Languages

Pages

Legal

IASA WisconsinStatutory Accounting 101March 24, 2015

Rich PullaraInsurance Solutions Specialist

Clearwater Analytics

Molly Petrowiak Insurance Team LeadClearwater Analytics

Agenda– Guiding SSAPs– GAAP and STAT Differences– Regulatory Reporting– It’s in the Details– Supplemental Investment Risk Interrogatories– Risk Based Capital– Other Schedules– SVO Designation Process

Statutory Accounting Principles

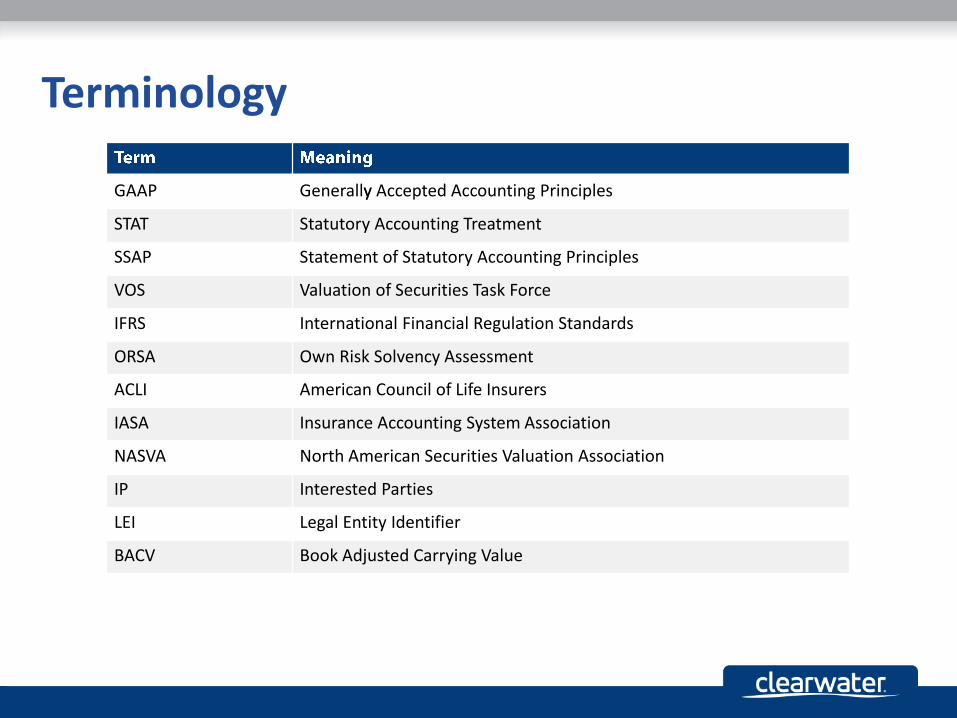

Terminology

GAAP Generallyy Accepted Accounting Principles

STAT Statutory Accounting Treatment

SSAP Statement of Statutory Accounting Principles

VOS Valuation of Securities Task Force

IFRS International Financial Regulation Standards

ORSA Own Risk Solvency Assessment

ACLI American Council of Life Insurers

IASA Insurance Accounting System Association

NASVA North American Securities Valuation Association

IP Interested Parties

LEI Legal Entity Identifier

BACV Book Adjusted Carrying Value

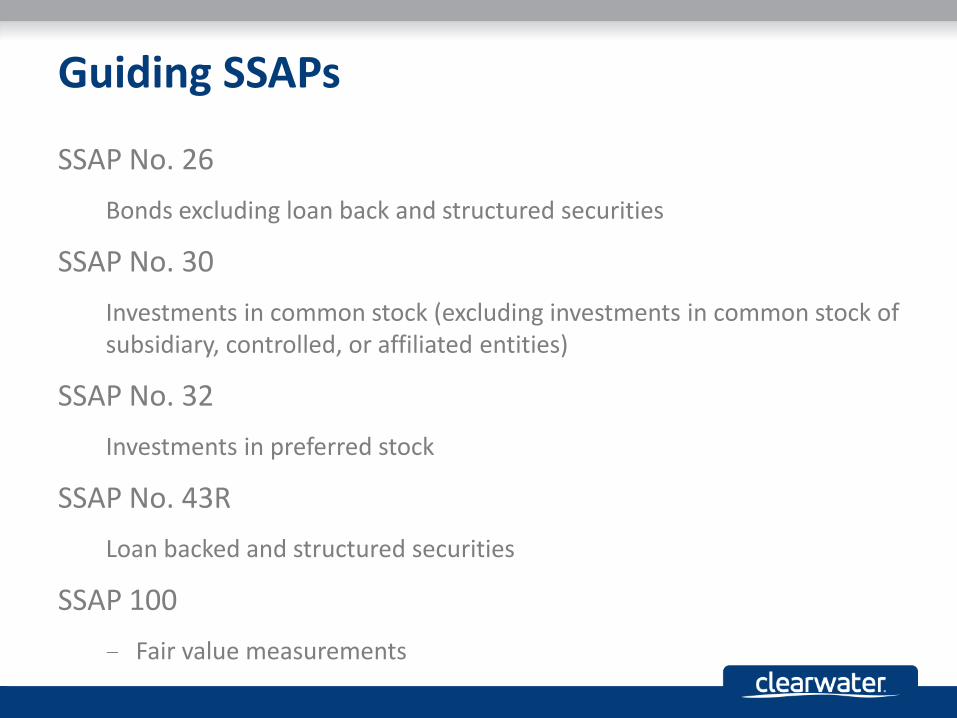

Guiding SSAPs

SSAP No. 26

Bonds excluding loan back and structured securities

SSAP No. 30

Investments in common stock (excluding investments in common stock of subsidiary, controlled, or affiliated entities)

SSAP No. 32

Investments in preferred stock

SSAP No. 43R

Loan backed and structured securities

SSAP 100

Fair value measurements

SSAP No. 26 – Bonds

Broad definition of bonds, excluding loan back and structured securities

– Any securities representing a creditor relationship, whereby this is a fixed schedule for one or more future payments

– U.S. treasury securities, U.S. government agency securities, municipal securities, corporate bonds, bank participations, convertible debt, CD with fixed schedule of payment, commercial paper, ETFs (that qualify for bond treatment), Class 1 bond mutual funds

