Languages

Pages

Legal

Kajaria Ceramics Limited (KCL) is the largest manufacturers of ceramic/vitrified tiles in India and has carved out distinct brand equity in the same. It has a capacity of 30.60 mn sq meter (MSM) (across 3 plants ‐ Sikandrabad in Uttar Pradesh, Gailpur in Rajasthan and Morbi in Gujarat). It has increased its capacity from 1 MSM to 30.60 MSM in last 22 years and offers more than 400 options in ceramic wall & floor tiles, vitrified tiles, designer tiles and much more. Robust demand in domestic tile market The Indian ceramic tiles industry is the world’s largest producer as well as consumer after China and Brazil. The 550 MSM domestic ceramic tile industry was estimated to be worth Rs.130 bn as on March, 2011, growing at a CAGR of ~15%. India’s per capita tiles consumption is a mere 0.42 sq. m while the world average is three times higher at 1.20 sq. m and China’s average is more than five times higher at 2.26 sq. m. Demand for tiles is expected to grow rapidly because of the following reasons: ‐ (1) Increasing middle‐class & rising population, (2) Improved disposable incomes and (3) Growth of replacement market in rural and semi‐urban markets. KCL is the 2nd largest tile company (turnover wise) with around 15% share in the organized market and is very well placed to benefit from the strong growth being witnessed in the tiles industry. Capacity expansions to ensure strong growth in volumes Kajaria has recently expanded its capacity to 30.6 MSM, led by a 6 MSM brownfield expansion (March 2011) at Gailpur to manufacture vitrified tiles (glazed and polished) & a 2.60 MSM vitrified capacity (conversion from ceramic tiles) at Sikandrabad (commenced operations in March 2011). In the last 15 months, KCL added 11 MSM of vitrified tiles capacity, the largest by any single company in India. Given its market positioning, demand growth & high capacity utilization, KCL’s volumes are expected to expand substantially following these expansions. Focus on value added products, strong Brand & distribution network to drive growth In India, the branded tiles segment is gaining market share owing to rapid capacity addition and shift to value‐added products, which explains the 20% growth of the top 10 players as against the industry average of 15%. KCL has one of the largest distribution channels in India with 800 dealers (apart from their network of sub‐dealers) that help in better market penetration. To leverage their strong distribution network and brand competencies, apart from adding capacities in the high end vitrified tiles category, KCL has also forayed into many high‐end sanitaryware segments which positions the company as a complete bathroom solution provider and has also established a foothold in high‐value wooden flooring solutions. This will help KCL to accelerate its market share in the high‐end segment, grow its volume strongly and will also enable it to address newer segments, where it was previously absent. Reducing Leverage & Sharp Improvement in ROCE & ROE Historically, the Indian tile companies have had a low asset turnover ratio, as the cost of machinery was very high. However, with the foray of Chinese companies into machine manufacturing in the recent past, the prices of Italian machines have also come down substantially. Apart from this, KCL’s focus higher end products, has helped it improve realizations. These factors have turned out to be game changers for the company as it has been able to improve margins, reduce leverage and report better ROCE/ROE. The ROCE and ROE for FY11 has improved to 24.9% & 29.5% respectively from 18.9% & 20.4% respectively in FY10.

OUTLOOK & VALUATION KCL has performed exceedingly well in the past few years on the back of rising tiles demand, its strong brand & distribution network, focus on value added products & consistent expansion in its capacities. Given its strong market positioning, increased capacities of its vitrified tiles, foray into new product lines of high end sanitaryware & wooden flooring segments, we expect KCL to deliver strong growth over the coming years. Going forward, we expect its Revenues and APAT to grow strongly by 23% & 21% in FY12 & 17.5% and 20.3% in FY13 respectively. We initiate our coverage on the Company with a “HOLD” rating and a target price of Rs.120 (10x FY13E EPS of Rs.12).

KEY FINANCIALS Y/E March

Revenue(Rsmn)

APAT(Rsmn)

APAT (% Ch.)

AEPS (Rs.)

P/E (x)

ROCE (%)

ROE (%)

P/BV(x)

FY10 7363.5 358.5 302.7 4.9 21.8 18.9 20.4 4.1 FY11 9534.2 606.6 69.2 8.2 12.9 24.9 29.5 3.5 FY12E 11725.4 733.5 20.9 10.0 10.6 28.4 29.3 2.8 FY13E 13776.6 882.6 20.3 12.0 8.8 32.5 28.1 2.2

Please refer to important disclosures at the end of the report For private Circulation Only.

