Languages

Pages

Legal

Economics

Introduction to Basis, Cash Forward Contracts, HTA

Contracts and Basis Contracts

UK Grain Marketing Series January 19, 2016

Todd D. Davis

Assistant Extension Professor

Economics

Outline

• What is basis and how can we use basis in marketing decisions?

• Using Cash Forward Contracts (CFC), basis contracts and Hedge-to-Arrive (HTA) contracts

• Update on January WASDE reports • Commodity Challenge update

Economics

Nuts and Bolts of Commodity Futures • Two markets that tend

to move together • Futures – like a national

price. Impacted by US and World Supply/Demand Conditions

• Cash – local price impacted by local factors

• Basis = Cash - Futures

$1.50$1.60$1.70$1.80$1.90$2.00$2.10$2.20$2.30$2.40$2.50$2.60$2.70$2.80$2.90$3.00

2-Apr 2-May 2-Jun 2-Jul 2-Aug 2-Sep 2-Oct 2-Nov

Futures Cash

Hedging - Review • Sell futures when you have commodity to

sell in the future • Sell contract month nearest when you

intend to deliver or the next one after • Offset (buy) futures position when you sell

commodity • If prices fall, we gain on futures • If prices rise, we gain in cash market

Economics

Put Options Motivation

$4.50$4.75$5.00$5.25$5.50$5.75$6.00$6.25$6.50$6.75$7.00$7.25$7.50$7.75$8.00$8.25$8.50$8.75$9.00

3-Jan 3-Feb 3-Mar 3-Apr 3-May 3-Jun 3-Jul 3-Aug 3-Sep 3-Oct 3-Nov

Dec Futures

Hedging locks in a price ($5.50). Put Options create a price floor to benefit from higher prices ($7.50)

Economics

Put Options Overview

• Put Option – Gives the buyer the “right to sell” a contract at a

predetermined strike price • You only “sell” if the market moves down and

it benefits you to do so – Buy the right to sell Dec Corn futures at $4.10

• If the market moves down, your put becomes more valuable

• You pay a premium for this flexibility

What price floor can you set?

Strike Price

- Premium

- Basis

Price Floor

Futures price for contract month in which you plan to sell

Local basis for the month in which you plan to sell

Cost of the option

Economics

Graphically

3.20

3.80

Put Option

Straight Hedge

Overall Market

$ / bu

No Protection

What is basis? • The difference between local cash prices

and the futures price • cash price – futures price = BASIS

– Cash price is local price – Futures is a national price – Basis localizes the Futures price

• Negative basis sometimes expressed as “under” – “New crop corn bids are $0.30 under the

December board” Economics

What Impacts Grain Basis? • Transportation costs

– Distance from market • Storage and handling costs • Interest costs • Local supply / demand conditions

– Short crop vs. record large crop – Local weather / logistical challenges – Local markets?

Economics

Strengthening / Weakening Basis

• Strengthening basis = becoming more positive or less negative – Beneficial for short hedger – Market wants cash sales

• Weakening basis =

becoming less positive or more negative – Bad for short hedger – Market wants storage

$0.40$0.30$0.20$0.10$0.00($0.10)($0.20)($0.30)($0.40)

Narrowing orStrengthening

Widening orWeakening

Economics

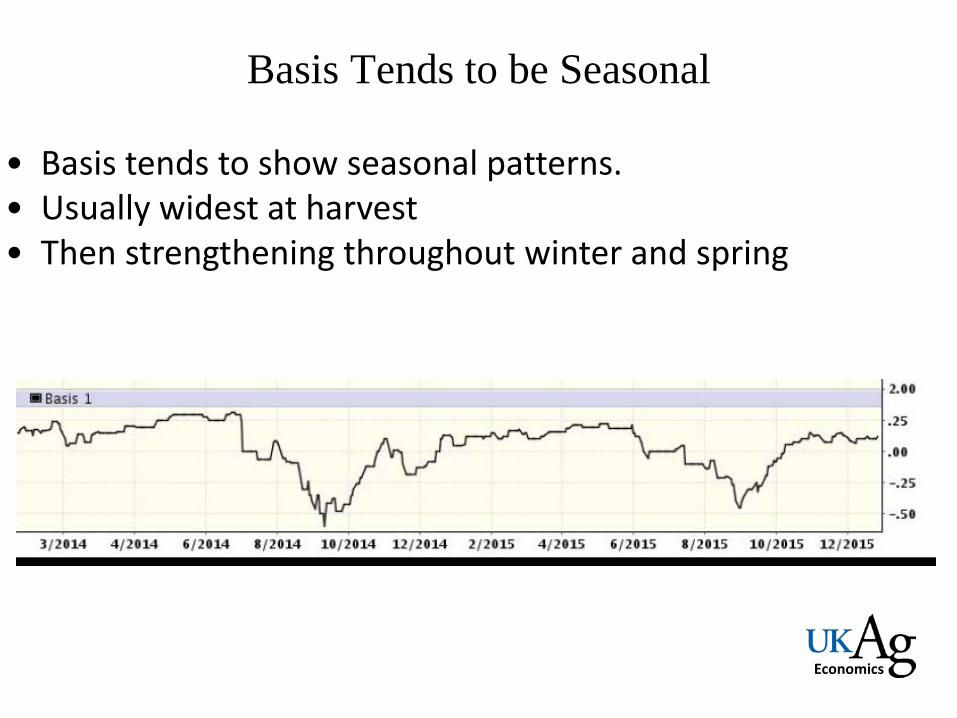

Basis Tends to be Seasonal

• Basis tends to show seasonal patterns. • Usually widest at harvest • Then strengthening throughout winter and spring

