Languages

Pages

Legal

Paul PangPaul PangManaging DirectorManaging Director

CMAI ChinaCMAI China

Global Petrochemical Industry Outlook

Global Petrochemical Industry Outlook

2011 Presentation to CSPC2011 Presentation to CSPCSingaporeSingapore ShanghaiShanghai HoustonHouston New YorkNew York LondonLondon DüsseldorfDüsseldorf DubaiDubai

May 17, 2011May 17, 2011Tianjin, ChinaTianjin, China

BangkokBangkok

Presentation OutlinePresentation OutlinePresentation OutlinePresentation Outline

EconomyEconomy

EnergyEnergy

2011 Presentation to CSPC2011 Presentation to CSPC

PetrochemicalPetrochemical

5959

6161

6363Trillions of 2007 Trillions of 2007 U.S. DollarsU.S. Dollars

Global GDP Through 2016Global GDP Through 2016Global GDP Through 2016Global GDP Through 2016

2011 Presentation to CSPC2011 Presentation to CSPC

5353

5555

5757

0606 0707 0808 0909 1010 1111 1212

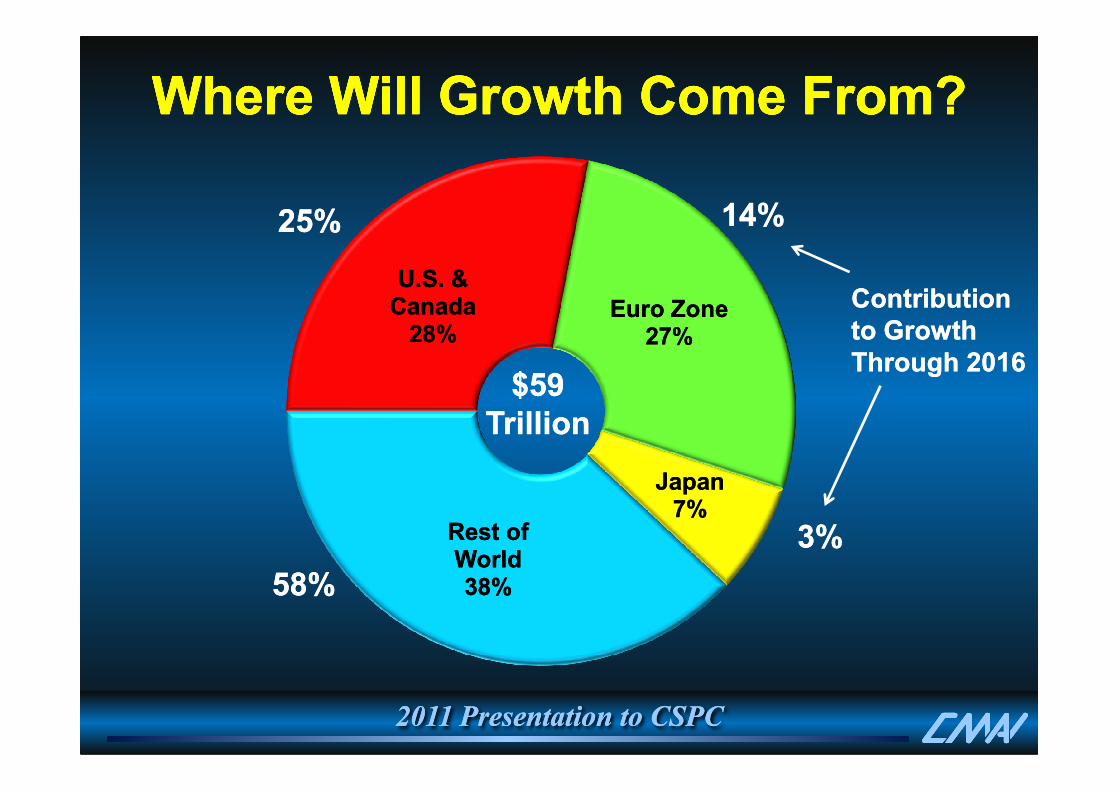

Where Will Growth Come From?Where Will Growth Come From?Where Will Growth Come From?Where Will Growth Come From?

