Languages

Pages

Legal

EFSE Annual Meeting 2012Tbilisi, June 01

Technical Workshop

Local Currency Finance – How to scale it up?

Hosted by the Currency Exchange Fund (TCX)

2

Moderator

Cornelis van Aerssen

Investment Officer, FMO

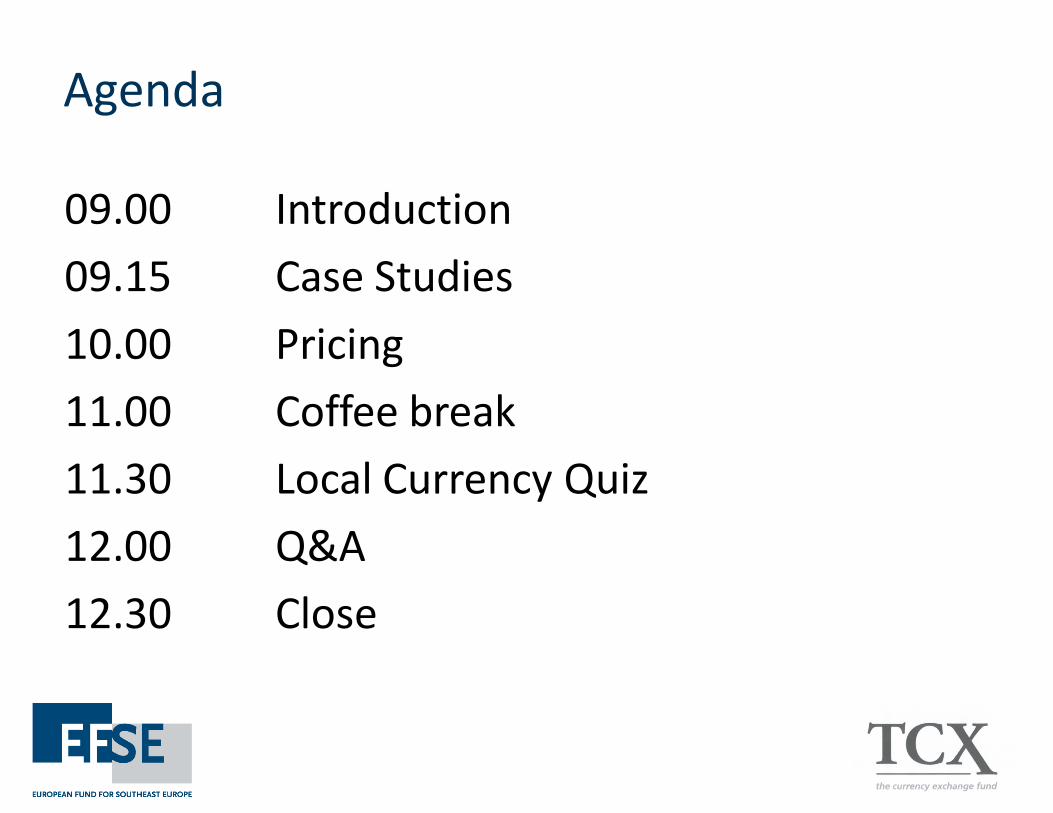

Agenda

09.00 Introduction

09.15 Case Studies

10.00 Pricing

11.00 Coffee break

11.30 Local Currency Quiz

12.00 Q&A

12.30 Close

EFSE and TCX - partners in local currency

• TCX– currency hedging for longer tenors in frontier markets

– quotes 15 currencies in SEE and Caucasus

– Largest exposures in AMD, AZN and GEL

– more than half in the microfinance sector

• EFSE and TCX– EFSE is one of TCX’s most active shareholders

– EFSE offers LCY funding in its focus countries with hedging support from market parties and TCX

– EFSE may support (guarantee) direct hedging with TCX

TCX investors & counterparties

TCX Team

Joost Zuidberg: CEO

Brice Ropion: COO

Diederik van Leur: BO

Martje Troost-Graffelman: BO

Leon Meppelink: BO

Bert van Lier: Trading

Andrej Sorochan: Trading

Othmane Boukrami: Trading

Damian Rozo Munoz: Trading

Harald Hirschhofer: Research

Jos Kramer: Research

Bill Piccolo: Operations

Ilona Eichler: Office Manager

Per van Swaay: Structuring

Jerome Pirouz: Structuring

Philip Buyskes: Structuring

Jorge Gomes: Structuring

EFSE countries of operations

Intro Question (1)35

You are working for :

1 – an Microfinance Institution

2 – a Bank

3 – a Central Bank

4 – A DFI (Development Finance Institution) or a MIV

5 - Other

You are working for :

1 – an Microfinance Institutions

2 – a Bank

3 – a Central Bank

4 – A DFI or a MIV

5 - Other

9%

26%

17%

37%

11%

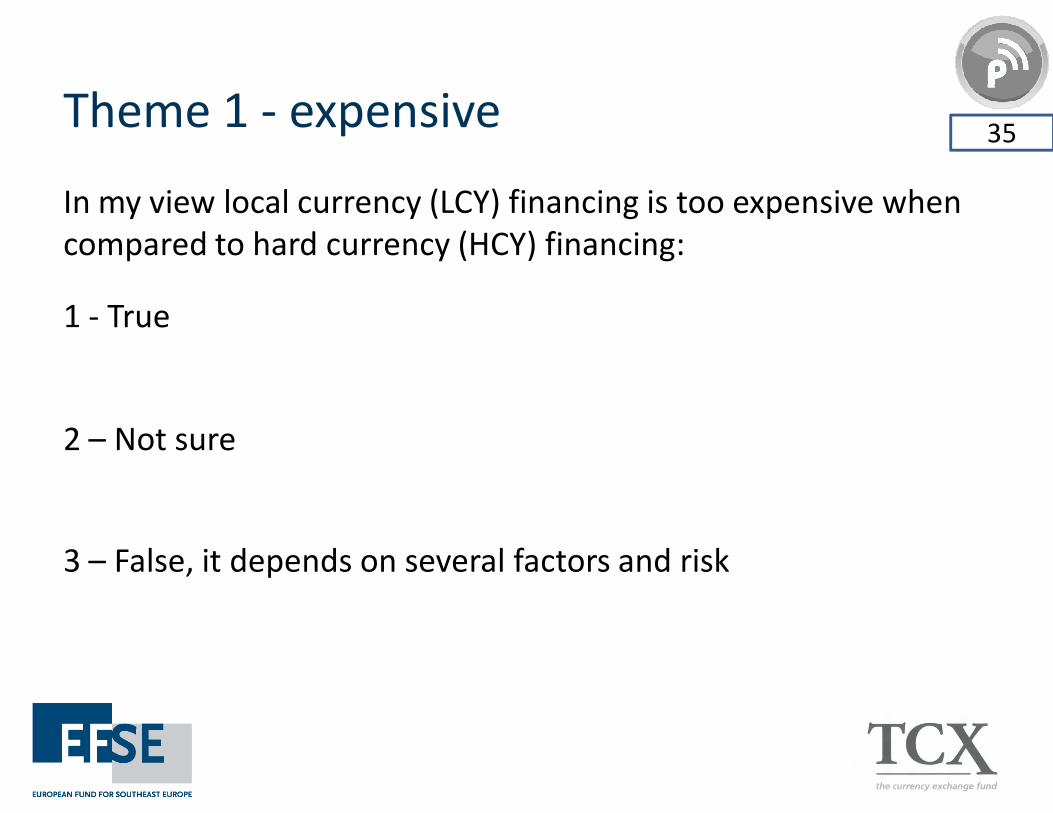

Theme 1 - expensive 35

In my view local currency (LCY) financing is too expensive when

compared to hard currency (HCY) financing:

1 - True

2 – Not sure

3 – False, it depends on several factors and risk

Theme 2 - complexity35

The legal and technical complexities of LCY hedging/funding

are too great for the beneift it provides

1 - Yes

2 – No

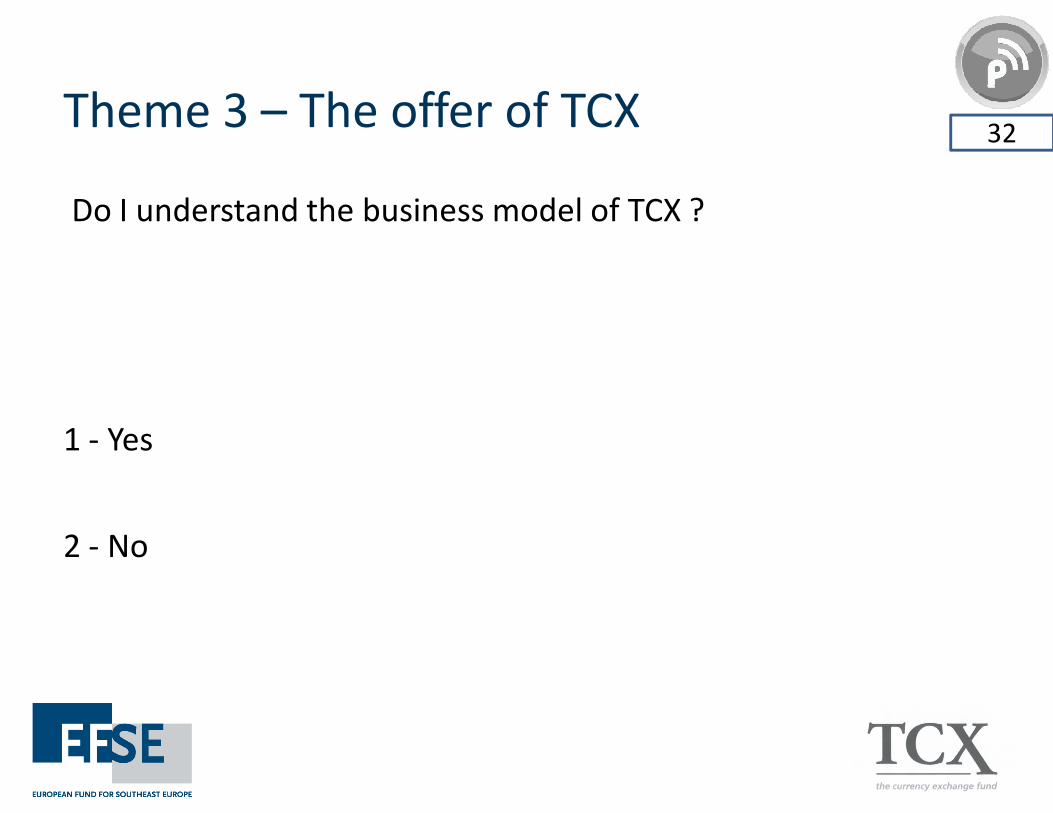

Theme 3 – The offer of TCX 32

Do I understand the business model of TCX ?

1 - Yes

2 - No

Original Sin

“A situation in which a borrower cannot borrow in his

local currency abroad, or even long term domestically”

Eichengreen & Haussman -1999

Original Sin may result in:32

1 - currency mismatches

2 - maturities mismatches

3 – none if EFSE is involved

4 - all of the above

1 - currency mismatches

2 - maturities mismatches

3 – none if EFSE is involved

4 - all of the above

63%

6%

0%

31%

Original Sin

Borrower requires

• Local Currency

• Long Term

Short Term XLocal Currency

Domestic

markets

Result: Maturity mismatch

Hard Currency

X

Foreign markets

Long Term

Result: Currency mismatch

Local Currency

Currency Match

Capital market development

LCY bond issues

Foreign guarantees for longer

tenor funding from local banks

Building longer deposit base

Local Back-To-Back facility

Commercial swap dealers

TCX Fund

ESRB recommendations

21 September 2011

On lending in foreign currencies

The European Systemic Risk Board (ESRB)

• 2008 financial crisis

• Focus on systemic risk in the EU

• 2011 recommendations on lending in foreign currency

“In response to excessive foreign currency lending in several Member States”

Excessive Foreign Currency Lending

Foreign Debt StockTotal Debt Stock

Systemic risks identified

• Exchange rate risk and interest rate risk

• Funding risks as local banks rely on parent and

wholesale markets instead of deposits

• FCY lending may fuel excessive credit growth

and asset bubbles

• Concentration and spill-over effects

• Monetary policy impairment

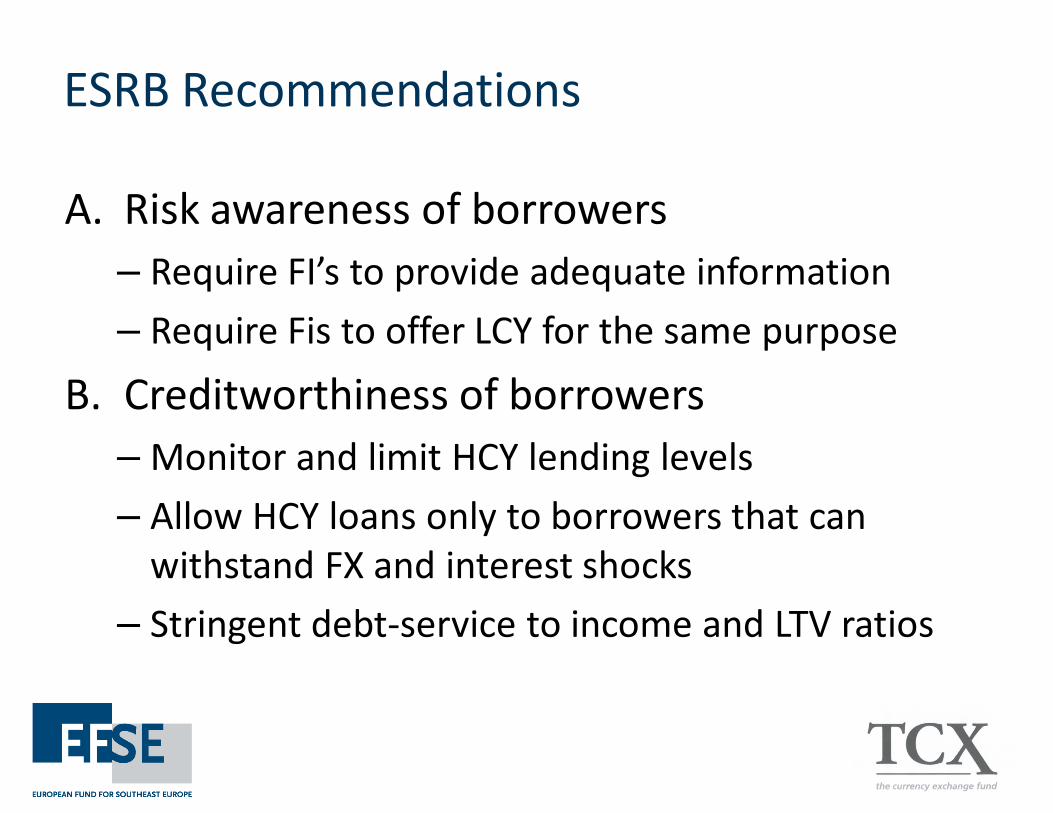

ESRB Recommendations

A. Risk awareness of borrowers

– Require FI’s to provide adequate information

– Require Fis to offer LCY for the same purpose

B. Creditworthiness of borrowers

– Monitor and limit HCY lending levels

– Allow HCY loans only to borrowers that can

withstand FX and interest shocks

– Stringent debt-service to income and LTV ratios

ESRB Recommendations

C. Credit Growth induced by HCY lending

– Monitor excessive credit growth and adopt more stringent measures if the case

D. Internal risk management

– FI to better incorporate foreign currency lending risk (internal risk pricing and capital allocation)

