Languages

Pages

Legal

1

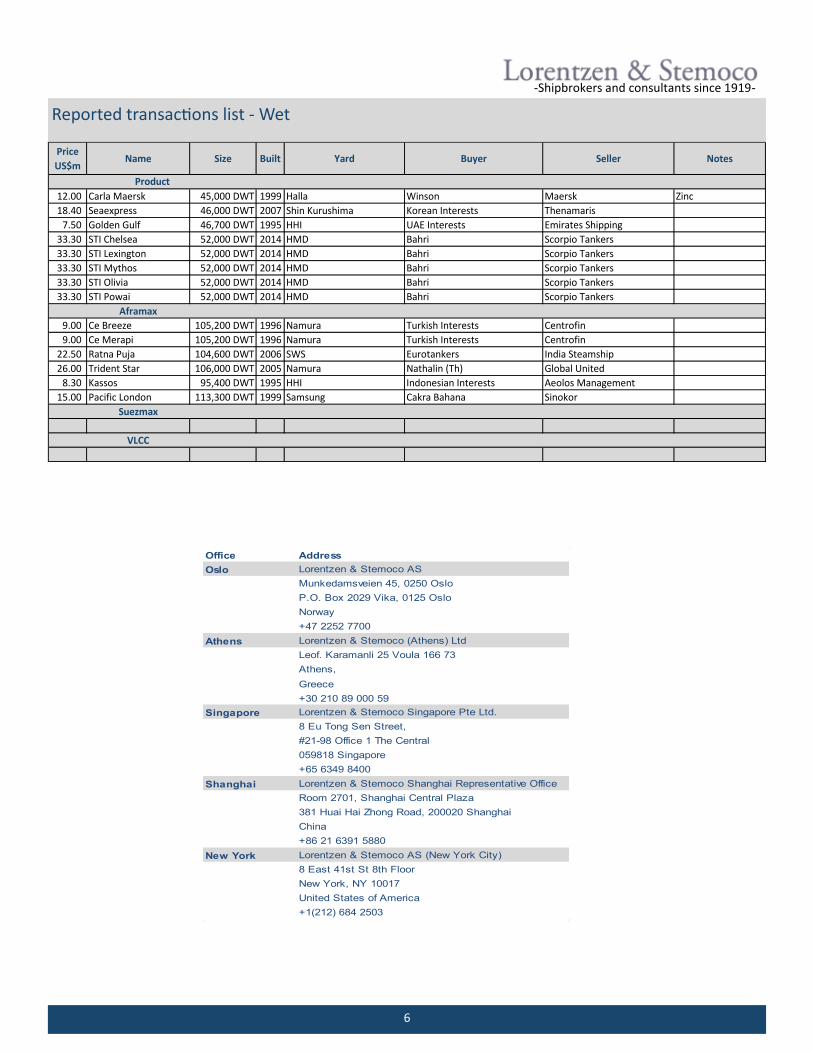

With so much of the S&P mar-ket dominated by dry cargo, it has been “All Quiet on the Western Front” regarding tank-ers. Crude tanker rates remain healthy although slightly vola-tile from week to week. Prod-uct tankers are extremely healthy and stable both for CPP and DPP cargos. Healthy rates combined with a lack of bank finance leads to the relative inactivity we have seen of late the S&P market. We have start-ed to see a change where own-ers of crude carriers start re-ducing prices and we expect this trend to continue. We un-derstand the Sea Express (46k dwt, 2007 built, Shin Kurashi-ma) has been committed for region US$ 18.4 mill. Please see more sales at the end of this report.

The latest deals give a clear picture of how much asset val-ues have dropped while cash-rich owners seem to be back for bargain hunting.

This makes it interesting to see how much the market values quality 2009-built units (non-Chinese) for all segments.

