Languages

Pages

Legal

Investor presentations:South Africa October 2008

Important information

This presentation has been prepared by British American Tobacco p.l.c. ("British American Tobacco") for information purposes only and does not constitute, or form part of any offer or invitation to acquire, or any solicitation of any offer to acquire any securities of British American Tobacco.The information on which this presentation is based has been obtained from sources which we believe to be reliable as at the date hereof, but we have not independently verified such information and do not guarantee that it is accurate or complete and all information and opinions are subject to update, correction, revision or amendment without notice. No representation or warranty, express or implied, is therefore made by or on behalf of British American Tobacco, its directors or employees or any other person as to, and no reliance for any purposes whatsoever should be placed on, the accuracy, completeness or fairness of the information or opinions contained in this presentation and no responsibility or liability is accepted for any such information or opinions.This presentation includes certain forward-looking statements with respect to British American Tobacco's financial condition, results of operations and business and certain plans and objectives of the British American Tobacco's board of directors with respect thereto. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Forward-looking statements are not guarantees of future performance and British American Tobacco's actual results of operations, financial condition, liquidity, prospects, growth and strategies and the development of the industry in which the British American Tobacco operates may differ materially from those expressed or implied by the forward-looking statements included in this presentation. Events that may cause actual results to differ from such forward-looking statements include, but are not limited to fluctuations in the capital markets; fluctuations in interest and exchange rates; increased regulation or regulatory scrutiny; the occurrence of unforeseen disasters or catastrophes; political or economic instability in their principal markets; adverse outcomes in litigation; general local and global economic, political, business and market conditions. Except as required by its legal or regulatory obligations, British American Tobacco does not undertake any obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future events or otherwise.Recipients of this presentation who intend to acquire any interests in securities which British American Tobacco may issue in the future are reminded that any such acquisition should only be made on the basis of the offering document prepared in connection therewith, which may be different from the information and opinions contained in this presentation.

Agenda

Jan du Plessis - Overview and review of the Group since the merger with

Rothmans

Paul Adams- Industry overview, the Group and strategy

John Taylor- BAT South Africa, innovations and Russia

Ben Stevens- The productivity strategy, financials and 2008 performance

Questions and answers

World’s most international tobacco group

Over 300 brandsFocus on Global Drive Brands + Vogue & Viceroy180 marketsLeadership in 50 marketsAlmost 54,000 employees£26 bn gross turnover£10 bn net turnover£3 bn profit from operations£17 bn tax contributions

Market capitalisation – currently number 6 in the UK

2007 statistics

Sales volume: 684 billion cigarettes 47 factories in 40 countries5 Regional Product CentresOver 460,000 tonnes of leaf bought280,000 farmers providing leaf

Our world

•Organised into 5 regions – Europe to split in 2009

•Two key associates: Reynolds American (US) and ITC (India)

42 bn

151 bn

101 bn

245 bn

145 bn

Associates

Reynolds American Inc.- 42% shareholding - Number 2 cigarette manufacturer in US- Brands include, Camel, Kool and Pall Mall- Significant non-combustible business

ITC Ltd.- 32% shareholding- Largest cigarette manufacturer in India- Includes paper and packaging and hotels businesses

Milestones since demerger in 1998

1998: British American Tobacco listed as a standalone tobacco company

1999: Rothmans merger completed2002: Growth, Productivity and Responsibility strategy

and 5 year cost savings programme announced2003: Acquisition of ETI in Italy2004: B&W and RJR form Reynolds American2008: Turkey and Scandinavia deals completed

Earnings per share

52.3 56.9 61.8 66.5 69.276.6

89.398.1

108.5

53.562.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2007 2008

penc

e

9.6% CAGR

The target of high single figure earnings growth has been delivered

YTD 6 months

Source: Company’s financial results

+16%

Dividends per share

26.2 29.0 32.0 35.2 38.8 41.947.0

55.966.7

18.6 22.1

1999 2000 2001 2002 2003 2004 2005 2006 2007 2007 2008

penc

e

12.4% CAGR

Targeting a 65% payout ratio in 2008

Interimdividend

+19%

Source: Company’s financial results

BAT share price since Jan 2000

Source: Reuters

Daily Relative performance to FTSE100 03/01/2000 - 07/10/2008 (GMT)ValueGBp

.1231

1.5

2

2.5

3

3.5

4

4.5

5

5.5

6

6.5

7

PriceGBp

.12300400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42000 2001 2002 2003 2004 2005 2006 2007 2008

BAT share price Relative performance to FTSE 100

Out-performance

Since Jan 2000 28.3%Since Jan 2003 27.7%Since Jan 2005 28.0%Since Jan 2007 24.1%

Total shareholder return per annum

Source: Bloomberg (Based BAT share price at close 3 October 2008)

