![PM 2014 investor day 2014-06-26-Operations Investor Day Slides [FINAL]](https://static.fdocuments.us/doc/165x107/577cbc651a28aba7118da314/pm-2014-investor-day-2014-06-26-operations-investor-day-slides-final.jpg)

![PM 2014 investor day 2014-06-26-CEO Investor Day Slides [FINAL]](https://static.fdocuments.us/doc/165x107/577cbc651a28aba7118da313/pm-2014-investor-day-2014-06-26-ceo-investor-day-slides-final.jpg)

Languages

Pages

Legal

HAWAIIAN AIRLINES INVESTOR DAY December 2, 2015

This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act

of 1995 that reflect the Company’s current views with respect to certain current and future events and financial

performance. Words such as “expects,” “anticipates,” “projects,” “intends,” “plans,” “believes,” “estimates,” variations of

such words, and similar expressions are also intended to identify such forward-looking statements. These forward-looking

statements are and will be, as the case may be, subject to many risks, uncertainties and assumptions relating to the

Company’s operations and business environment, all of which may cause the Company’s actual results to be materially

different from any future results, expressed or implied, in these forward-looking statements. These risks and uncertainties

include, without limitation, the Company’s ability to accurately forecast quarter and year-end results; economic volatility;

the price and availability of aircraft fuel; fluctuations in demand for transportation in the markets in which the Company

operates; the Company’s dependence on tourist travel; foreign currency exchange rate fluctuations; and the Company’s

ability to implement its growth strategy.

The risks, uncertainties and assumptions referred to above that could cause the Company’s results to differ materially from

the results expressed or implied by such forward-looking statements also include the risks, uncertainties and assumptions

discussed from time to time in the Company’s public filings and public announcements, including the Company’s Annual

Report on Form 10-K for the year ended December 31, 2014 and the Company’s Quarterly Reports on Form 10-Q, as well

as other documents that may be filed by the Company from time to time with the Securities and Exchange Commission. All

forward-looking statements included in this document are based on information available to the Company on the date

hereof. The Company does not undertake to publicly update or revise any forward-looking statements to reflect events or

circumstances that may arise after the date hereof even if experience or future changes make it clear that any projected

results expressed or implied herein will not be realized.

Forward-looking statements

MARK DUNKERLEY President and Chief Executive Officer

Today’s agenda

Commercial presentation

Finance presentation

Closing remarks

Lunch

• 9:00 a.m.

• 10:45 a.m.

• 11:15 a.m.

• 11:30 a.m.

LOOKING BACK

Tokyo

Beijing

Auckland

New York City

Beijing

Auckland

New York City

Tokyo

Beijing

Auckland

New York City

30%

62%

8%

2009 2015

North America Neighbor Island International

25%

53%

22%

Passenger Revenue

CURRENT

Our financial performance has improved

• Record earnings

• Record margins

• Stronger balance sheet

S&P

Jan

. 20

10

No

v. 2

01

5

Jan

. 2

01

3

Jan

. 20

15

Jan

. 20

11

SMALLCAP 600

$7

.10

$7

.92

$5

.78

$6

.74

$9

.62

Ja

n. 2

01

4

Jan

. 2

01

2

$2

5.2

7

$3

5.3

1

#1 On-Time

NEXT 18 MONTHS

Our greatest asset

Strengthen competitive

position Achieve mastery

Grow long-term shareholder value

2016 is going to be…

a better year than 2015.

PETER INGRAM Executive Vice President, Chief Commercial Officer

Improving trend for domestic unit revenue

Note: Capacity is defined as the industry seats from the West Coast to Hawai‘i in HA’s markets