Sushil Financial Services Private Limited Member : BSEL, SEBI Regn.No. INB/F010982338 | NSEIL, SEBI Regn.No.INB/F230607435. Regd.Office : 12, Homji Street, Fort, Mumbai 400 001. Phone: +91 22 40936000 Fax: +91 22 22665758 Email : [email protected]

October 07, 2011 HOLD MEDIUM RISK PRICE Rs.106 TARGET Rs.120

Initiating Coverage

Kajaria Ceramics Limited

CONSUMER

SHARE HOLDING (%)

Promoters 51.33 FII 5.53 FI 9.22 Body Corporates 12.75 Public & Others 21.17

STOCK DATA

Reuters Code Bloomberg Code

KAJR.BO KJC IN

BSE Code NSE Symbol

500233 KAJARIACER

Market Capitalization*

Rs.7802 mn US $ 156 mn

Shares Outstanding* 73.6 mn

52 Weeks (H/L) Rs.121 / 61

Avg. Daily Volume (6m)

131,724 Shares

Price Performance (%) 1M 3M 6M 2 8 38

200 Days EMA: Rs.91

*On fully diluted equity shares

Part of Bonanza

ANALYST Bhavika Shah | +91 22 4093 5054 [email protected]

SALES: Devang Shah | +91 22 4093 6060/61 [email protected]

October 07, 2011 2

Kajaria Ceramics Ltd.

COMPANY OVERVIEW Kajaria Ceramics Ltd. (KCL) is the largest manufacturers of ceramic/vitrified tiles in India. It has an annual capacity of 30.60 MSM, distributed across three plants‐Sikandrabad in Uttar Pradesh, Gailpur in Rajasthan and Morbi in Gujarat. Kajaria Ceramics has increased its capacity from 1 MSM to 30.60 MSM in last 22 years and offers more than 400 options in ceramic wall & floor tiles, vitrified tiles, designer tiles and much more. These tiles come in a wide range of colours and textures to complement bathrooms, living rooms, corridors, study rooms & kitchen, born out of an inspired creativity of those who feel that rooms should be an extension of the beauty reflected. With an unparalleled commitment towards quality, KCL has strived to adopt technologies and standards with the changing times.

.

BUSINESS OVERVIEW

CERAMIC WALL & FLOOR TILES KCL manufactures wall and floor tiles in diverse sizes, designs and finishes to cater to all segments of customers. The Company also provides decorative additions like High‐lighters and borders along with matching floors leading to comprehensive bathroom solutions. Its products are marketed through a robust distribution network of dealers and sub‐dealers and Kajaria Prima showrooms present in every major town of the country. At Kajaria, wall tiles are manufactured at its Gailpur facility (capacity 14.10 MSM) in six different sizes (20x20 cm, 25x40 cm, 30x20 cm, 30x45 cm, 30x 60 cm and 15x60 cm). Floor tiles are manufactured at the Sikandrabad facility (capacity 3.2 MSM) in the 30x 30 cm size and at its recently acquired Morbi unit (capacity 2.30 MSM) in the 60x60 cm size. Some wall (45x90 cm) and floor tiles (39.5 x 39.5 cm) are outsourced. Kajaria developed unique designs in digitally printed tiles in multiple sizes for exterior wall cladding and interior applications. Going ahead, the Company will continue to develop new sizes and designs in value added, large‐format tiles in line with customer aspirations

POLISHED VITRIFIED TILES Polished vitrified tiles are considered ‘next generation flooring’ marked by a polished surface, high gloss, extraordinary quality and durability. They are designed to withstand abrasion, chemical and fire resistance and staining. KCL enjoys a seven‐year presence in this business, marketing imported variants from China in three different sizes – 60x60 cm, 80x80 cm, 120x60 cm. KCL commissioned a 2.4 MSM polished vitrified tiles (60x60 cm) facility at its Sikandrabad unit which commenced operations in February 2010, its first vitrified tile manufacturing facility. During 2010‐11, the Company converted part of ceramic floor tile capacity into a vitrified tile capacity by adding balancing equipment and another 2.60 MSM of capacity, making the total polished vitrified capacity 5 MSM at Sikandrabad by March 2011. The Company further added 3 MSM high‐end polished vitrified tile capacity in Gailpur which commenced production in March, 2011. Kajaria