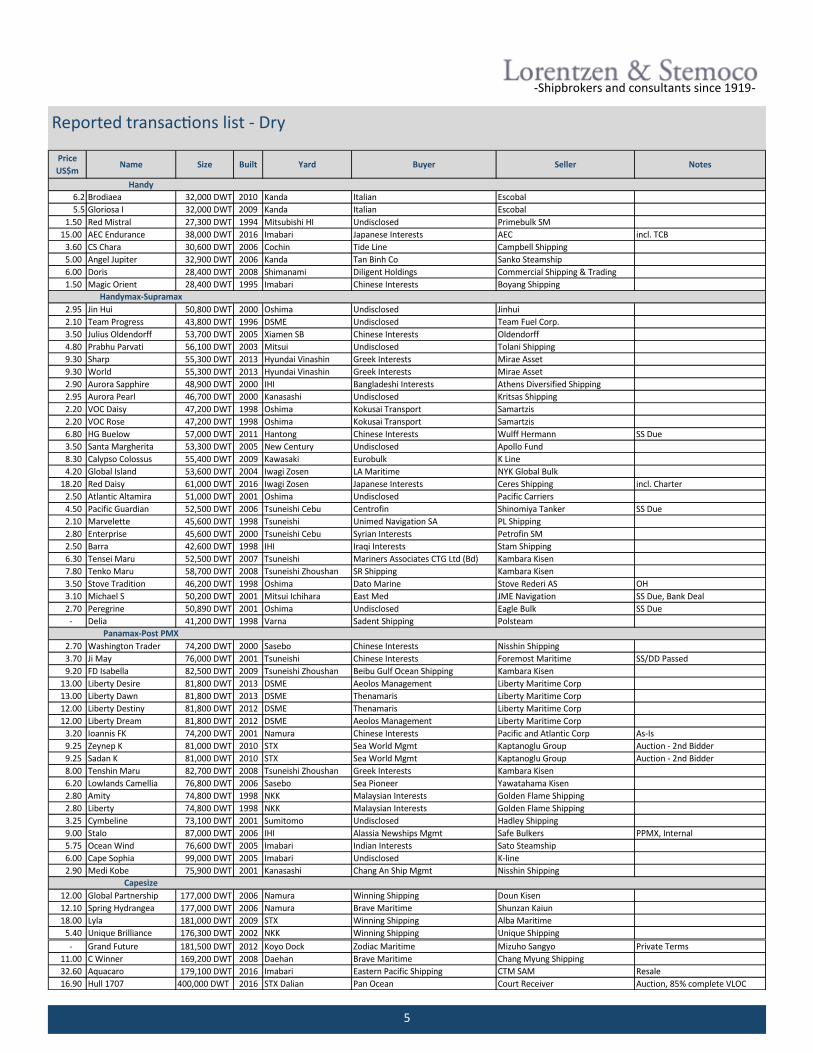

Such recent sales include the 181k dwt Capesize “Lyla” (2009 built, STX), committed to Win-ning at US$ 18m. The 82k dwt Kamsarmax “FD Isabella” (2009 built, Tsuneishi) committed to

Beibu Gulf Ocean Shipping (Chinese) at US$ 9.2m. The 55k dwt Supramaz “Calypso Colos-sus” (2009 built, Kawasaki) committed to Eurobulk / Pittas at US$ 8.3m. And the 32k dwt “Gloriosa I” (2009 built, Kanda) to Nova Carriers at US$ 5.5m.

The market is showing great interest for 13,000 dwt coated IMO2 tankers, of the Korean design which so many Owners were contracting before the crash.

We’re however seeing a mis-match between seller and buy-er expectations, causing us to expect prices to move north-wards, although the charter market is turning slightly softer.

Tristar picked up five chemical tankers in their acquisition of the remaining Eships fleet, whilst Team Tankers and Monjasa have also been active in the S&P market.

The spot market for VLGCs con-tinued to fall this month. Down 78% from peak in July 2015, the Baltic LPG Index now quotes US$29 basis the base route of 44’ mtons from Ras Tanura to Chiba, quite a dramatic fall. This year, one VLGC newbuilding is being delivered every week, and even with the substantial steady increase in LPG produc-tion, the supply of tonnage seems a bit over the top. At the same time shipyards are strug-gling to secure new orders, putting newbuilding prices fur-ther under pressure. Coupled with a weaker spot market, this is also causing second hand values to fall. We expect the spot market to recover, but not to the heights of last year. New-building prices will remain un-der strong pressure with likely further downward risk. With little activity in the market this month, there is only one new-building to report as SK Ship-ping declared an optional vessel at Hyundai HI, at a reported price of US$76m for delivery in 2018. Turkish owner Negmar Denizcilik is reported to have sold the handysize LPG carrier “Gas Master” (1985 built, Boel Verf) for demolition in India at a price of US$2.6m.