Economics

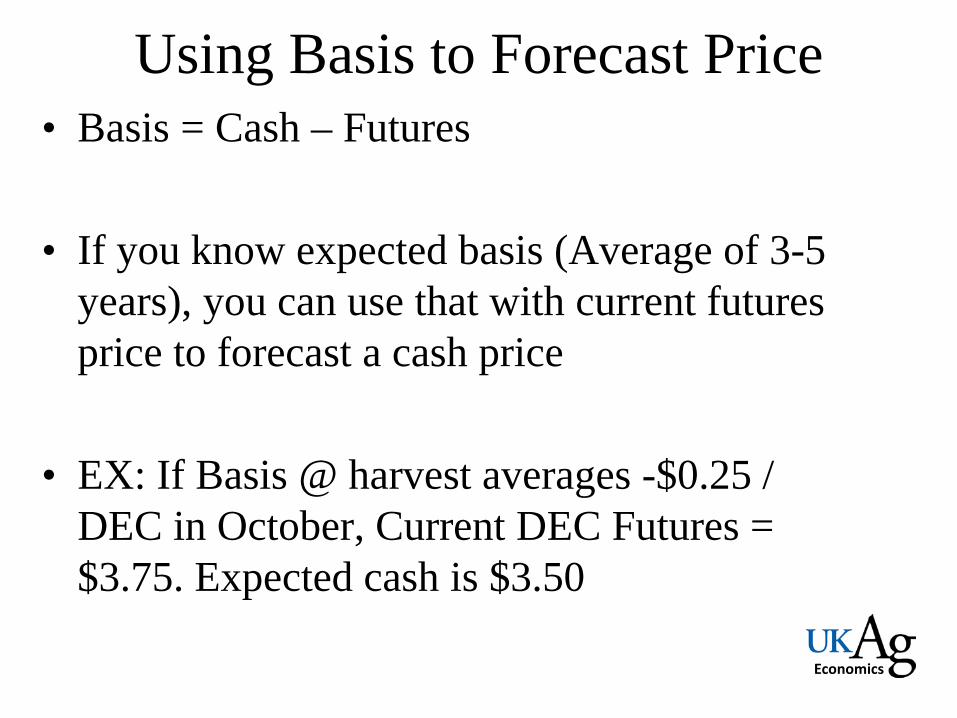

Using Basis to Forecast Price • Basis = Cash – Futures

• If you know expected basis (Average of 3-5

years), you can use that with current futures price to forecast a cash price

• EX: If Basis @ harvest averages -$0.25 / DEC in October, Current DEC Futures = $3.75. Expected cash is $3.50

Economics

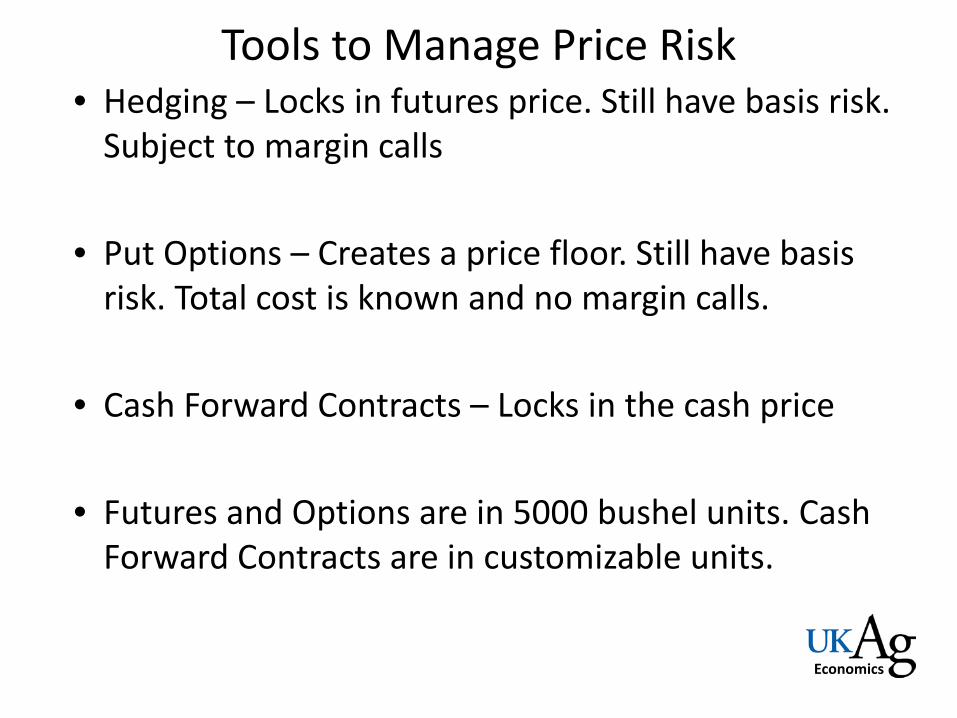

Tools to Manage Price Risk • Hedging – Locks in futures price. Still have basis risk.

Subject to margin calls

• Put Options – Creates a price floor. Still have basis risk. Total cost is known and no margin calls.

• Cash Forward Contracts – Locks in the cash price

• Futures and Options are in 5000 bushel units. Cash Forward Contracts are in customizable units.

Economics

• A contract that fixes the cash price. Farmer agrees to sell a fixed quantity at an agreed upon price at a specific date and location

• Advantages: – Ability to price before harvest – Eliminates futures price risk / basis risk; – Easy to understand – Not tied to 5000 bushel units

• Disadvantages: – Production risk – not able to fulfill contract – Locked into price. Don’t benefit if prices increase

Cash Forward Contracts

Economics

Using Cash Forward Contracts to Lock in a Price

Dec.Date Cash Futures BasisMar. 3 $4.00 $4.10 -$0.10 Actual

Nov. 3 $3.80 $3.90 -$0.10 Actual

Change in Price -$0.20

Cash Price $4.00 You've locked in a price.

Cash Forward Contract bid is $4.00 bushel. Contract 1000 bu for harvestdelivery

Sell 5,000 bushels of corn in cash market at $4.00 a bushel.

Economics

Using Cash Forward Contracts to Lock in a Price Dec.

Date Cash Futures BasisMar. 3 $4.00 $4.10 -$0.10 Actual

Nov. 3 $4.40 $4.50 -$0.10 Actual

Change in Price +$0.40

Cash Price $4.00 You've locked in a price.

Cash Forward Contract bid is $4.00 bushel. Contract 1000 bu for harvestdelivery

Sell 5,000 bushels of corn in cash market at $4.00 a bushel.

Economics

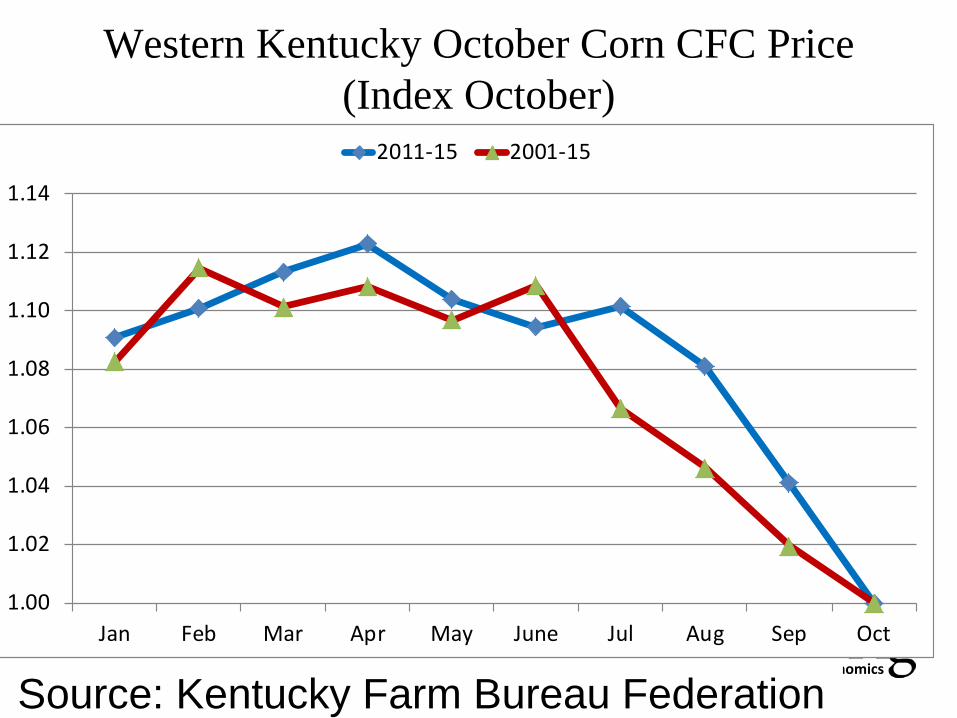

Western Kentucky October Corn CFC Price (Index October)