9.6%

4.0%

-4.7% -2.9%

-8.6% -8.1%

-1.5% -1%

6% 9%

11% 10% 13%

6% 5%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

PRASM yoy Annual capacity growth

Underlying international market performance improving…

2014 MarketPerformanceand Network

Changes

FX Fuel Surcharge 2015

International PRASM

…but FX and Fuel surcharges offset improvements

2014 MarketPerformanceand Network

Changes

FX Fuel Surcharge 2015

International PRASM

¥100

¥105

¥110

¥115

¥120

¥125

Jan Mar May Jul Sep Nov

FX headwinds weighed on 2015 unit revenue

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

Jan Mar May Jul Sep Nov

2014

AUD / $ JPY / $

2015

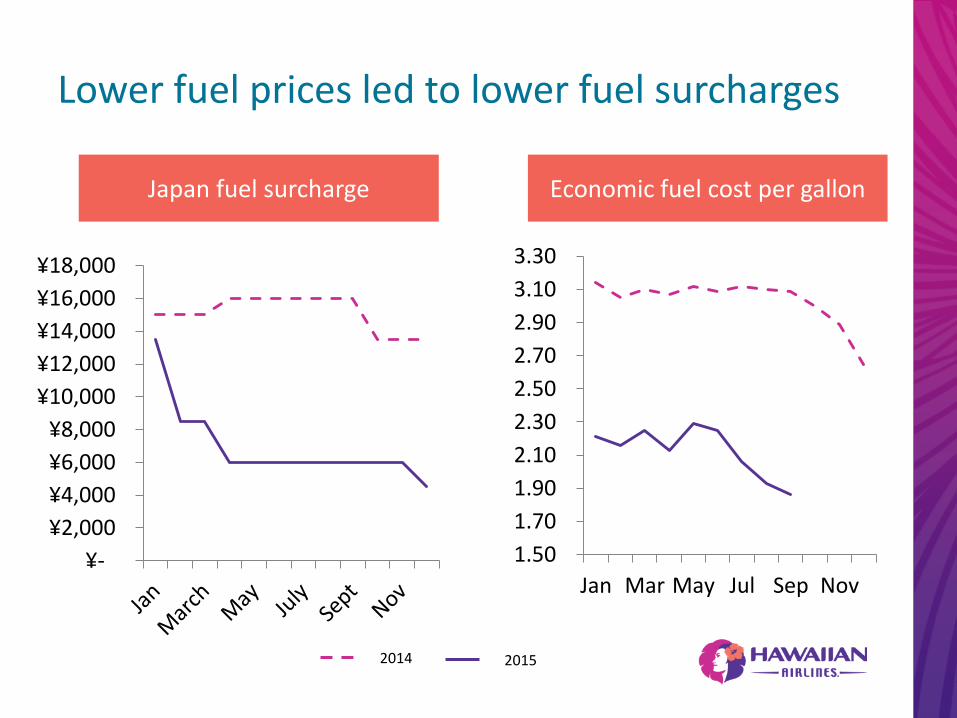

Lower fuel prices led to lower fuel surcharges

¥-

¥2,000

¥4,000

¥6,000

¥8,000

¥10,000

¥12,000

¥14,000

¥16,000

¥18,000

1.50

1.70

1.90

2.10

2.30

2.50

2.70

2.90

3.10

3.30

Jan Mar May Jul Sep Nov

Japan fuel surcharge Economic fuel cost per gallon

2014 2015

FLEET EVOLUTION

NETWORK EVOLUTION

PRODUCT EVOLUTION

ANCILLARY / OTHER

PRODUCT EVOLUTION

Best fleet for our missions

Aircraft: A321neo

Quantity: 16 on order delivery starting 2017

Aircraft: A330-200

Quantity: 23

Aircraft: B717

Quantity: 18

A330 allows us to grow into longer-haul destinations

Tokyo

Beijing

Auckland

Beijing

Tokyo New York City

A321neo (189 seats)

737-8Max (156 seats)

737-9Max (177 seats)

737-800 (157 seats)

A321-200 (181 seats)

A320-200 (146 seats)

Trip

Co

st

Seat Mile Cost

A321neo – most cost effective aircraft for the West Coast to Hawai‘i mission

Note: Fuel price adjusted to $2.05 per gallon Variable + Ownership Costs

Delivery of the A321neos allows for the A330 to be redeployed for longer-haul missions

