannum (46) – General Counsel &

Secretary

Former Deputy General Counsel of SM

Energy Company

Previously, a shareholder with Winstead

P.C., a large business law firm based in

Dallas, TX

Over 17 years of in-house and outside

counsel legal experience

Antoine Lafargue (38) – CFO

Former CFO of Falcon Gas Storage based

in Houston, TX

Previously, a principal with Arcapita, a

private equity fund focused on the energy

and infrastructure sectors

Previously held investment banking

positions with DLJ/Credit Suisse and Bank

of America

5

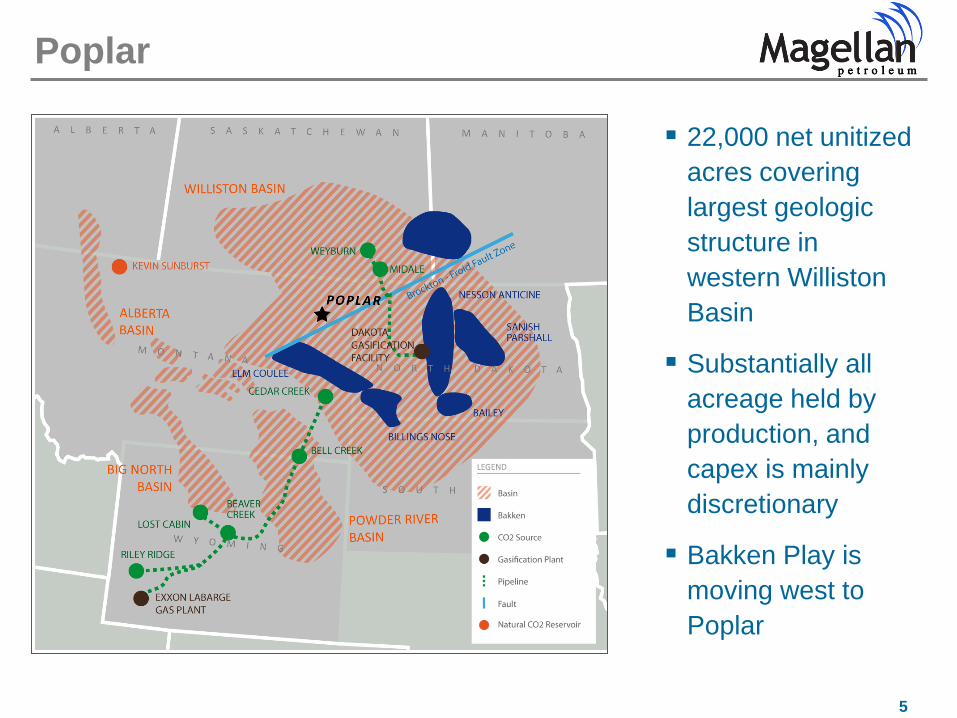

Poplar

22,000 net unitized

acres covering

largest geologic

structure in

western Williston

Basin

Substantially all

acreage held by

production, and

capex is mainly

discretionary

Bakken Play is

moving west to

Poplar

6

Poplar

Judith River

Shallow gas opportunity

Greenhorn

Oil potential – similar to Eagleford play

Amsden

New oil pool discovery Jan 12

1 producing well; currently planning

development strategy

Tyler

4 current wells

Additional potential

Charles

Approximately 250 bbls/day

CO2-EOR: pilot project in FY13

Several reserve development opportunities

7

Poplar – VAALCO Farm-Out

VAALCO farm-out in Sep 2011 to explore and develop deeper

formations at Poplar

– 100% carry for 3 wells in calendar 2012

– 35% interest in all wells to Magellan

Objective and rationale:

– Prove up reserves and value of deeper formations of Poplar, with

limited capital exposure through the exploration phase

– Remain focused on Charles and shallower formations

– Benefit from VAALCO’s horizontal well drilling expertise

Timing:

– First well drilled in Q1; no commercial quantities of hydrocarbons

below the Bakken/Three Forks formation; well temporarily suspended

– Second well completed in Q3 as a horizontal well to test

Bakken/Three Forks; found to be water-bearing; well temporarily

suspended to evaluate options

8

Poplar – CO2 Enhanced Oil Recovery

Evidence points to Charles formation being a prime candidate for a

CO2 enhanced oil recovery program

Offers the potential to increase reserves from current 10 MMbbls to 40

to 60 MMbbls

Laboratory tests confirm oil from Charles formation has requisite

miscibility for successful CO2 enhancement

Project assessment milestones:

– Laboratory tests complete; all results positive

– 5 well pilot project to start in FY13

Potential additional proved reserves of 30 to 50 MMbbls

9

Australian Onshore Assets

Palm Valley

145 km SW of Alice Springs

11 Bcf of proved gas reserves

and 14 Bcf of probable gas

reserves

~$100 m revenue contract over

17 years with price upside

100% owner / operator

Connected to Darwin pipeline

Dingo

65 km south of Alice Springs

Material gas resource

3 appraisal wells (’84 and ’90)

