Languages

Pages

Legal

© 2010 National Association of Publicly Traded Partnerships 1

Master LimitedPartnerships 101:

Presentation to the

American Association of Individual Investors

Silicon Valley Chapter

April 16, 2011

© 2011 National Association of Publicly Traded Partnerships 2

I. What is an MLP and why should I care?

II. History of MLPs

III. MLPs Today

IV. How MLPs Work

V. Investing in MLPs

VI. For more information…

Master Limited Partnerships 101

© 2011 National Association of Publicly Traded Partnerships 3

Master Limited Partnerships 101

What is a Master Limited Partnership? (MLP)

© 2011 National Association of Publicly Traded Partnerships 4

Master Limited Partnerships 101

• A more accurate term, and the one used in the tax code, is “publicly traded partnership.”

• Simply, it is a partnership, or an LLC that has chosen partnership taxation, that trades on a public exchange (NYSE, NASDAQ, AMEX) or over the counter market.

© 2011 National Association of Publicly Traded Partnerships 5

Master Limited Partnerships 101

Are master limited partnerships (MLPs) and

publicly traded partnerships (PTPs) the same thing?

© 2011 National Association of Publicly Traded Partnerships 6

Master Limited Partnerships 101

• Simple answer: For most purposes, yes. The two terms are used interchangeably.

• Technical answer: Technically, no. An MLP is a partnership with a certain structure, not necessarily publicly traded (though most are). And some PTPs are not MLPs, but publicly traded limited liability companies (LLCs) taxed as partnerships.

© 2011 National Association of Publicly Traded Partnerships 7

Master Limited Partnerships 101

Why should I know about

Master Limited Partnerships?

© 2011 National Association of Publicly Traded Partnerships 8

Master Limited Partnerships 101

The two biggest reasons:

• Income: Many investors are seeking investments that pay income regardless of share price fluctuations

• Tax Advantages: Because MLPs are partnerships, investors get more of the income and pay less tax on it.

© 2011 National Association of Publicly Traded Partnerships 9

Master Limited Partnerships 101

History of MLPsMaster limited partnerships have been around for almost three decades

© 2011 National Association of Publicly Traded Partnerships 10

• The first MLP was launched in 1981: Apache Oil Company.

• Its purpose was to raise capital from smaller investors by offering them a partnership investment in an affordable and liquid security.

• Other oil and gas MLPs soon followed and were joined by real estate MLPs.

History of MLPs

© 2011 National Association of Publicly Traded Partnerships 11

History of MLPs

Rapid Growth in the 1980s

• MLPs multiplied and began to be used in other industries: hotels and motels, restaurants, cable TV, investment advisors, even amusement parks and the Boston Celtics.

• Congress and tax officials worried about “disincorporation”--i.e., that large numbers of corporations would become MLPs to avoid corporate tax.

© 2011 National Association of Publicly Traded Partnerships 12

History of MLPs

In 1987 Congress passed legislation to define and limit publicly traded partnerships

• It created Section 7704 of the Tax Code, limiting partnership tax treatment to PTPs earning >90 percent of their income from specific sources.

• Existing PTPs with “bad” income were grand-fathered. Most gradually went private, were acquired or converted to other structures; only three remain today.

© 2011 National Association of Publicly Traded Partnerships 13

History of MLPs

What kinds of income can a PTP earn?

• Interest, dividends, and capital gains

• Rental income and capital gains from real estate

• Income and capital gains from natural resources activities

• Income from commodity investments

• Capital gains from sale of assets used to generate the above types of income

© 2011 National Association of Publicly Traded Partnerships 14

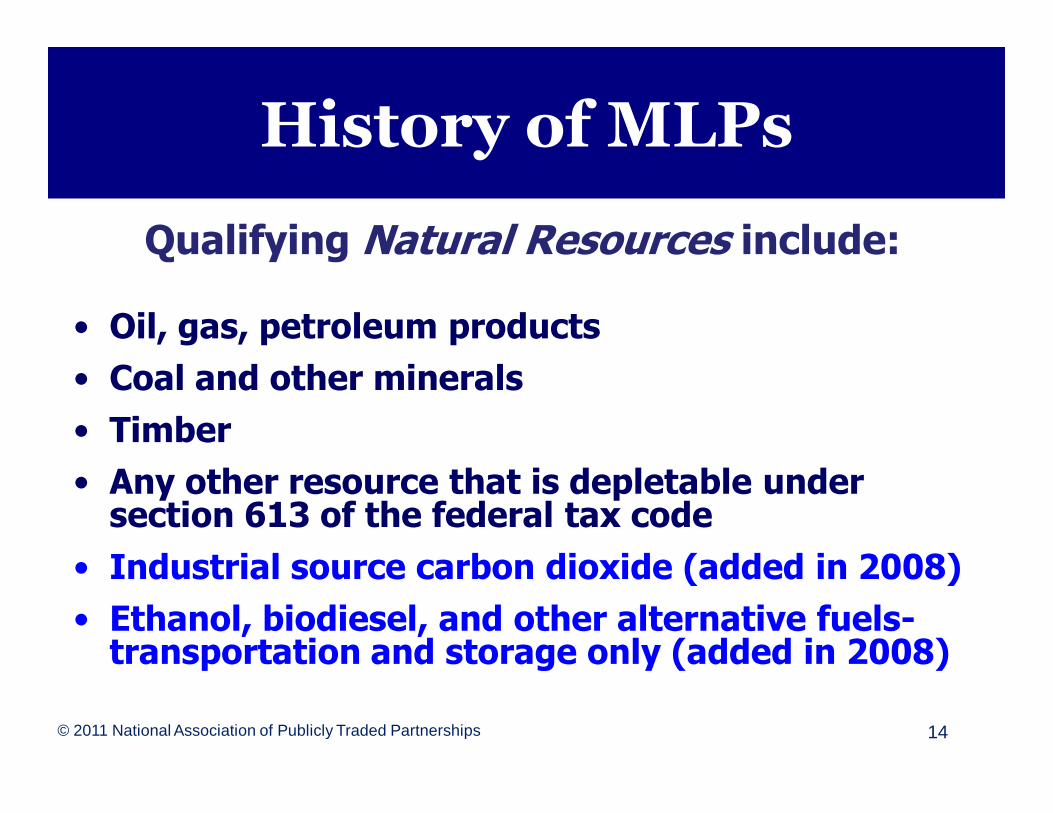

History of MLPs

Qualifying Natural Resources include:

• Oil, gas, petroleum products

• Coal and other minerals

• Timber

• Any other resource that is depletable under section 613 of the federal tax code

• Industrial source carbon dioxide (added in 2008)

• Ethanol, biodiesel, and other alternative fuels-transportation and storage only (added in 2008)

© 2011 National Association of Publicly Traded Partnerships 15

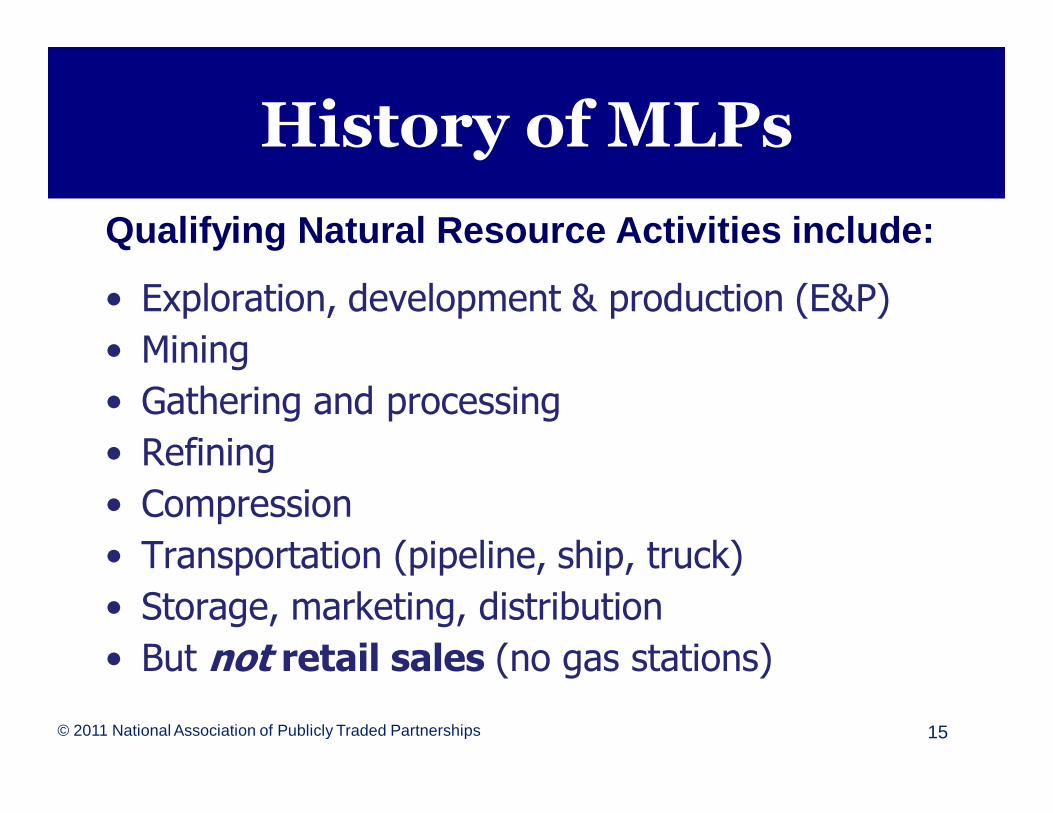

History of MLPs

• Exploration, development & production (E&P)

• Mining

• Gathering and processing

• Refining

• Compression

• Transportation (pipeline, ship, truck)

