Languages

Pages

Legal

Market Opportunities: Green Energy Technologies

in the Philippines

Georges Sander

29 August 2017 – Brussels

2

Presentation Agenda

Green Energy in the Philippines as Business Opportunity

The Philippines Green Energy Agenda

Green Energy Technologies: Facts, Figures & Trends

Energy Efficiency Industry Development

Overview of the Energy Sector

GET Case Studies in Philippines

Setting Up in Philippines

Philippines Facts & Figures

4

Long-Term Growth Potential

Source: CIA World Factbook, World Economic Outlook Database – International Monetary

Fund, World Economic Forum – Global Competitiveness Report (2016-2017), EU Commission

• A decade of strong, consistent GDP Growth:• 2011 – 2016: 6.1% p.a. on average

• 2017 – 2021: 6.1 - 6.3% p.a.

• Large Domestic Market:• 102.6 M people, expected to reach 145M people by 2045

• Household consumption represents 70% of GDP

• Young and skilled workforce• 53% < 24 years old

• 92% English speakers,

• #Build, Build, Build! Solving the Infrastructure Bottleneck• 5% of GDP to be invested in infrastructure (up from 2.2%)

• Pending fiscal reform

• Foreign Investment Legislation under review

Source: BMI

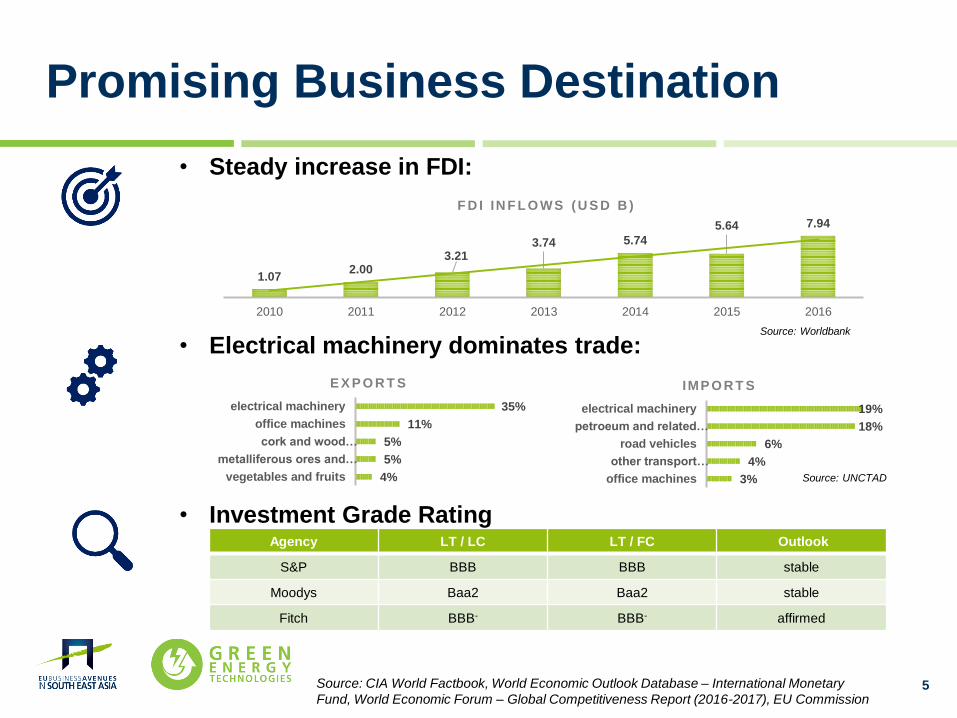

Agency LT / LC LT / FC Outlook

S&P BBB BBB stable

Moodys Baa2 Baa2 stable

Fitch BBB- BBB- affirmed

5

Promising Business Destination

Source: CIA World Factbook, World Economic Outlook Database – International Monetary

Fund, World Economic Forum – Global Competitiveness Report (2016-2017), EU Commission

• Steady increase in FDI:

• Electrical machinery dominates trade:

• Investment Grade Rating

4%

5%

5%

11%

35%

vegetables and fruits

metalliferous ores and…

cork and wood…

office machines

electrical machinery

E X P O R T S

3%

4%

6%

18%

19%

office machines

other transport…

road vehicles

petroeum and related…

electrical machinery

IMP O R T S

1.072.00

3.213.74 5.74

5.64 7.94

2010 2011 2012 2013 2014 2015 2016

F D I IN F L O WS (U S D B )