E. Capital requirement:

– Fis to hold capital for HCY lending (non lineair rrelationship between market and credit risk)

ESRB Recommendations

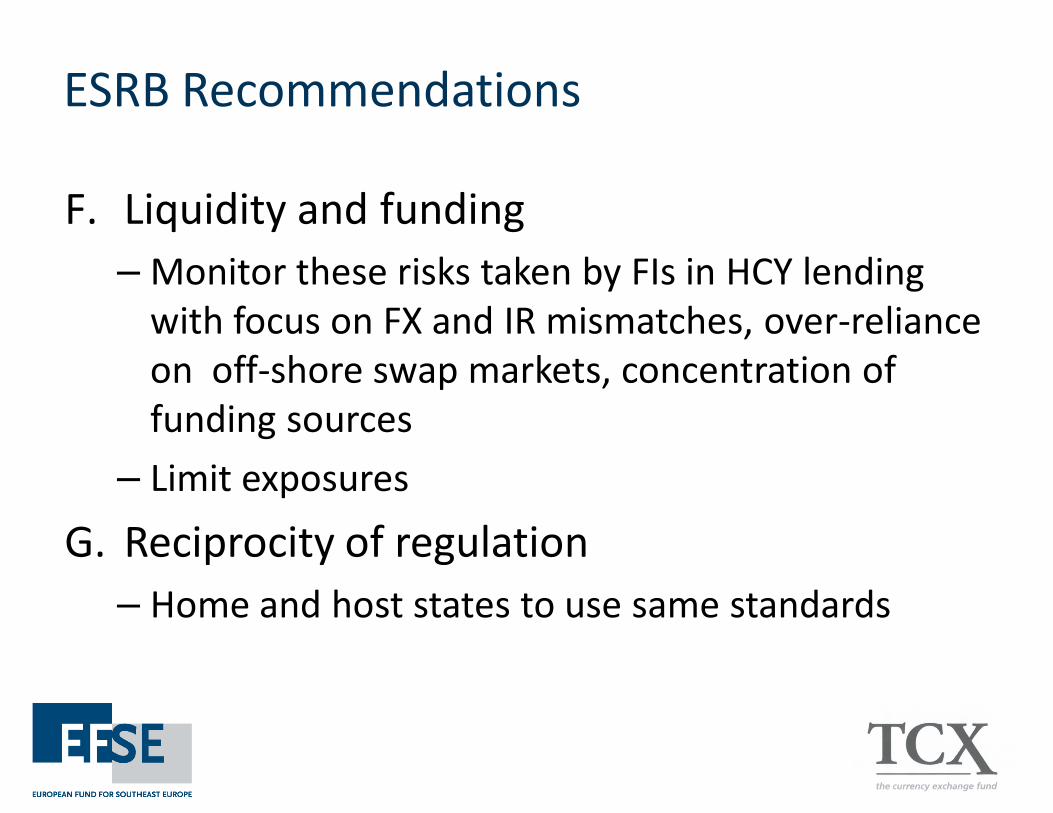

F. Liquidity and funding

– Monitor these risks taken by FIs in HCY lending

with focus on FX and IR mismatches, over-reliance

on off-shore swap markets, concentration of

funding sources

– Limit exposures

G. Reciprocity of regulation

– Home and host states to use same standards

2 Case studies

A borrower should fund itself in his local

currency, instead of USD/EUR

32

1 - If the cost of local currency is similar to that of USD funding

2 - to the extent that his revenue and assets are in local currency

3 - to the extent he has local currency expenses

4 - If the currency concerned is very volatile

1 - If the cost of local currency borrowing is similar to that of the alternative USD

funding

2 - If and to the extent that his revenue and assets are in local currency

3 - If its net profit margin is positive after factoring in the cost of the swap

4 - If the currency concerned is very volatile and has been devaluated in the past

6%

69%

6%

19%

Case Study 1

• In Macedonia

• A tier-1 bank

• Requires 3-year funding

• To lend to SME’s at the Bank’s deposit rates

What funding structures would you consider?

What benchmark should you select?

Case 1: the “synthetic” local currency loan

TCX

offshore

Macedonia

Case 1 -Disbursement of the Loan

Loan denominated in MKD, but disbursement in EUR

Floating rate: 28-Day CB Bill + 71 bps + EFSE credit margin

FX Spot Market for

EUR/MKD

Euribor 6-m

28-Day CB Bill + 71bp

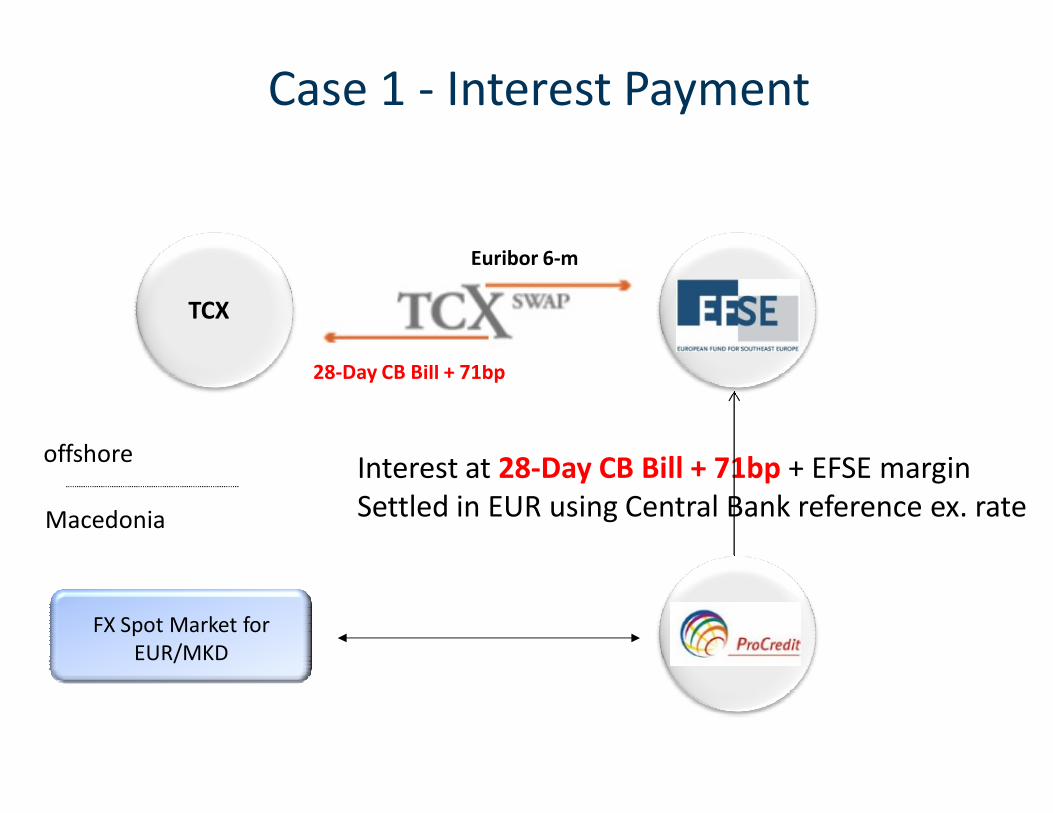

Interest at 28-Day CB Bill + 71bp + EFSE margin

Settled in EUR using Central Bank reference ex. rate

Case 1 - Interest Payment

TCX

offshore

Macedonia

FX Spot Market for

EUR/MKD

Euribor 6-m

28-Day CB Bill + 71bp

Case 1 - Principal Repayment

TCX

offshore

Macedonia

FX Spot Market for

EUR/MKD

EUR principal

MKD principal

MKD principal repaid in year 3

Settled in Euro’s using Central Bank reference ex. rate

Case 1 - “synthetic” vs “domestic”

• Synthetic– LCY but HCY settlement

– “non-deliverable”

• Alternative “domestic” LCY loan– LCY loan and settlements in LCY -> “deliverable”

– Supported by TCX (currently in 14 countries)

– Subject to commercial demand & legal framework

– Currently not in Caucasus

• Key benefits to borrower– No liquidity/settlement risk -> borne by TCX

– Convenience factor

Case 1 - “Synthetic” vs “domestic”

Risk type Synthetic

Loan

Domestic

Loan

Market Risk TCX TCX

Credit Risk Lender Lender

Hedge / Loan Match Risk Lender None

Liquidity Risk Borrower TCX

Convertibility Risk Lender Lender

Settlement Risk Borrower TCX

Case 1 - swap result and credit risk

Disbursement Repayment

Exchange rate 1:10 1:12 1:8

Borrower receives/repays in LCY 100 100 100

Lender disburses / receives in USD 10 8,3 12,5

Lender receives from TCX 1,7 -

Lender pays to TCX - 2,5

Net result Lender 10 10

Net result Borrower 100 100

Net result TCX -1,7 2,5

1. Swap fixes USD value of Lender’s assets and income 2. Swap fixes LCY value of Borrower’s obligation 3. TCX may owe or be owed money under the swap

Case 1 - ISDA / CSA

• Standard derivative documentation

• ATE, netting and collataral provisions

• Collateral subject to credit quality

– Independent Amount as a % of notional

– Thresholds

– Minimum Transfer Amounts

• TCX has concluded ISDA with EFSE and all other active shareholders

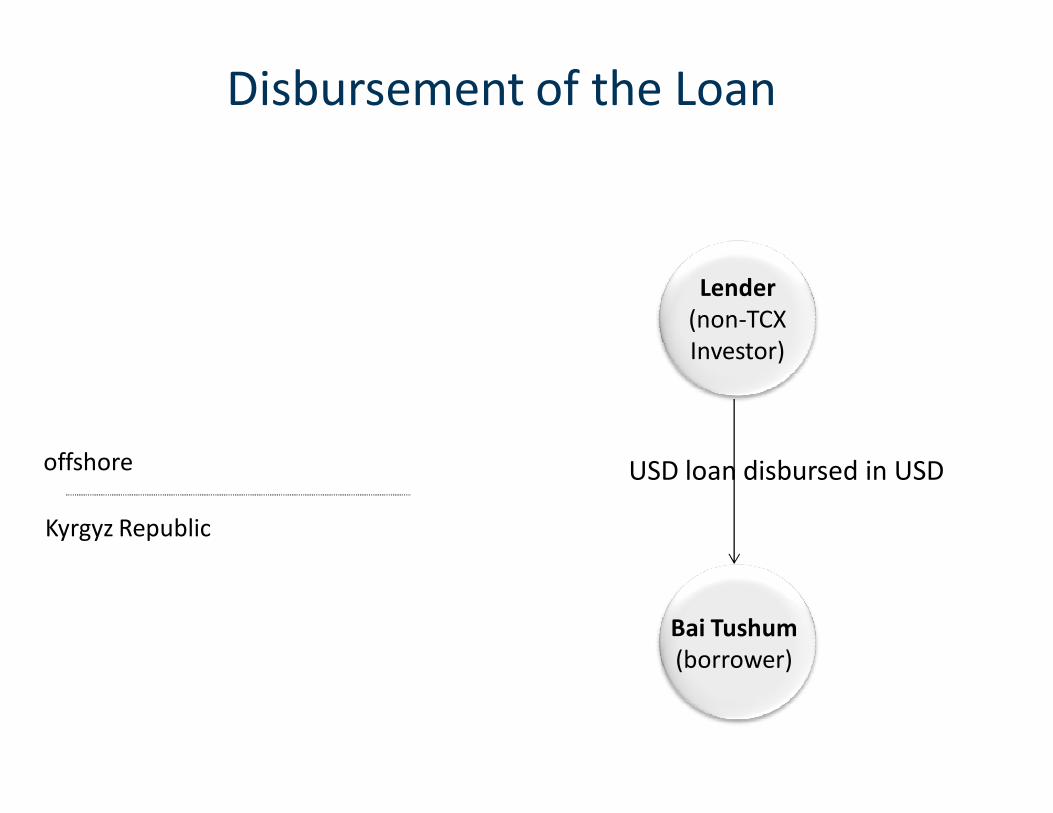

Case Study 2

• A top tier MFI in Kyrgyz

• With LCY and USD funding from multiple

sources, TCX and non-TCX shareholders

• Facing shortage of domestic hedging sources

• Must close open FX positions

Case 2 - Direct Hedging of the end-client

Lender

(non-TCX

Investor)

