Languages

Pages

Legal

November 2020

1

A MONTHLY CHARTBOOK

HOUSING FINANCE POLICY CENTER

HOUSING FINANCEAT A GLANCE

ABOUT THE CHARTBOOK

The Housing Finance Policy Center’s (HFPC) mission is to produce analyses and ideas that promote sound public policy, efficient markets, and access to economic opportunity in the area of housing finance. At A Glance, a monthly chartbook and data source for policymakers, academics, journalists, and others interested in the government’s role in mortgage markets, is at the heart of this mission.

We welcome feedback from our readers on how we can make At A Glance a more useful publication. Please email any comments or questions to [email protected].

To receive regular updates from the Housing Finance Policy Center, please visit here to sign up for our bi-weekly newsletter.

HOUSING FINANCE POLICY CENTER STAFF

Laurie GoodmanCenter Vice President

Alanna McCargoCenter Vice President

Janneke RatcliffeAssociate Vice President and Managing Director

Jim ParrottNonresident Fellow

Jun ZhuNonresident Fellow

Sheryl PardoAssociate Director of Communications

Karan KaulSenior Research Associate

Michael Neal Senior Research Associate

Jung ChoiResearch Associate

Linna ZhuResearch Associate

John WalshResearch Assistant

Caitlin YoungResearch Assistant

Daniel PangResearch Assistant

Alison Rincon

Director, Center Operations

Gideon Berger

Senior Policy Program Manager

Rylea Luckfield

Special Assistant and Project Administrator

CONTENTSOverview

Market Size OverviewValue of the US Residential Housing Market 6Size of the US Residential Mortgage Market 6Private Label Securities 7Agency Mortgage-Backed Securities 7

Origination Volume and Composition First Lien Origination Volume & Share 8

Mortgage Origination Product TypeComposition (All Originations) 9Percent Refi at Issuance

9Cash-Out Refinances

Loan Amount After Refinancing 10Cash-out Refinance Share of All Originations 10Total Home Equity Cashed Out 10

Nonbank Origination ShareNonbank Origination Share: All Loans 11Nonbank Origination Share: Purchase Loans 11Nonbank Origination Share: Refi Loans 11

Securitization Volume and CompositionAgency/Non-Agency Share of Residential MBS Issuance 12Non-Agency MBS Issuance 12Non-Agency Securitization 12

Credit Box

Housing Credit Availability Index (HCAI)Housing Credit Availability Index 13Housing Credit Availability Index by Channel 13-14

Credit Availability for Purchase LoansBorrower FICO Score at Origination Month 15Combined LTV at Origination Month 15DTI at Origination Month 15Origination FICO and LTV by MSA 16

Nonbank Credit BoxAgency FICO: Bank vs. Nonbank 17GSE FICO: Bank vs. Nonbank 17Ginnie Mae FICO: Bank vs. Nonbank 17GSE LTV: Bank vs. Nonbank 18Ginnie Mae LTV: Bank vs. Nonbank 18GSE DTI: Bank vs. Nonbank 18Ginnie Mae DTI: Bank vs. Nonbank 18

State of the Market

Mortgage Origination Projections & Originator ProfitabilityTotal Originations and Refinance Shares 19Originator Profitability and Unmeasured Costs 19

Housing SupplyMonths of Supply 20Housing Starts and Home Sales 20

Housing Affordability National Housing Affordability Over Time 21Affordability Adjusted for MSA-Level DTI 21

Home Price IndicesNational Year-Over-Year HPI Growth 22Changes in CoreLogic HPI for Top MSAs 22

First-Time HomebuyersFirst-Time Homebuyer Share 23Comparison of First-time and Repeat Homebuyers, GSE and FHA Originations 23

Delinquencies and Loss Mitigation Activity Negative Equity Share 24Loans in Serious Delinquency/Foreclosure 24Loan Modifications and Liquidations 24

GSEs under Conservatorship

GSE Portfolio Wind-DownFannie Mae Mortgage-Related Investment Portfolio 25Freddie Mac Mortgage-Related Investment Portfolio 25

Effective Guarantee Fees & GSE Risk-Sharing Transactions Effective Guarantee Fees 26Fannie Mae Upfront Loan-Level Price Adjustment 26GSE Risk-Sharing Transactions and Spreads 27-28

Serious Delinquency RatesSerious Delinquency Rates – Fannie Mae, Freddie Mac, FHA & VA 29Serious Delinquency Rates – Single-Family Loans & Multifamily GSE Loans 29

Agency Issuance

Agency Gross and Net IssuanceAgency Gross Issuance 30Agency Net Issuance 30

Agency Gross Issuance & Fed PurchasesMonthly Gross Issuance 31Fed Absorption of Agency Gross Issuance 31

Mortgage Insurance ActivityMI Activity & Market Share 32FHA MI Premiums for Typical Purchase Loan 33Initial Monthly Payment Comparison: FHA vs. PMI 33

Related HFPC Work

Publications and Events 34

Housing Supply Falls to Record Low Benefitting Home Sellers

The months’ supply of existing homes fell to an alarmingly low level of 2.5 months in October, and threatens to undermine the opportunity of homeownership for many households. The lack of homes alone makes homeownership difficult, but the lower supply also increases home prices, reducing affordability. One subtle reason that sales prices rise when supply is low, is that buyers must pay a higher price relative to the seller’s asking price. This suggests that sellers are benefitting from today’s low supply conditions. However, key supply and demand trends suggest that sellers’ advantage could erode somewhat in the coming months.

The 2.5 months’ supply of homes, reported by the National Association of Realtors (NAR), means that, at the current sales pace, the inventory of homes nationwide will be exhausted in less than 3 months. The recent decline in months’ supply from 4.8 months in May partly reflects a rebound in home sales. After existing home sales volume fell to 3.91 million in May, it then rose by 75 percent to approximately 6.85 million by October. NAR reports, however, that the inventory of homes for sale in October was just 1.4 million, a series low.

Amid shrinking inventory, sales prices have risen. Since May, existing home inventory has fallen by 5.0 percent according to NAR, while sales prices have risen by 1.3 percent according to Urban Institute calculations of Black Knight data. Since January 2012, when housing market activity began to sustainably improve after the sharp decline in the wake of the Great Recession, the inventory of existing homes has shrunk by 47.4 percent while house prices have risen 56.4 percent.

While the increase in sales prices tells us that demand is high, the sales-price to list-price ratio suggests that buyers are eager to purchase homes. As the inventory of for-sale homes has declined since 2012, the ratio of the sales-price to the list-price has increased. According to Redfin, the ratio of the sales-price to the list-price peaked in September 2020 at 99.4 percent, the latest month of data, a three-percentage point increase since February 2012, the first month of data. Inventory fell by 55 percent over this same period. In other words, as inventory has declined, the average homebuyer is paying a little closer to the sellers’ asking price.

The increase in the ratio of the sales-price to the list-price partly reflects a larger percentage of buyers paying a sales price that exceeds the seller’s list price. As inventory has declined since 2012, the share of buyers paying a sales price above the buyers asking price increased from 18.3 percent to 32.8 percent in September.

The housing market is tilted toward the seller, according to the current data, but that could change. There was a sharp rebound in single-family housing starts in recent months, suggesting that more supply is forthcoming. Additionally, the pace of purchase mortgage applications has moderated in recent months as COVID infections soar and the NAR Housing Affordability Index has fallen from its year ago level. Although the market currently favors sellers their advantage could inch somewhat closer to balance in the near future.

INSIDE THIS ISSUE• Although year-to-date 2020 nonagency

securitizations are down compared to 2019, there are clear signs of recovery. Securitization volumes in recent months have been highly comparable to the same months of last year (page 12).

• The serious delinquency rates for FHA and VA mortgages climbed higher in Q3 2020. FHA rose from 7.96 percent in Q2 to 10.76 percent in Q3. VA rose from 3.98 percent in Q2 to 5.77 percent in Q3 (page 29).

• VA’s share of new mortgage insurance written increased to 31 percent in Q3 2020, the highest level in at least 21 years (page 32).

INTRODUCTION

94%

95%

96%

97%

98%

99%

100%

0.0

0.5

1.0

1.5

2.0

2.5

Millions

For-sale Inventory Sale Price-List Price Ratio

Source: Redfin.

Sale-List Price Ratio Climbs Amid Inventory Decline

0%

10%

20%

30%

40%

2012 2013 2014 2015 2016 2017 2018 2019 2020

Share of Homes Sold Above List Price

Source: Redfin.

6

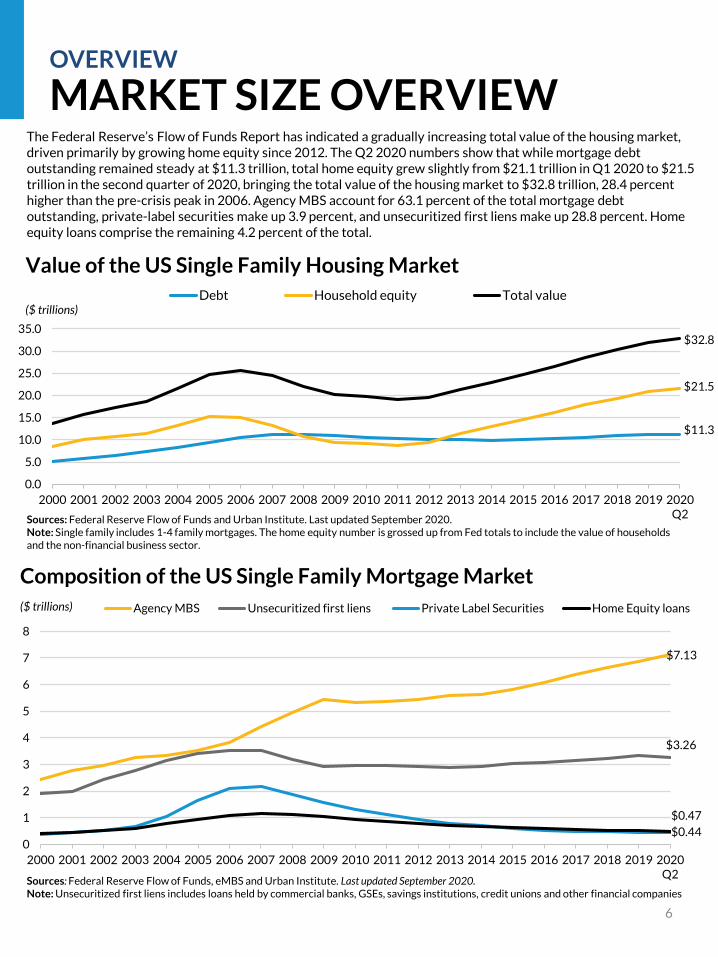

MARKET SIZE OVERVIEWThe Federal Reserve’s Flow of Funds Report has indicated a gradually increasing total value of the housing market, driven primarily by growing home equity since 2012. The Q2 2020 numbers show that while mortgage debt outstanding remained steady at $11.3 trillion, total home equity grew slightly from $21.1 trillion in Q1 2020 to $21.5 trillion in the second quarter of 2020, bringing the total value of the housing market to $32.8 trillion, 28.4 percent higher than the pre-crisis peak in 2006. Agency MBS account for 63.1 percent of the total mortgage debt outstanding, private-label securities make up 3.9 percent, and unsecuritized first liens make up 28.8 percent. Home equity loans comprise the remaining 4.2 percent of the total.

OVERVIEW

Debt,household mortgages,

$9,833

$7.13

$3.26

$0.44

$0.47

0

1

2

3

4

5

6

7

8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Q2

($ trillions)

Composition of the US Single Family Mortgage Market

Agency MBS Unsecuritized first liens Private Label Securities Home Equity loans

Sources: Federal Reserve Flow of Funds, eMBS and Urban Institute. Last updated September 2020.Note: Unsecuritized first liens includes loans held by commercial banks, GSEs, savings institutions, credit unions and other financial companies

$11.3

$21.5

$32.8

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Q2

($ trillions)Debt Household equity Total value

Value of the US Single Family Housing Market

Sources: Federal Reserve Flow of Funds and Urban Institute. Last updated September 2020.Note: Single family includes 1-4 family mortgages. The home equity number is grossed up from Fed totals to include the value of households and the non-financial business sector.

7

MARKET SIZE OVERVIEWOVERVIEW

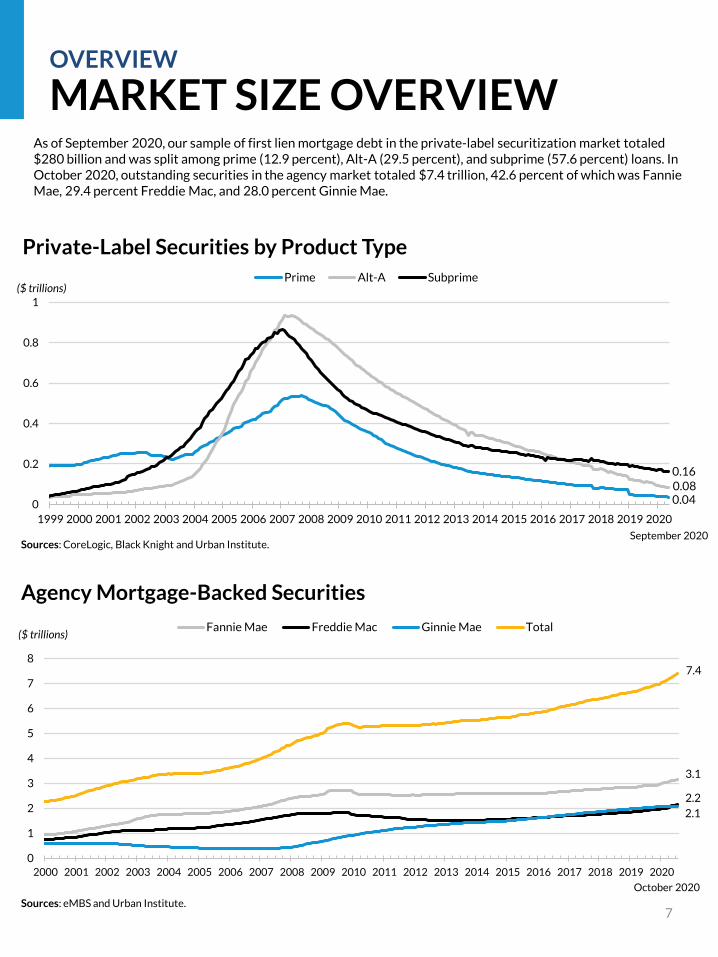

As of September 2020, our sample of first lien mortgage debt in the private-label securitization market totaled $280 billion and was split among prime (12.9 percent), Alt-A (29.5 percent), and subprime (57.6 percent) loans. In October 2020, outstanding securities in the agency market totaled $7.4 trillion, 42.6 percent of which was Fannie Mae, 29.4 percent Freddie Mac, and 28.0 percent Ginnie Mae.