Source: UNCTAD

Source: Worldbank

6

Strengthening EU Business Ties

Source: CIA World Factbook, World Economic Outlook Database – International Monetary Fund,

World Economic Forum – Global Competitiveness Report (2016-2017), EU Commission, BOI

• EU-28 as 4th biggest trade partner• 12B EUR in 2016 (9.2% of total trade) after China, US and Japan

• EU exports to Philippines doubled from 2006 to 2016

• EU exports include machinery, aircraft & pharmaceutical products

• 7 EU countries account for 90% trade with the Philippines:

• EU-28 largest investor into the Philippines• 2016 FDI inflows from EU at 6.1B EUR

• EU represents 20% - 30% of annual FDI inflows (2014 – 2016)

• Double taxation agreements in place with 15 EU countries

• EU – Philippines FTA negotiations launched on 22/12/2015

7

Growing Demand for Energy

2016 2017 2021 2025

Power Generation,TWh

86 91.6 111.4 136.9

Consumption, TWh 73.2 77.9 94.8 116.5

Population, m 102.3 103.8 110 116.2

95

100

105

110

115

120

0

20

40

60

80

100

120

140

160TWh Philippine power outlook• Power generation growth

from 2016 to 2025 will grow

a healthy 5.3% CAGR

• Rising affluence and

population growth of 1.4%

CAGR up to 2025, will drive

demand for electricity

• Strong potential for

renewables is forecasted,

given shift to self-sufficiency

and shelving of nuclear

power ambitions

• Privatisation & deregulation

of power sector is

progressing, with growth in

number of independent

generators and distributors

entering the market

Key power indicators and outlook, 2016-2025

Source: ‘Philippines Power Report, Q3 2017’- Business Monitor International Research,

2016 Philippine Power Situation Report – Philippine Department of Energy

• Wealth of Renewable Resources

• Highest cost of electricity in ASEAN

• Rural electrification to relieve poverty

• 82% electrification rate in rural areas

• 60% of rural population below poverty line

• Government support• Feed-In Tariffs

• Tax Incentives

8

The Green Energy Opportunity

Source: CIA World Factbook, World Economic Outlook Database – International Monetary

Fund, World Economic Forum – Global Competitiveness Report (2016-2017), EU Commission

Source Geothermal Wind Solar Biomass Ocean

Potential > 4,000 MW > 76,600 MW >5 kwh/m2/day > 500 MW > 170,000 MW

Source: DOE

The Philippines Green Energy Agenda

Political Commitment

10

.

Commitment

to

cutting Emissions

• In February 2017,

President Duterte

signed 2015 Paris

Agreement, pledging to

cut CO2 emissions by

70%, by 2030

• Domestic utility

companies stressed the

need to shift from

cheap coal to cheap

clean energy

• Government considers

power as critical to

enabling economic

growth

.

Diversification

of

Energy Mix

• National Renewable

Energy Plan (NREP)

has target of reaching

15.5TWh of installed

renewables energy

capacity by 2030, or

close to 50% of total

electricity generation

• 2030 Energy Plan aims

for 100% electrification

• Reducing dependency

on expensive thermal

energy imports and

unreliable large hydro

.

Supporting policies

already

in place

• Fiscal & non-fiscal

incentives are available

for renewable energy

developers e.g. VAT

exemption, duty-free

importation of

machinery, tax holidays

etc.

• Government support for

feed-in-tariff (FiT)

mechanisms remains

strong

• Move towards self-

sustainability, and lower

returns, remain GET

sector challenges

.

Focus on Improving

the

Grid Infrastructure

• Philippine grid

infrastructure remains

inefficient with

estimated T&D losses

of 15% of total output

• Philippine authorities

have now made grid

systems a government

priority

• E.g. Approved

US$138m

transmission-backbone

project in Mindanao for

National Grid

Corporation

Source: ‘Philippines Power Report, Q3 2017’- Business Monitor International Research,