FMCG Comparator Group

AltadisAltria (Phillip Morris)Anheuser-BuschCadbury SchweppesCampbell SoupCarlsberg Coca ColaColgate-PalmoliveDanoneDiageoGallaher HeinekenHeinzHershey FoodsImperial Tobacco

InBevJohnson & JohnsonKelloggKimberly-ClarkLVMH Möet HennessyNestléPepsicoProcter & GambleReckitt BenckiserReynolds American SAB MillerSara LeeScottish & NewcastleUnilever

Source: Company Annual Report & Accounts 2007

Total Shareholder Return v. FMCG group

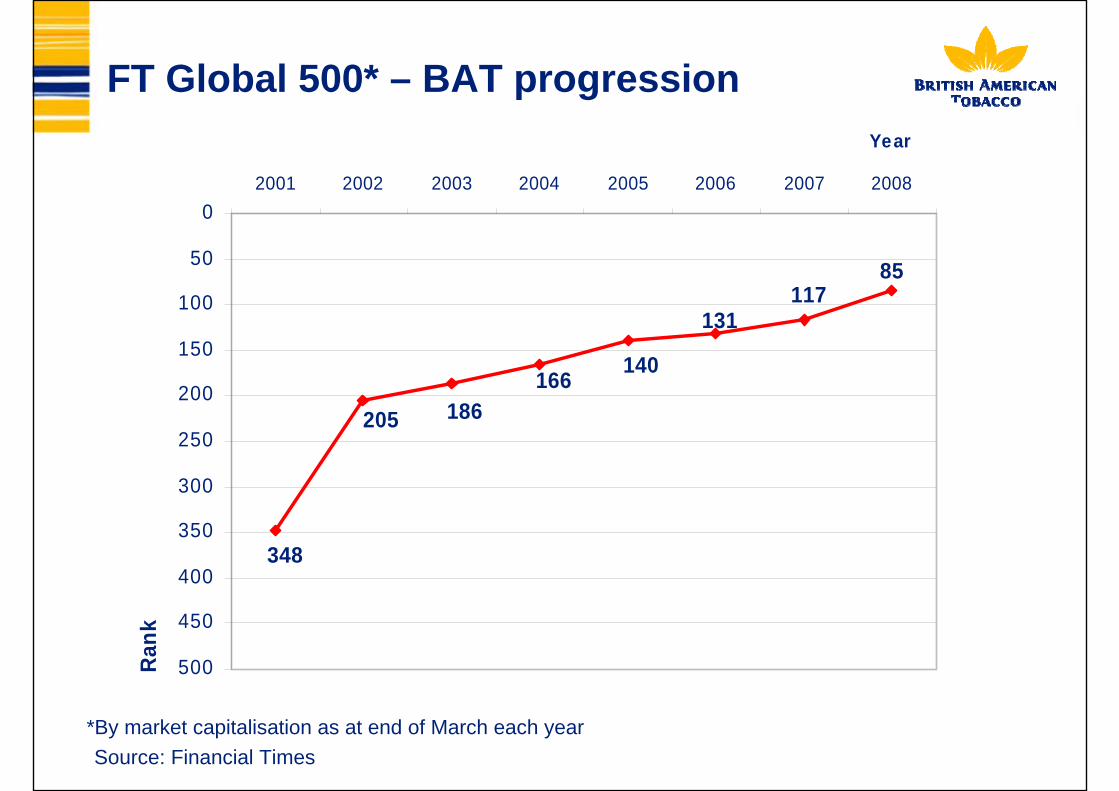

FT Global 500* – BAT progression

*By market capitalisation as at end of March each year

85117

131

140166186205

348

0

50

100

150

200

250

300

350

400

450

500

2001 2002 2003 2004 2005 2006 2007 2008

YearRa

nk

Source: Financial Times

Industry volume (excluding China) continues slow, steady decline

Geographic mix is deteriorating

Relatively few players

There are still opportunities for growth in key segments

Legitimate manufacturers squeezed by governments and illicit trade

The level of regulation will increase

Industry dynamics

Even with these dynamics, the industry profit pool is forecast to grow

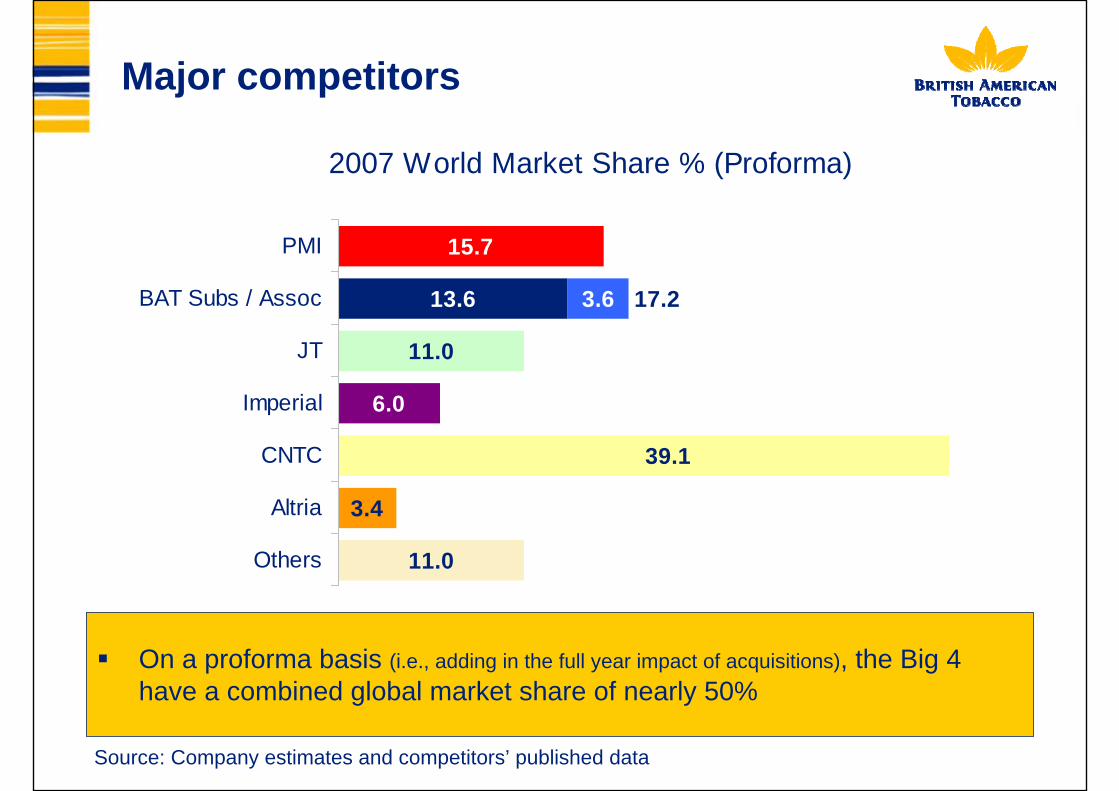

Major competitors

On a proforma basis (i.e., adding in the full year impact of acquisitions), the Big 4 have a combined global market share of nearly 50%

11.0

3.4

6.0

11.0

13.6

15.7

39.1

3.6 17.2

Others

Altria

CNTC

Imperial

JT

BAT Subs / Assoc

PMI

2007 World Market Share % (Proforma)

Source: Company estimates and competitors’ published data

GROWTH PRODUCTIVITY RESPONSIBILITY

WINNING ORGANISATION

VISION

STRATEGY

Great Place to Work Outstanding People

Organic Growth

Mergers & Acquisitions Standards of

Business Conduct

Business Principles

Smart Cost Management

Marketing Efficiency

Capital Effectiveness Sensible RegulationHarm Reduction

ACHIEVELEADERSHIP OF

THE GLOBALTOBACCO INDUSTRY

WINNING ORGANISATION

Great Place to Work- Leadership- Culture