0.040.080.16

0

0.2

0.4

0.6

0.8

1

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

($ trillions)

Private-Label Securities by Product Type

Prime Alt-A Subprime

Sources: CoreLogic, Black Knight and Urban Institute.

3.1

2.1

2.2

7.4

0

1

2

3

4

5

6

7

8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

($ trillions)Fannie Mae Freddie Mac Ginnie Mae Total

Agency Mortgage-Backed Securities

Sources: eMBS and Urban Institute.

September 2020

October 2020

8

OVERVIEW

ORIGINATION VOLUMEAND COMPOSITION

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Q1

2020Q2

2020Q3

($ trillions)

First Lien Origination Volume

GSE securitization FHA/VA securitization PLS securitization Portfolio

Sources: Inside Mortgage Finance and Urban Institute. Last updated November 2020.

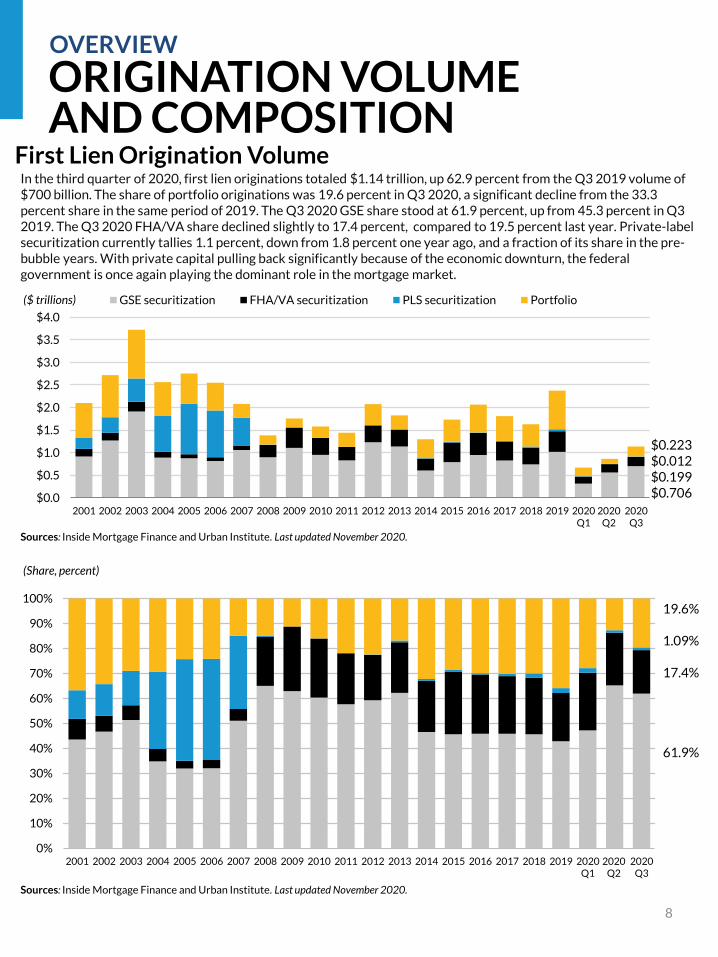

In the third quarter of 2020, first lien originations totaled $1.14 trillion, up 62.9 percent from the Q3 2019 volume of $700 billion. The share of portfolio originations was 19.6 percent in Q3 2020, a significant decline from the 33.3 percent share in the same period of 2019. The Q3 2020 GSE share stood at 61.9 percent, up from 45.3 percent in Q3 2019. The Q3 2020 FHA/VA share declined slightly to 17.4 percent, compared to 19.5 percent last year. Private-label securitization currently tallies 1.1 percent, down from 1.8 percent one year ago, and a fraction of its share in the pre-bubble years. With private capital pulling back significantly because of the economic downturn, the federal government is once again playing the dominant role in the mortgage market.

$0.223$0.012$0.199$0.706

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Q1

2020Q2

2020Q3

Sources: Inside Mortgage Finance and Urban Institute. Last updated November 2020.

(Share, percent)

19.6%

1.09%

17.4%

61.9%

9

MORTGAGE ORIGINATION PRODUCT

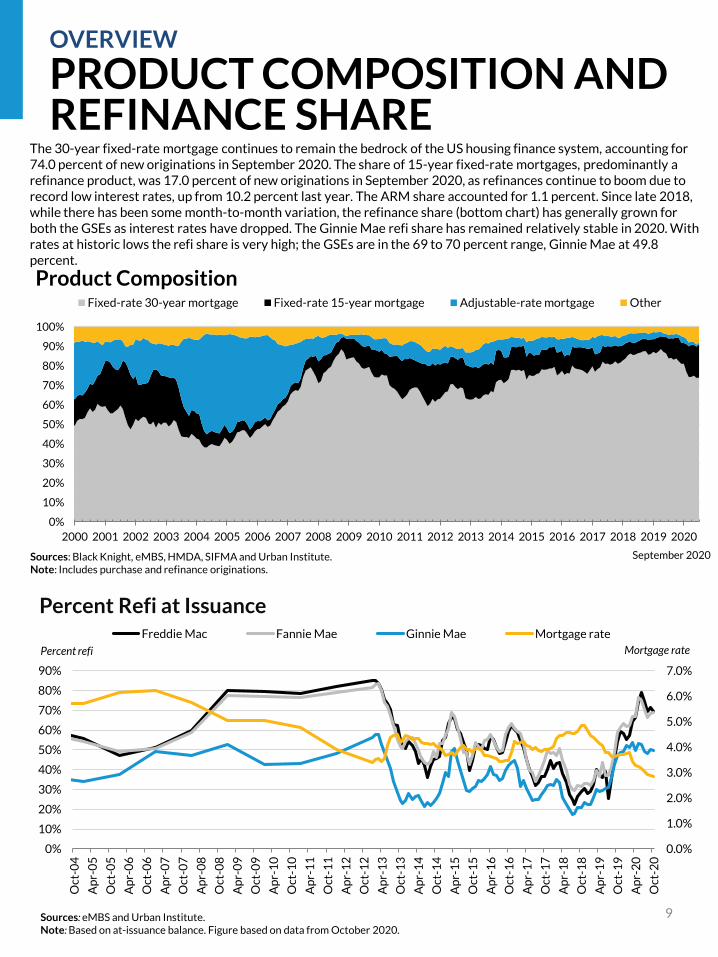

TYPEThe 30-year fixed-rate mortgage continues to remain the bedrock of the US housing finance system, accounting for 74.0 percent of new originations in September 2020. The share of 15-year fixed-rate mortgages, predominantly a refinance product, was 17.0 percent of new originations in September 2020, as refinances continue to boom due to record low interest rates, up from 10.2 percent last year. The ARM share accounted for 1.1 percent. Since late 2018, while there has been some month-to-month variation, the refinance share (bottom chart) has generally grown for both the GSEs as interest rates have dropped. The Ginnie Mae refi share has remained relatively stable in 2020. With rates at historic lows the refi share is very high; the GSEs are in the 69 to 70 percent range, Ginnie Mae at 49.8 percent.

OVERVIEW

PRODUCT COMPOSITION AND REFINANCE SHARE

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Product CompositionFixed-rate 30-year mortgage Fixed-rate 15-year mortgage Adjustable-rate mortgage Other

Sources: Black Knight, eMBS, HMDA, SIFMA and Urban Institute. Note: Includes purchase and refinance originations.

September 2020

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Oct

-04

Ap

r-0

5

Oct

-05

Ap

r-0

6

Oct

-06

Ap

r-0

7

Oct

-07

Ap

r-0

8

Oct

-08

Ap

r-0

9

Oct

-09

Ap

r-1

0

Oct

-10

Ap

r-1

1

Oct

-11

Ap

r-1

2

Oct

-12

Ap

r-1

3

Oct

-13

Ap

r-1

4

Oct

-14

Ap

r-1

5

Oct

-15

Ap

r-1

6

Oct

-16

Ap

r-1

7

Oct

-17

Ap

r-1

8

Oct

-18

Ap

r-1

9

Oct

-19

Ap

r-2

0

Oct

-20

Percent Refi at IssuanceFreddie Mac Fannie Mae Ginnie Mae Mortgage rate

Sources: eMBS and Urban Institute.Note: Based on at-issuance balance. Figure based on data from October 2020.

Mortgage ratePercent refi

CASH-OUT REFINANCESOVERVIEW

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

1996 1999 2002 2005 2008 2011 2014 2017 2020

$ billions

Equity Take-Out from Conventional Mortgage Refinance Activity

Sources: eMBS and Urban Institute.Note: Data as of September 2020.

2020 Q3

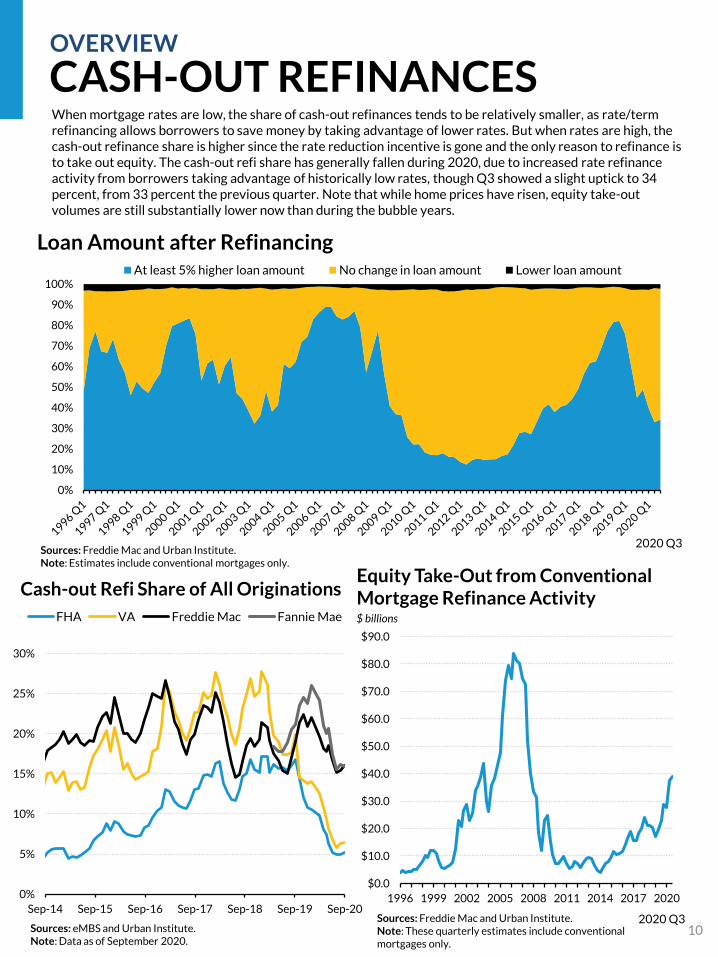

When mortgage rates are low, the share of cash-out refinances tends to be relatively smaller, as rate/term refinancing allows borrowers to save money by taking advantage of lower rates. But when rates are high, the cash-out refinance share is higher since the rate reduction incentive is gone and the only reason to refinance is to take out equity. The cash-out refi share has generally fallen during 2020, due to increased rate refinance activity from borrowers taking advantage of historically low rates, though Q3 showed a slight uptick to 34 percent, from 33 percent the previous quarter. Note that while home prices have risen, equity take-out volumes are still substantially lower now than during the bubble years.

0%

5%

10%

15%

20%

25%

30%

Sep-14 Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20

FHA VA Freddie Mac Fannie Mae

Sources: Freddie Mac and Urban Institute.Note: These quarterly estimates include conventional mortgages only.

Cash-out Refi Share of All Originations

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%At least 5% higher loan amount No change in loan amount Lower loan amount

10

Sources: Freddie Mac and Urban Institute.Note: Estimates include conventional mortgages only.

Loan Amount after Refinancing

2020 Q3

Sources: eMBS and Urban Institute. Sources: eMBS and Urban Institute.