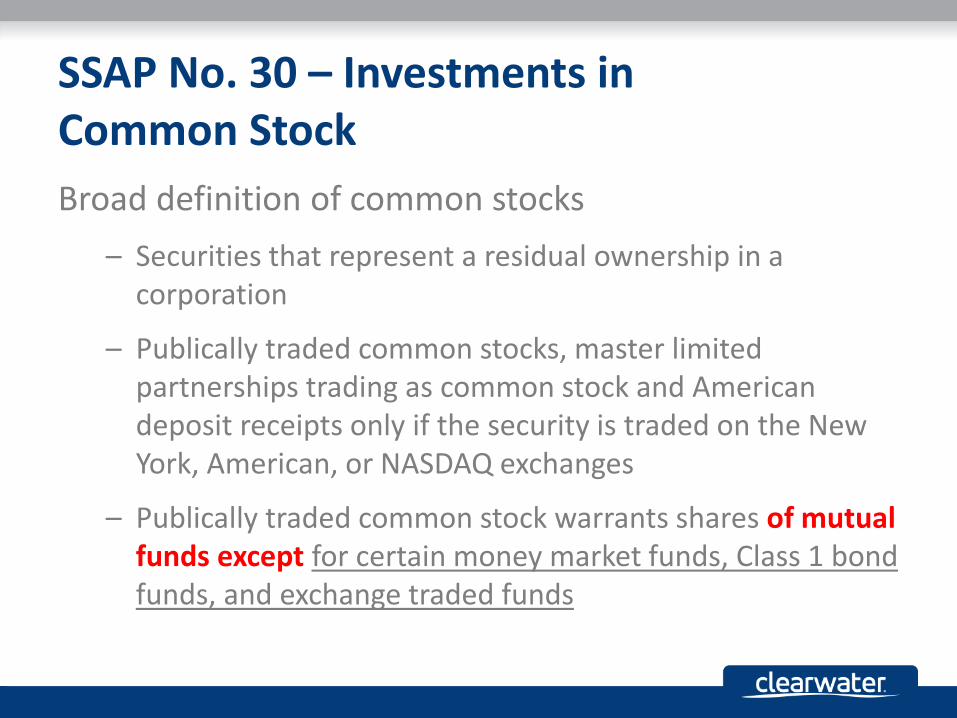

SSAP No. 30 – Investments in Common Stock

Broad definition of common stocks

– Securities that represent a residual ownership in a corporation

– Publically traded common stocks, master limited partnerships trading as common stock and American deposit receipts only if the security is traded on the New York, American, or NASDAQ exchanges

– Publically traded common stock warrants shares of mutual funds except for certain money market funds, Class 1 bond funds, and exchange traded funds

Mutual Funds

Mutual funds are typically common stock unless:

It’s a money market fund with U.S. direct obligations/full faith and credit exempt list on the Class 1 list

Bond mutual fund

U.S. Direct Obligations/Full Faith and Credit Exempt List

– Must maintain a MMK rating of AAA-m (S&P) or AAA-mf (Moody’s)

– Stable NAV of $1 per share

– Maximum of 7 day redemption

– 100% of assets in direct obligations of U.S. government or securities backed by U.S. government

– Class 1 list: same, except for 97% requirement

Bond Fund List

Highest credit ratings by NAIC CRPs

Must declare a dividend of investment income

No derivatives, leveraged notes, foreign currencies

SSAP No. 32 – Investments in Preferred Stock

Broad definition of preferred stocks

Any class or series of shares for which the holders have any preference, either as to payment of dividends or distribution of assets on liquidation over the holder of common stock

Redeemable preferred stock includes mandatory sinking fund preferred stock and payment-in-kin (PIK)

Perpetual preferred stock-nonredeemable and redeemable at the option of the issuer

SSAP No. 43R – Loan-Backed and Structured Securities

Loan-backed securities are securitized assets for which the payment of interest and principal is directly proportional to the payments received by the issuer from the underlying assets.

Structured securities are loan-backed securities that have been divided into two or more classes, for which the payment of interest and/or principal of any class of securities has been allocated disproportionately to payments received from the underlying assets.

SSAP No. 43R – Loan-Backed and Structured Securities Cont’d

Guidance on recording other-than-temporary-impairments (OTTI) on loan-backed and structured securities

SSAP No. 43R applies to all investments held by the reporting entity subsequent to September 30, 2009

Decision tree for determining OTTI for loan-backed securities

Additional SSAP effective 2010

Must be filed annually

Filed securities are modeled by 3rd parties

Modeling results are used to determine designation and valuation

PIMCO and BlackRock perform the modeling

SSAP No. 43R – Summary

GAAP and STAT Differences

STAT\GAAP Differences

GAAP

Reports on tax lot level

Can choose between constant yield and straight line amortization

Adjustments to amortization target date must be retrospective

Can choose fiscal year

STAT

Reports on position level

Must use constant yield amortization

Can choose retrospective or prospective adjustments to amortization target date

Fiscal period must be calendar year

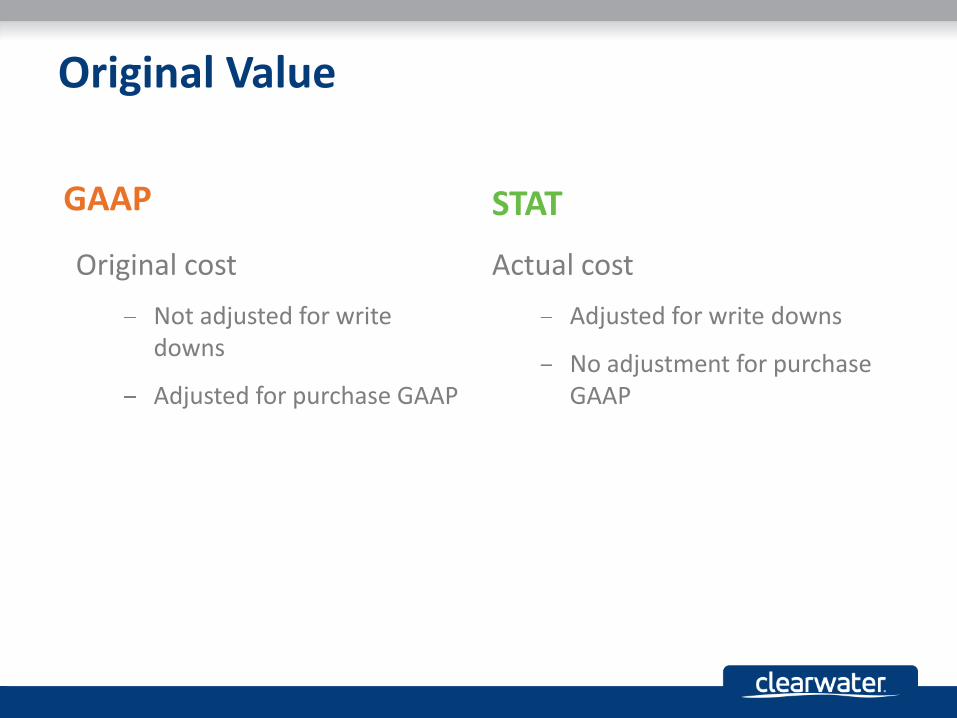

Original Value

GAAP

Original cost

Not adjusted for write downs

Adjusted for purchase GAAP

STAT

Actual cost

Adjusted for write downs

No adjustment for purchase GAAP

Book Adjusted Carrying Value

Represents either the Book Value or Market Value of Security based on Type of Insurance Company and Credit Quality of Security