U.S. & U.S. & CanadaCanada

28%28%Euro ZoneEuro Zone

27%27%

Contribution Contribution to Growth to Growth Through 2016Through 2016

25%25% 14%14%

$59$59

2011 Presentation to CSPC2011 Presentation to CSPC

JapanJapan7%7%

Rest of Rest of WorldWorld38%38%

3%3%

58%58%

$59$59TrillionTrillion

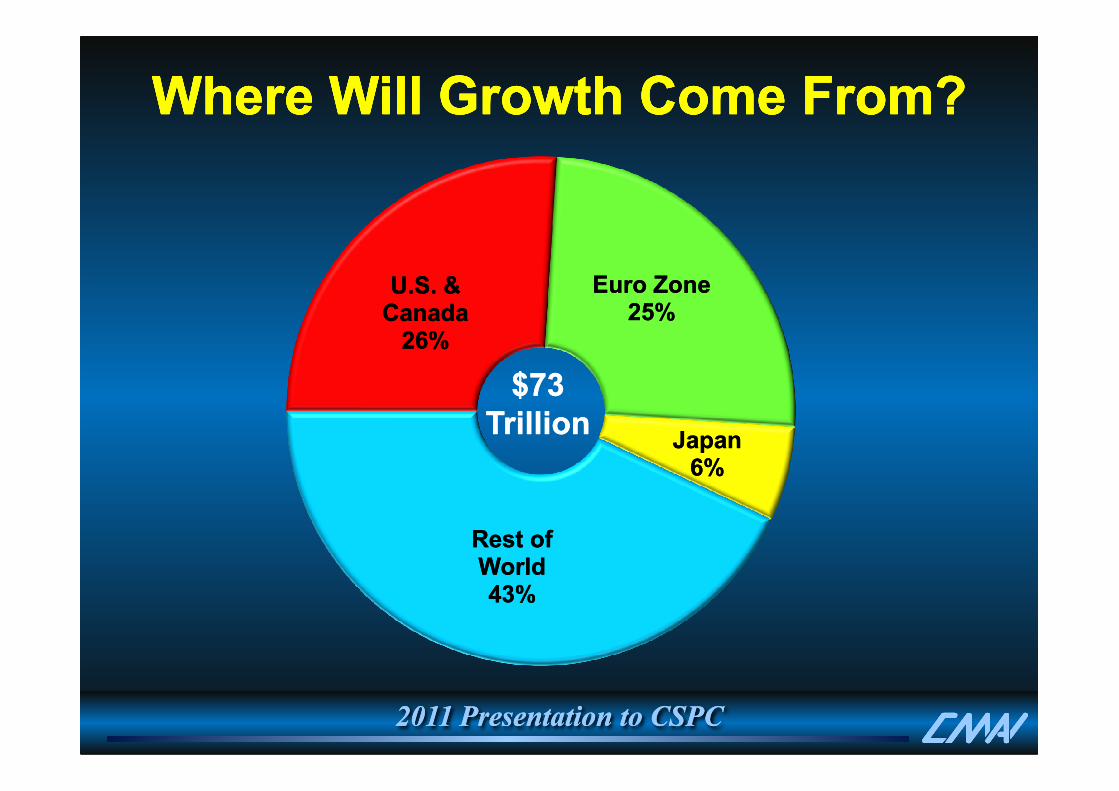

Where Will Growth Come From?Where Will Growth Come From?Where Will Growth Come From?Where Will Growth Come From?

U.S. & U.S. & CanadaCanada

26%26%

Euro ZoneEuro Zone25%25%

$73$73

2011 Presentation to CSPC2011 Presentation to CSPC

JapanJapan6%6%

Rest of Rest of WorldWorld43%43%

$73$73TrillionTrillion

8

12

16

4

6

8

Economic Outlook

Trillion U.S. Dollar (2007 Constant )Trillion U.S. Dollar (2007 Constant ) Growth Rate, PercentGrowth Rate, Percent

2011 Presentation to CSPC2011 Presentation to CSPC

-4

0

4

0

2

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China GDP Wld Avg Growth Rate China Growth Rate

EnergyEnergy

2011 Presentation to CSPC2011 Presentation to CSPC

Crude Oil Prices Are Expected to Remain High Driven Crude Oil Prices Are Expected to Remain High Driven By Growing Demand and Supply Concerns . . .By Growing Demand and Supply Concerns . . .

Crude Oil Prices Are Expected to Remain High Driven Crude Oil Prices Are Expected to Remain High Driven By Growing Demand and Supply Concerns . . .By Growing Demand and Supply Concerns . . .

Dollars per Barrel

60

80

100

120Brent Current

Brent Constant 2011$

WTI Current

WTI Constant 2011$

2011 Presentation to CSPC2011 Presentation to CSPC8

0

20

40

60

2000 2005 2010 2015

Global Industry OverviewGlobal Industry Overview

2011 Presentation to CSPC2011 Presentation to CSPC

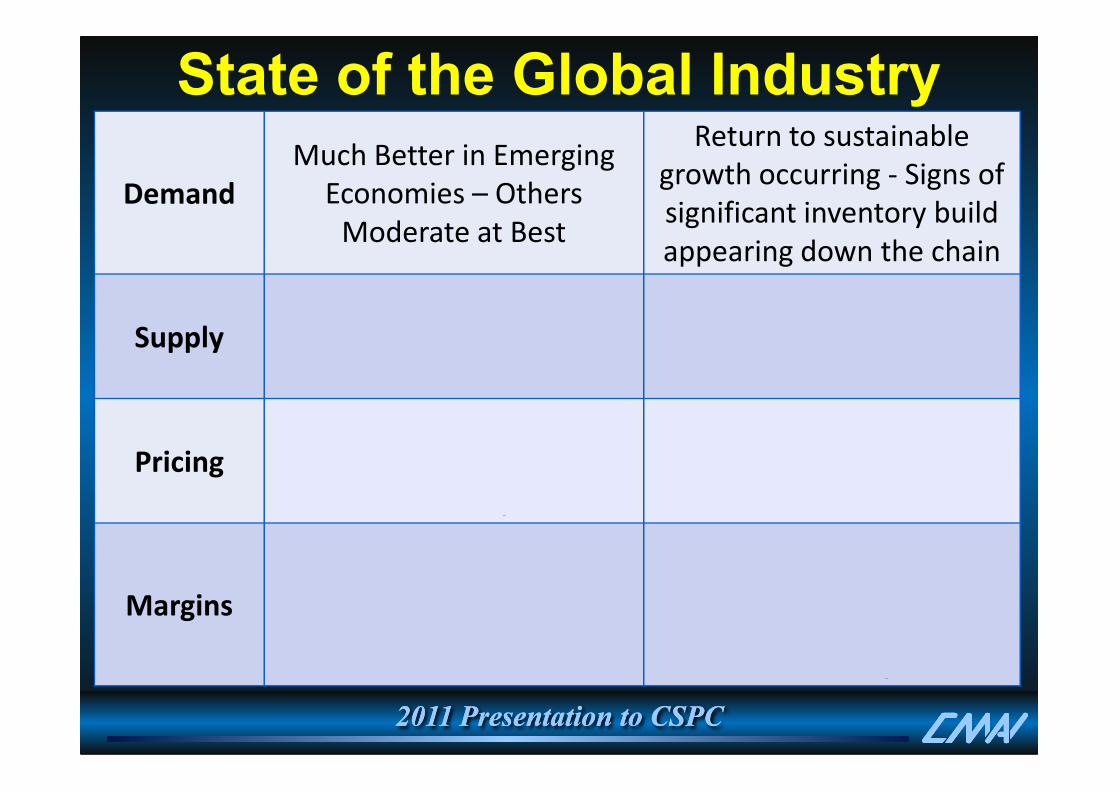

State of the Global Industry

Demand

Much Better in Emerging

Economies – Others

Moderate at Best

Return to sustainable

growth occurring - Signs of

significant inventory build

appearing down the chain

Supply

Less New Capacity on

Horizon – High Cost

Capacity out of market.

Market is balanced to tight

due to dislocations and

“cost-induced” discipline

2011 Presentation to CSPC2011 Presentation to CSPC

Pricing

Reaching record levels on

all fronts – severe cost push

inflates floor prices

Consolidations have helped

producers; higher prices

will impact growth

Margins

“Super Cycle” for integrated

gas position; bare

minimums for market

clearing producers

Results are more region

and value chain specific.