• Storage, marketing, distribution

• But not retail sales (no gas stations)

Qualifying Natural Resource Activities include:

© 2011 National Association of Publicly Traded Partnerships 16

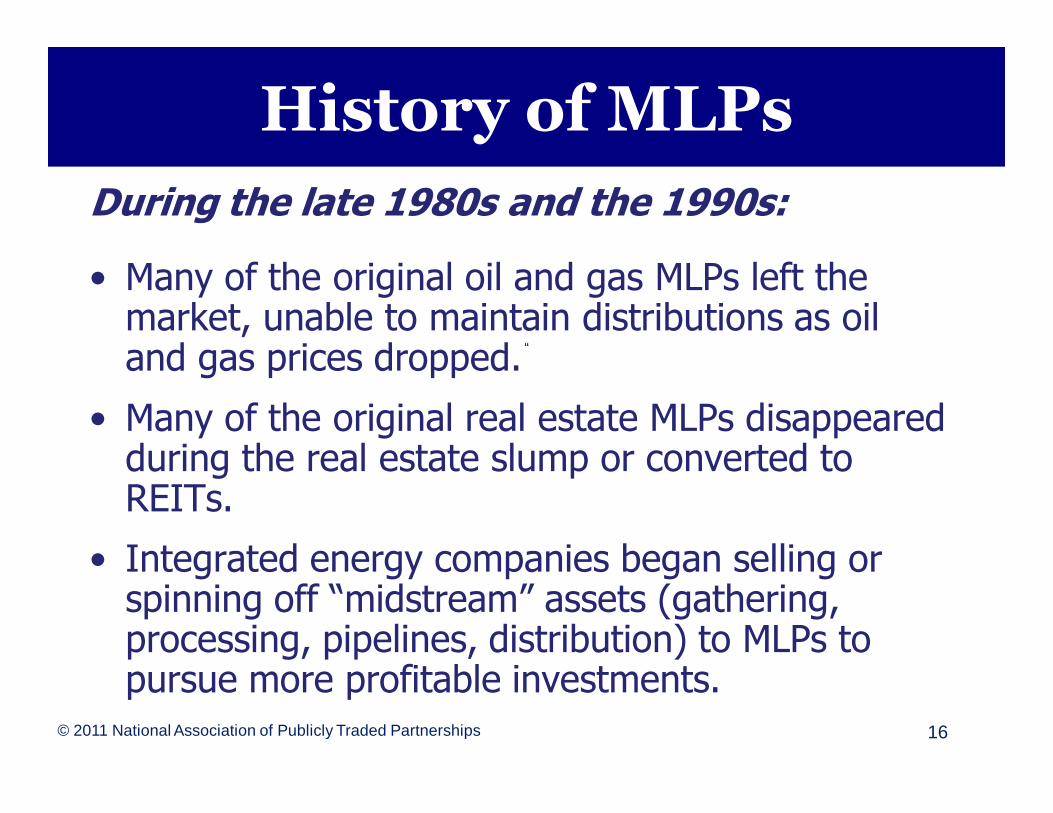

History of MLPs

During the late 1980s and the 1990s:

• Many of the original oil and gas MLPs left the market, unable to maintain distributions as oil and gas prices dropped.

• Many of the original real estate MLPs disappeared during the real estate slump or converted to REITs.

• Integrated energy companies began selling or spinning off “midstream” assets (gathering, processing, pipelines, distribution) to MLPs to pursue more profitable investments.

“

© 2011 National Association of Publicly Traded Partnerships 17

History of MLPs

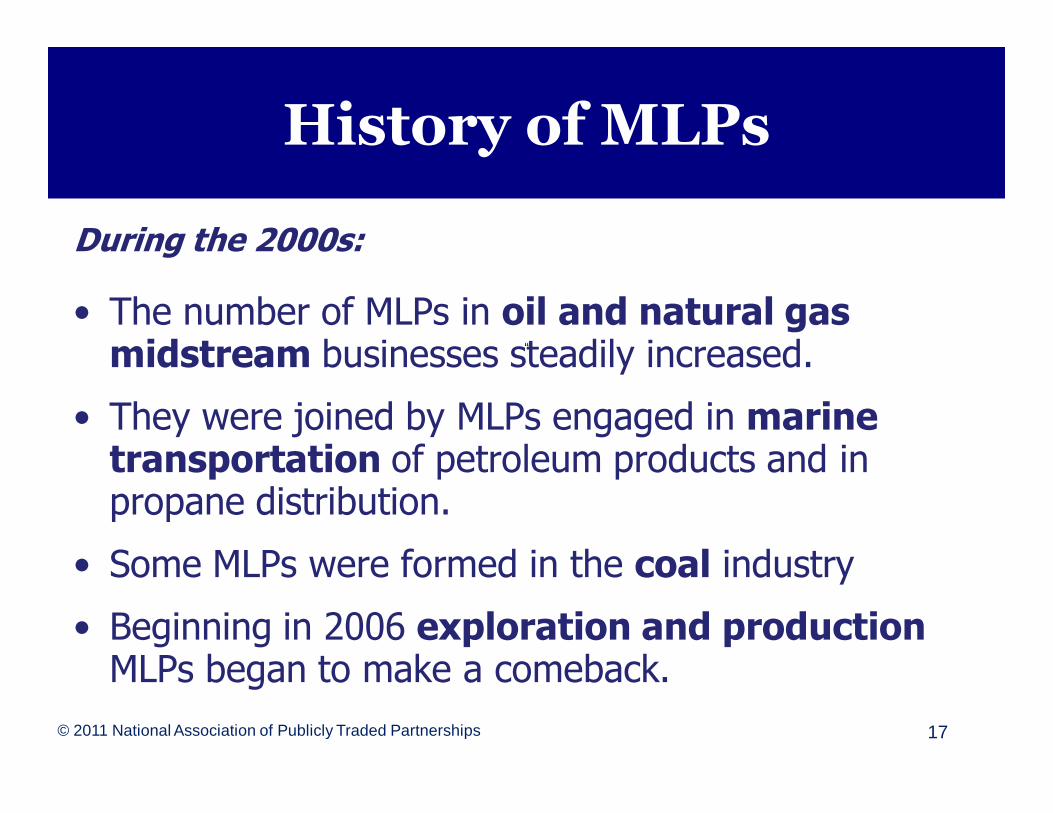

During the 2000s:

• The number of MLPs in oil and natural gas midstream businesses steadily increased.

• They were joined by MLPs engaged in marine transportation of petroleum products and in propane distribution.

• Some MLPs were formed in the coal industry

• Beginning in 2006 exploration and productionMLPs began to make a comeback.

“

© 2011 National Association of Publicly Traded Partnerships 18

History of MLPs

• Several general partners of MLPs went public as MLPs themselves in 2005 and 2006—but now several have recently been folded back into the original MLP.

• Several investment managers turned their holding companies into PTPs (e.g., Blackstone)—but Congress may stop investment managers from doing this in the future.

© 2011 National Association of Publicly Traded Partnerships 19

Master Limited Partnerships

Today

Master Limited Partnerships 101

© 2011 National Association of Publicly Traded Partnerships 20

MLPs Today

• Roughly 90 MLPs are actively trading (exact count is hard to get).

• Today’s MLPs primarily focus on energy-related industries and natural resources.

• Most are in oil and gas midstream industries; others are in other oil and gas activities and coal.

• A few remain in real estate; most of the rest are in investment/financial activities.

© 2011 National Association of Publicly Traded Partnerships 21

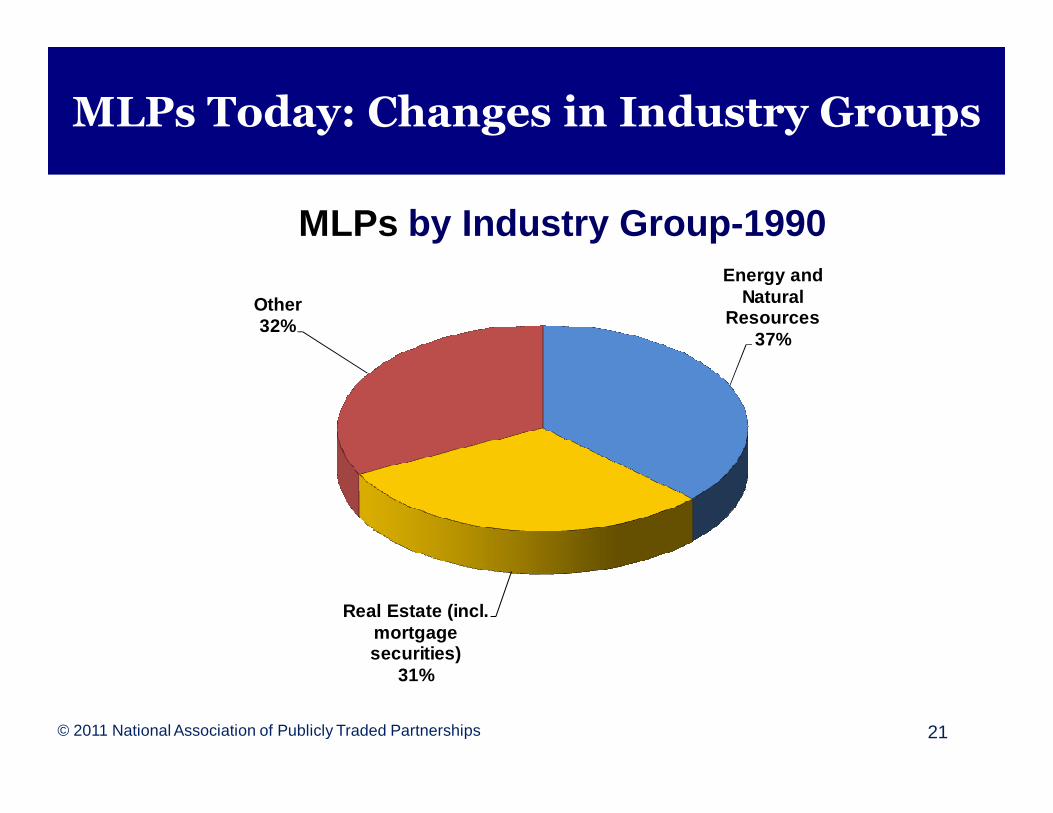

MLPs Today: Changes in Industry Groups

MLPs by Industry Group-1990Energy and

Natural Resources

37%

Real Estate (incl. mortgage securities)