Property & Casualty

– P&C holds only investment grade 1 and 2 at amortized cost

– 3 through 4 – lower of book or market value

• Life

– Life holds only investment grade 1 – 5 at amortized cost

– NAIC 6 – lower of book or market value

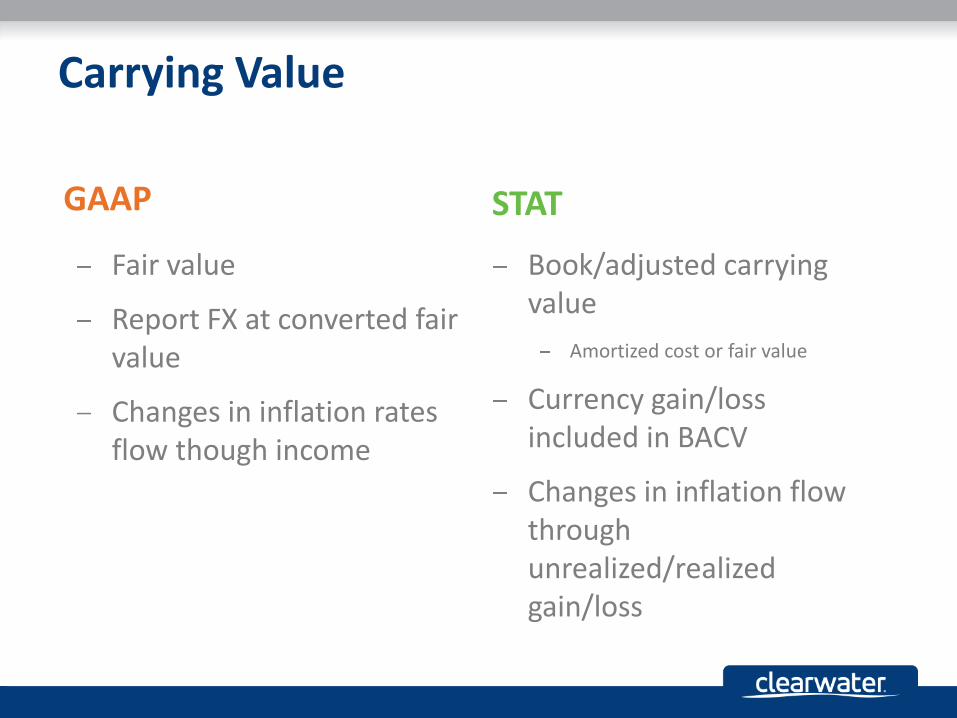

Carrying Value

GAAP

Fair value

Report FX at converted fair value

Changes in inflation rates flow though income

STAT

Book/adjusted carrying value

Amortized cost or fair value

Currency gain/loss included in BACV

Changes in inflation flow through unrealized/realized gain/loss

General Ledger Accounts

Balance Sheet Method

Due and accrued (BS)

Accrued interest

Interest income

Dividend income

Cash

Income Statement Method

Due and accrued (IS)Interest/dividend receivedPurchase accrued incomeSold accrued incomeChange in accrued income

Transferred in accrued incomeTransferred out accrued incomeChange in dividend income

Regulatory Reporting

Type of insurance companies

• Property and Casualty

• Life

• Health

• Title

• Fraternal

• Separate Accounts

• Yellow

• Blue

• Orange

• Pink

• Brown

• Green

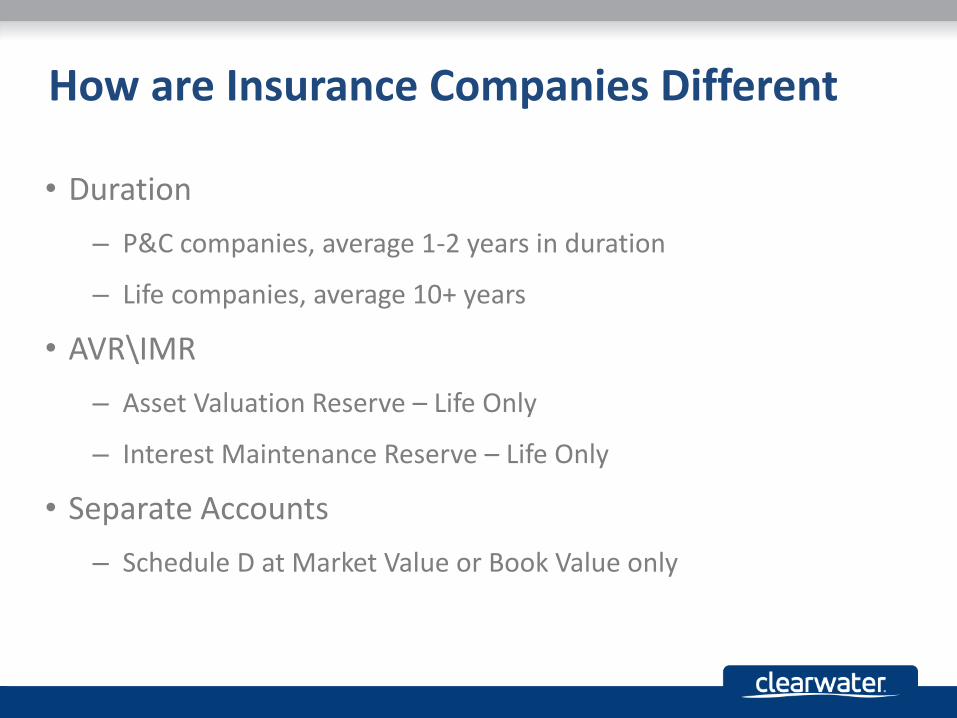

How are Insurance Companies Different

• Duration

– P&C companies, average 1-2 years in duration

– Life companies, average 10+ years

• AVR\IMR

– Asset Valuation Reserve – Life Only

– Interest Maintenance Reserve – Life Only

• Separate Accounts

– Schedule D at Market Value or Book Value only

Quarterly vs. Annual

Quarterly

– due 45 days after QE

– activity only

Annual

– due 60 days after QE

– include holdings

– Additional summary schedules

Investment Schedules

Statements are a combination of accounting and risk values

Some statements show CUSIP-level detail, while others show subtotals/totals

Everything is calculated on a lot level, but detailed schedules are always displayed by CUSIP/position level

Summary schedules show totals or grouped subtotals

What is a Schedule D?

Schedule D is a general term used by the insurance industry to describe the quarterly and annual statement investment-related schedules.

Schedule D is one of many types of investment schedules that insurance companies produce.

NAIC Naming Conventions

Schedule Description

Schedule A All Real Estate Owned

Schedule B Commercial Mortgage Loans

Schedule BA Other Long Term Assets

Schedule DPartPart 2 1 Part 2 2

Long Term BondsPreferredEquity

Schedule DA Short Term

Schedule DB Derivatives

Schedule E Cash,

Purpose of Investment Schedules

Holdings

Part 1: Main holdings report as of current period end

Part 2: Secondary holdings report as of current period end

Activity

Part 3: Acquisitions - anything that came in during the given period, such as buys, transfers, etc.

Part 4: Disposals - anything that went out during the given period, such as sells, pay downs, redemptions, etc.

Part 5: Acquired and fully disposed - any lot that came in and went out fully during the year

Purpose of Investment Schedules

Verification

All activity year-to-date

Summary Reports

Can be “as of” reports or spanning a specific period

Secret Schedule Decoder Ring

The vast majority of the time, you can tell what will be included in a report by the assigned letter and number of the report. For example:

What does the DA-1 show?

Short term investment holdings

What does the D-4 show?