Benefits of integration

have become very obvious

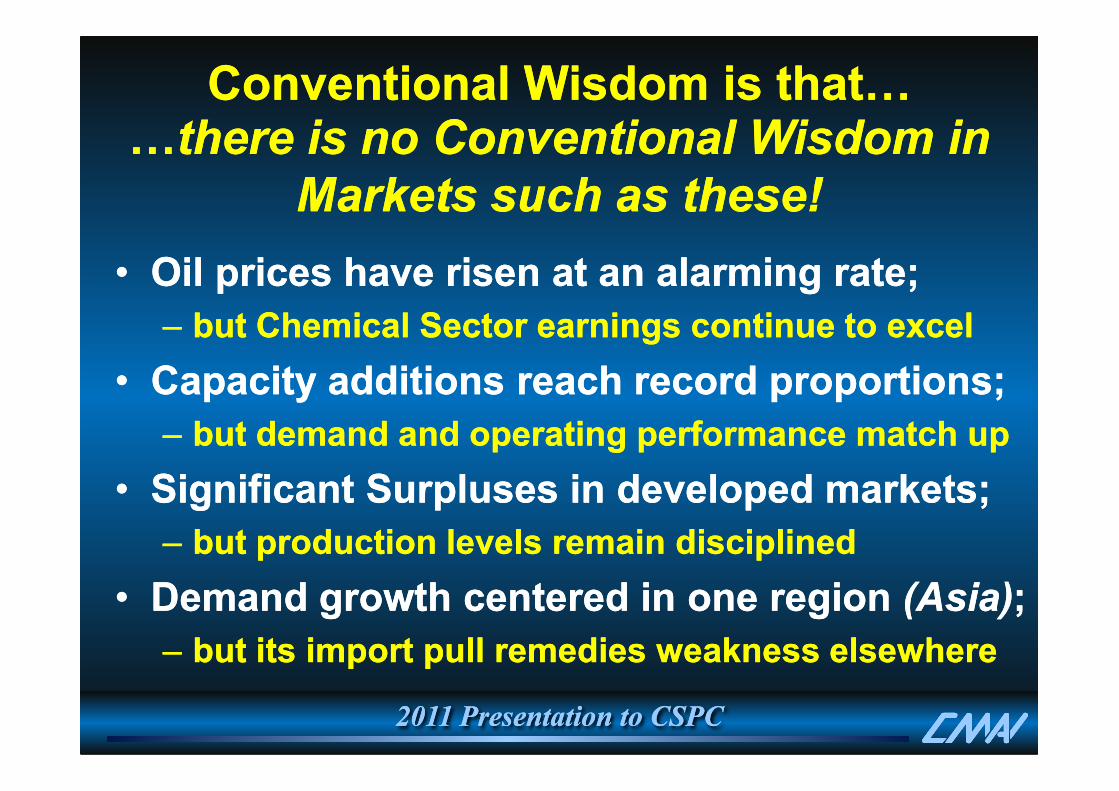

??there is no Conventional Wisdom in there is no Conventional Wisdom in

Markets such as these!Markets such as these!

•• Oil prices have risen at an alarming rate;Oil prices have risen at an alarming rate;

–– but Chemical Sector earnings continue to excelbut Chemical Sector earnings continue to excel

•• Capacity additions reach record proportions;Capacity additions reach record proportions;

Conventional Wisdom is that?Conventional Wisdom is that?

2011 Presentation to CSPC2011 Presentation to CSPC

•• Capacity additions reach record proportions;Capacity additions reach record proportions;

–– but demand and operating performance match upbut demand and operating performance match up

•• Significant Surpluses in developed markets;Significant Surpluses in developed markets;

–– but production levels remain disciplinedbut production levels remain disciplined

•• Demand growth centered in one region Demand growth centered in one region (Asia)(Asia);;

–– but its import pull remedies weakness elsewherebut its import pull remedies weakness elsewhere