92%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Fe

b-1

4

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct

-14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct

-15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-1

7

Fe

b-1

8

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

De

c-1

8

Fe

b-1

9

Ap

r-1

9

Jun

-19

Au

g-1

9

Oct

-19

De

c-1

9

Fe

b-2

0

Ap

r-2

0

Jun

-20

Au

g-2

0

Oct

-20

Nonbank Origination Share: All Loans

All Fannie Freddie Ginnie

75%70%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ap

r-1

4

Oct

-14

Ap

r-1

5

Oct

-15

Ap

r-1

6

Oct

-16

Ap

r-1

7

Oct

-17

Ap

r-1

8

Oct

-18

Ap

r-1

9

Oct

-19

Ap

r-2

0

Oct

-20

All Fannie Freddie Ginnie

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ap

r-1

4

Oct

-14

Ap

r-1

5

Oct

-15

Ap

r-1

6

Oct

-16

Ap

r-1

7

Oct

-17

Ap

r-1

8

Oct

-18

Ap

r-1

9

Oct

-19

Ap

r-2

0

Oct

-20

All Fannie Freddie Ginnie

Nonbank Origination Share: Refi Loans

11

AGENCY NONBANK ORIGINATION SHARE

OVERVIEW

Nonbank Origination Share: Purchase Loans

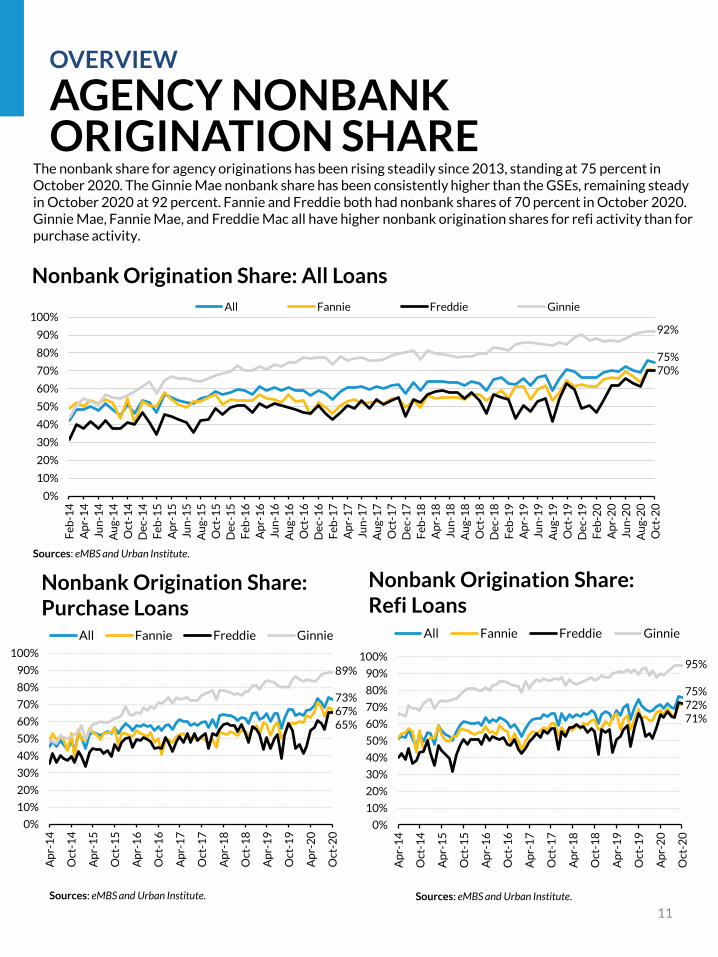

The nonbank share for agency originations has been rising steadily since 2013, standing at 75 percent in October 2020. The Ginnie Mae nonbank share has been consistently higher than the GSEs, remaining steady in October 2020 at 92 percent. Fannie and Freddie both had nonbank shares of 70 percent in October 2020. Ginnie Mae, Fannie Mae, and Freddie Mac all have higher nonbank origination shares for refi activity than for purchase activity.

Sources: eMBS and Urban Institute.

89%

73%67%65%

95%

75%72%71%

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

($ billions)Re-REMICs and other

Scratch and dentAlt A

Subprime

Prime

Sources: Inside Mortgage Finance and Urban Institute.

Non-Agency MBS Issuance

$4.80$12.90$7.59$4.63$8.99

12

SECURITIZATION VOLUME AND COMPOSITION

OVERVIEW

97.27%

2.73%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Agency share Non-agency share

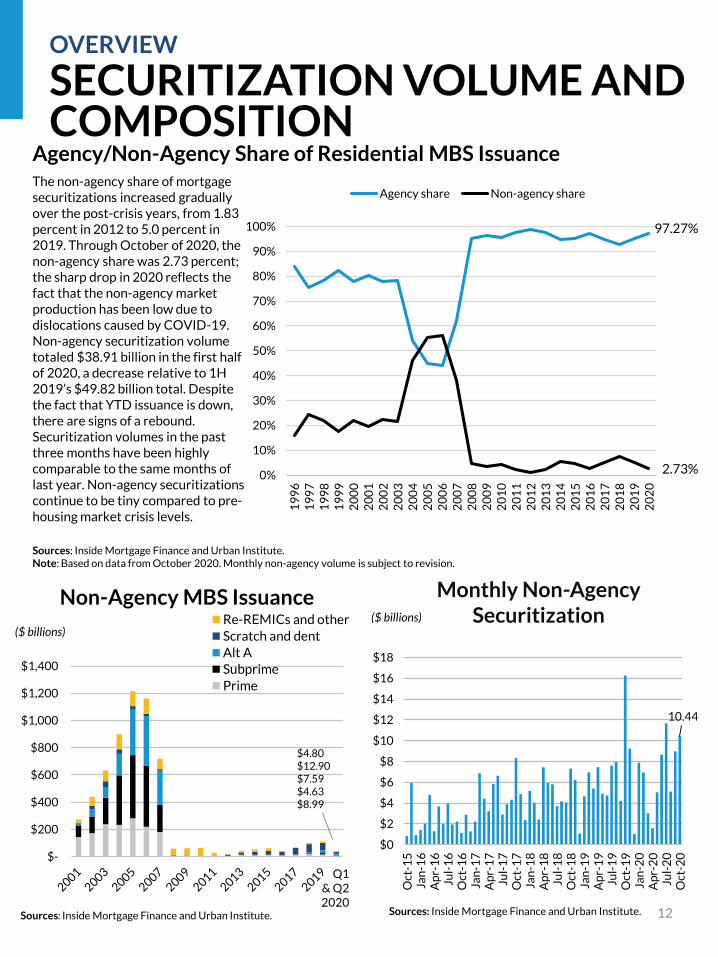

Agency/Non-Agency Share of Residential MBS IssuanceThe non-agency share of mortgage securitizations increased gradually over the post-crisis years, from 1.83 percent in 2012 to 5.0 percent in 2019. Through October of 2020, the non-agency share was 2.73 percent; the sharp drop in 2020 reflects the fact that the non-agency market production has been low due to dislocations caused by COVID-19. Non-agency securitization volume totaled $38.91 billion in the first half of 2020, a decrease relative to 1H 2019’s $49.82 billion total. Despite the fact that YTD issuance is down, there are signs of a rebound. Securitization volumes in the past three months have been highly comparable to the same months of last year. Non-agency securitizations continue to be tiny compared to pre-housing market crisis levels.

Sources: Inside Mortgage Finance and Urban Institute.Note: Based on data from October 2020. Monthly non-agency volume is subject to revision.

10.44

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

Oct

-15

Jan

-16

Ap

r-1

6Ju

l-1

6O

ct-1

6Ja

n-1

7A

pr-

17

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8Ju

l-1

8O

ct-1

8Ja

n-1

9A

pr-

19

Jul-

19

Oct

-19

Jan

-20

Ap

r-2

0Ju

l-2

0O

ct-2

0

($ billions)

Monthly Non-Agency Securitization

Sources: Inside Mortgage Finance and Urban Institute.

Q1 & Q22020

0

2

4

6

8

10

12

14

16

18

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

PercentTotal default risk

Borrower risk

Product risk

Reasonable

lending

standards

GSE Channel

13

HOUSING CREDIT AVAILABILITY INDEX

CREDIT BOX

The Urban Institute’s Housing Credit Availability Index (HCAI) assesses lenders’ tolerance for both borrower riskand product risk, calculating the share of owner-occupied purchase loans that are likely to go 90+ days delinquent over the life of the loan. The HCAI stood at 5.2 percent in Q2 2020, down from an adjusted 5.3 percent in Q1 2020. Note that we updated the methodology as of Q2 2020, see new methodology here. Tightening in the GSE and government channels has driven a retraction of credit availability through the first half of 2020, as the risk in the portfolio and private-label securitization market remains a shadow of what it once was. More information about the HCAI is available here.

Q2 2020

All Channels

0

1

2

3

4

5

6

7

8

9

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Percent Total default risk

Product risk

Borrower risk

Sources: eMBS, CoreLogic, HMDA, IMF, and Urban Institute.Note: Default is defined as 90 days or more delinquent at any point. Last updated October 2020.

Q2 2020

The GSE market has expanded the credit box proportionately more than the government channel in recent years, although the GSE box is still much narrower. From Q2 2011 to Q1 2019, the total risk taken by the GSE channel more than doubled, from 1.4 percent to 3.0 percent. This is still very modest by pre-crisis standards. However, over the past year, credit availability has trended down and tightened further in the first half of 2020 in response to changing market conditions due to COVID-19, standing at 2.7 percent in Q2 2020.

14

HOUSING CREDIT AVAILABILITY INDEX

CREDIT BOX

Government Channel

Portfolio and Private Label Securities Channels

0

5

10

15

20

25

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Percent

Total default risk

Borrower risk

Product risk

Q2 2020

0

5

10

15

20

25

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

PercentTotal default risk

Borrower risk

Product risk

Q2 2020Sources: eMBS, CoreLogic, HMDA, IMF, and Urban Institute.Note: Default is defined as 90 days or more delinquent at any point. Last updated October 2020.

The total default risk the government loan channel is willing to take bottomed out at 9.6 percent in Q3 2013. It fluctuated in a narrow range at or above that number for three years. In the nine quarters from Q4 2016 to Q1 2019, the risk in the government channel had risen significantly from 9.9 to 12.1 percent. In Q2 2020, risk in the government channel receded to 10.8 percent, moving closer to 2016 levels and still far below the pre-bubble level of 19 to 23 percent.

The portfolio and private-label securities (PP) channel took on more product risk than the Government and GSE channels during the bubble. After the crisis, the channel’s product and borrower risks dropped sharply. The numbers have stabilized since 2013, with product risk well below 0.5 percent and total risk largely in the range of 2.5 to 3.0 percent; it was 3.0 percent in Q2 2020. However, the PP market share plummeted during the COVID-19 crisis, as borrowers increasingly used government or GSE channels or could not obtain a mortgage at all.

15

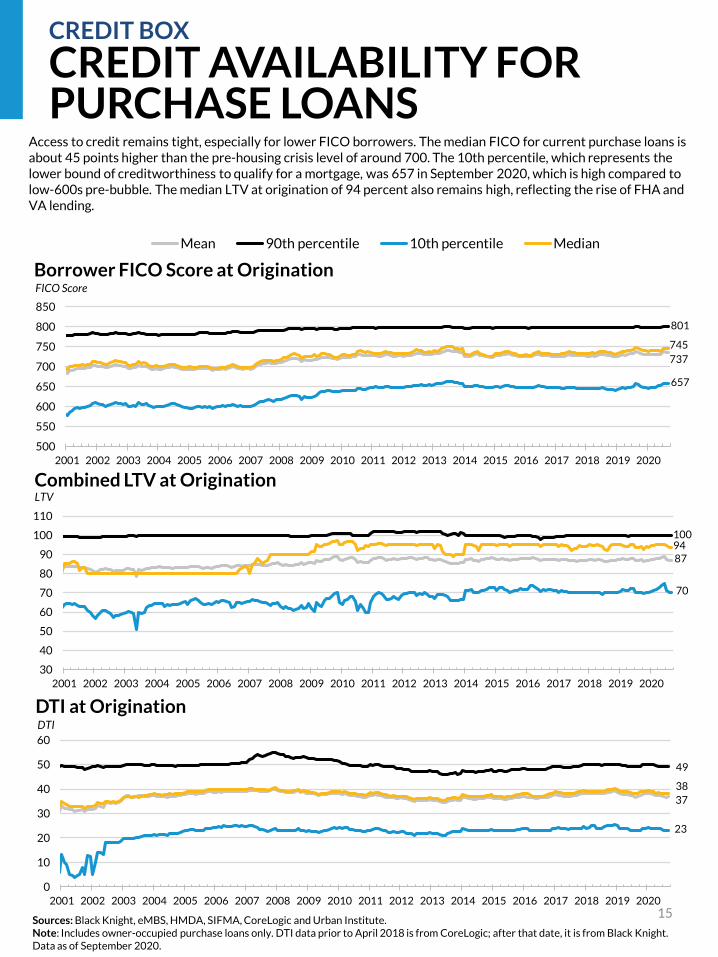

CREDIT AVAILABILITY FORAccess to credit remains tight, especially for lower FICO borrowers. The median FICO for current purchase loans is about 45 points higher than the pre-housing crisis level of around 700. The 10th percentile, which represents the lower bound of creditworthiness to qualify for a mortgage, was 657 in September 2020, which is high compared to low-600s pre-bubble. The median LTV at origination of 94 percent also remains high, reflecting the rise of FHA and VA lending.

CREDIT AVAILABILITY FOR PURCHASE LOANS

CREDIT BOX

100

8794

70

30

40

50

60

70

80

90

100

110

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

LTV

Combined LTV at Origination

Sources: Black Knight, eMBS, HMDA, SIFMA, CoreLogic and Urban Institute.Note: Includes owner-occupied purchase loans only. DTI data prior to April 2018 is from CoreLogic; after that date, it is from Black Knight.Data as of September 2020.

49

37

38

23

0

10

20

30

40

50

60

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

DTI at OriginationDTI

737

801

657

745

500

550

600

650

700

750

800

850

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

FICO Score

Borrower FICO Score at Origination

Mean 90th percentile 10th percentile Median

16

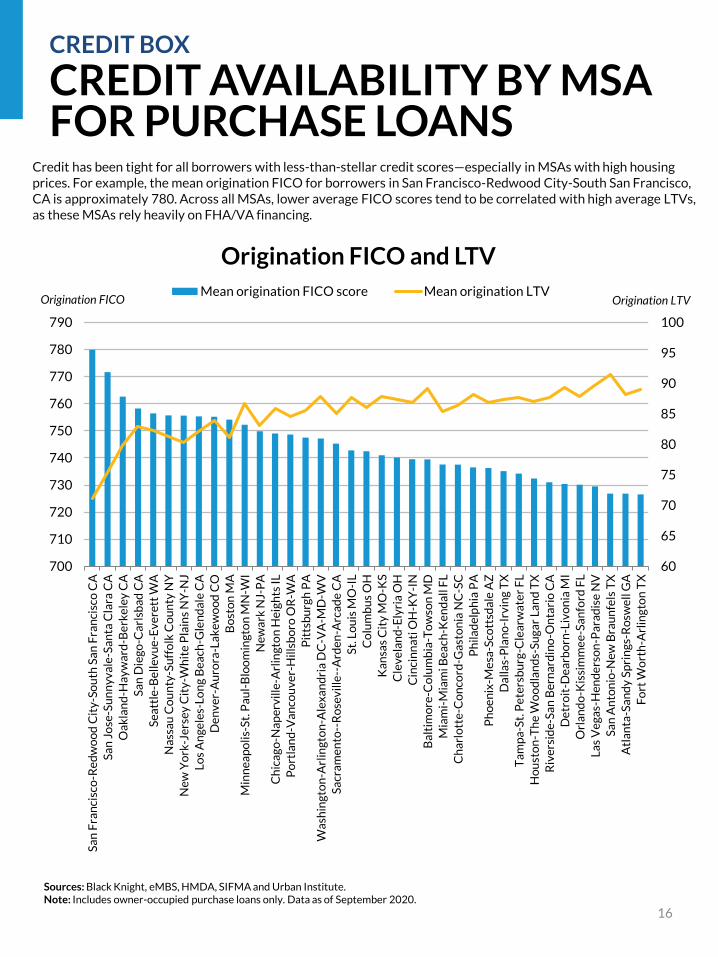

CREDIT AVAILABILITY FORCREDIT AVAILABILITY BY MSA FOR PURCHASE LOANS

CREDIT BOX

Credit has been tight for all borrowers with less-than-stellar credit scores—especially in MSAs with high housing prices. For example, the mean origination FICO for borrowers in San Francisco-Redwood City-South San Francisco, CA is approximately 780. Across all MSAs, lower average FICO scores tend to be correlated with high average LTVs, as these MSAs rely heavily on FHA/VA financing.