Long term investment disposals

It’s in the details

Schedule D – Part 1

Reports on all long term bonds owned

General

Used to subtotal and total asset categories

Focused on

If security is backed by some kind of governmental body

Do the assets have underlying collateral

Specific

Sub-categories

All fixed income security’s specific classification/ category per NAIC guidelines

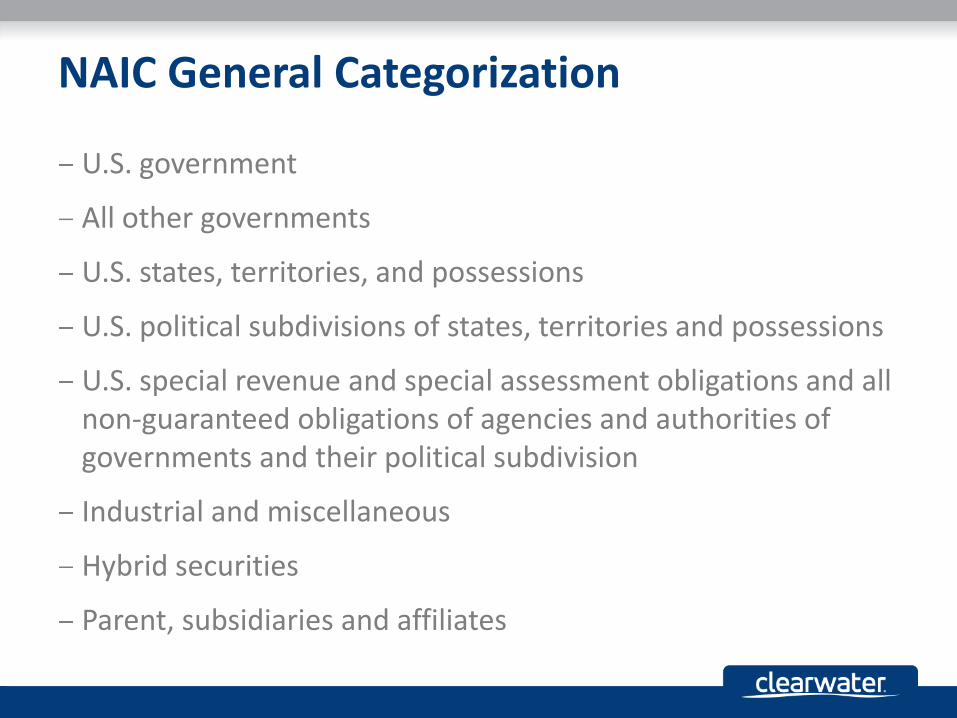

NAIC General Categorization

U.S. government

All other governments

U.S. states, territories, and possessions

U.S. political subdivisions of states, territories and possessions

U.S. special revenue and special assessment obligations and all non-guaranteed obligations of agencies and authorities of governments and their political subdivision

Industrial and miscellaneous

Hybrid securities

Parent, subsidiaries and affiliates

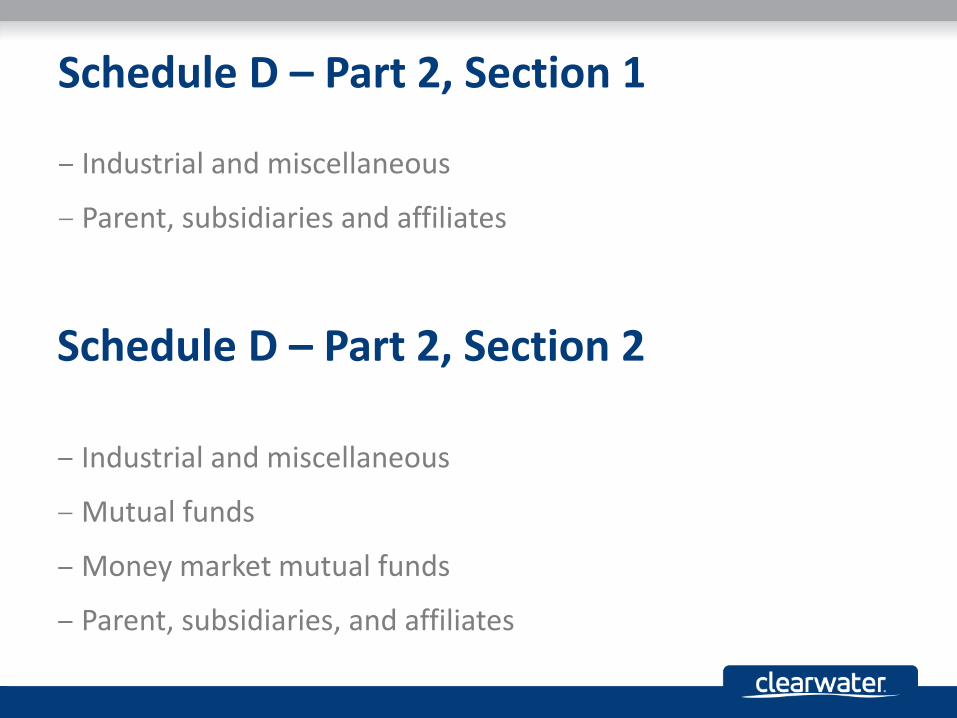

Schedule D – Part 2, Section 1

Industrial and miscellaneous

Parent, subsidiaries and affiliates

Schedule D – Part 2, Section 2

Industrial and miscellaneous

Mutual funds

Money market mutual funds

Parent, subsidiaries, and affiliates

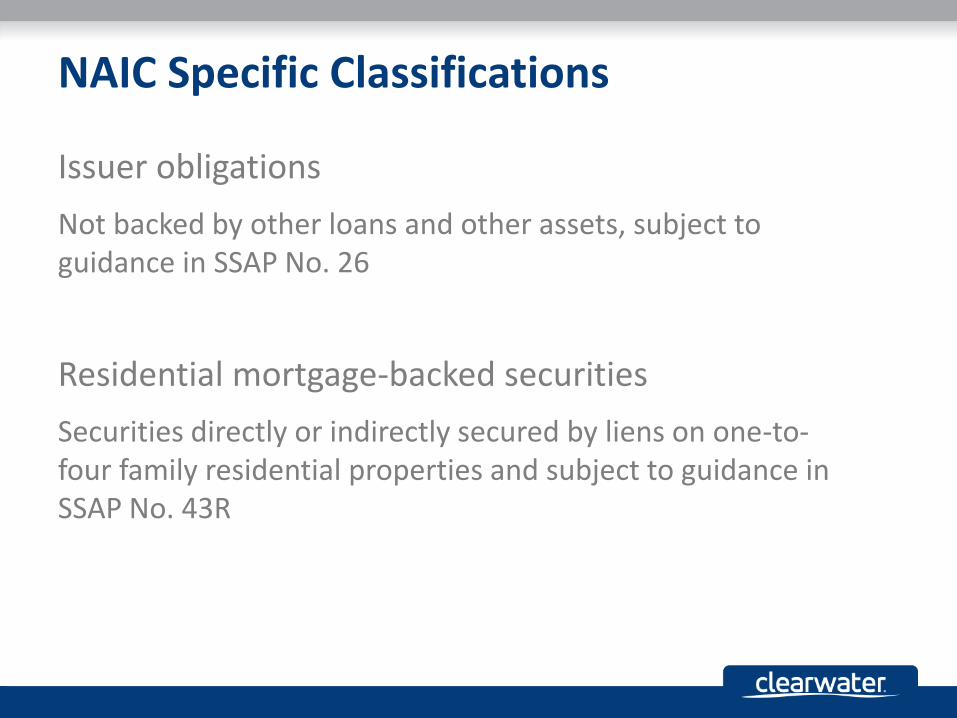

NAIC Specific Classifications

Issuer obligations

Not backed by other loans and other assets, subject to guidance in SSAP No. 26

Residential mortgage-backed securities

Securities directly or indirectly secured by liens on one-to-four family residential properties and subject to guidance in SSAP No. 43R