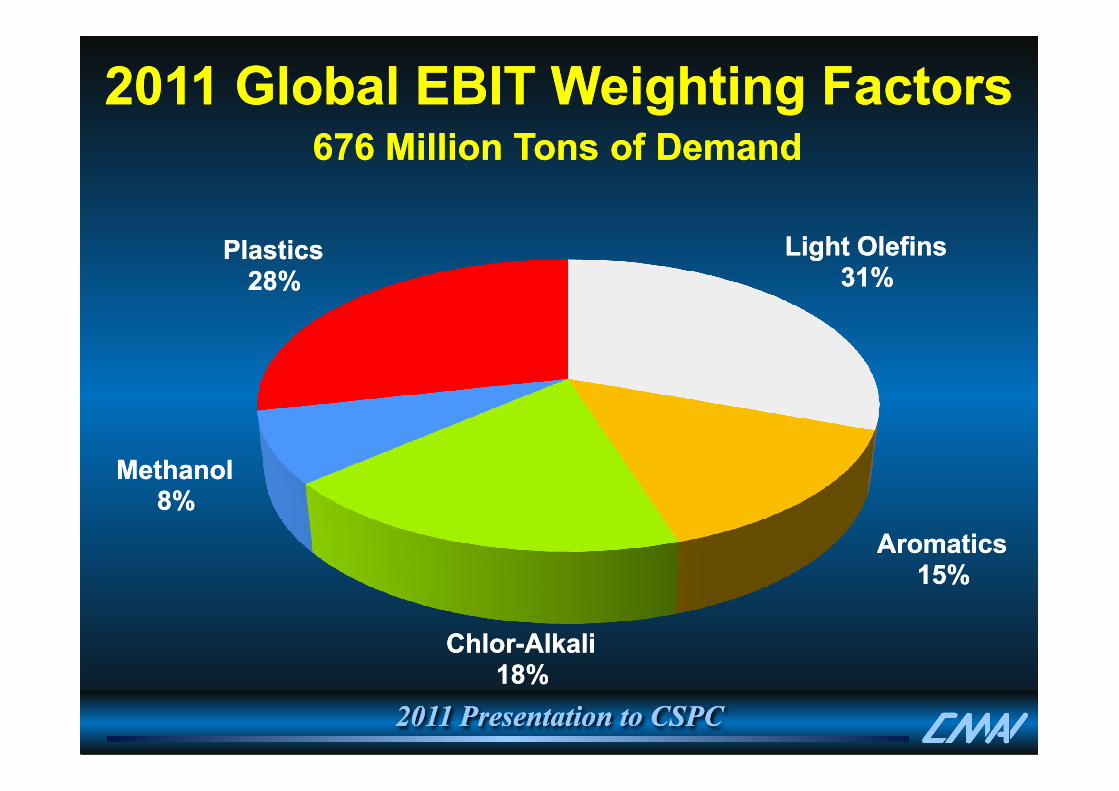

Current State of the Global IndustryCurrent State of the Global Industry

2011 Presentation to CSPC2011 Presentation to CSPC

Light OlefinsLight Olefins31%31%

PlasticsPlastics28%28%

2011 Global EBIT Weighting Factors2011 Global EBIT Weighting Factors676 Million Tons of Demand676 Million Tons of Demand

2011 Presentation to CSPC2011 Presentation to CSPC

AromaticsAromatics15%15%

ChlorChlor--AlkaliAlkali18%18%

MethanolMethanol8%8%

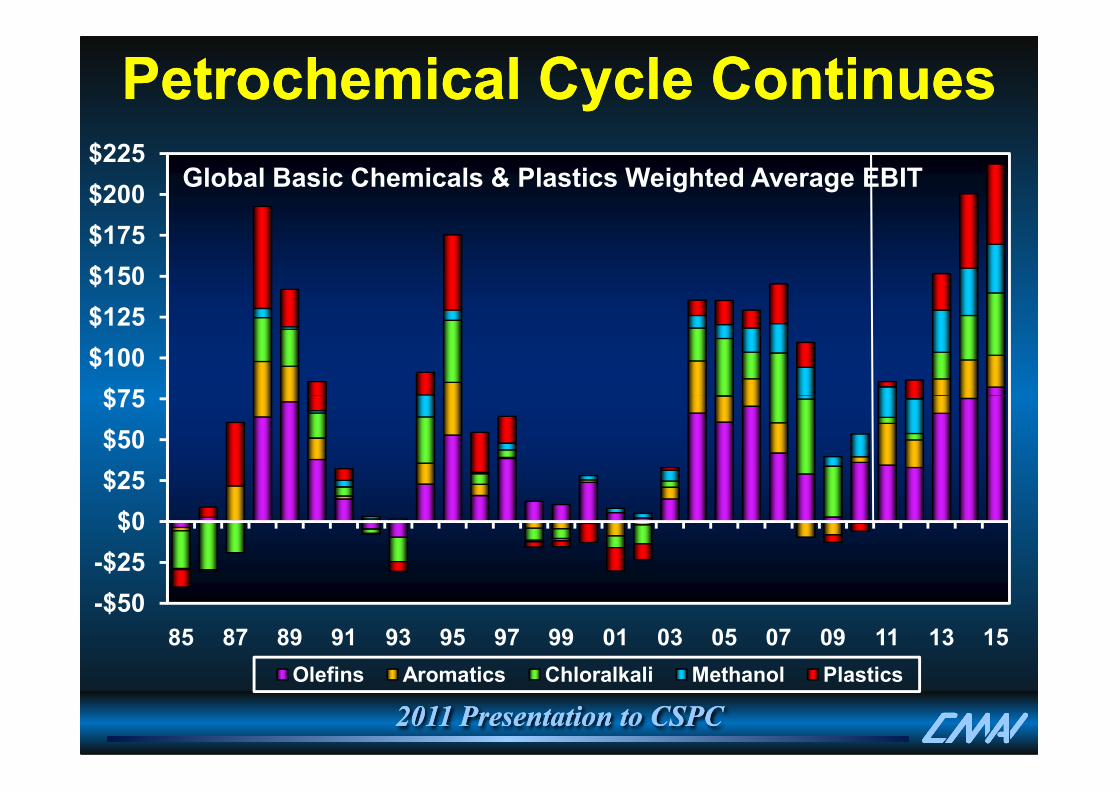

$75

$100

$125

$150

$175

$200

$225Global Basic Chemicals & Plastics Weighted Average EBIT

Petrochemical Cycle ContinuesPetrochemical Cycle Continues

2011 Presentation to CSPC2011 Presentation to CSPC

-$50

-$25

$0

$25

$50

$75

85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15

Olefins Aromatics Chloralkali Methanol Plastics

30

40

50

60

Basic Chemicals & PlasticsGlobal Demand Recovery and Growth are Impressive

•• Sharp decline Sharp decline followed by a followed by a sharp recovery in sharp recovery in the Developing the Developing World World (BRICs)(BRICs)

•• New spending New spending supports growth:supports growth:

Millions of Metric Tons Millions of Metric Tons

6%

8%

10%

12%

Percent Annual GrowthPercent Annual Growth

Demand ChangeDemand Change

Demand Change (%)Demand Change (%)

2011 Presentation to CSPC2011 Presentation to CSPC

-30

-20

-10

0

10

20

30

2000 2005 2010 2015

supports growth:supports growth:

–– Consumption Consumption levels risinglevels rising

–– Especially in Especially in ChinaChina

•• Concern Concern about about capacity capacity overhang overhang delays future delays future investment investment plansplans

-6%

-4%

-2%

0%

2%

4%

6%

Capacity AdditionsCapacity AdditionsCapacity Additions

Cumulative Production GrowthCumulative Production Growth

Million Metric TonsMillion Metric Tons

Cumulative Production GrowthCumulative Production Growth

Million Metric TonsMillion Metric Tons

500500500500

600600600600

700700700700

800800800800

Developing CountriesDeveloping CountriesDeveloping CountriesDeveloping Countries

Middle East Middle East (Hydrocarbon Rich)(Hydrocarbon Rich)Middle East Middle East (Hydrocarbon Rich)(Hydrocarbon Rich)Middle East Middle East (Hydrocarbon Rich)(Hydrocarbon Rich)

Developed CountriesDeveloped CountriesDeveloped CountriesDeveloped Countries

Growth Favors Labor & Hydrocarbon AdvantageGrowth Favors Labor & Hydrocarbon Advantage

•• Production growth is Production growth is indicative economic indicative economic development and/or development and/or relative cost positionrelative cost position

•• Mature Economies need Mature Economies need an export cost advantage an export cost advantage to advance productionto advance production

2011 Presentation to CSPC2011 Presentation to CSPC

0000

100100100100

200200200200

300300300300

400400400400

500500500500

90909090 95959595 00000000 05050505 10101010 15151515 20202020

Developed CountriesDeveloped CountriesDeveloped CountriesDeveloped Countries•• Developing economics Developing economics

attract local investment attract local investment to support local demandto support local demand

•• International Markets are International Markets are the perfect remedy for a the perfect remedy for a slow or lessslow or less--developed developed domestic environment domestic environment

-- if you can competeif you can compete

2020

2525

3030

35352010-2015

67%Share of Global Total:Share of Global Total:

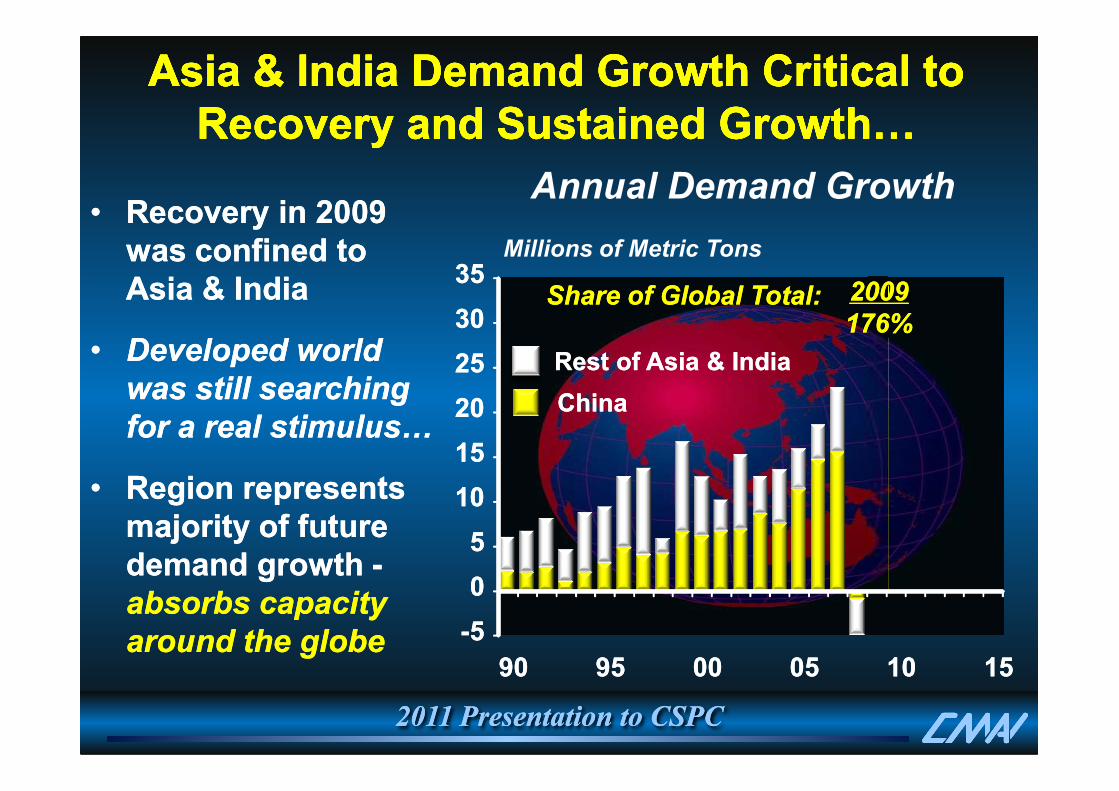

Asia & India Demand Growth Critical to Asia & India Demand Growth Critical to Recovery and Sustained Growth?Recovery and Sustained Growth?

Asia & India Demand Growth Critical to Asia & India Demand Growth Critical to Recovery and Sustained Growth?Recovery and Sustained Growth?

•• Recovery in 2009 Recovery in 2009 was confined to was confined to Asia & IndiaAsia & India

•• Developed world Developed world

was still searching was still searching

Millions of Metric Tons

Annual Demand Growth

ChinaChina

Rest of Asia & IndiaRest of Asia & India

20092009

176%176%

2011 Presentation to CSPC2011 Presentation to CSPC

--55

00

55

1010

1515

2020

9090 9595 0000 0505 1010 1515

was still searching was still searching

for a real stimulus/for a real stimulus/

•• Region represents Region represents majority of future majority of future demand growth demand growth --absorbs capacity absorbs capacity

around the globearound the globe

ChinaChina

4040

5050

6060

7070

8080

4040

5050

6060

7070

8080

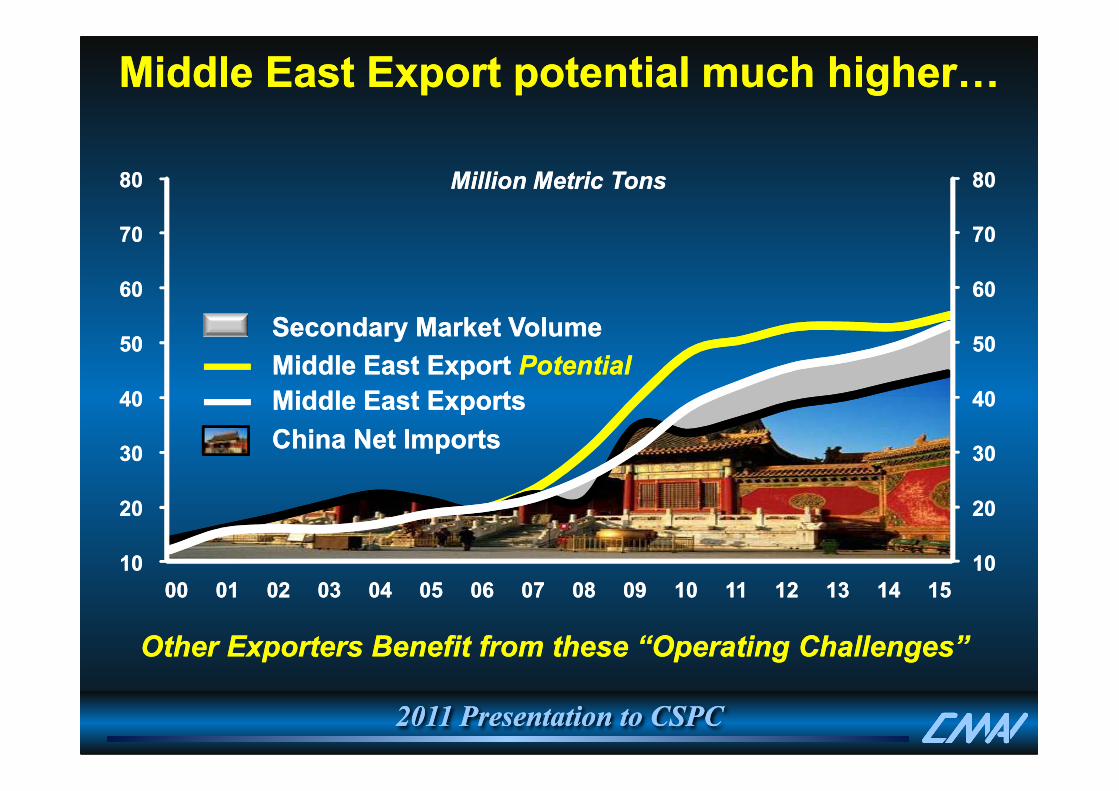

Middle East Export potential much higher?Middle East Export potential much higher?