PwC analysis

11

Ambitious Government Agenda (1) S

ho

rt-t

erm

2017-2

018

Med

ium

-

term

2019-2

022

Lo

ng

-te

rm

20

23

-2040

. Acceleration

of GET positioning

• Finalise rules and

implement Green Energy

Option

• Intensify development in

off-grid areas for wider

populace access to

energy

• Determine realistic GET

potential

• Continue and accelerate

implementation of GET

projects

. Creation of a conducive

business environment

• Streamline administrative

processes of RESC

applications

• Provide technical

assistance to lower

investment costs

• Establish GET

Information Exchange

• Explore & initiate on the

harmonisation of LGU

and government

programmes

. Reliable, efficient infrastructure

• Strengthen resiliency of

GET systems & facilities

• Harmonise transmission

Development Plan with

GET targets

• Develop geographical

installation target

• Enhance local technical

capabilities

• Conduct R&D on the

efficiency of GET

technologies on Smart

Grid Systems

OBJECTIVE

BY 2040 Increase GET installed capacity to at least 20,000MW

Source: ‘Philippine Renewable Energy Roadmap’ - Philippine Department of Energy

12

Sh

ort

-te

rm

2017-2

018

Med

ium

-

term

2019-2

022

Lo

ng

-te

rm

20

23

-2040

. Promote & enhance R&D agenda

• Strengthen the management and

operation of ARECs

• Continue conduct of GET technology

research and development studies

• Identify viability of new technologies

• Construct Ocean pilot / demo Energy

projects

• Implement, monitor and evaluate pilot /

demo projects for new GET

technologies

OBJECTIVE

BY 2040

. Other activities

• Identify parameters to determine the

viable Ocean Energy tariff rate

• Continue technical capacity-building on

GET

• Conduct research and promote low-

enthalpy geothermal areas for power

generation and direct use / non-power

application for development

• Harmonise DoE-related programmes

with agro-forestry policies for an

integrated use of biomass

• Continue conduct of IEC to attain social

acceptability

Increase GET installed capacity to at least 20,000MW

Source: ‘Philippine Renewable Energy Roadmap’ - Philippine Department of Energy

Ambitious Government Agenda (2)

Green Energy Technologyin the Philippines:

Facts, Figures & Trends

14

Philippines: GET Statistics

2016

86.2TWh

Total Power

Generation

Share of power

generation by source

62%4%

16%

6%

12%

Coal

Oil-based

Natural gas

Hydropower

Non-hydrolectricrenewables

21,423MW

Installed

Capacity

35%

17%16%

16%

9%

4%

2%1% Coal

Oil-based

Natural gas

Hydropower

Geothermal

Solar

Wind

Biomass

Share of installed

capacity by source

Overview of Philippine power capabilities

Source: ‘Philippines Power Report, Q3 2017’- Business Monitor International Research,

2016 Philippine Power Situation Report – Philippine Department of Energy, PwC analysis

15

Philippines: GET statistics

84%

6%

5% 5%

Geothermal Wind Solar Biomass

75%

15%

5% 5%

Geothermal Wind Solar Biomass

13.8TWh

Generation,

Non-hydroelectric

renewables

16.0%Of total Philippine

power generation

17.2TWh

Generation,

Non-hydroelectric

renewables

12.6%Of total Philippine

power generation

Share of various non-

hydroelectric renewables

Share of various non-

hydroelectric renewables

2016 2025

Philippine non-hydroelectric renewables forecast, 2016-2025

Source: ‘Philippines Power Report, Q3 2017’- Business Monitor International Research,