NAIC Specific Classifications

Commercial mortgage-backed securities

Securities directly or indirectly secured by a lien on one or more parcels of commercial real state with one or more structures located on the real estate and subject to SSAP No. 43R

Other loan-backed and structured securities

Securities subject to guidance in SSAP No. 43R not included in RMBS or CMBS above

Code Code

Code Description Code Description

* Class 1 Bond Mutual Funds S Certificates of Deposit

# Exchange Traded Funds & TBA

@ Principal STRIP Bonds or Other Zero Coupon Bonds

˄ Assets Bifurcated Between Separate Accounts

LS Loaned or Leased to Others RA Subject to Repurchase Agreement

RR Subject to Reverse Repurchase Agreement DR Dollar Repurchase Agreement

DRR Dollar Reverse Repurchase Agreement C Pledged as Collateral

CF Pledged as Collateral to FHLB DB Placed Under an Option Agreement

DBP Option Agreement Involving “Asset Transfers with Put Options”

R Restricted

RF FHLB Capital Stock SD Placed on Deposit with State or Other Regulatory Body

M Not Under Exclusive Control of the Reporting Entity

O Other

Discloses information on investments that are not under the exclusive control of the reporting entity

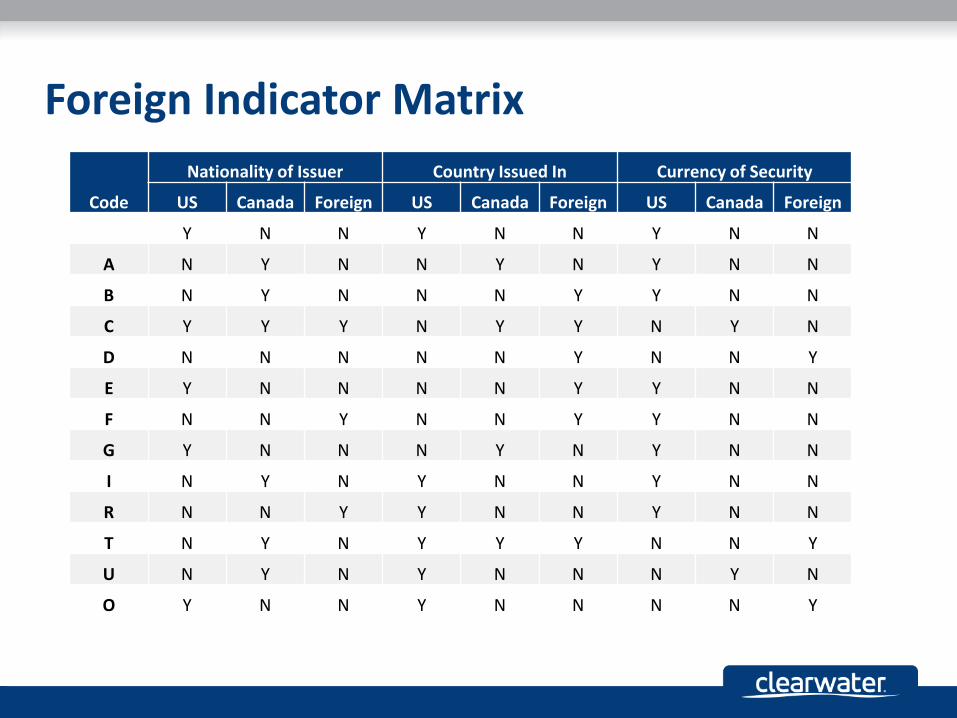

Foreign Indicator Matrix

Code

Nationality of Issuer Country Issued In Currency of Security

US Canada Foreign US Canada Foreign US Canada Foreign

Y N N Y N N Y N N

A N Y N N Y N Y N N

B N Y N N N Y Y N N

C Y Y Y N Y Y N Y N

D N N N N N Y N N Y

E Y N N N N Y Y N N

F N N Y N N Y Y N N

G Y N N N Y N Y N N

I N Y N Y N N Y N N

R N N Y Y N N Y N N

T N Y N Y Y Y N N Y

U N Y N Y N N N Y N

O Y N N Y N N N N Y

Foreign Indicator

A – Canadian securities issued in Canada and denominated in U.S. Dollars

B – Canadian securities issued in foreign country but denominated in U.S. Dollars

C – Securities denominated in Canadian currency

D – Foreign Securities that are denominated in a foreign currency (excluding Canadian)

E - US securities issued in a foreign country other than Canada denominated in U.S. Dollars

F – Securitas issued in a foreign country that are denominated in U.S. dollar

I – Canadian securities issued in U.S. and denominated in U.S. dollar

R – Foreign Securities issued in the U.S. and denominated in U.S. Dollars

T – Canadian securities denominated in any other foreign currency

U – Canadian securities issued in U.S. but denominated in Canadian currency

O – U.S. securities issued in U.S. but denominated in any foreign currency other than Canadian

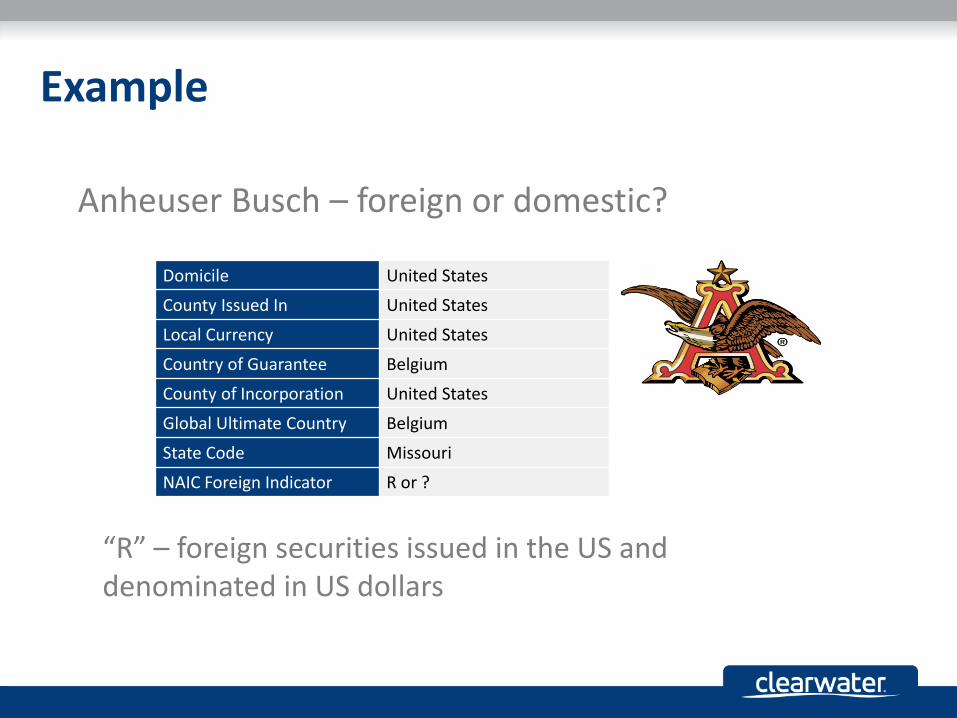

Example

“R” – foreign securities issued in the US and denominated in US dollars

Anheuser Busch – foreign or domestic?