60

65

70

75

80

85

90

95

100

700

710

720

730

740

750

760

770

780

790

Sa

n F

ran

cisc

o-R

ed

wo

od

Cit

y-S

ou

th S

an

Fra

nci

sco

CA

Sa

n J

ose

-Su

nn

yv

ale

-Sa

nta

Cla

ra C

A

Oa

kla

nd

-Ha

yw

ard

-Be

rke

ley

CA

Sa

n D

ieg

o-C

arl

sba

d C

A

Se

att

le-B

ell

ev

ue

-Ev

ere

tt W

A

Na

ssa

u C

ou

nty

-Su

ffo

lk C

ou

nty

NY

Ne

w Y

ork

-Je

rse

y C

ity

-Wh

ite

Pla

ins

NY

-NJ

Lo

s A

ng

ele

s-L

on

g B

ea

ch-G

len

da

le C

A

De

nv

er-

Au

rora

-La

ke

wo

od

CO

Bo

sto

n M

A

Min

ne

ap

oli

s-S

t. P

au

l-B

loo

min

gto

n M

N-W

I

Ne

wa

rk N

J-P

A

Ch

ica

go

-Na

pe

rvil

le-A

rlin

gto

n H

eig

hts

IL

Po

rtla

nd

-Va

nco

uv

er-

Hil

lsb

oro

OR

-WA

Pit

tsb

urg

h P

A

Wa

shin

gto

n-A

rlin

gto

n-A

lex

an

dri

a D

C-V

A-M

D-W

V

Sa

cra

me

nto

--R

ose

vil

le--

Ard

en

-Arc

ad

e C

A

St.

Lo

uis

MO

-IL

Co

lum

bu

s O

H

Ka

nsa

s C

ity

MO

-KS

Cle

ve

lan

d-E

lyri

a O

H

Cin

cin

na

ti O

H-K

Y-I

N

Ba

ltim

ore

-Co

lum

bia

-To

wso

n M

D

Mia

mi-

Mia

mi B

ea

ch-K

en

da

ll F

L

Ch

arl

ott

e-C

on

cord

-Ga

sto

nia

NC

-SC

Ph

ila

de

lph

ia P

A

Ph

oe

nix

-Me

sa-S

cott

sda

le A

Z

Da

lla

s-P

lan

o-I

rvin

g T

X

Ta

mp

a-S

t. P

ete

rsb

urg

-Cle

arw

ate

r F

L

Ho

ust

on

-Th

e W

oo

dla

nd

s-S

ug

ar

La

nd

TX

Riv

ers

ide

-Sa

n B

ern

ard

ino

-On

tari

o C

A

De

tro

it-D

ea

rbo

rn-L

ivo

nia

MI

Orl

an

do

-Kis

sim

me

e-S

an

ford

FL

La

s V

eg

as-

He

nd

ers

on

-Pa

rad

ise

NV

Sa

n A

nto

nio

-Ne

w B

rau

nfe

ls T

X

Atl

an

ta-S

an

dy

Sp

rin

gs-

Ro

swe

ll G

A

Fo

rt W

ort

h-A

rlin

gto

n T

X

Origination LTVOrigination FICO

Origination FICO and LTV

Mean origination FICO score Mean origination LTV

Sources: Black Knight, eMBS, HMDA, SIFMA and Urban Institute.Note: Includes owner-occupied purchase loans only. Data as of September 2020.

Sources: eMBS and Urban Institute. Sources: eMBS and Urban Institute.

680

690

700

710

720

730

740

750

760

770

780

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Ap

r-1

9

Jul-

19

Oct

-19

Jan

-20

Ap

r-2

0

Jul-

20

Oct

-20

Agency FICO: Bank vs. NonbankAll Median FICO Bank Median FICO Nonbank Median FICOFICO

Sources: eMBS and Urban Institute.

660

680

700

720

740

760

780

Oct

-14

Fe

b-1

5

Jun

-15

Oct

-15

Fe

b-1

6

Jun

-16

Oct

-16

Fe

b-1

7

Jun

-17

Oct

-17

Fe

b-1

8

Jun

-18

Oct

-18

Fe

b-1

9

Jun

-19

Oct

-19

Fe

b-2

0

Jun

-20

Oct

-20

All Median FICO

Bank Median FICO

Nonbank Median FICO

Ginnie Mae FICO: Bank vs. Nonbank

660

680

700

720

740

760

780

Oct

-14

Fe

b-1

5

Jun

-15

Oct

-15

Fe

b-1

6

Jun

-16

Oct

-16

Fe

b-1

7

Jun

-17

Oct

-17

Fe

b-1

8

Jun

-18

Oct

-18

Fe

b-1

9

Jun

-19

Oct

-19

Fe

b-2

0

Jun

-20

Oct

-20

All Median FICO

Bank Median FICO

Nonbank Median FICO

GSE FICO: Bank vs. Nonbank

17

CREDIT BOX

AGENCY NONBANK CREDIT BOX

FICO FICO

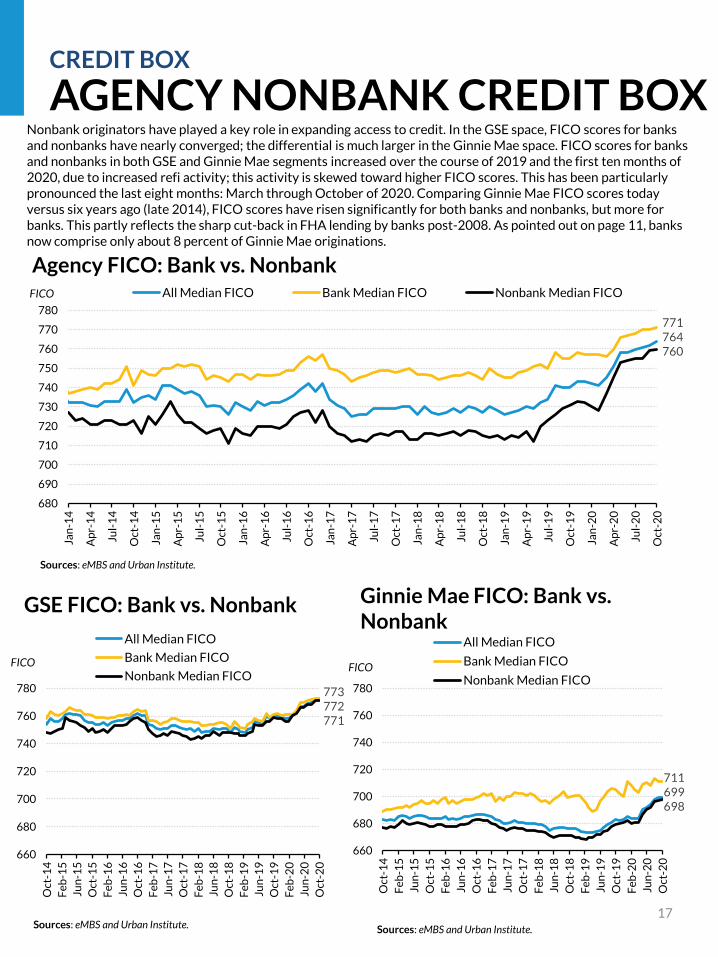

Nonbank originators have played a key role in expanding access to credit. In the GSE space, FICO scores for banks and nonbanks have nearly converged; the differential is much larger in the Ginnie Mae space. FICO scores for banks and nonbanks in both GSE and Ginnie Mae segments increased over the course of 2019 and the first ten months of 2020, due to increased refi activity; this activity is skewed toward higher FICO scores. This has been particularly pronounced the last eight months: March through October of 2020. Comparing Ginnie Mae FICO scores today versus six years ago (late 2014), FICO scores have risen significantly for both banks and nonbanks, but more for banks. This partly reflects the sharp cut-back in FHA lending by banks post-2008. As pointed out on page 11, banks now comprise only about 8 percent of Ginnie Mae originations.

773772771

711699698

771764760

Sources: eMBS and Urban Institute. Sources: eMBS and Urban Institute.

66687072747678808284868890

Oct

-13

Fe

b-1

4

Jun

-14

Oct

-14

Fe

b-1

5

Jun

-15

Oct

-15

Fe

b-1

6

Jun

-16

Oct

-16

Fe

b-1

7

Jun

-17

Oct

-17

Fe

b-1

8

Jun

-18

Oct

-18

Fe

b-1

9

Jun

-19

Oct

-19

Fe

b-2

0

Jun

-20

Oct

-20

GSE LTV: Bank vs. Nonbank

All Median LTV Bank Median LTV

Nonbank Median LTV

Sources: eMBS and Urban Institute.

90

91

92

93

94

95

96

97

98

99

100

Oct

-13

Fe

b-1

4

Jun

-14

Oct

-14

Fe

b-1

5

Jun

-15

Oct

-15

Fe

b-1

6

Jun

-16

Oct

-16

Fe

b-1

7

Jun

-17

Oct

-17

Fe

b-1

8

Jun

-18

Oct

-18

Fe

b-1

9

Jun

-19

Oct

-19

Fe

b-2

0

Jun

-20

Oct

-20

All Median LTV Bank Median LTV

Nonbank Median LTV

Sources: eMBS and Urban Institute.

30

32

34

36

38

40

42

44

46

Oct

-13

Fe

b-1

4

Jun

-14

Oct

-14

Fe

b-1

5

Jun

-15

Oct

-15

Fe

b-1

6

Jun

-16

Oct

-16

Fe

b-1

7

Jun

-17

Oct

-17

Fe

b-1

8

Jun

-18

Oct

-18

Fe

b-1

9

Jun

-19

Oct

-19

Fe

b-2

0

Jun

-20

Oct

-20

All Median DTI Bank Median DTI

Nonbank Median DTI

30

32

34

36

38

40

42

44

Oct

-13

Fe

b-1

4

Jun

-14

Oct

-14

Fe

b-1

5

Jun

-15

Oct

-15

Fe

b-1

6

Jun

-16

Oct

-16

Fe

b-1

7

Jun

-17

Oct

-17

Fe

b-1

8

Jun

-18

Oct

-18

Fe

b-1

9

Jun

-19

Oct

-19

Fe

b-2

0

Jun

-20

Oct

-20

GSE DTI: Bank vs. NonbankAll Median DTI Bank Median DTI

Nonbank Median DTI

18

CREDIT BOX

AGENCY NONBANK CREDIT BOX

Ginnie Mae LTV: Bank vs. Nonbank

Ginnie Mae DTI: Bank vs. Nonbank

LTV LTV

DTIDTI

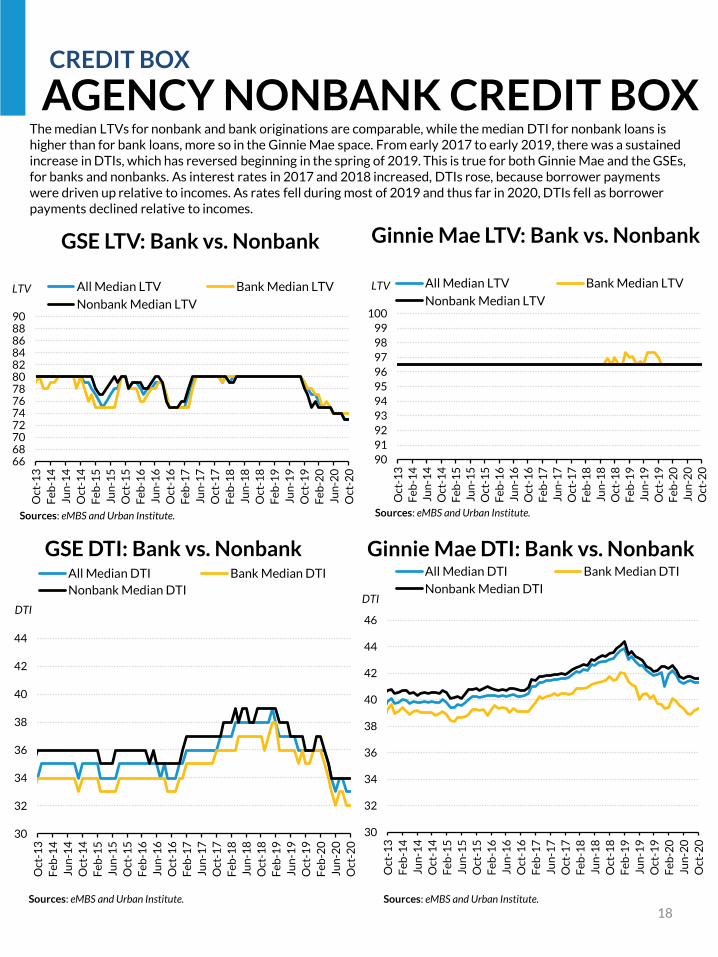

The median LTVs for nonbank and bank originations are comparable, while the median DTI for nonbank loans is higher than for bank loans, more so in the Ginnie Mae space. From early 2017 to early 2019, there was a sustained increase in DTIs, which has reversed beginning in the spring of 2019. This is true for both Ginnie Mae and the GSEs, for banks and nonbanks. As interest rates in 2017 and 2018 increased, DTIs rose, because borrower payments were driven up relative to incomes. As rates fell during most of 2019 and thus far in 2020, DTIs fell as borrower payments declined relative to incomes.