HIGHLIGHTS

Crude: Sellers

starting to reduce

prices

Dry: Latest deals

provide clearer

value picture

Chemical: S&P

interest focusing

on 13,000dwt

coated vessels

Gas: Little S&P

activity as market

drops and values

come under

pressure

March 2016

Dry

Crude/Product

Chemical

Gas

Monthly S&P Report

-Shipbrokers and consultants since 1919-

Hot Hulls

2

-Shipbrokers and consultants since 1919- Special Report

Tanker values in stagnant growth trajectory

Low crude prices, increasing demand, and longer haul trades

have been ramping up crude tanker earnings since the middle

of 2014. WS 100 was reached on the TD3 in March, and earn-

ings have been above US$100,000/day for VLCCs. In the past,

such strength in the physical tanker market would have played

through to asset values, increasing potential profit from asset

plays and attracting marginal players to the market. This time

around, a number of factors playing in from the peripheral ship-

ping industry and capital markets are hindering upwards devel-

opment in values.

The dry bulk and offshore markets are negatively impacting

tanker values in more than one way. With a slump in dry bulk

ordering, yards have been lowering newbuilding prices to

attract more orders, effectively putting a cap on the upwards

potential in second hand tanker values. This alone is however

not enough to restrict asset appreciation, and a larger part of

the story is painted by the drought in the capital markets where

shipping is concerned. Although banks are seen as returning to

the shipping equity market in spite of the blow to their shipping

portfolios by distressed shipping segments, their focus is in-

creasingly limited to less risky, strong industrial players instead

of marginal actors looking to take advantage of asset play. Simi-

larly, more risk-taking private equity funds active in the market

during the past few years are increasingly distancing them-

selves, as initial investments have mostly failed to provide ex-

pected returns, dis-incentivizing further investments.

Additionally, the weakness in other shipping sectors is causing

the equity market to discount stocks of public tanker owners in

response. According to L&S estimates, with the stock of most

public tanker owners trading at below NAV, the implied value of

a 5 year old VLCC is only around 80% of what the S&P market

estimates as fair value for such a vessel. With shares at discount

to NAV at the moment, it is making more sense to buy shares

than steel, highlighting the reason we are hearing a number of

owners speculating in share buybacks as a better option to in-

crease equity.

For the many owners with exposure to dry bulk and tanker seg-

ments, earnings from the tanker side of operations will likely be

put towards subsidizing loss-making dry bulk operations than go

towards funding new tanker acquisitions. We believe shares

trading at a discount to NAV should be taken as a ripple effect

of investors eying the dry bulk market with an unfavorable

view, rather than an underlying sentiment that the strength in

tankers is about to fold.

It seems likely that values will continue to come under pressure

as the pace of tanker deliveries picks up in the second half of

the year, and access to capital remains difficult. When the

bottom in prices is reached, which we think will happen after

the summer, the market will be interested to see who has got

the balance sheet strength to take advantage of apparent op-

portunities.

3

-Shipbrokers and consultants since 1919-

Time charter estimates Vessel values

VLGC US$/month Values US$m March 20161 yr TC 900,000 NB 75

8 yr 69

Capesize US$/day Values US$m (Japan/Korea) March 2016Spot rate 2,518 NB 481 yr TC 5,000-7,000 5 yr 222 Yr TC - 10 yr 12

Panamax US$/day Values US$m (Japan/Korea) March 2016Spot rate 4,008 NB 221 yr TC 5,500 5 yr 112 Yr TC - 10 yr 7

VLCC US$/day Values US$m (Japan/Korea) March 2016Spot rate 60,500 NB 931 yr TC 43,000 5 yr 762 Yr TC 42,000 10 yr 55

Suezmax US$/day Values US$m (Japan/Korea) March 2016Spot rate 25,900 NB 631 yr TC 32,000 5 yr 542 Yr TC 30,000 10 yr 40

Aframax US$/day Values US$m (Japan/Korea) March 2016Spot rate 28,500 NB 501 yr TC 24,000 5 yr 432 Yr TC 23,500 10 yr 28.5

LR2 US$/day Values US$m (Japan/Korea) March 2016Spot rate 20,000 NB 521 yr TC 25,000 5 yr 452 Yr TC 23,500 10 yr 30.5

LR1 US$/day Values US$m (Japan/Korea) March 2016Spot rate 17,000 NB 461 yr TC 20,000 5 yr 372 Yr TC 20,000 10 yr 27

MR (IMO II/III) US$/day Values US$m (Japan/Korea) March 2016Spot rate 8,500 NB 36.51 yr TC 18,000 5 yr 282 Yr TC 17,000 10 yr 19