2016 Philippine Power Situation Report – Philippine Department of Energy, PwC analysis

16

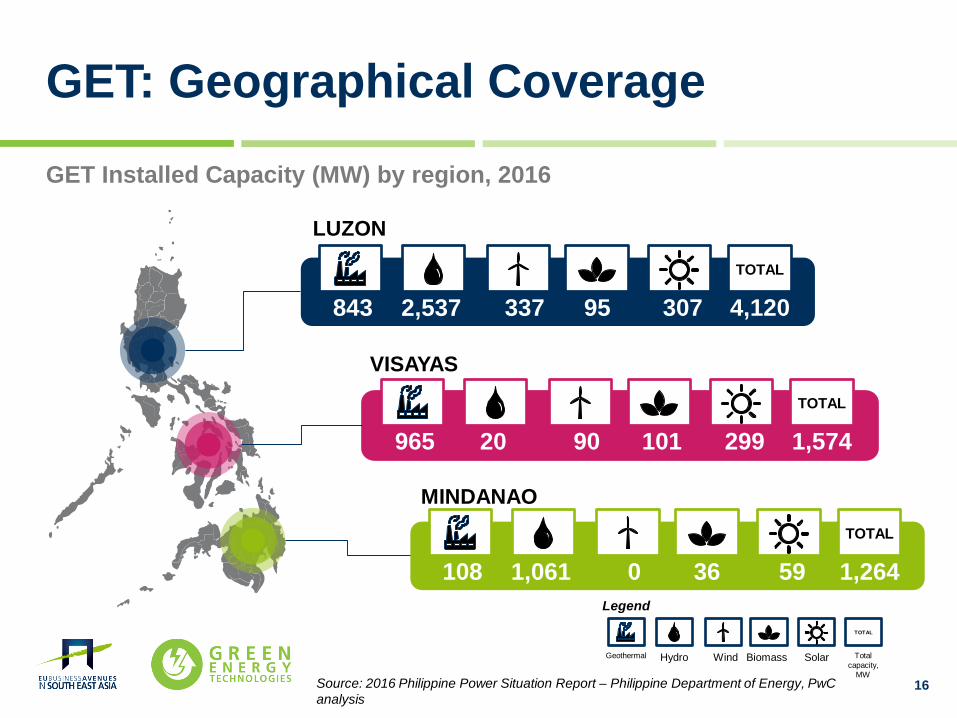

GET: Geographical Coverage

GET Installed Capacity (MW) by region, 2016

337 95 307 4,120

TOTAL

843 2,537

LUZON

90 101 299 1,574

TOTAL

965 20

VISAYAS

0 36 59 1,264

TOTAL

108 1,061

MINDANAO

TOTAL

Geothermal Hydro Wind Biomass Solar Total

capacity,

MW

Legend

Source: 2016 Philippine Power Situation Report – Philippine Department of Energy, PwC

analysis

17

GET: Geographical Coverage

0 4 4 13

TOTAL

2 3

LUZON

0 0 2 5

TOTAL

1 2

VISAYAS

0 3 0 8

TOTAL

0 5

MINDANAO

TOTAL

Geothermal Hydro Wind Biomass Solar Total

capacity,

MW

Legend

Summary of committed & indicative GET power projects by region, 2016

Source: 2016 Philippine Power Situation Report – Philippine Department of Energy, PwC

analysis

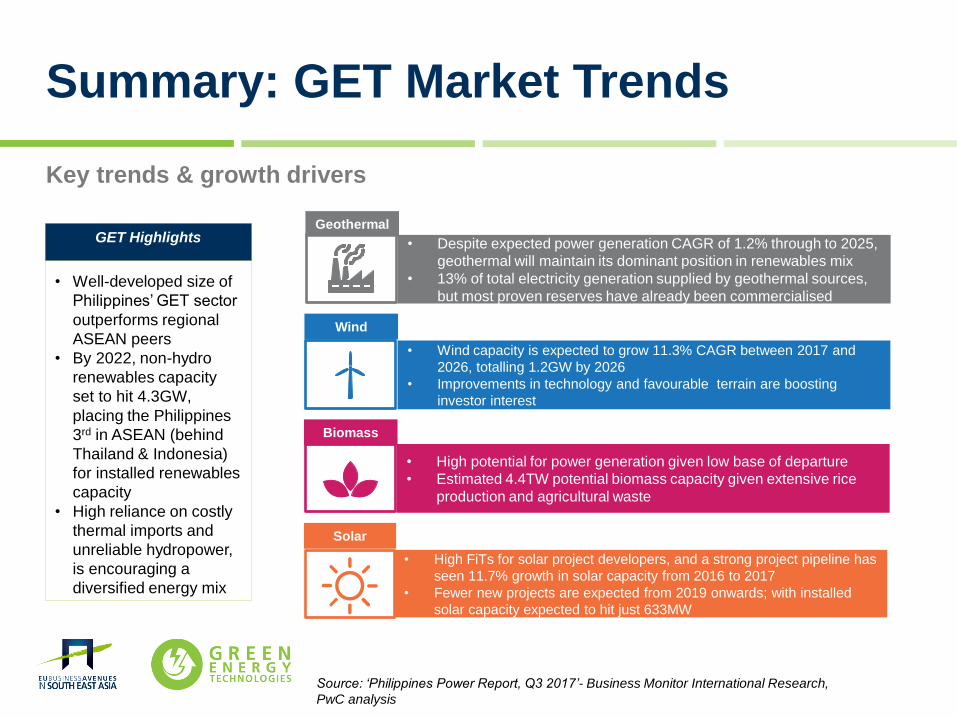

Summary: GET Market Trends

. GET Highlights

• Well-developed size of

Philippines’ GET sector

outperforms regional

ASEAN peers

• By 2022, non-hydro

renewables capacity

set to hit 4.3GW,

placing the Philippines

3rd in ASEAN (behind

Thailand & Indonesia)