Outstanding People- Talent- Learning

RESPONSIBILITYGROWTH PRODUCTIVITY

Organic Growth

Mergers & Acquisitions

Marketing Efficiency

Standards of Business Conduct

Business Principles

Smart Cost Management

Capital Effectiveness

Sensible Regulation

Harm Reduction

- Supply Chain

- Overheads & Indirects- Innovation

- Key Segments & Brands

- Priority Markets

ACHIEVELEADERSHIP OF

THE GLOBALTOBACCO INDUSTRY

VISION

STRATEGY

Strategy for shareholder value

Global Drive Brands

78 85 93 100113 114 125

146 161

7287

1999

2000

2001

2002

2003

2004

2005

2006

2007

H1 200

7 H1 2

008

Volu

me

(Bill

ions

)

Global drive brands sales volumes have grown consistently

9.5% CAGR

Source: Company’s financial results

+20%

Brand momentum The top-13 international brands

0

50

100

150

200

250

300

350-4.8

-2.4

+4.5 +3.1+8.4 +6.7 +5.0 +2.9 +2.1 +5.0

2007 global volumes and growth v 2006

-7.2+8.4

+3.0

Volume movement in billionsPMI -11JT +9BAT +22

International volumes, excluding the USA

Source: Company estimates and data published by competitors

Global Drive Brands: volume growth index

Base 100: 1997Advertising Principles International Marketing Standards

80

100

120

140

160

180

200

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

British American Tobacco

Japan Tobacco

Philip Morris

Source: Company estimates and competitors’ published data

Key consumer segments (top 22 markets)Designated Global Drive and/ or

"Flagship" Brands

35.042.139.6

2007 2012 2017

International Brands*54.1 56.3

48.7

2007 2012 2017

% S

hare

of T

22 m

arke

ts

Premium

32.4 34.233.3

2007 2012 2017

% S

hare

of T

22m

arke

ts

Lights

51.3 52.153.0

2007 2012 2017%

Sha

re o

f T22

mar

kets

GDB and/or “Flagship” brands, International brands and the Premium segment are all forecast to grow. The Lights segment is expected to fall as a proportion of the total market.