Kajaria Ceramics Ltd. (KCL)

Ceramic Wall & Floor Tiles

Polished Vitrified Tiles

Glazed Vitrifies Tiles

Retail Chain of Imported Tiles Bathware Wooden

Flooring

October 07, 2011 3

Kajaria Ceramics Ltd.

launched the Solitare series comprising technologically‐advanced, large‐format tiles (80x80 cm and 120x60 cm), providing Indian customers an authentic alternative to natural/Italian marble. These products are manufactured by superwhite, translucent and expensive colour bodies fused with integrative feeding of dye and pressing. The Company markets polished vitrified tiles through dealer and ‘Kajaria Vitro Studio’ network, a shop‐in‐shop concept for select high performing dealers providing dedicated space to showcase Kajaria’s products, facilitating customer engagement and off take. Kajaria will optimise capacity utilisation of its newly commissioned capacities at the Gailpur and Sikandrabad plants. The marketing team strategised to increase the proportion of high‐end tiles in the sales volume by expanding distribution network to establish presence in every district in India and introducing new product variants and contemporary designs by way of own production and import.

GLAZED VITRIFIED TILES KCL was the first company to introduce glazed vitrified tiles (GVT) in India in 2007‐08 in an organized manner under the Kajaria Eternity brand. The Company sourced products from the two leading GVT manufacturers in China. Currently, the Company is the largest importer of GVT providing the widest product offering: in terms of sizes (30x60 cm and 60x60 cm) and finishes (rustic, matt, satin, wood, stone, silk and metal, among others) for wall and floor applications. The Company commissioned a 3 MSM capacity to produce glazed vitrified tiles (60x60 cm, 30x60 cm and 45x90 cm) at its Gailpur unit which commenced commercial operations in March 2011. The products are distributed through Kajaria Eternity Studios and select dealers. The Kajaria Eternity Studios represent a shop‐in‐shop concept for select dealers in key cities – showrooms are upgraded, product visibility is enhanced and additional sales promotion schemes are offered – leading to a win‐win situation. Improved lifestyle consequent to increasing aspirations and disposable incomes is driving the demand for glazed vitrified tiles, which provide a superior‐value proposition over natural stone. The Company’s manufacturing facility will minimise import of glazed vitrified tiles (about 10% of sales volumes) and yield benefits through a reduction in product price, consistent supply of quality material and customised solutions. Consequently, the team will grow its market share (volume and value) and enter uncharted territories. The Company plans to introduce digital printing on glazed vitrified tiles and open more studios in 2011‐12 to strengthen market share.

RETAIL CHAIN ‐ KAJARIA WORLD Kajaria World showcases high‐end imported tiles sourced through its alliances with European brands (Saloni, Grespania, Argenta and Baldocer, among others) through a network of twelve showrooms across the country. The brand signifies international style & appeal and is popular in India’s architect fraternity. This chain offers the widest range of imported tiles including the large format tiles collection (45x90 cm and 30x90 cm series) and the stone collection series (i.e. exterior tile). Tiles are also available in 30x60 cm sizes with different finishes like rustic, matt, satin, wood, metal and fabric, among others. The price range varies from Rs.1,000‐ 3,000 per sq. m. The Company imports tiles produced with the latest digital printing technology, wherein the design of each tile is different and following commissioning, the cladding resembles natural stone. The Company possesses the largest logistic support for imported tiles; its 14 warehouses ensure seamless product supply across its network. The Company is looking to extend the Kajaria World network to all Tier I cities and implement new initiatives to accelerate retail sales.

October 07, 2011 4

Kajaria Ceramics Ltd.

BATHWARE KCL entered the bathware segment to emerge as a one‐stop solution provider. The business showcases bathware and wellness products (bath tubs, Jacuzzi, shower cubicles). KCL tied up with VitrA, a leading European brand, in January 2011 to market high‐end bathware and bath fittings. VitrA is a part of Eczacibasi, one of the largest industrial groups in Turkey, with a turnover of Rs.100 bn. The arrangement will position Kajaria as an exclusive and sole marketer and distributor of the VitrA range in India. The alliance will leverage the strong brand and distribution network of Kajaria. Kajaria and VitrA inaugurated the first showroom (3,000‐sq. ft.) of VitrA products showroom in Gurgaon. VitrA products will also be showcased in all Kajaria World showrooms across India. The real returns from the tie‐up are expected in 2011‐12 after the Company opens 10 VitrA‐Kajaria showrooms and appoints 30 exclusive dealers across India.