Source: Kentucky Farm Bureau Federation

1.00

1.02

1.04

1.06

1.08

1.10

1.12

1.14

Jan Feb Mar Apr May June Jul Aug Sep Oct

2011-15 2001-15

Economics

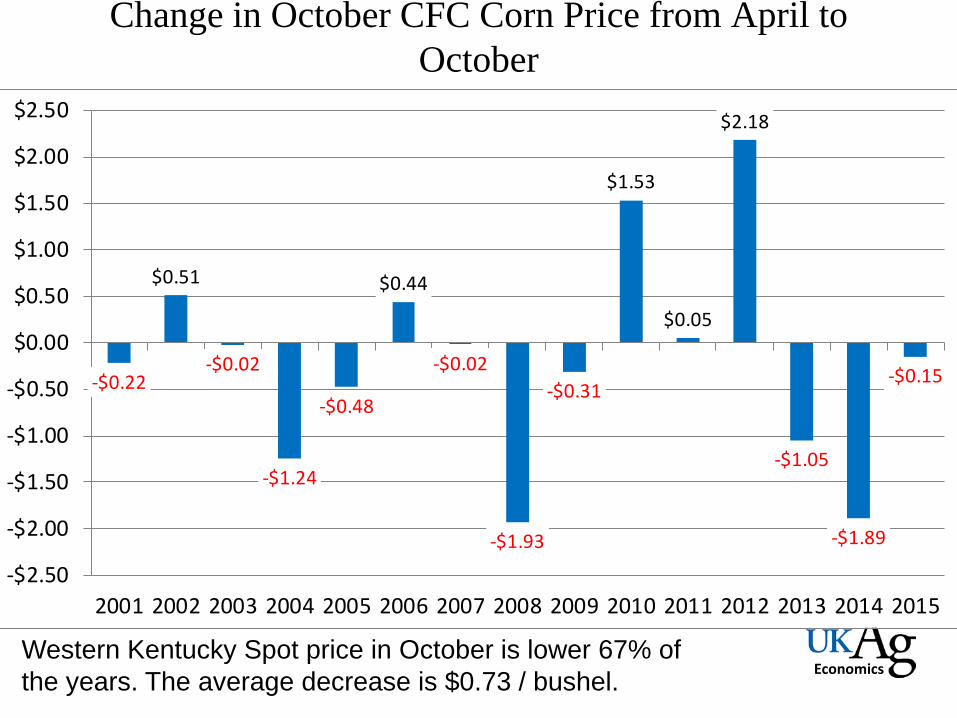

Change in October CFC Corn Price from April to October

-$0.22

$0.51

-$0.02

-$1.24

-$0.48

$0.44

-$0.02

-$1.93

-$0.31

$1.53

$0.05

$2.18

-$1.05

-$1.89

-$0.15

-$2.50

-$2.00

-$1.50

-$1.00

-$0.50

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Western Kentucky Spot price in October is lower 67% of the years. The average decrease is $0.73 / bushel.

Economics

Western Kentucky October Soybean CFC Price (Index October)

Source: Kentucky Farm Bureau Federation

0.900.920.940.960.981.001.021.041.061.081.10

Jan Feb Mar Apr May June July Aug Sep Oct

2011-15 2001-15

Economics

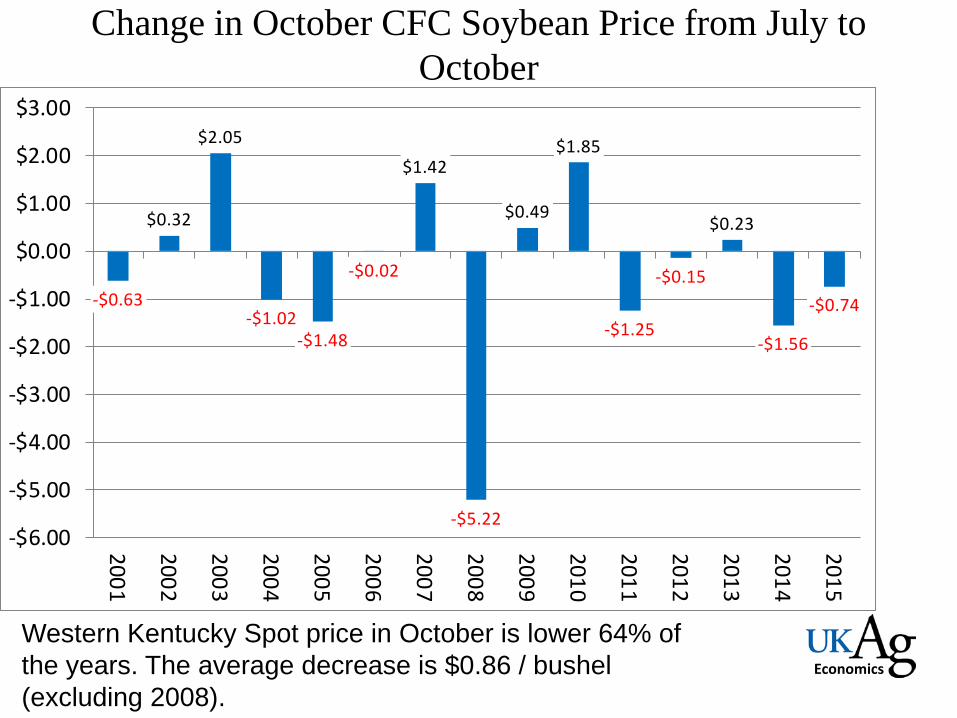

Change in October CFC Soybean Price from July to October

Western Kentucky Spot price in October is lower 64% of the years. The average decrease is $0.86 / bushel (excluding 2008).