19

STATE OF THE MARKET

MORTGAGE ORIGINATION PROJECTIONS

Fannie Mae, Freddie Mac and the MBA estimate 2020 origination volume to be between $3.39 and $4.12 trillion, higher than the $2.17 to $2.33 trillion in 2019. These numbers put 2020 in competition to be either the highest origination year in the 21st century, or just behind the 2003 number of $3.73 trillion; page 8 top provides the longer historical time series. The very robust 2020 origination volume is due to very strong refinance activity. All three groups expect the refinance share to be 12 to 17 percentage points higher than in 2019, based on continued low rates in the wake of COVID-19.

Total Originations and Refinance Shares Originations ($ billions) Refi Share (percent)

PeriodTotal, FNMA

estimateTotal, FHLMC

estimateTotal, MBA

estimateFNMA

estimateFHLMC

estimateMBA

estimate

2019 Q1 359 361 325 34 35 30

2019 Q2 581 584 501 35 36 29

2019 Q3 752 734 651 50 49 42

2019 Q4 770 753 696 57 57 55

2020 Q1 788 670 563 63 60 52

2020 Q2 1106 1008 928 68 67 61

2020 Q3 1283 1114 962 63 60 55

2020 Q4 940 791 937 56 53 55

2016 2052 2125 1891 49 47 49

2017 1826 1810 1760 36 37 35

2018 1766 1700 1677 30 32 28

2019 2462 2432 2253 46 46 44

2020 4117 3582 3390 63 61 56

2021 2721 2685 2561 41 46 36

Sources: Fannie Mae, Freddie Mac, Mortgage Bankers Association and Urban Institute.Note: Shaded boxes indicate forecasted figures. All figures are estimates for total single-family market. Regarding interest rates, the yearly averages for 2016, 2017, 2018 and 2019 were 3.8, 4.0, 4.6, and 3.9 percent. For 2020, the respective projections for Fannie, Freddie, and MBA are 3.1, 3.2, and 2.9 percent. Freddie Mac forecasts are now released quarterly, last updated October 2020.

5.4

0

1

2

3

4

5

6

7

Dollars per $100 loan

Originator Profitability and Unmeasured CostsIn September 2020, Originator Profitability and Unmeasured Costs (OPUC) stood at $5.42 per $100 loan, down slightly from lastmonth’s $5.9, the highest level on record. Increased profitability reflects lender capacity constraints amidst strong refi demand. Additionally, the Fed’s massive purchases of agency MBS since March pushed down secondary yields, thus widening the spread toprimary rates. We would expect OPUC to remain elevated for some time, declining as the backlog of refinance activity is processed, volumes ebb and originators begin to compete more aggressively on price. OPUC, formulated and calculated by the Federal Reserve Bank of New York, is a good relative measure of originator profitability. OPUC uses the sales price of a mortgage in the secondary market (less par) and adds two sources of profitability; retained servicing (both base and excess servicing, net of g-fees), and points paid by the borrower. OPUC is generally high when interest rates are low, as originators are capacity constrained due to refinance demand and have no incentive to reduce rates. Conversely, when interest rates are higher and refi activity low, competition forces originators to lower rates, driving profitability down.

Sources: Federal Reserve Bank of New York, updated monthly and available at this link: http://www.ny.frb.org/research/epr/2013/1113fust.html and Urban Institute. Last updated September 2020.Note: OPUC is a is a monthly (4-week moving) average as discussed in Fuster et al. (2013).

2.5

0

2

4

6

8

10

12

14

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Months of supply

20

SERIOUS DELINQUENCY RAHOUSING SUPPLYSTATE OF THE MARKET

Housing Starts and Home Sales

Housing Starts, thousands Home Sales. thousands

YearTotal,FNMA

estimate

Total, MBA estimate

Total, NAHB

estimate

Total, FNMA

estimate

Total, FHLMC estimate

Total, MBA estimate

Total, NAHB

estimate*

2016 1174 1177 1177 6011 6010 6001 5385

2017 1203 1208 1208 6123 6120 6158 5522

2018 1250 1250 1250 5957 5960 5956 5357

2019 1290 1295 1295 6023 6000 6016 5439

2020 1355 1363 1356 6365 6200 6423 5769

2021 1467 1473 1321 6413 6100 7168 6078

Sources: Mortgage Bankers Association, Fannie Mae, Freddie Mac, National Association of Home Builders and Urban Institute.Note: Shaded boxes indicate forecasted figures; column labels indicate source of estimate. Freddie Mac home sales are now updated quarterly instead of monthly, with the last update in October 2020. *NAHB home sales estimate is for single-family structures only, it excludes condos and co-ops. Other figures include all single-family sales.

Months of Supply

October 2020Source: National Association of Realtors and Urban Institute. Data as of October 2020.

Months of supply in October 2020 was 2.5, 1.4 months lower than it was in October 2019 and a new record low for the second month in a row. Strong demand for housing in recent years, fueled by low mortgage rates, has kept the months supply limited. Fannie Mae, the MBA, and the NAHB forecast 2020 housing starts to be 1.35 to 1.36 million units; these 2020 forecasts from are above 2019 levels. Fannie Mae, Freddie Mac, and the MBA predict total home sales of 6.2 to 6.4 million units in 2020, above 2019 levels.

HOUSING AFFORDABILITYSTATE OF THE MARKET

Despite price increases over the last 8 years, home prices remain affordable by historic standards, as interest rates are now near generational lows. As of October 2020, with a 20 percent down payment, the share of median income needed for the monthly mortgage payment stood at 24.3 percent; with 3.5 down, it is 27.7 percent. These numbers are very close to the 2001-2003 median, and represent a sharp decrease in affordability in recent months. The last time we were at this affordability level was in February of 2019, and before that, in 2008. As shown in the bottom picture, mortgage affordability varies widely by MSA.

National Mortgage Affordability Over Time

0%

5%

10%

15%

20%

25%

30%

35%

40%

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Mortgage affordability with 20% down

Mortgage affordability with 3.5% downMedian housing expenses to income

Average Mortgage Affordability with 3.5% down (2001-2003)

Average Mortgage Affordability with 20% down (2001-2003)

0%10%20%30%40%50%60%70%80%90%

100%

Sa

n F

ran

cisc

o-R

ed

wo

od

Cit

y-S

ou

th S

an

Fra

nci

sco

; CA

Sa

n J

ose

-Su

nn

yv

ale

-Sa

nta

Cla

ra; C

A

Sa

n D

ieg

o-C

arl

sba

d; C

A

Oa

kla

nd

-Hay

war

d-B

erk

ele

y; C

A

Lo

s A

ng

ele

s-L

on

g B

ea

ch-G

len

da

le; C

A

Mia

mi-

Mia

mi B

ea

ch-K

en

da

ll; F

L

Se

att

le-B

ell

ev

ue

-Ev

ere

tt; W

A

Riv

ers

ide

-San

Be

rna

rdin

o-O

nta

rio

; CA

Na

ssa

u C

ou

nty

-Su

ffo

lk C

ou

nty

; NY

De

nv

er-

Au

rora

-Lak

ew

oo

d; C

O

Po

rtla

nd

-Va

nco

uv

er-

Hil

lsb

oro

; OR

-WA

Sa

cra

me

nto

--R

ose

vil

le--

Ard

en

-Arc

ad

e; C

A

La

s V

eg

as-

He

nd

ers

on

-Pa

rad

ise

; NV

Bo

sto

n; M

A

Ne

w Y

ork

-Je

rse

y C

ity

-Wh

ite

Pla

ins;

NY

-NJ

Ne

wa

rk; N

J-P

A

Orl

an

do

-Kis

sim

me

e-S

an

ford

; FL

Ph

oe

nix

-Me

sa-S

cott

sda

le; A

Z

Wa

shin

gto

n-A

rlin

gto

n-A

lex

an

dri

a; D

C-V

A-M

D-W

V

Da

lla

s-P

lan

o-I

rvin

g; T

X

Ta

mp

a-S

t. P

ete

rsb

urg

-Cle

arw

ate

r; F

L

Ho

ust

on

-Th

e W

oo

dla

nd

s-S

ug

ar

La

nd

; TX

Sa

n A

nto

nio

-Ne

w B

rau

nfe

ls; T

X

Ch

ica

go

-Na

pe

rvil

le-A

rlin

gto

n H

eig

hts

; IL

Ch

arl

ott

e-C

on

cord

-Gas

ton

ia; N

C-S

C

Ba

ltim

ore

-Co

lum

bia

-To

wso

n; M

D

Fo

rt W

ort

h-A

rlin

gto

n; T

X

Atl

an

ta-S

an

dy

Sp

rin

gs-

Ro

swe

ll; G

A

Min

ne

apo

lis-

St.

Pa

ul-

Blo

om

ing

ton

; MN

-WI

Co

lum

bu

s; O

H

Ka

nsa

s C

ity

; MO

-KS

St.

Lo

uis

; MO

-IL

Cin

cin

na

ti; O

H-K

Y-I

N

Ph

ila

de

lph

ia; P

A

Cle

ve

lan

d-E

lyri

a; O

H

Pit

tsb

urg

h; P

A

De

tro

it-D

ea

rbo

rn-L

ivo

nia

; MI

Mortgage affordability with 20% downMortgage affordability with 3.5% down

Mortgage affordability index

Mortgage Affordability by MSA

Sources: National Association of Realtors, US Census Bureau, Current Population Survey, American Community Survey, Moody’sAnalytics, Freddie Mac Primary Mortgage Market Survey, and the Urban Institute.Note: Mortgage affordability is the share of median family income devoted to the monthly principal, interest, taxes, and insurance payment required to buy the median home at the Freddie Mac prevailing rate 2018 for a 30-year fixed-rate mortgage and property tax and insurance at 1.75 percent of the housing value. Data for the bottom chart as of Q2 2019.

21

October 2020

5.79

4.04

-15%

-10%

-5%

0%

5%

10%

15%

22

MSA

HPI changes (%)

% above peak2000 to peak

Peak totrough

Trough to current

United States 74.9 -25.2 59.9 19.6

New York-Jersey City-White Plains, NY-NJ 127.7 -22.5 50.4 16.6

Los Angeles-Long Beach-Glendale, CA 179.4 -38.1 95.7 21.1

Chicago-Naperville-Arlington Heights, IL 67.2 -38.4 48.5 -8.6

Atlanta-Sandy Springs-Roswell, GA 32.3 -35.0 85.9 20.8

Washington-Arlington-Alexandria, DC-VA-MD-WV 149.0 -28.3 43.0 2.4

Houston-The Woodlands-Sugar Land, TX 29.2 -6.6 52.2 42.1

Phoenix-Mesa-Scottsdale, AZ 113.1 -51.0 108.5 2.1

Riverside-San Bernardino-Ontario, CA 174.5 -51.6 97.0 -4.7

Dallas-Plano-Irving, TX 26.3 -7.3 71.9 59.4

Minneapolis-St. Paul-Bloomington, MN-WI 69.2 -30.6 67.1 16.0

Seattle-Bellevue-Everett, WA 90.3 -33.1 114.0 43.1

Denver-Aurora-Lakewood, CO 34.1 -12.2 97.7 73.5

Baltimore-Columbia-Towson, MD 123.2 -24.4 24.9 -5.5

San Diego-Carlsbad, CA 148.1 -37.4 85.6 16.1

Anaheim-Santa Ana-Irvine, CA 163.2 -35.2 70.9 10.7

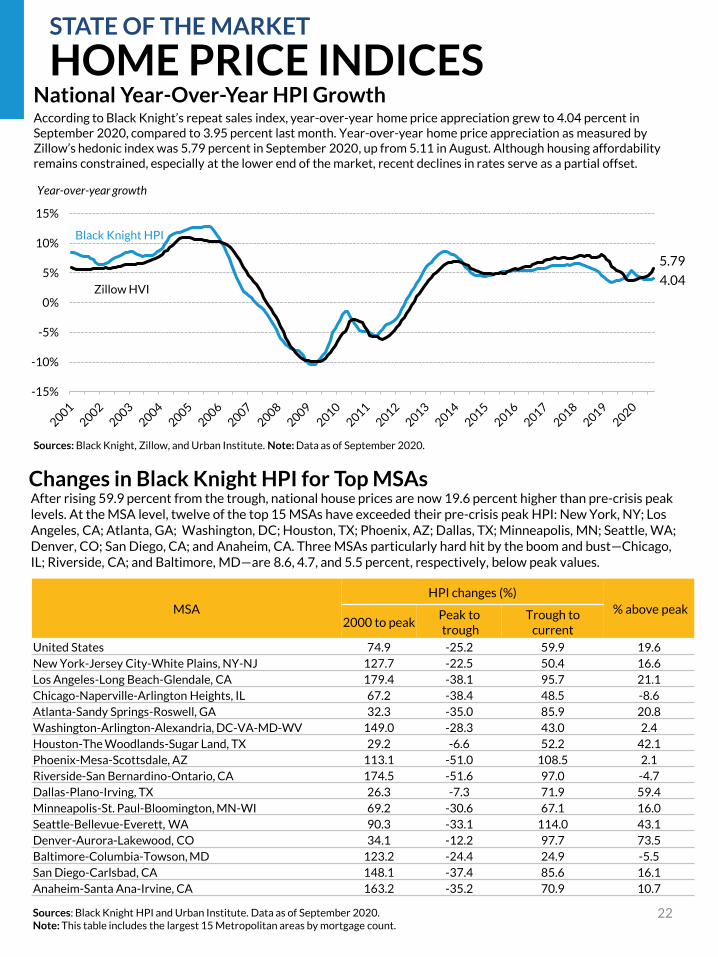

Sources: Black Knight HPI and Urban Institute. Data as of September 2020. Note: This table includes the largest 15 Metropolitan areas by mortgage count.

Changes in Black Knight HPI for Top MSAsAfter rising 59.9 percent from the trough, national house prices are now 19.6 percent higher than pre-crisis peak levels. At the MSA level, twelve of the top 15 MSAs have exceeded their pre-crisis peak HPI: New York, NY; Los Angeles, CA; Atlanta, GA; Washington, DC; Houston, TX; Phoenix, AZ; Dallas, TX; Minneapolis, MN; Seattle, WA; Denver, CO; San Diego, CA; and Anaheim, CA. Three MSAs particularly hard hit by the boom and bust—Chicago, IL; Riverside, CA; and Baltimore, MD—are 8.6, 4.7, and 5.5 percent, respectively, below peak values.