2015 2020

ASMs Departures Block hours

2015 2020

Flights of 8 or more hours

2015 2020

70%

0%

Neighbor Island network

LĀNA‘I

LĪHU‘E

KONA

HILO

MAUI

HONOLULU

• 160 daily flights • ~ 90% seat share • 2/3 is local traffic

B717

ATR42

B717 / ATR42

MOLOKA‘I

18 B717 retrofitted to a standard seat count of 128 seats

125 additional seats

Equivalent to one additional B717

B717 interior retrofits

FLEET EVOLUTION

NETWORK EVOLUTION

PRODUCT EVOLUTION

ANCILLARY / OTHER

PRODUCT EVOLUTION

FLEET EVOLUTION

NETWORK EVOLUTION

PRODUCT EVOLUTION

ANCILLARY / OTHER

PRODUCT EVOLUTION

BRENT OVERBEEK Vice President - Revenue Management & Network Planning

Upgauge Peak-PeriodFrequencyIncreases

Off-PeakFrequencyReductions

NRT Other

2016: Moderate capacity growth

2011 2012 2013 2014 2015E 2016E

Up 3% to 5%

Year-over-Year ASM Growth

Composition of Projected 2016 ASM growth

19% 22%

14%

Up 2.5% to 5.5% 2%

2.5% to 5.5%

Due to the solid demand in Japan, we are growing in Tokyo

• Launching daily Narita-

Honolulu service in summer

2016

• Japan is the largest source of

international visitors to Hawai‘i

• Our Haneda-Honolulu route

averages >90% load factor

• With this addition, we will have

a 20% seat share in the Japan-

Hawai‘i market

Strong West Coast position to grow from

Source: USDOT DB1B, Innovata schedules

LAX-HNL

SFO-HNL

OGG-LAX

SEA-HNL

LAS-HNL

PHX-HNL SJC-HNL

SEA-OGG

SAN-HNL

PDX-HNL

OGG-OAK

SJC-OGG

OAK-HNL

SMF-HNL

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

HA

sh

are

of

no

nst

op

O&

D

HA seat share

Passenger share > seat share

Nonstop O&D pax share vs. seat share, YE 2Q15

Passenger share < seat share

Outperforming competitors on the West Coast

Hawaiian Airlines West Coast PRASM Premium, YE2Q15

HNL OGG

LAX

SFO

OAK

SJC

SEA

LAS

PDX

SAN

PHX

Over 10%

2% to 10%

-2% to 2%

Below -2%

*

* SFO-OGG 1H15 only

Source: Estimates based on USDOT DB1B and T100

433

791 102

289

45

101

2011 1H15

Intra-Hawaii connect via OGG

West Coast-Hawaii connect via OGG

West Coast-OGG nonstop

Successful development of the Maui hub

631

1,439

2011 2012 2013 2014 2015

HA West Coast-OGG Daily Seats HA PDEW to/via OGG, YE2Q15

+126%

+184%

+83%

SFO

SJC

SEA

OAK

LAX

PDX

LAS

Source: Innovata schedules, USDOT DB1B

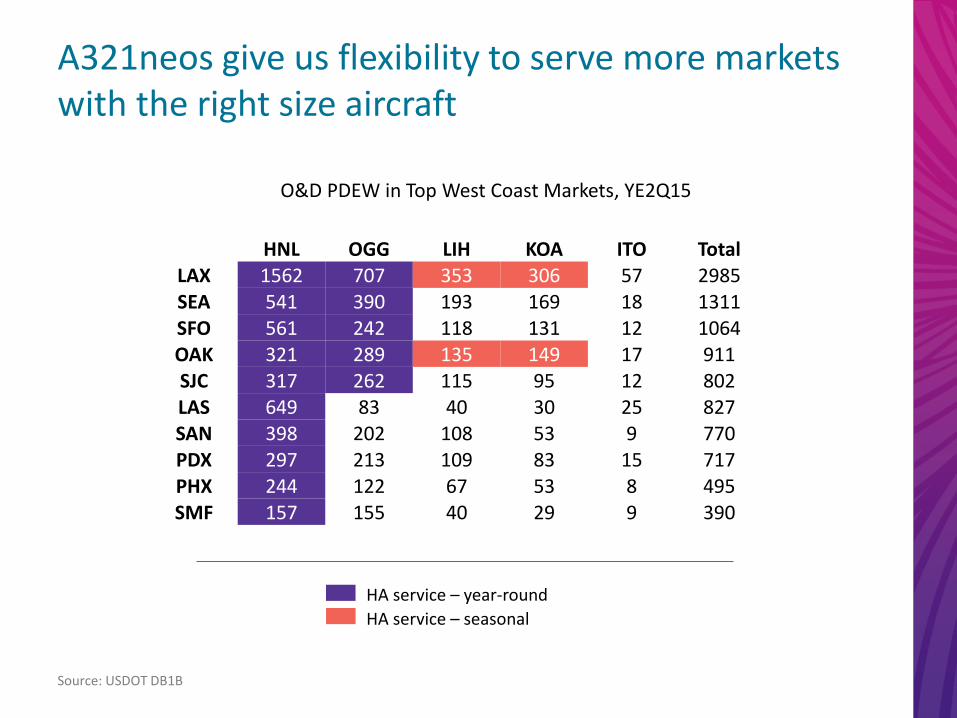

A321neos give us flexibility to serve more markets with the right size aircraft

HA service – year-round

HA service – seasonal

HNL OGG LIH KOA ITO Total LAX 1562 707 353 306 57 2985 SEA 541 390 193 169 18 1311 SFO 561 242 118 131 12 1064 OAK 321 289 135 149 17 911 SJC 317 262 115 95 12 802 LAS 649 83 40 30 25 827 SAN 398 202 108 53 9 770 PDX 297 213 109 83 15 717 PHX 244 122 67 53 8 495 SMF 157 155 40 29 9 390