WOODEN FLOORING Kajaria entered the wooden flooring space as a trading initiative in November 2010, representing a neat fit with its existing businesses for the following reasons:

Western culture is being replicated across Indian households faster than before. The average age of the urban house purchaser is declining (from about 37‐39 years

to about 28‐30 years) with a corresponding increase in their receptivity to lifestyle products.

The target buyer group (builder/architect in urban locations) is largely the same as ceramic and vitrified tiles.

The new product helps fill dealer shelf‐space, enhancing opportunity and returns. The Company procures the product from quality‐respecting Chinese suppliers and markets it under the Kajaria Wood brand, supported by regional marketing teams and incentivized dealer off take. The Company is strengthening pan‐India product visibility through focused marketing, new product variants and distribution network addition and also exploring the possibility of importing value added products from reputed European companies.

October 07, 2011 5

Kajaria Ceramics Ltd.

INVESTMENT RATIONALE Robust demand in domestic tile market The Indian ceramic tiles industry is the world’s third largest producer as well as consumer after China and Brazil. The industry grew 15% annually over the last few years (outpacing global average growth of 6% per annum) owing to the emergence of tiles as a durable, cost‐effective and convenient flooring solution over natural stone. Increasing disposable incomes, affordability, urbanization, brand aspiration and home aesthetics also catalyzed the demand for high‐end variants. The 550‐MSM domestic ceramic tile industry was estimated at around Rs.130 bn. The Indian ceramic industry is equally divided into the branded and unbranded segments. The unbranded segment comprises small players concentrated in Gujarat. KCL is the largest player in the Indian space in terms of installed capacity. The branded segment is gaining market share owing to rapid capacity addition and shift to value‐added products, which explains the 20% growth of the top 10 players as against the industry average of 10%, correspondingly increasing market share from 32% in 2005‐06 to about 40% in 2010‐11. Per capita consumption: India’s per capita tiles consumption is a mere 0.42 sq. m while the world average is three times higher at 1.20 sq. m and China’s average is more than five times higher at 2.26 sq. m.

Source: ‐ Ceramic World Review

Kajaria Ceramics is the second largest company turn‐over wise with around 15% share in the organized market.

2.26

3.24

4.47

2.76

1.79 1.67

0.42

0

1

2

3

4

5

China Brazil Iran Vietnam Turkey Egypt India

Per Capita Consumption of Tiles (MSM)

October 07, 2011 6

Kajaria Ceramics Ltd.

Growth in real estate sector to trigger demand: Across 2010‐15, India’s real estate sector is expected to grow at a CAGR of 15‐16. Demand for tiles is also expected to rise in tandem. 70% of the tiles distributed by Kajaria cater to the retail segment (against industry average of 50%), thus providing better returns. The retail demand for tiles is likely to grow because of the following triggers:

Increasing middle‐class & rising population: India’s middle‐class is expected to account for 85% of urban households. India’s urban population is expected to increase by 100 million over 10 years or 10 million annually, creating a huge annual demand for houses and flooring solutions. India is projected to stay the youngest with its working‐age population estimated to grow to 70% of its total population by 2030 – the largest such quantum in the world.

Improved disposable incomes: with the improvement in disposable incomes discretionary spending in lifestyle and premium products is expected to increase to around 70% of annual household expenses by 2025.

Replacement market:‐ Growing earnings in rural and semi‐urban markets due to government policies (MGNREGS and higher price fixation for agri‐commodities) have fuelled aspirations, manifested in improved flooring solutions.

The growth from institutional and projects segment is expected to come from urbanization leading to increase in commercial space. Demand for commercial space is expected to come from sectors such as organized retail, hospitality sector, healthcare care and other infrastructure development activities like airport development.

H&R Johnson

Kajaria Ceramics

Somany Ceramics

Nitco Tiles

Asian Granito

Orient Ceramics

Euro Ceramics

Gokul Ceramics

Bell Ceramics

Regency Ceramics

Murudeshwar Ceramics

Bell Granito

Decolight Ceramics Others

ORGANISED TILE MARKET TURNOVER

October 07, 2011 7

Kajaria Ceramics Ltd.

