Languages

Pages

Legal

In Dialogue with

ATAFMr Thulani Shongwe

Mr Ted Silkiluwasha

Davis Tax

Commission Professor Annet Oguttu

SARSMs Sunita Manik,

Ms Nishana Gosai

OECD Transfer Pricing

Guidelines in the Spotlight

Welcome Address

2 © 2015 Deloitte Touche Tohmatsu Limited

Nazrien Kader

Deloitte Africa

Tax Leader

Deloitte Africa Transfer Pricing

Leader

3 © 2015 Deloitte Touche Tohmatsu Limited

Billy Joubert

Guest Speakers

Guest Speakers

Professor Annet

Oguttu Chairman of the

BEPS Sub-

Committee

Thulani Shongwe

Specialist: Multi-

Lateral Co-operation

Africa Tax

Administration Forum

Nishana Gosai

Transfer Pricing

Manager

South Africa

Revenue Services

Sunita Manik

Group Executive at

the Large Business

Centre

South Africa

Revenue Services

Ted SilkiluwashaCross Border Taxation

Technical Committee at

Africa Tax

Administration Forum

Africa Tax

Administration

Forum

Presentation

Mr Thulani Shongwe

Mr Ted Silkiluwasha

Africa Tax Administration Forum

Thulani Shongwe

Head of Multi-Lateral

Co-operation at

Africa Tax

Administration Forum

Ted Silkiluwasha

Cross Border

Taxation Technical

Committee at Africa

Tax Administration

Forum

AFRICAN TAX ADMINISTRATION FORUMLeading Africa in tax administration

BEPS AND THE OECD ACTIONS: APPLICATION TO AN AFRICAN CONTEXT

Ted Silkiluwasha & Thulani Shongwe

UNECA Sub-Regional Workshop on IFFs

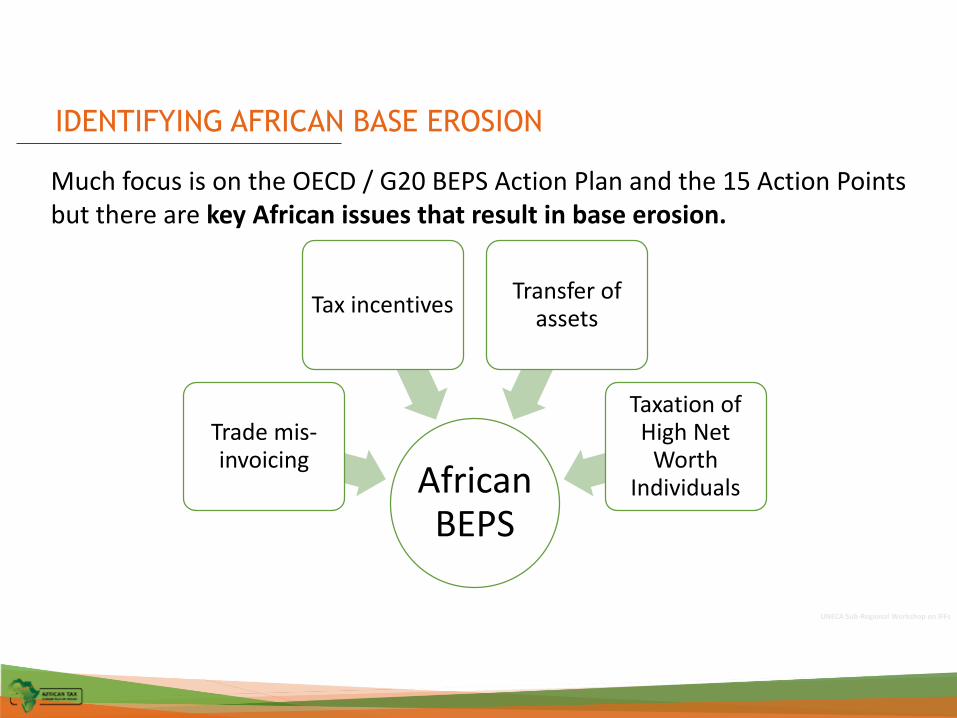

IDENTIFYING AFRICAN BASE EROSION

Much focus is on the OECD / G20 BEPS Action Plan and the 15 Action Points but there are key African issues that result in base erosion.

African BEPS

Trade mis-invoicing

Tax incentivesTransfer of

assets

Taxation of High Net

Worth Individuals

UNECA Sub-Regional Workshop on IFFs

AFRICAN GAINS IN THE OECD BEPS PROCESS

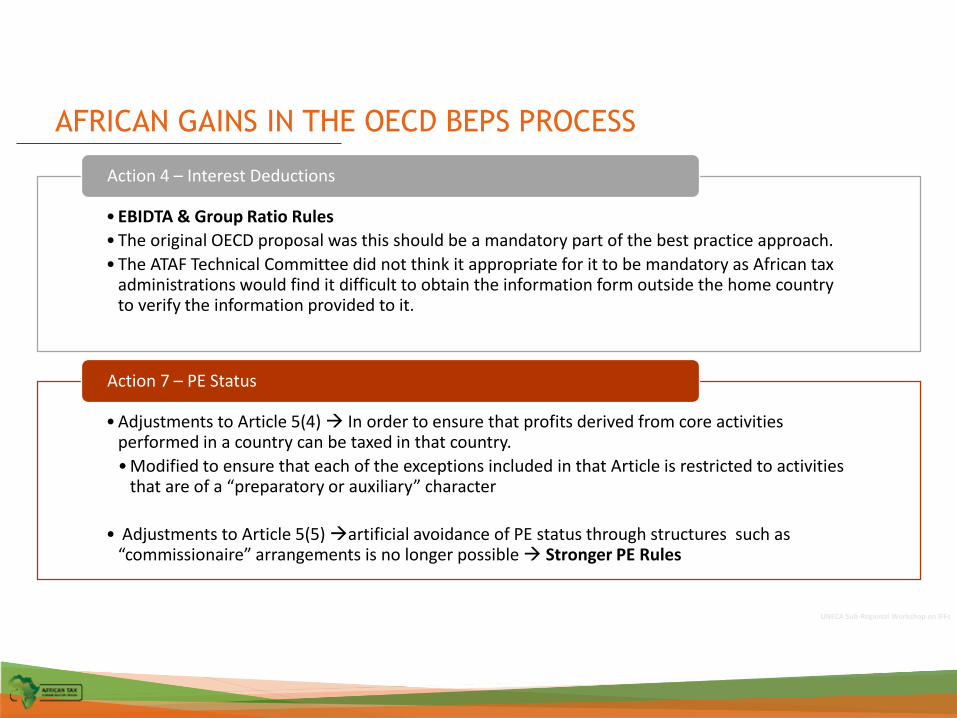

• EBIDTA & Group Ratio Rules

• The original OECD proposal was this should be a mandatory part of the best practice approach.

• The ATAF Technical Committee did not think it appropriate for it to be mandatory as African tax administrations would find it difficult to obtain the information form outside the home country to verify the information provided to it.

Action 4 – Interest Deductions

• Adjustments to Article 5(4) In order to ensure that profits derived from core activities performed in a country can be taxed in that country.

• Modified to ensure that each of the exceptions included in that Article is restricted to activities that are of a “preparatory or auxiliary” character

• Adjustments to Article 5(5) artificial avoidance of PE status through structures such as “commissionaire” arrangements is no longer possible Stronger PE Rules

Action 7 – PE Status

UNECA Sub-Regional Workshop on IFFs

AFRICAN GAINS IN THE OECD BEPS PROCESS

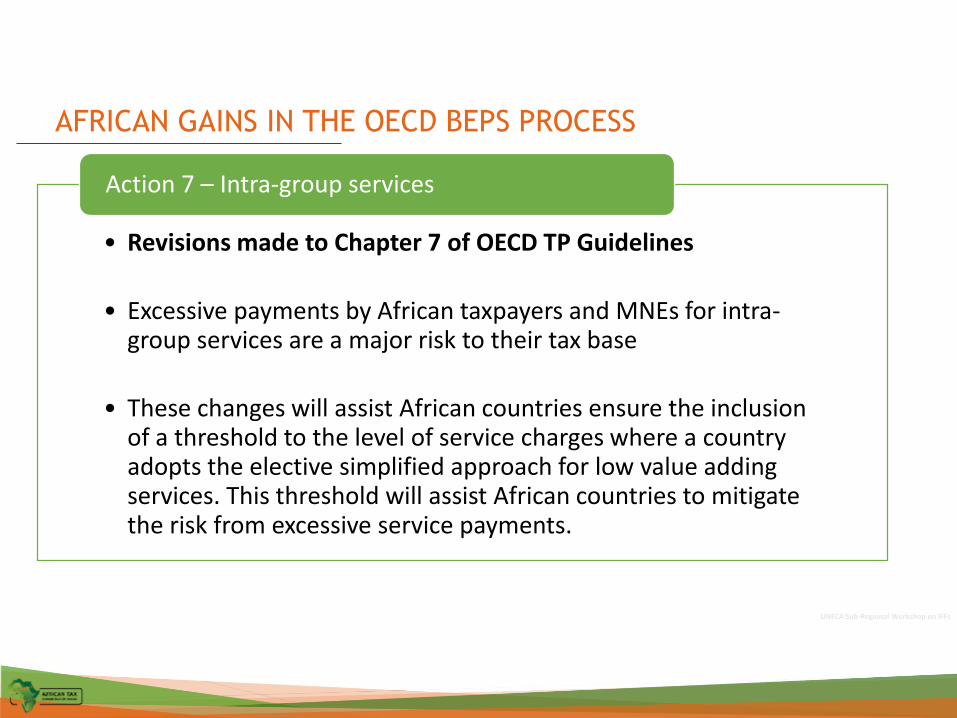

• Revisions made to Chapter 7 of OECD TP Guidelines

• Excessive payments by African taxpayers and MNEs for intra-group services are a major risk to their tax base

• These changes will assist African countries ensure the inclusion of a threshold to the level of service charges where a country adopts the elective simplified approach for low value adding services. This threshold will assist African countries to mitigate the risk from excessive service payments.

