Languages

Pages

Legal

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 1/91

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 2/91

2

GLA INSTITUTE OF TECHNOLOGY AND

MANAGEMENT MATHURA, Affilated to MTU, Noida

Declaration

I, Parvendr Singh,MBA final year student of GLA Institute of

Technlogy And Management, Mathura, hereby declare that the

Research report work titled “A Study On Impulsive Buying

Behaviour Of Customer With Special Reference To Big Bazaar

” submitted in partial fulfillment of the requirements for the award

of the degree of Master of Business Administration under of

Mahamaya Technical University, Noida, is my own work.

The contents of the study in full or parts have not been submitted

to any other institution or university for the award of any Degree /

Diploma.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 3/91

3

Acknowledgement

A project is never the sole product of a person whose name has appeared on the cover.

Even the best effort may not prove successful without proper guidance. For a good

project one needs proper time, energy, efforts, patience, and knowledge. But without any

guidance it remains unsuccessful. I have done this project with the best of my ability and

hope that it will serve its purpose.

“To be or not to be is not anything which matters, how to be thankful is what really

matters”

It was really a great learning experience and I am really thankful to my faculties, who not

only helped me in the successful completion of this report but also spread his precious

and valuable time in expanding my knowledge base.

I wish to acknowledge my gratitude towards GLAITM, my friends and all those persons

who are responsible for the successful completion of this project.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 4/91

4

Executive Summary

As customers taste and preferences are changing, the market scenario is also changing

from time to time. Today‟s market scenario is very different from that of the market

scenario before 1990. There have been many factors responsible for the changing market

scenario. It is the customers changing tastes and preference, which has bought in a

change in the market. Income level of the people has changed; life styles and social class

of people have completely changed now than that of olden days. There has been a shift in

the market demand in today‟s world. Technology is one of the major factors, which is

responsible for this paradigm shift in the market. Today‟s generation people are no more

dependent on hat market and far off departmental stores. Today we can see a new era in

market with the opening up of many departmental stores, hypermarket, shopper‟s stop,

malls, branded retail outlets and specialty stores. In today‟s world shopping is not any

more tiresome work rather it‟s a pleasant outing phenomenon now.

The study is based on a survey done on customers of a hypermarket named big bazaar.Big bazaar is a new type of market, which came in to existence in India since 1994. It is a

type of market where various kinds of products are available under one roof. My study is

on determining the impulsive buying behavior of customer in big bazaar . The study will

find out the current status of big bazaar and determine where it stands in the current

market.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 5/91

5

This market field survey will help us in knowing the present customers tastes and

preferences. It will help in estimating the customer‟s future needs and wants.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 6/91

6

Introduction

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 7/91

7

Introduction

The retail industry in India gathered a new momentum with the establishment of different

international brand outlets, hyper or super markets, shopping malls and departmental

stores.

The organised retail segment in India is projected to be 9 per cent of total retail market by

2015 and 20 per cent by 2020. Hypermarkets would be the largest retail segment,

accounting for 21 per cent of the total retail space by 2013 – 14.

India has one of the largest number of retail outlets in the world. The retail sector is

experiencing exponential growth, with retail development taking place not just in major

cities, but also in Tier-II and Tier-III cities. India's growing population and urbanisationprovides a huge market for organised retail. Growing economic prosperity and

transformation in consumption pattern drives retail demand.

India ranks fourth among the 30 countries that were surveyed in Global Retail

Development Index and ranked sixth in the 2011 Global Apparel Index.

Organized retail in India constitutes a very little share of around 7.8% of the total retail

market. Of that 96% is in the ten biggest cities, and 86% in the biggest six. Through the1990s organized retail added just 1million sq.ft. of space a year. From 2001 onwards, the

pace quickened dramatically and 2003 alone saw an addition of 10 million sq.ft. retail

space. As per the Marketing White book 2009-2010, Indian retail market is estimated at

US$ 280 billion but organized retail is estimated at only US$ 14 billion. The sector

accounts for over 10% of the country's GDP and 8% of total employment of the nation's

workforce. Growth in the retail sector had fuelled a rapid mall building scenario across

the country, with the total number of malls expected to increase to 600 by 2010 from an

estimated 300 by end of 2007. Several retailers, including Indian corporate houses, are

foraying into the retail sector through different formats, unlike foreign retailers who

usually maintain three to four formats.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 8/91

8

Evolution of Retail Market in India

India as a country has the most unorganized retail market. "Kirana stores" the traditional

retail outlets work with an age old set up of a shop in the front & house at the back. More

than 99% retailers function in less than 500Sq.Ft of area. The producers distribute goods

through C & F agents to Distributors & Wholesalers. Retailers happen to source the

merchandise from Wholesalers & reach to end-users. The merchandise price gets inflated

to a great extent till it reaches from Manufacturer to End-user. Selling prices are largely

not controlled by Manufacturers.

The vibrant change in the market that has occurred in the past decade has made retailing

probably the hottest area to venture into. There is an elementary budge stirring in the

market.

In India Retail Industry has undergone with two different phases and in recent past it is

changing at faster speed form traditional Informal retailing sector to modern Formal and

Organized Retailing sector.

Informal Retailing Sector, consisting of typically small retailers who most of times

organize the things through sole proprietorship type of organizations. Due to there small

size and lack of capital investment they were mainly suffering from inefficient supply

chain management and approximately no monitoring of labor laws. Even from the

government's point of view, there was enough tax evasion as the tax enforcing

mechanism could never be applied over then due to their complex structure.

Formal Retailing Sector, consist of large retailers, who generally made available all

the consumer goods at one center. They are managed by corporate houses and

involves huge capital intake with them. As they are 'organized' there is absolute

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 9/91

9

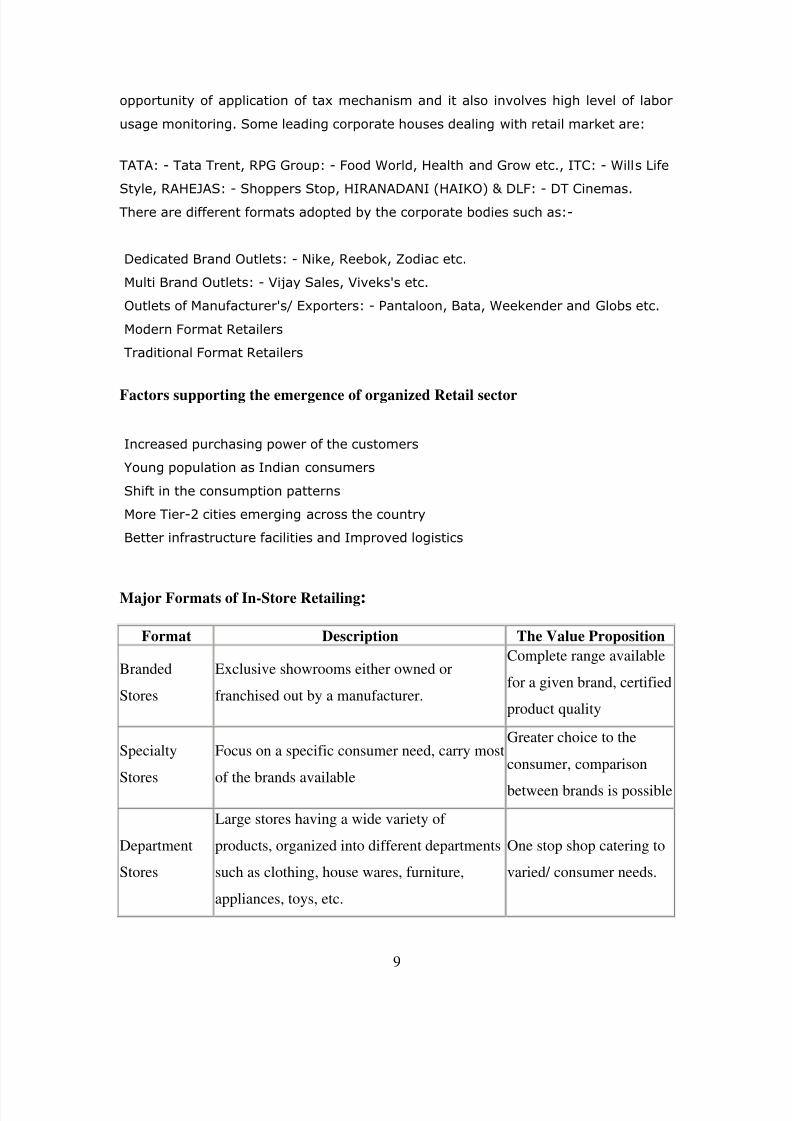

opportunity of application of tax mechanism and it also involves high level of labor

usage monitoring. Some leading corporate houses dealing with retail market are:

TATA: - Tata Trent, RPG Group: - Food World, Health and Grow etc., ITC: - Wills Life

Style, RAHEJAS: - Shoppers Stop, HIRANADANI (HAIKO) & DLF: - DT Cinemas.

There are different formats adopted by the corporate bodies such as:-

Dedicated Brand Outlets: - Nike, Reebok, Zodiac etc.

Multi Brand Outlets: - Vijay Sales, Viveks's etc.

Outlets of Manufacturer's/ Exporters: - Pantaloon, Bata, Weekender and Globs etc.

Modern Format Retailers

Traditional Format Retailers

Factors supporting the emergence of organized Retail sector

Increased purchasing power of the customers

Young population as Indian consumers

Shift in the consumption patterns

More Tier-2 cities emerging across the country

Better infrastructure facilities and Improved logistics

Major Formats of In-Store Retailing:

Format Description The Value Proposition

Branded

Stores

Exclusive showrooms either owned or

franchised out by a manufacturer.

Complete range available

for a given brand, certified

product quality

Specialty

Stores

Focus on a specific consumer need, carry most

of the brands available

Greater choice to the

consumer, comparison

between brands is possible

Department

Stores

Large stores having a wide variety of

products, organized into different departments

such as clothing, house wares, furniture,

appliances, toys, etc.

One stop shop catering to

varied/ consumer needs.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 10/91

10

Supermarkets Extremely large self-service retail outletsOne stop shop catering to

varied consumer needs

Discount

Stores

Stores offering discounts on the retail price

through selling high volumes and reaping

economies of scale

Low Prices

Hyper- mart

Larger than a supermarket, sometimes with a

warehouse appearance, generally located in

quieter parts of the city

Low prices, vast choice

available including

services such as cafeterias.

Convenience

stores

Small self-service formats located in crowded

urban areas.

Convenient location and

extended operating hours.

Shopping

Malls

An enclosure having different formats of in-

store retailers, all under one roof.

Variety of shops available

to each other.

Indian Retail- expanding the number of formats:

In modern retailing, a key strategic choice is the format. Innovation in formats canprovide an edge to retailers. Organized retailers in India are trying a variety of formats,ranging from discount stores to supermarkets to hypermarkets to specialty chains.