31%

Other32%

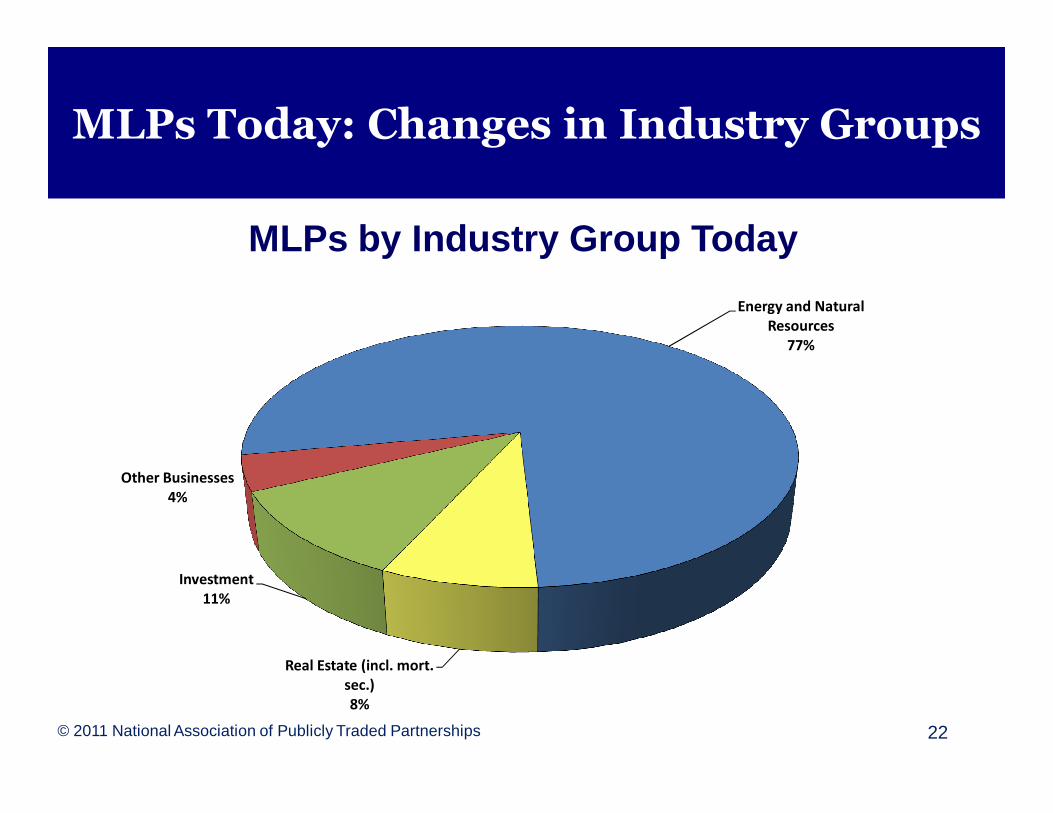

MLPs Today: Changes in Industry Groups

© 2011 National Association of Publicly Traded Partnerships 22

MLPs by Industry Group Today

Energy and Natural

Resources

77%

Real Estate (incl. mort.

sec.)