Action 7 – Intra-group services

UNECA Sub-Regional Workshop on IFFs

AFRICAN GAINS IN THE OECD BEPS PROCESS

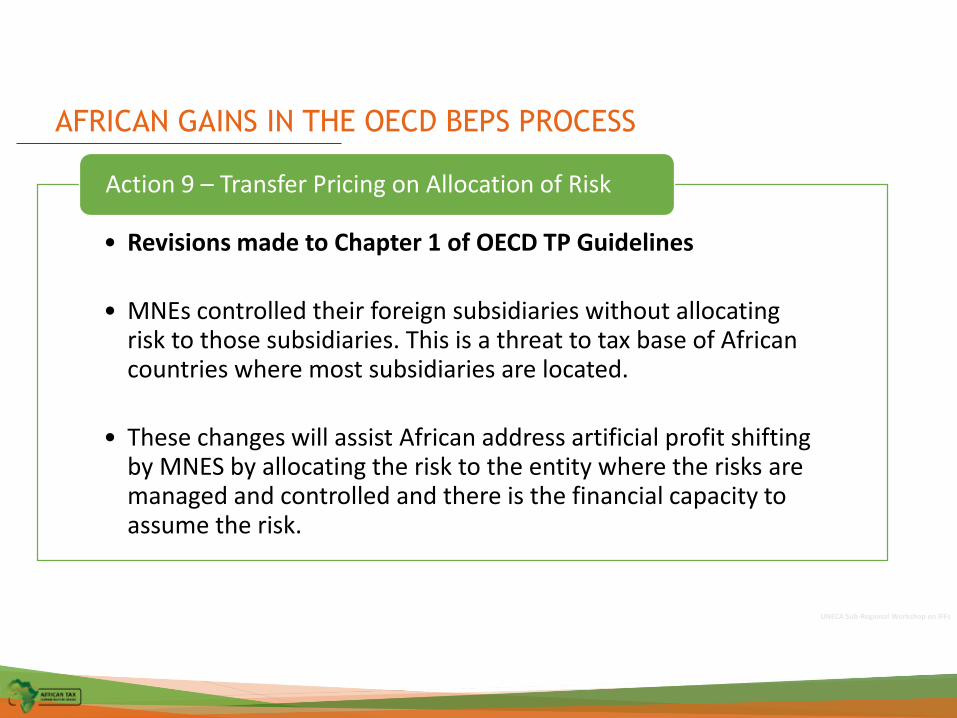

• Revisions made to Chapter 1 of OECD TP Guidelines

• MNEs controlled their foreign subsidiaries without allocating risk to those subsidiaries. This is a threat to tax base of African countries where most subsidiaries are located.

• These changes will assist African address artificial profit shifting by MNES by allocating the risk to the entity where the risks are managed and controlled and there is the financial capacity to assume the risk.

Action 9 – Transfer Pricing on Allocation of Risk

UNECA Sub-Regional Workshop on IFFs

AFRICAN GAINS IN THE OECD BEPS PROCESS

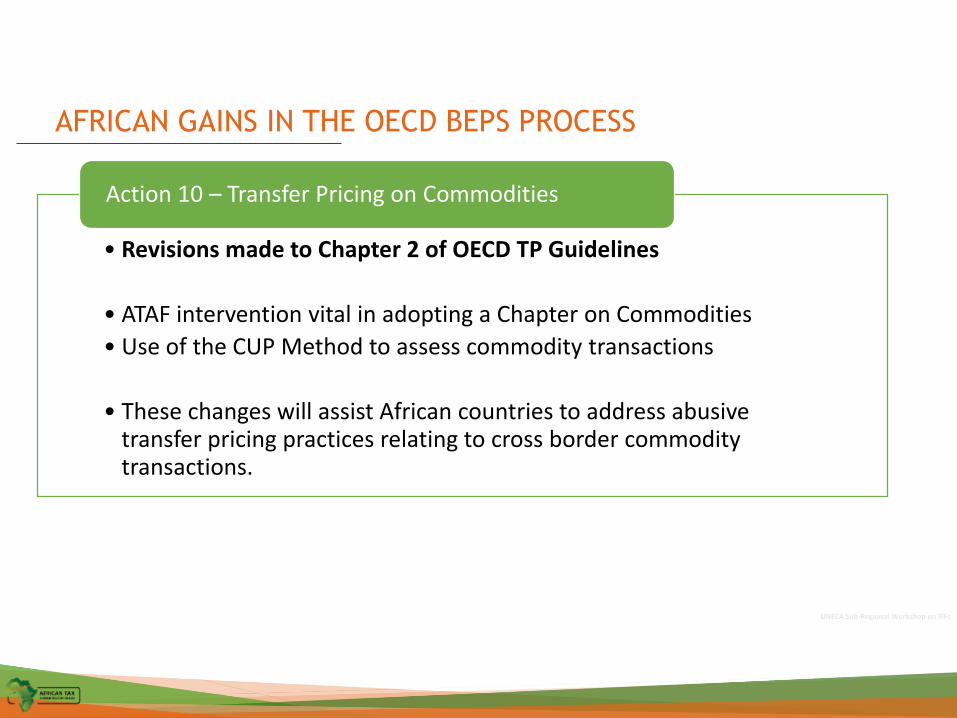

• Revisions made to Chapter 2 of OECD TP Guidelines

• ATAF intervention vital in adopting a Chapter on Commodities

• Use of the CUP Method to assess commodity transactions

• These changes will assist African countries to address abusive transfer pricing practices relating to cross border commodity transactions.

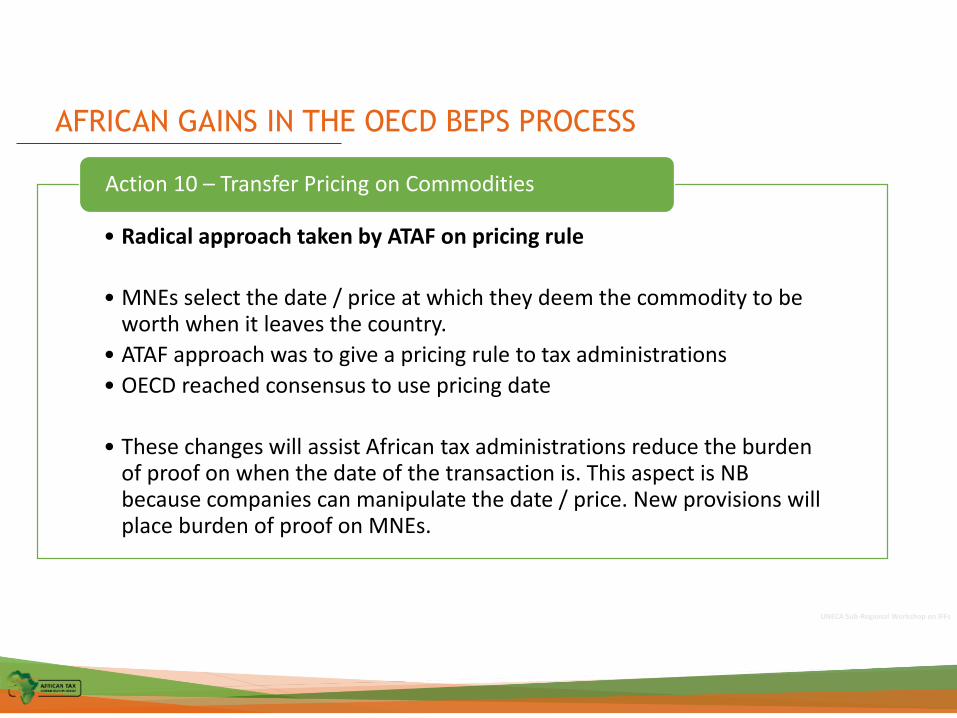

Action 10 – Transfer Pricing on Commodities

UNECA Sub-Regional Workshop on IFFs

AFRICAN GAINS IN THE OECD BEPS PROCESS

• Radical approach taken by ATAF on pricing rule

• MNEs select the date / price at which they deem the commodity to be worth when it leaves the country.

• ATAF approach was to give a pricing rule to tax administrations

• OECD reached consensus to use pricing date

• These changes will assist African tax administrations reduce the burden of proof on when the date of the transaction is. This aspect is NB because companies can manipulate the date / price. New provisions will place burden of proof on MNEs.

Action 10 – Transfer Pricing on Commodities

2nd ATAF International Conference on Tax in Africa

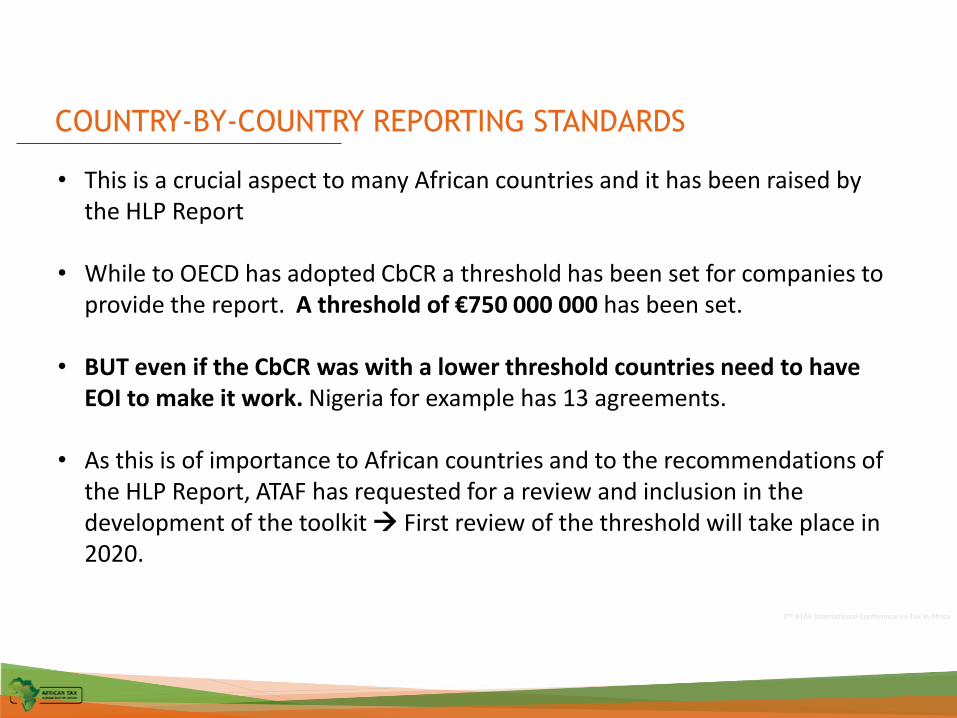

COUNTRY-BY-COUNTRY REPORTING STANDARDS

• This is a crucial aspect to many African countries and it has been raised by the HLP Report

• While to OECD has adopted CbCR a threshold has been set for companies to provide the report. A threshold of €750 000 000 has been set.

• BUT even if the CbCR was with a lower threshold countries need to have EOI to make it work. Nigeria for example has 13 agreements.

• As this is of importance to African countries and to the recommendations of the HLP Report, ATAF has requested for a review and inclusion in the development of the toolkit First review of the threshold will take place in 2020.