O&D PDEW in Top West Coast Markets, YE2Q15

Source: USDOT DB1B

A321neos give us flexibility to serve more markets with the right size aircraft

HA service – year-round

HA service – seasonal

HNL OGG LIH KOA ITO Total LAX 1562 707 353 306 57 2985 SEA 541 390 193 169 18 1311 SFO 561 242 118 131 12 1064 OAK 321 289 135 149 17 911 SJC 317 262 115 95 12 802 LAS 649 83 40 30 25 827 SAN 398 202 108 53 9 770 PDX 297 213 109 83 15 717 PHX 244 122 67 53 8 495 SMF 157 155 40 29 9 390

O&D PDEW in Top West Coast Markets, YE2Q15

Source: USDOT DB1B

A330 still optimal for largest markets - Deepest markets - Large cargo markets A321 enables - Smaller growth increments - Seasonal flexing - Balance HNL / OGG service

A321neos give us flexibility to serve more markets with the right size aircraft

HA service – year-round

HA service – seasonal

HNL OGG LIH KOA ITO Total LAX 1562 707 353 306 57 2985 SEA 541 390 193 169 18 1311 SFO 561 242 118 131 12 1064 OAK 321 289 135 149 17 911 SJC 317 262 115 95 12 802 LAS 649 83 40 30 25 827 SAN 398 202 108 53 9 770 PDX 297 213 109 83 15 717 PHX 244 122 67 53 8 495 SMF 157 155 40 29 9 390

O&D PDEW in Top West Coast Markets, YE2Q15

Source: USDOT DB1B

Nonstop Connecting flows

A321 non-stops to mid-size Maui markets, supported by KOA/LIH/ITO connections

A321neos give us flexibility to serve more markets with the right size aircraft

HA service – year-round

HA service – seasonal

HNL OGG LIH KOA ITO Total LAX 1562 707 353 306 57 2985 SEA 541 390 193 169 18 1311 SFO 561 242 118 131 12 1064 OAK 321 289 135 149 17 911 SJC 317 262 115 95 12 802 LAS 649 83 40 30 25 827 SAN 398 202 108 53 9 770 PDX 297 213 109 83 15 717 PHX 244 122 67 53 8 495 SMF 157 155 40 29 9 390