8%

Investment

11%

Other Businesses

4%

© 2011 National Association of Publicly Traded Partnerships 23

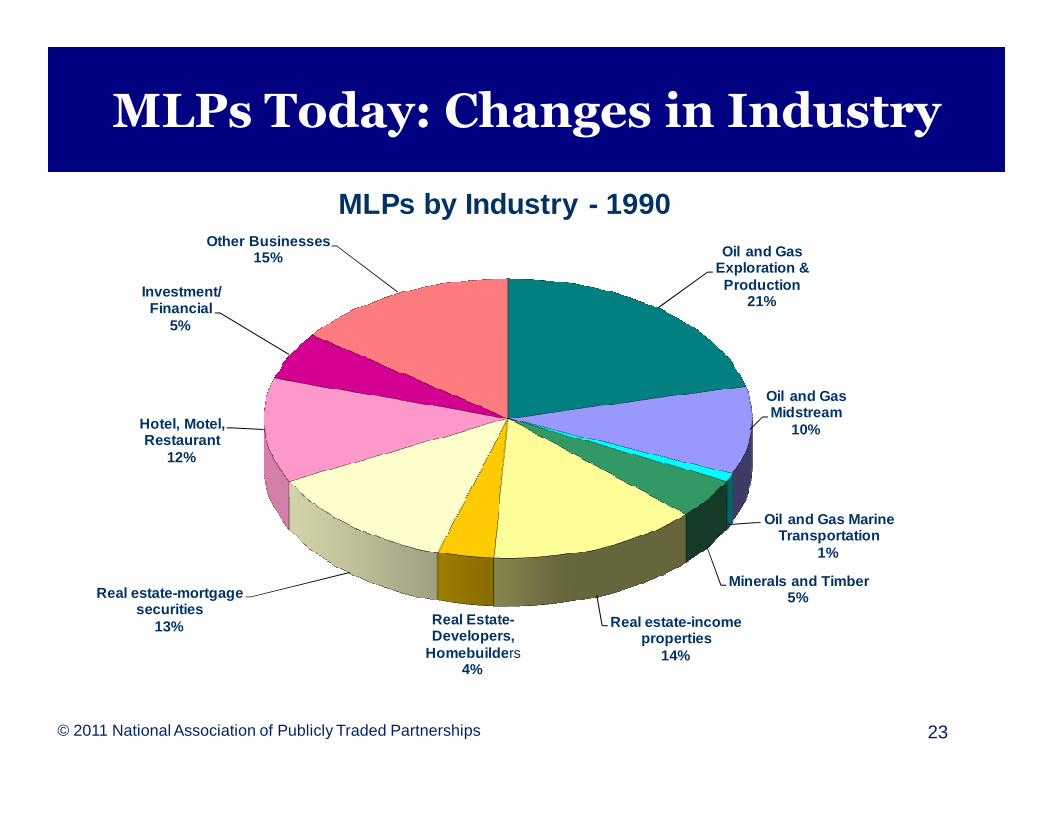

MLPs Today: Changes in Industry

Oil and Gas Exploration & Production

21%

Oil and Gas Midstream

10%

Oil and Gas Marine Transportation

1%

Minerals and Timber5%

Real estate-income properties

14%

Real Estate-Developers,

Homebuilde rs4%

Real estate-mortgage securities

13%

Hotel, Motel, Restaurant

12%

Investment/Financial

5%

Other Businesses15%

MLPs by Industry - 1990

© 2011 National Association of Publicly Traded Partnerships 24

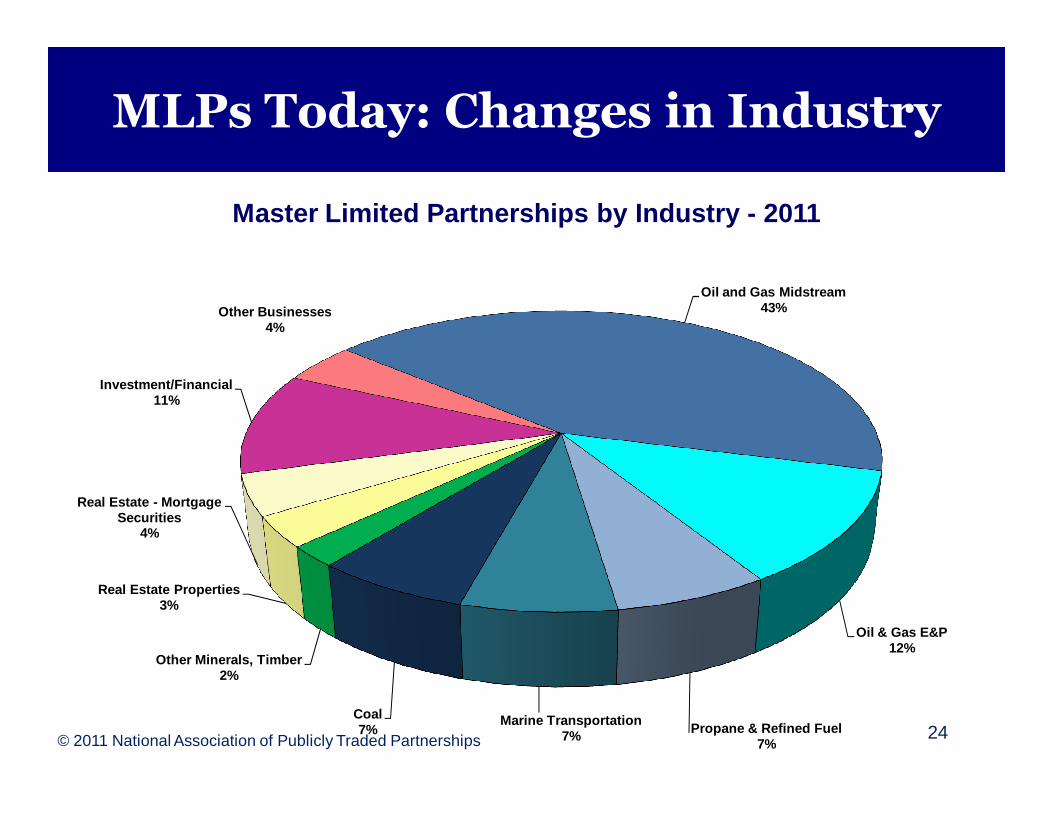

MLPs Today: Changes in Industry

Master Limited Partnerships by Industry - 2011

Oil and Gas Midstream43%

Oil & Gas E&P12%

Propane & Refined Fuel 7%

Marine Transportation7%

Coal7%

Other Minerals, Timber2%

Real Estate Properties3%

Real Estate - Mortgage Securities

4%

Investment/Financial11%

Other Businesses4%

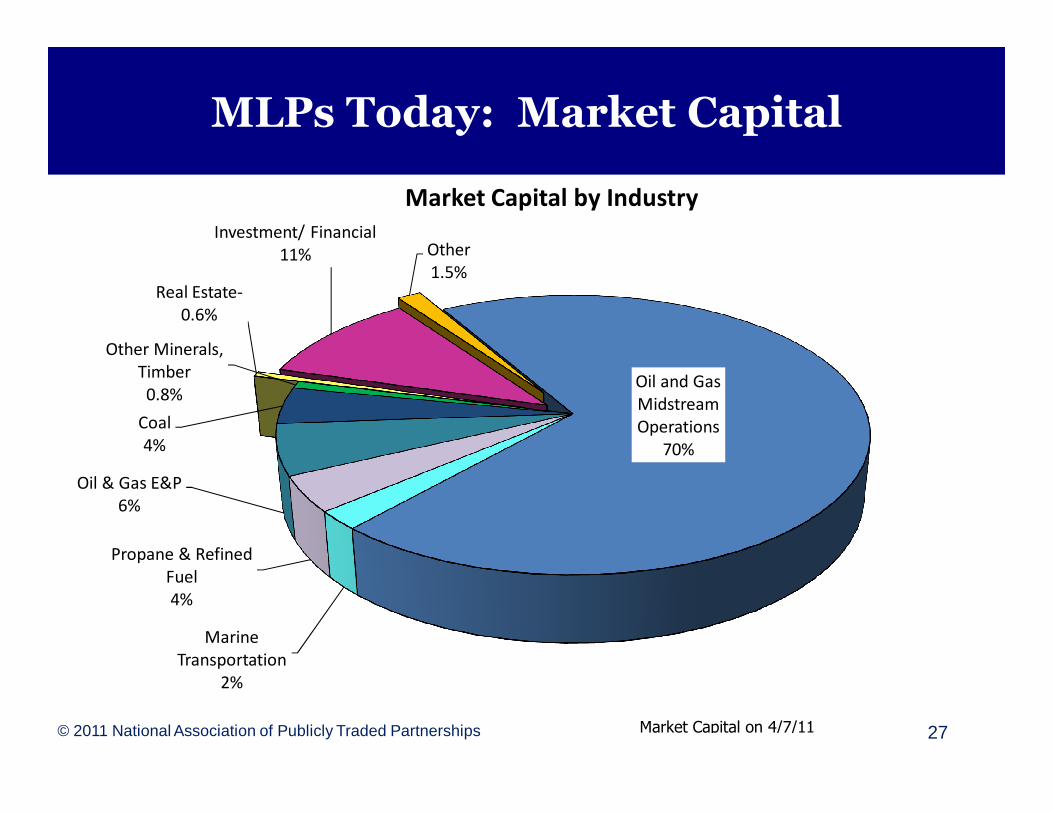

MLPs Today: Market Capital

• Total MLP market capital today is around $283 billion

• About 87 percent of the total, about $245 billion, is attributable to energy and natural resource MLPs.

© 2011 National Association of Publicly Traded Partnerships 25

MLPs Today: Market Capital

© 2011 National Association of Publicly Traded Partnerships 26

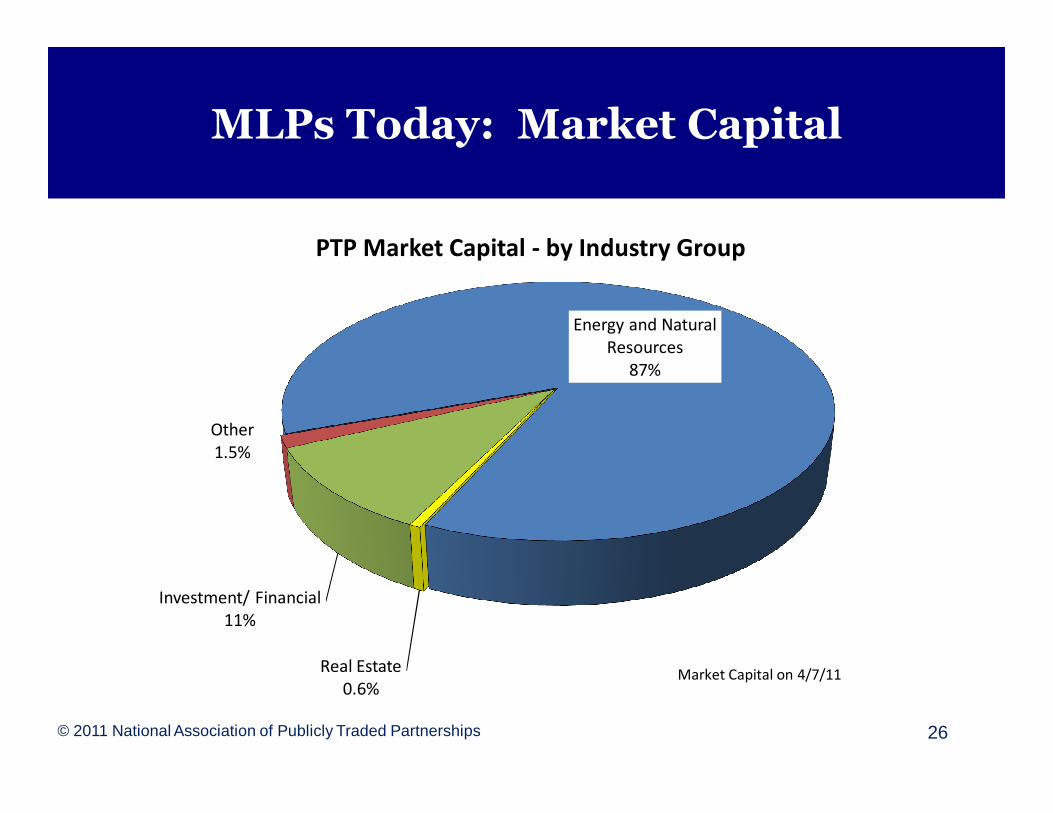

Energy and Natural

Resources

87%

Real Estate

0.6%

Investment/ Financial

11%

Other

1.5%

PTP Market Capital - by Industry Group

Market Capital on 4/7/11

MLPs Today: Market Capital

© 2011 National Association of Publicly Traded Partnerships 27

Oil and Gas

Midstream

Operations

70%

Marine

Transportation

2%

Propane & Refined

Fuel

4%

Oil & Gas E&P

6%

Coal

4%

Other Minerals,

Timber

0.8%

Real Estate-

0.6%

Investment/ Financial

11% Other

1.5%

Market Capital by Industry

Market Capital on 4/7/11

© 2011 National Association of Publicly Traded Partnerships 28

Master Limited Partnerships 101

HOW MLPs WORK

© 2011 National Association of Publicly Traded Partnerships 29

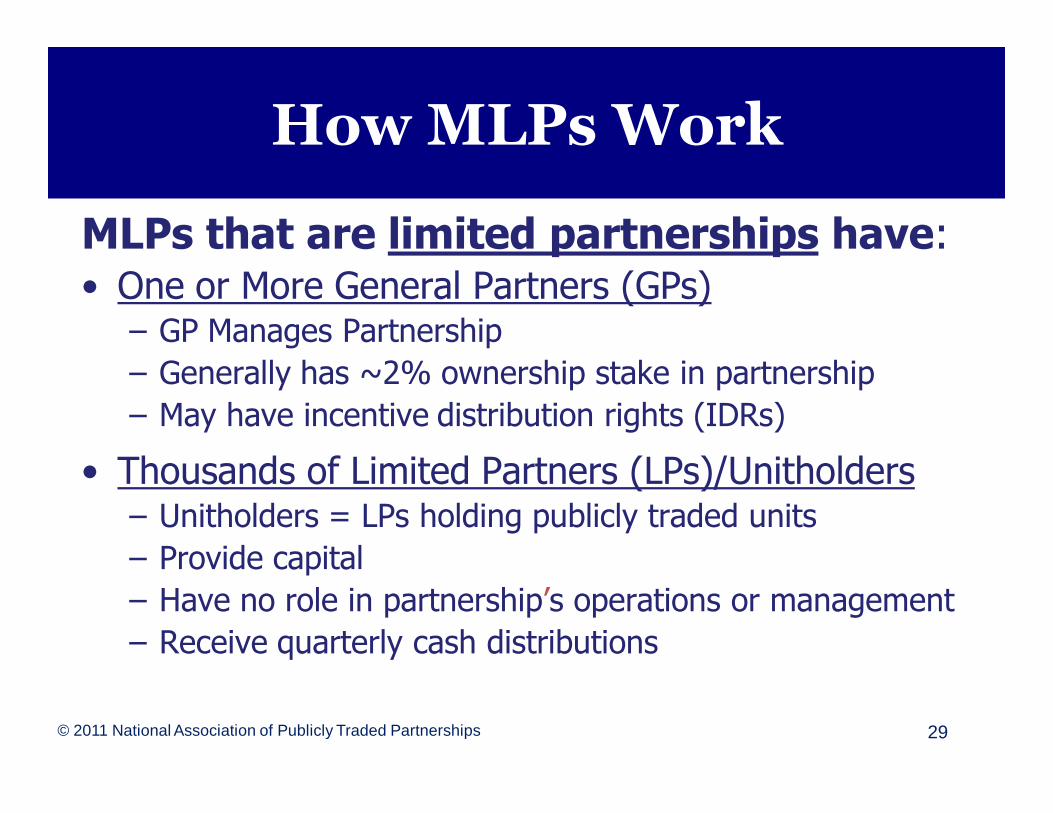

MLPs that are limited partnerships have:• One or More General Partners (GPs)