SAIT Transfer Pricing Summit 2015

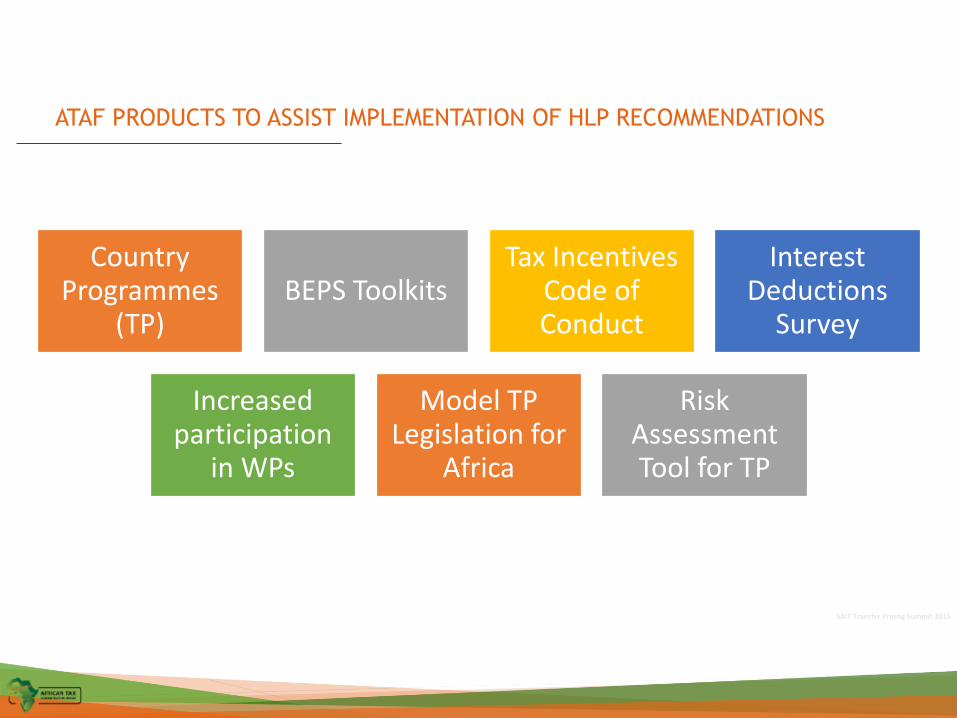

ATAF PRODUCTS TO ASSIST IMPLEMENTATION OF HLP RECOMMENDATIONS

Country Programmes

(TP)BEPS Toolkits

Tax Incentives Code of Conduct

Interest Deductions

Survey

Increased participation

in WPs

Model TP Legislation for

Africa

Risk Assessment Tool for TP

UNECA Sub-Regional Workshop on IFFs

THANK YOU FOR YOUR ATTENTION

MERCI POUR VOTRE ATTENTION

: +27 12 451 8806

: www.ataftax.org

http://www.twitter.com/ataftax

http://www.linkedin.com/company/2324754

http://www.flickr.com/photos/ataftax

http://www.facebook.com/pages/African-Tax-Administration-Forum-ATAF/167890176622405

Thulani ShongweMultilateral Cooperation

Chairman of the BEPS Sub-Committee Davis Tax Commission

Chairman of the BEPS Sub-Committee

19 © 2015 Deloitte Touche Tohmatsu Limited

Professor Annet Oguttu

DELOITTE’S DIALOGUE

BEPS AND TAX TREATIES

Prof Annet Wanyana Oguttu

University of South Africa

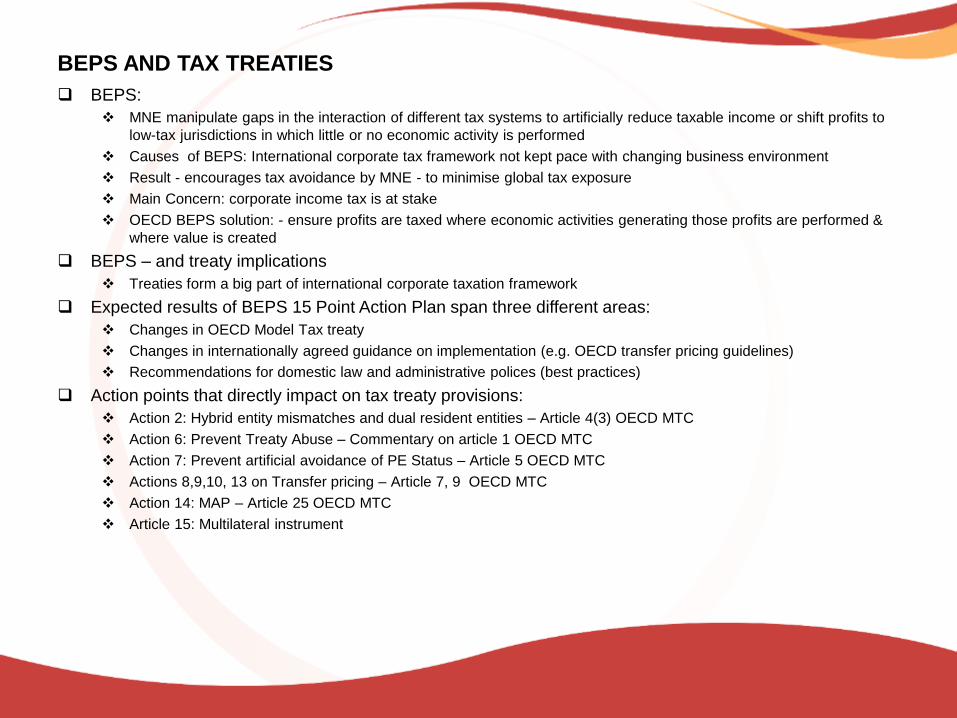

BEPS AND TAX TREATIES

BEPS:

MNE manipulate gaps in the interaction of different tax systems to artificially reduce taxable income or shift profits to

low-tax jurisdictions in which little or no economic activity is performed

Causes of BEPS: International corporate tax framework not kept pace with changing business environment

Result - encourages tax avoidance by MNE - to minimise global tax exposure

Main Concern: corporate income tax is at stake

OECD BEPS solution: - ensure profits are taxed where economic activities generating those profits are performed &

where value is created

BEPS – and treaty implications

Treaties form a big part of international corporate taxation framework

Expected results of BEPS 15 Point Action Plan span three different areas:

Changes in OECD Model Tax treaty

Changes in internationally agreed guidance on implementation (e.g. OECD transfer pricing guidelines)

Recommendations for domestic law and administrative polices (best practices)

Action points that directly impact on tax treaty provisions:

Action 2: Hybrid entity mismatches and dual resident entities – Article 4(3) OECD MTC

Action 6: Prevent Treaty Abuse – Commentary on article 1 OECD MTC

Action 7: Prevent artificial avoidance of PE Status – Article 5 OECD MTC

Actions 8,9,10, 13 on Transfer pricing – Article 7, 9 OECD MTC

Action 14: MAP – Article 25 OECD MTC

Article 15: Multilateral instrument

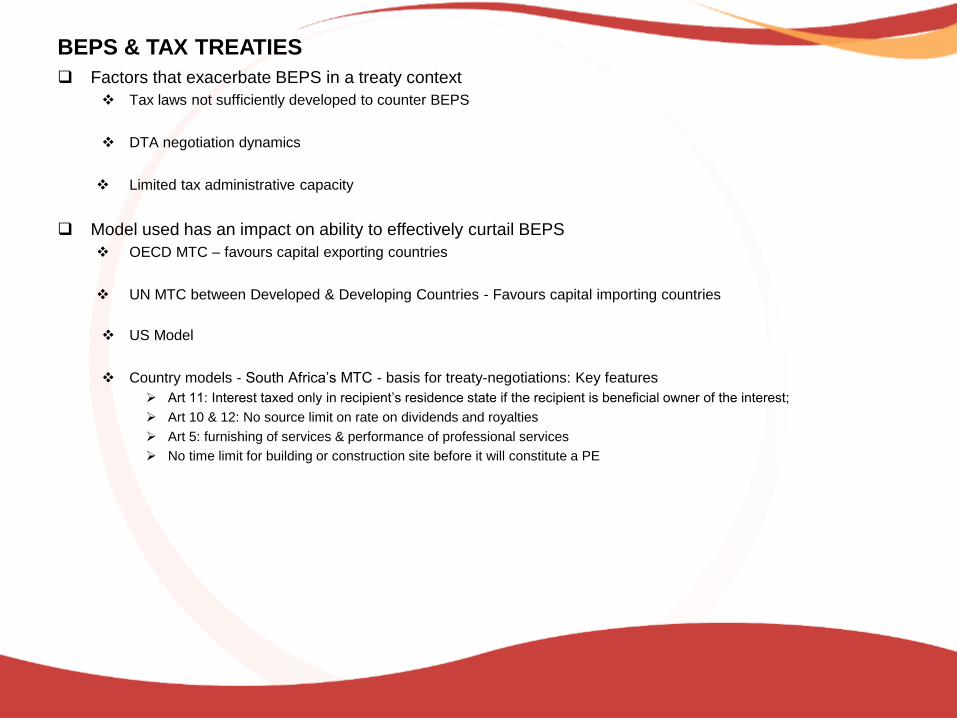

BEPS & TAX TREATIES

Factors that exacerbate BEPS in a treaty context

Tax laws not sufficiently developed to counter BEPS

DTA negotiation dynamics

Limited tax administrative capacity

Model used has an impact on ability to effectively curtail BEPS

OECD MTC – favours capital exporting countries

UN MTC between Developed & Developing Countries - Favours capital importing countries

US Model

Country models - South Africa’s MTC - basis for treaty-negotiations: Key features

Art 11: Interest taxed only in recipient’s residence state if the recipient is beneficial owner of the interest;

Art 10 & 12: No source limit on rate on dividends and royalties

Art 5: furnishing of services & performance of professional services

No time limit for building or construction site before it will constitute a PE

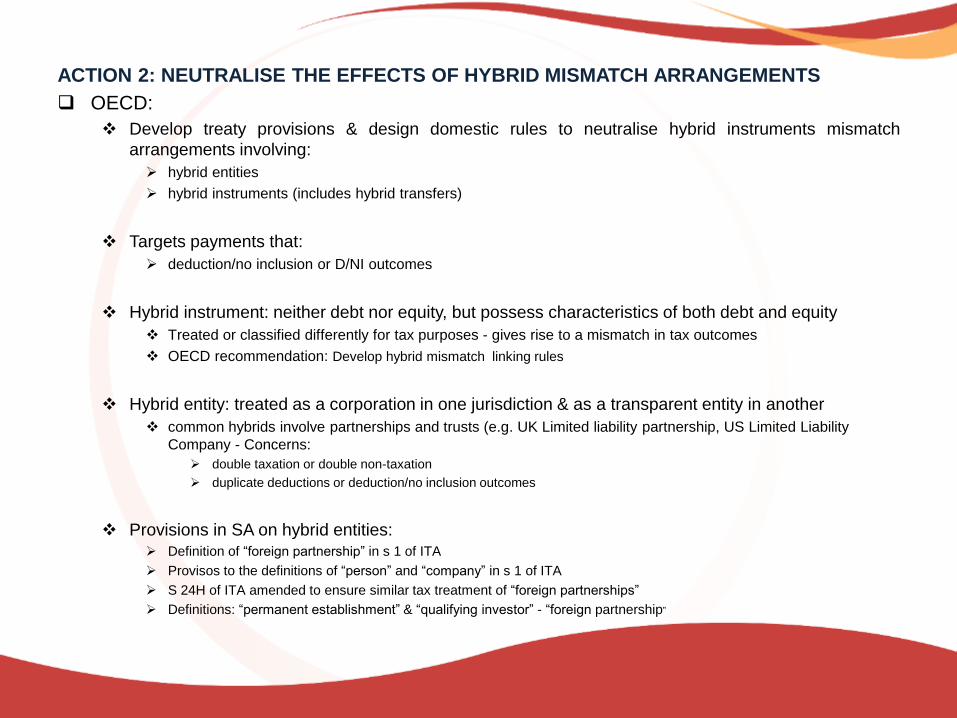

ACTION 2: NEUTRALISE THE EFFECTS OF HYBRID MISMATCH ARRANGEMENTS

OECD:

Develop treaty provisions & design domestic rules to neutralise hybrid instruments mismatch

arrangements involving:

hybrid entities

hybrid instruments (includes hybrid transfers)

Targets payments that:

deduction/no inclusion or D/NI outcomes

Hybrid instrument: neither debt nor equity, but possess characteristics of both debt and equity

Treated or classified differently for tax purposes - gives rise to a mismatch in tax outcomes

OECD recommendation: Develop hybrid mismatch linking rules

Hybrid entity: treated as a corporation in one jurisdiction & as a transparent entity in another

common hybrids involve partnerships and trusts (e.g. UK Limited liability partnership, US Limited Liability

Company - Concerns:

double taxation or double non-taxation

duplicate deductions or deduction/no inclusion outcomes

Provisions in SA on hybrid entities:

Definition of “foreign partnership” in s 1 of ITA

Provisos to the definitions of “person” and “company” in s 1 of ITA

S 24H of ITA amended to ensure similar tax treatment of “foreign partnerships”

Definitions: “permanent establishment” & “qualifying investor” - “foreign partnership”

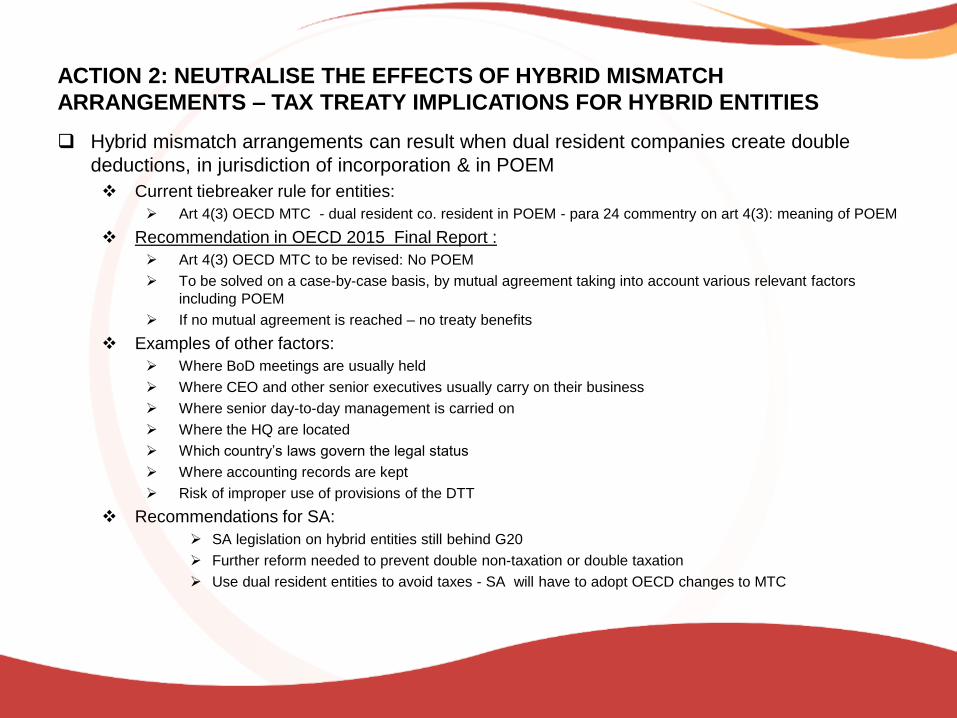

ACTION 2: NEUTRALISE THE EFFECTS OF HYBRID MISMATCH

ARRANGEMENTS – TAX TREATY IMPLICATIONS FOR HYBRID ENTITIES

Hybrid mismatch arrangements can result when dual resident companies create double

deductions, in jurisdiction of incorporation & in POEM

Current tiebreaker rule for entities:

Art 4(3) OECD MTC - dual resident co. resident in POEM - para 24 commentry on art 4(3): meaning of POEM

Recommendation in OECD 2015 Final Report :

Art 4(3) OECD MTC to be revised: No POEM

To be solved on a case-by-case basis, by mutual agreement taking into account various relevant factors

including POEM

If no mutual agreement is reached – no treaty benefits

Examples of other factors:

Where BoD meetings are usually held

Where CEO and other senior executives usually carry on their business

Where senior day-to-day management is carried on

Where the HQ are located

Which country’s laws govern the legal status

Where accounting records are kept

Risk of improper use of provisions of the DTT

Recommendations for SA:

SA legislation on hybrid entities still behind G20

Further reform needed to prevent double non-taxation or double taxation

Use dual resident entities to avoid taxes - SA will have to adopt OECD changes to MTC

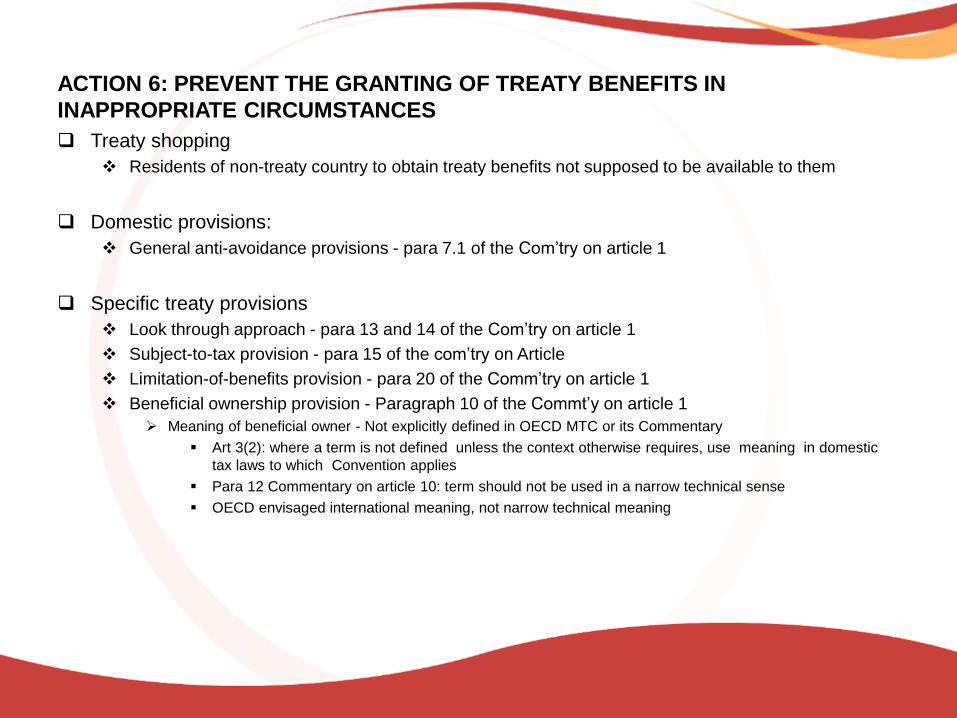

ACTION 6: PREVENT THE GRANTING OF TREATY BENEFITS IN

INAPPROPRIATE CIRCUMSTANCES

Treaty shopping

Residents of non-treaty country to obtain treaty benefits not supposed to be available to them

Domestic provisions:

General anti-avoidance provisions - para 7.1 of the Com’try on article 1

Specific treaty provisions

Look through approach - para 13 and 14 of the Com’try on article 1

Subject-to-tax provision - para 15 of the com’try on Article

Limitation-of-benefits provision - para 20 of the Comm’try on article 1

Beneficial ownership provision - Paragraph 10 of the Commt’y on article 1

Meaning of beneficial owner - Not explicitly defined in OECD MTC or its Commentary

Art 3(2): where a term is not defined unless the context otherwise requires, use meaning in domestic

tax laws to which Convention applies

Para 12 Commentary on article 10: term should not be used in a narrow technical sense

OECD envisaged international meaning, not narrow technical meaning

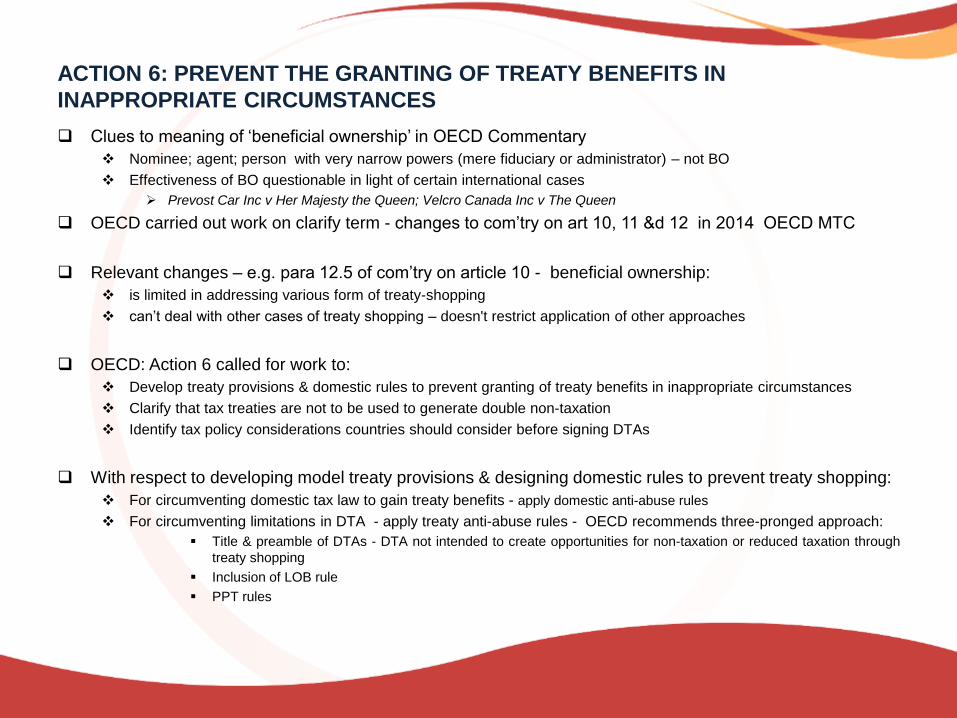

ACTION 6: PREVENT THE GRANTING OF TREATY BENEFITS IN

INAPPROPRIATE CIRCUMSTANCES

Clues to meaning of ‘beneficial ownership’ in OECD Commentary

Nominee; agent; person with very narrow powers (mere fiduciary or administrator) – not BO