* Includes Designated GDB/Flagship Brands %

Sha

re o

f T22

mar

kets

Source: Company’s internal estimates and forecasts

Priority markets

Eastern EuropeFar EastNorth AfricaMiddle East

Growth summary

We have delivered growth- Improvements in key Industry segments

- Spectacular GDB volume growth

- Value added deals

Going forward -- we are well positioned for further growth- Real momentum in the business

Regulation

Engage with stakeholders to:

- compete in the legal market;

- differentiate and innovate with our product category (including harm reduced products);

- maintain channels of communication;

- ensure there are opportunities for consumers to smoke;

- enjoy free trade; and

- combat illicit trade.

Winning organisation strategy

Ensure we have the right people and the right working environment to deliver our Vision.

Great Place to Work

Outstanding People

A loose federation An integrated global enterprise

From To

High single figure EPS growth model*

Volume growth of 1 to 1½%Drive brands to grow at high single figures

Net turnover growth of 3 to 3½%Implies volume growth and pricing

Profit from ops growth of 6%Implies significant cost savings

EPS growth of around 8%Implies balance sheet & below the line efficiencies

* Based on internal estimates over the medium to long term

The business model

Earnings growth

Cost savings

Bad stuff Invest in long term

Earnings per share growth

11%9%

4%

10%

17%

10% 11%

16%

8%

2000 2001 2002 2003 2004 2005 2006 2007 2008

% G

row

th

YTD 6months

Source: Company’s financial results

In previous economic downturns…

Tobacco is not recession proof…… but recession resistantOur geographic diversity mitigates riskConsumers are loyal to their brandsSwitching where they buy not what they buyHigh unemployment may lead to changing behaviourBalanced portfolio covering consumer price points

An enterprise which has:

A leading portfolio of sustainable brands -- having a strong brand in each segment which the consumer perceives to be of greater value thancompetition

A highly effective, flexible and efficient operation that leverages the synergies of being part of a global group

An agile, learning, innovative organisation that has outstanding leaders and that re-invents and improves itself

Recognition that it acts responsibly and has a sustainable business

Delivered on shareholders’ expectations of high single-digit earnings growth over the medium to long term

Achieved leadership of the global tobacco industry and created long term shareholder value

Common vision of success

Agenda

11

22

33

SA Market Context

BATSA – Progress to date

Learning from other markets

PopulationTotal: 49 mn18-65: 27 mn Growth Rate: 0.6%

IndustryAdult Smokers 18-65 years

All Products: 27.7% (7.5 mn)Cigarettes: 23.6% (6.4 mn)

4 International Players (c. 98% of vol)Retail Universe: c. 140,000 outletsExcise Rate: 52%R 9 bn+ in taxes to governmentIndustry creates c. 53,000 jobs

EconomyMacro Economic Stability Servicing EconomyShielded by ResourcesSlowed GDP GrowthInflation Peaking

South Africa at a glance

Source: BER; Estimated Sales; Nielsen

Emerging consumer class...

0

1

2

3

4

5

6

7

8

9

'96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07

Final household consumption expReal disposable income

Growing per capita income

0

1000

2000

3000

4000

5000

6000

7000

'96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07

GDP per Capita (US$)