Capacity expansion will drive volume growth KCL commissioned a 2.4 MSM polished vitrified tiles facility at its Sikandrabad unit which commenced operations in February 2010, its first vitrified tile manufacturing facility. During 2010‐11, the Company converted part of ceramic floor tile capacity into a vitrified tile capacity by adding balancing equipment and another 2.60 MSM of capacity, making the total polished vitrified capacity 5 MSM at Sikandrabad by March 2011. The Company further added 3 MSM high‐end polished vitrified tile capacity in Gailpur which commenced production in March, 2011.

Ceramic glazed tiles v/s vitrified tiles

Ceramic glazed tiles Vitrified tiles

Nature

Glazed and burned clay products principally used for decorative and sanitary effects on walls and floors; has 3‐6% water absorption.

Specialized kind, hard‐backed with low porosity and water absorption (less than 0.5%), making it stain‐resistant and strong.

Composition

Decorative coat on the top of the tile body, hence their composition is non‐consistent.

Homogeneous body and consistent in Composition.

Application

Mainly used in wall coverings for bathrooms and kitchens.

Used for all types of flooring.

Price range Rs.200‐700 per sq. m Rs.400‐1,500 per sq. m.

In 14 months (February 2010 to March 2011), KCL added 11 MSM of vitrified tile capacity, the largest by any single company in India. KCL also acquired a 51% stake in Soriso Ceramic Pvt Ltd, having a 2.30 MSM per annum ceramic floor tile manufacturing facility in Gujarat in February 2011 for an investment of Rs.56.20 mn. Now the total capacity is 30.6MSM. For its future growth requirements, the company plans to have a judicious mix of imports, outsourcing and own capacities, and has already planned to double the manufacturing capacity at its Morbi Plant, Gujarat (from 2.3MSM to 4.6 MSM) by January, 2012. Given its market positioning, demand growth & high capacity utilization, KCL’s volumes are expected to expand substantially following these expansions.

Plant Ceramic Tiles (MSM) Vitrified Tiles (MSM) Total (MSM)

Sikandrabad (UP) 3.2 5.0 8.2

Gailpur (Rajasthan) 14.1 6.0 20.1

Morbi (Gujarat)* 2.3 0.0 2.3

19.6 11.0 30.6 * KCL acquired 51% stake in Soriso Ceramic Pvt. Ltd. in Morbi, Gujarat.

October 07, 2011 8

Kajaria Ceramics Ltd.

Focus on value added products, strong Brand & distribution network to drive growth further In India, the branded tiles segment is gaining market share owing to rapid capacity addition and shift to value‐added products, which explains the 20% growth of the top 10 players as against the industry average of 15%. KCL has one of the largest distribution channels in India with 800 dealers (apart from their network of sub‐dealers) that help in better market penetration. To leverage their strong distribution network and brand competencies, apart from adding capacities in the high end vitrified tiles category, KCL has also forayed into many high‐end sanitaryware segments which positions the company as a complete bathroom solution provider and has also established a foothold in high‐value wooden flooring solutions. This business showcases bathware and wellness products (bath tubs, Jacuzzi, shower cubicles). KCL has also tied up with VitrA, a leading European brand, in January 2011 to market high‐end bathware and bath fittings. VitrA is a part of Eczacibasi, one of the largest industrial groups in Turkey, with a turnover of Rs.100 bn. The arrangement will position Kajaria as an exclusive and sole marketer and distributor of the VitrA range in India. The alliance will leverage the strong brand and distribution network of Kajaria. Kajaria and VitrA inaugurated the first showroom (3,000‐sq. ft.) of VitrA products in Gurgaon. VitrA products will also be showcased in all Kajaria World showrooms across India. This will help KCL to accelerate its market share in the high‐end segment, grow its volume strongly and will also enable it to address newer segments, where it was previously absent.

Reducing Leverage & Sharp Improvement in ROCE & ROE Historically, the Indian tile companies have had a low asset turnover ratio, as the cost of machinery was very high. However, with the foray of Chinese companies into machine manufacturing in the recent past, the prices of Italian machines have also come down substantially. Apart from this, KCL’s focus higher end products, has helped it improve realizations. These factors have turned out to be game changers for the company as it has been able to improve margins, reduce leverage and report better ROCE/ROE. The ROCE and ROE for FY11 has improved to 24.9% & 29.5% from 18.9% & 20.4% respectively in FY10.