Formats Adopted by Key Players in India :

Retailer Original formats Later Formats

RPG Retail Supermarket (Food world)Hypermarket (Spencer's)Specialty Store

(Health and Glow)

Piramal'sDepartment Store (Pyramid

Megastore)Discount Store (TruMart)

Pantaloon

Retail

Small format outlets

(Shoppe)

Department Store(Pantaloon)

Supermarket (Food Bazaar)

Hypermarket (Big Bazaar) Mall (Central)

K Raheja

Group

Department Store (shopper's

stop)

Specialty Store (Crossword)

Supermarket (TBA)

Hypermarket (TBA)

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 11/91

11

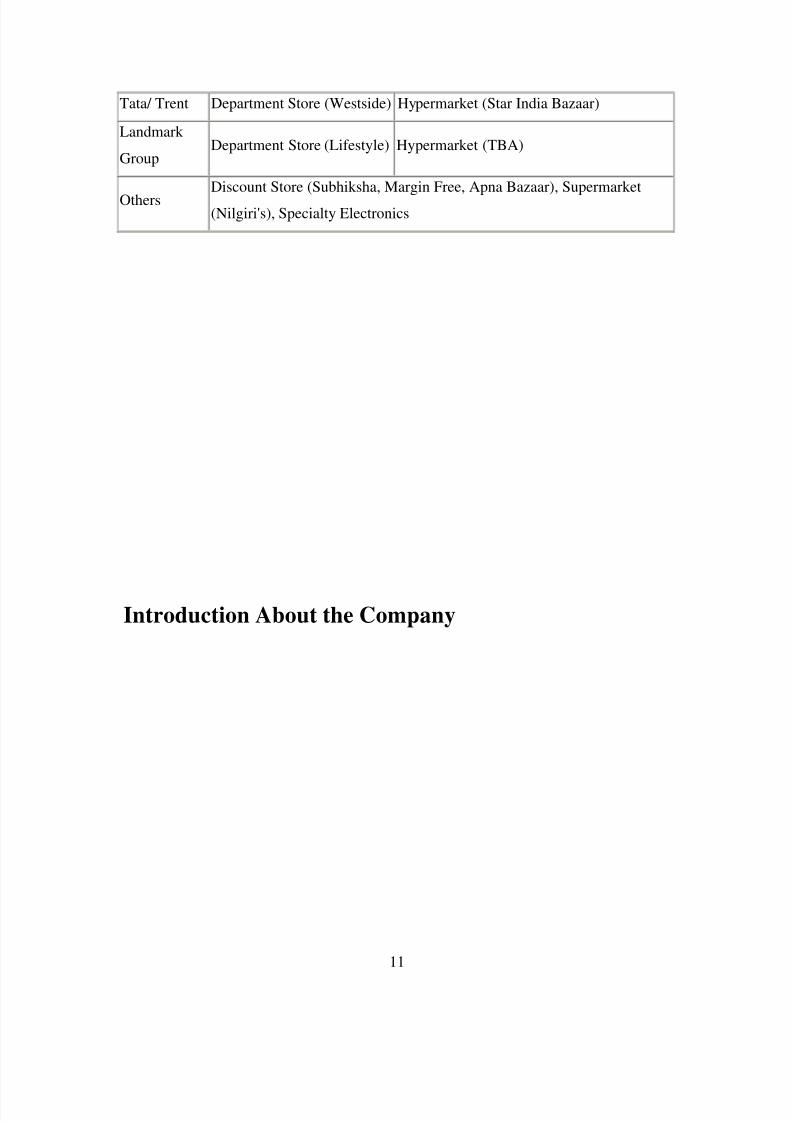

Tata/ Trent Department Store (Westside) Hypermarket (Star India Bazaar)

Landmark

GroupDepartment Store (Lifestyle) Hypermarket (TBA)

OthersDiscount Store (Subhiksha, Margin Free, Apna Bazaar), Supermarket

(Nilgiri's), Specialty Electronics

Introduction About the Company

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 12/91

12

Pantaloon Retail India Ltd (PRIL) has emerged as the leading retailer in India with its

chain of Pantaloon, Big Bazaar and Food Bazaar stores. With the right mix of

management capabilities, high growth product profile, well-developed strategy and

extensive IT and logistics capabilities, PRIL has ensured rapid growth. More importantly,

while most organized retailers are struggling to be in black, PRIL has demonstrated a

consistent track record of profitable growth.

PRIL has chalked out an aggressive expansion plan to increase its retail space to over

1,740,000 sq.ft. over the next two years. Space for additional 4 Pantaloon‟s, 11Big

Bazaars and 2 Food Bazaar‟s has already been finalized, and these would be Operational

over the next two years. PRIL aims to set up over 30 Food Bazaar‟s and is scouting for

appropriate locations for the same.

After popularizing the concept of hypermarket in India, PRIL is now also setting up a

new format shopping mall in the country under the name „Central‟. The format would be

on the lines of a Selfridges in London or a Central Mall in Bangkok. Two malls of

100,000 and 240,000 sq.ft. are being set up in Bangalore and Hyderabad respectively

Pantaloon Retail (India) Ltd. The Company's principal activity is to operate chain retails

stores in names of Big Bazaar, Food Bazaar, Central and Pantaloons. The Big Bazaar is

the discount store which offers a wide range of products under one roof. The products

include apparels and non-apparels such as utensils, sports goods and footwear. The

Company also has its presence into gold retailing by launching Gold Bazaar. The

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 13/91

13

Company's Food Bazaar provides a range of food and grocery products ranging from

fresh fruits and vegetables, staples, FMCG products and ready-to-cook products. The

Central offers a chain of stores including books and music stores, global brands in

fashion, sports and lifestyle accessories, grocery store and restaurants. The Pantaloon

retail stores focus largely apparels and accessories.

Pantaloon: Fashion by Pantaloon

Pantaloon is the company's departmental store and part of life style retail format. In fact,

PRIL took its very initial steps in the retail journey by setting up the first Pantaloon store

in Kolkata in 1997. In a short time Pantaloon has been able to carve a special place for it

self in the hearts and minds of the aspirational Indian customers. The company has depth

of offering for both men and women at affordable prices. A striking characteristic of Pantaloon has been the strength of its private label programme. John Miller, Ajile.

Scottsvile, Lombard, Annabelle are some of the successful brands created by the

company. With 13 stores across the country and an ever-increasing stable of private

brands, Pantaloon - in the coming years is poised to become a leading fashion trendsetter.

Big Bazaar: Is se sasta aur acha kahin nahin

Big bazaar is the company‟s foray into the world of hypermarket discount stores, the first

of its kind in India. Price and the wide array of products are the USP‟s in Big Bazaar.

Close to two lakh products are available under one roof at prices lower by 2 to 60 per

cent over the corresponding market prices. The high quality of service, good ambience,

implicit guarantees and continuous discount programmes have helped in changing the

face of the Indian retailing industry. A leading foreign broking house compared the rushat Big Bazaar to that of a local suburban train.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 14/91

14

Diversity of product range will ensure profitable volume growth To achieve better return on retail space, PRIL uses certain product categories as margin

managers and certain product categories to generate traffic. The food and groceries

business will act as key volume growth driver while high share of apparel (which account

for over 80% sales in Pantaloon Stores and 40% in Big Bazaar) will enable PRIL to

maintain high margins. The management has demonstrated its ability to improve stock

turnovers in both the formats successfully, which has enabled significant margin

improvement.

Fully integrated value chain and own labels give competitive edge

PRIL has a completely integrated value chain in apparels from fabric manufacturing to

apparel manufacturing, branding, distribution to retailing. The company controls the total

value chain from yarn to apparel retailing and gives a competitive edge in terms of speed

of delivery; lower inventory carrying costs and better realizations. Also, large part of

PRIL‟s apparel revenues comes from own private labels. PRIL has developed significant

competencies in apparel branding over a period of time and has developed own labels

(John Miller, Shrishti, Bare, Annabelle, AFL) in all the apparel product categories.

Worldwide, private labels give higher margin to retailers than the national brands.

Also growth of private labels is faster as retailer controls shelf space and visibility. Other

initiatives such as faster turnover of stocks by introducing 6 seasons in a year (against 2

earlier) has helped in bringing down inventory levels and at the same time providing

wider choice to customer and improving frequency of customer visits.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 15/91

15

High scalability of business model – multiplier effect will set in

Size and scale drive economies on procurement and lower logistics costs, which enables a

retailer to deliver better value to customers. The hyper-market format has much higher

scalability as compared to the pure apparel-retailing format. Also, the potential to expand

and scale is virtually unlimited in the food & grocery segment, where efficiencies

improve dramatically with scale as the multiplier effect sets in. Food constitutes the

largest expenditure item (estimated at over 50%) of an average

Indian‟s monthly personal expenditure. However, the share of modern retail formats in

the Rs6700bn Food & Grocery market is a minuscule 0.3%, revealing the high growth

potential in the segment.

New product categories and innovative tie-ups to aid growth

PRIL offers large number of products to the customer to give them better choice for

selection. Different product categories have different depth and width in merchandise

offering. Besides, PRIL has tied up with Shop-in-Shop partners in its Big Bazaar stores.

Some product categories where the company does not have core competency or does not

want to invest, but would attract customers are catered through these partners.

Eventually, in the long run, the Company may manage some of these product categorieson its own as volumes grow and it develops competencies in these businesses.

Shop-in-Shop partners typically pay a fixed rental for their space and share a part of their

profits. By expanding the range of product offerings and retail formats, PRIL today has

been able to target a much larger share of the consumer‟s basket (about 70% as against

less than 8% in 1994).

PRIL will be adding new product categories to its business in both Pantaloons as well as

Big Bazaar stores. Gold, Investment products, White goods and Appliances, Footwear

will be the new product categories that will be added. These product categories will help

in improving Walk In‟s into its stores and generate additional business from the existing

categories too.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 16/91

16

Competition from global players would pose a major threat

Most global retailing majors have been keen on entering into the huge untapped Indian

market. However policy restricts Direct Foreign Investment in the sector. There is a high

likelihood of the Government lifting restriction on FDI into the retail sector in the near

future. Entry of these foreign giants - with significant experience and skills in retail

management would increase competition for PRIL. However, we believe that given the

widely dispersed and heterogeneous nature of Indian markets, a foreign entrant would

find it extremely difficult to establish a national presence. Pantaloon with its early

Mover advantage and understanding of local markets is well entrenched to retain high

customer share.

Pantaloon Retail (India) Limited (PRIL) was incorporated on October 12, 1987 as Mainz

Wear Private Limited under the stewardship of Mr. Kishore Biyani. It was converted into

a public limited company in September, 1991. The company sold branded garments

under Pantaloon, Bare and John Miller brands. PRIL set up its first menswear Pantaloon

Shoppe outlet in 1993. The company‟s name was changed to Pantaloon Retail (India)

Limited in 1999, when it made a full-fledged entry into the retail segment through the

Pantaloons Family Store.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 17/91

17

Emerging trends in organized retailing

Over the last five years, a number of large business groups such as Tata‟s, RPG, Raheja‟s

and Piramal‟s has set up stores/malls and built businesses within retail. These include the

Rs1.9bn Food World - a leading supermarket chain set up by RPG; the Raheja ‟s Rs1.8bn

Shopper‟s Stop - a multi-brand departmental outlet and the Crossroads Mall set up by the

Piramal‟s. While many of these initiatives were initially driven by the need to use

existing real estate, they are beginning to assume the contours of a serious business today.

Fuel retailers, notably BPCL and HPCL are also expanding their presence from fuel retail

to grocery and convenience stores. Suitability of location, optimal utilization of real

estate, diversifying business to reduce reliance on the commodity nature of fuel retail

business and improve margins are the key factors that has lead fuel majors to

enter into the retailing.

Also, existing family owned businesses are expanding their businesses. The more

successful of them are the Nilgiris - a Bangalore base food retailer, Viveks - a 40-year old

Chennai based chain selling consumer durables and Narula‟s - the food chain in North

India.