Domicile United States

County Issued In United States

Local Currency United States

Country of Guarantee Belgium

County of Incorporation United States

Global Ultimate Country Belgium

State Code Missouri

NAIC Foreign Indicator R or ?

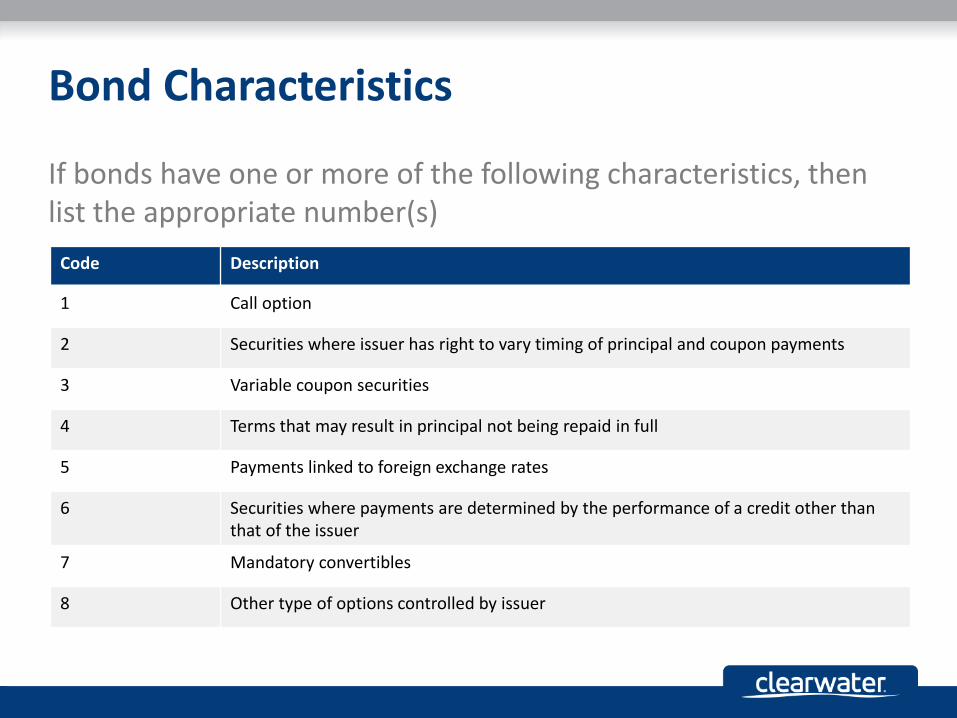

Bond Characteristics

If bonds have one or more of the following characteristics, then list the appropriate number(s)

Code Description

1 Call option

2 Securities where issuer has right to vary timing of principal and coupon payments

3 Variable coupon securities

4 Terms that may result in principal not being repaid in full

5 Payments linked to foreign exchange rates

6 Securities where payments are determined by the performance of a credit other than that of the issuer

7 Mandatory convertibles

8 Other type of options controlled by issuer

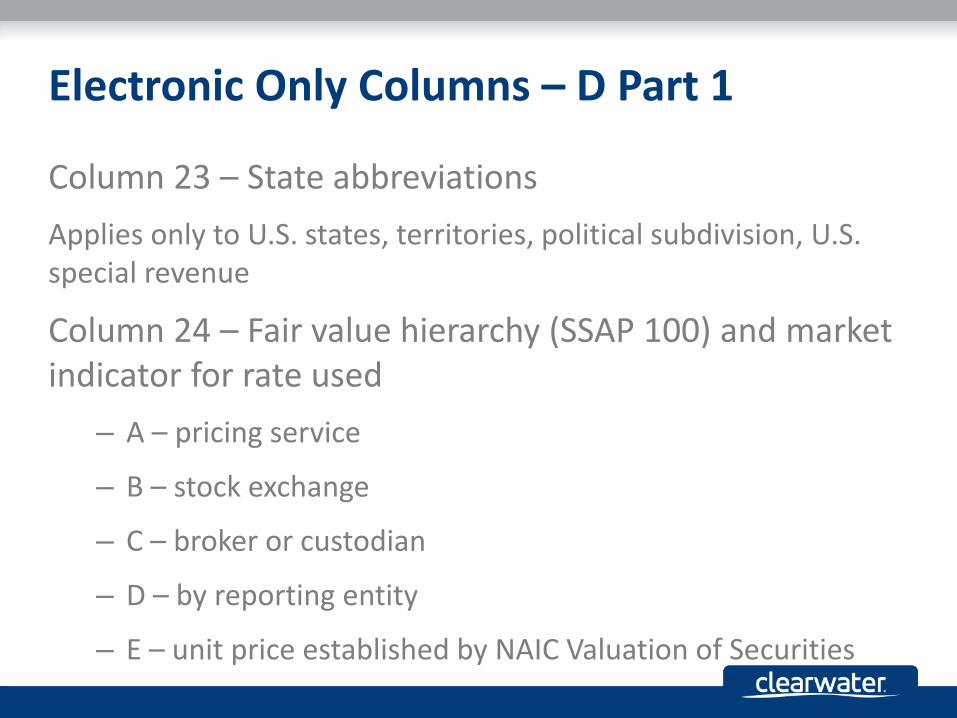

Electronic Only Columns – D Part 1

Column 23 – State abbreviations

Applies only to U.S. states, territories, political subdivision, U.S. special revenue