Bai Tushum

(borrower)

offshore

Kyrgyz Republic

Disbursement of the Loan

USD loan disbursed in USD

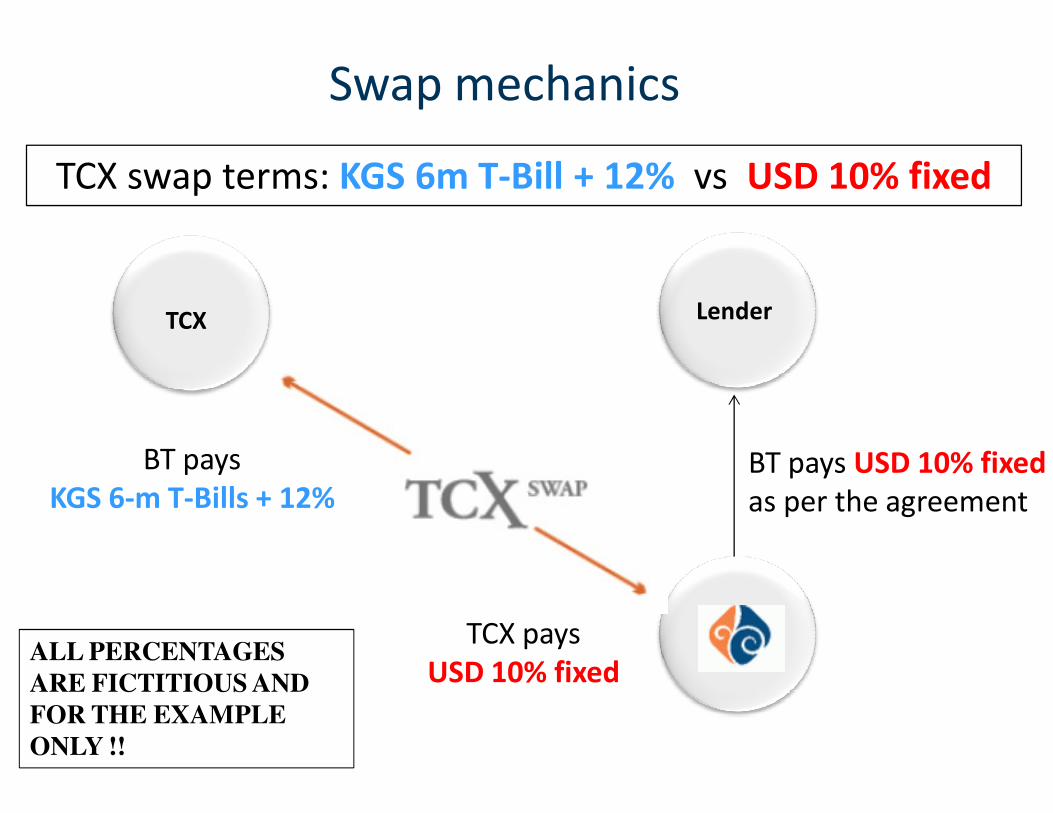

Swap mechanics

TCX pays

USD 10% fixed

BT pays

KGS 6-m T-Bills + 12% BT pays USD 10% fixed

as per the agreement

TCX Lender

TCX swap terms: KGS 6m T-Bill + 12% vs USD 10% fixed

ALL PERCENTAGES

ARE FICTITIOUS AND

FOR THE EXAMPLE

ONLY !!

Direct hedging and collateral

• TCX and counterparty both run credit risk

• TCX is “in the money” if the LCY appreciates and if LCY interest rates go down

• TCX must mitigate this risk; options:

– Standard ISDA/ CSA terms

– Investor / Lender guarantee -> EFSE support !

– Credit Support Fund ?

– Daily valuation to minimize collataral upfront ?

MFI

(borrower)

offshore

onshore

Cash collateral exchange

TCX

(hedger)

An EFSE guarantee to cover TCX credit risk…

.....may reduce the need for

cash collateral (completely)

Cash collateral as MtM moves

Rolling forwards

Rolling Forwards

Borrowers concerns with

swaps

• Benchmark selection

• Interest rate volatility

• Unwind costs

• The high level of the fixed

rate alternative

Solution? Rolling Forward product

• Rolling 6m FX Forwards

• Option to request

conversion to USD If

benchmark exceeds an

agreed threshold

• TCX commits to price

forwards for duration of

the deal

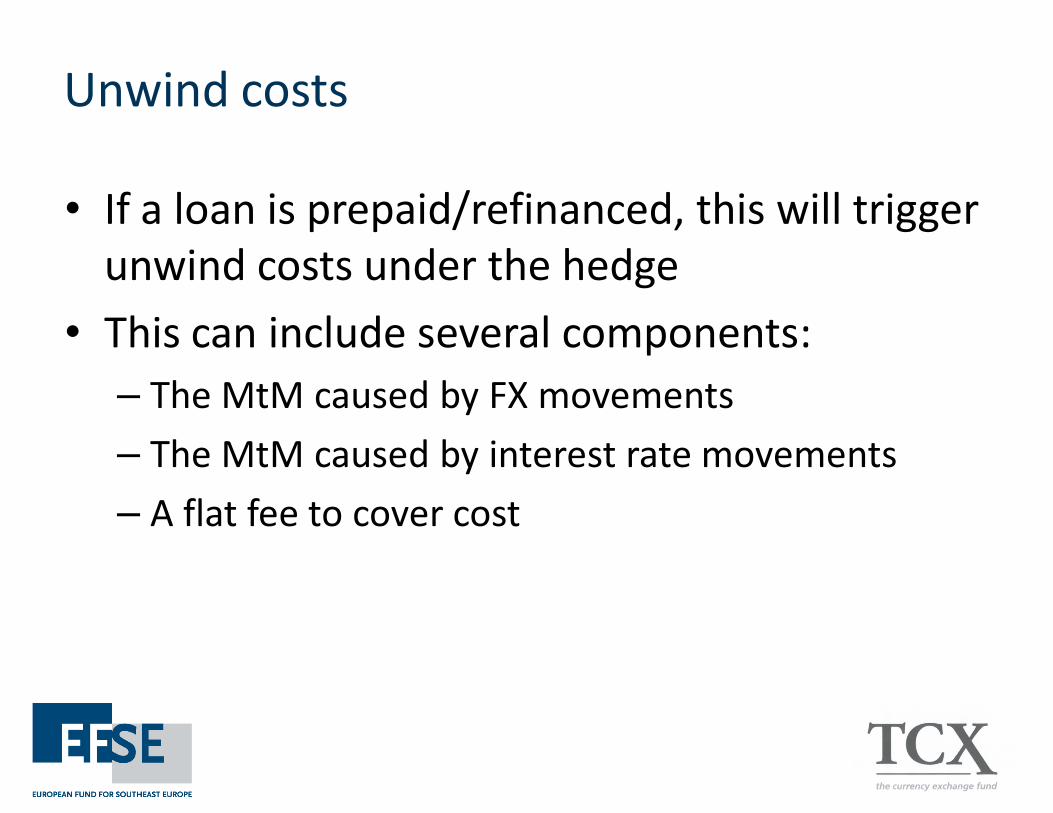

Unwind costs

• If a loan is prepaid/refinanced, this will trigger

unwind costs under the hedge

• This can include several components:

– The MtM caused by FX movements

– The MtM caused by interest rate movements

– A flat fee to cover cost

Unwind costs – an Example

• In June 2012

– Lender provides a 3 year bullet GEL 1m at 12%

– Lender hedges with TCX: GEL 12% vs EUR 7%

– EUR:GEL is 1:2.0 and 3 year fixed rate is 12%

• In June 2013

– EUR:GEL is 1:2.2 and 3 year fixed rate is 14%

– For lender, the FX component of MtM is

– For lender, the interest component MtM is

Borrower TCX Lender

GEL 12%GEL 12%

EUR 7%

positive

positive

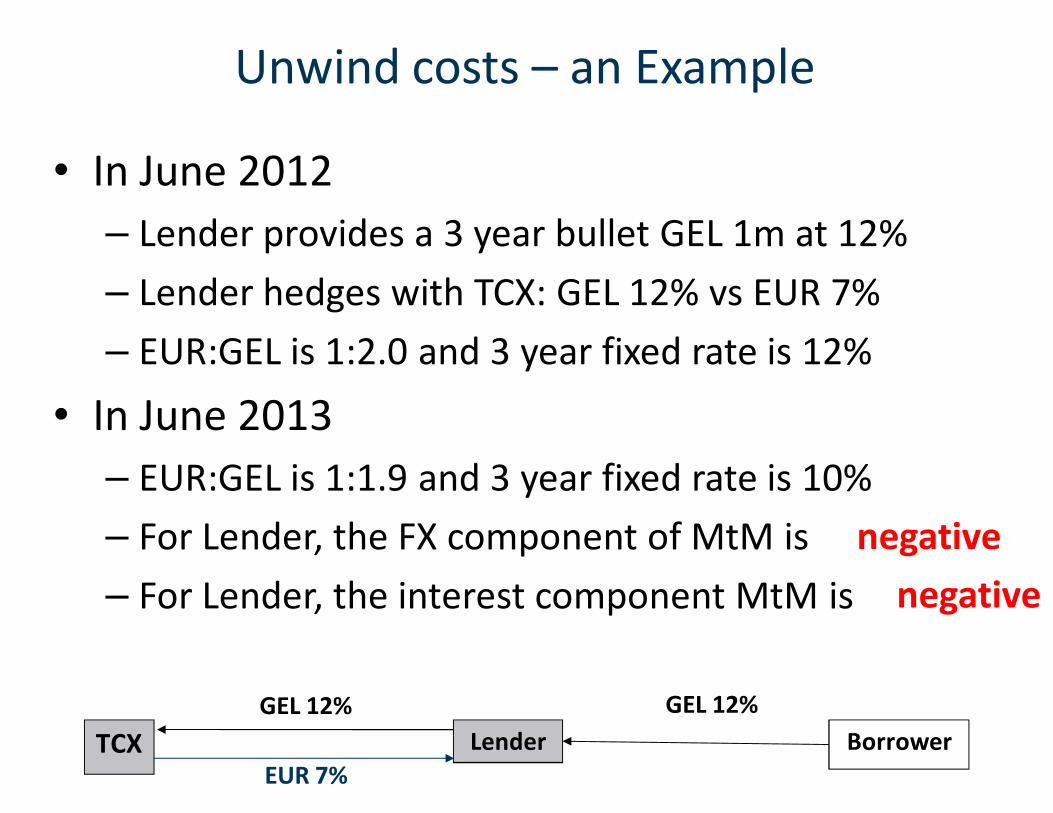

Unwind costs – an Example

• In June 2012

– Lender provides a 3 year bullet GEL 1m at 12%

– Lender hedges with TCX: GEL 12% vs EUR 7%

– EUR:GEL is 1:2.0 and 3 year fixed rate is 12%

• In June 2013

– EUR:GEL is 1:1.9 and 3 year fixed rate is 10%

– For Lender, the FX component of MtM is

– For Lender, the interest component MtM is

Borrower TCX Lender

GEL 12%GEL 12%

EUR 7%

negative

negative

Unwind costs

• The FX component of MtM is off-set by an opposite movement in the USD value of the loan

• The interest component of MtM is not off-set by an opposite movement in the value of the loan

• Lender and borrower negotiate who bears which unwind costs under which circumstances

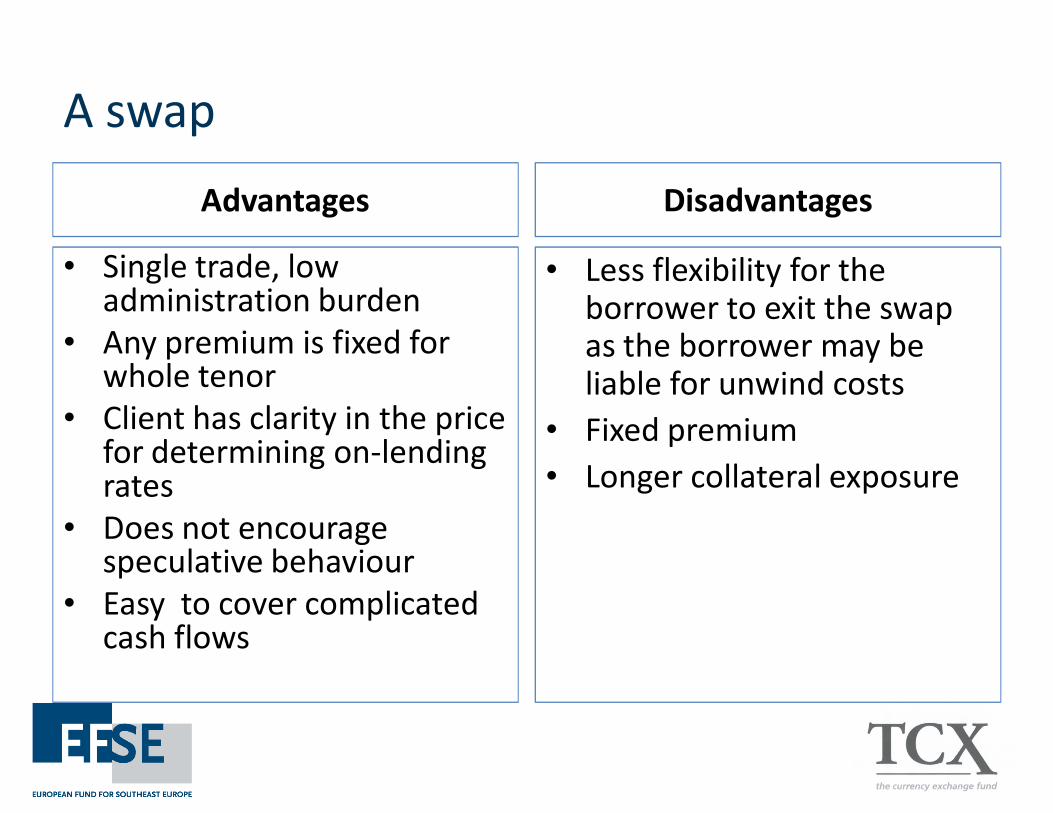

A swap

Advantages

• Single trade, low administration burden

• Any premium is fixed for whole tenor

• Client has clarity in the price for determining on-lending rates

• Does not encourage speculative behaviour

• Easy to cover complicated cash flows

Disadvantages

• Less flexibility for the borrower to exit the swap as the borrower may be liable for unwind costs

• Fixed premium

• Longer collateral exposure

Rolling forward product

Advantages

• Minimises potential

unwinding costs if borrower

wants to prepay or convert

• Does not lock-in a long term

premium

• Minimises collateral

exposure

Disadvantages

• No pricing certainty

• Less pricing transparency

• Swap premiums may move

against the borrower

• Heavier administration

burden for the lender

Pricing local currency

Andrej Sorochan

An MFI is offered a 3 year USD loan of USD Libor + 6% and a

Manat loan, his local currency, at a rate of 6m T-Bill + 7%. The

current 6m T-Bill rate is 3%. The Manat loan:

29

1 - Is 3% more expensive than the USD loan

2 - is cheaper because of lower operational cost in Manat

3 - has a higher nominal interest rate but does not necessarily

present a higher economic cost

1 - Is 12% more expensive than the USD loan

2 - is cheaper because of lower operational cost in Manat

3 - has a higher nominal interest rate but does not necessarily

present a higher economic cost

14%

0%

86%

You can ask EFSE

(who will interact with TCX) to : 28

1 - Quote floating rates provided there is a benchmark

2 - Quote fixed rates in most markets

3 - Start quoting a new currency on request

4 - All above are true

1 - Quote floating rates provided there is a benchmark

2 - Quote fixed rates in most markets

3 - Start quoting a new currency on request

4 - All above are true

29%

11%

11%

50%

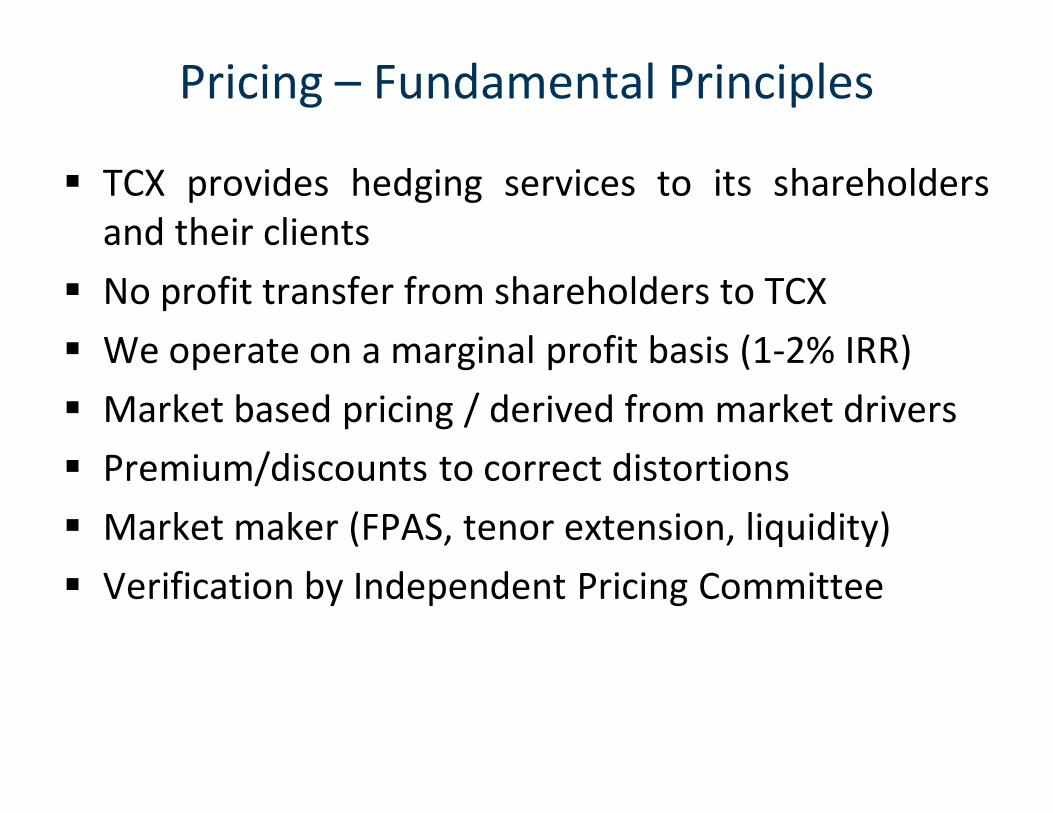

Pricing – Fundamental Principles

� TCX provides hedging services to its shareholders

and their clients

� No profit transfer from shareholders to TCX

� We operate on a marginal profit basis (1-2% IRR)

� Market based pricing / derived from market drivers

� Premium/discounts to correct distortions

� Market maker (FPAS, tenor extension, liquidity)

� Verification by Independent Pricing Committee

TCX pricing categories

� Developed Markets

– TCX uses offshore screen-rates. Additionality principle needs to be

proven. (UAH, KZT, TRY)

� Undeveloped offshore markets, but a functioning benchmark and

onshore curve

– TCX uses the onshore curve plus or minus a spread approved by the

Pricing Committee (ALL, HRK, RSD, GEL, AMD, AZN)

� Unavailability of offshore and onshore curve, but a functioning

benchmark could be selected

– TCX prices floating rates only, based on the approved benchmark plus

or minus a spread (MKD, MDL)

� No suitable onshore and/or offshore reference:

– TCX prices fixed rate only up to 4-5 years based on macro-economical

models on selected countries (BYR)

TCX pricing rules

� Benchmark selection must be

– liquid

– independent, without any political interference

– market driven (reflect macro economic conditions)

– legally definable and observable on a daily basis

– expected to exist for the term of the transaction

� TCX adjusts to correct market distortions (plus/minus a spread)

� Floating rate using approved benchmark: no maximum tenor

� Fixed rate/Forwards: 1,5x longer than longest market point

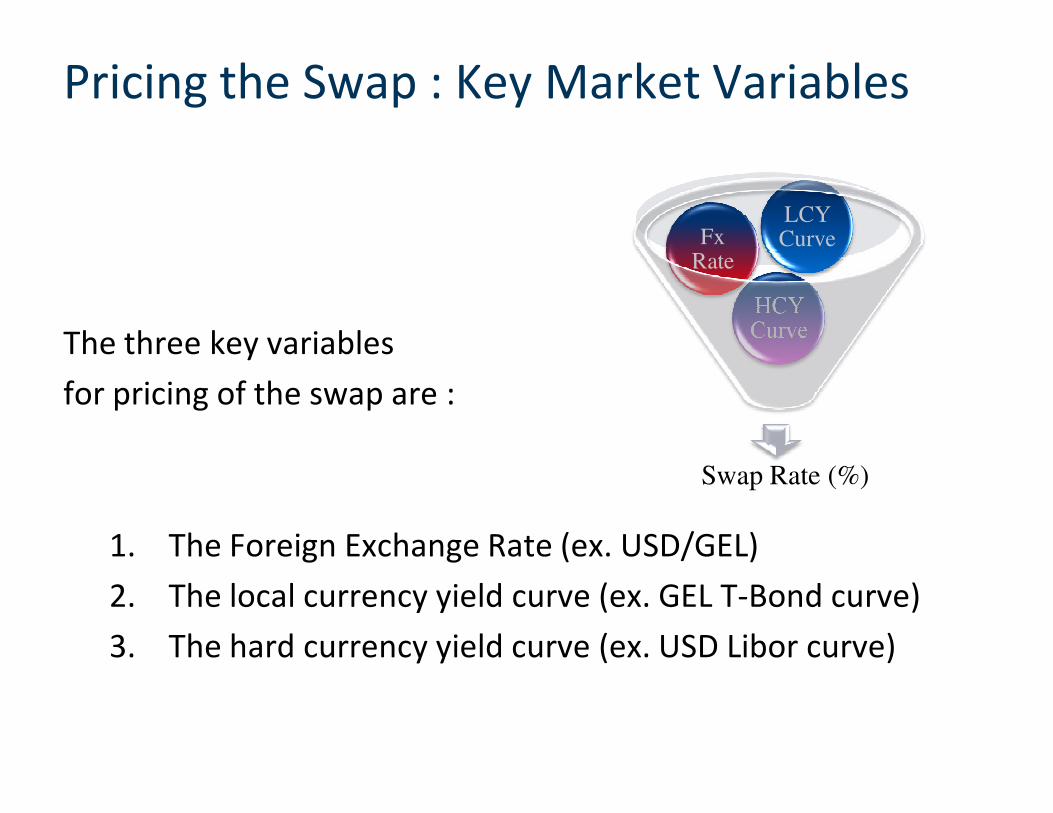

Pricing the Swap : Key Market Variables

The three key variables

for pricing of the swap are :

1. The Foreign Exchange Rate (ex. USD/GEL)

2. The local currency yield curve (ex. GEL T-Bond curve)

3. The hard currency yield curve (ex. USD Libor curve)

Swap Rate (%)

HCY Curve

FxRate

LCY Curve

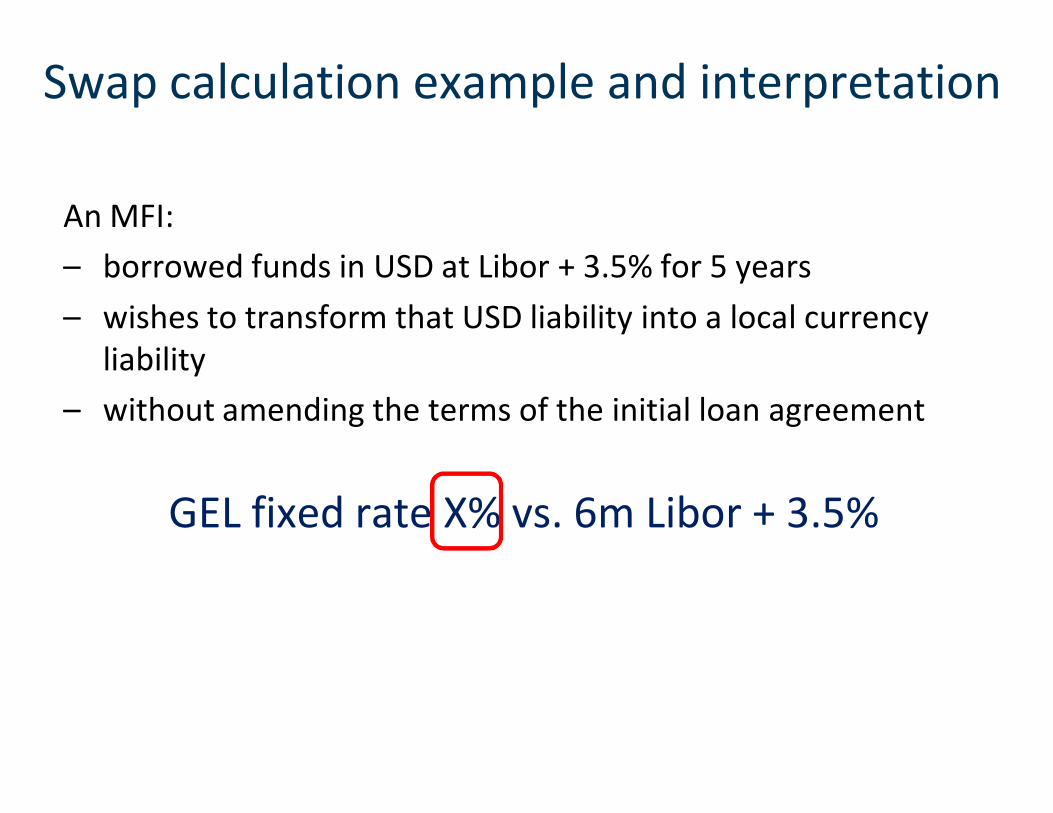

Swap calculation example and interpretation

An MFI:

– borrowed funds in USD at Libor + 3.5% for 5 years

– wishes to transform that USD liability into a local currency

liability

– without amending the terms of the initial loan agreement

GEL fixed rate X% vs. 6m Libor + 3.5%

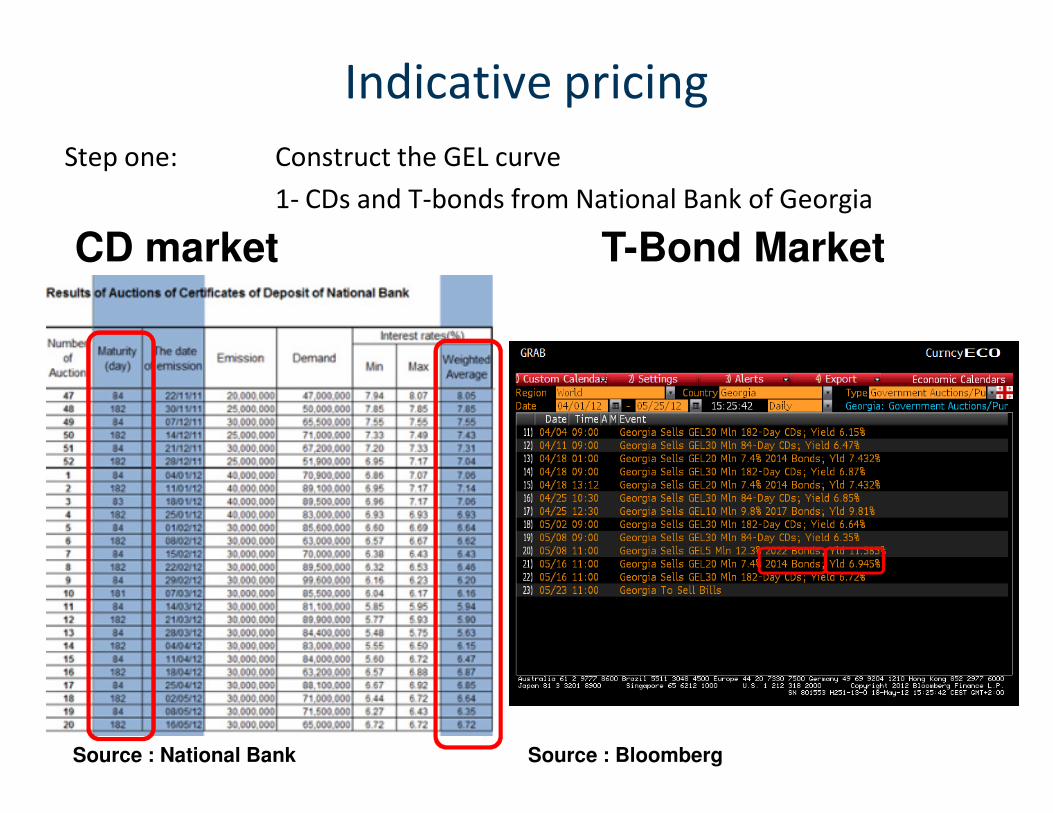

Indicative pricing

Step one: Construct the GEL curve

1- CDs and T-bonds from National Bank of Georgia

CD market T-Bond Market

Source : National Bank Source : Bloomberg

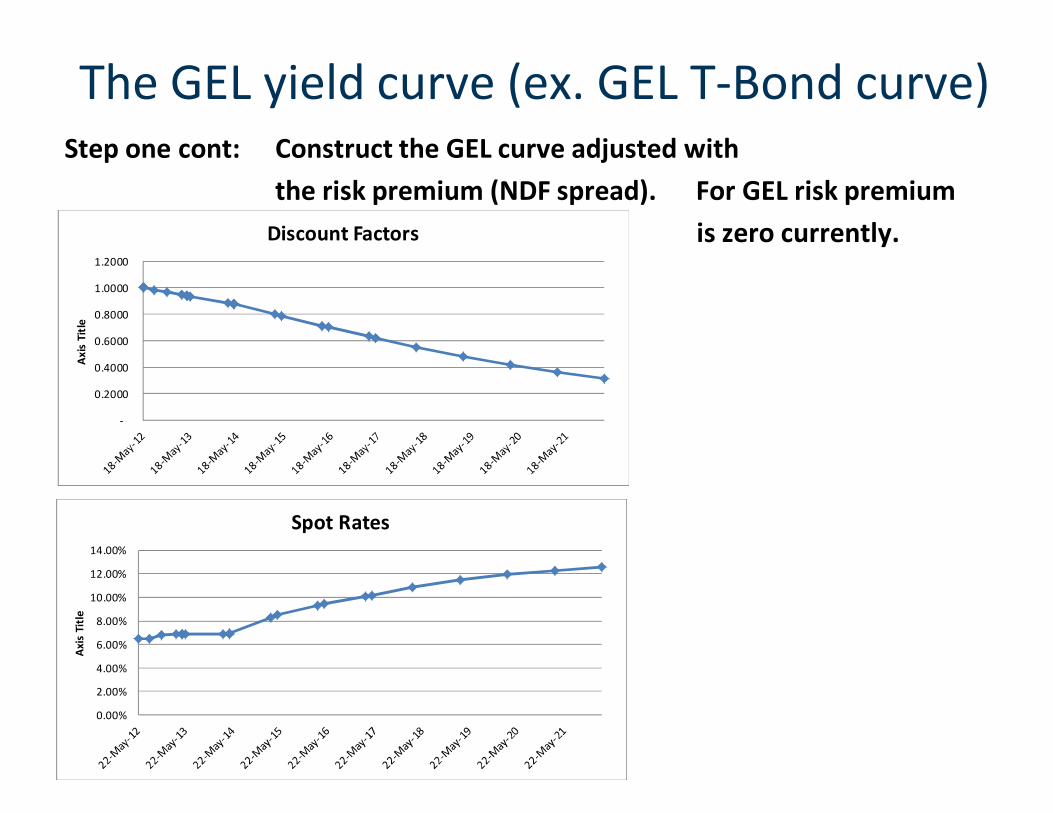

The GEL yield curve (ex. GEL T-Bond curve)Step one cont: Construct the GEL curve adjusted with

the risk premium (NDF spread). For GEL risk premium

is zero currently.

-

0.2000

0.4000

0.6000

0.8000

1.0000

1.2000

Ax

is T

itle

Discount Factors

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Ax

is T

itle

Spot Rates

The USD yield curve (ex. USD Libor curve)

Step two: Contruct the USD Curve. Libor up to 6m and swap rates

thereafter

Grid Point rate

1M 0.24%

2M 0.35%

3M 0.47%

6M 0.74%

9M 0.91%

12M 1.07%

2 year 0.66%

3 year 0.75%

4 year 0.91%

5 year 1.10%

6 year 1.29%

7 year 1.46%

8 year 1.62%

9 year 1.75%

10 year 1.86%

12 year 2.06%

15 year 2.26%

20 year 2.41%

The Foreign Exchange Rate (ex. USD/GEL)

Step three: Discount all future USD flows with the USD curve and solve

for the GEL rate to have zero present value

Pricing of the Swap : Concept

NPV of LCY leg

-

NPV of USD leg

0

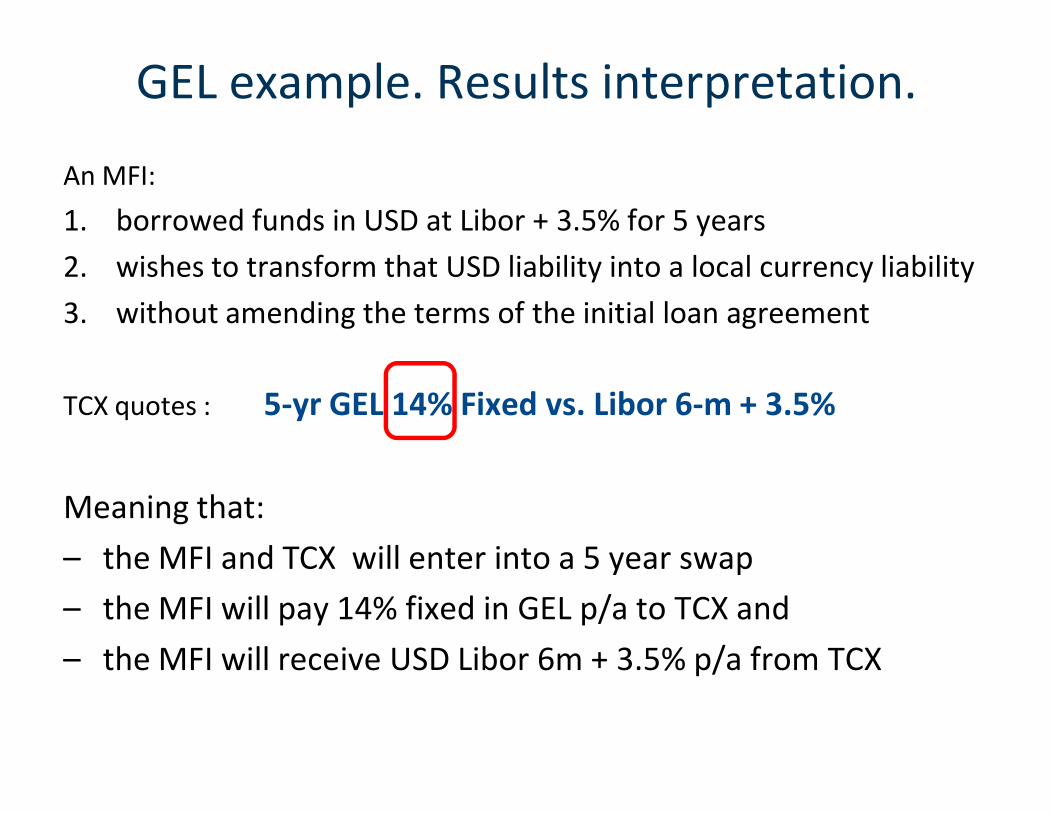

GEL example. Results interpretation.

An MFI:

1. borrowed funds in USD at Libor + 3.5% for 5 years

2. wishes to transform that USD liability into a local currency liability

3. without amending the terms of the initial loan agreement

TCX quotes : 5-yr GEL 14% Fixed vs. Libor 6-m + 3.5%

Meaning that:

– the MFI and TCX will enter into a 5 year swap

– the MFI will pay 14% fixed in GEL p/a to TCX and

– the MFI will receive USD Libor 6m + 3.5% p/a from TCX

GEL example. Price interpretation.

Client pays Libor + 3.5% to DFI under loan agreement (-)

Client receives Libor +3,5% from TCX under the swap (+)

Client pays 14% Fixed GEL to TCX under the swap (-)

----------------------------------------------------------------------------------

= Client pays 14% Fixed GEL to TCX under the swap (-)

The swap helped the client to transform a USD loan into a

GEL loan

Pricing of the Swap : Concept

When you enter into the swap on the day of the trade

• You pay GEL 14% fixed to TCX

• You receive Libor 6-m +3.5% from TCX

For the swap to be a fairly priced on the day of the trade the value (NPV) of

the LCY leg paid to TCX must be equal to the value of the USD leg received

from TCX.

The premium paid on the GEL is the X of the equation that makes :

NPV {5-yr GEL X% Fixed} – NPV {5-yr Libor 6-m + 3.5%} = 0

or

NPV {5-yr GEL X% Fixed} = NPV {5-yr Libor 6-m + 3.5%}

NPV of LCY leg

-

NPV of USD leg

Central and Eastern Europe & the Caucasus

Country ISO Benchmark Basis

Swap

max

tenor

Fixed rate

max tenor

5 year floating vs.

USD Libor

3 year fixed

vs. USD Libor

Latest

6m

yield

Armenia AMD 6m T-Bill none 15 years 6m T-Bill +50 bps 13.85% 8.31%

Azerbajian AZN 6m T-Bill none 4,5 years 6m T-Bill+68 bps 4.89% 2.95%

Georgia GEL 6m CD none 15 years 6m CD+44 bps 8.48% 6.72%

Albania ALL 6m T-bill none 3 years 6m T-bill+ 30 bps 8.92% 6.30%

Croatia HRK1 6m ZIBOR none 15 years 6m ZIBOR flat 5.63% 4.10%

Moldova MDL 6m CHIMID none 1.5 years 6m Chimid+45 bps NA – 1.5Y fix max 7.57%

Serbia RSD 1 6m Belibor none 3 years 6m Belibor-63 bps 14.55% 11.01%

Ukraine UAH NA – only fixed NA 7.5 years NA 15% NA

1 Priced vs. Euribor 6m flat

All indications exclusive of lender credit margins

LCY Lender credit margin

The credit margin on a local currency loan should be equal or lower

than a credit margin on a straight USD Loan (adverse to market

practice!)..

The expected exposure of a local currency loan is less than the USD loan

exposure. To ensure constant risk / return the LCY margin (save for other

reasons to reduce) be at exactly the same level as the USD margin

� Reduced currency mismatches reduces default risk

� Currency risk and political risk are generally to some degree correlated,

implying that a currency hedge offers protection against political risk.

Local currency risk margins can be reduced relative to USD margins when

hedged with a A- rated entity.

• Compared to the USD alternative ?

• Nominal rates are high

• Inflation and depreciation effects

• Consider real interest rates

• Compared to local currency alternatives ?

• What are local banks borrowing and lending at?

• Relative to the bond curve ?

Too Expensive?

Too Expensive?

• LCY risk free curve, inflation level

• Interest rates – risk relation

Too Expensive?

• LCY risk free curve, inflation level

• Interest rates – risk relation

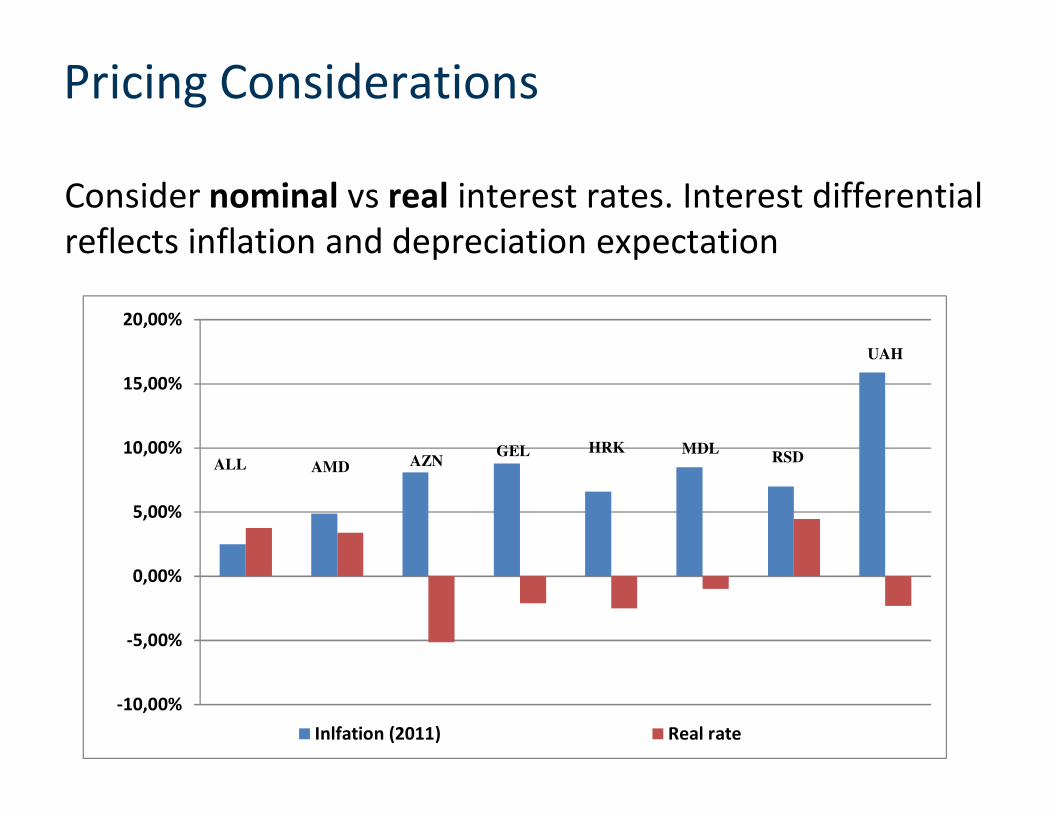

Pricing Considerations

Consider nominal vs real interest rates. Interest differential

reflects inflation and depreciation expectation

-10,00%

-5,00%

0,00%

5,00%

10,00%

15,00%

20,00%

Inlfation (2011) Real rate

ALL AMD AZNGEL HRK MDL

RSD

UAH

Forward vs. Swap

� Minimum amount for a swap is USD 1m and USD 0.5m for a forward)

� There is no arbitrage between the price of a forward and the price of a

fixed rate swap altough visually it might not seem to be the case.