for installed renewables

capacity

• High reliance on costly

thermal imports and

unreliable hydropower,

is encouraging a

diversified energy mix

• Despite expected power generation CAGR of 1.2% through to 2025,

geothermal will maintain its dominant position in renewables mix

• 13% of total electricity generation supplied by geothermal sources,

but most proven reserves have already been commercialised

Geothermal

• Wind capacity is expected to grow 11.3% CAGR between 2017 and

2026, totalling 1.2GW by 2026

• Improvements in technology and favourable terrain are boosting

investor interest

Wind

• High potential for power generation given low base of departure

• Estimated 4.4TW potential biomass capacity given extensive rice

production and agricultural waste

Biomass

• High FiTs for solar project developers, and a strong project pipeline has

seen 11.7% growth in solar capacity from 2016 to 2017

• Fewer new projects are expected from 2019 onwards; with installed

solar capacity expected to hit just 633MW

Solar

Key trends & growth drivers

Source: ‘Philippines Power Report, Q3 2017’- Business Monitor International Research,

PwC analysis

Energy EfficiencyIndustry Development

20

Energy Efficiency Roadmap

Short-term

2017-2018

Medium-term

2019-2022

Long-term

2023-2040

• Conduct market demand scoping

• Advocate legislation of EE&C bill

• Establish cross-sectoral energy

performance & rating systems

• Create business tool kit for

ESCOs

• Collaboration with stakeholders

for expanded financing models

for EE&C Projects

• Information, Education and

Communication campaigns on

EE practices

• Create enabling mechanisms

for private sector participation

• Enhance Demand-Side

management mechanisms

• Integrate EE&C in the

learning and education

system

• Mainstream EE&C at LGU

level

• Institutionalise EE&C

Knowledge Management

System

• Develop advanced EE&C

R&D capacity

Industry development Strengthening Sustaining

Key objective is to ensure measurable reduction in energy intensity and

consumption across all user types

Source: ‘Philippine Renewable Energy Roadmap’ - Philippine Department of Energy

The Philippines Energy Sector

22

The Regulatory Environment

NEAPSALM ERCNPC

COORDINATIONSUPERVISION

DoE

AbbreviationsDoE: Department of Energy

NPC: National Power Corporation

NEA: National Electrification Administration

PSALM: Power Sector Assets and Liabilities Management Corp,

ERC: Energy Regulatory Commission

Key stakeholders and jurisdictions under EPIRA**Electric Power Industry Reform Act (2001)

Source: Philippine Energy Regulatory Commission’s Regulatory Framework

24

Value Chain

Generation

Transmission

Distribution

Consumers

• Recently privatised to different entities to foster competition

• PMEC acts as market operator, administering the wholesale Electricity Spot Market

• NGCP operates transmission assets owned by Transco

• Private distribution utilities or electric cooperatives

• Captive customers served by Distribution Utilities

• Contestable customers ( > 750 kw) served by Retail Suppliers

Various players

Various players

Electricity industry structure after EPIRA**Electric Power Industry Reform Act (2001)

Source: Philippine Department of Energy

Stakeholders

Various players

GET Success Storiesin the Philippines

26

GET Success Stories in the Philippines

Source: ADB

ADB Backs First Climate Bond in

Asia in Landmark $225 Million

Philippines Deal• Investment into the rehabilitation of

the life of Tiwi-MakBan geothermal

energy facilities (776 MW) to

improve performance and extend

their operating life.

• ADB backed 75% of Bond’s principal

PHP10.7 billion ($225 million

equivalent) local currency bond.

• Transaction considered mitigating

local currency risks and promoting

project bonds (as an alternative to

project finance and corporate bonds)

27

GET Success Stories in the Philippines

Source: EVEEI

Electric Vehicle Expansion

Enterprises, Inc. - Sustainable

Transport. Electrified with Passion

• Replacing diesel jeepneys with electric

powered jeepneys.

• Diesel-fueled jeepneys, buses, trucks

and other vehicles in Metro Manila are

responsible for about 70 percent of the

total soot or black carbon emissions

• World Bank estimates that some 5,000

annual premature deaths make up 12

percent of all deaths in Metro Manila,

due primarily to respiratory and

cardiovascular diseases from exposure

to air pollution

28

GET Success Stories in the Philippines

Source: Climate Action Programme - UN Environment

The Philippines pursues renewable

energy expansion largest solar power

project• Solar Philippines has recently begun work on

the 150 megawatts (MW) solar photovoltaic

(PV) project in Concepcion, Tarlac.