Theme for a mall

Although the retail sector in India highly fragmented and consists predominantly of

small, independent, owner-managed shops, it happens to be the country's second largest

employer after agriculture. The country is currently witnessing a boom in retailing,

thanks mainly on account of an increase in the disposable incomes of middle and upper-

middle class households.

More and more corporate houses, including large real estate companies, are now entering

the retail business directly or indirectly. One sign of the modernization of Indian retailing

is the rapid growth in the number of specialty malls and theme malls. The Piramals,

Tatas, Rahejas, ITC, S. Kumar's, RPG Enterprises, Aerens, Omaxe and mega retailers

like Crosswords, Shopper's Stop and Pantaloon have taken the lead in organized retailing.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 18/91

18

Emergence of specialty retailing

Though organized retailing is still at a nascent stage - accounting for only around two per

cent of the $180 billion retail market in India - it is likely to touch 10 per cent by the end

of this decade. Four product categories have led the organized retailing wave: foods,

apparel, lifestyle products, consumer durables and electronics. In recent times, several

theme malls such as Gold Souk (jewellery malls), Wedding Mall, Electronic Mall, Auto

Mall, etc catering to specific needs and occasions have been completed or announced.

Many top developers are now toying with the idea of developing specialty malls.

Specialty malls are already a success in the West, whereas the concept is in its infancy in

India. One could venture so far as to say specialty and theme based retailing will drive

the growth of organized retailing in India.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 19/91

19

ORGAINSED RETAILING

Organised retailing got a leg up during 2008 with the opening of new format stores, rapid

growth of existing players, start-up of new-generation shopping malls, the Government'sintention of allowing a certain level of foreign direct investment in retail and the

formation of a retailers' association. With consumer sentiment positive during most of

2008, it led to substantial spending across a number of categories such as consumer

durables, clothing and lifestyle, automobiles and telecom products. At the beginning of

this decade, organized retailing accounted for a mere $2.9 billion in India. This is only

1.25 per cent of the estimated total retail market. This share has already grown to 2 per

cent. Growth projections for retail business vary widely. Some studies estimate that by

2011, the share of organized retail in the retail pie will jump three times to reach 5-6 per

cent.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 20/91

20

Major retail players in India

Future Groups-

Raymond Ltd.

Spencers-

Reliance

Aditya Birla Group -

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 21/91

21

Introduction to Topic

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 22/91

22

Impulsive buying behavior of Customer

Impulsive purchasing, generally de fined as a consumer‟s unplanned

purchase which is an important part of buyer behavior. It accounts for as much as

62% of supermarket sales and 80%of all sales in certain product categories. Thoughimpulsive purchasing has attracted attention in consumer research. Unfortunately, there is

a dearth of research on group-level determinants. This research suggests that the

presence of other persons in a purchasing situation is likely to have a normative

influence on the decision to make a purchase. The nature of this influence,

however, depends on both perceptions of the normative expectations of the individuals

who expert the influence and the motivation to comply with these expectations. Peers and

family members are the two primary sources of social influence, often have different

normative expectations. Thus, it has been evaluated two factors that are likely to

affect the motivation to conform to social norms The inherent susceptibility to

social influence and b)The structure of the group Group cohesiveness refers to the

extent to which a group is attractive to its members. The theory proposed by Fishbein

and Ajzen helps conceptualize these effects. This theory assumes that behavior is

a multiplicative function of expectations for what others consider to be socially

desirable and the motivation to comply with these expectations.

Promoting impulse buying behavior

The business implications are fairly obvious. If businesses wish to promote impulse

buying, they should create an environment where consumers can be relieved of their

negative perceptions of impulse. Businesses should stress the relative rationality of

impulse buying in their advertising efforts. Similarly, they should stress the non-

economic rewards of impulse buy

Additionally, businesses can make the environment more complex, further straining

consumers‟ abilities to process information accurately. Such techniques as stocking more

merchandise, creating stimulating atmospherics, and increasing information may be

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 23/91

23

useful to stimulate impulse buying. Businesses have to make impulse purchasing more

risk-free, through convenient return policies, or increase enablers such as credit and store

hours. Importantly, this model also offers options for consumers to control their buying

impulses, if they choose to, or feel better about their impulse buying, by relieving their

negative evaluations of impulse.

How to promote impulsive buying

Emphasise needs versus wants

Highlight that it will not impact on their shopping budgets over time

Create a store environment which dazzles them and where they loose control

Provide flexible payment methods. Some people have less cash in your wallet andsometimes leave credit cards at home

Avoid making the customer wait 24 hours before making an unplanned purchase

Demonstrate that this deal/offer will not last tomorrow before they realize that

such deals occur on a regular basis

Stress on the emotional aspect of owning the product.

Good amount of effort should be put into messages which should make consumer

recognize that buying on impulse is not bad. Once consumers recognize that products are

more than commodities and that they are buying to please their desires, they will feel

more comfortable with the impulse buying decision.

Traditionally impulse buying is defined as “Unplanned buying refers to all purchases

made without such advance planning and includes impulse buying, which is distinguished

by the relative speed with which buying “decisions” occur. Impulse buying occurs when

a consumer experiences a sudden, often powerful and persistent urge to buy something

immediately. The impulse to buy is hedonically complex and may stimulate emotional

conflict. Also, impulse buying is prone to occur with diminished regard for its

consequences.”

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 24/91

24

Why people buy impulsively?

Some say that it acts as a stress reliever

Perceive it as the best buy of that time

People are captivated as an audience

Consumers have extra money in their budget

These are some of the characteristics of impulsive buying

Unplanned, Spontaneous and intense urge to buy the purchaser often ignoring the

consequences

Without much prior knowledge of the product or intension to buy

A kind of emotional and irrational purchase often for reasons like fun, fantasy and

social and economic pleasure

Consumer often regret their purchase after purchasing

Internal factors affecting impulsive buying

Depends on the mood of the individual, positive mood triggers impulsive buying

Impulsive buying is more a need than a want Potential entertainment and emotional worth of shopping

Cognitive/affective

External factors affecting impulsive buying

Windows display

Visual merchandising

In-store form display

Promotional signage

Word of mouth messages

E-commerce

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 25/91

25

Impact of impulsive buying on the consumer

Disturbs the overall financial budget

Often gives product dissatisfaction and less alternatives are considered

People who go for impulsive buying often have post purchase regret

Irrational decision making being more emotional

The managerial implications of this analysis should be fairly obvious. If retailers wish to

promote impulse buying, they should create an environment where consumers can be

relieved of their negative perceptions of impulse. Retailers may stress the relative

rationality of impulse buying in their advertising efforts. Similarly, they may stress the

non-economic rewards of impulse buying.

Additionally, retailers can make the environment more complex, further straining

consumers' abilities to process information accurately. Such techniques as stocking more

merchandise, creating stimulating atmospherics, and increasing information may be

useful to stimulate impulse buying. Retailers can make impulse purchasing more risk-

free, through convenient return policies, or increase enablers such as credit and store

hours.

Consumers

Impulse buying processes are alternatives to planned decision making and consumers

must use these techniques with that in mind. If impulse is a response to information

overload, consumers may reduce the information processing demands by restricting their

search either to a few products or to several features of a larger number of products. They

may also develop decision aids, such as lists, comparison tables or graphs, reducing

reliance on heuristics. Similarly, they can allow enough time for gathering information

and evaluating options before purchase. These options will help make purposeful analysis

less frustrating and more productive. Other options include limiting unnecessary

emotional distractions like shopping buddies, especially children. Consumers can also

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 26/91

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 27/91

27

Remember then that shopping is fun. If you do, and you encourage your employees, then

the impulse shoppers will come to your store because it is a pleasure. And they will buy.

The understanding of impulse purchasing was greatly improved through Stern's

identification of four distinct classifications of impulse purchasing: planned, pure,

reminder and suggestion impulse purchasing. The four categories are as follows:

(1) Pure impulse buying is a novelty or escape purchasing which breaks a normal buying

pattern;

(2) Reminder impulse buying occurs when a shopper sees an item and remembers that the

stock at home is exhausted or low or recalls an advertisement or other information about

the item and a previous decision to buy;

(3) Suggestion impulse buying occurs when a shopper sees a product for the first time

and visualizes a need for it, even though he has no previous knowledge of it; and

(4) Planned impulse buying occurs when a shopper enters the store with some specific

purchases in mind, but with the expectation and intention to make purchases that depend

on price specials, coupon offers, and the like.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 28/91

28

NEED FOR THE STUDY

Impulsive purchasing, generally defined as a consumer‟s unplanned purchase is an

important part of buyer behavior. It accounts for as much as 62per cent of supermarket

sales and 80per cent of all sales in certain product categories. Moreover it can beunderstood from various literature reviews that Indian consumer‟s exhibits impulsiveness

and price consciousness behavioral dimension. Retail consumers tend to purchase

impulsively as they do not plan in advance and they also go for other brand if their

preferred brand is not available in a particular store. They are influenced by the store

brands‟ prices and try them during discounts and if the quality is delivered. In turn the

satisfied customers prefer to visit the retailer again and again. Thus, it could be concluded

that customer loyalty is customer‟s intention to purchase a specific product or services in

future repeatedly and customer loyalty is an important indicator of store health.

Customers can have long-term loyalty to the retail outlets. Long-term loyal customers do

not easily Change their store and product choice. Researchers understand that impulsive

buyers can be converted into loyal customer if they are satisfied. Moreover, it also

understood from that review of earlier studies that though impulsive purchases has

attracted much attention in consumer research, unfortunately there is a dearth of research

on group-level determinants.

Purpose of the Study

The purpose of the research study is to test the association of the independent variables

that are; shopping life style, fashion involvement, pre-decision stage, post-decision stage

regarding consumer purchasing with the dependent variable that is; impulse buying

behavior of consumers who shop in the Big Bazaar.

OBJECTIVES To analyse the buying behavior of the consumers‟ of Big Bazaar.

To measure the level of satisfaction derived by the shoppers at Big Bazaar.

To assess the future relationship between the retailer and his customers.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 29/91

29

To offer product and services according to the behavior of consumers.

To differentiate our offerings.

To fabricate loyalty programmes according to buying behavior of consumers.

REVIEW OF LITERATURE

International Journal Of Research In Commerce & Management.

Researchers have looked into the importance of customer satisfaction (Kotler, 2000)

defined satisfaction as “person‟s feelings of pleasure or disappointment results from

comparing a products perceived performance (or outcome) in relation to his or her

expectations”. The key of achieving organizational goals consists in determining the

needs and wants of target markets and delivering the desired satisfaction more effectively

and efficiently than competitors‟ (Kotler, 1991, p.10)Muhammad Ali Tirmizi, Kashif-ul-

Rehman, M.Iqbal saif (2009), in their study on “An Empirical Study of Consumer

Impulse Buying Behavior in Local Markets” have clearly indicated that there exists a

weak association between consumer lifestyle, fashion involvement and post decision

stage of customer purchasing behaviour with the impulsive buying behaviour.