Middle East Export Middle East Export PotentialPotential

Secondary Market VolumeSecondary Market Volume

Middle East ExportsMiddle East Exports

Million Metric TonsMillion Metric Tons

2011 Presentation to CSPC2011 Presentation to CSPC

1010

2020

3030

4040

1010

2020

3030

4040

0000 0101 0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 1212 1313 1414 1515

China Net Imports China Net Imports

Middle East ExportsMiddle East Exports

Other Exporters Benefit from these “Operating Challenges”Other Exporters Benefit from these “Operating Challenges”

Olefins: Strategic Issues And Emerging Trends

Olefins: Strategic Issues And Emerging Trends

•• Accelerated demand Accelerated demand growth in emerging growth in emerging marketsmarkets

•• North America is “back North America is “back

2011 Presentation to CSPC2011 Presentation to CSPC

•• North America is “back North America is “back in the game”in the game”

•• Middle East operations Middle East operations below expectationsbelow expectations

•• Alternate technologies Alternate technologies & feedstocks emerge& feedstocks emerge

Petrochemical Supply Chain

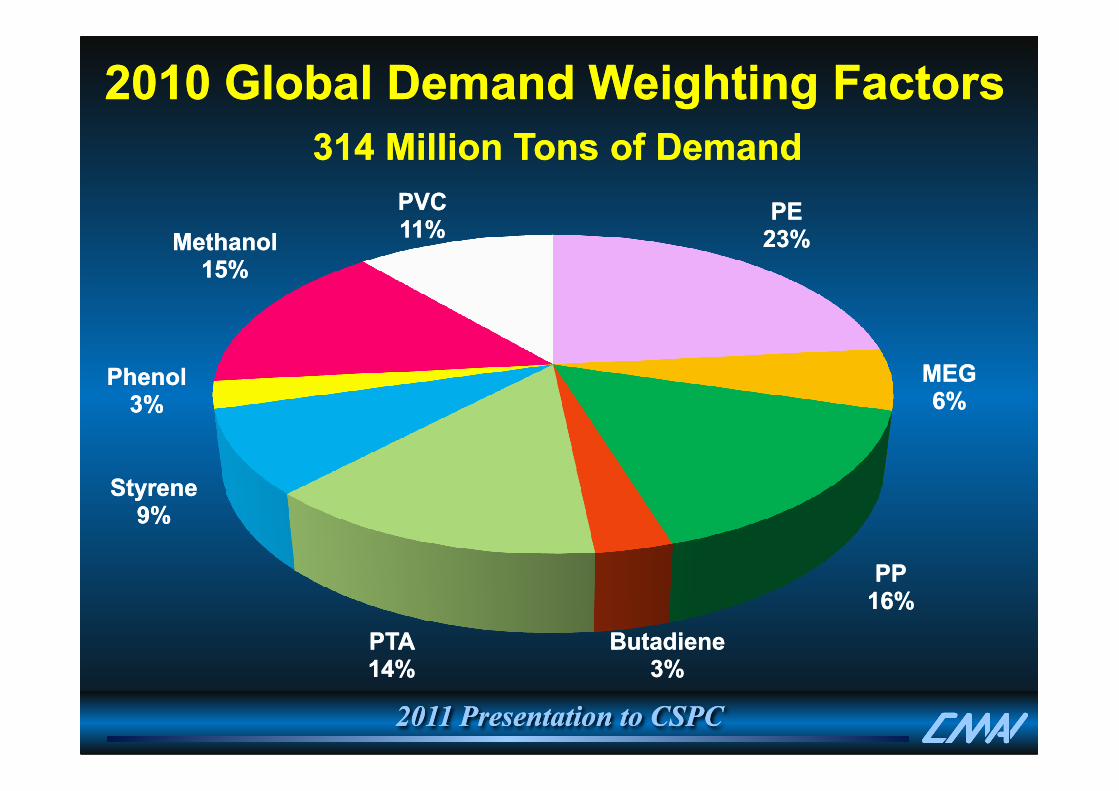

2010 Global Demand Weighting Factors2010 Global Demand Weighting Factors

314 Million Tons of Demand314 Million Tons of Demand

PEPE23%23%

MEGMEG6%6%

PhenolPhenol3%3%

MethanolMethanol15%15%

PVCPVC11%11%

2011 Presentation to CSPC2011 Presentation to CSPC

6%6%

PPPP16%16%

ButadieneButadiene3%3%

PTAPTA14%14%