100% owner / operator

Marketing gas to mining industry

Mereenie

Opportunity to earn up to A$17.5

million in bonus payments from

Santos

10

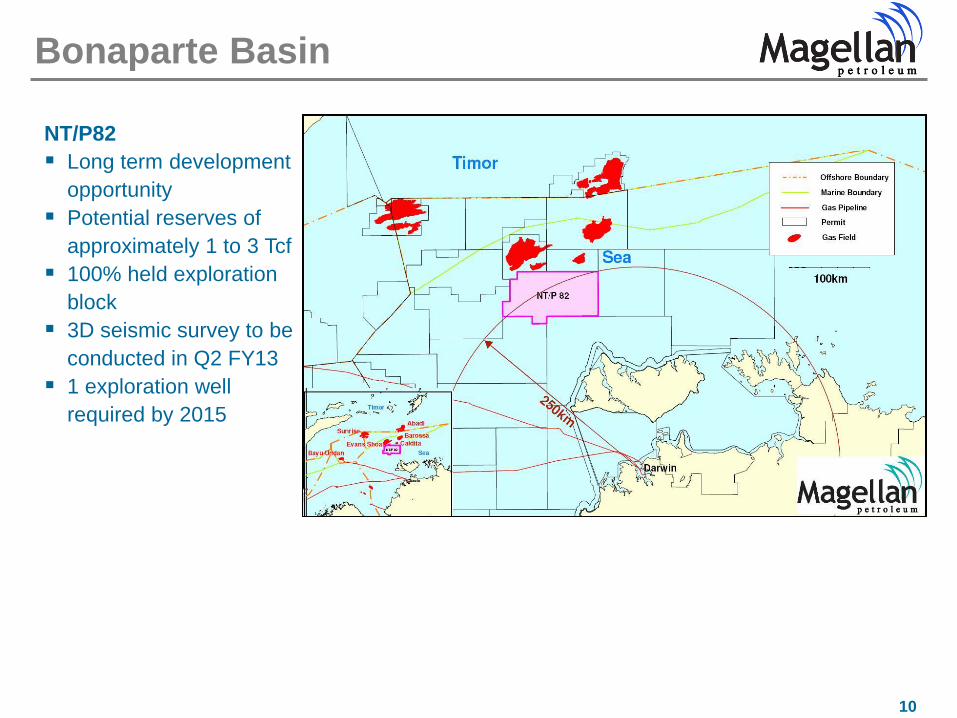

Bonaparte Basin

NT/P82

Long term development

opportunity

Potential reserves of

approximately 1 to 3 Tcf

100% held exploration

block

3D seismic survey to be

conducted in Q2 FY13

1 exploration well

required by 2015

11

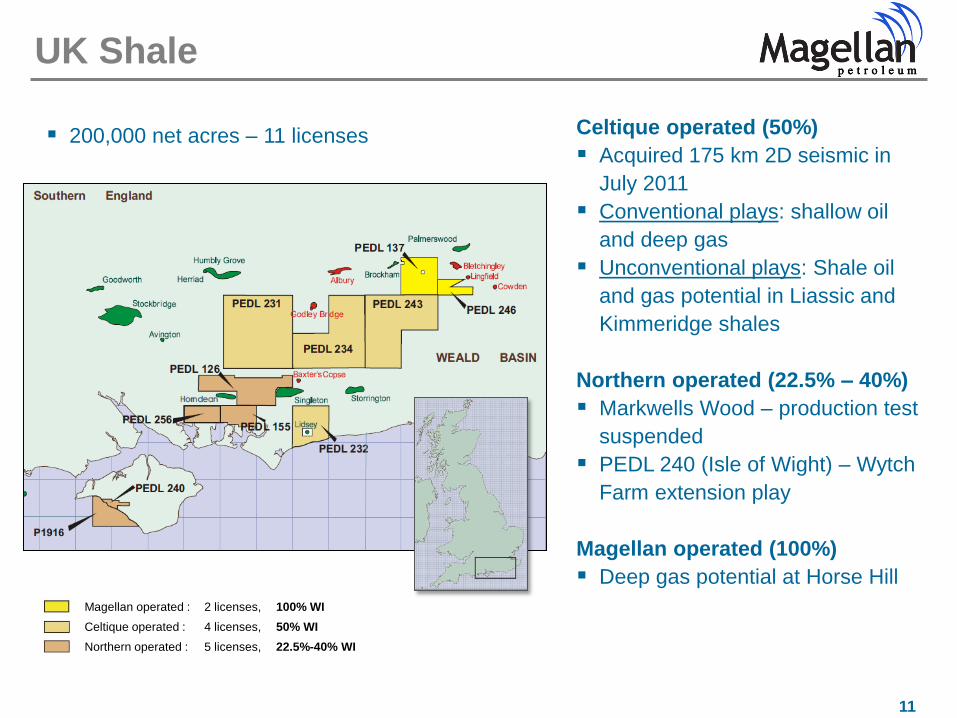

UK Shale

Celtique operated (50%)