Effectiveness of BO questionable in light of certain international cases

Prevost Car Inc v Her Majesty the Queen; Velcro Canada Inc v The Queen

OECD carried out work on clarify term - changes to com’try on art 10, 11 &d 12 in 2014 OECD MTC

Relevant changes – e.g. para 12.5 of com’try on article 10 - beneficial ownership:

is limited in addressing various form of treaty-shopping

can’t deal with other cases of treaty shopping – doesn't restrict application of other approaches

OECD: Action 6 called for work to:

Develop treaty provisions & domestic rules to prevent granting of treaty benefits in inappropriate circumstances

Clarify that tax treaties are not to be used to generate double non-taxation

Identify tax policy considerations countries should consider before signing DTAs

With respect to developing model treaty provisions & designing domestic rules to prevent treaty shopping:

For circumventing domestic tax law to gain treaty benefits - apply domestic anti-abuse rules

For circumventing limitations in DTA - apply treaty anti-abuse rules - OECD recommends three-pronged approach:

Title & preamble of DTAs - DTA not intended to create opportunities for non-taxation or reduced taxation through

treaty shopping

Inclusion of LOB rule

PPT rules

ACTION 6: PREVENT THE GRANTING OF TREATY BENEFITS IN

INAPPROPRIATE CIRCUMSTANCES

Examples of treaty shopping in South Africa:

Companies registered in Mauritius under Global Business Licenses 1

Mauritius’ extensive tax treaty network - investors use Mauritius as an intermediary to invest in

Africa

Conduit companies in low tax countries (Netherlands/Switzerland) - used to dispose

assets in African countries

Low interest & dividend withholding tax rates in treaties with Netherlands & Switzerland - treaty

shopping

Tax sparing provisions in African tax treaties encourage treaty shopping

Developed countries amend their taxation of foreign source income to allow their residents who

invest in developing countries to retain advantages of tax incentives provided by those

countries

Generous tax sparing credits in DTAs can encourage treaty shopping

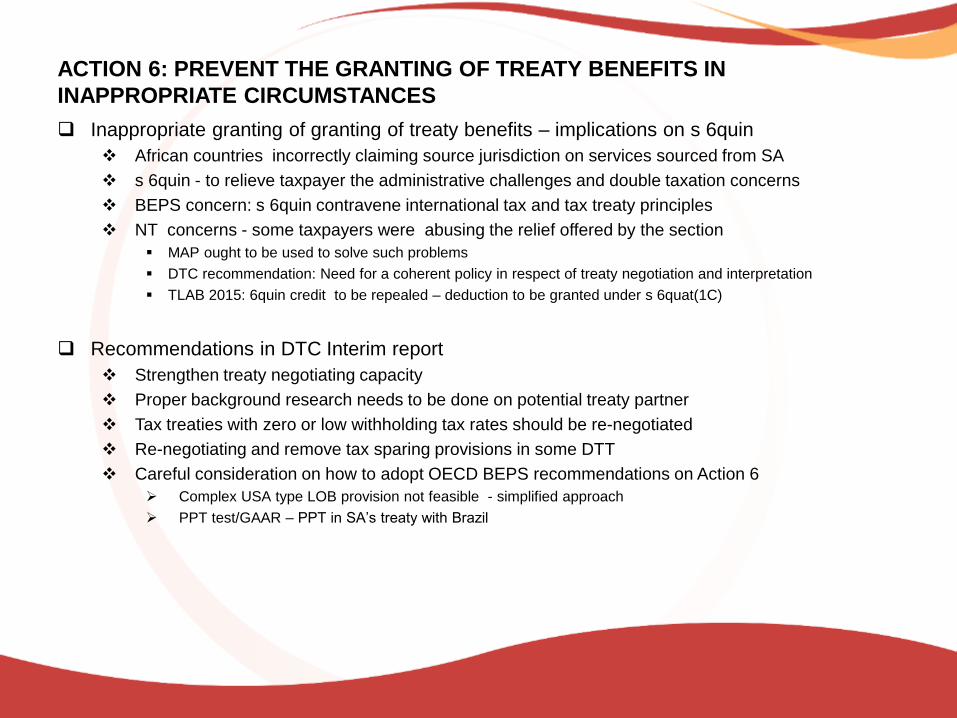

ACTION 6: PREVENT THE GRANTING OF TREATY BENEFITS IN

INAPPROPRIATE CIRCUMSTANCES

Inappropriate granting of granting of treaty benefits – implications on s 6quin

African countries incorrectly claiming source jurisdiction on services sourced from SA

s 6quin - to relieve taxpayer the administrative challenges and double taxation concerns

BEPS concern: s 6quin contravene international tax and tax treaty principles

NT concerns - some taxpayers were abusing the relief offered by the section

MAP ought to be used to solve such problems

DTC recommendation: Need for a coherent policy in respect of treaty negotiation and interpretation

TLAB 2015: 6quin credit to be repealed – deduction to be granted under s 6quat(1C)

Recommendations in DTC Interim report

Strengthen treaty negotiating capacity

Proper background research needs to be done on potential treaty partner

Tax treaties with zero or low withholding tax rates should be re-negotiated

Re-negotiating and remove tax sparing provisions in some DTT

Careful consideration on how to adopt OECD BEPS recommendations on Action 6

Complex USA type LOB provision not feasible - simplified approach

PPT test/GAAR – PPT in SA’s treaty with Brazil

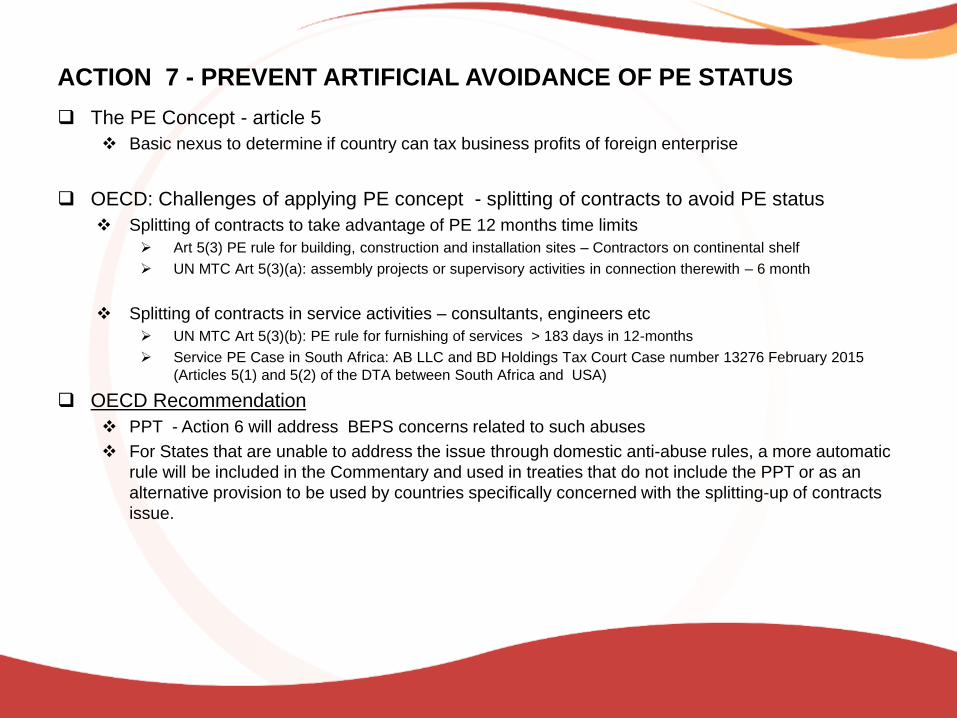

ACTION 7 - PREVENT ARTIFICIAL AVOIDANCE OF PE STATUS

The PE Concept - article 5

Basic nexus to determine if country can tax business profits of foreign enterprise

OECD: Challenges of applying PE concept - splitting of contracts to avoid PE status

Splitting of contracts to take advantage of PE 12 months time limits

Art 5(3) PE rule for building, construction and installation sites – Contractors on continental shelf

UN MTC Art 5(3)(a): assembly projects or supervisory activities in connection therewith – 6 month

Splitting of contracts in service activities – consultants, engineers etc

UN MTC Art 5(3)(b): PE rule for furnishing of services > 183 days in 12-months

Service PE Case in South Africa: AB LLC and BD Holdings Tax Court Case number 13276 February 2015

(Articles 5(1) and 5(2) of the DTA between South Africa and USA)

OECD Recommendation

PPT - Action 6 will address BEPS concerns related to such abuses

For States that are unable to address the issue through domestic anti-abuse rules, a more automatic

rule will be included in the Commentary and used in treaties that do not include the PPT or as an

alternative provision to be used by countries specifically concerned with the splitting-up of contracts

issue.

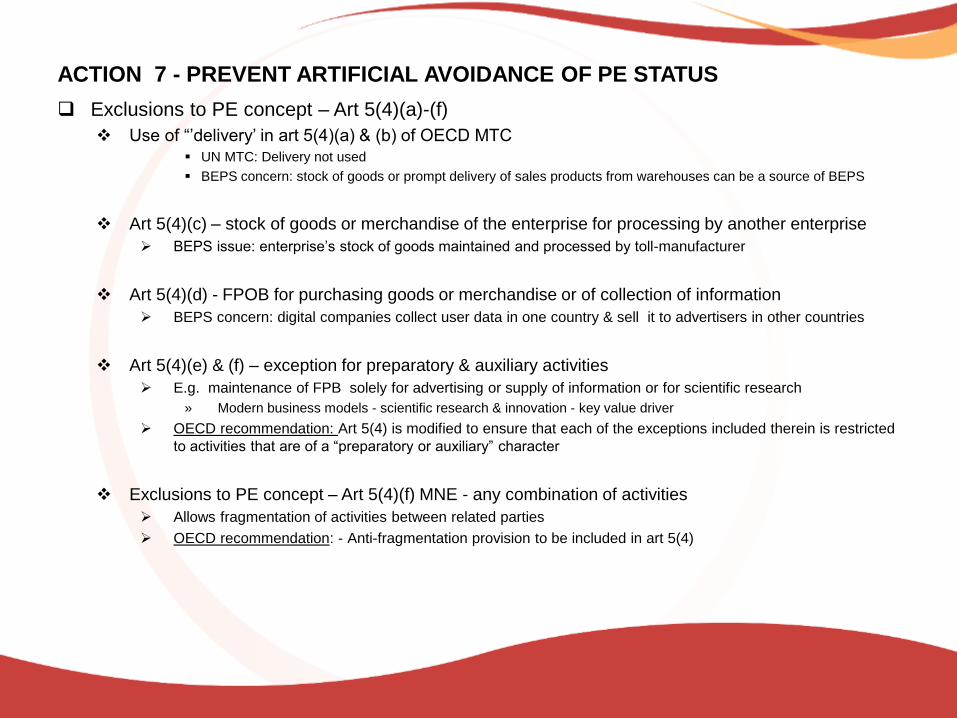

ACTION 7 - PREVENT ARTIFICIAL AVOIDANCE OF PE STATUS

Exclusions to PE concept – Art 5(4)(a)-(f)