HOME PRICE INDICESSTATE OF THE MARKET

National Year-Over-Year HPI Growth According to Black Knight’s repeat sales index, year-over-year home price appreciation grew to 4.04 percent in September 2020, compared to 3.95 percent last month. Year-over-year home price appreciation as measured by Zillow’s hedonic index was 5.79 percent in September 2020, up from 5.11 in August. Although housing affordability remains constrained, especially at the lower end of the market, recent declines in rates serve as a partial offset.

Sources: Black Knight, Zillow, and Urban Institute. Note: Data as of September 2020.

Black Knight HPI

Zillow HVI

Year-over-year growth

23

FIRST-TIME HOMEBUYERSSTATE OF THE MARKET

20%

30%

40%

50%

60%

70%

80%

90%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

First-Time Homebuyer Share

GSEs FHA VA

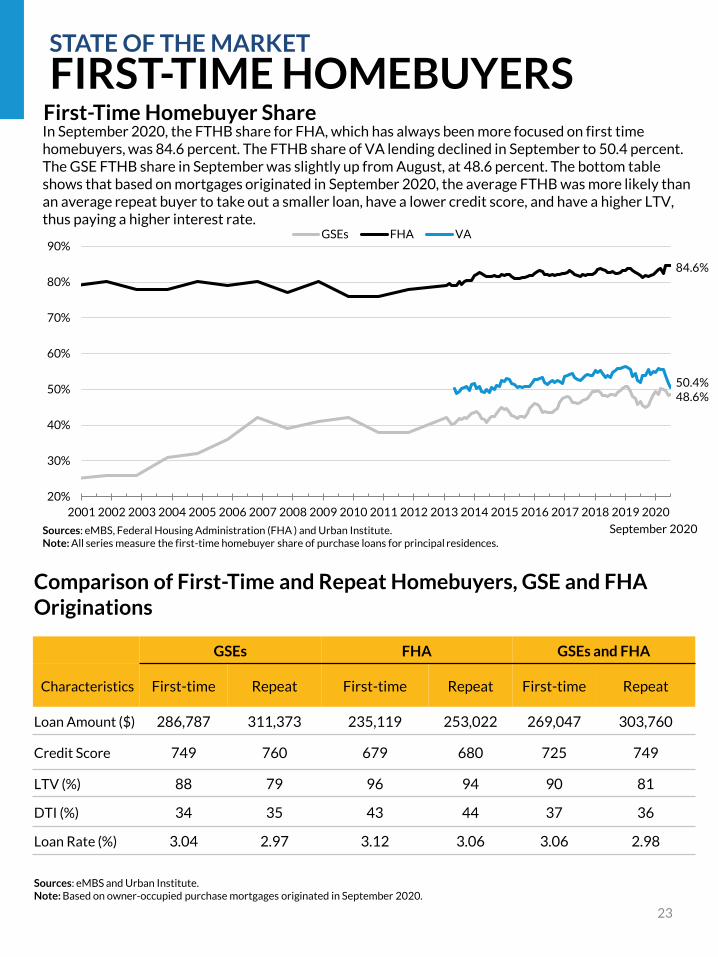

In September 2020, the FTHB share for FHA, which has always been more focused on first time homebuyers, was 84.6 percent. The FTHB share of VA lending declined in September to 50.4 percent. The GSE FTHB share in September was slightly up from August, at 48.6 percent. The bottom table shows that based on mortgages originated in September 2020, the average FTHB was more likely than an average repeat buyer to take out a smaller loan, have a lower credit score, and have a higher LTV, thus paying a higher interest rate.

Sources: eMBS, Federal Housing Administration (FHA ) and Urban Institute.Note: All series measure the first-time homebuyer share of purchase loans for principal residences.

84.6%

50.4%48.6%

Comparison of First-Time and Repeat Homebuyers, GSE and FHA Originations

GSEs FHA GSEs and FHA

Characteristics First-time Repeat First-time Repeat First-time Repeat

Loan Amount ($) 286,787 311,373 235,119 253,022 269,047 303,760

Credit Score 749 760 679 680 725 749

LTV (%) 88 79 96 94 90 81

DTI (%) 34 35 43 44 37 36

Loan Rate (%) 3.04 2.97 3.12 3.06 3.06 2.98

Sources: eMBS and Urban Institute.Note: Based on owner-occupied purchase mortgages originated in September 2020.

September 2020

0

200

400

600

800

1,000

1,200

1,400

1,600

2007Q3-Q4

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019Q1-Q3

Number of loans (thousands)Loan Modifications and Liquidations

Hamp Permanent Mods

Proprietary mods completed

Total liquidations

Sources: Hope Now and Urban Institute.Note: Liquidations include both foreclosure sales and short sales. Last updated March 2020.

STATE OF THE MARKET

DELINQUENCIES AND LOSS MITIGATION ACTIVITY

0%

2%

4%

6%

8%

10%

12%1

Q0

1

1Q

02

1Q

03

1Q

04

1Q

05

1Q

06

1Q

07

1Q

08

1Q

09

1Q

10

1Q

11

1Q

12

1Q

13

1Q

14

1Q

15

1Q

16

1Q

17

1Q

18

1Q

19

1Q

20

Percent of loans 90 days or more delinquent

Percent of loans in foreclosure

Percent of loans 90 days or more delinquent or in foreclosure

Sources: Mortgage Bankers Association and Urban Institute. Last updated September 2020.

0%

5%

10%

15%

20%

25%

30%

35%

1Q

11

4Q

11

3Q

12

2Q

13

1Q

14

4Q

14

3Q

15

2Q

16

1Q

17

4Q

17

3Q

18

2Q

19

1Q

20

Negative Equity ShareNegative equity Near or in negative equity

Sources: CoreLogic and Urban Institute.Note: Loans with negative equity refer to loans above 100 percent LTV. Loans near negative equity refer to loans above 95 percent LTV. Last updated September 2020.

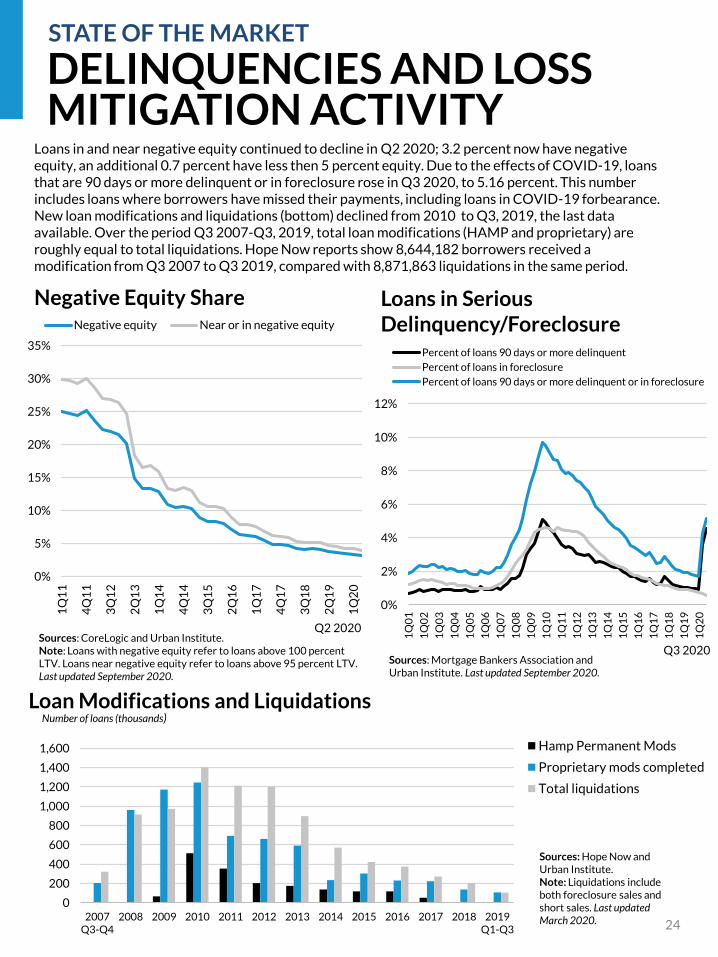

Loans in and near negative equity continued to decline in Q2 2020; 3.2 percent now have negative equity, an additional 0.7 percent have less then 5 percent equity. Due to the effects of COVID-19, loans that are 90 days or more delinquent or in foreclosure rose in Q3 2020, to 5.16 percent. This number includes loans where borrowers have missed their payments, including loans in COVID-19 forbearance. New loan modifications and liquidations (bottom) declined from 2010 to Q3, 2019, the last data available. Over the period Q3 2007-Q3, 2019, total loan modifications (HAMP and proprietary) are roughly equal to total liquidations. Hope Now reports show 8,644,182 borrowers received a modification from Q3 2007 to Q3 2019, compared with 8,871,863 liquidations in the same period.

Loans in Serious Delinquency/Foreclosure

24

Q3 2020

Q2 2020

25

Even though the Fannie Mae and Freddie Mac portfolios are well below the $250 billion size they were required to reach by year-end 2018, the portfolios have continued to shrink. From September 2019 to September 2020, the Fannie portfolio contracted by 2.8 percent, and the Freddie portfolio contracted by 10.6 percent. Within the portfolio, Fannie Mae held their less liquid assets (mortgage loans, non-agency MBS), relatively constant from the year prior, while Freddie Mac increased theirs. This reflects both a smaller overall portfolio and the increased need to hold loans in portfolio for loss mitigation purposes.

GSE PORTFOLIO WIND-DOWNGSES UNDER CONSERVATORSHIP

0

100

200

300

400

500

600

700

800

900

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

($ billions)

FHLMC MBS in portfolio Non-FHLMC agency MBS Non-agency MBS Mortgage loans

Sources: Freddie Mac and Urban Institute.

Freddie Mac Mortgage-Related Investment Portfolio Composition

Current size: $198.2 billion2018 cap: $250 billionShrinkage year-over-year: 10.6 percentGrowth in less-liquid assets year-over-year: 9.5 percent

0

100

200

300

400

500

600

700

800

900

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

($ billions)

FNMA MBS in portfolio Non-FNMA agency MBS Non-agency MBS Mortgage loans

Fannie Mae Mortgage-Related Investment Portfolio Composition

Current size: $172.1 billion2018 cap: $250 billionShrinkage year-over-year: 2.8 percentShrinkage in less-liquid assets year-over-year: 1.2 percent

September 2020

September 2020

Sources: Fannie Mae and Urban Institute.

26

GSES UNDER CONSERVATORSHIP

EFFECTIVE GUARANTEE FEES

Fannie Mae Upfront Loan-Level Price Adjustments (LLPAs)

LTV (%)

Credit Score ≤60 60.01 – 70 70.01 – 75 75.01 – 80 80.01 – 85 85.01 – 90 90.01 – 95 95.01 – 97 >97

> 740 0.00 0.25 0.25 0.50 0.25 0.25 0.25 0.75 0.75

720 – 739 0.00 0.25 0.50 0.75 0.50 0.50 0.50 1.00 1.00

700 – 719 0.00 0.50 1.00 1.25 1.00 1.00 1.00 1.50 1.50

680 – 699 0.00 0.50 1.25 1.75 1.50 1.25 1.25 1.50 1.50

660 – 679 0.00 1.00 2.25 2.75 2.75 2.25 2.25 2.25 2.25

640 – 659 0.50 1.25 2.75 3.00 3.25 2.75 2.75 2.75 2.75

620 – 639 0.50 1.50 3.00 3.00 3.25 3.25 3.25 3.50 3.50

< 620 0.50 1.50 3.00 3.00 3.25 3.25 3.25 3.75 3.75

Product Feature (Cumulative)

Investment Property 2.125 2.125 2.125 3.375 4.125 4.125 4.125 4.125 4.125

Sources: Fannie Mae and Urban Institute.Last updated March of 2019.

56.054.9

0

10

20

30

40

50

60

70

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

2Q

18

4Q

18

2Q

19

4Q

19

2Q

20

Guarantee Fees Charged on New AcquisitionsFannie Mae single-family average charged g-fee on new acquisitions

Freddie Mac single-family guarantee fees charged on new acquisitions

Basis points

Sources: Fannie Mae, Freddie Mae and Urban Institute. Last updated November 2020.

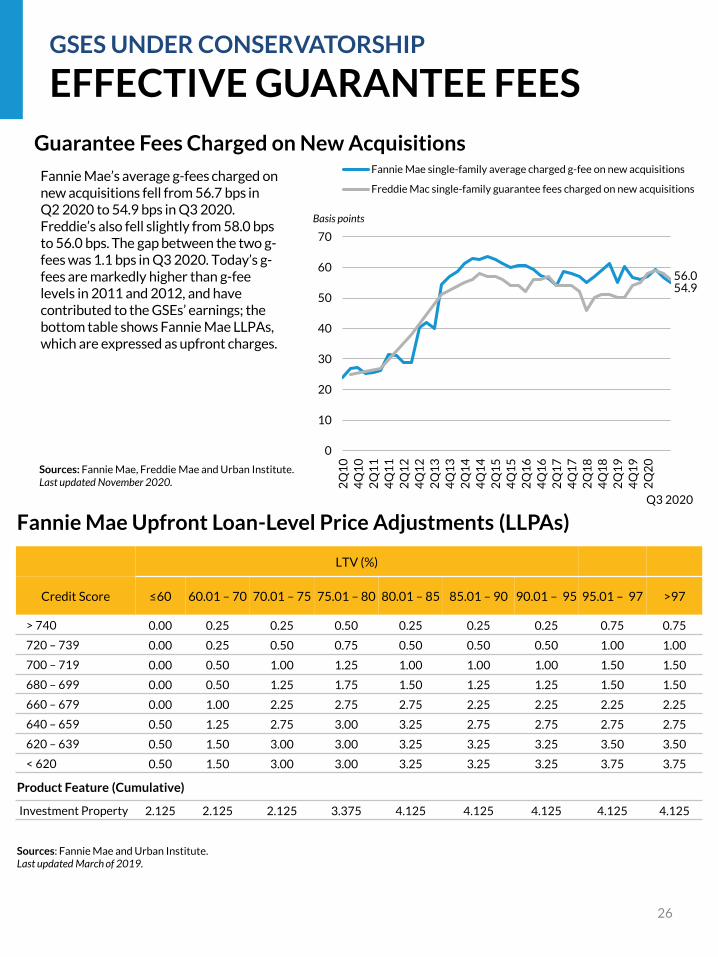

Fannie Mae’s average g-fees charged on new acquisitions fell from 56.7 bps in Q2 2020 to 54.9 bps in Q3 2020. Freddie’s also fell slightly from 58.0 bps to 56.0 bps. The gap between the two g-fees was 1.1 bps in Q3 2020. Today’s g-fees are markedly higher than g-fee levels in 2011 and 2012, and have contributed to the GSEs’ earnings; the bottom table shows Fannie Mae LLPAs, which are expressed as upfront charges.