RISKS & CONCERNS Low‐cost Chinese imports could affect market share: ‐ The Indian government has imposed anti‐dumping duty on Chinese ceramic tiles coming into India. Withdrawal of this anti dumping duty is likely to impact the industry as well as Kajaria, due to higher imports. Competition from the unbranded sector could dent profitability: ‐ The ceramic industry is governed by unorganized sector, which competes with organized sector on the pricing front. Low price realizations impose a major threat on ceramic and vitrified tile prices. This competitive pressure can result in the shrinkage of market share, thereby impacting revenue and earnings growth. Slowdown in the housing & infrastructure sector: ‐ Tile industry growth is largely dependent on overall economic, housing and infrastructure growth. The revival in construction sector has been the single largest factor for growth in demand. Any slowdown in the buying, projects or economy may impact the sales volume.

October 07, 2011 9

Kajaria Ceramics Ltd.

FINANCIAL OUTLOOK Sales to grow at CAGR of 20% over FY11‐FY13 KCL’s net sales have grown at a 21% CAGR of the past three years (FY07‐FY10). The Company is well‐positioned to encash the market growth opportunities as it enjoys higher brand equity. We expect its sales to grow at a CAGR of 20% over FY11‐FY13.

Source: Company & Sushil Finance Research estimates

EBITDA to grow at a CAGR of 20% over FY11‐13

Source: Company & Sushil Finance Research estimates

5027

66497355

9523

11714

13764

0

2000

4000

6000

8000

10000

12000

14000

16000

FY08 FY09 FY10 FY11 FY12 FY13

SALES (Rs. in mn)

824959

1157

1485

1828

2151

13.0

13.5

14.0

14.5

15.0

15.5

16.0

16.5

17.0

0

500

1000

1500

2000

2500

FY08 FY09 FY10 FY11 FY12 FY13

EBIDTA (Rs. In mn) EBIDTA (Margins)

EBIDTA & EBIDTA Margins

October 07, 2011 10

Kajaria Ceramics Ltd.