Johan Anselmsson (2006) “on sources of customer satisfaction with shopping malls,

comparative study of different customers segments”, a study mainly f ocused on customer

satisfaction and visit frequency at shopping malls among customer segments based on

age and gender. It was found eight underlying factors are important to customer

satisfaction. Those are selection, atmosphere, convenience, sales people, refreshments,

location, and promotional activities and merchanding policy. Graeme D.Hutcheson and

Luiz Moutinho (1988) study on “measuring preferred store satisfaction using consumer

choice criteria as mediating factors” attempts to model causal effect that consumer‟s

perception of choice criteria used to determine supermarket patronage has on the levels of

perceived satisfaction with a preferred store. The likely importance of quality and value

for money as choice criteria was reinforced by strength of their releationship with

satisfaction, a variable generally believed to be one of the most important in determining

store patronization and repatronization. Robert A. Westbrook, (1981) “ study on sources

of consumer satisfaction for a large conventional department store has found that

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 30/91

30

satisfaction from multiple sources serves to raise overall satisfaction while dissatisfaction

from multiple sources corresponding lowers it. Peter Kennings (2007) study found that an

overall positive effect of trust buying behavior in food retailing. It is also found that

general trust has no influence on specific trust and the meaning of specific trust for

buying increases when general trust is low.Rajagopal (2008) in his “Study on point of

sales promotions and buying stimulation in retail stores” analyses buying behaviour in

reference to the point of sales promotion offered by retailing firm and the determinants of

sensitivity towards stimulating shopping arousal and satisfaction customer in order to

build store loyalty have been discussed in this paper. It is found that loyal customers are

attracted to the store brands. Lutz (1981) in his study has concluded that “A perspective

into consumer behaviour is motivated by a desire to understand the relationship between

attitude and behaviour” psychologists have sought to constant models to capture the

underlying dimensions‟ of an attitude. Eldon M. Kenneth E. Miller (1977) in their study

related to the post purchase communication found that it results in increased satisfaction

with the purchase letter communication.

For over fifty years, consumer researchers have strived to form a better definition of

impulse buying. Early studies on impulse buying stemmed from managerial and retailer

interests. Research in this vein placed its emphasis on the taxonomic approach to

classifying products into impulse and non-impulse items in order to facilitate marketing

strategies such as point-of-purchase advertising, merchandising, or in-store promotions.

This approach is limited by a definitional myopia, which simply equates impulse buying

to unplanned purchasing (Bellenger, Robertson, and Hirschman 1978; Kollat and Willet

1967; Stern 1962).

In response to this definitional problem, researchers began to focus on identifying the

internal psychological states underlying consumers‟ impulse buying episodes (e.g., Rook

1987; Rook and Gardner 1993; Rook and Hoch 1985). Impulse buying was redefined as

occurring "when a consumer experiences a sudden, often powerful and persistent urge to

buying something immediately. The impulse to buy is hedonically complex and may

stimulate emotional conflict. Also, impulse buying is prone to occur with diminished

regard for its consequences" (Rook 1987, p. 191). In the same vein, Hoch and

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 31/91

31

Loewenstern (1991) explained the impulse buying as a struggle between the

psychological forces of desires and willpower.

The shift in defining impulse buying has drawn particular attention to systematically

investigating factors that may underlie or cause impulse buying. This work includes

examinations of the mood-impulse buying relationship (Gardner and Rook 1988; Rook

and Gardner 1993); the relationship between affective states, in-store browsing, and

impulse buying (Jeon 1990); the holistic processing and self-object meaning-matching in

impulsive buying (Burroughs 1996); and the normative influences on impulse buying

(Rook and Fisher 1995).

Personality Factors Potentially Related to Impulse Buying

Several measurement instruments and models of personality exist. One which may have

particular value for studying impulse buying is the Multidimensional Personality

Questionnaire (MPQ) developed by Tellegen (1982). This instrument was developed in

an exploratory manner over a period of 10 years (Tellegen and Waller, in press). Items

originally based on personality attributes identified in prior models were developed,

tested, refined and revised by empirical testing. The final instrument identified 11

primary personality dimensions (Tellegen 1982). They are wellbeing, social potency,

achievement, social closeness, stress reaction, alienation, aggression, control, harm

avoidance, traditionalism, and absorption. Among these 11 dimensions are three that

seem to have particular relevance for the study of impulse buying. These dimensions are:

Lack of Control (or Impulsivity), Stress Reaction, and Absorption.

A Lack of Control (or Impulsivity).

Control relates to the individual‟s characteristic mode of monitoring impulse. When

dimensionalized, the underlying continuum is conceived of as representing excessive

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 32/91

32

containment of impulse and delay of gratification versus an insufficient modulation of

impulse and an inability to delay gratification. Controllers are reflective, cautious,

careful, rational, and sensible. They like to plan their activities (Tellegen 1982). On the

contrary, impulse-ridden individuals are spontaneous, reckless, and careless; they prefer

to "play things by ear." Their decisions are made rapidly and their emotional fluctuations

are readily visible. They tend toward immediate gratification of their desires even when

such gratification is inconsistent with the reality of their situation or their own ultimate

goal.

Impulse buying may be one manifestation of this personality trait Representing a lack of

control. Preferring planned-out activities seem to be counter to prior definitions of

impulse buying. Control would also run counter to Hoch and Loewenstern‟s conceptualization of impulse buying since it should provide people with the ability to

maintain high levels of willpower. A generalized lack of control or impulsivity would

therefore seem to be a potential contributor to impulse buying behaviors.

Cues That Trigger Impulse Buying

Many different factors have been suggested as triggering the impulse to purchase. By and

large, triggers are divided into two types Externals cues and internal cues (Wansink

1994). External cues are specific triggers associated with buying or shopping. They

involve marketer-controlled environmental and sensory factors. Internal cues refer to

consumers‟ self -feelings, moods, and emotional states.

Recent studies have stated that atmospheric cues in the retail environment (i.e., sights,

sounds, and smells) are important triggers that can influence a desire to purchase

impulsively (Eroglu and Machleit 1993; Mitchell 1994). Also it has been suggested that

marketing innovations such as credit cards, cash machines, instant credit, 24-hour

retailing, and telemarketing make it easier than ever before for consumers to buy things

on impulse (Rook 1987; Rook and Fisher 1995). Additionally, marketing mix cues such

as point-of-purchase, displays, promotions, and advertisements also can affect the desire

to buy something on impulse.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 33/91

33

Consumers‟ emotions or affective states have been regarded as potent internal triggers for

impulse buying. It is speculated that impulsive buyers are more likely to be responsive

(or sensitive) to their emotional conditions than non-impulsive buyers (Rook and Gardner1993). For impulsive buyers, their affective state can stimulate pursuit of the immediate

gratification that buying provides. In fact, recent work has proposed that buying impulses

may be partially motivated by a desire to change or manage emotions or mood states

(Gardner and Rook 1988; Rook 1987; Rook and Gardner 1993). Impulse buyers were

found to be more likely to buy on impulse in both negative moods and positive moods

than non-impulse buyers. The results suggest that impulse buyers are more prone to act

when experiencing hedonically charged moods regardless of their direction. Thus, it is

expected that both positive and negative affective states are closely ted to the tendency to

engage in impulse buying.

Most early efforts to study impulse buying behavior - those before 1987 - were concerned

with definitional issues and attempted to classify impulse into one of several sub-

categories, rather than to understand why so many consumers appear to act on their

buying impulses so frequently. This concern with developing classificational schemata

has generated a body of research that ignores the behavioral motivations leading to

impulse buying behavior for a large variety of products and instead focuses on a small

number of relatively inexpensive products. More recent studies have reported impulse

purchases across a broad range of product offerings in a variety of price ranges (Cobb

and Hoyer, 1986; Rook, 1987; Rook and Fisher, 1995). The pervasiveness of impulse

buying, even for relatively expensive products, is counter-intuitive and has led to a few

preliminary studies looking at impulse buying as an inherent individual trait, rather than a

response to inexpensive product offerings.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 34/91

34

RESEARCH METHODOLOGY OF THE STUDY

Technology and customers tastes and preferences plays a vital role in today‟s generation.

Research Methodology is a set of various methods to be followed to find out various

information‟s regarding market strata of different products. Research Methodology is

required for every industrial service industries for getting acquire knowledge of their

products.

RESEARCH DESIGN

Considering this work as a basic research, this study has followed descriptive researchdesign. An attempt is made in this study to understand an association between the

impulsive purchase made by the customers visiting a store and their association with the

concept of customer satisfaction. Data were collected from the potential customers of big

bazaar Mathura, Uttar Pradesh, India.

DATA COLLECTION

This study both primary & secondary data were collected for the study.

Primary Data

A questionnaire was designed to collect the primary data from the customers of BigBazaar ,Mathura.

Secondary Data

Articles on impulse buying were studied.

Measurement Technique

A questionnaire was designed by the researchers to be administered during the personal

interview. Care was taken to avoid loaded, double barreled, biased questions.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 35/91

35

POPULATION & SAMPLING FRAME

A Non-probability convenient sampling method was used to obtain the data from the

customers- Any shopping party leaving the Big Bazaar after making some purchases.

SAMPLING METHOD

A Sample of 100 respondents was chosen for data collection. It was observed at the end

of the week (data collected) nearly 25 questionnaires were incomplete. They were deleted

from actual population which gave a sample of 125 respondents in total.

.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 36/91

36

Limitations

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 37/91

37

Preparation of a project report and concluding a research is a whole process which is

carried out in a number of steps. Therefore through out the whole process of research

there are a number of difficulties encountered by researcher, at every step. In the present

study we may assume following limitation.

1. The data has been collected from the respondent of Mathura city. The result are

location specific and therefore the conclusion , the applicable to a different

district have different socio-economic condition.

2. As students, the researchers had limited amount of resources (time, money, etc)

to spend on this research.

3. The study related to a service quality is entirely based on the responses given

by the respondents. The view of respondents relating to a perception ,satisfaction and expectation may be based.

4. This research focuses on the incidence of impulse buying and a few factors

affecting it such as gender of the shopper, size of the shopping bill, presence of

a shopping list and the number of items purchased. This does not suggest that

these are the only factors that influence impulse buying decisions.

5. Some other influencing factors such as in-store stimuli (communication mix,

shelf placement), consumer traits other than gender, situational factors (mood,

time, money) and normative traits of decision making have not been studied.Hence, the findings of this study cannot be extended to those areas.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 38/91

38

Analysis

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 39/91

39

ANALYSIS

The survey is done on big bazaar. Survey is done of 100 respondents of Mathura who

come to visit big bazaar. A specific questionnaire is prepared for the customers and data

is obtained from them by moving around big bazaar and personally interacting with them.

The customers gave valuable information regarding their consumption pattern in big

bazaar. All informations are collected and a proper analysis is done.