Example: GEL

• 3 year Swap:

• 8.30% GEL fixed (act/365) vs. 6m USD Libor Flat (act/360)

• 14% GEL fixed (act/365) vs. 6m USD Libor + 5% (act/360)

• 14% GEL fixed (act/365) vs. USD 5,75% USD fixed

• 3 year FX Forward

• Spot: 1.6250

• Forward: 2.0181

Forward Calcs Cont

• Forward (3 years), number of days 1095

• Spot: 1.6250

• Forward: 2.0181

(1 + GEL rate) ^ (number days) / 365)

• Forward = Spot *

(1 + USD rate) ^ (number days) / 360)

If you wish to achieve a USD rate of 5,75%, then

(1 + GEL rate) ^ ((number days) / 365) = Forward * (1 + USD rate) ^ (num

ber days) / 360) / Spot

(1 + GEL rate) ^ (1095 / 365) = 2.0181 * (1 + 5,75%) ^ (1095) / 360)

/ 1.6250

(1 + GEL rate) ^ (1095 / 365) = 1,4724

GEL rate = 13.8%, is 13.8% more expensive than 14% on the swap?

TCX webpage

a) TCX benchmarks and maturities:

https://www.tcxfund.com/countries-benchmarks

b) TCX Model based pricing:

FPAS Countries:

Central Europe & Asia: Belarus, Tajikistan, Uzbekistan & Mongolia

East Asia: Cambodia

Africa: Kenya, DR Congo, Ethiopia, Nigeria, Tanzania, Uganda & Rwanda

Central America & Caribbean: Guatemala & Haiti

https://www.tcxfund.com/macroeconomic-country-forecasts

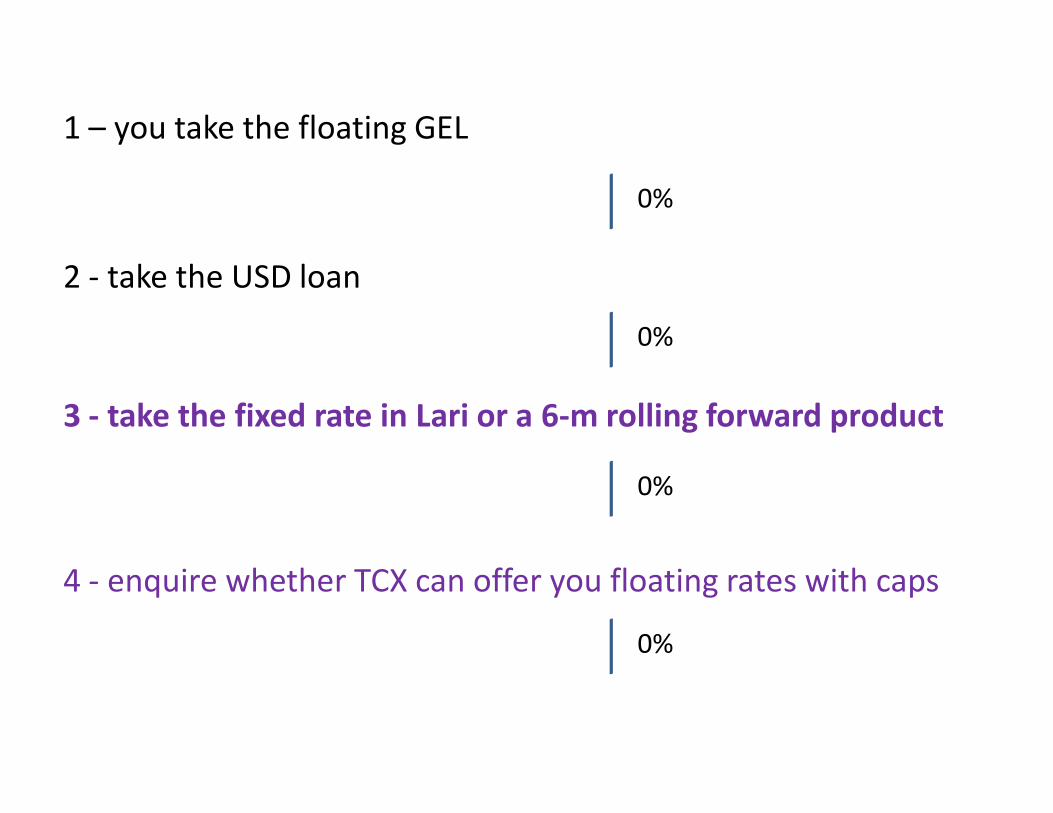

A Georgian bank lends to its clients in Lari at fixed rates.

A Lender offers the choice between :

- USD floating loan at Libor + 6%

- Lari loan T-bill + 7% or a fixed rate loan at 22%.

You

0

1 – take the GEL floating because currency risk is worse

than interest rate risk

2 - take the USD loan

3 - take the fixed rate in Lari or request a 6-m rolling forward product

4 - enquire whether TCX can offer you floating rates with caps

1 – you take the floating GEL

2 - take the USD loan

3 - take the fixed rate in Lari or a 6-m rolling forward product

4 - enquire whether TCX can offer you floating rates with caps

0%

0%

0%

0%

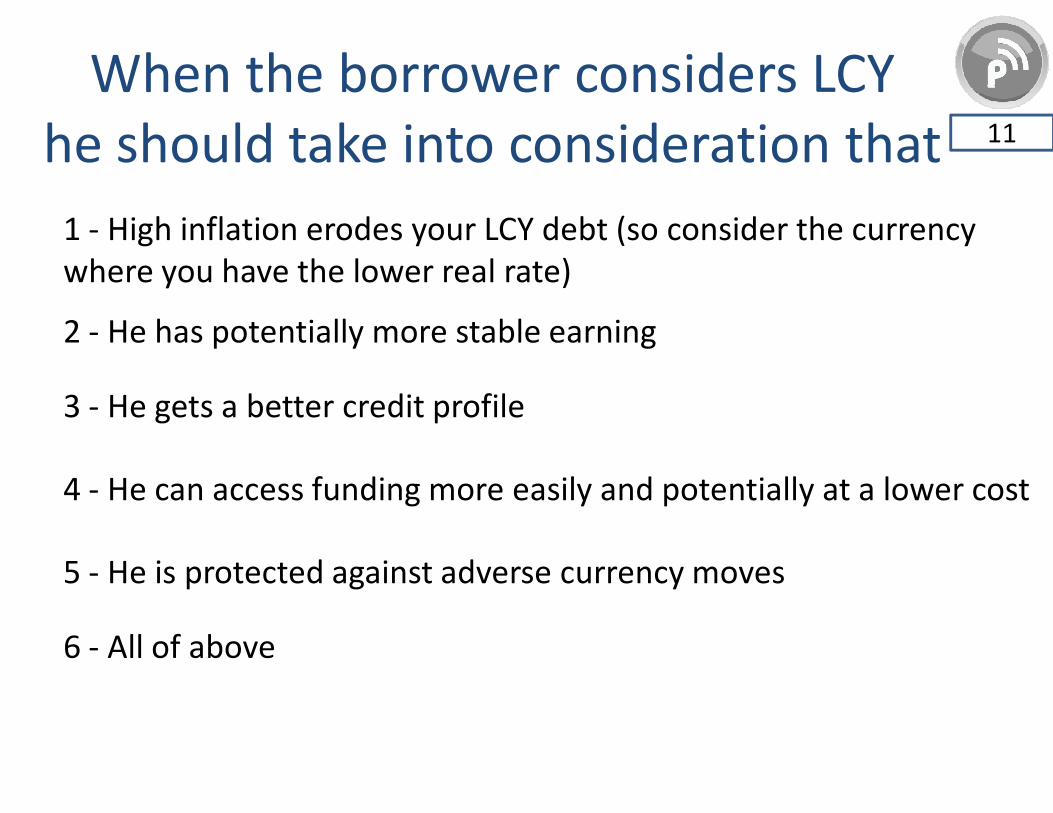

When the borrower considers LCY

he should take into consideration that 11

1 - High inflation erodes your LCY debt (so consider the currency

where you have the lower real rate)

2 - He has potentially more stable earning

3 - He gets a better credit profile

4 - He can access funding more easily and potentially at a lower cost

5 - He is protected against adverse currency moves

6 - All of above

1 - High inflation erodes your LCY debt (so consider the currency

where you have the lower real rate)

2 - He has potentially more stable earning

3 - He gets a better credit profile

4 - He can access funding more easily and potentially at a lower cost

5 - He is protected against adverse currency moves

6 - All of above

9%

0%

9%

0%

36%

45%

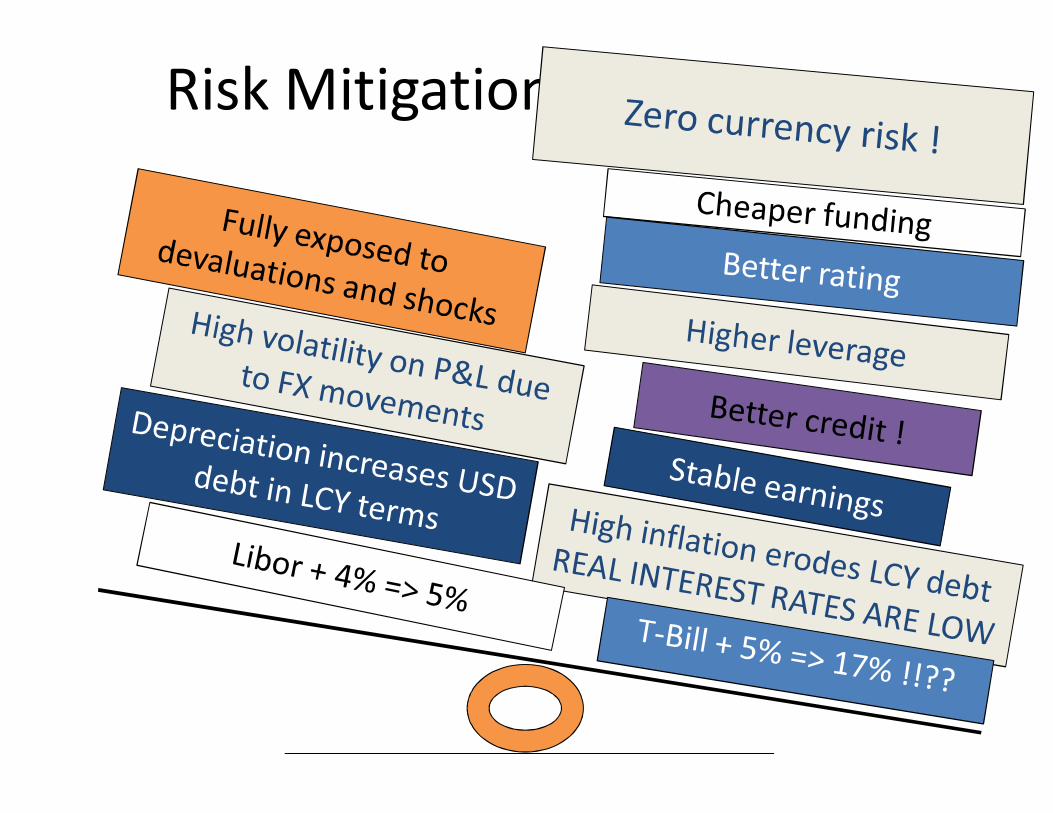

Risk Mitigation Benefits

Libor + 4% => 5% T-Bill + 5% => 17% !!??

High inflation erodes debt

LOW REAL RATES

Depreciation increases USD

debt in LCY terms

High volatility on P&L due

to FX movements Stable earnings

Fully exposed to

devaluations and shocks

Zero currency risk !

Better credit !

Higher leverage

Better rating

Cheaper funding

Risk Mitigation Benefits

Have you changed your mind ?

Theme 1 - expensive (2) 26

In my view local currency (LCY) financing is too expensive

(as opposed to HCY):

1 - True

2 - Not sure

3 - False, it depends on several factors and risk appetite

Theme 1 - expensive (2)

In my view local currency (LCY) financing is too expensive

(as opposed to HCY):

1 - True34%

2 – Not sure

14%

3 – False, it depends on several factors and risk

51%

12%

27%

62%

TCX Profitability - IRR over Libor

Source : TCX, 30 April 12

-1,73%

0,31%

1,15%

-3%

-2%

-1%

0%

1%

2%

3%

Diversification at work

Source : TCX, 31 December 2011

Theme 2 – complexity (2)26

LCY hedging is too complex. The legal and technical

complexities are too great for the beneift it provides.

1 - Yes

2 – No

0

1 - Yes

2 - No

37%

63%

8%

92%

LCY hedging is too complex. The legal and technical

complexities are too great for the beneift it provides.

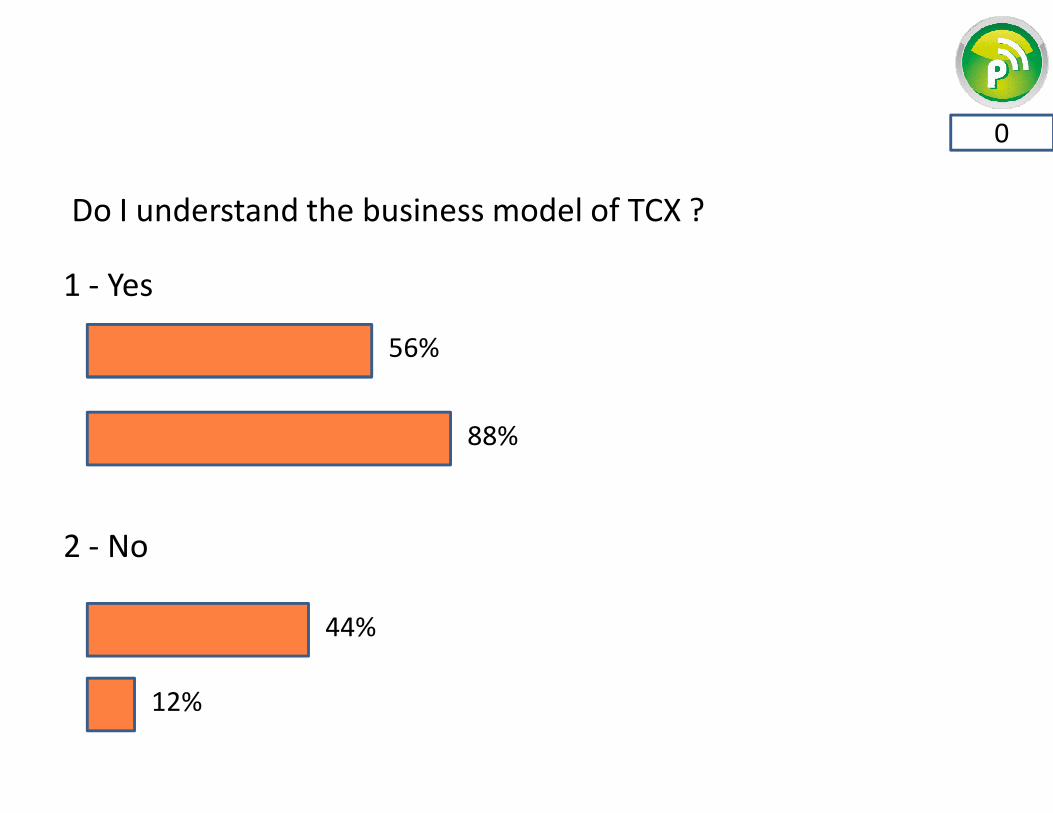

Theme 3 – The offer of TCX (2) 26

Do I understand the business model of TCX ?