Use of “’delivery’ in art 5(4)(a) & (b) of OECD MTC

UN MTC: Delivery not used

BEPS concern: stock of goods or prompt delivery of sales products from warehouses can be a source of BEPS

Art 5(4)(c) – stock of goods or merchandise of the enterprise for processing by another enterprise

BEPS issue: enterprise’s stock of goods maintained and processed by toll-manufacturer

Art 5(4)(d) - FPOB for purchasing goods or merchandise or of collection of information

BEPS concern: digital companies collect user data in one country & sell it to advertisers in other countries

Art 5(4)(e) & (f) – exception for preparatory & auxiliary activities

E.g. maintenance of FPB solely for advertising or supply of information or for scientific research

» Modern business models - scientific research & innovation - key value driver

OECD recommendation: Art 5(4) is modified to ensure that each of the exceptions included therein is restricted

to activities that are of a “preparatory or auxiliary” character

Exclusions to PE concept – Art 5(4)(f) MNE - any combination of activities

Allows fragmentation of activities between related parties

OECD recommendation: - Anti-fragmentation provision to be included in art 5(4)

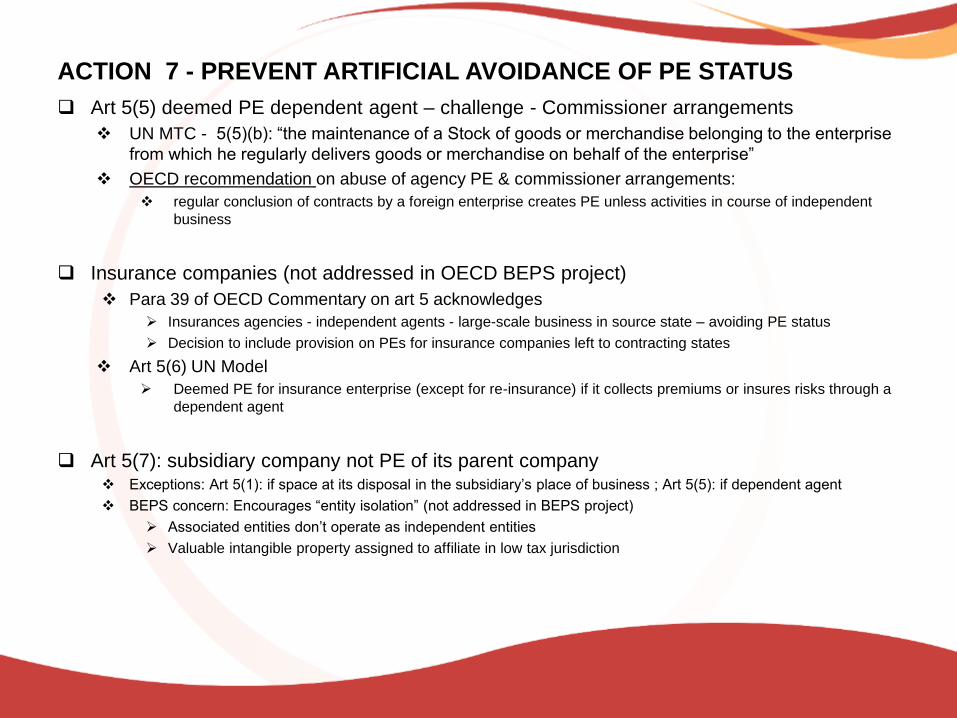

ACTION 7 - PREVENT ARTIFICIAL AVOIDANCE OF PE STATUS

Art 5(5) deemed PE dependent agent – challenge - Commissioner arrangements

UN MTC - 5(5)(b): “the maintenance of a Stock of goods or merchandise belonging to the enterprise

from which he regularly delivers goods or merchandise on behalf of the enterprise”

OECD recommendation on abuse of agency PE & commissioner arrangements:

regular conclusion of contracts by a foreign enterprise creates PE unless activities in course of independent

business

Insurance companies (not addressed in OECD BEPS project)

Para 39 of OECD Commentary on art 5 acknowledges

Insurances agencies - independent agents - large-scale business in source state – avoiding PE status

Decision to include provision on PEs for insurance companies left to contracting states

Art 5(6) UN Model

Deemed PE for insurance enterprise (except for re-insurance) if it collects premiums or insures risks through a

dependent agent

Art 5(7): subsidiary company not PE of its parent company Exceptions: Art 5(1): if space at its disposal in the subsidiary’s place of business ; Art 5(5): if dependent agent

BEPS concern: Encourages “entity isolation” (not addressed in BEPS project)

Associated entities don’t operate as independent entities

Valuable intangible property assigned to affiliate in low tax jurisdiction

ACTION 7 - PREVENT ARTIFICIAL AVOIDANCE OF PE STATUS

PEs, BEPS & the digital economy

PE concept based on physical presence as the primary basis for taxation

Nowadays - heavy involvement in economic life of another country, without taxable presence

Current OECD guidance in Com’try in art 5:

Internet website - intangible property - not PE

Location of computer equipment may constitute a PE - requirements of art 5 must be met

Server operated by enterprise – PE -

Hosting enterprise’s website on server of ISP – not at disposal of enterprise - ISP are independent

agents:

OECD BEPS concerns: Taking advantage of exclusions to PE concept

Art 5(4)(b): Maintenance of stock of goods solely for purpose of storage, display or delivery

digital companies maintain extensive inventory in target country - delivery of products to customers from a local

ware house that is not under its control - avoiding PE status

Art 5(4)(d) - Maintenance of FPB solely for collection of information for the enterprise

digital companies collect user data in one country and sell it to advertisers in other countries

Concern: previously preparatory or auxiliary activities nowadays core business activities

Solution: Art 5(4) to be modified - each of exception is restricted to activities of a “preparatory or auxiliary”

character

ACTION 7 - PREVENT ARTIFICIAL AVOIDANCE OF PE STATUS

Addressing avoidance of PE status in SA Previously tax policy - emphasis on outward bound investments more than inward bound

Risk: non-resident temporary activities – consultants, engineering services

• Service PE Tax Court Case in South Africa: AB LLC and BD Holdings Case number 13276 February 2015

(Articles 5(1) and 5(2) of the DTA between SA & USA) – company created PE in SA.

Risk: Non-residents preparatory or auxiliary activities - representative offices

Non-residents required to submit tax returns for trade carried on through PE in SA

Lack of data on inbound flows - little evidence indicating tax abuse.

SARS is now working hard to determine when a PE exists

Tax treatment of branches - art 24 discrimination issues – BEPS concerns

BEPS & TAX TREATIES: TRANFER PRICING

BEPS Action 8, 9 & 10 require TP out comes to be in line with value creation

To prevent TP, OECD recommends ALP - Art 9

OECD: Although ALP effectively & efficiently allocates income of MNE, in some instances MNE misapply the rules

to separate income from economic activities that produce income & shift it low-tax jurisdictions

Action 8: develop rules to prevent BEPS resulting from moving intangibles among MNE

group members - Chapters I, II & VI - OECD Transfer Pricing Guidelines revised Clarifies definition of intangibles

Identifies transactions involving intangibles

Determination of arm’s length conditions for transactions involving intangibles

Distinguish intangibles from location savings & other local market features

OECD recommendation in final 2015 report:

legal ownership alone does not necessarily generate a right to all (or indeed any) of the return that is generated by the

exploitation of the intangible.

The group companies performing important functions, controlling economically significant risks and contributing

assets, as determined through the accurate delineation of the actual transaction, will be entitled to an appropriate

return reflecting the value of their contributions

ACTION PLANS 9: ASSURE TRANSFER PRICING OUTCOMES ARE IN LINE

WITH VALUE CREATION WITH REGARD TO RISKS AND CAPITAL

Action 10: develop rules to prevent BEPS that result from transferring risks among,

or allocating excessive capital to, group members

OECD recommendation in its final report:

Revised guidance: In the situation where a capital-rich member of the group provides

funding but performs few activities

If the associated enterprise does not in fact control the financial risks associated with its funding

(for example because it just provides the money when it is asked to do so, without any

assessment of whether the party receiving the money is creditworthy), it will not be allocated the

profits associated with the financial risks and will be entitled to no more than a risk-free return, or

less if, for example, the transaction is not commercially rational and therefore the guidance on

non-recognition applies.

BEPS AND TAX TREATIES IN AFIRCA: ACTION PLAN 10: ASSURE THAT

TRANSFER PRICING OUTCOMES ARE IN LINE WITH VALUE

CREATION/OTHER HIGH-RISK TRANSACTIONS

Action 10 requires countries to adopting TP rules that:

clarify the circumstances in which transactions can be re-characterised

clarify the application of transfer pricing methods, in particular profit splits, in the context of

global value chains

provide protection against common types of base eroding payments, such as management fees

and head office expenses

Action 10 base eroding payments in Africa: Management fees

MNE keep claiming deductions for management, technical & service fees

Responses to the challenge of base eroding management fees Treaties with articles on services, management & technical fees

Deviating from OECD & UN MTC – not addressed in OECD BEPS project

No standard way of drafting these articles - creates uncertainties

OECD countries oppose such article – prefer PE taxation under art 5 and 7 or “fixed base” – art 14 UN MTC

2012: UN proposed new article on technical services fees

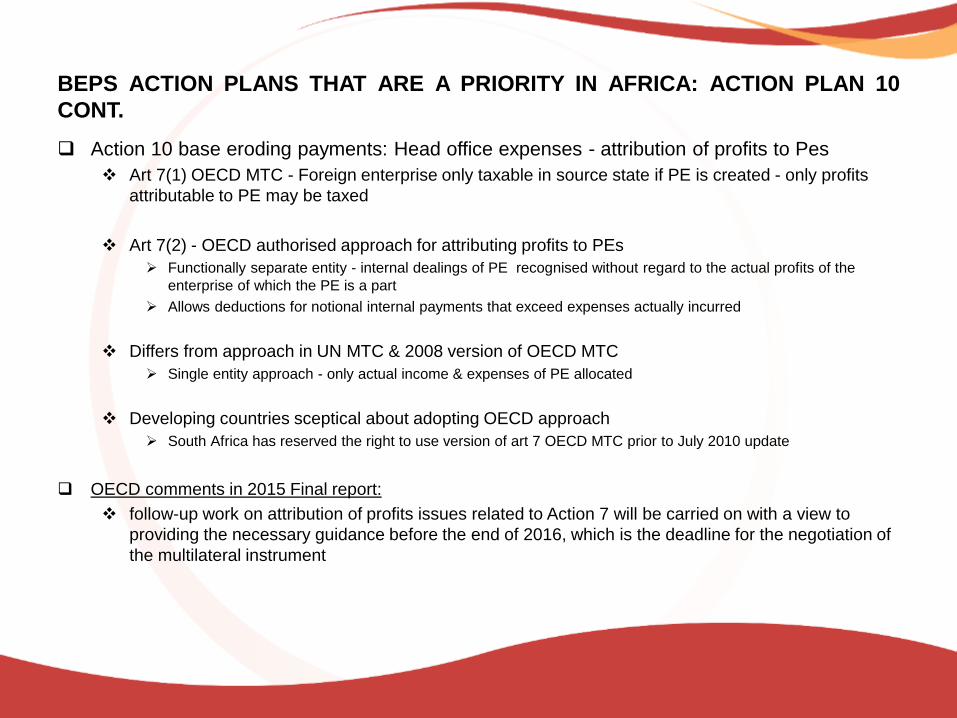

BEPS ACTION PLANS THAT ARE A PRIORITY IN AFRICA: ACTION PLAN 10

CONT.