– GP Manages Partnership

– Generally has ~2% ownership stake in partnership

– May have incentive distribution rights (IDRs)

• Thousands of Limited Partners (LPs)/Unitholders– Unitholders = LPs holding publicly traded units

– Provide capital

– Have no role in partnership’s operations or management

– Receive quarterly cash distributions

How MLPs Work

© 2011 National Association of Publicly Traded Partnerships 30

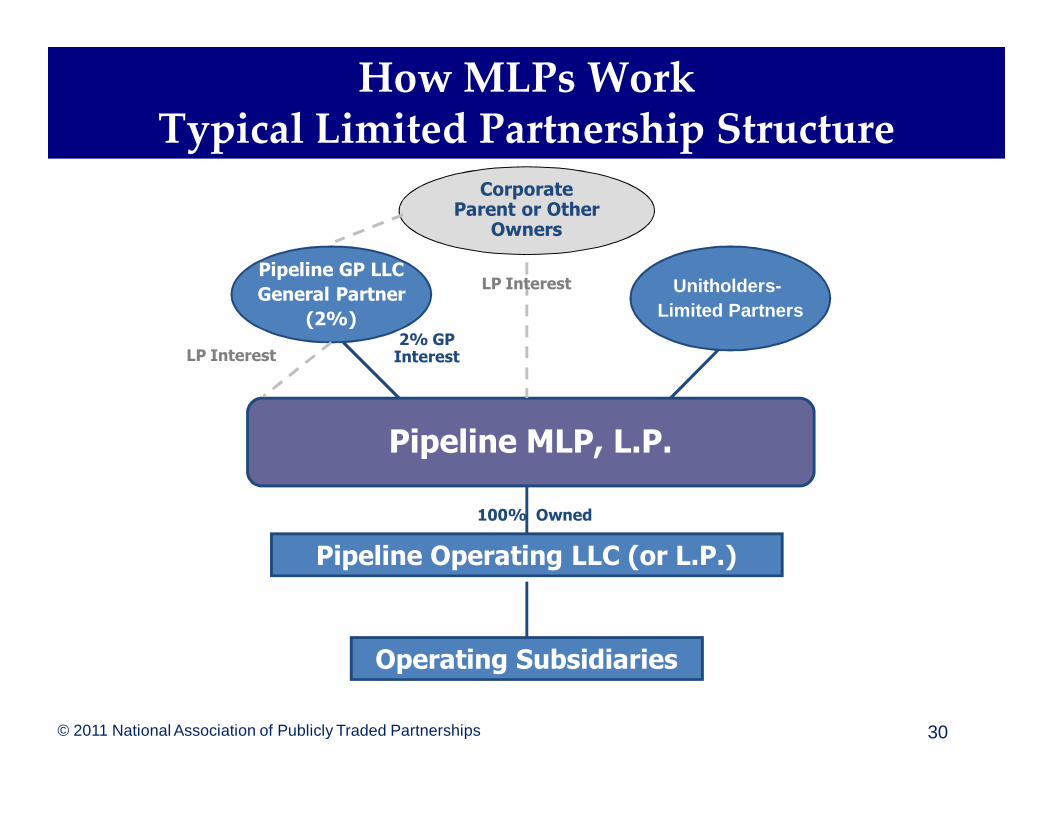

How MLPs WorkTypical Limited Partnership Structure

Pipeline GP LLC

General Partner

(2%)

Pipeline Operating LLC (or L.P.)

Operating Subsidiaries

Unitholders-Limited Partners

Pipeline MLP, L.P.

2% GPInterestLP Interest

LP Interest

Corporate Parent or Other

Owners

100% Owned

© 2011 National Association of Publicly Traded Partnerships 31

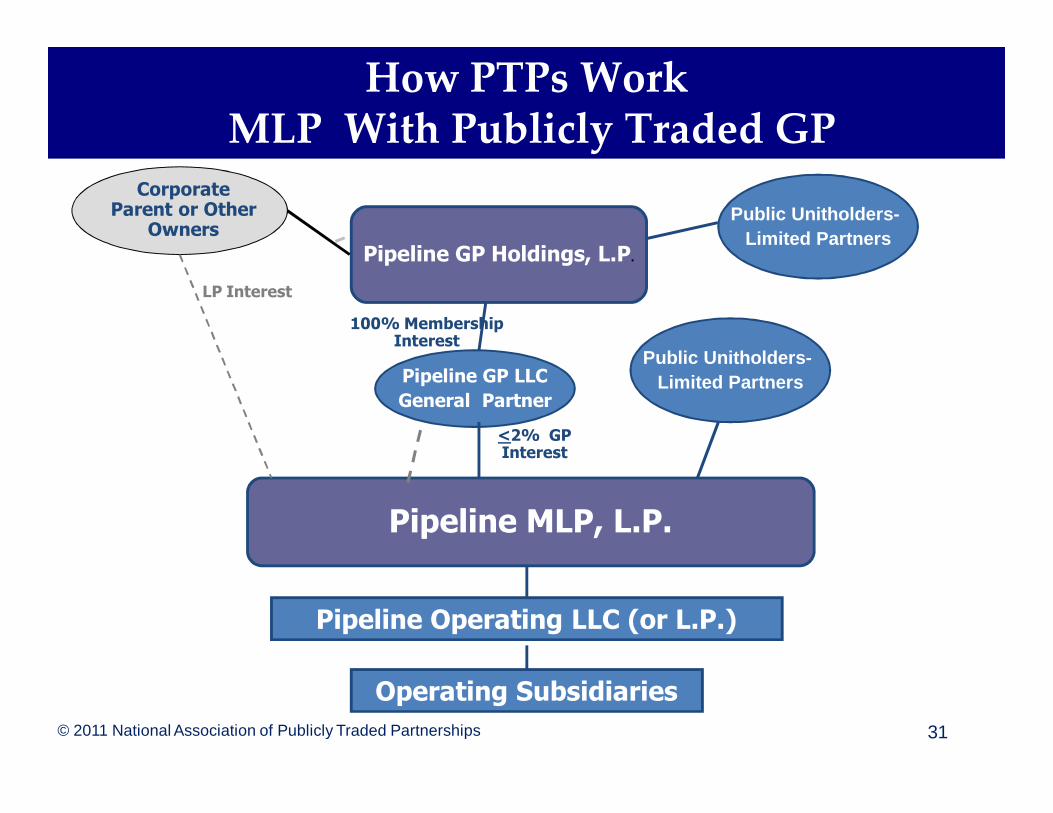

How PTPs WorkMLP With Publicly Traded GP

Pipeline GP LLC

General Partner

Pipeline Operating LLC (or L.P.)

Operating Subsidiaries

Public Unitholders-Limited Partners

Pipeline MLP, L.P.

<2% GP Interest

LP Interest

Corporate Parent or Other

Owners

Pipeline GP Holdings, L.P.

Pipeline GP Holdings, L.P.Public Unitholders-Limited Partners

100% Membership Interest

© 2011 National Association of Publicly Traded Partnerships 32

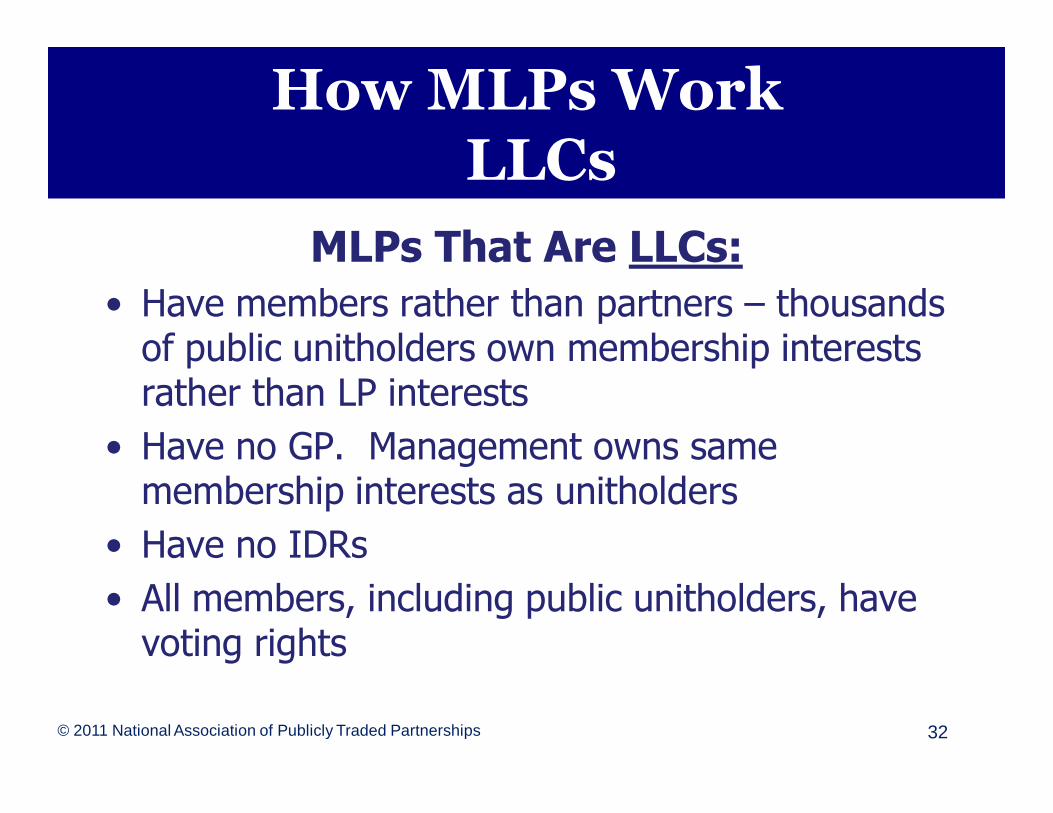

MLPs That Are LLCs:

• Have members rather than partners – thousands of public unitholders own membership interests rather than LP interests

• Have no GP. Management owns same membership interests as unitholders

• Have no IDRs

• All members, including public unitholders, have voting rights

How MLPs WorkLLCs

© 2011 National Association of Publicly Traded Partnerships 33

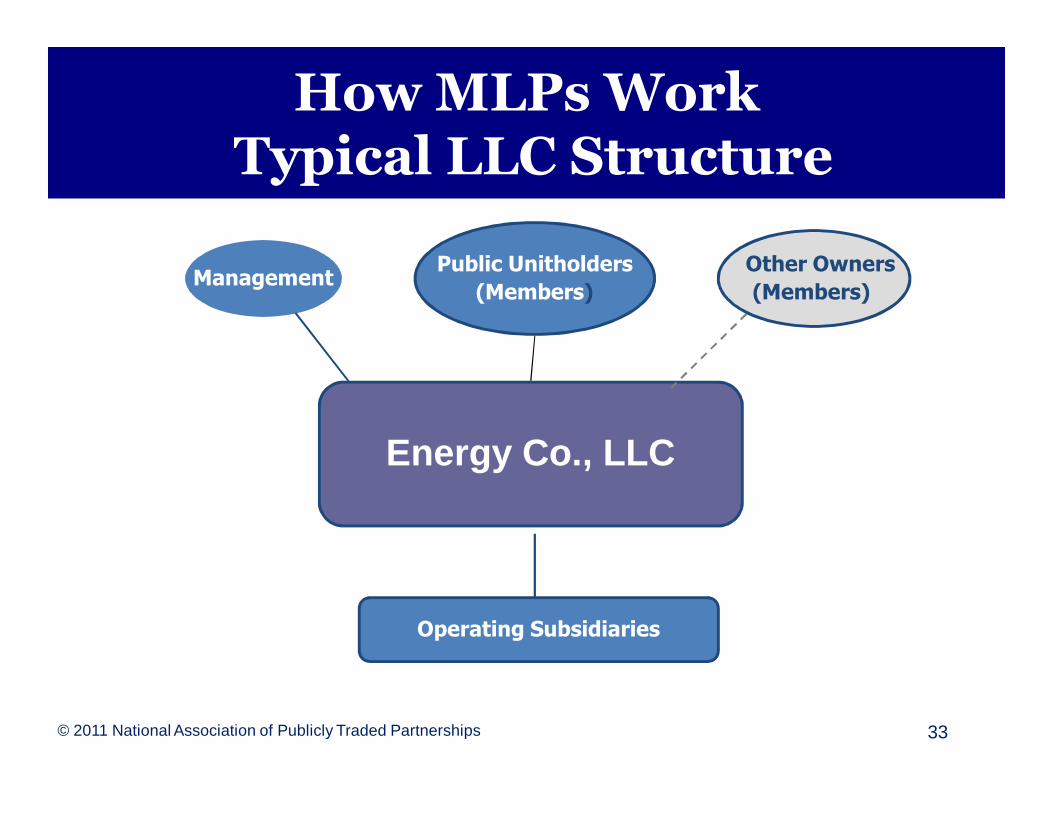

ManagementPublic Unitholders

(Members)

Other Owners

(Members)

Energy Co., LLC

Operating Subsidiaries

How MLPs WorkTypical LLC Structure

© 2011 National Association of Publicly Traded Partnerships 34

In both Limited Partnerships and LLCs:

• Lower-level entities, not the MLP, own the assets and conduct operations

• Taxation is on a pass-through basis

– There is no corporate or other entity-level tax

–All tax items flow through to the LPs or members, who pay tax at their own rates

How MLPs Work

© 2011 National Association of Publicly Traded Partnerships 35

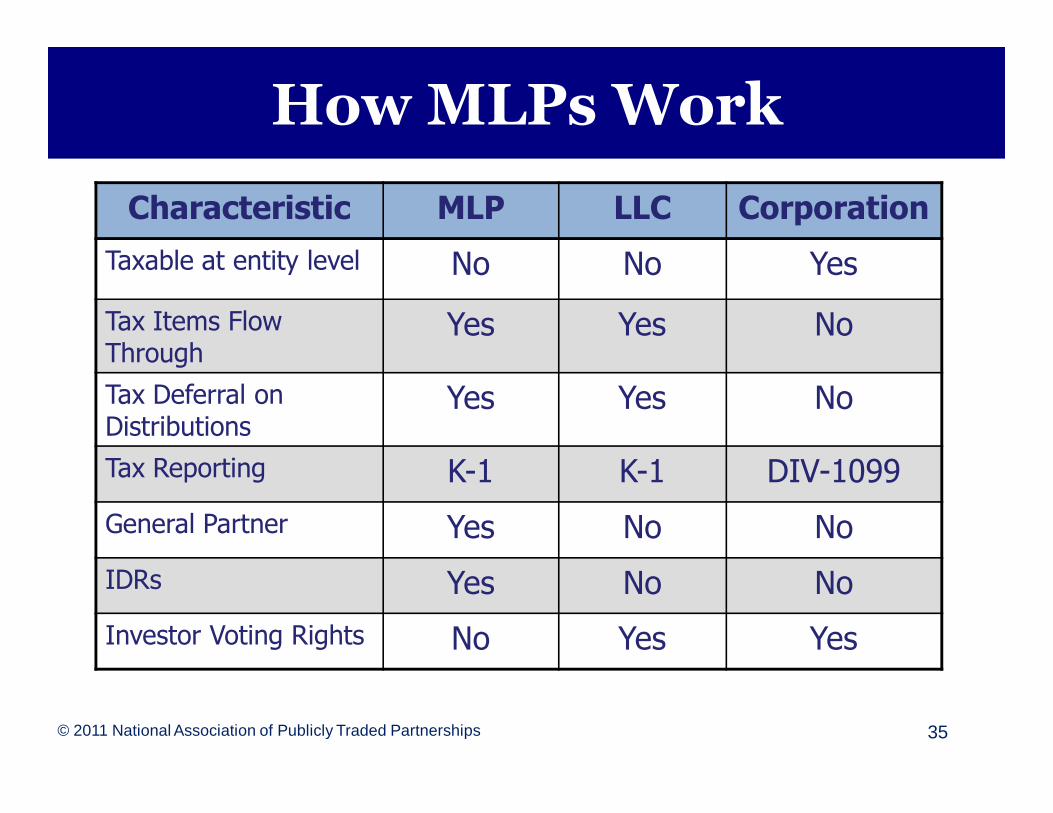

Characteristic MLP LLC Corporation

Taxable at entity level No No Yes

Tax Items Flow Through

Yes Yes No

Tax Deferral on Distributions

Yes Yes No

Tax Reporting K-1 K-1 DIV-1099

General Partner Yes No No

IDRs Yes No No

Investor Voting Rights No Yes Yes

How MLPs Work

© 2011 National Association of Publicly Traded Partnerships 36

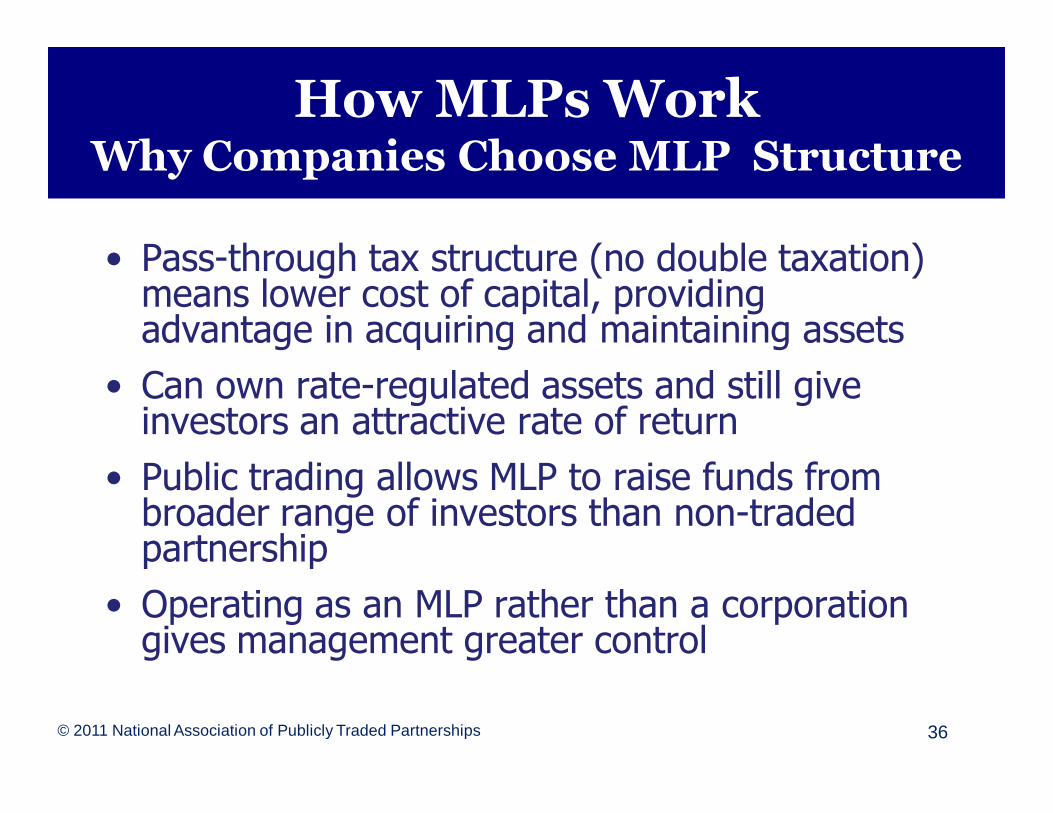

• Pass-through tax structure (no double taxation) means lower cost of capital, providing advantage in acquiring and maintaining assets