O&D PDEW in Top West Coast Markets, YE2Q15

Source: USDOT DB1B

A321 helps us: - Convert seasonal and sub-daily KOA/LIH

service to year-round and daily - Grow into additional KOA/LIH markets

Philadelphia

Washington Nagoya

SYDNEY

SEOUL TOKYO / HANEDA

OSAKA SAN FRANCISCO

LOS ANGELES

LAS VEGAS

PAGO PAGO PAPEETE

SEATTLE

PORTLAND

PHOENIX SAN DIEGO

SACRAMENTO OAKLAND

SAN JOSE

KAHULUI

NEW YORK / JFK

POTENTIAL MARKETS

BRISBANE

SAPPORO

AUCKLAND

1-2M 3-5M 5-10M 10-20M >20M

Singapore

Melbourne

Boston

Montreal

Toronto

Austin

2015 Metropolitan Population

Vancouver Calgary

Edmonton

Jakarta Bangkok

Many Growth Opportunities Remain

EXISTING ROUTES SEASONAL ROUTES

Saigon

BEIJING

Shanghai

LIHUE

KONA

Hong Kong

Guangzhou

Chengdu

TOKYO / NARITA

Anchorage

48

HNL

FLEET EVOLUTION

NETWORK EVOLUTION

PRODUCT EVOLUTION

ANCILLARY / OTHER

PRODUCT EVOLUTION

FLEET EVOLUTION

NETWORK EVOLUTION

PRODUCT EVOLUTION

ANCILLARY / OTHER

PRODUCT EVOLUTION

AVI MANNIS Senior Vice President - Marketing

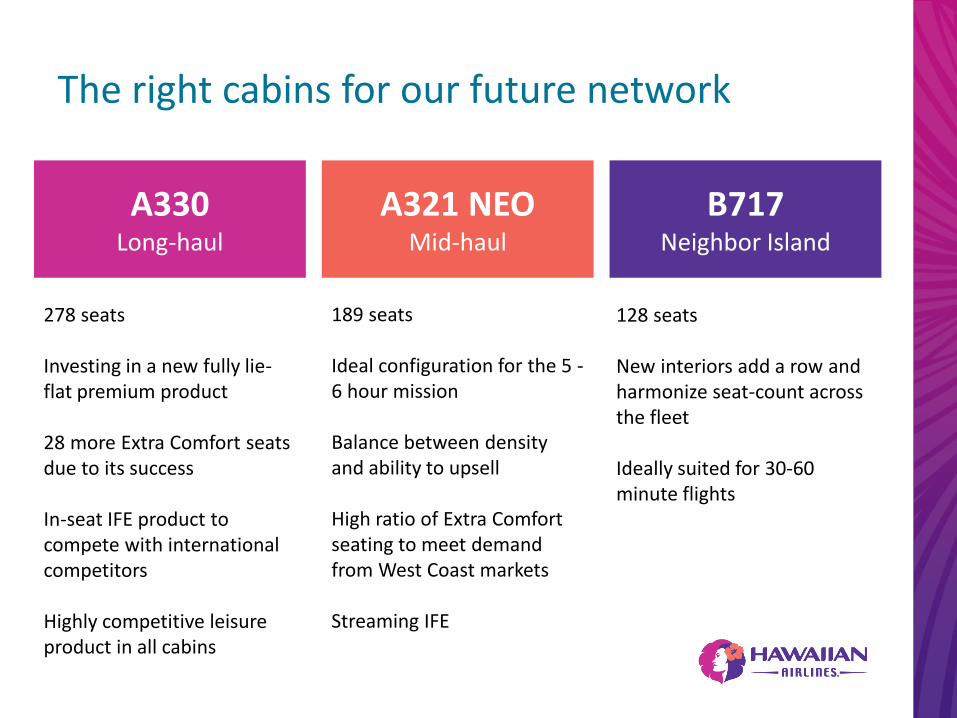

The right cabins for our future network

A330 Long-haul

A321 NEO Mid-haul

B717 Neighbor Island

189 seats Ideal configuration for the 5 - 6 hour mission Balance between density and ability to upsell High ratio of Extra Comfort seating to meet demand from West Coast markets Streaming IFE

278 seats Investing in a new fully lie-flat premium product 28 more Extra Comfort seats due to its success In-seat IFE product to compete with international competitors Highly competitive leisure product in all cabins

128 seats New interiors add a row and harmonize seat-count across the fleet Ideally suited for 30-60 minute flights

• Our competitors are increasingly operating lie-flat products on their long-haul wide-body services

• Analysis suggests a 20-40% premium for lie-flats vs. recliner seats on comparable routes

• Varies by route and competitor

2015 2020

Under 8 Hours

Compelling business case for new A330 premium product

Significant yield premium for lie-flat product on leisure routes >8 hrs

And more of our A330 fleet will be serving these routes

0%

70%

We designed a fully lie-flat product uniquely suited to our leisure mission

Materials and industrial design evoke a sense of

Hawai‘i

High density, with options for shared

or private experience

Tablet-based IFE designed into the seat minimizes

weight and obsolescence

Lie-flat bed with simple actuation

to minimize weight and maintenance

Highly customized product – first to market with this

seat platform

And a unique brand statement

Success of the Extra Comfort seat product

• > 80% paid utilization in North America

• Improving

international distribution

• Outstanding ROI

A321-NEO cabins will be ideally configured for their mission

• Bringing our award-winning

wide-body guest service to the

A321-NEO

• 189 seats (16F / 45 PY / 128 Y)

• Comfortable seats and living

space in the main cabin

• Streaming IFE– no seat-back

screens

• Cabin aesthetics that extend

our unique design language

Old seats New seats

13% increase

B717 cabin renovations have been well-received by consumers

Customer satisfaction survey, Aircraft Comfort and Condition

• Aircraft modifications will be complete by the end of 2015

• Dense configuration

has been well received by our customers

FLEET EVOLUTION

NETWORK EVOLUTION

PRODUCT EVOLUTION

ANCILLARY / OTHER

PRODUCT EVOLUTION

FLEET EVOLUTION

NETWORK EVOLUTION

PRODUCT EVOLUTION

ANCILLARY / OTHER

PRODUCT EVOLUTION

VICKI NAKATA Vice President – Loyalty & Travel Products

$38.4

$79.5

2011 2012 2013 2014 TTM Sep-2015

Building on our recent cargo success

Growing our neighbor island cargo business:

• New service with ATR72 freighters in 2016

• Lowest operating cost

• Seamless connections

Cargo revenue (in millions)

Growing sales of value-added products

• Averaging $3.5M/month*

• Growth will come from additional inventory, pricing optimization, and new distribution channels

• >10% credit card portfolio growth

• >20% growth in credit card spend

$14.69

$19.72 $21.91

2013 2014 TTM Sep 2015

Other

Baggage

Sales of HawaiianMiles

Extra Comfort / Preferred Seat Sales

Value-added revenue per passenger

Note: “Other” includes ticket fees, first class upgrades, vacation commissions and on-board sales * Includes Extra Comfort and Preferred Seat revenue