Action 10 base eroding payments: Head office expenses - attribution of profits to Pes

Art 7(1) OECD MTC - Foreign enterprise only taxable in source state if PE is created - only profits

attributable to PE may be taxed

Art 7(2) - OECD authorised approach for attributing profits to PEs

Functionally separate entity - internal dealings of PE recognised without regard to the actual profits of the

enterprise of which the PE is a part

Allows deductions for notional internal payments that exceed expenses actually incurred

Differs from approach in UN MTC & 2008 version of OECD MTC

Single entity approach - only actual income & expenses of PE allocated

Developing countries sceptical about adopting OECD approach

South Africa has reserved the right to use version of art 7 OECD MTC prior to July 2010 update

OECD comments in 2015 Final report:

follow-up work on attribution of profits issues related to Action 7 will be carried on with a view to

providing the necessary guidance before the end of 2016, which is the deadline for the negotiation of

the multilateral instrument

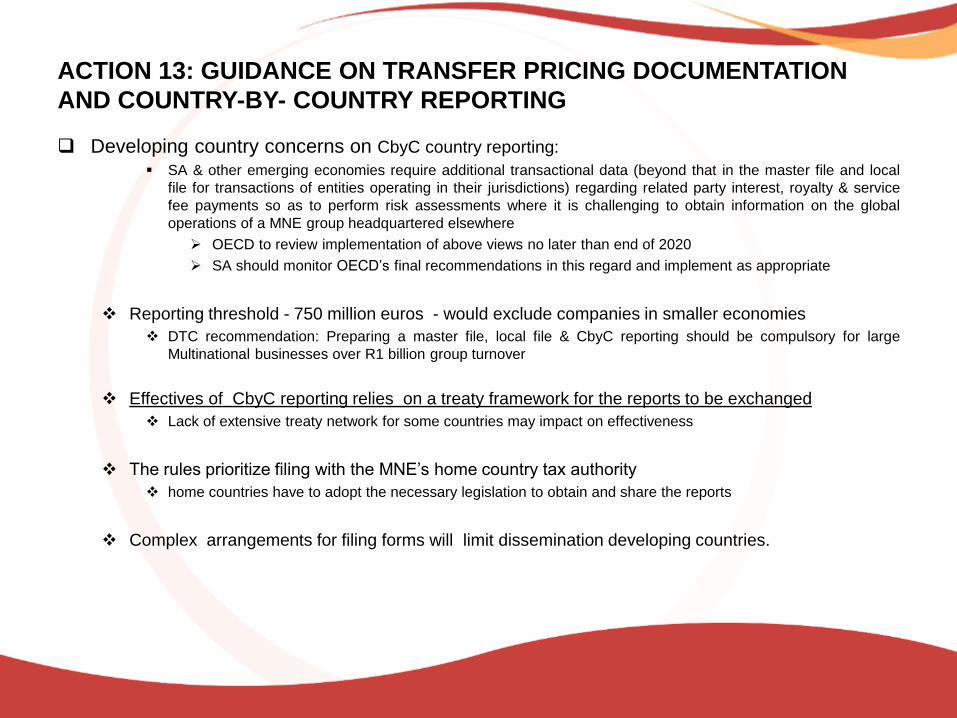

ACTION 13: GUIDANCE ON TRANSFER PRICING DOCUMENTATION AND

COUNTRY-BY- COUNTRY REPORTING – TREATY IMPLICATIONS

OECD: Enhancing transparency for tax administrations by providing them with adequate information to

conduct transfer pricing risk assessments & examinations is essential to preventing BEPS

Chapter V Transfer Pricing Guidelines revised - sets out objectives of transfer pricing documentation

rules

To achieve these objectiveness: countries to follow a three-tiered documentation structure consisting

of:

A master file

containing standardised information relevant for all MNE group members

A local file

referring specifically to material transactions of the local taxpayer

A country-by-country report

containing information on global allocation of MNE’s income & taxes paid together with

certain indicators of the location of economic activity within the MNE group

Guidelines on compliance matters

ACTION 13: GUIDANCE ON TRANSFER PRICING DOCUMENTATION

AND COUNTRY-BY- COUNTRY REPORTING

Developing country concerns on CbyC country reporting:

SA & other emerging economies require additional transactional data (beyond that in the master file and local

file for transactions of entities operating in their jurisdictions) regarding related party interest, royalty & service

fee payments so as to perform risk assessments where it is challenging to obtain information on the global

operations of a MNE group headquartered elsewhere

OECD to review implementation of above views no later than end of 2020

SA should monitor OECD’s final recommendations in this regard and implement as appropriate

Reporting threshold - 750 million euros - would exclude companies in smaller economies

DTC recommendation: Preparing a master file, local file & CbyC reporting should be compulsory for large

Multinational businesses over R1 billion group turnover

Effectives of CbyC reporting relies on a treaty framework for the reports to be exchanged

Lack of extensive treaty network for some countries may impact on effectiveness

The rules prioritize filing with the MNE’s home country tax authority

home countries have to adopt the necessary legislation to obtain and share the reports

Complex arrangements for filing forms will limit dissemination developing countries.

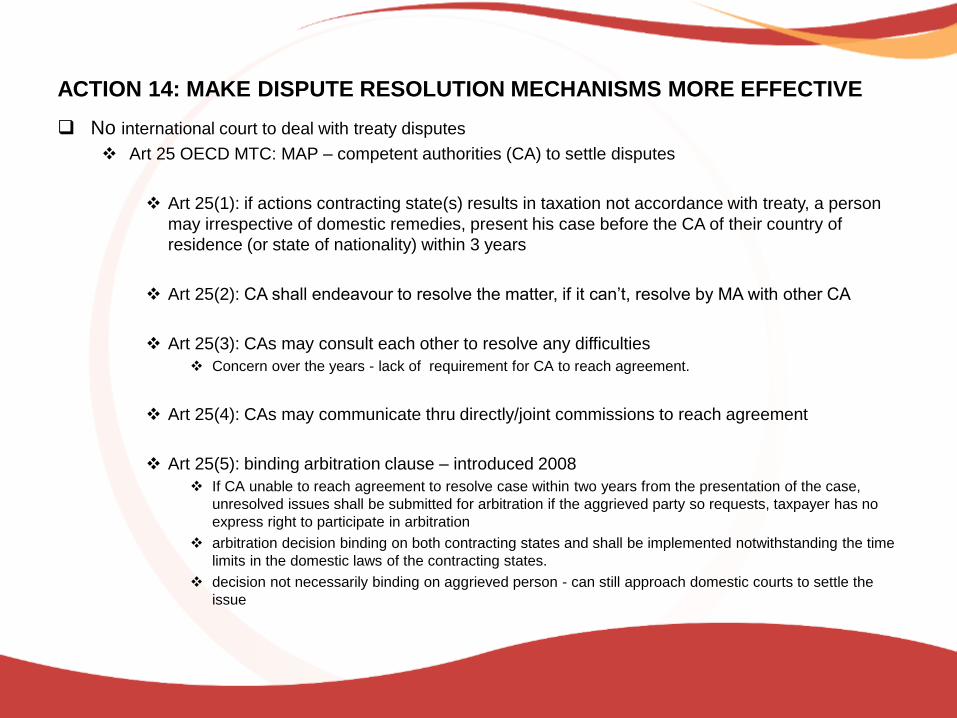

ACTION 14: MAKE DISPUTE RESOLUTION MECHANISMS MORE EFFECTIVE

No international court to deal with treaty disputes

Art 25 OECD MTC: MAP – competent authorities (CA) to settle disputes

Art 25(1): if actions contracting state(s) results in taxation not accordance with treaty, a person

may irrespective of domestic remedies, present his case before the CA of their country of

residence (or state of nationality) within 3 years

Art 25(2): CA shall endeavour to resolve the matter, if it can’t, resolve by MA with other CA

Art 25(3): CAs may consult each other to resolve any difficulties

Concern over the years - lack of requirement for CA to reach agreement.