Disposable income and expenditure growth

Growing middle class

Increased demand for branded consumer products

Source: Business Monitor International; Bureau of Economic Research

Local portfolio positioning

VFM

Premium

Premium + 1.5%

16%

2.7%

81%

64%

97%

Low 6.3%

Popular 73%97%

40%

Note: SA Local Price Card; Source: Estimated Sales, Nielsen

1.2% 1.4% 1.8%

4.1%

1.8% 1.8% 1.8% 2.0%

4.7%3.9% 3.5%

2005 2006 2007 2008YTD

07Q1 07Q2 07Q3 07Q4 08Q1 08Q2 08Q3

4.7% 5.0% 5.5% 5.7% 5.0% 5.3% 5.7% 6.1% 5.9% 5.6% 5.3%

2005 2006 2007 2008YTD

07Q1 07Q2 07Q3 07Q4 08Q1 08Q2 08Q3

Competitors struggling in changing market dynamics

Source: Estimated Sales; Nielsen

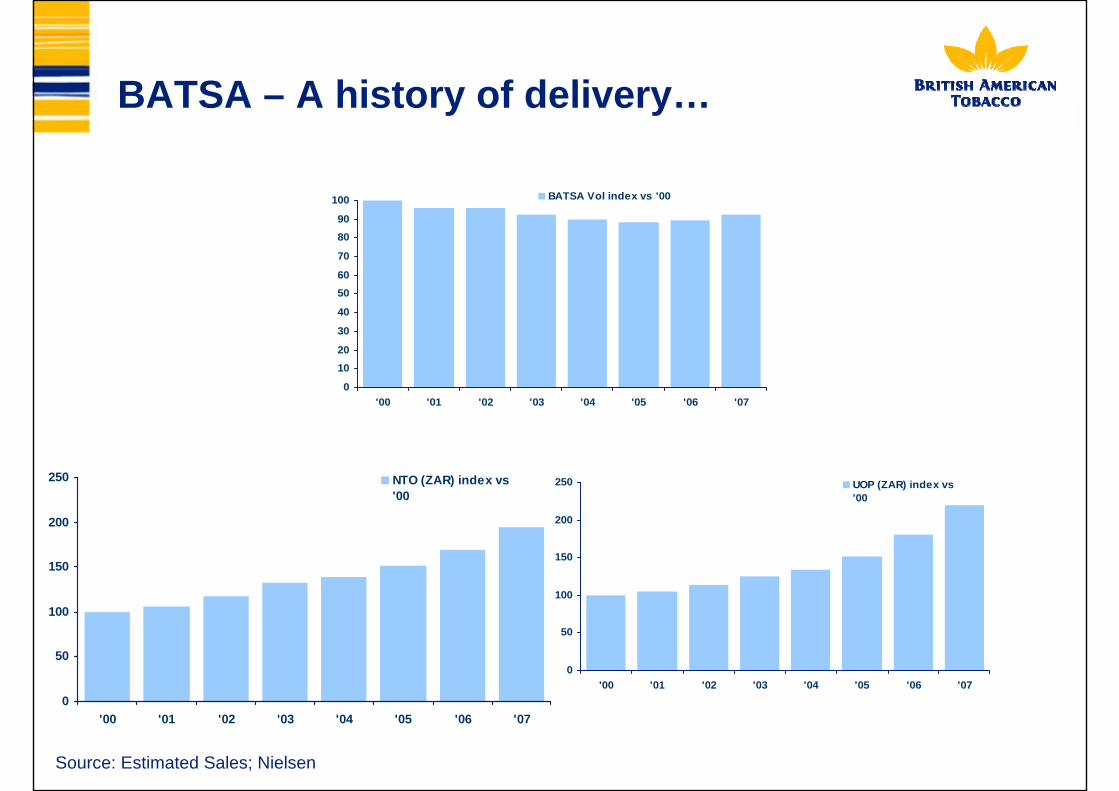

Agenda

11

22

33

SA Environment

BATSA – Progress to date

Learning from other markets

0

50

100

150

200

250

'00 '01 '02 '03 '04 '05 '06 '07

NTO (ZAR) index vs'00

BATSA – A history of delivery…

0

1020

30

40

5060

70

8090

100

'00 '01 '02 '03 '04 '05 '06 '07

BATSA Vol index vs '00

0

50

100

150

200

250

'00 '01 '02 '03 '04 '05 '06 '07

UOP (ZAR) index vs'00

Source: Estimated Sales; Nielsen

Embracing innovation

Our challenge is to deliver sustainable NTO growth…

Innovation allows us a platform to do so.

Innovation:- Creates excitement- Provides a competitive advantage- Delivers value to the consumer- Justifies higher pricing

BATSA … driving innovation harder

RetailProduction Sales & Distribution

Wholesalers

Cash & Carry

RetailProductionProduction Sales & DistributionSales & Distribution

Wholesalers

Cash & Carry

RetailProduction Sales & Distribution

TM Rep

RetailProductionProduction Sales & DistributionSales & Distribution

TM Rep

No commercial relationship with retailReduced flexibility and agility

Source: Team Shosholoza

We challenge even our own success models

Indirect Sales Model Direct Sales Model

Speed to MarketTargeted distributionOwning the commercial relationship with retail

Focus on International and Premiumbrands, Lights and ASU30 (adult smokers under the age of 30)

Global Drive Brands -Dunhill-Kent

International Brands-Peter Stuyvesant-Rothmans

Inspiring consumers

Changing with the timesGrowing in the lights segment

Peter Stuyvesant undoubtedly no 1

39.0%40.3%

41.1%41.9%

43.4%44.5% 43.8% 43.8%

44.9%

2000 2001 2002 2003 2004 2005 2006 2007 2008

Agenda

11

22

33

SA Environment

BATSA – Progress to date

Learning from other markets

A Strategy for Value Creation…

2 key value creation opportunities

Consumer saliency to Premium, Lights & International

The ability to drive Innovation hard…..both to build market share and as a value-generator