-$0.63

$0.32

$2.05

-$1.02-$1.48

-$0.02

$1.42

-$5.22

$0.49

$1.85

-$1.25

-$0.15

$0.23

-$1.56

-$0.74

-$6.00

-$5.00

-$4.00

-$3.00

-$2.00

-$1.00

$0.00

$1.00

$2.00

$3.00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Economics

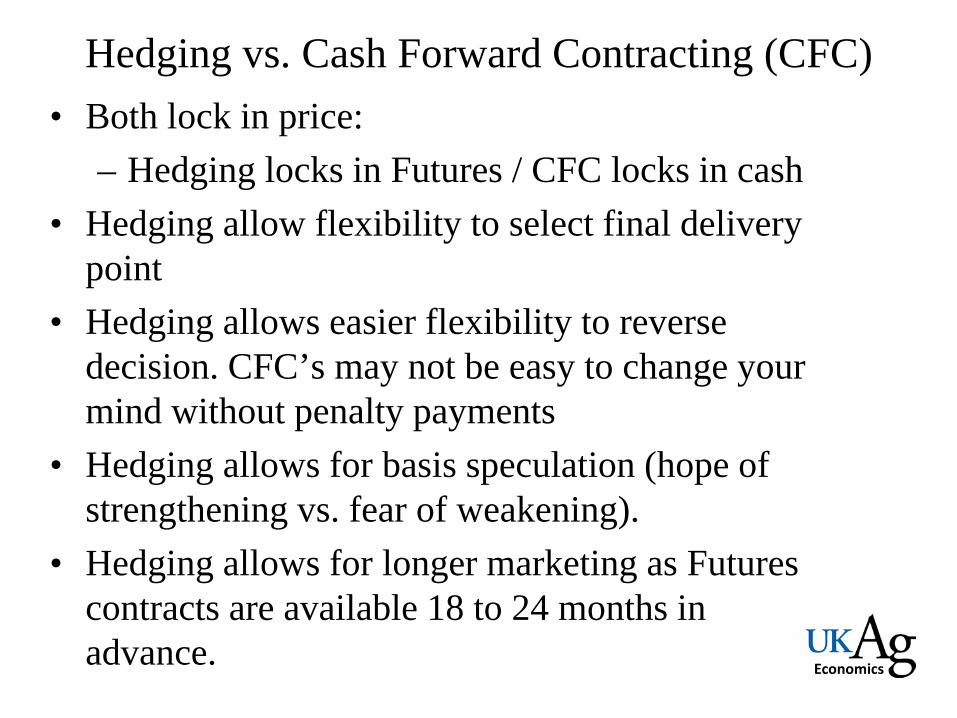

Hedging vs. Cash Forward Contracting (CFC) • Both lock in price:

– Hedging locks in Futures / CFC locks in cash • Hedging allow flexibility to select final delivery

point • Hedging allows easier flexibility to reverse

decision. CFC’s may not be easy to change your mind without penalty payments

• Hedging allows for basis speculation (hope of strengthening vs. fear of weakening).

• Hedging allows for longer marketing as Futures contracts are available 18 to 24 months in advance.

Economics

Advantages of CFC • Forward contracting – know the final price with

certainty • Forward contracting is simpler as don’t need

broker or understanding futures • Forward contracting doesn’t require margin

accounts or margin calls for cash flow problems • Forward contracting isn’t in 5000 bu lots. Can

customize to meet needs.

Economics

Basis Contracts • Allows to lock in basis for grain when basis is acceptable but

futures price is unacceptable and believe there will be higher future prices

• Have deadline to fix the futures price. At decision-time, can fix futures price or roll into another contract month (after paying a fee)

• Advantages: – Basis is locked and can’t widen (weaken) – Can benefit from rallies in the futures market

• Disadvantages – Can’t benefit from strengthening (narrowing) basis – Exposed to future price risk – If roll the contract, subject to market spreads and fees to roll

between contract months.

Economics

Examples: Basis Contracts

• Sell 5000 bu new crop corn for October delivery at basis of -$0.25 DEC futures.

• At harvest, decides to price at DEC Futures $6.05. • Net cash price is: $6.05 + -$0.25 = $5.80 bushel

Currently have a basis contract for -0.30 DEC Futures. DEC Futures = $2.60; May = $2.75

DEC – May Spread = -0.15 (2.60 – 2.75) Original basis = -$0.30 - -0.15 spread = new basis of $-0.45

Economics

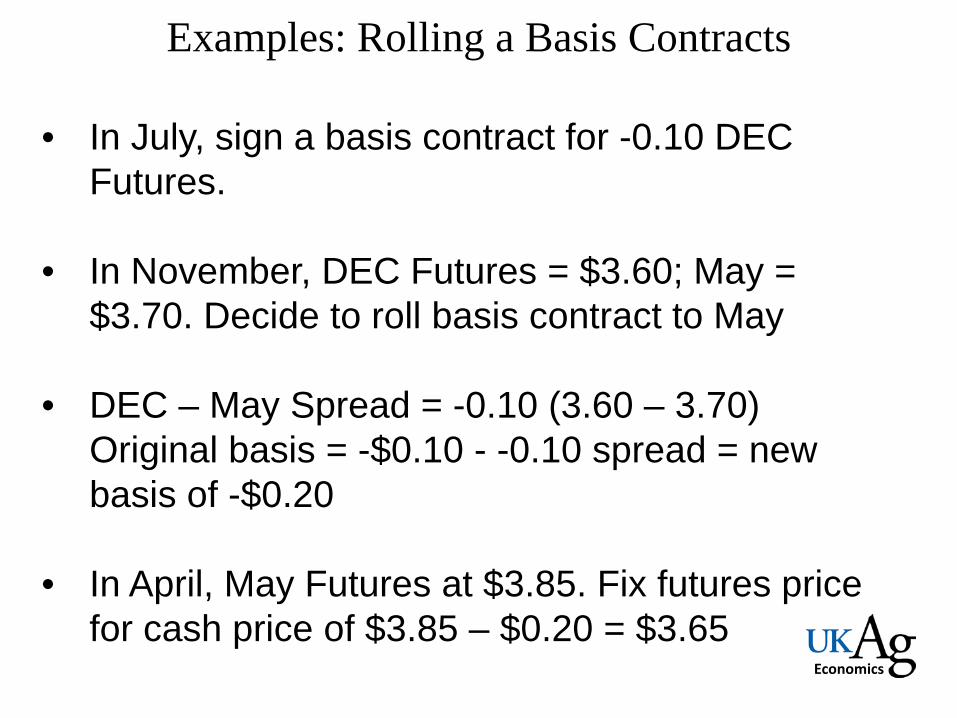

Examples: Rolling a Basis Contracts

• In July, sign a basis contract for -0.10 DEC Futures.