All the analysis and its interpretations are discussed below. Each of the analysis is done

as per the information obtained from the customers and a serious interpretation has been

done to best of my effort.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 40/91

40

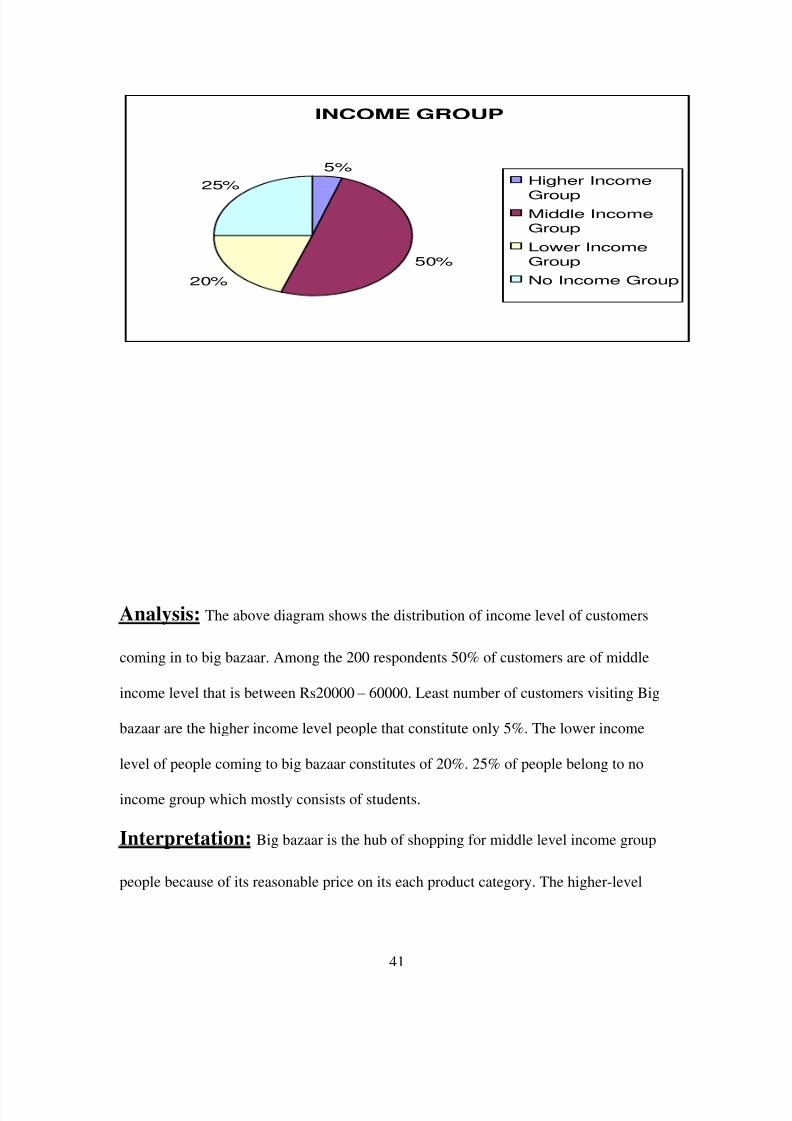

Income wise distribution of customers coming to big bazaar

Higher Income Group 5%

Middle Income Group 50%

Lower Income Group 20%

No Income Group 25%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 41/91

41

Analysis: The above diagram shows the distribution of income level of customers

coming in to big bazaar. Among the 200 respondents 50% of customers are of middle

income level that is between Rs20000 – 60000. Least number of customers visiting Big

bazaar are the higher income level people that constitute only 5%. The lower income

level of people coming to big bazaar constitutes of 20%. 25% of people belong to no

income group which mostly consists of students.

Interpretation: Big bazaar is the hub of shopping for middle level income group

people because of its reasonable price on its each product category. The higher-level

INCOME GROUP

5%

50%

20%

25% Higher Income

GroupMiddle Income

Group

Lower Income

Group

No Income Group

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 42/91

42

income group people don‟t prefer to do shopping in big bazaar, as it doesn‟t deal with

branded products. The higher-level income group people are very status conscious and

their psychology is such type that they don‟t prefer much to visit big bazaar, as it is a

discounted store. The lower income group people come in to big bazaar as they get goods

at a discounted price. Hence big bazaar should include branded products in its product

category, which will encourage higher income group people to come in to big bazaar.

Probably not much of lower income group people come to big bazaar as they don‟t like to

have any shopping experience rather they just go for near by store where they can get

their necessity goods. Even they purchase goods on a regular basis on a small quantity.

So they don‟t have much interest to come to big bazaar and do shopping.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 43/91

43

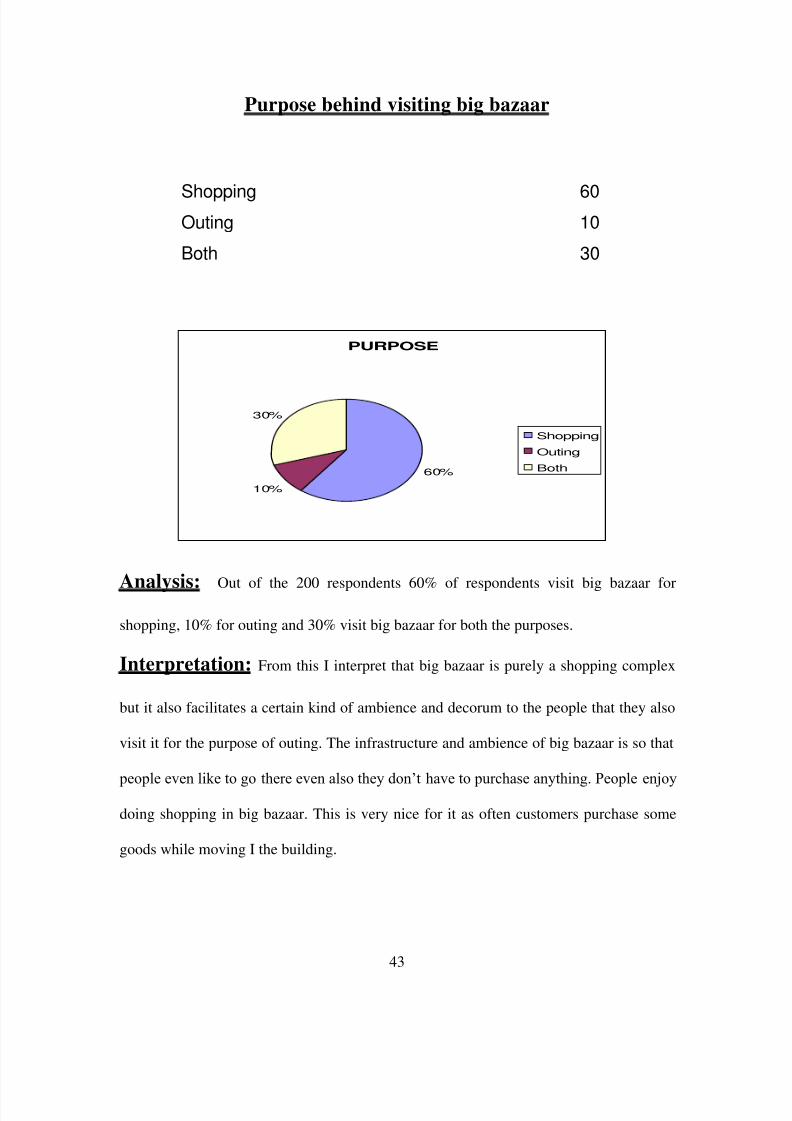

Purpose behind visiting big bazaar

Shopping 60Outing 10

Both 30

Analysis: Out of the 200 respondents 60% of respondents visit big bazaar for

shopping, 10% for outing and 30% visit big bazaar for both the purposes.

Interpretation: From this I interpret that big bazaar is purely a shopping complex

but it also facilitates a certain kind of ambience and decorum to the people that they also

visit it for the purpose of outing. The infrastructure and ambience of big bazaar is so that

people even like to go there even also they don‟t have to purchase anything. People enjoy

doing shopping in big bazaar. This is very nice for it as often customers purchase some

goods while moving I the building.

PURPOSE

60%

10%

30%

Shopping

Outing

Both

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 44/91

44

Demand for other retail outlets in a mall

Garment Outlet 40%

Footwear Outlet 15%Food Court 20%

Entertainment 10%

Gift Corner 10%

Jewellery and Watches Store 5%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 45/91

45

Analysis: The above graph shows that 40% of people visit garment outlet in a mall

other than that of big bazaar. 20% of people also prefer to visit food court in a mall other

40%

15%

20%

10%

10%

5%

garment outlet

foot wear outlet

food court

entertainment

gift corner

jewelery andwatches

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 46/91

46

than big bazaar. 15% of the people go to footwear outlet in a mall other than big bazaar.

10% of people also go to mall for entertainment purpose. Some people that are 15% each

also visit gift corner store and jewellery & watches store in a mall other than big bazaar.

Interpretation: From this analysis I come to know that most of the people tend to

visit garment outlets in a mall other than big bazaar as it has some exclusive branded

outlets. People also go for footwear stores as malls have branded footwear stores in it.

People go for watching movies to mall for entertainment. Yet a few people visits gift

corners and jewellery stores in a mall. This is of course a threat for big bazaar that it is

not able to attract customers from other retail outlets and retain them with it. Big bazaar

should definitely include more of branded products in its product category in order to

bring in the customers of mall to it and retain them with it. It can include some of the

exclusive branded outlets of cloths and jewellery in it in order to attract the brand choosy

customers.

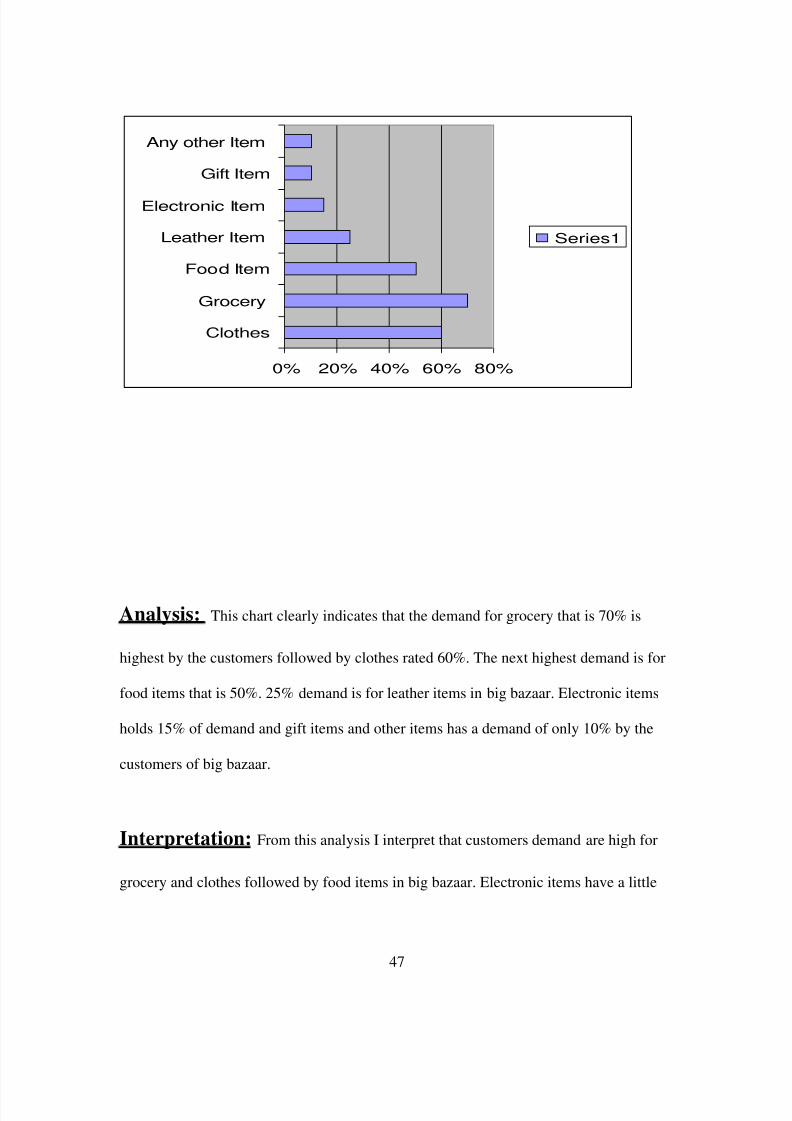

Products mostly purchased by customers in big bazaar

Clothes 60%

Grocery 70%

Food Item 50%

Leather Item 25%

Electronic Item 15%

Gift Item 10%

Any other Item 10%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 47/91

47

Analysis: This chart clearly indicates that the demand for grocery that is 70% is

highest by the customers followed by clothes rated 60%. The next highest demand is for

food items that is 50%. 25% demand is for leather items in big bazaar. Electronic items

holds 15% of demand and gift items and other items has a demand of only 10% by the

customers of big bazaar.