4

-Shipbrokers and consultants since 1919-

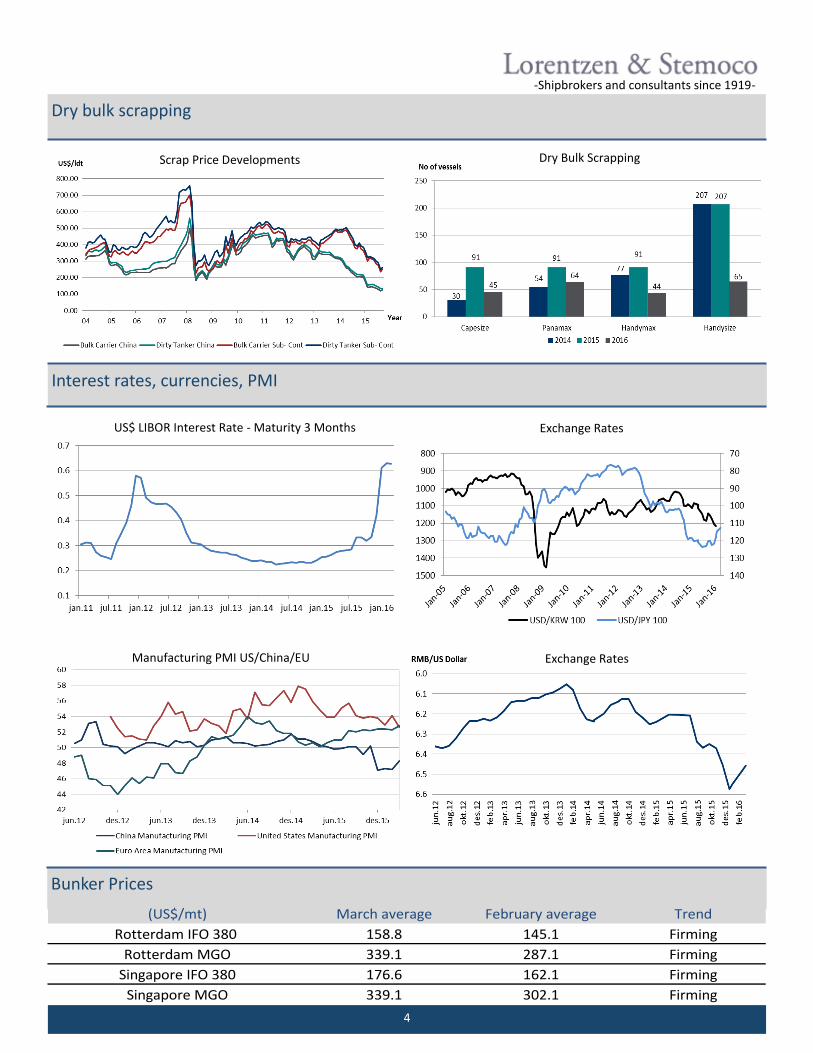

Dry bulk scrapping

Interest rates, currencies, PMI

Bunker Prices

Dry Bulk Scrapping Scrap Price Developments

US$ LIBOR Interest Rate - Maturity 3 Months Exchange Rates

Manufacturing PMI US/China/EU Exchange Rates

(US$/mt) March average February average Trend

Rotterdam IFO 380 158.8 145.1 Firming

Rotterdam MGO 339.1 287.1 Firming

Singapore IFO 380 176.6 162.1 Firming

Singapore MGO 339.1 302.1 Firming

5

Reported transactions list - Dry

-Shipbrokers and consultants since 1919-

- Grand Future 181,500 DWT 2012 Koyo Dock Zodiac Maritime Mizuho Sangyo Private Terms