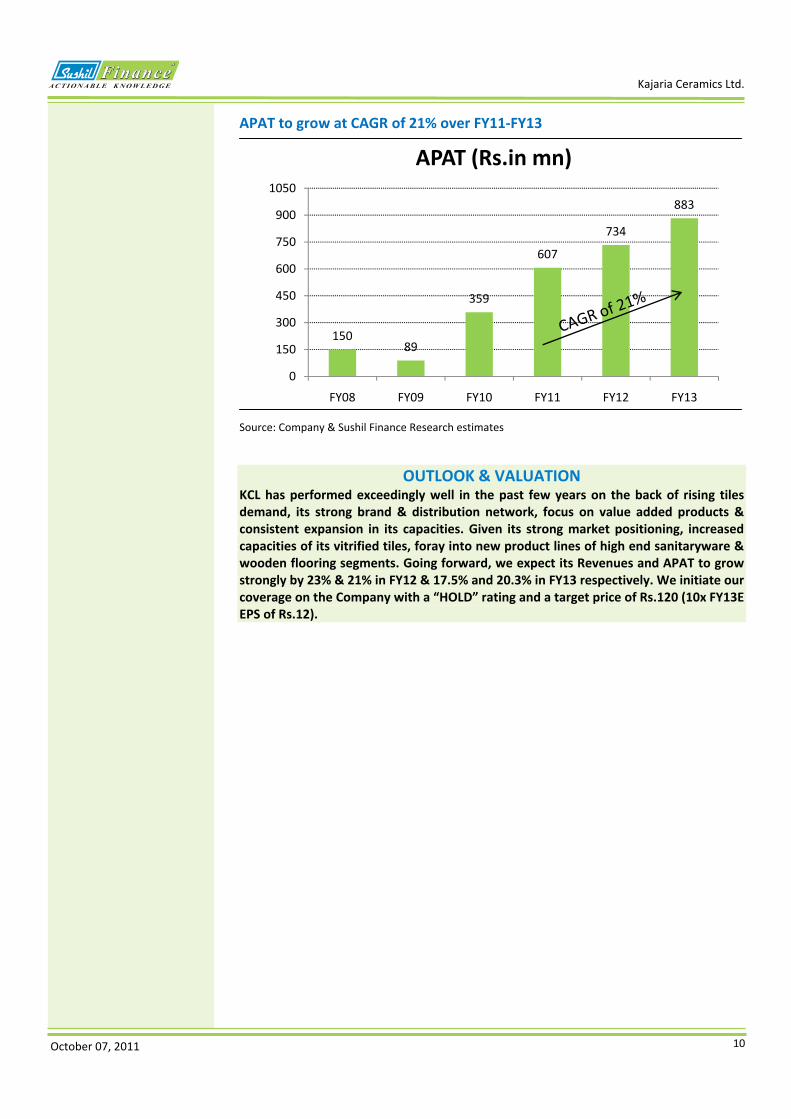

APAT to grow at CAGR of 21% over FY11‐FY13

Source: Company & Sushil Finance Research estimates

OUTLOOK & VALUATION KCL has performed exceedingly well in the past few years on the back of rising tiles demand, its strong brand & distribution network, focus on value added products & consistent expansion in its capacities. Given its strong market positioning, increased capacities of its vitrified tiles, foray into new product lines of high end sanitaryware & wooden flooring segments. Going forward, we expect its Revenues and APAT to grow strongly by 23% & 21% in FY12 & 17.5% and 20.3% in FY13 respectively. We initiate our coverage on the Company with a “HOLD” rating and a target price of Rs.120 (10x FY13E EPS of Rs.12).

15089

359

607

734

883

0

150

300

450

600

750

900

1050

FY08 FY09 FY10 FY11 FY12 FY13

APAT (Rs.in mn)

October 07, 2011 11

Kajaria Ceramics Ltd.

PROFIT & LOSS STATEMENT Rs.mn

Y/E March FY10 FY11 FY12E FY13E

Total Sales 7363.5 9534.2 11725.4 13776.6

Total Raw Mat. Cost 3600.2 5398.9 6715.6 7994.7

Power & Fuel Cost 1048.8 926.6 1153.6 1320.9

Staff Cost 612.8 758.1 985.5 1162.9

Other Expenditure 945.0 965.3 1042.6 1146.8

EBITDA 1156.7 1485.3 1828.1 2151.3

Interest 375.2 298.6 380.7 382.6

Depreciation 267.1 295.0 368.7 431.4

Other Income 0.0 0.0 0.0 0.0

PBT incl OI 514.4 891.7 1078.7 1337.3

Tax 155.9 285.1 345.2 454.7

APAT 358.5 606.6 733.5 882.6

BALANCE SHEET STATEMENT Rs.mn

As on 31stMarch FY10 FY11 FY12E FY13E

Share Capital 147.2 147.2 147.2 147.2Reserves 1746.2 2078.5 2639.8 3350.2Shareholders Funds 1893.4 2225.6 2786.9 3497.3Total Debt 2628.3 2796.8 2452.2 1849.1Def. Tax Liability (Net) 548.5 601.9 617.0 647.8Total Liabilities 5070.2 5624.3 5856.1 5994.3Fixed Assets 3473.3 4791.0 4746.7 4715.2Investments 33.9 90.1 90.1 90.1

Sundry Debtors 773.2 909.0 1118.1 1313.8 Cash and Bank 44.9 29.9 142.0 158.1Loans and Adv. 755.8 808.4 994.4 1168.4 Inventory 1402.6 1515.1 1863.6 2189.7Other Current Assets 0.0 0.0 0.0 0.0Current Assets 2976.4 3262.5 4118.1 4829.9 Current Liabilities 1197.7 2129.9 2619.8 3078.2 Provisions 215.8 389.4 479.0 562.8Current Liabilities 1413.5 2519.3 3098.8 3641.0Net Current Assets 1562.9 743.2 1019.3 1188.9Total Assets 5070.2 5624.3 5856.1 5994.3

CASH FLOW STATEMENT Rs. mn

Y/E March FY10 FY11 FY12E FY13E

RPAT 272.7 435.6 561.3 710.4

Depreciation 249.2 221.9 368.7 431.4

Chg in Deferred tax 14.0 53.4 15.0 30.8

Chg in Working cap 499.5 804.8 (164.1) (153.5)Cash flow from operations 1035.4 1515.7 781.0 1019.2

Chg in Gross PPE (446.0) (1539.6) (324.4) (400.0)

Chg in Investments 0.0 (56.2) 0.0 0.0 Cash flow from investing (446.0) (1595.8) (324.4) (400.0)

Chg in debt (623.4) 168.5 (344.6) (603.0)