• In November, DEC Futures = $3.60; May = $3.70. Decide to roll basis contract to May

• DEC – May Spread = -0.10 (3.60 – 3.70) Original basis = -$0.10 - -0.10 spread = new basis of -$0.20

• In April, May Futures at $3.85. Fix futures price for cash price of $3.85 – $0.20 = $3.65

Economics

Hedge-to-Arrive (HTA) Contracts • A contract where fix the futures contract price but

not the basis – Like a short hedge except elevator manages the futures account

and margin calls – Can choose to roll contract within the same marketing-year

(September to August)

• A non-roll HTA: – Requires a specific quantity and quality of grain to sell at a

predetermined date and place – Basis risk is the main risk for non-roll HTA’s – Non-roll HTA’s prevent producer from benefiting from higher

prices.

Economics

Non-Rolling HTA Contract On July 1: DEC corn futures are at $3.75 with an expected harvest

basis of -$0.30. The CFC is $3.30. Decides to use a non-roll HTA contract to establish a better price.

• The Non-Roll HTA fixes DEC Futures at $3.75. Expected price is $3.75+-$0.30 = $3.45.

• At Harvest, producer delivers corn to elevator to fulfill HTA. Cash price is $3.35 and DEC contract is at $3.65. Basis is actually -$0.30

• Producer’s price is: $3.35 (cash) plus Futures gain ($3.75 - $3.65 = $0.10)

• Net price is $3.35 + $0.10 = $3.45 as expected o Like hedging, a stronger basis benefits farmers oA weaker basis is detrimental to farmers.

Economics

Intra-Year Rolling HTA • Similar to the non-roll HTA EXCEPT that the delivery date

can be changed to another time within the same crop marketing year (September – August for Corn/Soybeans)

• This can create intra-year spread risk between different contract month’s prices

• Potential price gains are from basis strengthening or rolling the price up to a later delivery contract month. Both are risky and could result in lower prices.

• More complicated as producer has to decide when to set the basis and when to roll the contract.

Economics

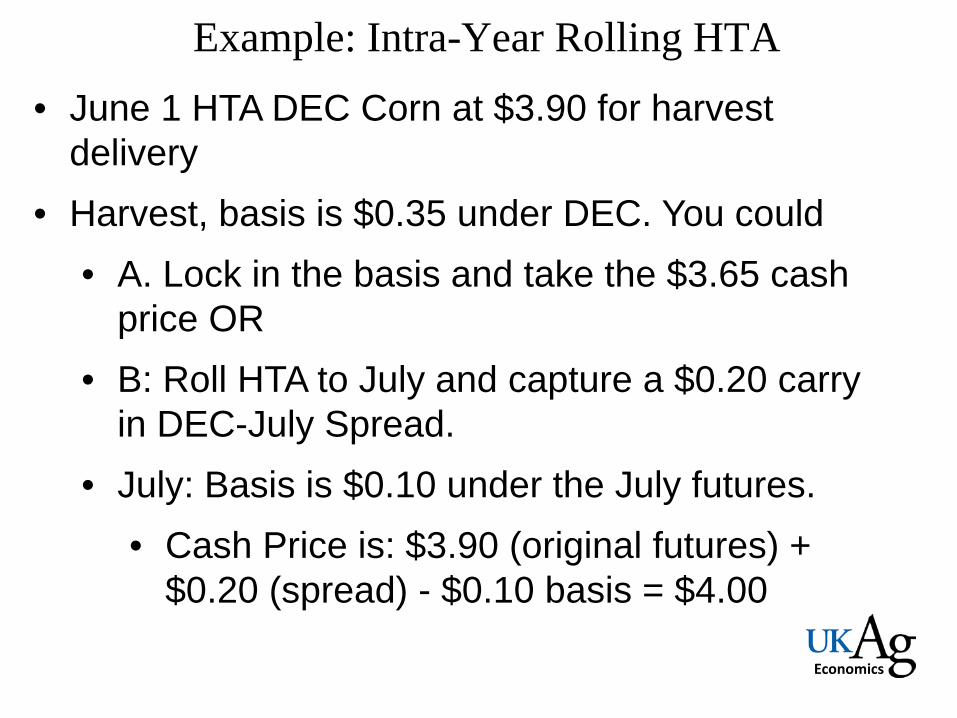

Example: Intra-Year Rolling HTA • June 1 HTA DEC Corn at $3.90 for harvest

delivery • Harvest, basis is $0.35 under DEC. You could

• A. Lock in the basis and take the $3.65 cash price OR

• B: Roll HTA to July and capture a $0.20 carry in DEC-July Spread.

• July: Basis is $0.10 under the July futures. • Cash Price is: $3.90 (original futures) +

$0.20 (spread) - $0.10 basis = $4.00

Economics

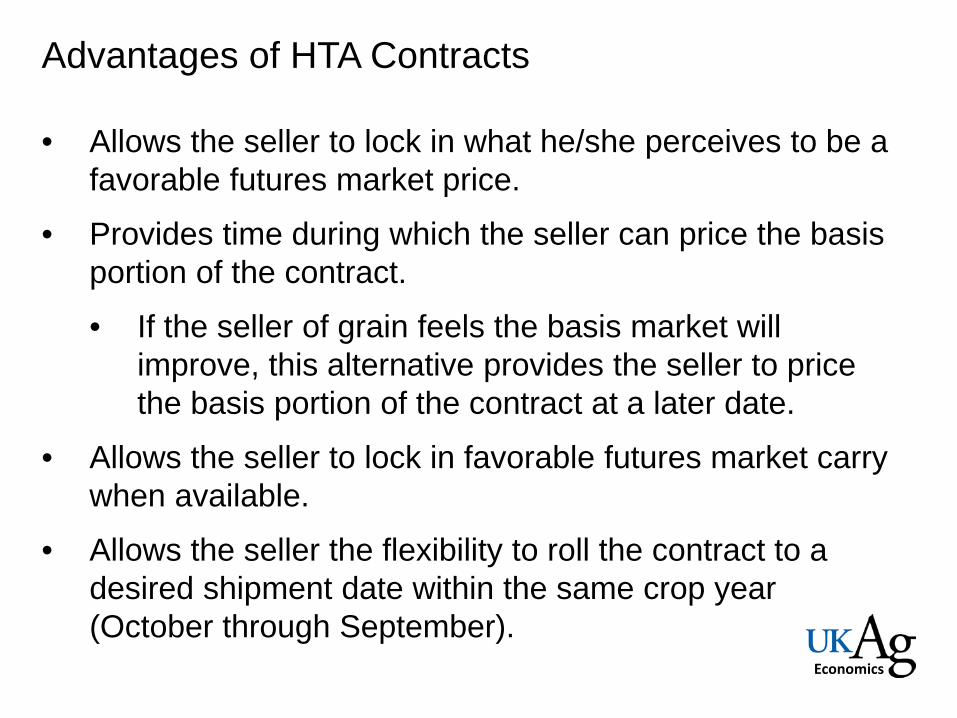

Advantages of HTA Contracts • Allows the seller to lock in what he/she perceives to be a

favorable futures market price.