• Can own rate-regulated assets and still give investors an attractive rate of return

• Public trading allows MLP to raise funds from broader range of investors than non-traded partnership

• Operating as an MLP rather than a corporation gives management greater control

How MLPs WorkWhy Companies Choose MLP Structure

© 2011 National Association of Publicly Traded Partnerships 37

Master Limited Partnerships 101

Investing in MLPs

© 2011 National Association of Publicly Traded Partnerships 38

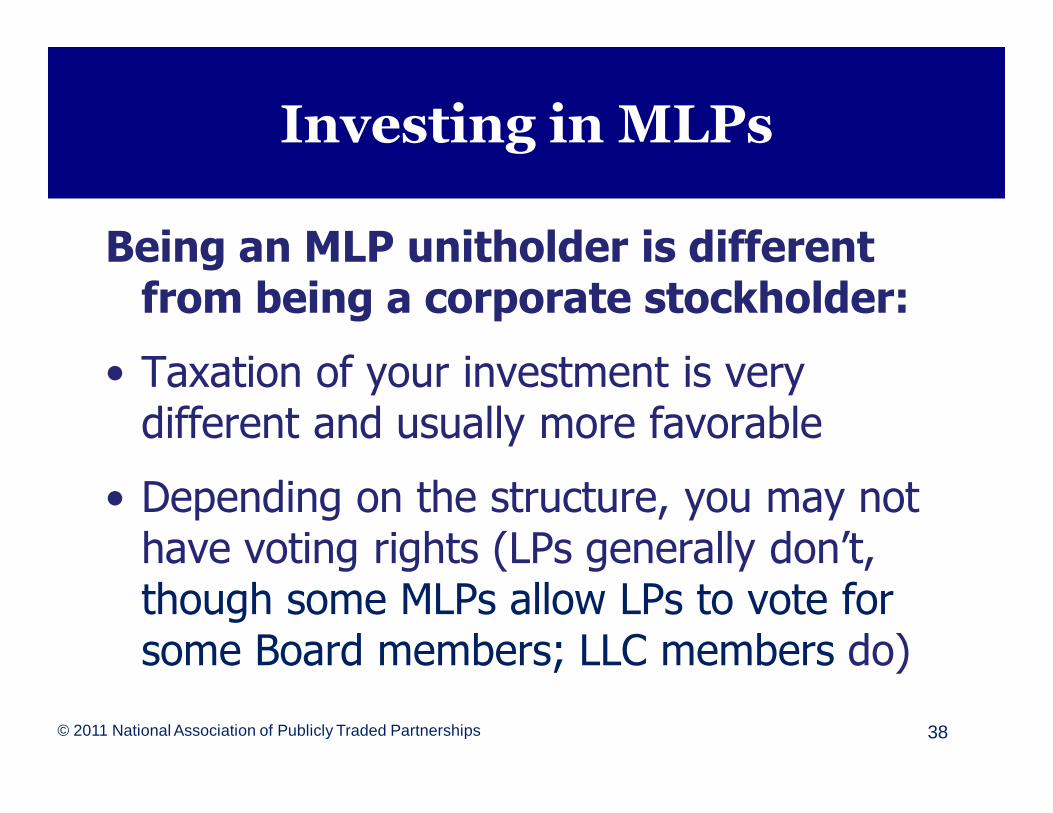

Being an MLP unitholder is different from being a corporate stockholder:

• Taxation of your investment is very different and usually more favorable

• Depending on the structure, you may not have voting rights (LPs generally don’t, though some MLPs allow LPs to vote for some Board members; LLC members do)

Investing in MLPs

© 2011 National Association of Publicly Traded Partnerships 39

Partnership Tax Basics: Income

• An MLP is a pass-though entity which pays no tax itself.

• The unitholder is treated for tax purposes as if he is directly earning the MLP’s income.

• Each unitholder is allocated on paper a share of the MLP’s income, gain, deductions, losses, and credits. This is reported annually on the K-1.

• The unitholder calculates his share of taxable income and pays tax on it at his own tax rate.

Investing in MLPsTaxation

© 2011 National Association of Publicly Traded Partnerships 40

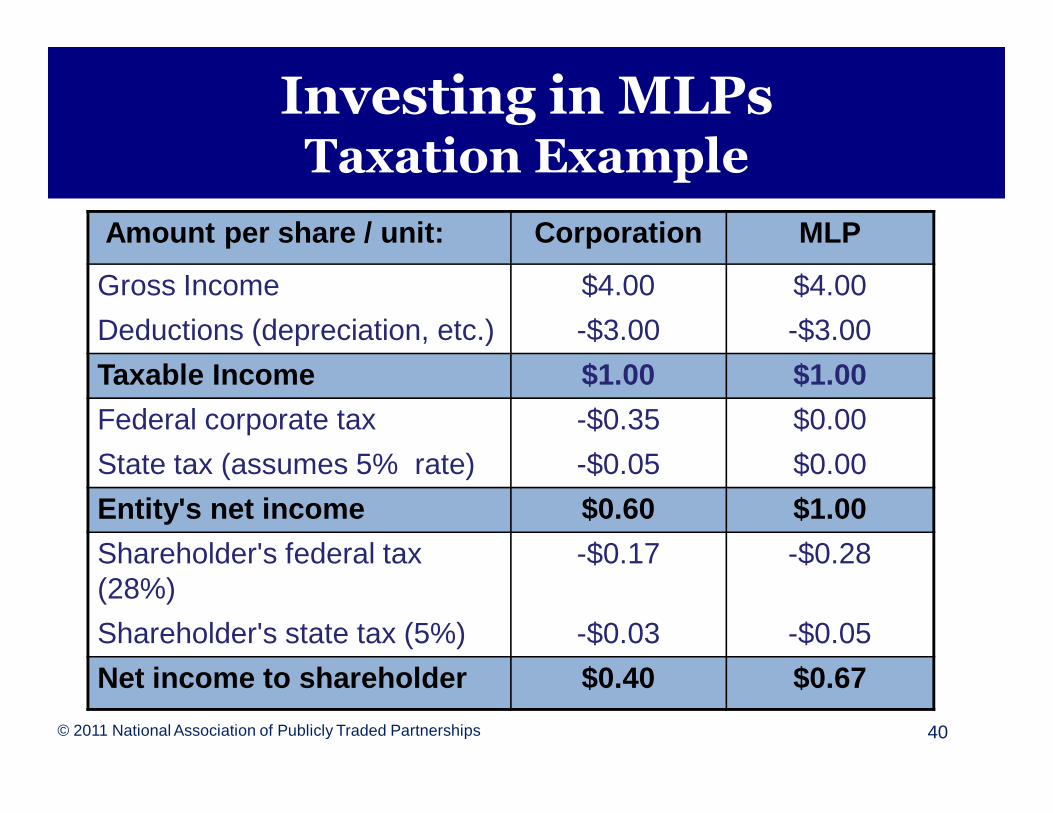

Amount per share / unit: Corporation MLP

Gross Income $4.00 $4.00

Deductions (depreciation, etc.) -$3.00 -$3.00

Taxable Income $1.00 $1.00

Federal corporate tax -$0.35 $0.00

State tax (assumes 5% rate) -$0.05 $0.00

Entity's net income $0.60 $1.00

Shareholder's federal tax (28%)

-$0.17 -$0.28

Shareholder's state tax (5%) -$0.03 -$0.05

Net income to shareholder $0.40 $0.67

Investing in MLPsTaxation Example

© 2011 National Association of Publicly Traded Partnerships 41

Tax Basics: Distributions

• You will receive quarterly cash distributions, which are not the same as your taxable share of the MLP’s income.

• Distributions are based on distributable cash flow (DCF), which is:

– Net earnings, plus

– Depreciation (which is subtracted from income in the earnings calculation but is not a cash expense), minus

– Amounts needed for maintainance and repair of assets used in producing income

Investing in MLPsTaxation

© 2011 National Association of Publicly Traded Partnerships 42

Tax Basics: Distributions

• Under the tax code, the distributions are a return of capital and are not taxed when received.

• Your basis in your partnership units (the amount you paid + or - adjustments) is lowered by the amount of the distribution.

• Thus, when you sell your units, your taxable gain (sales price minus adjusted basis) is increased by the amount of the distributions.

Investing in MLPsTaxation

© 2011 National Association of Publicly Traded Partnerships 43

• Often you will hear someone say that “80% of the MLP’s distribution is tax-deferred.”

• What they really mean is that the unitholder’s allocated share of taxable income as reported on the K-1 ($.50 per unit in the example) equals only 20% of the distribution.