Chg in Net Worth 85.8 67.7 172.2 172.2

Dividend (85.8) (171.0) (172.2) (172.2)Cash flow from financing (623.4) 65.2 (344.6) (603.0)

Chg in cash (34.0) (15.0) 112.1 16.1

Cash at start 78.9 44.9 29.9 142.0

Cash at end 44.9 29.9 142.0 158.1

FINANCIAL RATIO STATEMENT Y/E March FY10 FY11 FY12E FY13E

Growth (%) Net Sales 10.6 29.5 23.0 17.5APAT 302.7 69.2 20.9 20.3EBITDA 20.6 28.4 23.1 17.7Profitability (%) EBITDA Margin 15.7 15.6 15.6 15.6Adj. PAT Margin 4.9 6.4 6.3 6.4ROCE 18.9 24.9 28.4 32.5ROE 20.4 29.5 29.3 28.1Per Share Data (Rs.) Adj. EPS 4.9 8.2 10.0 12.0Adj. CEPS 8.7 13.0 15.9 19.2BVPS 25.7 30.2 37.9 47.5Valuations (X) PER 21.8 12.9 10.6 8.8PEG 0.1 0.2 0.5 0.4P/BV 4.1 3.5 2.8 2.2EV / EBITDA 9.0 7.1 5.6 4.5EV / Net sales 1.4 1.1 0.9 0.7Turnover Days Debtors days 36 32 32 32Creditors days 80 96 110 112Gearing Ratio Total Debt to Equity 1.4 1.3 0.9 0.5

Source : Company, Sushil Finance Research Estimates

October 07, 2011 12

Kajaria Ceramics Ltd.

Rating Scale This is a guide to the rating system used by our Institutional Research Team. Our rating system comprises of six rating categories, with a corresponding risk rating.

Risk Rating

Risk Description Predictability of Earnings / Dividends; Price VolatilityLow Risk High predictability / Low volatility

Medium Risk Moderate predictability / volatility

High Risk Low predictability / High volatility

Total Expected Return Matrix

Rating Low Risk Medium Risk High RiskBuy Over 15 % Over 20% Over 25%

Accumulate 10 % to 15 % 15% to 20% 20% to 25%

Hold 0% to 10 % 0% to 15% 0% to 20%

Sell Negative Returns Negative Returns Negative Returns

Neutral Not Applicable Not Applicable Not Applicable

Not Rated Not Applicable Not Applicable Not Applicable

Please Note

Recommendations with “Neutral” Rating imply reversal of our earlier opinion (i.e. Book Profits / Losses).

** Indicates that the stock is illiquid With a view to combat the higher acquisition cost for illiquid stocks, we have enhanced our return criteria for such stocks by five percentage points.

Stock Review Reports: These are Soft coverage’s on companies where Management access is difficult or Market capitalization is below Rs. 2000 mn. Views and recommendation on such companies may not necessarily be based on management meeting but may be based on the publicly available information and/or attending Company AGMs. Hence Stock Reviews may be just one‐time coverage’s with an occasional Update, wherever possible.

Additional information with respect to any securities referred to herein will be available upon request. This report is prepared for the exclusive use of Sushil Group clients only and should not be reproduced, re‐circulated, published in any media, website or otherwise, in any form or manner, in part or as a whole, without the express consent in writing of Sushil Financial Services Private Limited. Any unauthorized use, disclosure or public dissemination of information contained herein is prohibited. This report is to be used only by the original recipient to whom it is sent.

This is for private circulation only and the said document does not constitute an offer to buy or sell any securities mentioned herein. While utmost care has been taken in preparing the above, we claim no responsibility for its accuracy. We shall not be liable for any direct or indirect losses arising from the use thereof and the investors are requested to use the information contained herein at their own risk.

This report has been prepared for information purposes only and is not a solicitation, or an offer, to buy or sell any security. It does not purport to be a complete description of the securities, markets or developments referred to in the material. The information, on which the report is based, has been obtained from sources, which we believe to be reliable, but we have not independently verified such information and we do not guarantee that it is accurate or complete. All expressions of opinion are subject to change without notice.

Sushil Financial Services Private Limited and its connected companies, and their respective directors, officers and employees (to be collectively known as SFSPL), may, from time to time, have a long or short position in the securities mentioned and may sell or buy such securities. SFSPL may act upon or make use of information contained herein prior to the publication thereof.

Top Related