Q3 2020

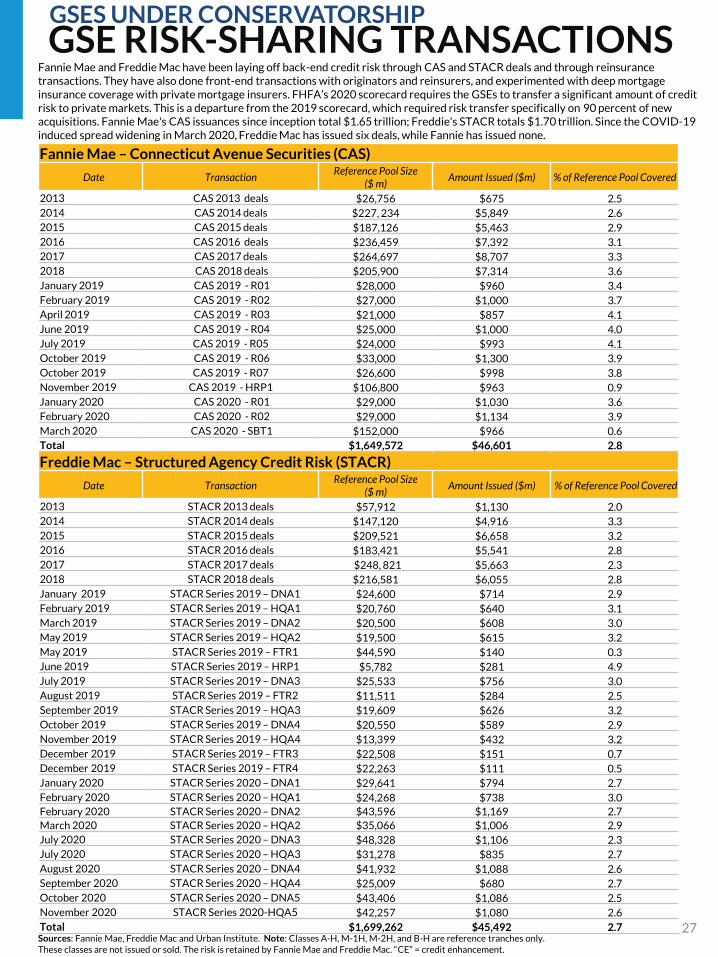

GSE RISK-SHARING TRANSACTIONS

Sources: Fannie Mae, Freddie Mac and Urban Institute. Note: Classes A-H, M-1H, M-2H, and B-H are reference tranches only. These classes are not issued or sold. The risk is retained by Fannie Mae and Freddie Mac. “CE” = credit enhancement.

27

GSES UNDER CONSERVATORSHIP

Fannie Mae – Connecticut Avenue Securities (CAS)

Date TransactionReference Pool Size

($ m)Amount Issued ($m) % of Reference Pool Covered

2013 CAS 2013 deals $26,756 $675 2.5

2014 CAS 2014 deals $227, 234 $5,849 2.6

2015 CAS 2015 deals $187,126 $5,463 2.9

2016 CAS 2016 deals $236,459 $7,392 3.1

2017 CAS 2017 deals $264,697 $8,707 3.3

2018 CAS 2018 deals $205,900 $7,314 3.6

January 2019 CAS 2019 - R01 $28,000 $960 3.4

February 2019 CAS 2019 - R02 $27,000 $1,000 3.7

April 2019 CAS 2019 - R03 $21,000 $857 4.1

June 2019 CAS 2019 - R04 $25,000 $1,000 4.0

July 2019 CAS 2019 - R05 $24,000 $993 4.1

October 2019 CAS 2019 - R06 $33,000 $1,300 3.9

October 2019 CAS 2019 - R07 $26,600 $998 3.8

November 2019 CAS 2019 - HRP1 $106,800 $963 0.9

January 2020 CAS 2020 - R01 $29,000 $1,030 3.6

February 2020 CAS 2020 - R02 $29,000 $1,134 3.9

March 2020 CAS 2020 - SBT1 $152,000 $966 0.6

Total $1,649,572 $46,601 2.8

Freddie Mac – Structured Agency Credit Risk (STACR)

Date TransactionReference Pool Size

($ m)Amount Issued ($m) % of Reference Pool Covered

2013 STACR 2013 deals $57,912 $1,130 2.0

2014 STACR 2014 deals $147,120 $4,916 3.3

2015 STACR 2015 deals $209,521 $6,658 3.2

2016 STACR 2016 deals $183,421 $5,541 2.8

2017 STACR 2017 deals $248, 821 $5,663 2.3

2018 STACR 2018 deals $216,581 $6,055 2.8

January 2019 STACR Series 2019 – DNA1 $24,600 $714 2.9

February 2019 STACR Series 2019 – HQA1 $20,760 $640 3.1

March 2019 STACR Series 2019 – DNA2 $20,500 $608 3.0

May 2019 STACR Series 2019 – HQA2 $19,500 $615 3.2

May 2019 STACR Series 2019 – FTR1 $44,590 $140 0.3

June 2019 STACR Series 2019 – HRP1 $5,782 $281 4.9

July 2019 STACR Series 2019 – DNA3 $25,533 $756 3.0

August 2019 STACR Series 2019 – FTR2 $11,511 $284 2.5

September 2019 STACR Series 2019 – HQA3 $19,609 $626 3.2

October 2019 STACR Series 2019 – DNA4 $20,550 $589 2.9

November 2019 STACR Series 2019 – HQA4 $13,399 $432 3.2

December 2019 STACR Series 2019 – FTR3 $22,508 $151 0.7

December 2019 STACR Series 2019 – FTR4 $22,263 $111 0.5

January 2020 STACR Series 2020 – DNA1 $29,641 $794 2.7

February 2020 STACR Series 2020 – HQA1 $24,268 $738 3.0

February 2020 STACR Series 2020 – DNA2 $43,596 $1,169 2.7

March 2020 STACR Series 2020 – HQA2 $35,066 $1,006 2.9

July 2020 STACR Series 2020 – DNA3 $48,328 $1,106 2.3

July 2020 STACR Series 2020 – HQA3 $31,278 $835 2.7

August 2020 STACR Series 2020 – DNA4 $41,932 $1,088 2.6

September 2020 STACR Series 2020 – HQA4 $25,009 $680 2.7

October 2020 STACR Series 2020 – DNA5 $43,406 $1,086 2.5

November 2020 STACR Series 2020-HQA5 $42,257 $1,080 2.6

Total $1,699,262 $45,492 2.7

Fannie Mae and Freddie Mac have been laying off back-end credit risk through CAS and STACR deals and through reinsurance transactions. They have also done front-end transactions with originators and reinsurers, and experimented with deep mortgage insurance coverage with private mortgage insurers. FHFA’s 2020 scorecard requires the GSEs to transfer a significant amount of credit risk to private markets. This is a departure from the 2019 scorecard, which required risk transfer specifically on 90 percent of new acquisitions. Fannie Mae's CAS issuances since inception total $1.65 trillion; Freddie's STACR totals $1.70 trillion. Since the COVID-19 induced spread widening in March 2020, Freddie Mac has issued six deals, while Fannie has issued none.

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Ma

r-1

7M

ay

-17

Jul-

17

Se

p-1

7N

ov

-17

Jan

-18

Ma

r-1

8M

ay

-18

Jul-

18

Se

p-1

8N

ov

-18

Jan

-19

Ma

r-1

9M

ay

-19

Jul-

19

Se

p-1

9N

ov

-19

Jan

-20

Ma

r-2

0M

ay

-20

Jul-

20

Se

p-2

0N

ov

-20

2014/15 Low Index 2016 Low Index

2017 Low Index 2018 Low Index

2019 Low Index

28Sources: Vista Data Services and Urban Institute. Note: Data as of November 13, 2020.

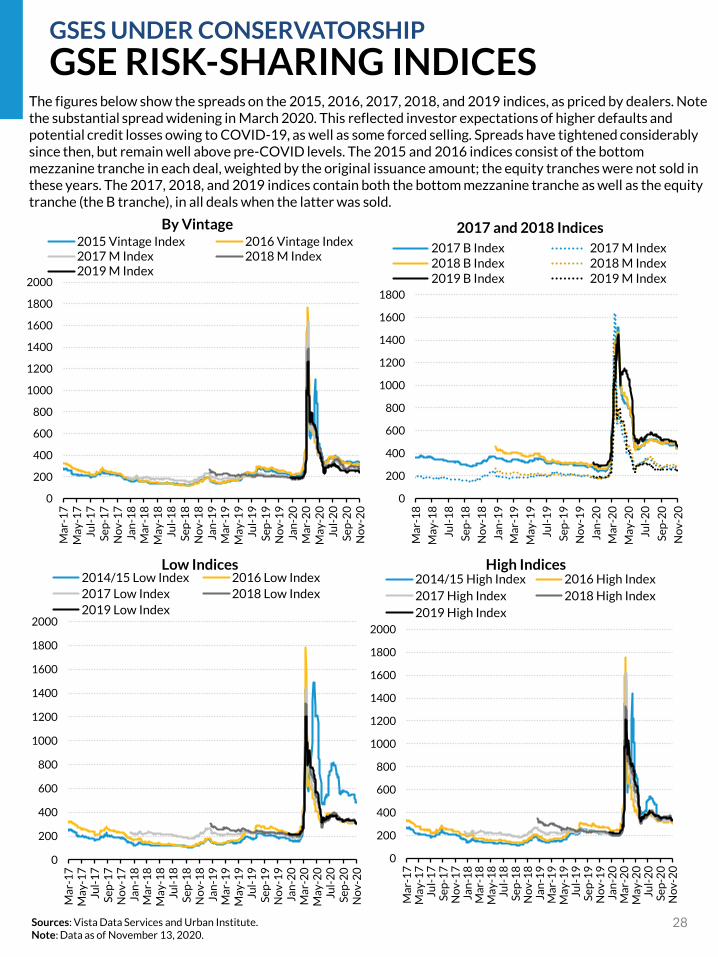

GSE RISK-SHARING INDICESGSES UNDER CONSERVATORSHIP

The figures below show the spreads on the 2015, 2016, 2017, 2018, and 2019 indices, as priced by dealers. Note the substantial spread widening in March 2020. This reflected investor expectations of higher defaults and potential credit losses owing to COVID-19, as well as some forced selling. Spreads have tightened considerably since then, but remain well above pre-COVID levels. The 2015 and 2016 indices consist of the bottom mezzanine tranche in each deal, weighted by the original issuance amount; the equity tranches were not sold in these years. The 2017, 2018, and 2019 indices contain both the bottom mezzanine tranche as well as the equity tranche (the B tranche), in all deals when the latter was sold.

0

200

400

600

800

1000

1200

1400

1600

1800

Ma

r-1

8

Ma

y-1

8

Jul-

18

Se

p-1

8

No

v-1

8

Jan

-19

Ma

r-1

9

Ma

y-1

9

Jul-

19

Se

p-1

9

No

v-1

9

Jan

-20

Ma

r-2

0

Ma

y-2

0

Jul-

20

Se

p-2

0

No

v-2

0

2017 B Index 2017 M Index2018 B Index 2018 M Index2019 B Index 2019 M Index

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Ma

r-1

7M

ay

-17

Jul-

17

Se

p-1

7N

ov

-17

Jan

-18

Ma

r-1

8M

ay

-18

Jul-

18

Se

p-1

8N

ov

-18

Jan

-19

Ma

r-1

9M

ay

-19

Jul-

19

Se

p-1

9N

ov

-19

Jan

-20

Ma

r-2

0M

ay

-20

Jul-

20

Se

p-2

0N

ov

-20

2015 Vintage Index 2016 Vintage Index2017 M Index 2018 M Index2019 M Index

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Ma

r-1

7M

ay

-17

Jul-

17

Se

p-1

7N

ov

-17

Jan

-18

Ma

r-1

8M

ay

-18

Jul-

18

Se

p-1

8N

ov

-18

Jan

-19

Ma

r-1

9M

ay

-19

Jul-

19

Se

p-1

9N

ov

-19

Jan

-20

Ma

r-2

0M

ay

-20

Jul-

20

Se

p-2

0N

ov

-20

2014/15 High Index 2016 High Index

2017 High Index 2018 High Index

2019 High Index

Low Indices High Indices

By Vintage 2017 and 2018 Indices

28

29

SERIOUS DELINQUENCY RATESGSES UNDER CONSERVATORSHIP

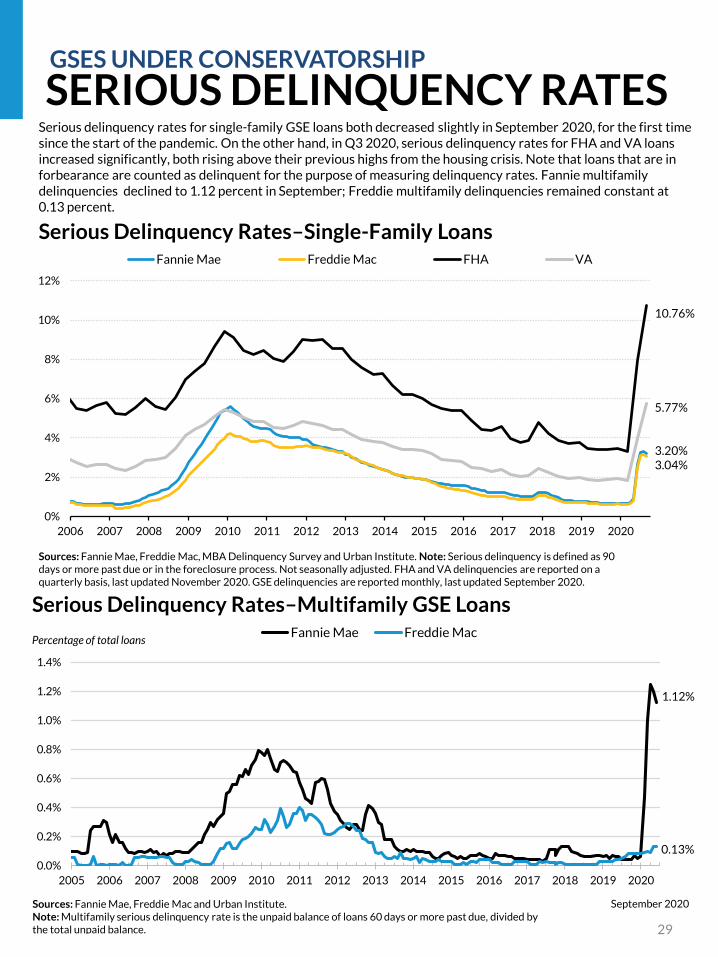

Serious delinquency rates for single-family GSE loans both decreased slightly in September 2020, for the first time since the start of the pandemic. On the other hand, in Q3 2020, serious delinquency rates for FHA and VA loans increased significantly, both rising above their previous highs from the housing crisis. Note that loans that are in forbearance are counted as delinquent for the purpose of measuring delinquency rates. Fannie multifamily delinquencies declined to 1.12 percent in September; Freddie multifamily delinquencies remained constant at 0.13 percent.