Art 25(4): CAs may communicate thru directly/joint commissions to reach agreement

Art 25(5): binding arbitration clause – introduced 2008

If CA unable to reach agreement to resolve case within two years from the presentation of the case,

unresolved issues shall be submitted for arbitration if the aggrieved party so requests, taxpayer has no

express right to participate in arbitration

arbitration decision binding on both contracting states and shall be implemented notwithstanding the time

limits in the domestic laws of the contracting states.

decision not necessarily binding on aggrieved person - can still approach domestic courts to settle the

issue

ACTION 14: MAKE DISPUTE RESOLUTION MECHANISMS MORE EFFECTIVE

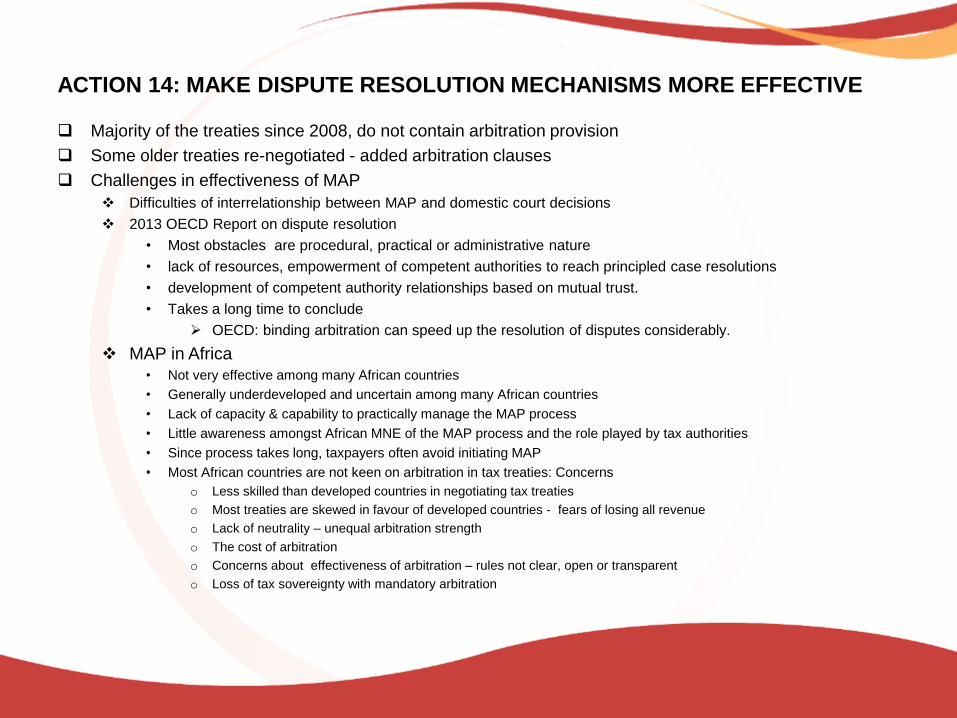

Majority of the treaties since 2008, do not contain arbitration provision

Some older treaties re-negotiated - added arbitration clauses

Challenges in effectiveness of MAP

Difficulties of interrelationship between MAP and domestic court decisions

2013 OECD Report on dispute resolution

• Most obstacles are procedural, practical or administrative nature

• lack of resources, empowerment of competent authorities to reach principled case resolutions

• development of competent authority relationships based on mutual trust.

• Takes a long time to conclude

OECD: binding arbitration can speed up the resolution of disputes considerably.

MAP in Africa

• Not very effective among many African countries

• Generally underdeveloped and uncertain among many African countries

• Lack of capacity & capability to practically manage the MAP process

• Little awareness amongst African MNE of the MAP process and the role played by tax authorities

• Since process takes long, taxpayers often avoid initiating MAP

• Most African countries are not keen on arbitration in tax treaties: Concerns

o Less skilled than developed countries in negotiating tax treaties

o Most treaties are skewed in favour of developed countries - fears of losing all revenue

o Lack of neutrality – unequal arbitration strength

o The cost of arbitration

o Concerns about effectiveness of arbitration – rules not clear, open or transparent

o Loss of tax sovereignty with mandatory arbitration

BEPS AND TAX TREATIES: ACTION 14: MAKE DISPUTE RESOLUTION

MECHANISMS MORE EFFECTIVE

OECD recommendations to strengthen the effectiveness & efficiency of MAP

Developed a set of minimum standards for the resolution of treaty-related disputes

Objectives - countries should ensure that:

treaty obligations related to MAP are fully implemented in good faith & that MAP cases are resolved in a

timely manner;

administrative processes promote the prevention & timely resolution of treaty-related disputes; and

taxpayers that meet the requirements of Article 25(1) can access MAP

The minimum standard is complemented by a set of MAP best practices

The OECD developed a framework for implementing the minimum standards

20 countries committed to mandatory binding MAP arbitration to guarantee that treaty

disputes will be resolved within a specified timeframe

Australia, Austria, Belgium, Canada, France, Germany, Ireland, Italy, Japan, Luxembourg, the

Netherlands, New Zealand, Norway, Poland, Slovenia, Spain, Sweden, Switzerland, the United

Kingdom and the United States

BEPS AND TAX TREATIES: ACTION 15: DEVELOP A MULTILATERAL

INSTRUMENT

Some solutions to BEPS require changes to DTAs

DTA network & their number would make updating burdensome, time

consuming & expensive

Action 15 - explore feasibility of multilateral instrument – effective as

simultaneous renegotiation of thousands of DTAs

Experience: Multilateral Convention on Administrative Assistance (OECD &

Council of Europe) amended by a Protocol in 2010 and opened all countries

In 2011, South Africa signed, but has not yet ratified the Multilateral Convention

Many developing counties have not benefited from the experience – administrative

capacity needed before admission - similar concerns for OECD multilateral

instrument

BEPS AND TAX TREATIES: ACTION 15 - MULTILATERAL INSTUMENT

Concerns of developing countries regarding the Multilateral instrument

Interests of developing may not be addressed in a multinational instrument.

OECD MTC favours capital exporting countries, UN MTC favours capital importing

countries

Experience could be gained through regional multinational treaties: ATAF, SADC & EAC

(yet to be finalised)

Caution:

IMF: developing countries should be cautious about tax treaties

OECD BEPS Action Plan 6 - OECD will “identify the tax policy considerations that

countries should consider before deciding to enter into a tax treaty with another country

South African

Revenue

Service(SARS)

Representatives

SARS Representatives

Nishana Gosai

Transfer Pricing

Manager

South Africa

Revenue Services

Sunita Manik

Group Executive at

the Large Business

Centre

South Africa

Revenue Services

Panel

Discussion and

Q&A

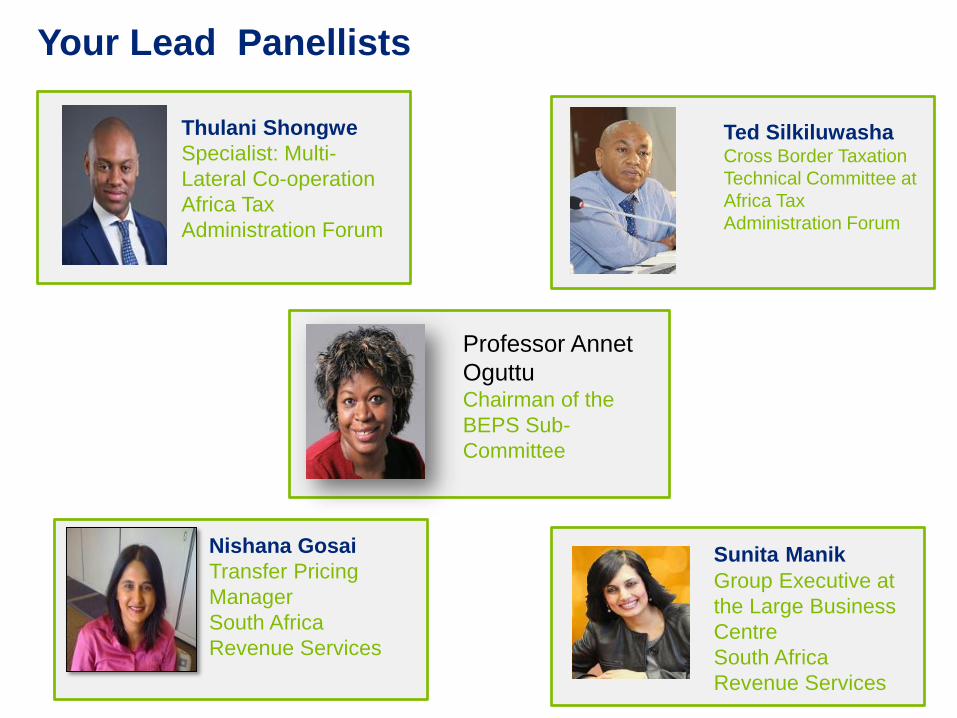

Your Lead Panellists

Professor Annet

Oguttu Chairman of the

BEPS Sub-

Committee

Thulani Shongwe

Specialist: Multi-

Lateral Co-operation

Africa Tax

Administration Forum

Nishana Gosai

Transfer Pricing

Manager

South Africa

Revenue Services

Sunita Manik

Group Executive at

the Large Business

Centre

South Africa

Revenue Services

Ted SilkiluwashaCross Border Taxation

Technical Committee at

Africa Tax

Administration Forum

Closing Remarks

Billy Joubert

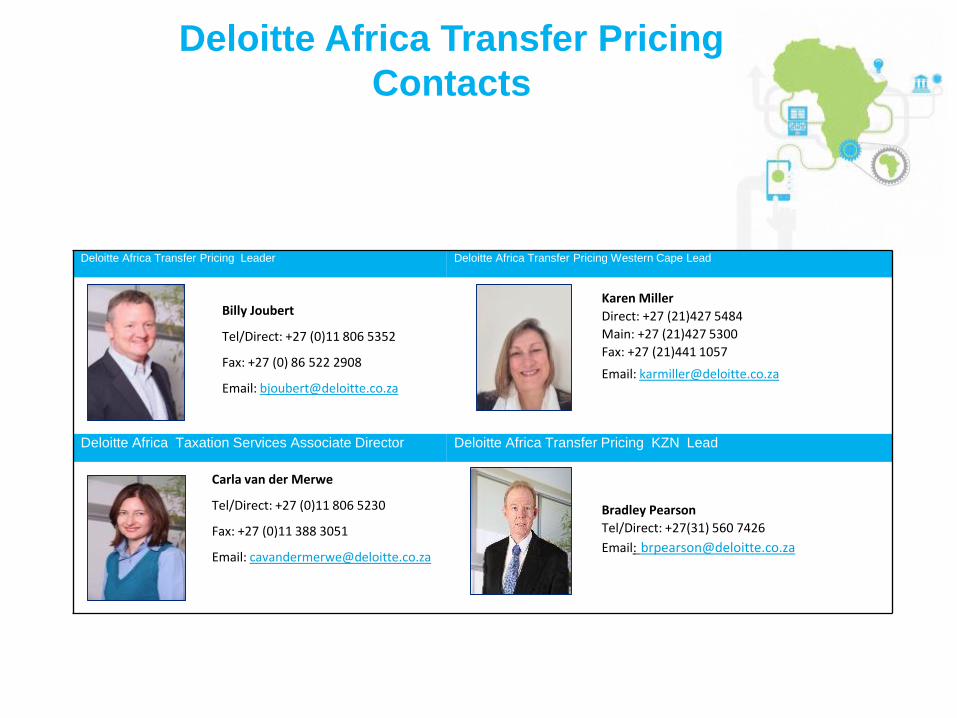

Deloitte Africa Transfer Pricing Leader Deloitte Africa Transfer Pricing Western Cape Lead

Billy Joubert

Tel/Direct: +27 (0)11 806 5352

Fax: +27 (0) 86 522 2908

Email: [email protected]

Karen Miller

Direct: +27 (21)427 5484

Main: +27 (21)427 5300

Fax: +27 (21)441 1057

Email: [email protected]

Deloitte Africa Taxation Services Associate Director Deloitte Africa Transfer Pricing KZN Lead

Carla van der Merwe

Tel/Direct: +27 (0)11 806 5230

Fax: +27 (0)11 388 3051

Email: [email protected]

Bradley Pearson

Tel/Direct: +27(31) 560 7426

Email: [email protected]

Deloitte Africa Transfer Pricing

Contacts

Top Related