StyreneStyrene9%9%

3%3%

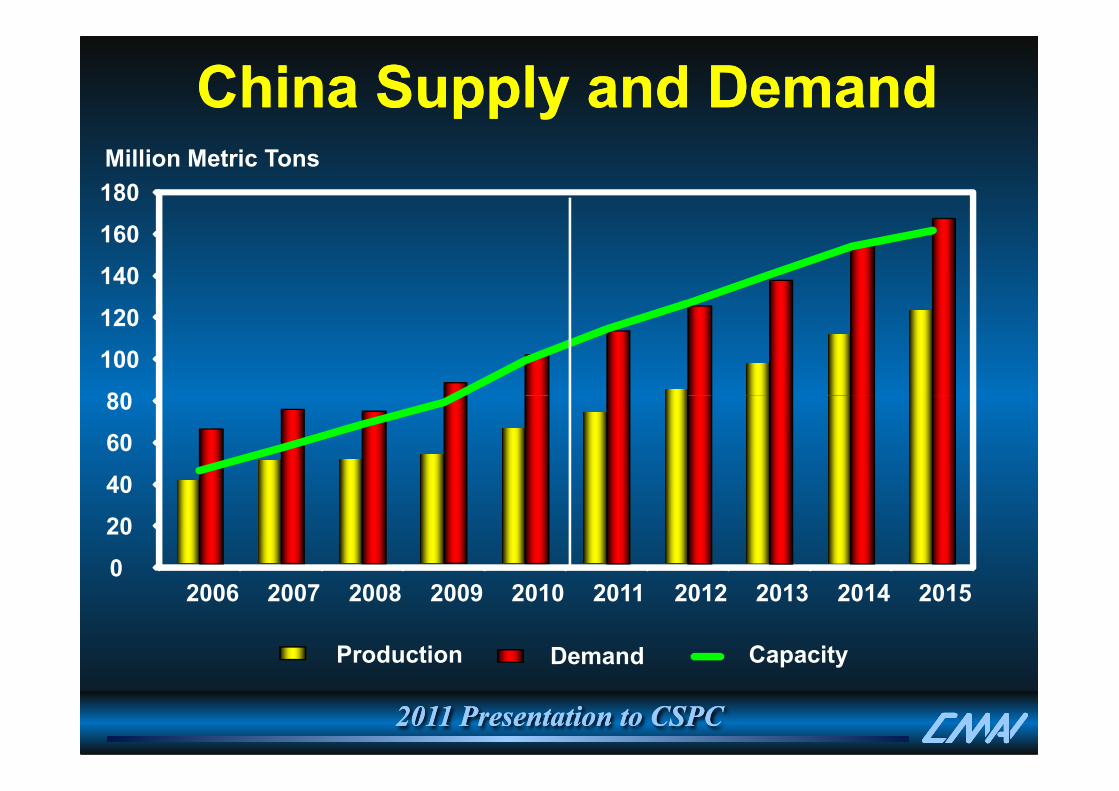

China Supply and DemandChina Supply and Demand

80

100

120

140

160

180

Million Metric Tons

2011 Presentation to CSPC2011 Presentation to CSPC

0

20

40

60

80

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Production Demand Capacity

Major Petrochemical ProjectsMajor Petrochemical ProjectsDaqing PCDaqing PCC2: 600 KTAC2: 600 KTAQ1/2013Q1/2013

Fushun PCFushun PCC2: 800 KTAC2: 800 KTAQ2/2012Q2/2012

Sichuan PCSichuan PC

Urumqi PCUrumqi PCPX: 1,000 KTAPX: 1,000 KTAQ2/2011Q2/2011

Shanghai PCShanghai PC

BohaiBohaiChemChemC3: 600 KTAC3: 600 KTAQ4/2012Q4/2012

2011 Presentation to CSPC2011 Presentation to CSPC

C2: 800 KTA/PX: 650 KTAC2: 800 KTA/PX: 650 KTAQ1/2012Q1/2012

Wuhan PCWuhan PCC2: 800 KTAC2: 800 KTAQ1/2013Q1/2013

Shanghai PCShanghai PCC2: 600 KTAC2: 600 KTAQ1/2014Q1/2014

Hainan RefHainan RefPX: 600 KTAPX: 600 KTAQ3/2012Q3/2012

Sinopec/KPC JVSinopec/KPC JVC2: 1,000 KTAC2: 1,000 KTAQ1/2015Q1/2015

Tenlong PCTenlong PCPX: 800 KTAPX: 800 KTAMid/2012Mid/2012

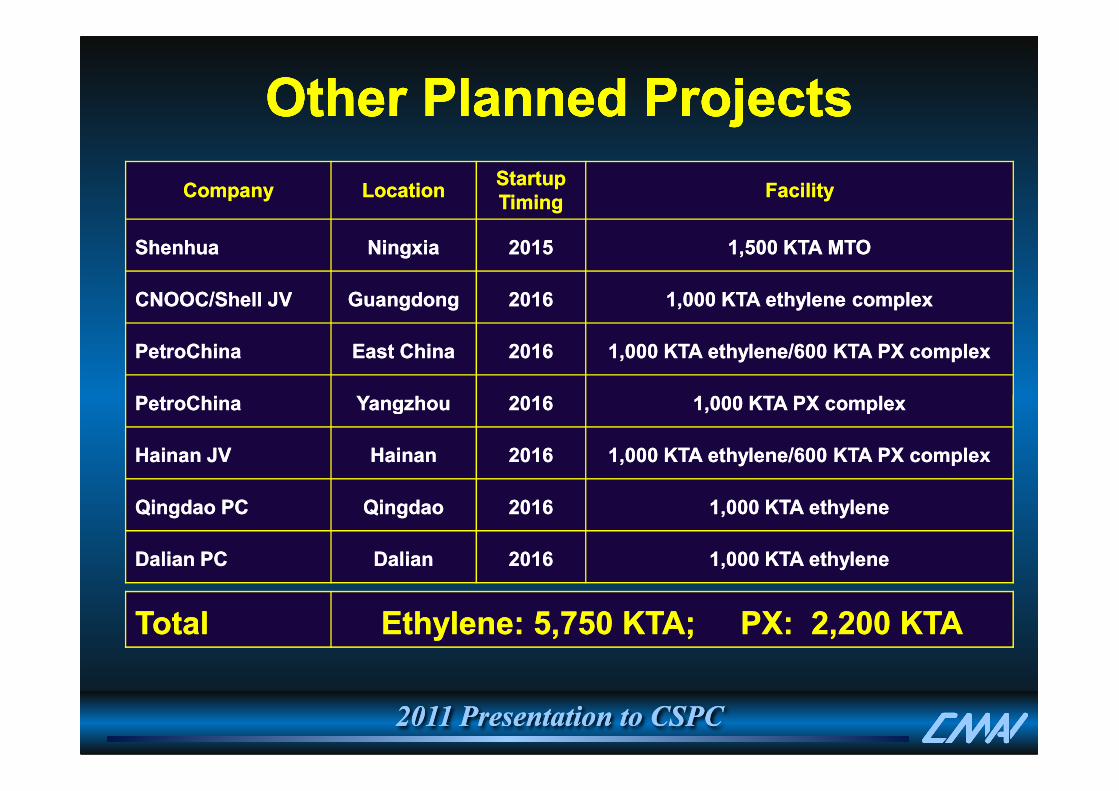

CompanyCompany LocationLocationStartup Startup TimingTiming

FacilityFacility

ShenhuaShenhua NingxiaNingxia 20152015 1,500 KTA MTO1,500 KTA MTO

CNOOC/Shell JV CNOOC/Shell JV GuangdongGuangdong 20162016 1,000 KTA ethylene complex1,000 KTA ethylene complex

PetroChinaPetroChina East ChinaEast China 20162016 1,000 KTA ethylene/600 KTA PX complex1,000 KTA ethylene/600 KTA PX complex