1 - Yes

2 - No

0

1 - Yes

56%

2 - No

44%

88%

12%

Do I understand the business model of TCX ?

10 Questions Quiz

Question 1 :

The term “synthetic” loan refers to the fact that 28

1 - a derivative contract is traded next to the loan

2 – the loan is provided by an off-shore lender

3 – The fact that the currency hedge shields the currency rate and

the interest rate when you enter into the swap making your loss

completely remote

4 - the fact that settlement by the borrower of his obligations is in

hard currency, although the amount payable is a function of a local

currency principal and interest rate.

1 - The fact I trade a derivative contract on the top of a loan

2 - the loan is provided by an off-shore lender

3 - The currency hedge makes your loss remote therefore the term

synthetic

4 - the fact that settlement by the borrower of his obligations is in

hard currency, although the amount payable is a function of a

local currency principal and interest rate.

4%

11%

21%

64%

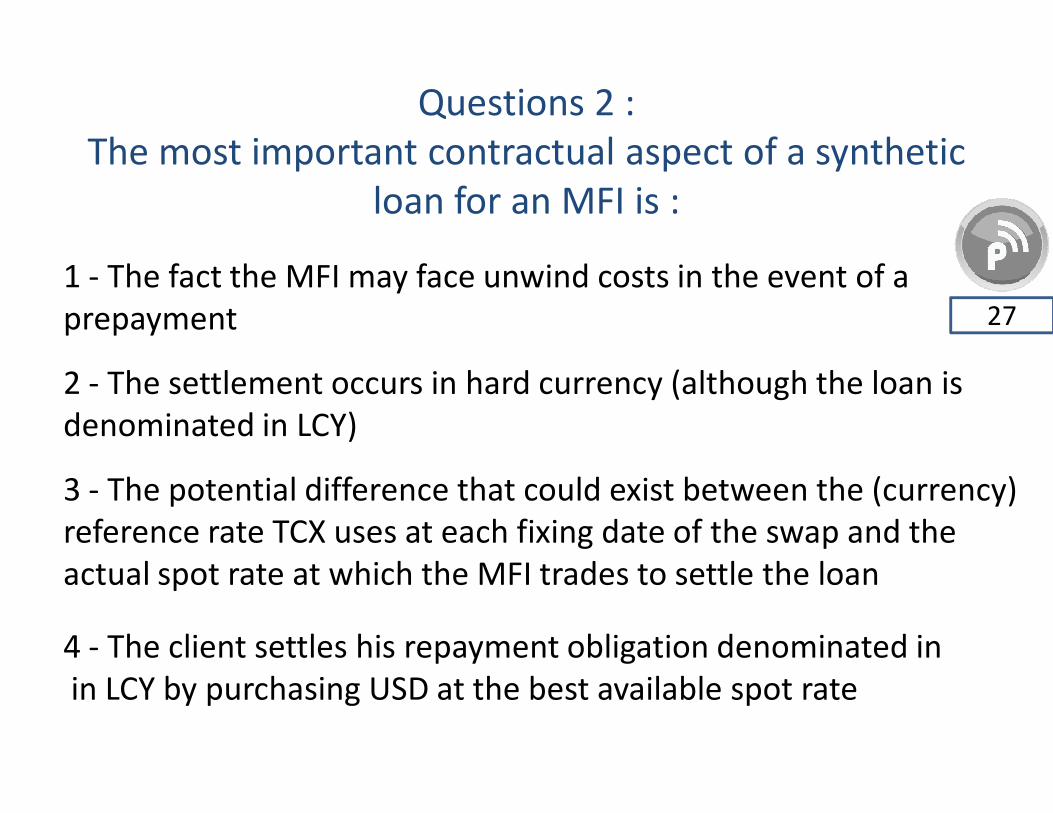

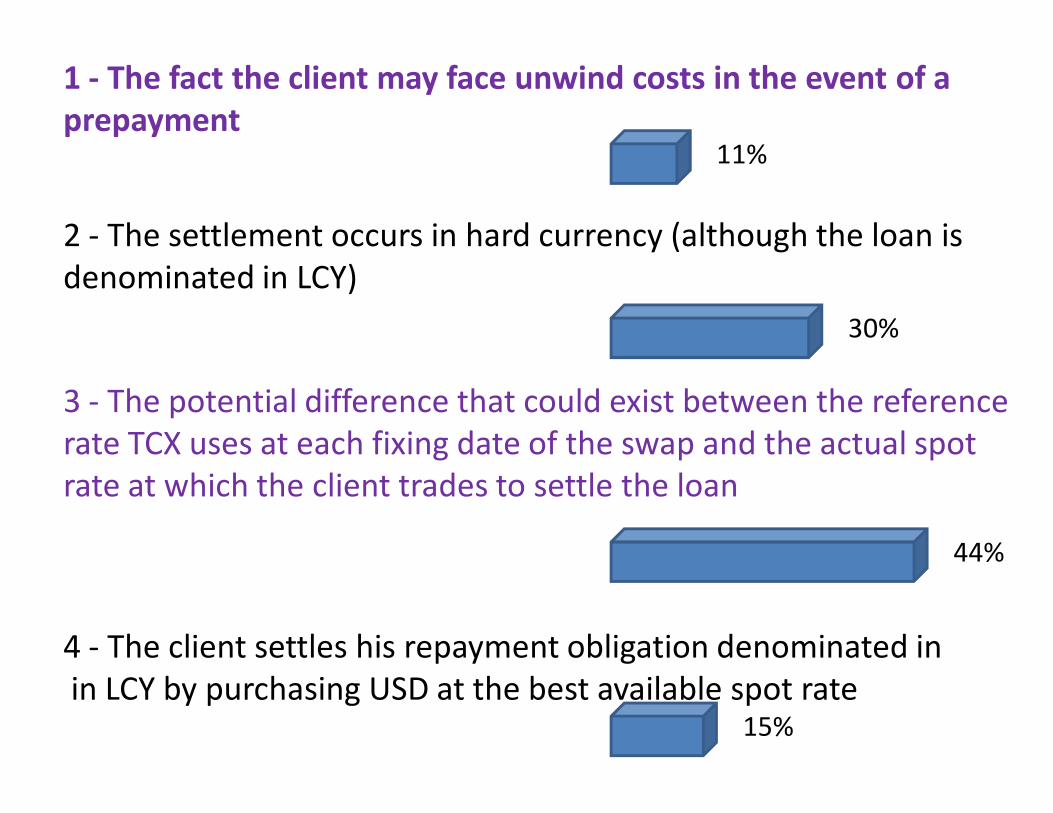

Questions 2 :

The most important contractual aspect of a synthetic

loan for an MFI is :

27

1 - The fact the MFI may face unwind costs in the event of a

prepayment

2 - The settlement occurs in hard currency (although the loan is

denominated in LCY)

3 - The potential difference that could exist between the (currency)

reference rate TCX uses at each fixing date of the swap and the

actual spot rate at which the MFI trades to settle the loan

4 - The client settles his repayment obligation denominated in

in LCY by purchasing USD at the best available spot rate

1 - The fact the client may face unwind costs in the event of a

prepayment

2 - The settlement occurs in hard currency (although the loan is

denominated in LCY)

3 - The potential difference that could exist between the reference

rate TCX uses at each fixing date of the swap and the actual spot

rate at which the client trades to settle the loan

4 - The client settles his repayment obligation denominated in

in LCY by purchasing USD at the best available spot rate

11%

30%

44%

15%

Question 3 :

TCX could directly hedge a bank for the following

reasons 27

1 – the bank has an existing USD loan that he would like to restate

in LCY but cannot amend the existing USD loan

2 - the interest rates in LCY have decreased rapidly and an bank

would like to benefit from these rates

3 - the bank feels the danger of being exposed to a currency risk

and wishes to hedge that risk

4 – the bank would like to lend more in LCY to his clients and for

that needs to swap his USD into LCY

5 - All above are good reasons to hedge with TCX

1 – a bank has an existing USD loan that he would like to restate in

LCY but cannot amend the existing USD loan

2 - the interest rates in LCY have decreased rapidly and an MFI

would like to benefit from these rates

3 - a bank feels the danger of being exposed to a currency risk and

wishes to hedge that risk

4 – a bank would like to lend more in LCY to his clients and for that

needs to swap his USD into LCY

5 - All above are good reasons to

hedge with TCX

4%

4%

15%

15%

63%

Question 4 :

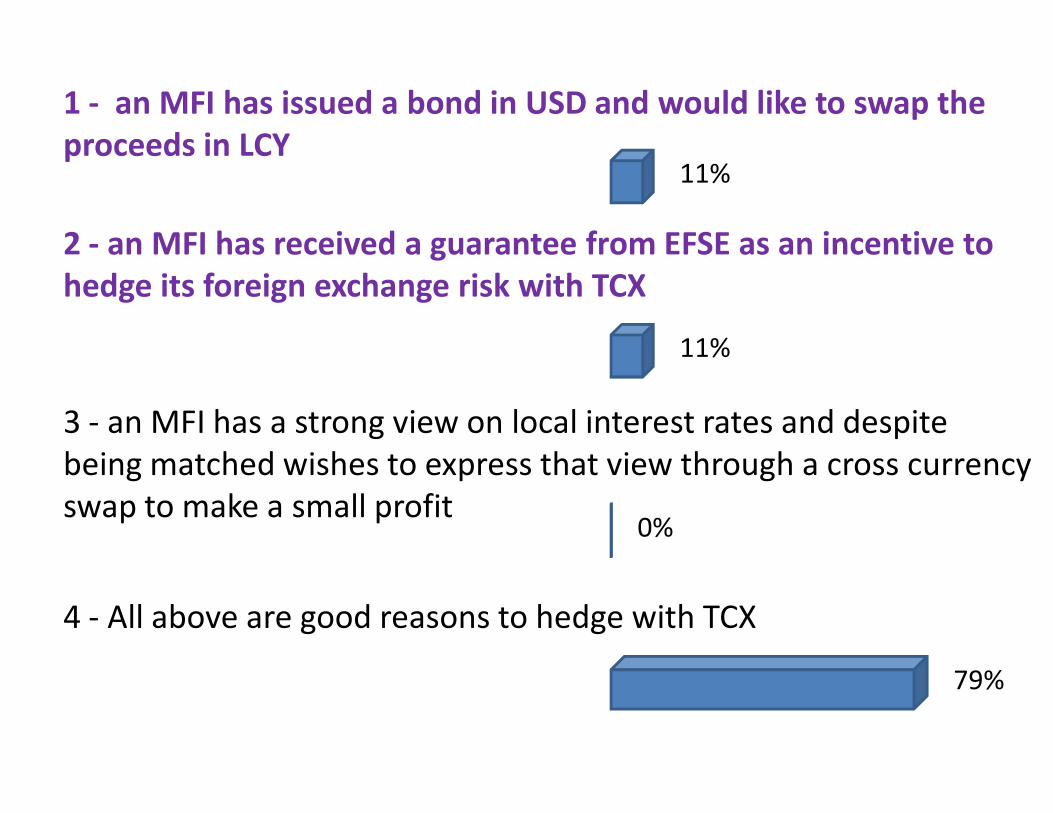

TCX can directly hedge an MFI for the following reasons 19

1 - an MFI has issued a bond in USD and would like to swap the

proceeds in LCY

2 - an MFI has received a guarantee (collateral waiver) from EFSE as

an incentive to hedge its foreign exchange risk with TCX

3 - an MFI has a strong view on local interest rates and despite

being matched wishes to express that view through a cross currency

swap to make a small profit

4 - All above are good reasons to hedge with TCX

1 - an MFI has issued a bond in USD and would like to swap the

proceeds in LCY

2 - an MFI has received a guarantee from EFSE as an incentive to

hedge its foreign exchange risk with TCX

3 - an MFI has a strong view on local interest rates and despite

being matched wishes to express that view through a cross currency

swap to make a small profit

4 - All above are good reasons to hedge with TCX

11%

11%

0%

79%

Question 5 :