Attractive segment dynamics

7%

42%

13%

24%

14%

5%14%

41%43%

12%

15%26%

19%

16%9%

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007 2008 2009

NF Low VFM Medium Premium

0%

10%

20%

30%

40%

50%

60%

70%

80%

2004 2005 2006 2007 2004 2005 2006 2007 2004 2005 2006 2007

Share of Market Share Of ASU30

Premium

LightsInternational

Brands

Price Segment Dynamics

Emerging Segments

Nielsen Retail Audit

2004 2005 2006 2007 2008

2.0%

98.1%

27.5%

72.5%

35.9%

64.1%

45.3%

54.7%

53.0%

47.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Innovations Others

New product development / Innovation as a value New product development / Innovation as a value driverdriver

Derived Value Share2008

Vogue Collections: Ephemere (Feb)Yava Export (Jan)

2007

Dunhill Top Leaf (Jan)Vogue Collections: B&W (Feb)Kent Nanotek (Apr)Pall Mall SS Aromatic & TT (Jun & Oct)Dunhill Tribute (July)Dunhill FC (Nov)

2006

Vogue Arome 2&3 (Mar & Jul)Viceroy Filters (Mar)Pall Mall SS Menthol (Apr)

2005

Vogue Arome 1 (Feb)Kent Mintek (Apr)Pall Mall SS Lights, Ultra (Aug) Viceroy Special (Jun)

2004

Kent 3-tek launch Dunhill KS launch (Oct)

850

690

550

440370330

310280230

1201000

100

200

300

400

500

600

700

800

900

'98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 LE

NTO index vs '98

-10%

0%

13%17% 17%

26%

'98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 LE

UOP

OpMargin (Market View)

36%34%31%29%26%

41%41%44%48%

54%

20%

25%

30%

35%

40%

45%

50%

55%

60%

JAN 2004 MAR 2005 MAR 2006 APR 2007

PMI Prem ShareBAT Prem Share

26.8%

23%

27.2%

26.6%

28%

26.8%

0%

5%

10%

15%

20%

25%

30%

35%

JAN '04 AUG '04 MAR '05 OCT '05 MAY '06 NOV '06 MAY '07 NOV '07

BAT MS PMI MS GLH MS JTI MS

T30 SOM

Creating accelerated value and enhancing sustainability…

JUN ’08JAN’04

**

5%0% +0.4%

** Nielsen data National Russia (Jan 2004 – Jun’ 2008)QPR 2 2008Please note : All figures are for consolidated (commercial and ops) excluding Belarus and internal Export business to ensure like for like comparison at budget rate ([email protected], 2008- @51)

BAT VOLUME

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08

4+2 Other

* Volumes with Captain Black included

JUN’08

Summary

Our business in South Africa is GREAT!!

Growing consumer class with $$ looking for more

The innovations journey is the road to take

We are on the way…..taking learnings from where we have a proven track record.

Productivity initiatives 2003 – 2007

Cumulative savings, £m

2003 2004 2005 2006 2007

Overheads & indirects 64 153 256 355 455 Supply chain 27 120 226 374 551Total 91 273 482 729 1,006

Factory Footprint 2003 2004 2005 2006 2007

Cigarette factories 72 67 64 52 47

Countries 61 58 55 45 40

Annualised savings of £1bn by 2007Source: Company data

Productivity savings goal: 2008 – 2012

Productivity savings a significant driver of profit growthSome drop through to the bottom lineBalance reinvested in the businessTarget of a further £800m by 2012