Improved website conversion of vacation packages

• Dynamic offers in the booking path

• Exclusive hotel deals

• 25% better conversion

• Enables cross-sell of other products

Better merchandising of seat upgrades

Testing new products and sales touch points

New products in the pipeline

FLEET EVOLUTION

NETWORK EVOLUTION

PRODUCT EVOLUTION

ANCILLARY / OTHER

PRODUCT EVOLUTION

• Ideal fleet positioning

• Network opportunities in North America and

International

• Optimizing our product for our guests throughout

the network

• Pursuing ancillary revenue

Conclusion

Mahalo.

SHANNON OKINAKA Executive Vice President, Chief Financial Officer

Improving financial performance

Record financial performance in 2015

$0.87 $0.85 $1.06

$0.88

$1.55

$2.65

2010 2011 2012 2013 2014 TTMSep

2015

Adjusted Earnings per share Adjusted Pre-Tax Margin

6.0%

4.6% 4.6% 3.6%

6.9%

11.7%

2010 2011 2012 2013 2014 TTMSep

2015

We are generating returns on our investments

15.6%

25.0%

2010 2011 2012 2013 2014 TTMSep

2015

Pre-Tax ROIC

2010 2011 2012 2013 2014 2015E2016E

CASM ex-fuel (in cents)

1.0%

1.0%

0.5%

2016 CASM ex-fuel yoy headwinds

Controlling our costs

Note<1>: 2015E is based on the mid-point of FY15 CASM ex-fuel guidance of up 1% - 3%

Note<2>: 2011 represents CASM ex-fuel and lease terminations expense of $70.0M

Up in the low single digit range

Maintenance

Wages

Space Rent 8.31

8.15 7.88

8.18

8.70 8.83

$2.00 - $2.10

Lower fuel costs provide a tailwind

Note<1>: 2015E and 2016E economic fuel cost per gallon estimates are based on the forward fuel

curve as of November 18, 2015.

Note<2>: Based on the Company’s hedge portfolio as of November 18, 2015

% Hedged Price

4Q15 60% $2.12

1Q16 49% $1.85

2Q16 36% $1.80

3Q16 22% $1.71

4Q16 10% $1.70

Heating Oil Hedge Position

2010 2011 2012 2013 2014 2015E2016E

Economic Fuel Cost per gallon

$3.13 $3.03

$2.31

$3.20 $3.15

$1.65 - $1.75

Strengthening our balance sheet

$600M

2010-2014

Net Debt Increase

Cash Flow from Ops

2010-2014: Borrowed to fund heavy Capex

Return to shareholders

1%

Investments in the business

99%

Sources of cash Uses of cash

$1,184M

$189M

$462M

$661M

$806M

$914M

2010 2011 2012 2013 2014 Q315

Decreasing our debt (YTD 3Q15)

$1,050M

YTD Sep 2015

Convertible Note Repurchase

$68M

Principal debt payments

$68M

Total $136M

Interest savings of $4M 3Q15

Equity repurchases (YTD 3Q15)

Represents ~7% of our outstanding market cap

TOTAL

Convertible Note – Equity Repurchase $103M

Share Repurchases $38M

Total Equity Repurchases $141M

-81-

Savings from equity repurchases

Convertible Notes

Share Buyback

Total

Value of repurchase at 9/30/15 $259M $40M $299M

Cash expended (216)M (38)M (254)M

Unrealized savings at 9/30/15 $43M $2M $45M

$45M in unrealized benefits

$2.25

$0.25

$0.06

$0.06

Lower share count in 2016 increases EPS

Tailwinds from the full

year effects of:

• Warrant unwind

• Convertible note

repurchase

• Share buyback

16% or 37 cent improvement to pro forma EPS

$2.62 Share buyback

Convertible note

repurchases

Warrant unwind

Adjusted EPS YTD 9/30/15

Diluted EPS

Capital Allocation

30%

2014 TTM Sep 2015

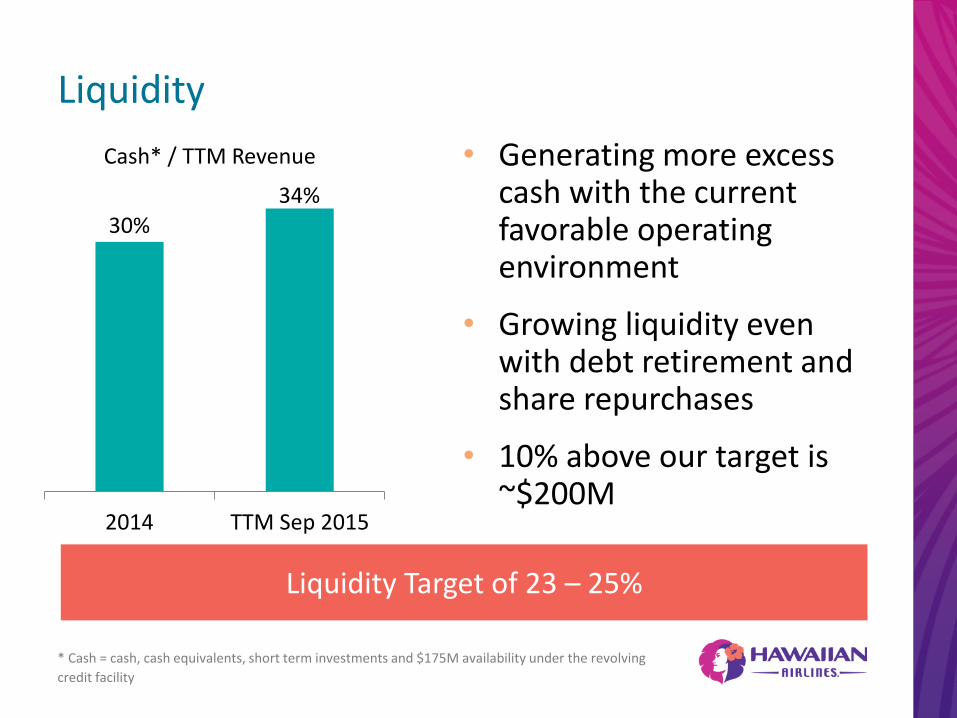

Liquidity

• Generating more excess cash with the current favorable operating environment

• Growing liquidity even with debt retirement and share repurchases

• 10% above our target is ~$200M

* Cash = cash, cash equivalents, short term investments and $175M availability under the revolving

credit facility

Cash* / TTM Revenue

34%

Liquidity Target of 23 – 25%

2014 TTM Sep 2015

4.2x

• Met the leverage target

we set last year

• Continue to de-lever

through debt

retirement

Leverage

Note: Aircraft Rent is capitalized at 7x.

3.1x

Optimize our capitalization and minimize cost of capital

Adjusted Debt / Adjusted EBITDAR

$1,184M

$600M

2010-2014 Projected2015 - 2019

Net Debt Increase

Cash Flow from Ops

Investments in the

business

Return to shareholders

(2010 – 2014)

2015-2019: Cash flow funds multiple uses

Net Debt Reduction

Sources of cash

(2015 – 2019)

Investments in the

business

Return to shareholders

Uses of Cash

Funding our 16 A321neo deliveries

Cash available for ….. Financing required for only….

Anticipated additional debt retirement

Results in Interest expense savings of ~$5 - $10M

TOTAL

Early debt retirement $150M

Contractual principal debt payments $80M

$230M

Anticipated additional pension plan contributions

$199M

Reducing our pension

liability leads to:

- Lower future

contributions

- Decreases future

pension expense

- Decreases PBGC

premiums

3Q15

Pension liability OPEB

Detail of pension liability

$209M

$199M

Pension and other postretirement liability Benefits

$161M

$30M

$8M

Pathway to long-term value

Optimize cost of capital

Increase enterprise

value

Strengthen balance

sheet

Strong financial

performance

SHAREHOLDER VALUE

• Improving financial performance

• Strengthening balance sheet

• Capital allocation

Creating long-term value

Mahalo.

MARK DUNKERLEY President and Chief Executive Officer

• Strengthen competitive position

• Achieve mastery

• Grow long-term value for our shareholders

2016 is going to be a better year than 2015

Mahalo.

Non-GAAP Reconciliations

NON-GAAP RECONCILIATIONS ($ in thousands, except CASM data) FY 2010 FY 2011 FY 2012 FY 2013 FY 2014

GAAP Operating Expenses $1,218,815 $1,630,176 $1,832,955 $2,022,118 $2,069,747

Less: aircraft fuel, including taxes and delivery (322,999) (513,284) (631,741) (698,802) (678,253)

Less: lease termination expense - (70,014) - - -

Adjusted operating expenses - excluding aircraft fuel and lease termination

$895,816 $1,046,878 $1,201,214 $1,323,316 $1,391,494

Available Seat Miles 10,150,659 12,039,933 14,687,472 16,785,827 17,073,630

CASM - GAAP (in cents) 12.01 13.54 12.48 12.05 12.12

Less: aircraft fuel and lease termination expense (in cents) (3.18) (4.84) (4.30) (4.16) (3.97)