Interpretation: From this analysis I interpret that customers demand are high for

grocery and clothes followed by food items in big bazaar. Electronic items have a little

0% 20% 40% 60% 80%

Clothes

Grocery

Food Item

Leather Item

Electronic Item

Gift Item

Any other Item

Series1

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 48/91

48

demand by the customers. Gift items and other items are not much in demand by the

customers. I can interpret that clothes, grocery and food items are the major products

which hold maximum number of customers. So big bazaar should maintain its low

pricing and product quality to keep hold of the customers and also it should keep more

qualitative products of gift and leather items so that people would go for more purchase

of these items from it. Big bazaar has many local branded products of grocery and cloths

and it is successfully selling it. It should also include branded products so that more sales

can take place.

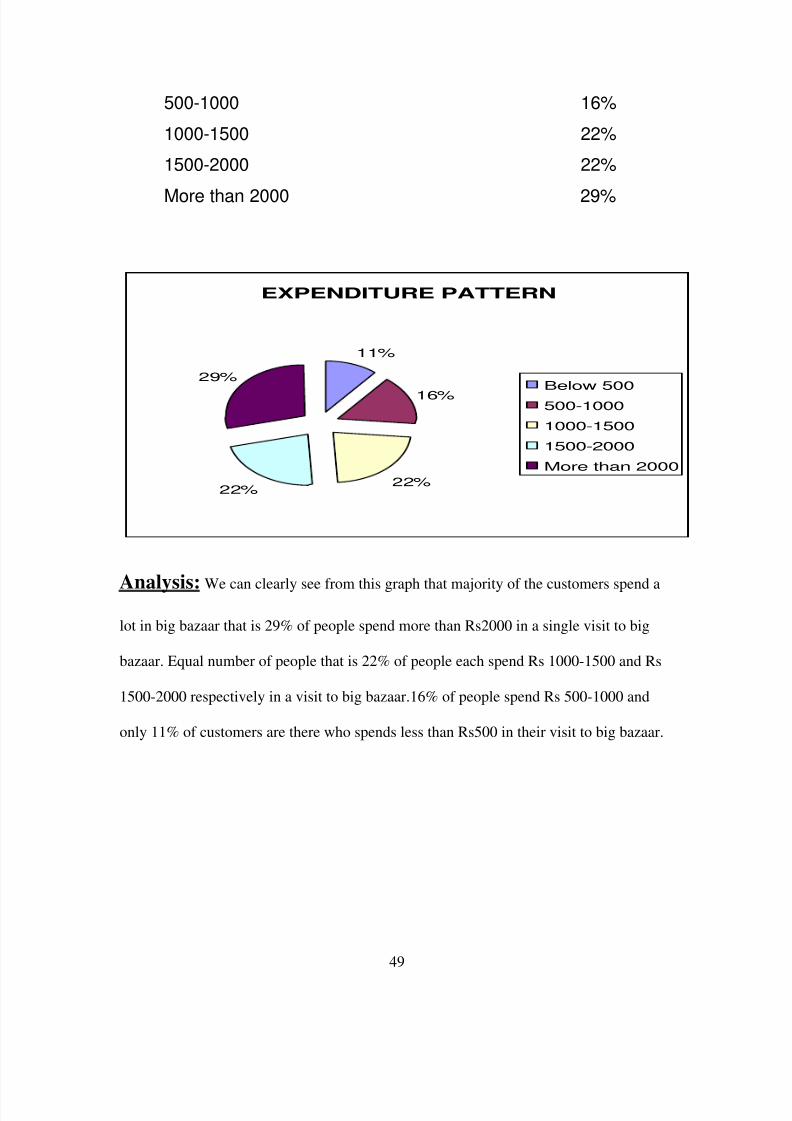

Expenditure pattern of customers coming in to big bazaar

Below 500 11%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 49/91

49

500-1000 16%

1000-1500 22%

1500-2000 22%

More than 2000 29%

Analysis: We can clearly see from this graph that majority of the customers spend a

lot in big bazaar that is 29% of people spend more than Rs2000 in a single visit to big

bazaar. Equal number of people that is 22% of people each spend Rs 1000-1500 and Rs

1500-2000 respectively in a visit to big bazaar.16% of people spend Rs 500-1000 and

only 11% of customers are there who spends less than Rs500 in their visit to big bazaar.

EXPENDITURE PATTERN

11%

16%

22%22%

29%

Below 500500-1000

1000-1500

1500-2000

More than 2000

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 50/91

50

Interpretation: From this I interpret that most of the customers purchase goods in

bulk which leads them to spend a lot. Volume sales are high in big bazaar. Customers

tend to purchase more goods from big bazaar as it provides goods at a discounted rate.

Probably those persons who spend more in a visit to big bazaar are purchasing on a

monthly basis. Those customers who are spending very less money that is below Rs 500

are mostly coming in just to move around big bazaar and spend time. In the process they

used to spend money on food items and also purchase some products while roaming in it.

Impulse buying behavior of customers comes in to play to a large extent. More discounts

shall be provided to people who does bulk purchase. This will encourage people to

purchase more products.

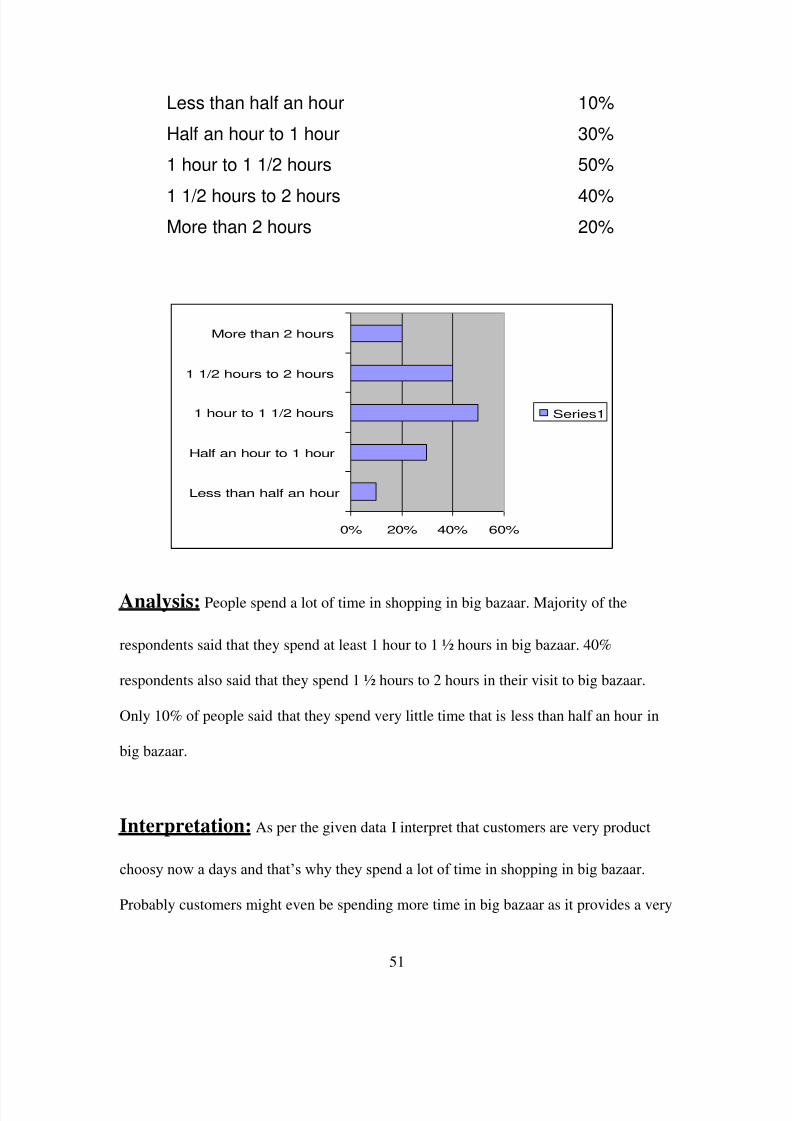

Time spent by customers in shopping in big bazaar

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 51/91

51

Less than half an hour 10%

Half an hour to 1 hour 30%

1 hour to 1 1/2 hours 50%

1 1/2 hours to 2 hours 40%

More than 2 hours 20%

Analysis: People spend a lot of time in shopping in big bazaar. Majority of the

respondents said that they spend at least 1 hour to 1 ½ hours in big bazaar. 40%

respondents also said that they spend 1 ½ hours to 2 hours in their visit to big bazaar.

Only 10% of people said that they spend very little time that is less than half an hour in

big bazaar.

Interpretation: As per the given data I interpret that customers are very product

choosy now a days and that‟s why they spend a lot of time in shopping in big bazaar.

Probably customers might even be spending more time in big bazaar as it provides a very

0% 20% 40% 60%

Less than half an hour

Half an hour to 1 hour

1 hour to 1 1/2 hours

1 1/2 hours to 2 hours

More than 2 hours

Series1

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 52/91

52

nice ambience and atmosphere for the people to shop in. Hence those persons who spend

half an hour or less than half an hour in big bazaar are those persons who just come to

purchase limited products and come only because of low pricing of products. People also

spend much time in it but purchase very few goods. The sales personnel should focus on

the people who take long time in shopping and purchases a lot and provide special kind

of service to them as they are the major customers.

