Languages

Pages

Legal

8/7/2019 hw1 Wenbo Zhang

1/13

FinancialEconometricsHomework1

Dr.Cai

WenboZhang

8/7/2019 hw1 Wenbo Zhang

2/13

FINN6219 Homework1 WenboZhang

2

1.DownloadweeklypricedataforIBMandMicrosoftstock.IBM(P1t)01/02/6201/15/08

MSFT(P2t)03/13/8601/15/08

a) CreateatimeseriesofcontinuouslycompoundedweeklyreturnsforIBMandMicrosoft.

Usetheequation: ,wecangetthereturnsseries.

b) Use the constructedweekly returns toconstruct a series ofmonthlyreturns. Youmayassumeforsimplicitythatonemonthconsistsoffourweeks.

Use the equation: mi,k = ri,tt=4( k1)+1t=4( k1)+4

, where i =1,2, k=1,2,3, , we can get the

returnsseries.

c) Constructagraphofstockpriceseries(P1t,P2t)andreturnsseries(r1t,r2t).

Time

p1t

0 500 1000 1500 2000

1

00

200

300

400

500

600

Time

p2t

0 200 400 600 800 1000

50

100

150

8/7/2019 hw1 Wenbo Zhang

3/13

8/7/2019 hw1 Wenbo Zhang

4/13

FINN6219 Homework1 WenboZhang

4

Time

p1rv

0 500 1000 1500 2000

0

5000

10000

15000

20000

Time

p2rv

0 200 400 600 800 1000

0

500

1000

1500

Time

r1rm

0 500 1000 1500 2000

0.00

0.05

0.10

Time

r2rm

0 200 400 600 800 1000

-0.06

-0

.04

-0.02

0.00

0.02

0.04

0.06

0.08

8/7/2019 hw1 Wenbo Zhang

5/13

FINN6219 Homework1 WenboZhang

5

e) What is the definition of a stationary stochastic process? Do prices look likestationaryprocess?Why?Doreturnslooklikeastationaryprocess?Why?

Definition of a stationary stochastic process: In the mathematical sciences, a

stationaryprocessisastochasticprocesswhosejointprobabilitydistributiondoes

notchangewhenshiftedintimeorspace.Asaresult,parameterssuchasthemean

andvariance,iftheyexist,alsodonotchangeovertimeorposition.Asanexample,

whitenoiseisstationary.

Fromtheobservationofthegraphsabove,pricesforbothstocksarenotstationaryprocesssincetherollingmeanischangingovertimeandrollingvarianceincludes

severalhighvalues.

However, the rollingmeanofreturn processes doesnt appear any obvious trend

overtime.Butthebignumbersinvariancedeterminethatreturnprocessesarenot

stationaryeither.

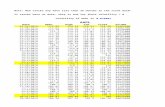

f) Computeautocorrelationcoefficientskfor1k5forpricesandreturnsseries.

P1t[,1]

[1,] 1.0000000

[2,] 0.9952586

[3,] 0.9905095

[4,] 0.9856203

[5,] 0.9807094

[6,] 0.9760011

Time

r1rv

0 500 1000 1500 2000

0.00

0.05

0.10

0.15

Time

r2rv

0 200 400 600 800 1000

0.00

0.01

0.02

0.03

0.04

8/7/2019 hw1 Wenbo Zhang

6/13

FINN6219 Homework1 WenboZhang

6

P2t

[,1]

[1,] 1.0000000

[2,] 0.9808425

[3,] 0.9619482

[4,] 0.9441063[5,] 0.9262671

[6,] 0.9107144

r1t

[,1]

[1,] 1.000000000

[2,] -0.003720422

[3,] 0.020920001

[4,] 0.015134049

[5,] -0.035417986

[6,] -0.063093877

r2t

[,1]

[1,] 1.000000000

[2,] -0.002964954

[3,] -0.012364290

[4,] 0.015955982

[5,] -0.024635205

[6,] -0.060960500

0 1 2 3 4 5

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

Series p1t

0 1 2 3 4 5

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

Series p2t

8/7/2019 hw1 Wenbo Zhang

7/13

FINN6219 Homework1 WenboZhang

7

g) BasedonthecomputedautocorrelationsforIBMandMSFTstockpricesandreturns,whatcanyousayaboutcorrelationbetweenstockpricesfordifferentdays?What

canyousayaboutcorrelationbetweenstockreturnsfordifferentdays?

Fromthegraphin(f),wecanseethatthestockpricesseriesarehighlycorrelated,

since the correlationcoefficients are very close to1. So, the correlationbetween

stockpricesfordifferentdaysisverystrong.But,thestockreturnsseriesareweakly

correlated,sincethecorrelationcoefficientsareverycloseto0.So,thecorrelation

betweenstockreturnsfordifferentdaysisveryweak.

h) UsingyourstockreturnsforIBMandMSFT,rit,i=1,2,constructfourmoreseriesyit=|rit|,i=1,2and=1,2.Computeautocorrelationcoefficientskfor1k5forthe

newlyconstructedseries.Comparethecomputedcorrelationsfor| rit|,=1,2,and

|rit|.Areresultsasyouexpected?