Investing in MLPsTaxation

© 2011 National Association of Publicly Traded Partnerships 44

Corporations - Dividends

• Corporation pays tax on earnings

• After-tax earnings paid to shareholder as dividend

• Shareholder pays tax on dividend

Partnerships - Distributions

• Partnership does not pay tax; income and deductions flow through to partners

• Partners pay tax on net earnings (regardless of cash received)

• Cash distribution treated as tax deferred return of capital

Investing in MLPsTaxation

© 2011 National Association of Publicly Traded Partnerships 45

Basis Adjustments

Your basis is adjusted not only by distributions but by tax items:

• Your share of partnership income each year adjusts the basis upwards.

• Your share of deductions like depreciation adjusts it downwards.

• The idea is that all income you receive from the partnership is taxed once and only once—either in the year you receive it, or when you sell your units

Investing in MLPsTaxation

© 2011 National Association of Publicly Traded Partnerships 46

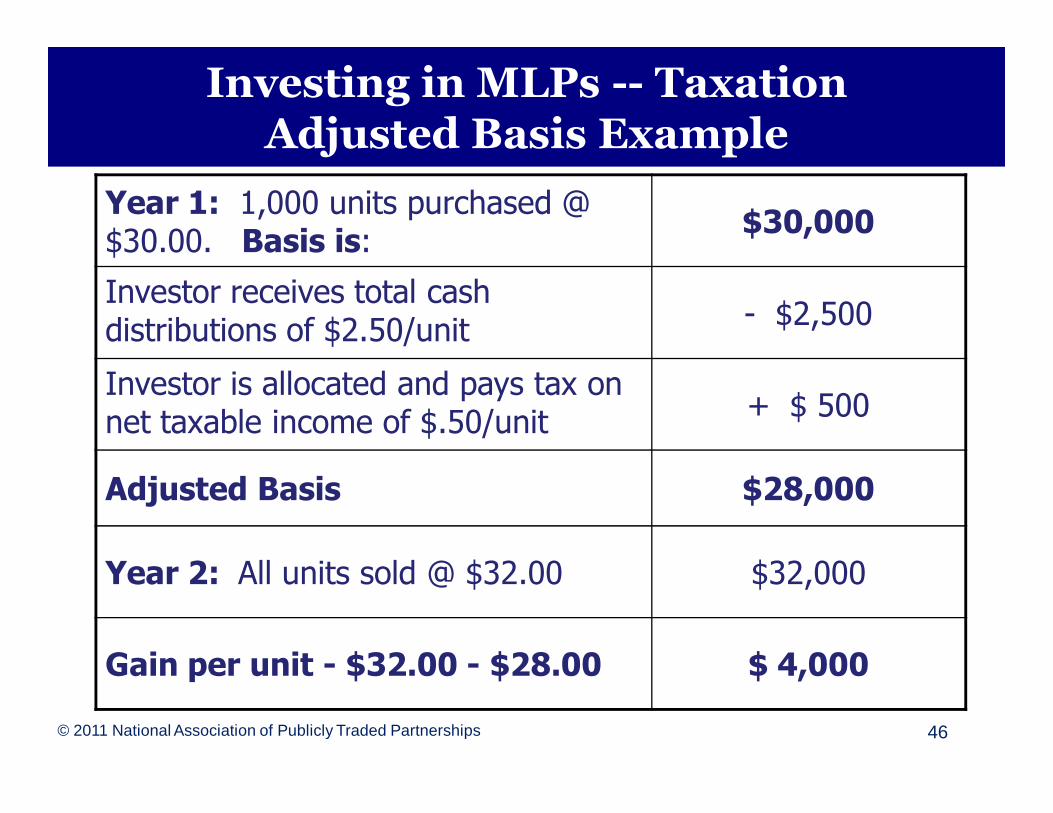

Year 1: 1,000 units purchased @ $30.00. Basis is:

$30,000

Investor receives total cash distributions of $2.50/unit

- $2,500

Investor is allocated and pays tax on net taxable income of $.50/unit

+ $ 500

Adjusted Basis $28,000

Year 2: All units sold @ $32.00 $32,000

Gain per unit - $32.00 - $28.00 $ 4,000

Investing in MLPs -- TaxationAdjusted Basis Example

Investing in MLPsTaxation

Important Note:

Not all of the gain when units are sold is taxed at capital gains rates.

• The gain resulting from basis reductions due to depreciation is taxed at ordinary income rates—this is called “recapture.”

• Gain attributable to your share of some types of assets—substantially appreciated inventory and unrealized receivables—is also taxed as ordinary income.

© 2011 National Association of Publicly Traded Partnerships 47

© 2011 National Association of Publicly Traded Partnerships 48

Investing in MLPsAdvantages

• Income:

– MLPs pay out earnings not needed for current operations and maintenance of capital assets to their unitholders in the form of quarterly cash distributions.

– Most MLPs strive to increase their distributions as often as is possible and prudent.

• Tax benefits: no double taxation, sheltering of income, tax deferral on distributions

© 2011 National Association of Publicly Traded Partnerships 49

Investing in MLPsAdvantages

• Liquidity—MLPs provide the tax benefits of partnerships without tying up your money for years.

• Estate planning: as with other securities, the basis in PTP units is stepped up to fair market value at death—the heir receives a fresh start with no taxation of previous distributions

© 2011 National Association of Publicly Traded Partnerships 50

Investing in MLPsChallenges

• As we’ve seen, tax reporting for an MLP investment is more complex than for shares in a corporation.

– Investor receives a K-1 instead of a 1099

– The K-1 reports investor’s share of all MLP tax items, which investor must enter on his/her own return

– MLPs make the process as easy as possible. Many post K-1s online, and they can be downloaded into Turbotax.

Investing in MLPsChallenges

• State tax issues:

– Partners may owe tax on their share of income allocable to each state in which PTP operates

– Practically, after PTP income is divided among all partners and all states, and depreciation and other deductions applied, a unitholder’sincome in each state will likely be too small for tax to be owed, except for those with large holdings.

© 2011 National Association of Publicly Traded Partnerships 51

© 2011 National Association of Publicly Traded Partnerships 52

Think carefully before investing your IRA, 401(k), or other retirement plan in MLPs.

• These plans are tax-exempt already, so don’t need the tax advantages.

• More importantly, the plan’s share of net partnership income over $1,000 (not the distributions) is likely to be subject to “unrelated business income tax (UBIT)”.

Investing in MLPsRetirement Plans

© 2011 National Association of Publicly Traded Partnerships 53

• UBIT is imposed on tax-exempt entities (including retirement plans) that earn income from a business that is not related to the purpose of their tax exemption.

• Because MLPs are pass-through entities, tax-exempt partners (e.g., your IRA) are treated as directly “earning” the MLP’s business income and are taxed on it.

• Investment income like interest, dividends, and royalties is not taxed.

Investing in MLPsRetirement Plans

© 2011 National Association of Publicly Traded Partnerships 54

Some analysts feel MLPs are still a good investment for IRAs and other retirement funds, because:

• The tax is on net income. Passthrough of depreciation and other deductions means net income may be below $1,000.

• Even if tax is owed, the income may be sufficient to produce a very good return.

• If your IRA or 401(k) does owe UBIT, it, not you, owes the tax. The plan custodian should file a return and pay tax from the plan’s funds.

Investing in MLPsRetirement Plans

© 2011 National Association of Publicly Traded Partnerships 55

• I-Shares: Kinder Morgan and Enbridge Energy Partners have publicly traded management companies (KMR and EEQ) that issue “I-shares.” The companies’ only assets are the underlying MLPs, and distributions consist of additional i-shares. Because KMR and EEQ are in corporate form, there are no K-1 and no UBIT—but also no distributions in cash.

• Investing Through Funds: Over the last few years, a number of options have been developed for investing in MLPs through mutual and other funds.

Investing in MLPsAlternatives to Direct Investment

Investing in MLPsAlternatives to Direct Investment

© 2011 National Association of Publicly Traded Partnerships 56

• Closed-end mutual funds: There are a variety of closed-end funds focusing on MLPs. Tortoise Capital and Kayne Anderson are the leaders in this area; there are several others as well.

• Open-end mutual funds: New this year, SteelPath has a family of three MLP funds; and Swank Capital just added an open-end fund to its Cushing® fund family.

• Exchange Traded Funds: Another recent development—there are 4 MLP-focused ETNs and one ETF pegged to MLP indexes.

© 2011 National Association of Publicly Traded Partnerships 57

Investing in MLPsAlternatives to Direct Investment

Advantages to investing through funds:

• A diverse MLP portfolio selected by experts.

• The fund is the limited partner; it rather than the investor deals with the K-1 form and paying federal and state taxes on partnership income.

• The investor receives a dividend and the familiar 1099 form. The dividend retains return of capital treatment to a large extent.

• The investment can be placed in a retirement account without generating UBIT.

Investing in MLPsAlternatives to Direct Investment

Disadvantages to Investing Through Funds

• Reduced tax benefits: The funds are generally corporations and must tax on their share of K-1 income at the corporate rate before paying you. You will not get the benefit of any deduction or loss pass-throughs.

• Reduced return: In addition to taxes, your return will be diminished by administrative fees and expenses charged by the fund. Be sure to examine and compare these before investing.

© 2011 National Association of Publicly Traded Partnerships 58

© 2011 National Association of Publicly Traded Partnerships 59

How can I find out more about MLPs?

Publicly Traded Partnerships 101

© 2011 National Association of Publicly Traded Partnerships 60

Visit the NAPTP website

www.naptp.org

© 2011 National Association of Publicly Traded Partnerships 61

Contact Information

Mary LymanExecutive Director, NAPTP1940 Duke Street, Suite 200

Alexandria, VA 22314

(703) [email protected]

Top Related