- Savings from supply chain, overheads & indirects- Supply chain efficiencies

- Back office integration

- Management structures

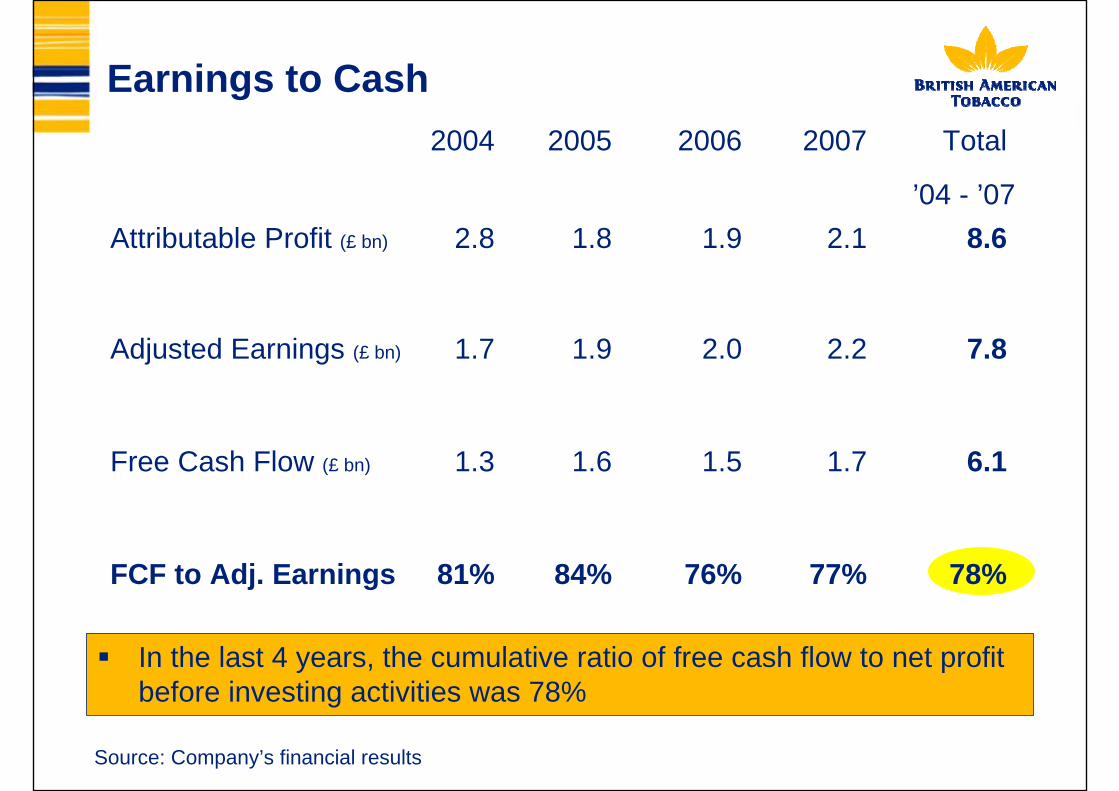

Earnings to Cash

In the last 4 years, the cumulative ratio of free cash flow to net profit before investing activities was 78%

2004 2005 2006 2007 Total

’04 - ’07Attributable Profit (£ bn) 2.8 1.8 1.9 2.1 8.6

Adjusted Earnings (£ bn) 1.7 1.9 2.0 2.2 7.8

Free Cash Flow (£ bn) 1.3 1.6 1.5 1.7 6.1

FCF to Adj. Earnings 81% 84% 76% 77% 78%

Source: Company’s financial results

Use of funds

In the last five years, £7.7bn has been returned to shareholders through dividends and share buy backs – and we are now returning all the free cash flow.

£ bn 2003 2004 2005 2006 2007 Total ’02 - ’07

Free Cash Flow (1.6) 1.3) 1.6) 1.5) 1.7) 7.7)Dividends Paid (0.8) (0.8) (0.9) (1.0) (1.2) (4.7)Share buy-back (0.7) (0.5) (0.5) (0.5) (0.8) (3.0)Sub Total 0.1) (0.1) 0.2) 0.0) (0.3) 0.0)Other net flows (1.9) 0.2) (0.1) 0.0) 0.2) (1.6)Net cash flows (1.8) 0.1) 0.1) 0.0) (0.1) (1.7)

Financial policies

Board commitment to investment grade ratingsLiquidity: to maintain minimum of £1bn in cash and committed facilitiesMaturity profile has an average maturity of 5 yearsGross interest cover targeted between 5 and 9 times Dividend policy is to distribute 65% of long term sustainable earnings from 2008Share repurchase programme target was £750m in 2007 but currently scaled back to £400m

£1.75bn committed Group revolving credit facility

Strong cash flows and cash balances

Smooth maturity profile

Almost all debt is unsecured with a limited use of leasing

Credit ratings

Financing plan / liquidity

Moody’s S&P FitchLong term rating Baa1 BBB+ BBB+Short term rating P-2 A-2 F2Outlook Stable Stable Stable