0.13%

1.12%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Percentage of total loans

Serious Delinquency Rates–Multifamily GSE LoansFannie Mae Freddie Mac

Sources: Fannie Mae, Freddie Mac and Urban Institute.Note: Multifamily serious delinquency rate is the unpaid balance of loans 60 days or more past due, divided by the total unpaid balance.

September 2020

0%

2%

4%

6%

8%

10%

12%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Fannie Mae Freddie Mac FHA VA

Sources: Fannie Mae, Freddie Mac, MBA Delinquency Survey and Urban Institute. Note: Serious delinquency is defined as 90 days or more past due or in the foreclosure process. Not seasonally adjusted. FHA and VA delinquencies are reported on a quarterly basis, last updated November 2020. GSE delinquencies are reported monthly, last updated September 2020.

Serious Delinquency Rates–Single-Family Loans

10.76%

5.77%

3.20%3.04%

30

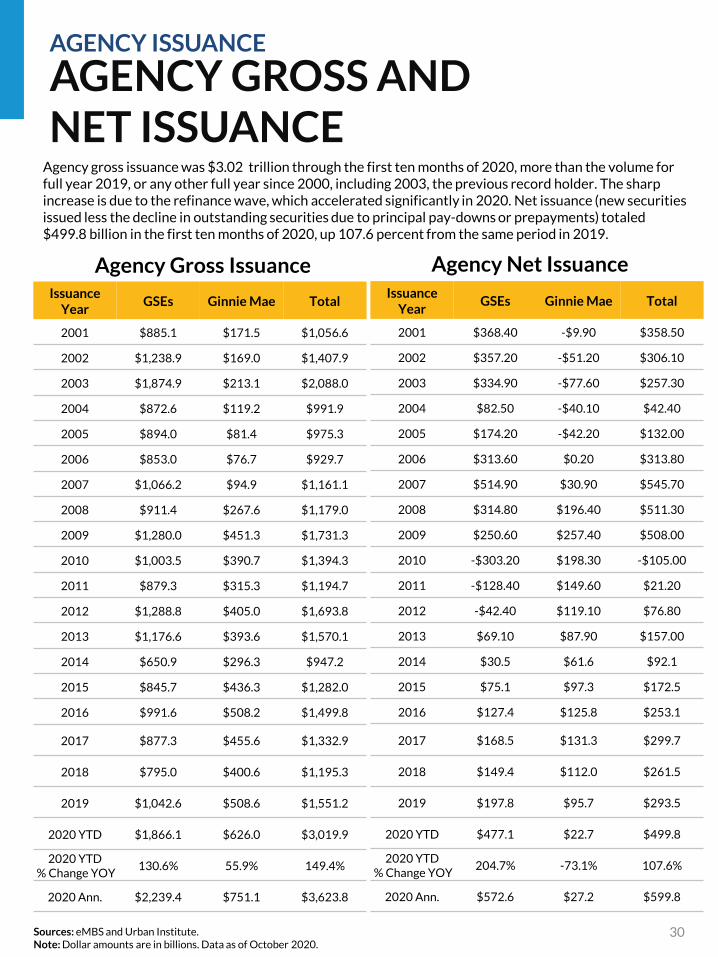

Agency Gross Issuance Agency Net Issuance

AGENCY GROSS AND NET ISSUANCE

AGENCY ISSUANCE

Issuance Year

GSEs Ginnie Mae Total

2001 $885.1 $171.5 $1,056.6

2002 $1,238.9 $169.0 $1,407.9

2003 $1,874.9 $213.1 $2,088.0

2004 $872.6 $119.2 $991.9

2005 $894.0 $81.4 $975.3

2006 $853.0 $76.7 $929.7

2007 $1,066.2 $94.9 $1,161.1

2008 $911.4 $267.6 $1,179.0

2009 $1,280.0 $451.3 $1,731.3

2010 $1,003.5 $390.7 $1,394.3

2011 $879.3 $315.3 $1,194.7

2012 $1,288.8 $405.0 $1,693.8

2013 $1,176.6 $393.6 $1,570.1

2014 $650.9 $296.3 $947.2

2015 $845.7 $436.3 $1,282.0

2016 $991.6 $508.2 $1,499.8

2017 $877.3 $455.6 $1,332.9

2018 $795.0 $400.6 $1,195.3

2019 $1,042.6 $508.6 $1,551.2

2020 YTD $1,866.1 $626.0 $3,019.9

2020 YTD% Change YOY

130.6% 55.9% 149.4%

2020 Ann. $2,239.4 $751.1 $3,623.8

Agency gross issuance was $3.02 trillion through the first ten months of 2020, more than the volume for full year 2019, or any other full year since 2000, including 2003, the previous record holder. The sharp increase is due to the refinance wave, which accelerated significantly in 2020. Net issuance (new securities issued less the decline in outstanding securities due to principal pay-downs or prepayments) totaled $499.8 billion in the first ten months of 2020, up 107.6 percent from the same period in 2019.

Sources: eMBS and Urban Institute.Note: Dollar amounts are in billions. Data as of October 2020.

Issuance Year

GSEs Ginnie Mae Total

2001 $368.40 -$9.90 $358.50

2002 $357.20 -$51.20 $306.10

2003 $334.90 -$77.60 $257.30

2004 $82.50 -$40.10 $42.40

2005 $174.20 -$42.20 $132.00

2006 $313.60 $0.20 $313.80

2007 $514.90 $30.90 $545.70

2008 $314.80 $196.40 $511.30

2009 $250.60 $257.40 $508.00

2010 -$303.20 $198.30 -$105.00

2011 -$128.40 $149.60 $21.20

2012 -$42.40 $119.10 $76.80

2013 $69.10 $87.90 $157.00

2014 $30.5 $61.6 $92.1

2015 $75.1 $97.3 $172.5

2016 $127.4 $125.8 $253.1

2017 $168.5 $131.3 $299.7

2018 $149.4 $112.0 $261.5

2019 $197.8 $95.7 $293.5

2020 YTD $477.1 $22.7 $499.8

2020 YTD% Change YOY

204.7% -73.1% 107.6%

2020 Ann. $572.6 $27.2 $599.8

0

50

100

150

200

250

300

350

400($ billions)

Fed Absorption of Agency Gross Issuance

Gross issuance Total Fed purchases

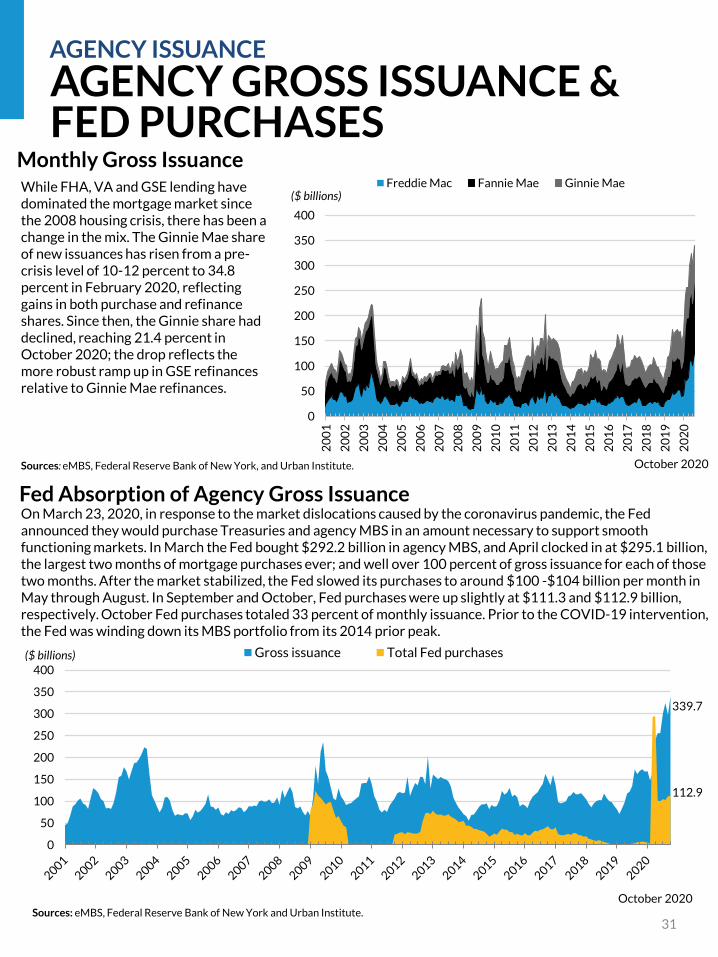

On March 23, 2020, in response to the market dislocations caused by the coronavirus pandemic, the Fed announced they would purchase Treasuries and agency MBS in an amount necessary to support smooth functioning markets. In March the Fed bought $292.2 billion in agency MBS, and April clocked in at $295.1 billion, the largest two months of mortgage purchases ever; and well over 100 percent of gross issuance for each of those two months. After the market stabilized, the Fed slowed its purchases to around $100 -$104 billion per month in May through August. In September and October, Fed purchases were up slightly at $111.3 and $112.9 billion, respectively. October Fed purchases totaled 33 percent of monthly issuance. Prior to the COVID-19 intervention, the Fed was winding down its MBS portfolio from its 2014 prior peak.

Sources: eMBS, Federal Reserve Bank of New York and Urban Institute.

October 2020

339.7

112.9

31

AGENCY GROSS AND NET ISSUANCE BY MONTH

AGENCY ISSUANCE

AGENCY GROSS ISSUANCE & FED PURCHASES

0

50

100

150

200

250

300

350

400

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

($ billions)

Monthly Gross IssuanceFreddie Mac Fannie Mae Ginnie Mae

October 2020Sources: eMBS, Federal Reserve Bank of New York, and Urban Institute.

While FHA, VA and GSE lending have dominated the mortgage market since the 2008 housing crisis, there has been a change in the mix. The Ginnie Mae share of new issuances has risen from a pre-crisis level of 10-12 percent to 34.8 percent in February 2020, reflecting gains in both purchase and refinance shares. Since then, the Ginnie share had declined, reaching 21.4 percent in October 2020; the drop reflects the more robust ramp up in GSE refinances relative to Ginnie Mae refinances.

32

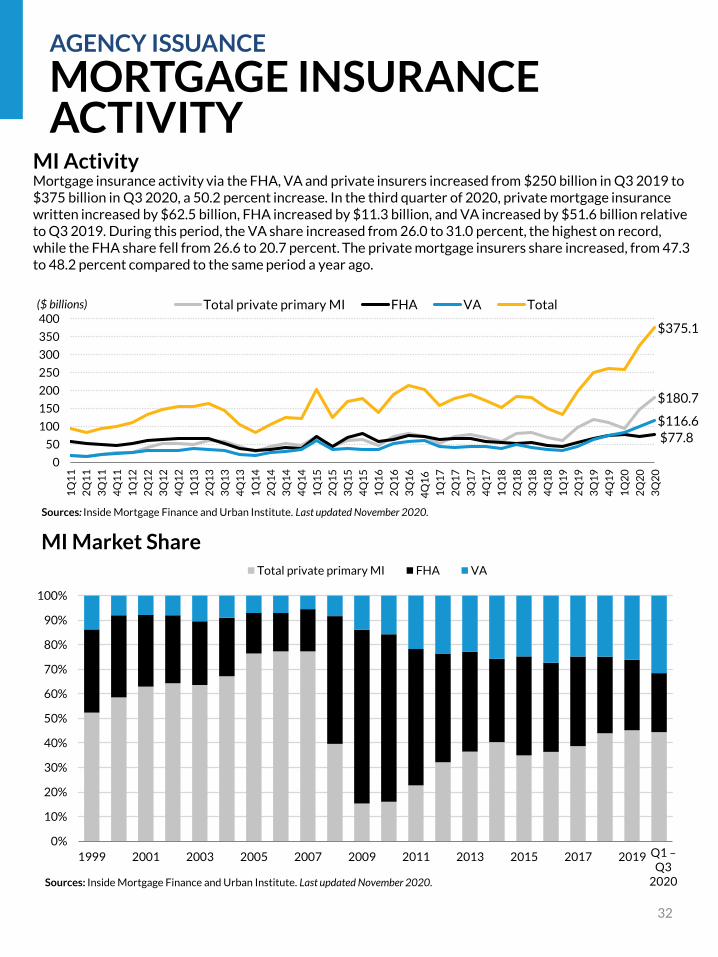

MORTGAGE INSURANCE ACTIVITY

AGENCY ISSUANCE

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

MI Market Share Total private primary MI FHA VA

Sources: Inside Mortgage Finance and Urban Institute. Last updated November 2020.

$180.7

$77.8

$116.6

$375.1

0

50

100

150

200

250

300

350

400

1Q

11

2Q