• 450,000 solar panels to be installed across

150 hectares, making the project one of

south-east Asia’s largest solar farms.

• Panels to be manufactured locally in addition

to using batteries to supply 24-hour

electricity.

• Project cost estimated at $195 million, and

produce enough power to fulfil the entire

province’s needs.

Setting Up in the Philippines

30

Areas of Caution

Source: CIA World Factbook, World Economic Outlook Database – International Monetary

Fund, World Economic Forum – Global Competitiveness Report (2016-2017), EU Commission

• Local Partner to facilitate stakeholder engagement:• Central Government in Manila

• Local communities and regional authorities around project site

• Foreign Exchange Risk:• PHP expected to depreciate due to

• Lower remittance flows

• Negative trade balance

• High frequency of natural disasters

• Political Instability

• Foreign Ownership Restrictions:• Maximum 40% foreign ownership

• “Negative List” currently under review

• Renewables qualified as Investment Priority by BOI

31

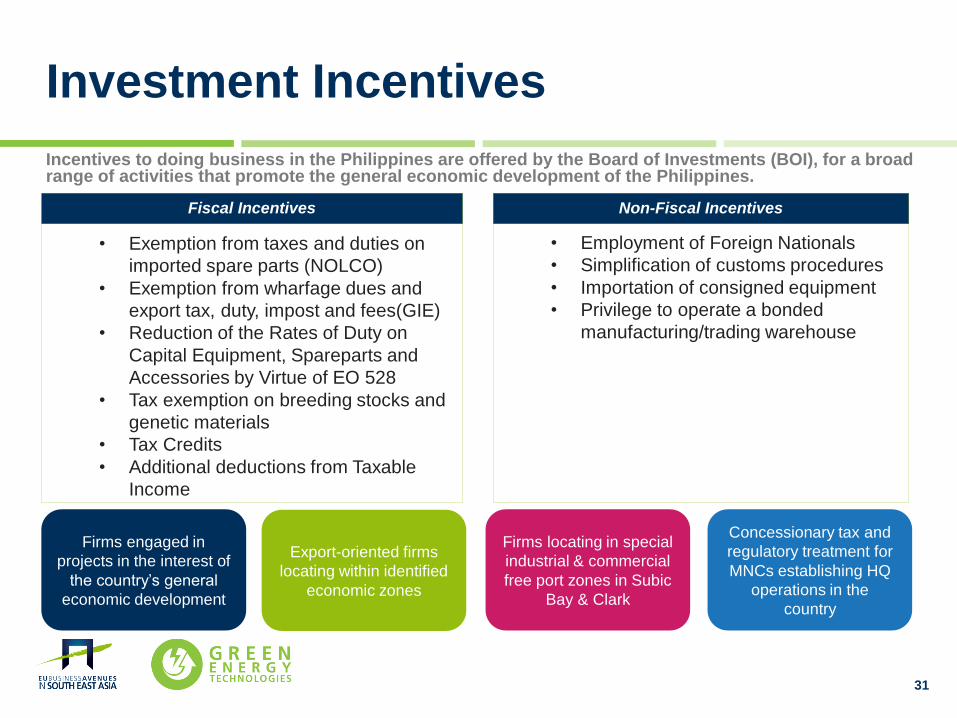

Investment Incentives

Incentives to doing business in the Philippines are offered by the Board of Investments (BOI), for a broad range of activities that promote the general economic development of the Philippines.

Firms engaged in

projects in the interest of

the country’s general

economic development

Export-oriented firms

locating within identified

economic zones

Firms locating in special

industrial & commercial

free port zones in Subic

Bay & Clark

Concessionary tax and

regulatory treatment for

MNCs establishing HQ

operations in the

country

. Fiscal Incentives

• Exemption from taxes and duties on

imported spare parts (NOLCO)

• Exemption from wharfage dues and

export tax, duty, impost and fees(GIE)

• Reduction of the Rates of Duty on

Capital Equipment, Spareparts and

Accessories by Virtue of EO 528

• Tax exemption on breeding stocks and

genetic materials

• Tax Credits

• Additional deductions from Taxable

Income

. Non-Fiscal Incentives

• Employment of Foreign Nationals

• Simplification of customs procedures

• Importation of consigned equipment

• Privilege to operate a bonded

manufacturing/trading warehouse

THANK YOU

Top Related