Acquired 175 km 2D seismic in

July 2011

Conventional plays: shallow oil

and deep gas

Unconventional plays: Shale oil

and gas potential in Liassic and

Kimmeridge shales

Northern operated (22.5% – 40%)

Markwells Wood – production test

suspended

PEDL 240 (Isle of Wight) – Wytch

Farm extension play

Magellan operated (100%)

Deep gas potential at Horse Hill

200,000 net acres – 11 licenses

Magellan operated : 2 licenses, 100% WI

Celtique operated : 4 licenses, 50% WI

Northern operated : 5 licenses, 22.5%-40% WI

12

Historical Financials1

1. June 30 fiscal year end.

2. See Appendix: EBITDAX Reconciliation for reconciliation to net income and for further information on EBITDAX.

Production

Oil (Mbbls) 139 123 122

Gas (Bcf) 3.4 0.7 0.4

Total (Mboe) 711 241 196

boepd 1,947 661 537

28.5

18.2

13.7

(1.4)

(32.4)

26.5

7.4

(4.8)

(11.2)

FY10 FY11 FY12

$ m

Revenue Net income (loss) EBITDAX (2)

13

Operational Milestones

Milestone Cost FY2013 FY2014

Dec Mar Jun

Poplar

CO2-EOR – 5-well pilot ~$10 m

VAALCO/Deep Rights – test wells -

Charles formation – various testing

Australia

NT/P82 – 3D seismic ~$5 m

Palm Valley – new gas contracts -

Dingo – develop marketing strategy -

UK

Development assessment

14

Poised for Improved Cash Flow

12-Month revenue enhancement opportunities

Replacement gas contracts for Palm Valley

Increased Charles production

Amsden potential production

Poplar deep interval potential production

12-Month operating cost savings

Lower Palm Valley operating costs

Eliminated Mereenie operating costs

Reduced G&A expenses

Australian stock exchange listing expenses

Appendix

16

Adjusted EBITDAX Reconciliation

We define Adjusted EBITDAX as net income (loss) attributable to Magellan, plus (i) depletion, depreciation, amortization, and accretion expense, (ii) exploration expense, (iii) stock

based compensation expense, (iv) foreign transaction loss (gain), (v) impairment expense, (vi) loss on Evans Shoal, (vii) gain on sale of assets, (viii) warrant expense, (ix) net interest

income, (x) other income, (xi) income tax benefit (provision), and net (loss) income attributable to non-controlling interest in subsidiaries. Adjusted EBITDAX is not a measure of net

income or cash flow as determined by accounting principles generally accepted in the United States ("GAAP"), and excludes certain items that we believe affect the comparability of

operating results.

Our Adjusted EBITDAX measure provides additional information which may be used to better understand our operations. Adjusted EBITDAX is one of several metrics that we use as

a supplemental financial measurement in the evaluation of our business and should not be considered as an alternative to, or more meaningful than, net income (loss) as an indicator

of our operating performance. Certain items excluded from Adjusted EBITDAX are significant components in understanding and assessing a company's financial performance, such

as the historic cost of depreciable and depletable assets. Adjusted EBITDAX, as used by us, may not be comparable to similarly titled measures reported by other companies. We

believe that Adjusted EBITDAX is a widely followed measure of operating performance and is one of many metrics used by our management team and by other users of our

consolidated financial statements. For example, Adjusted EBITDAX can be used to assess our operating performance and return on capital in comparison to other independent

exploration and production companies without regard to financial or capital structure, and to assess the financial performance of our assets and our company without regard to

historical cost basis and items affecting the comparability of period to period operating results.

Adjusted EBITDAX: Non-GAAP financial measure reconciliation to net income (loss)

Fiscal Years Ended June 30,

2012 2011 2010

(In thousands)

Net (loss) attributable to Magellan $ 26,498 $ (32,432) $ (1,446)

Depletion, depreciation, amortization, and accretion expense 1,744 2,890 5,428

Exploration expense 6,291 2,854 1,273

Stock-based compensation expense 1,560 1,670 2,305

Foreign transaction (gain) loss (475) 951 677

Impairment expense 328 173 2,050

Loss on Evans Shoal - 15,893 -

(Gain) on sale of assets (40,413) (969) (6,817)

Warrant expense - - 4,276

Net interest (income) (749) (923) (1,038)

Other (income) (9) - (1,975)

Income tax (benefit) provision (5,951) 5,141 2,646

Net (loss) income attributable to non-controlling interest in subsidiaries (15) (5) (11)

Adjusted EBITDAX $ (11,191) $ (4,757) $ 7,368

Top Related