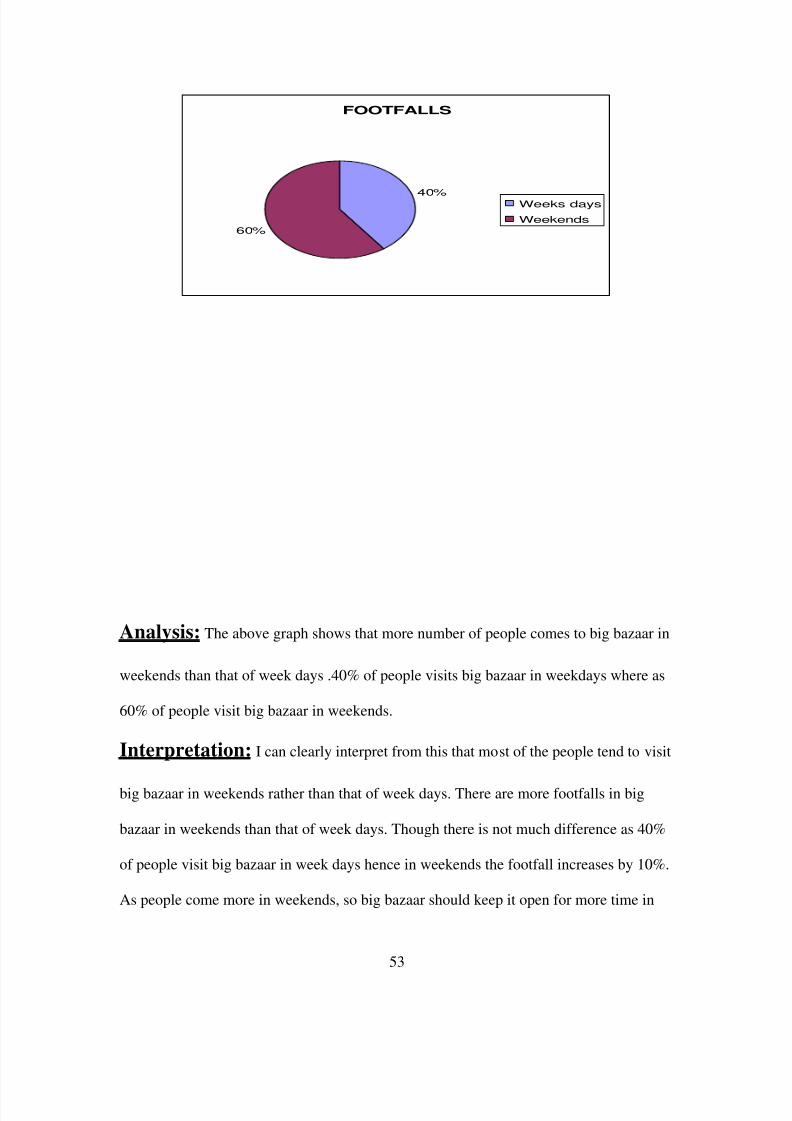

Comparison of footfalls in weekdays and weekends

Weeks days 40%

Weekends 60%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 53/91

53

Analysis: The above graph shows that more number of people comes to big bazaar in

weekends than that of week days .40% of people visits big bazaar in weekdays where as

60% of people visit big bazaar in weekends.

Interpretation: I can clearly interpret from this that most of the people tend to visit

big bazaar in weekends rather than that of week days. There are more footfalls in big

bazaar in weekends than that of week days. Though there is not much difference as 40%

of people visit big bazaar in week days hence in weekends the footfall increases by 10%.

As people come more in weekends, so big bazaar should keep it open for more time in

FOOTFALLS

40%

60%

Weeks days

Weekends

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 54/91

54

weekends. The infrastructure can be changed a bit in weekends so that customers can see

more products clearly and can move around comfortably. In order to bring in more

number of customers in week days big bazaar should provide some schemes in week days

which will encourage people to come in to it in week days also. Hence the crowd is more

in weekends and big bazaar should avail more parking spaces for its customers in

weekends. It can make some temporary arrangement for parking every weekend. It

should not spend much money in advertising and displaying of products in weekdays

rather it should advertise and display products more in weekends as more number of

people comes in weekends.

Customer’s preference of timing to visit big bazaar

10 A.M. - 6 P.M. 42%

6 P.M. -10P.M. 58%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 55/91

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 56/91

56

Interpretation: From the above analysis I interpret that evening time is the peak

time for big bazaar and daytime is the off peak time for big bazaar. There is more number

of people found in big bazaar during evening time than that of daytime. Probably more of

products are being sold during evening time in big bazaar than that of daytime. Big

bazaar shall provide some special offerings during daytime so that more people should

come in during daytime. It could offer some special kind of product in daytime, which

will be not available during evening time. In this way it will bring in more number of

people during day time for getting the special kind of products but along with that it will

be able to sale other products as people do a lot of impulse buying at big bazaar.

Comparison of customers purchasing with planned list of

products and purchasing products on an unplanned basis

Yes 80%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 57/91

57

Analysis: As shown in the graph out of my total respondents of 200, 80% of

customers come to big bazaar with a planned list of products. Only 20% of people come

in to big bazaar without any planned list of products to be purchased from big bazaar.

PLANNED AND UNPLANNED

BUYERS

80%

20%

Yes

No

No 20%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 58/91

58

Interpretation: As per the data obtained from the customers of big bazaar I

interpret that most of the customers comes in to big bazaar with a planned list of

products. Few customers come to big bazaar without any planned list of products and

purchases products depending on their selection. These people basically come to the mall

and hence get in to big bazaar. Depending on the product category and brand and quality

of products they purchases goods. Some couples come to mall and go to food bazaar to

have food together and to have chit chat among them. The customer who comes with a

planned list of products purchases more products than that of the customers who comes

without any planned list of products. So big bazaar should provide more variety and

essential goods so that more number of people should come in with a planned list of

products.

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 59/91

59

Brand preference of customers in big bazaar

Yes 10%

No 50%

Depends on category 40%

Analysis: As seen in the above chart it is clearly known that only 10% of people

come in to big bazaar with a list of brands in advance. 50% of people completely deny

that they don‟t prepare in list of brand in advance. 40% of people told that they prepare a

list of brand depending on the product category.

BRAND PREFERENCE

10%

50%

40%

Yes

No

Depends on

category

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 60/91

60

Interpretation: From this I interpret that customers don‟t opt for much brand

preference while purchasing products in big bazaar. A few customers search for brands

but depending on the product category. Customers probably don‟t decide for brands on

products as there are not much of known branded products available at big bazaar. On

product categories like grocery and clothes, big bazaar has many local branded products.

Customers purchase a lot of these, as it‟s cheap in price even though its quality is not so

good. As most of the customers belong to lower class and middle class people, they

purchase those local branded products as it gives them value for money. Different

products of the same category have different prices. Quality of products varies with the

price. This enables customization of products for various types of customers. Customers

search for brands mostly in apparel section. Some customers also pre decides the brand

on the local manufactured grocery and food products of big bazaar. Big bazaar should

include more of the branded products in its each category so that customers have more

options to choose among the brands. This will bring in more number of people to big

bazaar, which will definitely increase the sales.

Comparison of brand preference on different product category

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 61/91

61

Analysis: This graph shows that cloths and grocery are the only two items on which

customers mostly prefer the brands that is 40% each. 33% brand preference is on gift

0%

5%

10%

15%

20%

25%

30%

35%

40%45%

C l o t h s

L e a t h

e r I t e m

E l e c t r o

n i c I t e m

s

G

Cloths 40%

Grocery 40%

Gift Items 33%Electronic Items 25%

Leather Items 2%

Any Other Item 12%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 62/91

62

items and 25% is on electronic items. Brand preference on leather items is 2% and 12%

on any other item.

Interpretation: From this I interpret that some of the products brand are predecided

in advance and for some of the products customers don‟t at all predecide any brand. As

per electronic goods are concerned customers predecide the brand as many branded

electronic products are available in big bazaar. The customers predecides brands on

cloths and grocery most as big bazaar produces much of local brands and also have some

well known branded products of clothes with it like flying machine jeans.

Mode of payment of customers in big bazaar

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 63/91

63

Analysis: As per my study is concerned, out of the total respondents 73% of people

make cash payment in big bazaar. 21% of them uses credit card as their mode of payment

and 6% of the people makes payment in big bazaar through their debit card.

MODE OF PAYMENT

73%

21%

6%

Cash Payment

Credit Card

Debit Card

Cash Payment 73%

Credit Card 21%Debit Card 6%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 64/91

64

Interpretation: As per the obtained data I interpret that maximum number of

people makes cash payment in big bazaar. A fraction of people uses their credit card for

payment in big bazaar and a very few people uses their debit card for payment. I can

interpret that quick exchange of money for goods is done in big bazaar as most of the

people mode of payment is cash payment. Hence some times big bazaar has to wait for a

short time period as some of the customers make their payment through credit and debit

card.

Customers’ mode of transport to big bazaar

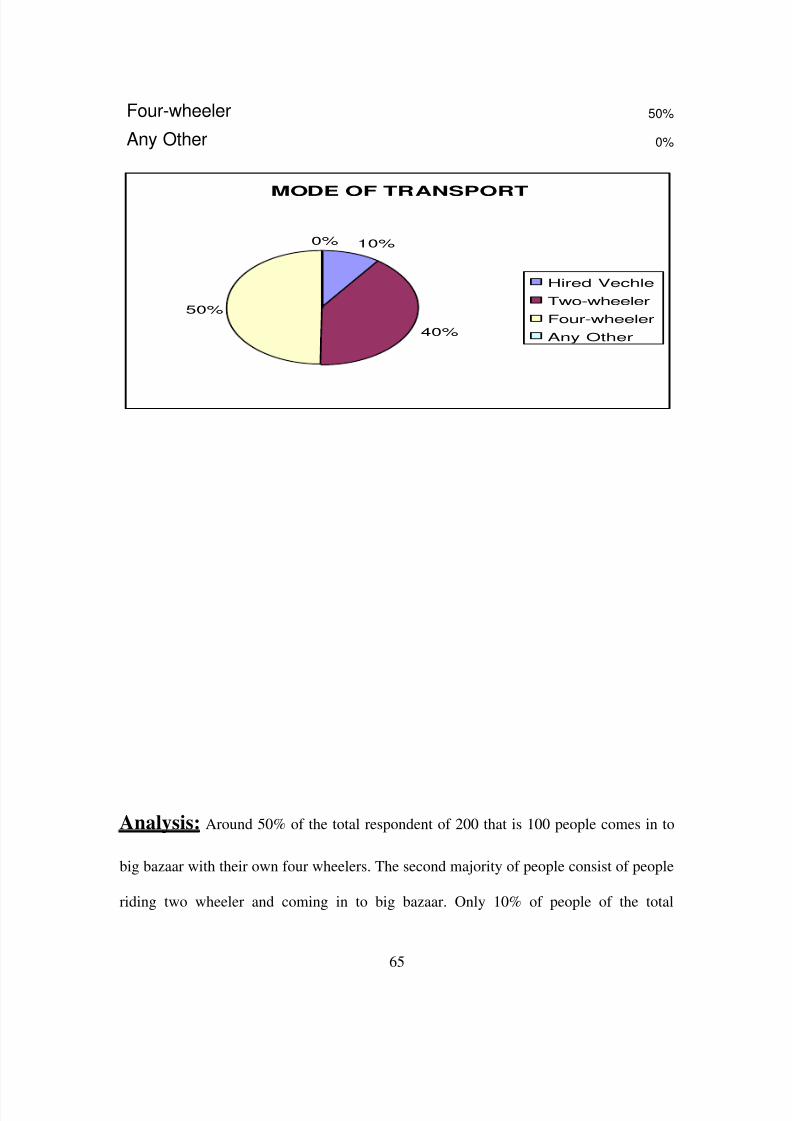

Hired Vehicle 10%

Two-wheeler 40%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 65/91

65

Four-wheeler 50%

Any Other 0%

Analysis: Around 50% of the total respondent of 200 that is 100 people comes in to

big bazaar with their own four wheelers. The second majority of people consist of people

riding two wheeler and coming in to big bazaar. Only 10% of people of the total

MODE OF TRANSPORT

10%

40%

50%

0%

Hired Vechle

Two-wheeler

Four-wheeler

Any Other

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 66/91

66

respondent visits big bazaar on hired vehicles. None of the customers of the total

respondent comes in any other mode of transport.

Interpretation: From the above data I interpret that there are more number of four

wheelers coming found in big bazaar than that of two wheelers. People prefer more to go

to big bazaar in four wheelers than that of two wheelers. A few people are found who

comes in to big bazaar with a hire vehicle. Probably they might be the tourists.