Column 24 – Fair value hierarchy (SSAP 100) and market indicator for rate used

– A – pricing service

– B – stock exchange

– C – broker or custodian

– D – by reporting entity

– E – unit price established by NAIC Valuation of Securities

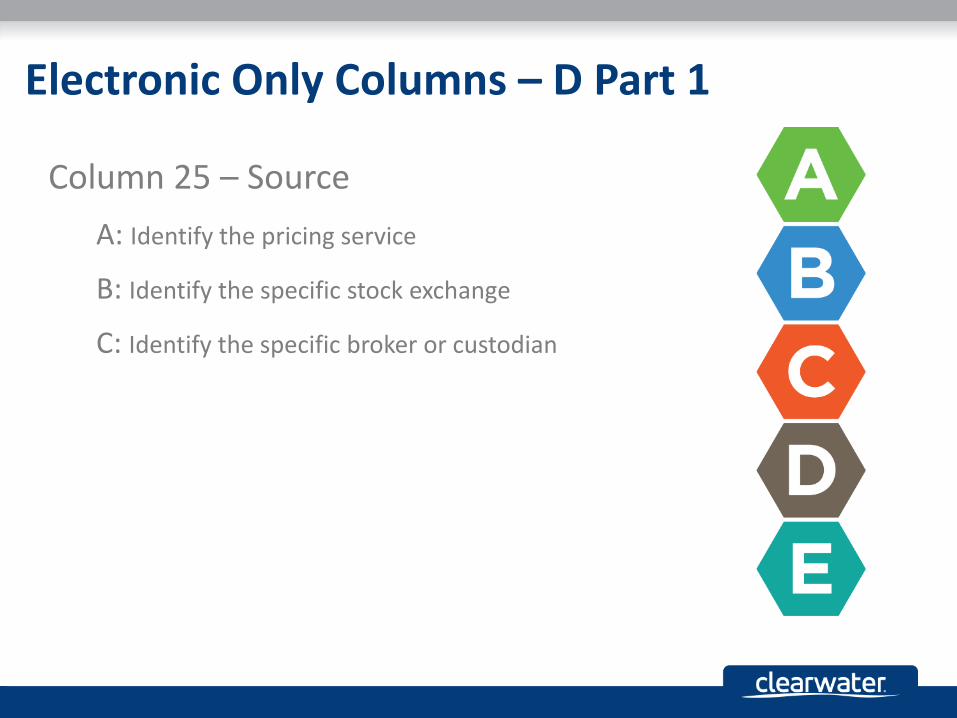

Electronic Only Columns – D Part 1

Column 25 – Source

A: Identify the pricing service

B: Identify the specific stock exchange

C: Identify the specific broker or custodian

Electronic Only Columns – D Part 1, cont.

Column 26: Collateral type

Identify collateral with code for RMBS, CMBS and other loan back and structured securities

Column 27: Call date

Column 28: Call price

Column 29: Effective date of maturity

Column 30: Legal entity identifier

BA – Other Long Term Assets

Used as a catch all for all asset classes

Invested assets not clearly or normally includable in any other invested asset schedule

High RBC charges

BA – Categories

Fix/variable interest rate investments that have underlying characteristics of bonds, mortgage loans, and other fixed income instruments

– Real estate

– Mortgage loans

– Surplus debentures

– Collateral loans

– Non-collateral loans

– Capital notes

– Tax credits

– Working capital finance investments

BA – Categories, cont.

Oil and gas production

Transportation equipment

Mineral rights

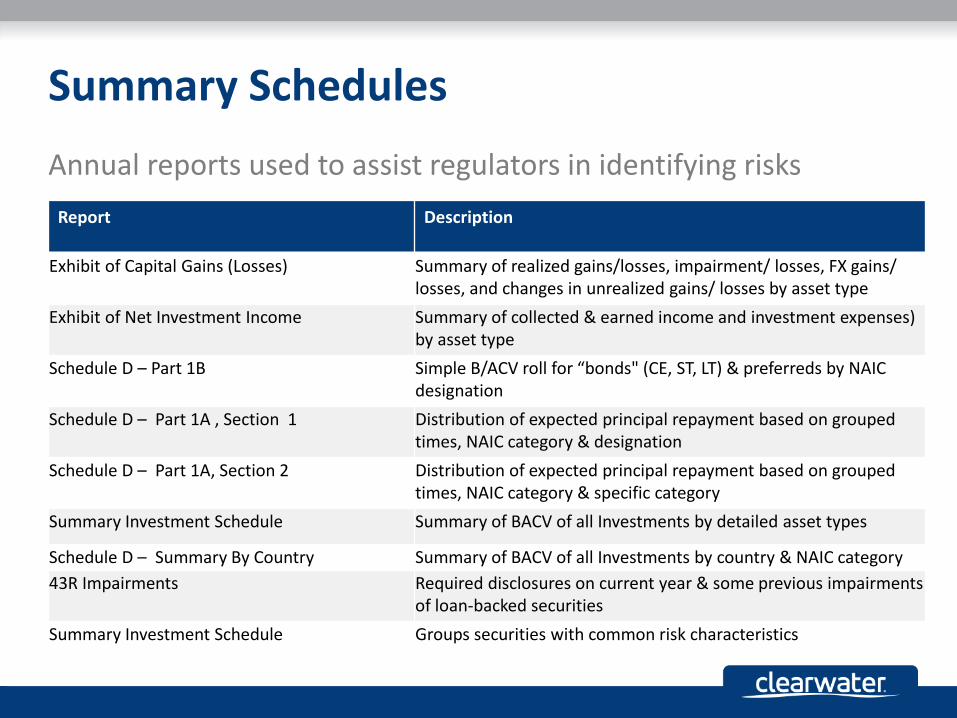

Summary Schedules

Annual reports used to assist regulators in identifying risks

Report Description

Exhibit of Capital Gains (Losses) Summary of realized gains/losses, impairment/ losses, FX gains/ losses, and changes in unrealized gains/ losses by asset type

Exhibit of Net Investment Income Summary of collected & earned income and investment expenses) by asset type

Schedule D – Part 1B Simple B/ACV roll for “bonds" (CE, ST, LT) & preferreds by NAIC designation

Schedule D – Part 1A , Section 1 Distribution of expected principal repayment based on grouped times, NAIC category & designation

Schedule D – Part 1A, Section 2 Distribution of expected principal repayment based on grouped times, NAIC category & specific category

Summary Investment Schedule Summary of BACV of all Investments by detailed asset types

Schedule D – Summary By Country Summary of BACV of all Investments by country & NAIC category

43R Impairments Required disclosures on current year & some previous impairments of loan-backed securities

Summary Investment Schedule Groups securities with common risk characteristics

Footnotes at Year End

Part of annual instructions

– Note 5 – Investments

– Note 20 – Fair value measurement

Asset Valuation Reserve

Capital required to be set aside in order to cover a company against unexpected debt. The asset valuation reserve serves as a backup for equity and credit losses. A reserve will have capital gains or losses credited or debited against the reserve account.

Interest Maintenance Reserve (IMR)

Liability reserve, establishment required by the National Association of Insurance Commissioners (NAIC), the purpose of which is to accumulate realized capital gains and losses resulting from fluctuations in the interest rate.

These gains and losses in the IMR are amortized and shown as an adjustment to the net investment income over the remaining life of the sold assets.

Supplemental Investment Risk Interrogatories

Supplemental Investment Risk Interrogatories

Purpose: to assist regulators in identifying and analyzing the risks inherent in the entity’s investment portfolio

Based off net admitted assets

The SIRI filings are due by April 1 of the year following the filing date

What is Required?

• All reporting entities are required to answer Interrogatories 1–4, 11–16, 18–19, and if applicable 20–23

• Interrogatories 5–10 must be answered if the holdings of foreign investments is equal to or exceeds 2.5% of the reporting entity’s total admitted assets

• Interrogatory 17 must be answered if the holdings of mortgage loans is equal to or exceeds 2.5% of the reporting entity’s total admitted assets

Inconsistent definitions and guidance

Difficult to find an aggregated, automated solution

Data maintenance expense

Unable to tie back to other investment schedules

Manual intervention necessary

SIRI Key Challenges

Risk-Based Capital (RBC)

What is RBC?– Method of measuring minimum amount of capital

required

Intended to limit risk by requiring more capital for more risk

Capital is intended to provide a cushion against insolvency

Giant formula calculated in Excel, filed annually w/ NAIC & state

Before RBC fixed capital standard based on state, line of business

What Are the Components?

3 main areas

– Asset risk (what Clearwater provides)

Focus is different for Life (interest rate) than P&C (credit)

This is a much bigger part for Life than for P&C

– Underwriting risk

Most of P&C RBC is here

– Other risk

catastrophe, fraud, etc.