11.00 C Winner 169,200 DWT 2008 Daehan Brave Maritime Chang Myung Shipping

32.60 Aquacaro 179,100 DWT 2016 Imabari Eastern Pacific Shipping CTM SAM Resale

16.90 Hull 1707 400,000 DWT 2016 STX Dalian Pan Ocean Court Receiver Auction, 85% complete VLOC

Price

US$mName Size Built Yard Buyer Seller Notes

6.2 Brodiaea 32,000 DWT 2010 Kanda Italian Escobal

5.5 Gloriosa I 32,000 DWT 2009 Kanda Italian Escobal

1.50 Red Mistral 27,300 DWT 1994 Mitsubishi HI Undisclosed Primebulk SM

15.00 AEC Endurance 38,000 DWT 2016 Imabari Japanese Interests AEC incl. TCB

3.60 CS Chara 30,600 DWT 2006 Cochin Tide Line Campbell Shipping

5.00 Angel Jupiter 32,900 DWT 2006 Kanda Tan Binh Co Sanko Steamship

6.00 Doris 28,400 DWT 2008 Shimanami Diligent Holdings Commercial Shipping & Trading

1.50 Magic Orient 28,400 DWT 1995 Imabari Chinese Interests Boyang Shipping

2.95 Jin Hui 50,800 DWT 2000 Oshima Undisclosed Jinhui

2.10 Team Progress 43,800 DWT 1996 DSME Undisclosed Team Fuel Corp.

3.50 Julius Oldendorff 53,700 DWT 2005 Xiamen SB Chinese Interests Oldendorff

4.80 Prabhu Parvati 56,100 DWT 2003 Mitsui Undisclosed Tolani Shipping

9.30 Sharp 55,300 DWT 2013 Hyundai Vinashin Greek Interests Mirae Asset

9.30 World 55,300 DWT 2013 Hyundai Vinashin Greek Interests Mirae Asset

2.90 Aurora Sapphire 48,900 DWT 2000 IHI Bangladeshi Interests Athens Diversified Shipping

2.95 Aurora Pearl 46,700 DWT 2000 Kanasashi Undisclosed Kritsas Shipping

2.20 VOC Daisy 47,200 DWT 1998 Oshima Kokusai Transport Samartzis

2.20 VOC Rose 47,200 DWT 1998 Oshima Kokusai Transport Samartzis

6.80 HG Buelow 57,000 DWT 2011 Hantong Chinese Interests Wulff Hermann SS Due

3.50 Santa Margherita 53,300 DWT 2005 New Century Undisclosed Apollo Fund

8.30 Calypso Colossus 55,400 DWT 2009 Kawasaki Eurobulk K Line

4.20 Global Island 53,600 DWT 2004 Iwagi Zosen LA Maritime NYK Global Bulk

18.20 Red Daisy 61,000 DWT 2016 Iwagi Zosen Japanese Interests Ceres Shipping incl. Charter

2.50 Atlantic Altamira 51,000 DWT 2001 Oshima Undisclosed Pacific Carriers

4.50 Pacific Guardian 52,500 DWT 2006 Tsuneishi Cebu Centrofin Shinomiya Tanker SS Due

2.10 Marvelette 45,600 DWT 1998 Tsuneishi Unimed Navigation SA PL Shipping

2.80 Enterprise 45,600 DWT 2000 Tsuneishi Cebu Syrian Interests Petrofin SM

2.50 Barra 42,600 DWT 1998 IHI Iraqi Interests Stam Shipping

6.30 Tensei Maru 52,500 DWT 2007 Tsuneishi Mariners Associates CTG Ltd (Bd) Kambara Kisen

7.80 Tenko Maru 58,700 DWT 2008 Tsuneishi Zhoushan SR Shipping Kambara Kisen

3.50 Stove Tradition 46,200 DWT 1998 Oshima Dato Marine Stove Rederi AS OH

3.10 Michael S 50,200 DWT 2001 Mitsui Ichihara East Med JME Navigation SS Due, Bank Deal

2.70 Peregrine 50,890 DWT 2001 Oshima Undisclosed Eagle Bulk SS Due

- Delia 41,200 DWT 1998 Varna Sadent Shipping Polsteam

2.70 Washington Trader 74,200 DWT 2000 Sasebo Chinese Interests Nisshin Shipping

3.70 Ji May 76,000 DWT 2001 Tsuneishi Chinese Interests Foremost Maritime SS/DD Passed

9.20 FD Isabella 82,500 DWT 2009 Tsuneishi Zhoushan Beibu Gulf Ocean Shipping Kambara Kisen

13.00 Liberty Desire 81,800 DWT 2013 DSME Aeolos Management Liberty Maritime Corp

13.00 Liberty Dawn 81,800 DWT 2013 DSME Thenamaris Liberty Maritime Corp