0 1 2 3 4 5

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

Series r1t

0 1 2 3 4 5

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

Series r2t

8/7/2019 hw1 Wenbo Zhang

8/13

FINN6219 Homework1 WenboZhang

8

Theresultsareasexpected.

i) UsetheJarque-Beratest(seeJarqueandBera(1980,1987))totesttheassumptionofreturnnormalityforIBMandMSFTstockreturns.

JarqueBeraTest

data:r1t

X-squared=6966470,df=2,p-value

8/7/2019 hw1 Wenbo Zhang

9/13

FINN6219 Homework1 WenboZhang

9

2.UseRprogramtoestimatetheprobabilitydensityfunctionofstandardizedIBMand

MSFTstockreturns.

(a)EstimateandconstructagraphoftheestimatedprobabilitydensityfunctionforIBM

andMSFTstockreturns.

-3 -2 -1 0 1 2 3

0.0

0.2

0.4

0.6

8/7/2019 hw1 Wenbo Zhang

10/13

FINN6219 Homework1 WenboZhang

10

(b) Onthe same graphwith the empiricaldensity, construct a graphof the standard

normaldensityfunction.Commentyourresults.

Comparedtothestandardnormaldistribution,whichisthegreencurveinthis

graph,thetwoempiricaldistributionshaveahigherpeakandheavy-tail,whichis

normalaccordingtothetextbook.

-3 -2 -1 0 1 2 3

0.0

0.2

0.4

0.6

8/7/2019 hw1 Wenbo Zhang

11/13

FINN6219 Homework1 WenboZhang

11

(c)ConstructQQ-plotforstandardizedIBMandMSFTreturns.YoumayusetheR

commandforthis.Commentyourresults.

AccordingtothetwoQQplotgraphsabove,itsonlysimilartostandardnormal

distributionfrom-2to1.5forIBMstockreturn.Andits-1.5to1.5forMSFTstock

return.

-3 -2 -1 0 1 2 3

0

5

10

15

20

25

Normal Q-Q Plot

Theoretical Quantiles

SampleQuantiles

-3 -2 -1 0 1 2 3

-2

0

2

4

6

8

10

Normal Q-Q Plot

Theoretical Quantiles

SampleQuantiles

8/7/2019 hw1 Wenbo Zhang

12/13

FINN6219 Homework1 WenboZhang

12

Rcodes

Problem1

library(fTrading)

library(tseries)

IBM=read.csv(file="/Users/brianzwb/Documents/Financial

Econometrics/IBM.csv",header=T,skip=1)

MSFT=read.csv(file="/Users/brianzwb/Documents/Financial

Econometrics/MSFT.csv",header=T,skip=1)

IBMprice=IBM[,5]

IBMreturn=diff(log(IBMprice))

MSFTprice=MSFT[,5]

MSFTreturn=diff(log(MSFTprice))

MSFTreturn

r1t=IBMreturn

r2t=MSFTreturn

dim(r1t)=c(4,length(r1t)/4)

monthly1=colSums(r1t)

r1t=IBMreturn

dim(r2t)=c(4,length(r2t)/4)

r2t=r2t[1:1136]

dim(r2t)=c(4,length(r2t)/4)

monthly2=colSums(r2t)

r2t=MSFTreturn

p1t=IBMprice

p2t=MSFTpricets.plot(p1t)

ts.plot(p2t)

ts.plot(r1t)

ts.plot(r2t)

p1rm=rollMean(p1t,13)

p1rv=rollVar(p1t,13)

p2rm=rollMean(p2t,13)

p2rv=rollVar(p2t,13)

r1rm=rollMean(r1t,13)

r1rv=rollVar(r1t,13)r2rm=rollMean(r2t,13)

r2rv=rollVar(r2t,13)

ts.plot(p1rm)

ts.plot(p2rm)

ts.plot(p1rv)

ts.plot(p2rv)

ts.plot(t1rm)

8/7/2019 hw1 Wenbo Zhang

13/13

FINN6219 Homework1 WenboZhang

13

ts.plot(r1rm)

ts.plot(r2rm)

ts.plot(r1rv)

ts.plot(r2rv)

acf(p1t,5)$acfacf(p2t,5)$acf

acf(r1t,5)$acf

acf(r2t,5)$acf

absr1t=abs(r1t)

absr2t=abs(r2t)

absqr1t=r1t^2

absqr2t=r2t^2

acf(absr1t)$acf

acf(absr1t,5)$acf

acf(absr2t,5)$acfacf(absqr1t,5)$acf

acf(absqr2t,5)$acf

jarque.bera.test(r1t)

jarque.bera.test(r2t)

Problem2

d1={r1t-mean(r1t)}/sd(r1t)

d2={r2t-mean(r2t)}/sd(r2t)

x0=seq(-3,3,length=100)

y0=density(d1,n=100,from=-3,to=3)

y1=y0$y

qqnorm(d1)

qqline(d1,col=2)

y2=density(d2,n=100,from=-3,to=3)

y3=y2$y

qqnorm(d2)

qqline(d2,col=2)

matplot(x0,cbind(y1,y3),type="l",lty=1:3,xlab="",ylab="")

matplot(x0,cbind(y1,y3,dnorm(x0)),type="l",lty=c(1,2),xlab="",ylab="")