What Do the Results Mean?

If you don’t meet RBC:

“Tripwire system”

Confidential filings—cannot view on SNL

Company action File a report

Regulatory action Increased scrutiny on report

Authorized control Commissioner can take over

Mandatory control Commissioner must take over

Other Schedules

Schedule A

Report Content Notes

A – 1 Real estate held at period end Only required at year end

A – 2 Acquisitions of real estate during the period Required every quarter, normally don’t include transfers, exchanges, or CACs

A – 3 Disposals of real estate during the period Required every quarter, normally don’t include transfers, exchanges, or CACs

A – Verification Year-to-date roll forward of book/adjusted carrying value

Required every quarter

Reports on all directly owned real estate

Includes: land, buildings, or permanent improvements

Excludes: indirectly owned real estate (ex. Joint venture owned)

Used to identify property occupied by reporting entity, property held for income completion, and property held for sale

Schedule B

Report Content Notes

B – 1 Mortgage loans held at period end Only required at year end

B – 2 Acquisitions of mortgage loans during the period

Required every quarter, normally don’t include transfers, exchanges, or CACs

B – 3 Disposals of mortgage loans during the period Required every quarter, includes transfers but normally don’t include exchanges, or CACs

B – Verification Year-to-date roll forward of book/ adjusted carrying value

Required every quarter

Reports on mortgage loans

Includes: residential, commercial, and other real estate backed and owned loans

Used to identify mortgages in good standing, restructured mortgages, mortgages in and at risk of foreclosures

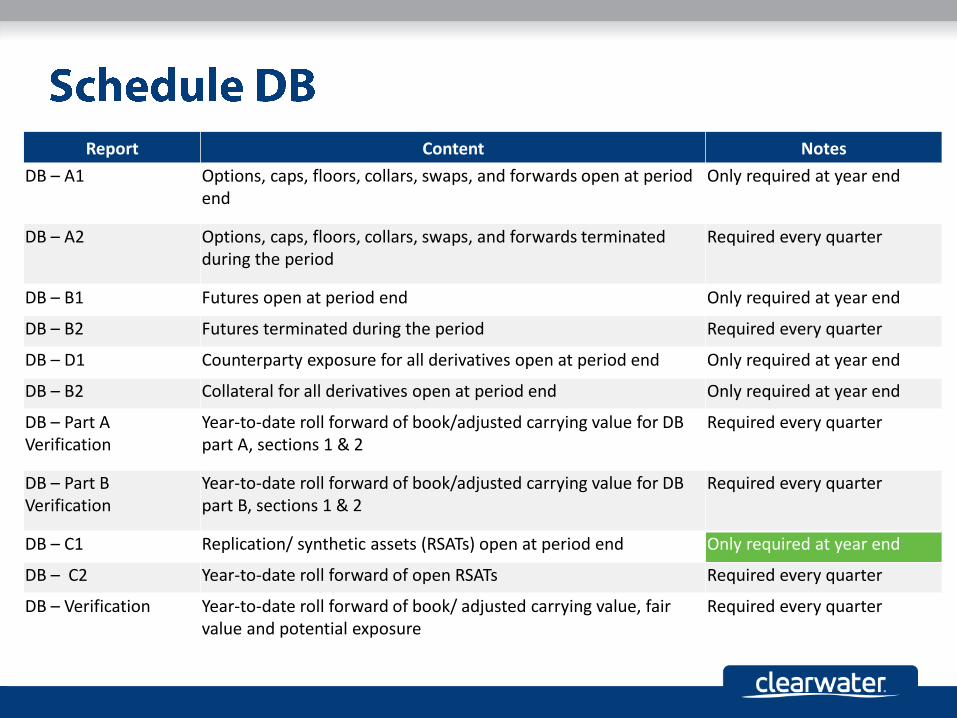

Schedule DBReports on all derivative instruments

Includes: options, warrants, caps, floors, collars, swaps, forwards, futures

SSAP No. 86 – Hedging, income generation, replication strategies

Used to determine intent (SSAP No. 86) of derivative investment strategy and the associated risk and exposures of each

Report Content Notes

DB – A1 Options, caps, floors, collars, swaps, and forwards open at period end

Only required at year end

DB – A2 Options, caps, floors, collars, swaps, and forwards terminated during the period

Required every quarter

DB – B1 Futures open at period end Only required at year end

DB – B2 Futures terminated during the period Required every quarter

DB – D1 Counterparty exposure for all derivatives open at period end Only required at year end

DB – B2 Collateral for all derivatives open at period end Only required at year end

DB – Part A Verification

Year-to-date roll forward of book/adjusted carrying value for DB part A, sections 1 & 2

Required every quarter

DB – Part B Verification

Year-to-date roll forward of book/adjusted carrying value for DB part B, sections 1 & 2

Required every quarter

DB – C1 Replication/ synthetic assets (RSATs) open at period end Only required at year end

DB – C2 Year-to-date roll forward of open RSATs Required every quarter

DB – Verification Year-to-date roll forward of book/ adjusted carrying value, fair value and potential exposure

Required every quarter

SVO Designation Process

SVO Policies and Responsibilities

1. Analysis of credit risk for purposes of NAIC designation

2. Valuation analysis to determine a unit price

3. Identification and analysis of securities that contain other non-payment risk

4. Other analytical assignments requested by the VOS/TF or members of the regulatory community

SVO Designation Process

Most securities do not require filing

– Government-backed or sponsored

– Automatically NAIC 1

– Rated & monitored by an approved rating organization

– Credit rating is converted into designation

Securities not meeting a filing exemption must be filed annually

Exception for loan-backed and structured securities

NAIC Designations

1 – Highest quality investment (A – AAA)

2 – Investment grade (BBB)

3 – Medium quality (BB)

4 – Low quality (B)

5 – Lowest quality not in/near default

6 – In or near default

NAIC Designations, cont.

P&C holds only investment grade 1 and 2 at amortized cost

Life holds only investment grade 1 – 5 at amortized cost

Worse designation = higher RBC charge

Proposal to increase number of designation classes in the works

Filing Exempt & NRSRO

Filing exempt – exempt from filing with certain conditions

National Recognized Statistical Rating Organization

– Must be rated at least annually

Moody’s Investors' Service

Standard and Poor’s

Fitch Ratings

Dominion Bond Ratings Service (DBRS)

AM Best Company (A.M. Best)

Morningstar Credit Ratings

Kroll Bond Rating Agency

Egan Jones Rating Company

5 Star/6 Star

5

– Only assigned by SVO for corporate, municipal, and structured securities that have never been rated by an NAIC CRP

– Given after review of completed and executed principal and interest certification form

6

– May be assigned by the insurer for corporate, municipal and to structured securities that have never been rated by an NAIC CRP

– SVO may assign if security was a 5* in the past and no newer documentation received

Not Rated NR

For bonds:

– Information to arrive at NAIC designation not available to SVO

– Received too late to be processed

Bonds with NR will be deleted from the VOS database if is not fixed by end of the first quarter following year end

Z

NAIC designation reported by the insurance company was not derived or obtained form the SVO

Submit to SVO within 120 days of acquisition

Not be used for securities that are exempt from filing

Questions?

Top Related