• Provides time during which the seller can price the basis portion of the contract.

• If the seller of grain feels the basis market will improve, this alternative provides the seller to price the basis portion of the contract at a later date.

• Allows the seller to lock in favorable futures market carry when available.

• Allows the seller the flexibility to roll the contract to a desired shipment date within the same crop year (October through September).

Economics

Disadvantages of HTA Contracts • Does not allow the seller to benefit if the futures market

rally after the futures portion of the contract is priced.

• Does not lock in the basis portion of the trade. The seller is exposed to a potential basis decline.

• May expose the seller to quality deterioration if the seller has to store grain until a later delivery date.

Economics

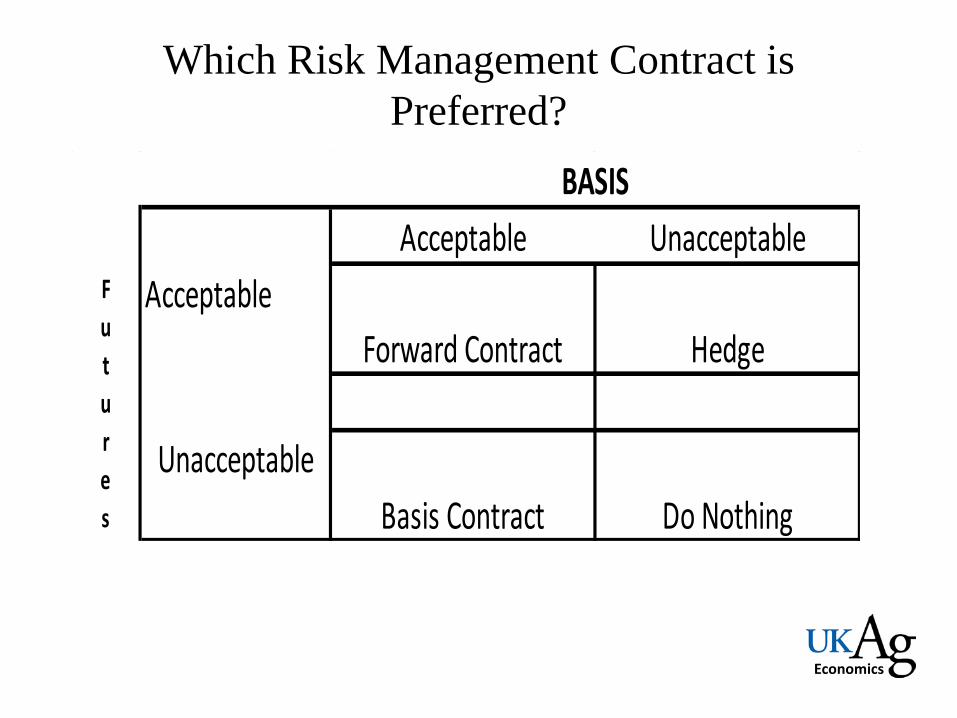

Which Risk Management Contract is Preferred?

Acceptable UnacceptableAcceptable

Unacceptable

BASIS

Forward Contract Hedge

Basis Contract Do Nothing

Futures

Economics

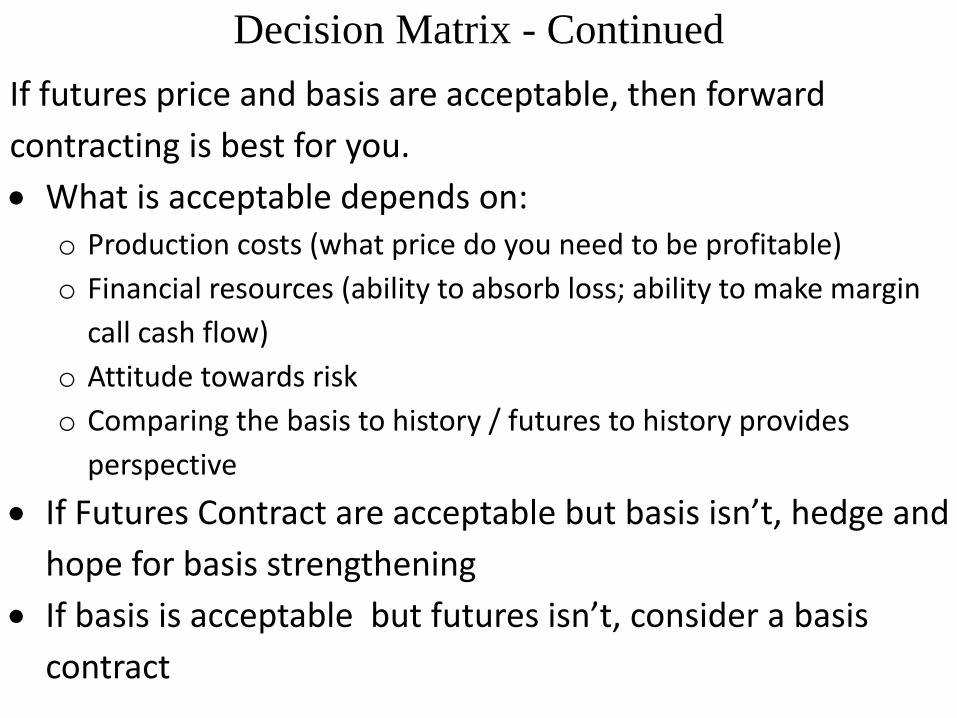

Decision Matrix - Continued If futures price and basis are acceptable, then forward contracting is best for you. • What is acceptable depends on:

o Production costs (what price do you need to be profitable) o Financial resources (ability to absorb loss; ability to make margin

call cash flow) o Attitude towards risk o Comparing the basis to history / futures to history provides

perspective • If Futures Contract are acceptable but basis isn’t, hedge and

hope for basis strengthening • If basis is acceptable but futures isn’t, consider a basis