Parking space availability in big bazaar

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 67/91

67

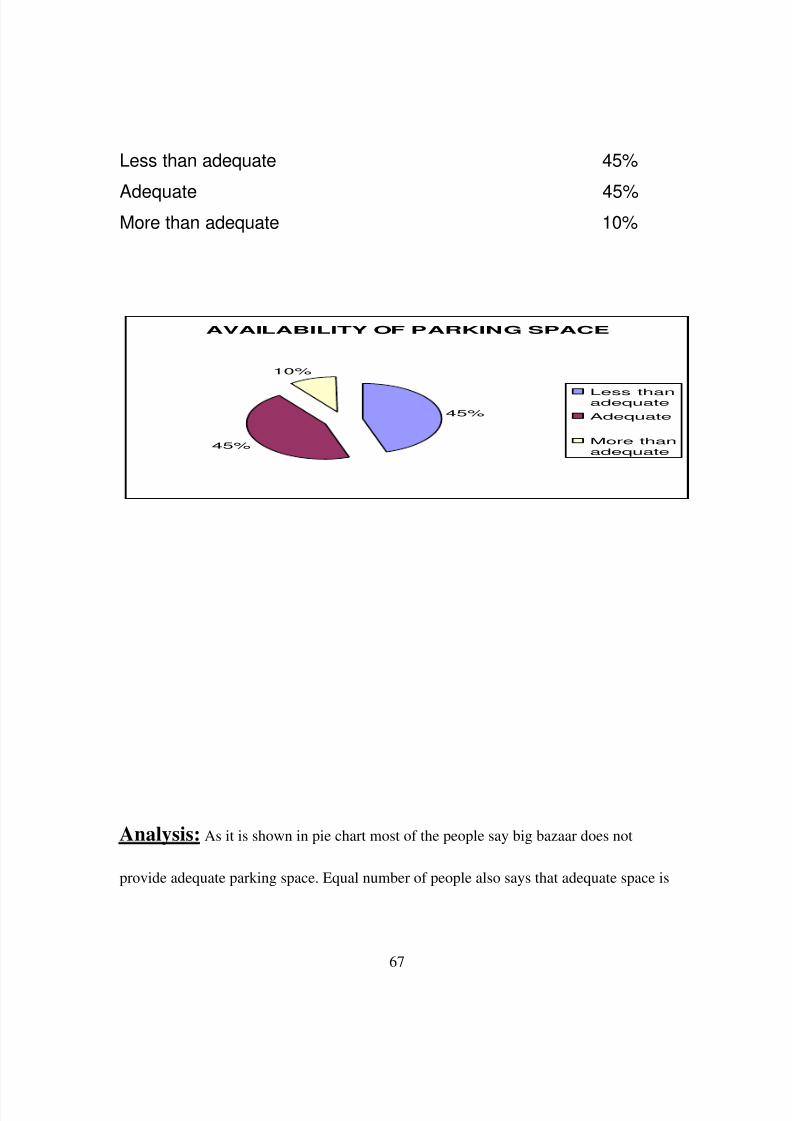

Analysis: As it is shown in pie chart most of the people say big bazaar does not

provide adequate parking space. Equal number of people also says that adequate space is

AVAILABILITY OF PARKING SPACE

45%

45%

10%

Less thanadequate

Adequate

More than

adequate

Less than adequate 45%

Adequate 45%More than adequate 10%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 68/91

68

provided for parking big bazaar. Only 10% of people say that more than adequate space

is available for parking in big bazaar.

Interpretation: Analyzing the above data, I interpret that customers are not

satisfied with the parking space availability provided by big bazaar. Hence it‟s a threat

for big bazaar as it may loose its customers because of less parking space availability.

Even though many customers say adequate space is available for parking in big bazaar

but also it is a threat for big bazaar as it is seen more number of people are expected to

come in to big bazaar. In holidays probably it will be very difficult for customers to park

their vehicle in big bazaar.

Customers preference towards Kirana store

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 69/91

69

Analysis: Out of my total respondent of 200 customers, 85% of them says they go to

their near by kirana store and 15% said that they don‟t at all go to any kirana store. This

PREFERENCE TOWARDS KIRANA

STORE

85%

15%

Yes

No

Yes 85%

No 15%

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 70/91

70

shows that majority of people go to kirana store even though they visit big bazaar. But

some customers are there who never goes to any kirana store.

Interpretation: As per the given data I analyze that most number of people tend to

purchase goods from near by kirana store even if they come to big bazaar. I can conclude

from this that a kirana store is a competitor of big bazaar. Some customers never go for

shopping in kirana store as of it does not have much variety option available with it.

Probably they are more interested in having a shopping experience rather than to just go

and purchase goods from kirana store.

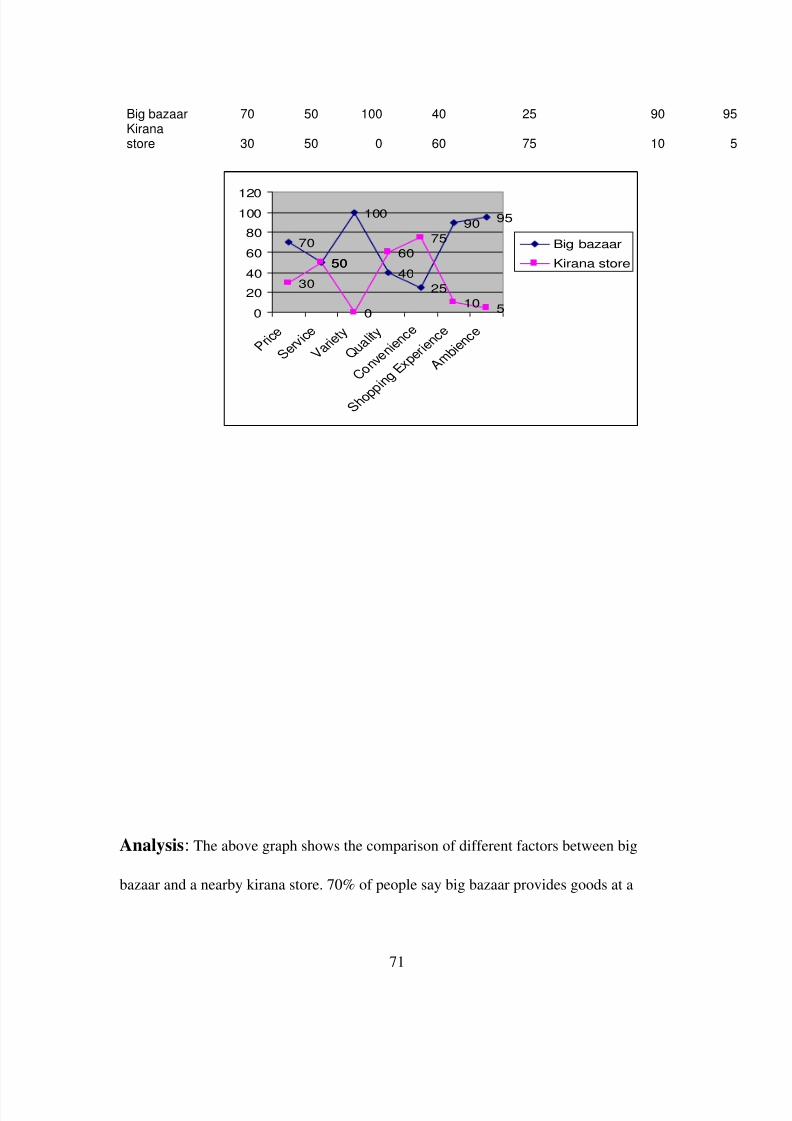

Comparison of Big bazaar with any Kirana store

Price Service Variety Quality ConvenienceShoppingExperience Ambience

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 71/91

71

Big bazaar 70 50 100 40 25 90 95Kiranastore 30 50 0 60 75 10 5

Analysis: The above graph shows the comparison of different factors between big

bazaar and a nearby kirana store. 70% of people say big bazaar provides goods at a

70

50

100

40

25

9095

30

50

0

60

75

10 50

20

40

60

80

100120

P r i c e

S e r v i c e

V a r i e t y

Q u a l i t y

C o n v e n i e n

c e

S h o p p

i n g E x p

e r i e n c e

A m b i e n c e

Big bazaar

Kirana store

8/2/2019 Intial Report

http://slidepdf.com/reader/full/intial-report 72/91

72

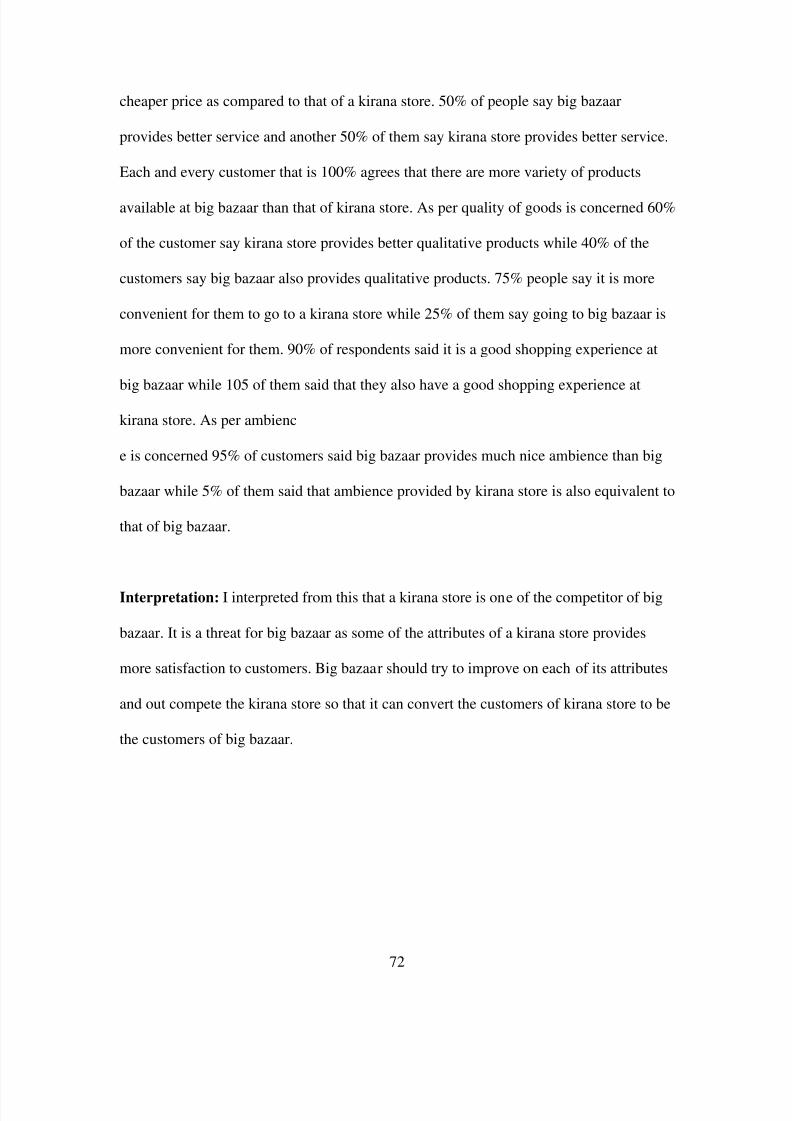

cheaper price as compared to that of a kirana store. 50% of people say big bazaar

provides better service and another 50% of them say kirana store provides better service.

Each and every customer that is 100% agrees that there are more variety of products