The term non-deliverable swap (NDS) or non-

deliverable forward (NDF) refers to

25

1 - The fact neither me or TCX will ever get paid in HCY

2 - The total value of the swap is paid only over the life of the swap

3 - the fact that these are used to hedge currency risk but that all

cash flows between the two counterparties are made in HCY

4 - The fact TCX will net off the HCY and LCY leg of the instrument

on a LCY basis only

1 - The fact neither me or TCX will ever get paid in HCY

2 - The total value of the swap is paid only over the life of the swap

3 - the fact that these are used to hedge currency risk but that all

cash flows between the two counterparties are made in HCY

4 - The fact TCX will net off the HCY and LCY leg of the instrument

on a LCY basis only

0%

8%

60%

32%

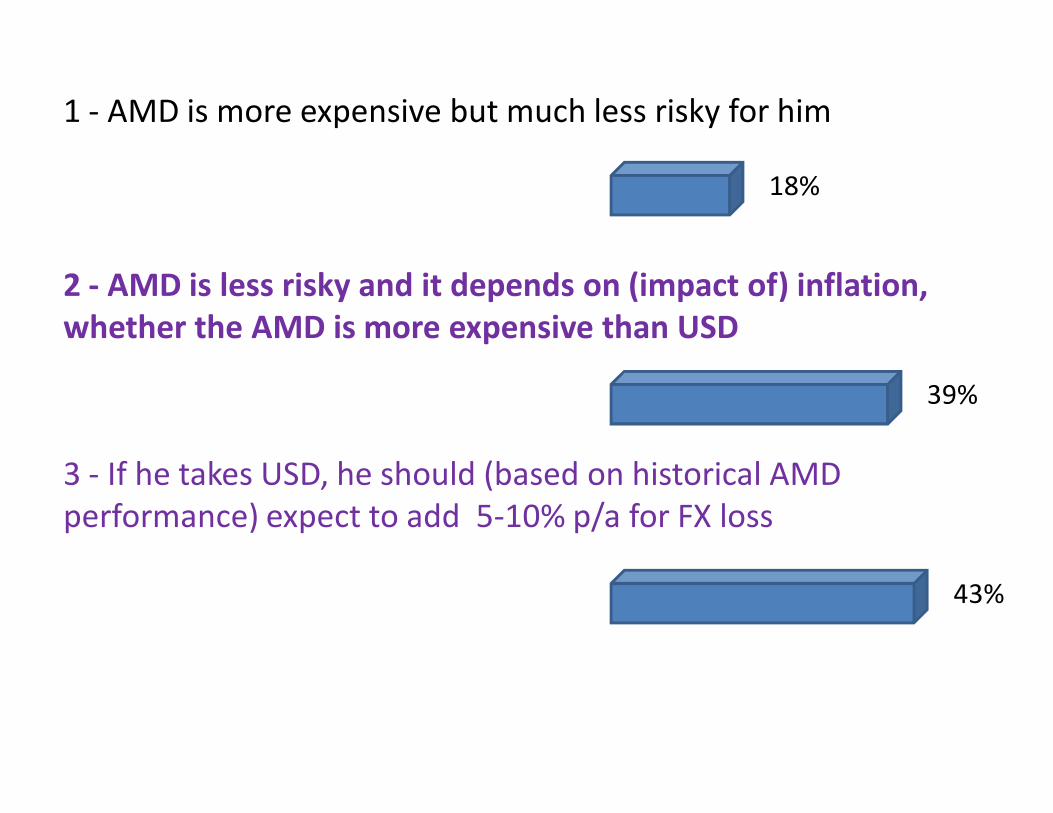

Question 6 :

You can receive 4-yr funding

at 8% in USD or at 21% in AMD.

You say that:

28

1 - AMD is more expensive but much less risky for me than USD

2 - AMD is less risky and it depends on (impact of) inflation,

whether the AMD is more expensive than USD

3 - If I take USD, I should (based on historical AMD performance)

expect to add 5-10% p/a for FX loss

1 - AMD is more expensive but much less risky for him

2 - AMD is less risky and it depends on (impact of) inflation,

whether the AMD is more expensive than USD

3 - If he takes USD, he should (based on historical AMD

performance) expect to add 5-10% p/a for FX loss

18%

39%

43%

Question 7 :

Your bank wants to better serve its customers

through local currency products in Hryvnya and

has requested funding from EFSE:

24

1 – You request a EUR loan because Hryvnya funding rates are too

high

2 - You do not bother about the Hryvnya alternative and take the

EUR but factor in the increased risk into the credit margin you

charge to your customers

3 – you take the cheapest EUR loan, request a guarantee from EFSE

to hedge it with TCX right after disbursement

4 - you take the cheapest EUR loan, knowing that when the

currency will start depreciating you will hedge the principal with

a forward (possibly with TCX)

1 – You request a EUR loan because Hryvnya funding rates are too

high

2 - You do not bother about the Hryvnya alternative and take the

EUR but factor in the increased risk into the credit margin you

charge to your customers

3 – you take the cheapest EUR loan, request a guarantee from EFSE

to hedge it with TCX right after disbursement

4 - you take the cheapest EUR loan, knowing that when the

currency will start depreciating you will hedge the principal with

a forward (possibly with TCX)

0%

4%

79%

17%

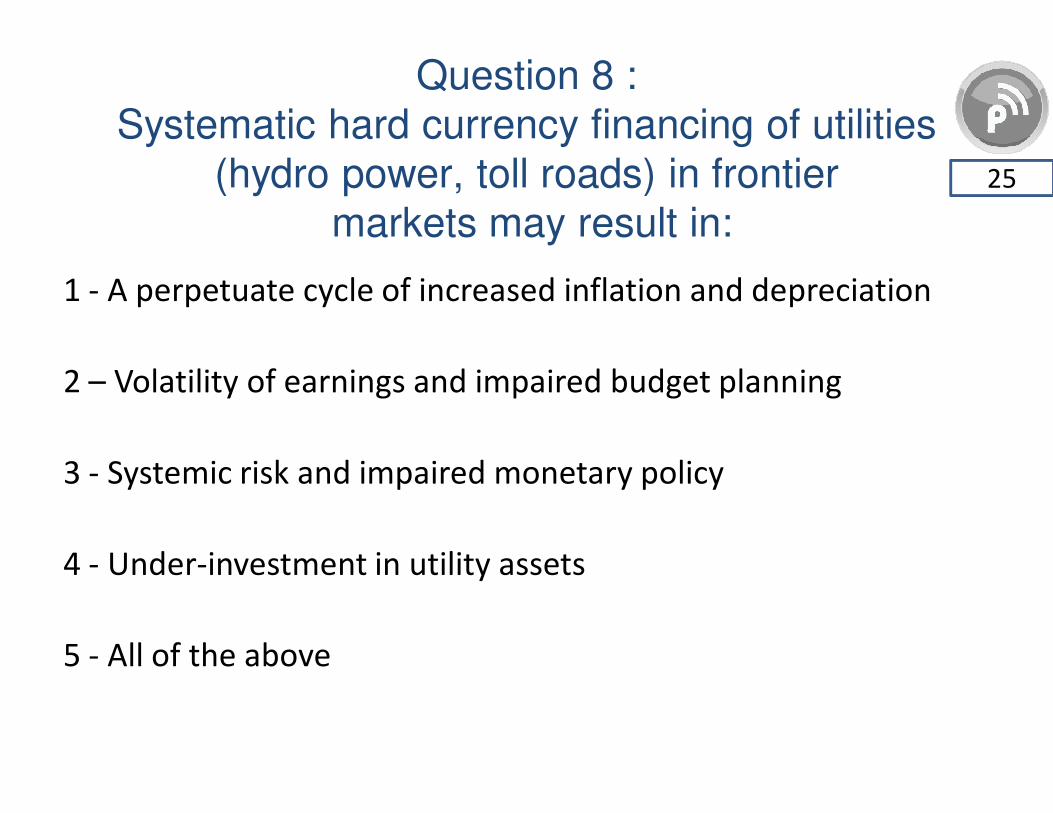

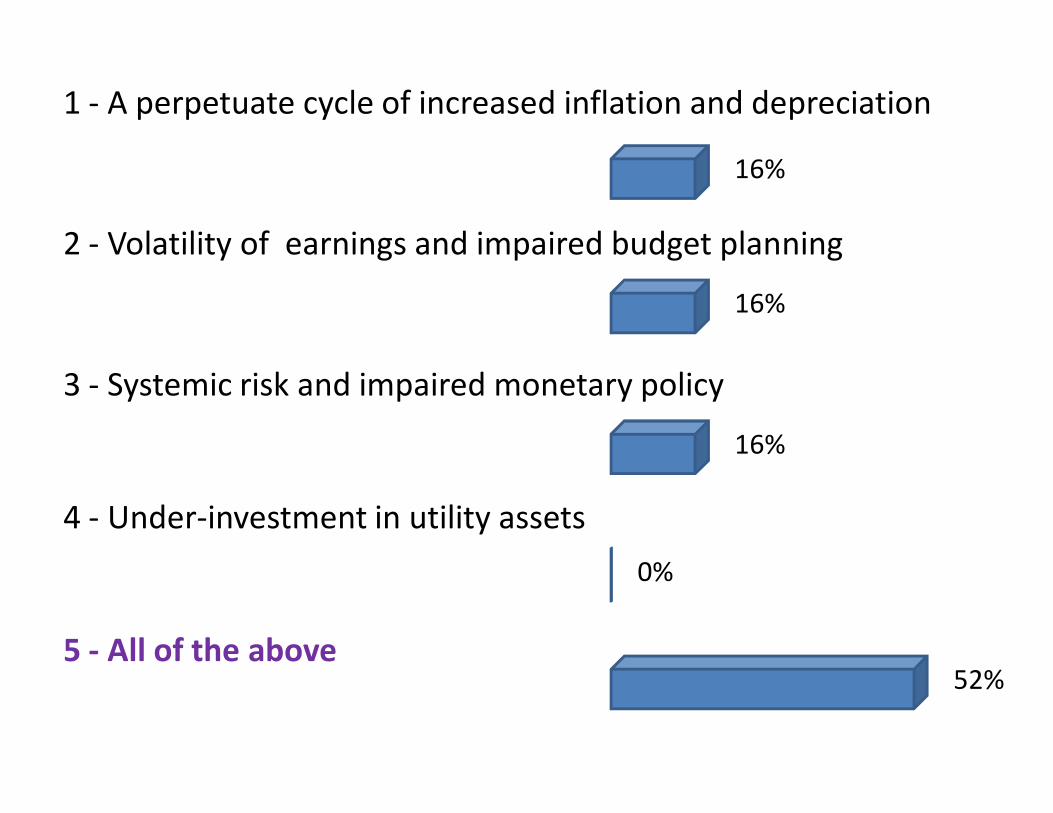

Question 8 :

Systematic hard currency financing of utilities

(hydro power, toll roads) in frontier

markets may result in:25

1 - A perpetuate cycle of increased inflation and depreciation

2 – Volatility of earnings and impaired budget planning

3 - Systemic risk and impaired monetary policy

4 - Under-investment in utility assets

5 - All of the above

1 - A perpetuate cycle of increased inflation and depreciation

2 - Volatility of earnings and impaired budget planning

3 - Systemic risk and impaired monetary policy

4 - Under-investment in utility assets

5 - All of the above

16%

16%

16%

0%

52%

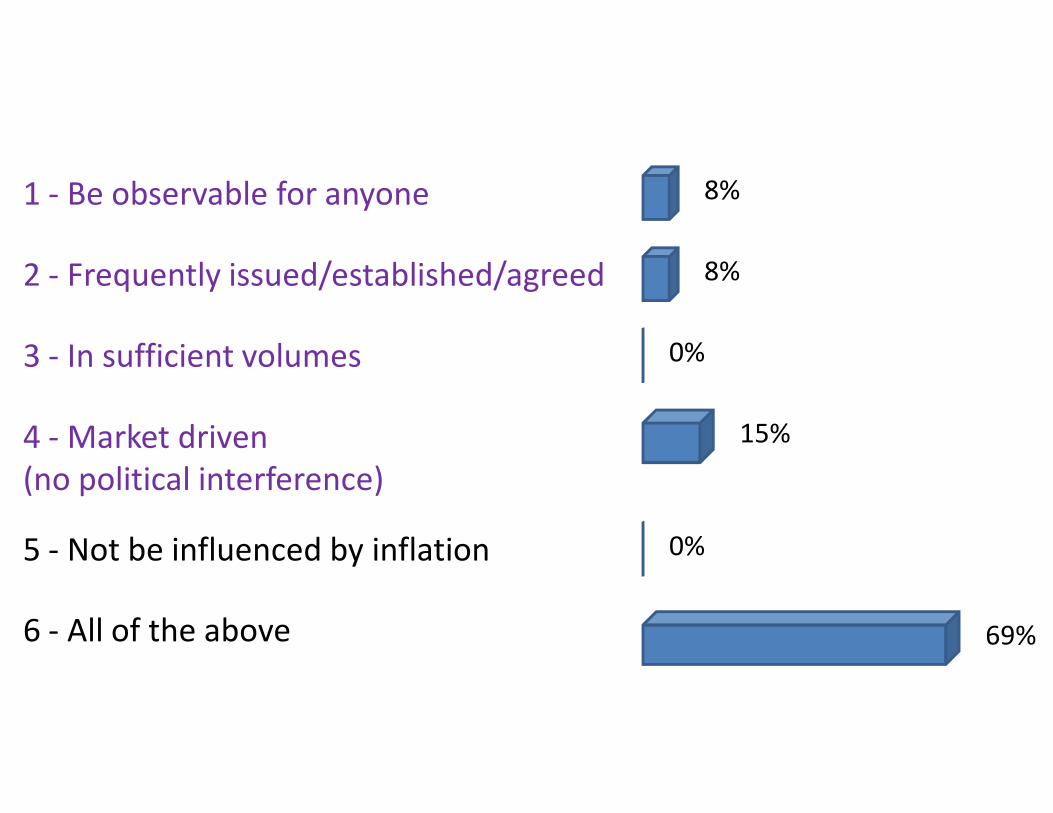

Question 9 :

To price a floating rate local currency loan, lenders

and EFSE select a local benchmark.

A benchmark must:26

1 - Be observable for anyone

2 - Frequently issued/established/agreed

3 - In sufficient volumes

4 - Market driven (no political interference)

5 - Not be influenced by inflation

6 - All of the above

1 - Be observable for anyone

2 - Frequently issued/established/agreed

3 - In sufficient volumes

4 - Market driven

(no political interference)

5 - Not be influenced by inflation

6 - All of the above

8%

8%

0%

15%

0%

69%

Question 10 :

Local currency financing:22

1 - Is more expensive than USD/EURO financing, but in return, the

borrower is less exposed to risk

2 - Should with normal functioning markets be fully price

competitive with hard currency

3 - Is, aggregating all costs and benefits, cheaper than USD funding

4 - It depends on the borrower, tenor of the loan, the currency

1 - Is more expensive than USD/EURO financing, but in return, the

borrower is less exposed to risk

2 - Should with normal functioning markets be fully price

competitive with hard currency

3 - Is, aggregating all costs and benefits, cheaper than USD funding

4 - It depends on the borrower, tenor of the loan, the currency

18%

36%

0%

45%

And the winner is

28 7

30 7

40 6

42 6

1 5

www.tcxfund.com

+31 20 531 4851

Local Currency Matters

Thank you for your attention!

Top Related