contract

Economics

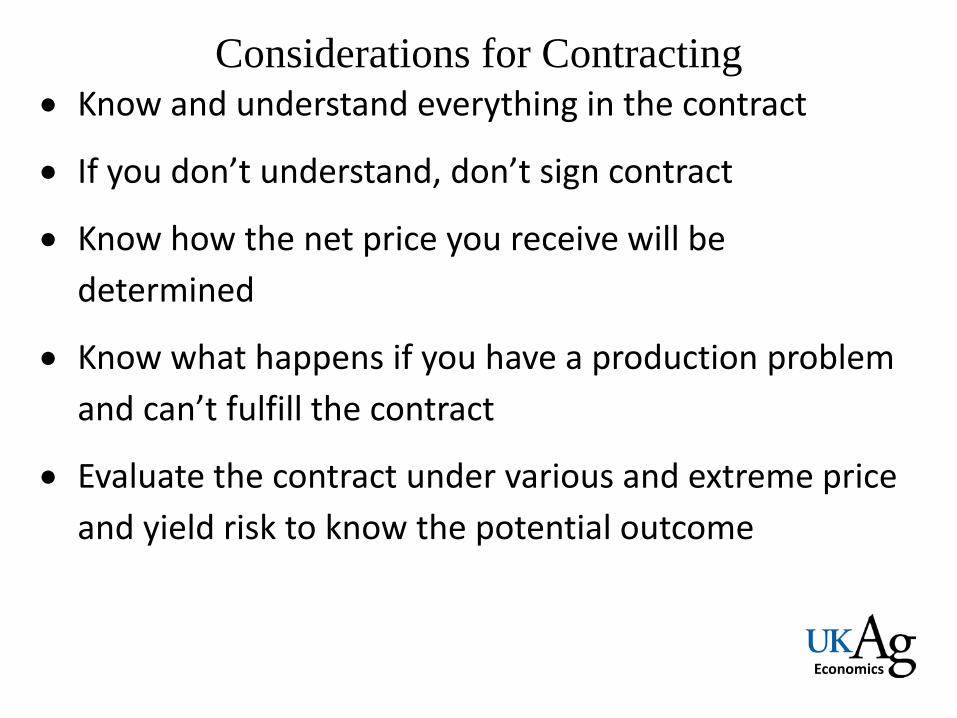

Considerations for Contracting • Know and understand everything in the contract

• If you don’t understand, don’t sign contract

• Know how the net price you receive will be determined

• Know what happens if you have a production problem and can’t fulfill the contract

• Evaluate the contract under various and extreme price and yield risk to know the potential outcome

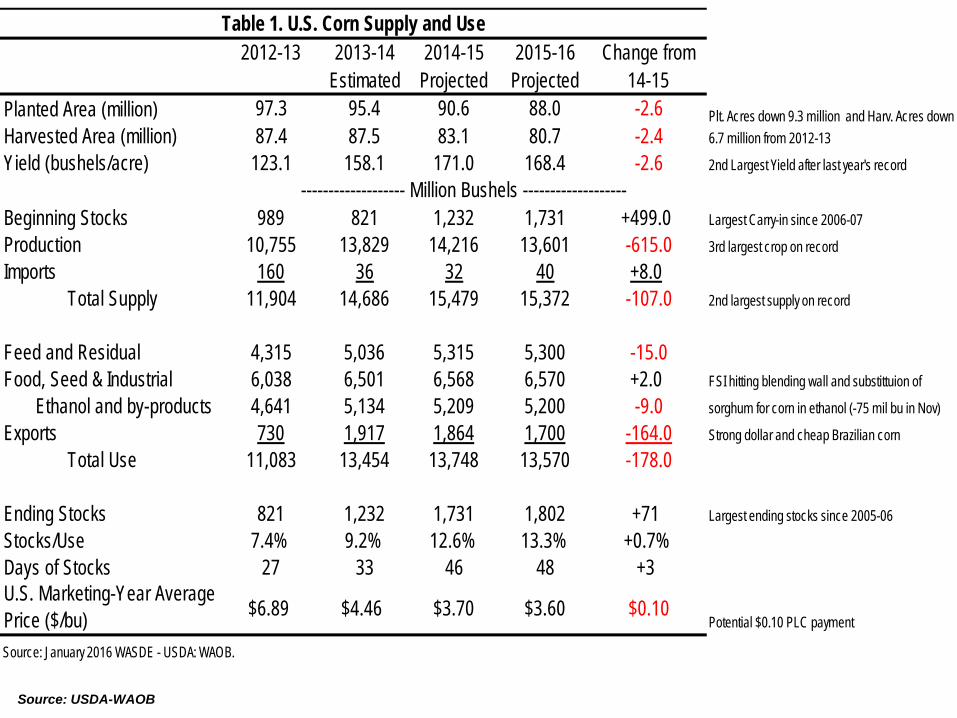

Source: USDA-WAOB

2012-13 2013-14 2014-15 2015-16 Change fromEstimated Projected Projected 14-15

Planted Area (million) 97.3 95.4 90.6 88.0 -2.6Harvested Area (million) 87.4 87.5 83.1 80.7 -2.4Yield (bushels/acre) 123.1 158.1 171.0 168.4 -2.6 2nd Largest Yield after last year's record

Beginning Stocks 989 821 1,232 1,731 +499.0 Largest Carry-in since 2006-07

Production 10,755 13,829 14,216 13,601 -615.0 3rd largest crop on record

Imports 160 36 32 40 +8.0 Total Supply 11,904 14,686 15,479 15,372 -107.0 2nd largest supply on record

Feed and Residual 4,315 5,036 5,315 5,300 -15.0Food, Seed & Industrial 6,038 6,501 6,568 6,570 +2.0 FSI hitting blending wall and substittuion of

Ethanol and by-products 4,641 5,134 5,209 5,200 -9.0 sorghum for corn in ethanol (-75 mil bu in Nov)

Exports 730 1,917 1,864 1,700 -164.0 Strong dollar and cheap Brazilian corn

Total Use 11,083 13,454 13,748 13,570 -178.0

Ending Stocks 821 1,232 1,731 1,802 +71 Largest ending stocks since 2005-06

Stocks/Use 7.4% 9.2% 12.6% 13.3% +0.7%Days of Stocks 27 33 46 48 +3U.S. Marketing-Year Average Price ($/bu) $6.89 $4.46 $3.70 $3.60 $0.10

Potential $0.10 PLC payment

Source: January 2016 WASDE - USDA: WAOB.

Table 1. U.S. Corn Supply and Use

------------------- Million Bushels -------------------

Plt. Acres down 9.3 million and Harv. Acres down 6.7 million from 2012-13

Economics

Strong dollar makes US exports less competitive Strongest Dollar since January 2003

Source: St. Louis Federal Reserve Bank

Economics Source: WAOB

US & World Ending Stocks -- Corn

42%

44%

46%

48%

50%

52%

54%

56%

0

50

100

150

200

250

2012 2013 2014 2015

Chin

a Sh

are

(%)

Endi

ng S

tock

s (M

MT)

US ROW China %

Economics Source: USDA-ERS

USDA’s Marketing-Year Price Projections (December 2015)