Volume and revenue: first half 2008

-6%

4%

14%

Volumes 2% 3% -4% 5% 1% 1%

Revenue (const) 8% 6% -1% 12% 3% 6%

Revenue (curr) 21% 10% 12% 12% 17% 15%

Europe AsiaPac LatAm AME AmPac Total

Source: Company data

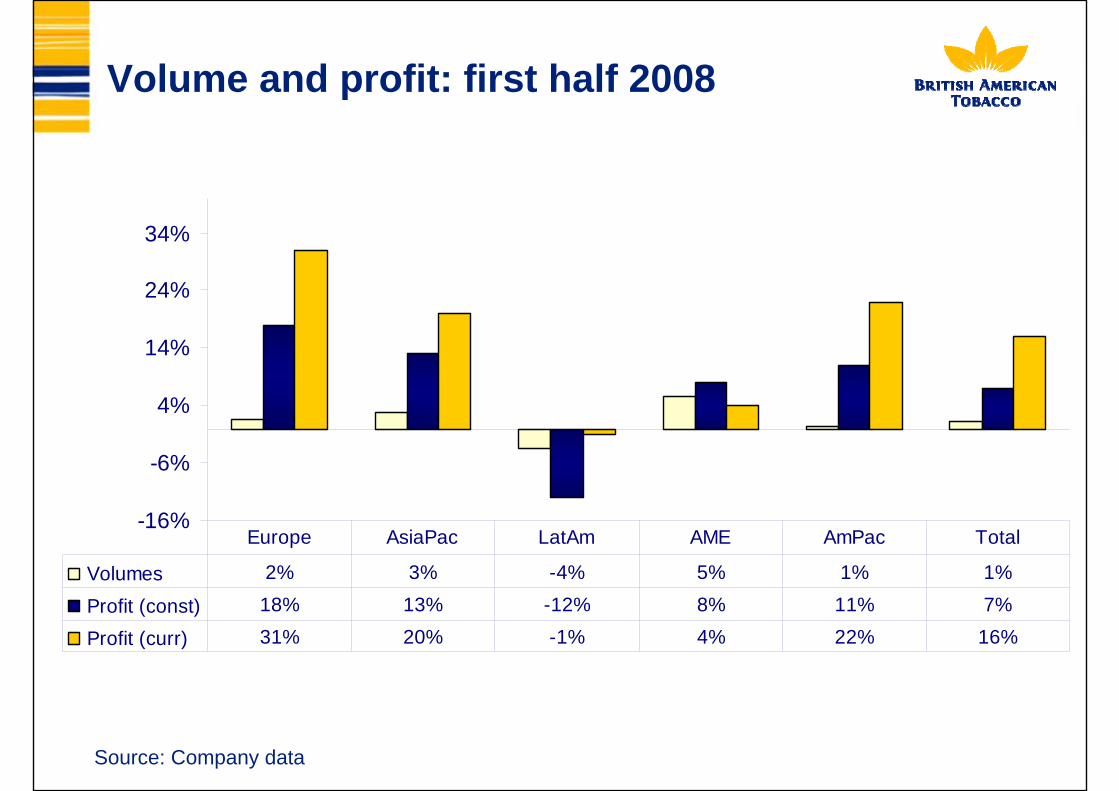

Volume and profit: first half 2008

-16%

-6%

4%

14%

24%

34%

Volumes 2% 3% -4% 5% 1% 1%

Profit (const) 18% 13% -12% 8% 11% 7%

Profit (curr) 31% 20% -1% 4% 22% 16%

Europe AsiaPac LatAm AME AmPac Total

Source: Company data

Margins: profit per 1000 cigarettes

H1 2008H1 2007

£3.53

£4.51

£5.21 £5.33

£9.56

£4.61£4.55

£5.26 £5.34 £5.28

£11.62

£5.26

£0

£12

Europe Asia-Pac Lat Am AME Am-Pac Group

Source: Company’s interim report 2008

Operating margin

23.6%

36.0%

40.9%

37.5%

40.3%

32.2%

25.7%

39.2%

36.1%34.7%

42.2%

32.2%

0.0%

45.0%

Europe Asia-Pac Lat Am AME Am-Pac Group

Source: Company’s interim report 2008

H1 2008H1 2007

Drivers of adjusted EPS growth

Pence %EPS H1 2007 53.5.Profit performance 3.5. 6.5.Net finance costs (1.1) (2.0)AssociatesTaxationMinoritiesShare buy-backExchangeEPS H1 2008

0.3.0.7.0.1.0.9.4.1.

62.0.

0.5.1.3.0.3.1.7.7.6.

15.9.

Source: Company data

Distributing 65% of sustainable net earnings as dividends (with balance of free cash flow for strategic acquisitions or share buy-backs, subject

to maintaining an acceptable credit rating)

Future expectations

Top Line Growth• Volume growth• Pricing• Mix Improvements

Productivity Savings• Overheads• Indirects• Supply Chain

Operating Profit growth of 6% p.a. on averageFinancial Efficiencies• Share buy backs• Others

High single digit earnings growth

* Based on internal estimates over the medium to long term

In summary:

Significant global business

Geographically diversified to mitigate risk

Leadership position in more than 50 markets

Clearly articulated strategy that works

Powerful brand portfolio

Innovative business developing new propositions

Improving margins through brand mix and productivity strategies

Highly cash generative with a strong balance sheet

Track record of consistent performance

Focused on delivering great shareholder value

Investor queries should be addressed to the Investor Relations Department in London. Please do not contact the local offices in South Africa.

Ralph Edmondson +44 207 845 1180

Rachael Brierley +44 207 845 1519

Top Related