12.00 Liberty Destiny 81,800 DWT 2012 DSME Thenamaris Liberty Maritime Corp

12.00 Liberty Dream 81,800 DWT 2012 DSME Aeolos Management Liberty Maritime Corp

3.20 Ioannis FK 74,200 DWT 2001 Namura Chinese Interests Pacific and Atlantic Corp As-Is

9.25 Zeynep K 81,000 DWT 2010 STX Sea World Mgmt Kaptanoglu Group Auction - 2nd Bidder

9.25 Sadan K 81,000 DWT 2010 STX Sea World Mgmt Kaptanoglu Group Auction - 2nd Bidder

8.00 Tenshin Maru 82,700 DWT 2008 Tsuneishi Zhoushan Greek Interests Kambara Kisen

6.20 Lowlands Camellia 76,800 DWT 2006 Sasebo Sea Pioneer Yawatahama Kisen

2.80 Amity 74,800 DWT 1998 NKK Malaysian Interests Golden Flame Shipping

2.80 Liberty 74,800 DWT 1998 NKK Malaysian Interests Golden Flame Shipping

3.25 Cymbeline 73,100 DWT 2001 Sumitomo Undisclosed Hadley Shipping

9.00 Stalo 87,000 DWT 2006 IHI Alassia Newships Mgmt Safe Bulkers PPMX, Internal

5.75 Ocean Wind 76,600 DWT 2005 Imabari Indian Interests Sato Steamship

6.00 Cape Sophia 99,000 DWT 2005 Imabari Undisclosed K-line

2.90 Medi Kobe 75,900 DWT 2001 Kanasashi Chang An Ship Mgmt Nisshin Shipping

12.00 Global Partnership 177,000 DWT 2006 Namura Winning Shipping Doun Kisen

12.10 Spring Hydrangea 177,000 DWT 2006 Namura Brave Maritime Shunzan Kaiun

18.00 Lyla 181,000 DWT 2009 STX Winning Shipping Alba Maritime

5.40 Unique Brilliance 176,300 DWT 2002 NKK Winning Shipping Unique Shipping

Capesize

Handy

Handymax-Supramax

Panamax-Post PMX

6

Reported transactions list - Wet

-Shipbrokers and consultants since 1919-

Office Address

Oslo Lorentzen & Stemoco AS

Munkedamsveien 45, 0250 Oslo

P.O. Box 2029 Vika, 0125 Oslo

Norway

+47 2252 7700

Athens Lorentzen & Stemoco (Athens) Ltd

Leof. Karamanli 25 Voula 166 73

Athens,

Greece

+30 210 89 000 59

Singapore Lorentzen & Stemoco Singapore Pte Ltd.

8 Eu Tong Sen Street,

#21-98 Office 1 The Central

059818 Singapore

+65 6349 8400

Shanghai Lorentzen & Stemoco Shanghai Representative Office

Room 2701, Shanghai Central Plaza

381 Huai Hai Zhong Road, 200020 Shanghai

China

+86 21 6391 5880

New York Lorentzen & Stemoco AS (New York City)

8 East 41st St 8th Floor

New York, NY 10017

United States of America

+1(212) 684 2503

Price

US$mName Size Built Yard Buyer Seller Notes

12.00 Carla Maersk 45,000 DWT 1999 Halla Winson Maersk Zinc

18.40 Seaexpress 46,000 DWT 2007 Shin Kurushima Korean Interests Thenamaris

7.50 Golden Gulf 46,700 DWT 1995 HHI UAE Interests Emirates Shipping

33.30 STI Chelsea 52,000 DWT 2014 HMD Bahri Scorpio Tankers

33.30 STI Lexington 52,000 DWT 2014 HMD Bahri Scorpio Tankers

33.30 STI Mythos 52,000 DWT 2014 HMD Bahri Scorpio Tankers

33.30 STI Olivia 52,000 DWT 2014 HMD Bahri Scorpio Tankers

33.30 STI Powai 52,000 DWT 2014 HMD Bahri Scorpio Tankers

Aframax

9.00 Ce Breeze 105,200 DWT 1996 Namura Turkish Interests Centrofin

9.00 Ce Merapi 105,200 DWT 1996 Namura Turkish Interests Centrofin

22.50 Ratna Puja 104,600 DWT 2006 SWS Eurotankers India Steamship

26.00 Trident Star 106,000 DWT 2005 Namura Nathalin (Th) Global United

8.30 Kassos 95,400 DWT 1995 HHI Indonesian Interests Aeolos Management

15.00 Pacific London 113,300 DWT 1999 Samsung Cakra Bahana Sinokor

Suezmax

VLCC

Product

Top Related