$3.70$3.65 $3.68 $3.65

$3.70 $3.70 $3.70 $3.70 $3.70 $3.70$3.75 $3.75

$3.00$3.10$3.20$3.30$3.40$3.50$3.60$3.70$3.80$3.90$4.00

Source: USDA-WAOB

Economics

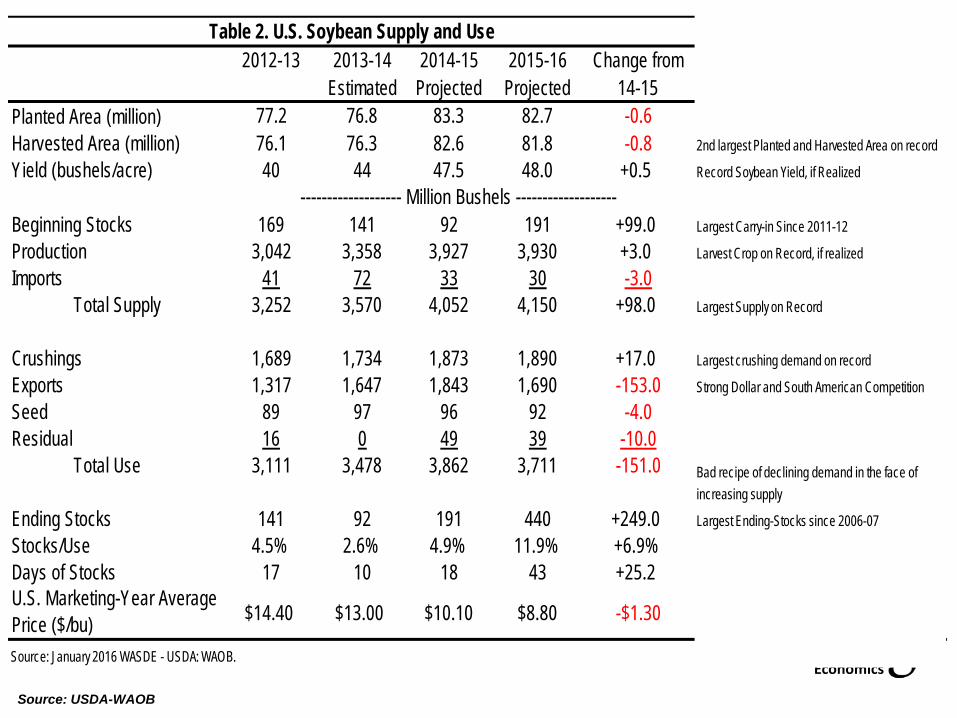

2012-13 2013-14 2014-15 2015-16 Change fromEstimated Projected Projected 14-15

Planted Area (million) 77.2 76.8 83.3 82.7 -0.6Harvested Area (million) 76.1 76.3 82.6 81.8 -0.8Yield (bushels/acre) 40 44 47.5 48.0 +0.5 Record Soybean Yield, if Realized

Beginning Stocks 169 141 92 191 +99.0 Largest Carry-in Since 2011-12

Production 3,042 3,358 3,927 3,930 +3.0 Larvest Crop on Record, if realized

Imports 41 72 33 30 -3.0 Total Supply 3,252 3,570 4,052 4,150 +98.0 Largest Supply on Record

Crushings 1,689 1,734 1,873 1,890 +17.0 Largest crushing demand on record

Exports 1,317 1,647 1,843 1,690 -153.0 Strong Dollar and South American Competition

Seed 89 97 96 92 -4.0Residual 16 0 49 39 -10.0 Total Use 3,111 3,478 3,862 3,711 -151.0

Ending Stocks 141 92 191 440 +249.0 Largest Ending-Stocks since 2006-07

Stocks/Use 4.5% 2.6% 4.9% 11.9% +6.9%Days of Stocks 17 10 18 43 +25.2U.S. Marketing-Year Average Price ($/bu) $14.40 $13.00 $10.10 $8.80 -$1.30

Source: January 2016 WASDE - USDA: WAOB.

2nd largest Planted and Harvested Area on record

Bad recipe of declining demand in the face of increasing supply

------------------- Million Bushels -------------------

Table 2. U.S. Soybean Supply and Use

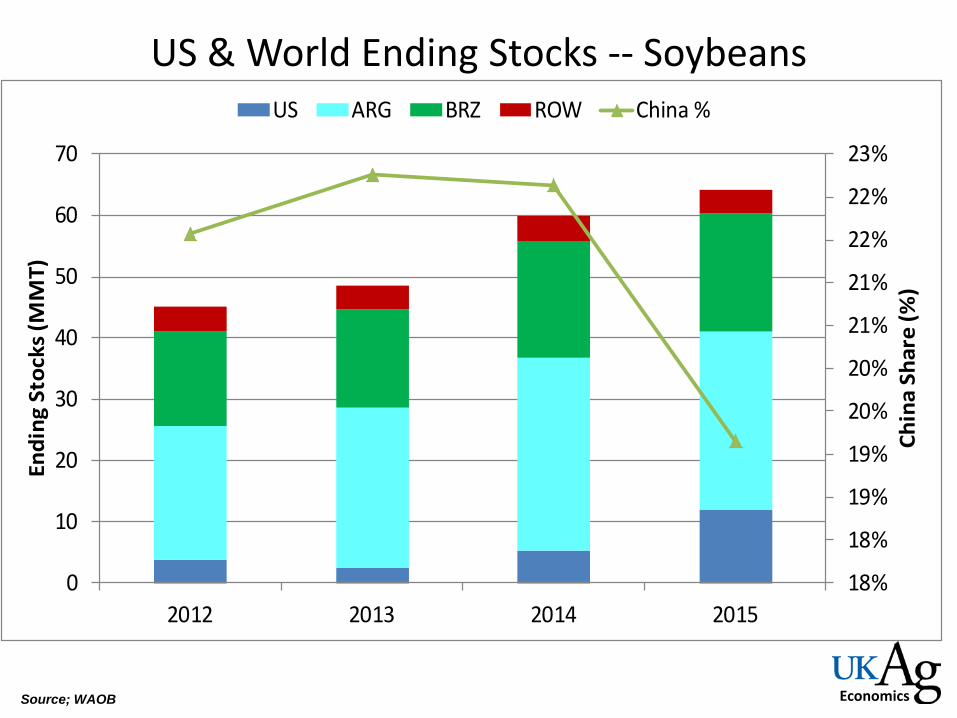

Economics Source; WAOB

US & World Ending Stocks -- Soybeans

18%

18%

19%

19%

20%

20%

21%

21%

22%

22%

23%

0

10

20

30

40

50

60

70

2012 2013 2014 2015

Chin

a Sh

are

(%)

Endi

ng S

tock

s (M

MT)

US ARG BRZ ROW China %

Economics Source: USDA-ERS

USDA’s Baseline Marketing-Year Price Projections (December 2015)

$10.10

$8.90$9.10

$8.80$8.95 $9.00

$9.10$9.20 $9.20 $9.20

$9.30 $9.35

$8.20$8.40$8.60$8.80$9.00$9.20$9.40$9.60$9.80

$10.00$10.20$10.40$10.60

Economics

Summary • World and U.S. rebuilt corn, soybean and

wheat stocks • China holds a large percentage of corn (of

questionable quality). Import needs? • South American economic uncertainty,

currency strength, export tax policy

Top Related