PetroChinaPetroChina YangzhouYangzhou 20162016 1,000 KTA PX complex1,000 KTA PX complex

Other Other Planned ProjectsPlanned ProjectsOther Other Planned ProjectsPlanned Projects

2011 Presentation to CSPC2011 Presentation to CSPC

PetroChinaPetroChina YangzhouYangzhou 20162016 1,000 KTA PX complex1,000 KTA PX complex

Hainan JVHainan JV HainanHainan 20162016 1,000 KTA ethylene/600 KTA PX complex1,000 KTA ethylene/600 KTA PX complex

Qingdao PCQingdao PC QingdaoQingdao 20162016 1,000 KTA ethylene1,000 KTA ethylene

Dalian PCDalian PC DalianDalian 20162016 1,000 KTA ethylene1,000 KTA ethylene

TotalTotal Ethylene: 5,750 KTA; PX: 2,200 KTAEthylene: 5,750 KTA; PX: 2,200 KTA

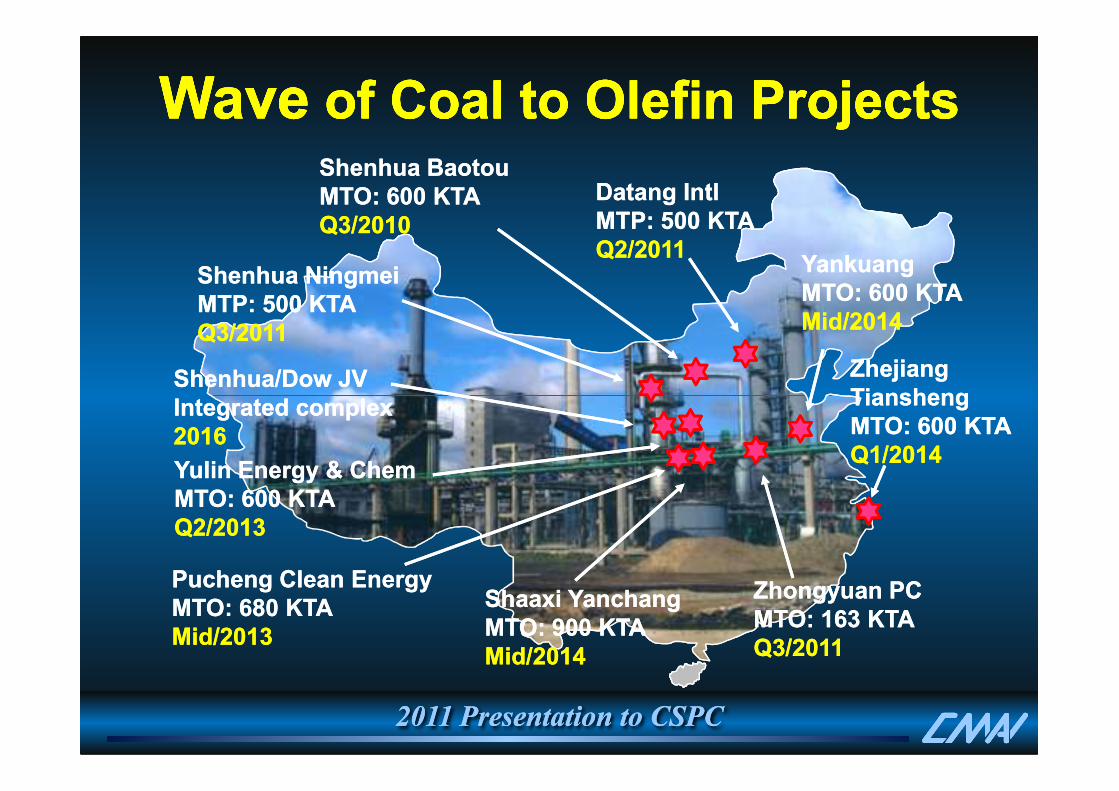

WaveWave of Coal to Olefin Projectsof Coal to Olefin ProjectsWaveWave of Coal to Olefin Projectsof Coal to Olefin Projects

Shenhua/Dow JVShenhua/Dow JVIntegrated complexIntegrated complex

Shenhua BaotouShenhua BaotouMTO: 600 KTAMTO: 600 KTAQ3/2010Q3/2010

Shenhua NingmeiShenhua NingmeiMTP: 500 KTAMTP: 500 KTAQ3/2011Q3/2011

DatangDatang IntlIntlMTP: 500 KTAMTP: 500 KTAQ2/2011Q2/2011

YankuangYankuangMTO: 600 KTAMTO: 600 KTAMid/2014Mid/2014

Zhejiang Zhejiang TianshengTiansheng

2011 Presentation to CSPC2011 Presentation to CSPC

Integrated complexIntegrated complex20162016

Yulin Energy & Yulin Energy & ChemChemMTO: 600 KTAMTO: 600 KTAQ2/2013Q2/2013

PuchengPucheng Clean EnergyClean EnergyMTO: 680 KTAMTO: 680 KTAMid/2013Mid/2013

ZhongyuanZhongyuan PCPCMTO: 163 KTAMTO: 163 KTAQ3/2011Q3/2011

ShaaxiShaaxi YanchangYanchangMTO: 900 KTAMTO: 900 KTAMid/2014Mid/2014

TianshengTianshengMTO: 600 KTAMTO: 600 KTAQ1/2014Q1/2014

“Global Chemicals” “Global Chemicals” Summary PerspectivesSummary Perspectives

“Global Chemicals” “Global Chemicals” Summary PerspectivesSummary Perspectives

Developed Developed World MaturesWorld Matures

•• Lower DemandLower Demand

•• Higher Imports Higher Imports (Finished Goods)(Finished Goods)

Developing Developing World ExpandsWorld Expands

•• More CapacityMore Capacity

•• Higher ImportsHigher Imports

2011 Presentation to CSPC2011 Presentation to CSPC

•• Higher Imports Higher Imports (Finished Goods)(Finished Goods)

•• Higher ImportsHigher Imports

(Raw Materials)(Raw Materials)

New Gulf (ME) New Gulf (ME) Advantage Advantage RemainsRemains

•• Higher ExportsHigher Exports

•• Diverse CapacityDiverse Capacity

Renewed Renewed Gulf (GOM) Gulf (GOM) ReemergesReemerges

•• Wide Oil vs Gas GapWide Oil vs Gas Gap

•• Higher ExportsHigher Exports

Top Related