CASM Excluding Fuel and lease termination expense (in cents) 8.83 8.70 8.18 7.88 8.15

NON-GAAP RECONCILIATIONS ($ in thousands)

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 TTM Sep 2015

Net Income (Loss), GAAP $110,255 $(2,649) $53,237 $51,854 $68,926 $48,834

Add: lease termination expense, net of tax - 42,008 - - - -

Add: loss on extinguishment of debt, net of tax - - - - 2,331 178

Add: changes in fair value of fuel derivatives, net of tax 3,859 3,859 2,375 (5,210) 25,864 (11,519)

Add: non-recurring tax benefits (62,546) - - - - -

Adjusted Net Income, Non-GAAP $45,405 $43,218 $55,612 $46,644 $97,121 $37,493

The Company evaluates its financial performance utilizing various GAAP and non-GAAP financial measures, including operating income and CASM. Pursuant to Regulation G, the Company has included the following reconciliation of reported non-GAAP financial measures to comparable financial measures reported on a GAAP basis. The Company believes that excluding fuel costs from certain measures is useful to investors because it provides an additional measure of management’s performance excluding the effects of a significant cost item over which management has limited influence.

Pre-tax margin

NON-GAAP RECONCILIATIONS ($ in thousands)

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 TTM Sep 2015

Income Before Income Taxes, as reported $ 81,989 $(1,082) $85,786 $86,410 $113,447 $252,638

Add: changes in fair value of fuel derivatives (3,840) 6,432 3,958 (8,684) 43,106 7,147

Add: loss on extinguishment of debt - - - - 3,885 11,181

Add: lease termination expense - 70,014 - - - -

Adjusted Income Before Income Taxes, Non-GAAP $78,149 $75,364 $89,744 $77,726 $160,438 $270,966

Revenue $1,310,093 $1,650,459 $1,962,353 $2,155,865 $2,314,879 $2,318,152

NON-GAAP RECONCILIATIONS ($ in thousands)

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 TTM Sep 2015

Pre-Tax Margin, as reported 6.3% (0.1)% 4.4% 4.0% 4.9% 10.9%

Add: changes in fair value of fuel derivatives, net of tax (0.3)% 0.4% 0.2% (0.4)% 1.9% 0.3%

Add: loss on extinguishment of debt, net of tax - - - - 0.1% 0.5%

Add: lease termination expense, net of tax - 4.3% - - - -

Pre-Tax Margin, adjusted 6.0% 4.6% 4.6% 3.6% 6.9% 11.7%

Leverage NON-GAAP RECONCILIATIONS

($ in thousands) FY 2015 TTM 3Q2015

Debt and capital lease obligations 1,049,637 914,413

Plus: Aircraft leases capitalized at 7x last 12 months’ aircraft rent 744,954 798,312

Adjusted debt and capital lease obligations 1,794,591 1,712,805

Income Before Income Taxes 113,447 252,638

Add back:

Interest and amortization of debt expense 64,240 58.871

Depreciation and amortization 96,374 104,192

Rent Expense 106,422 114,056

EBITDAR 380,483 529,757

Adjustments:

Add: changes in fair value of derivative contracts 43,106 7,147

Add: Loss on extinguishment of debt 3,885 11,181

Adjusted EBITDAR 427,474 548,085

Leverage Ratio 4.2x 3.1x

The Company evaluates its financial performance utilizing various GAAP and non-GAAP financial measures, including operating income and CASM. Pursuant to Regulation G, the Company has included the following reconciliation of reported non-GAAP financial measures to comparable financial measures reported on a GAAP basis. The Company believes that excluding fuel costs from certain measures is useful to investors because it provides an additional measure of management’s performance excluding the effects of a significant cost item over which management has limited influence.

99

Return on Invested Capital

HAWAIIAN AIRLINES – RETURN ON INVESTED CAPITAL (ROIC) – WORKING CAPITAL CASH METHODOLOGY 1

(in ‘000s) 2010 2011 2012 2013 2014 3Q2015 TTM

Operating Income $91,278 $20,283 $129,400 $133,745 $245,132 $348,080

Add Back One-Time Charges $0 $70,014 $0 $0 $0 $0

Operating Income Less One-Time Charges $91,278 $90,297 $129,400 $133,745 $245,132 $348,080

Add Back Aircraft Rent Expense for Operating Leases $112,721 $112,883 $98,784 $108,535 $106,422 $111,236

Add Depreciation for Operating Lease Add Back 2 ($28,406) ($28,446) ($24,894) ($27,351) ($26,818) ($28,032)

Add Return on Invested Cash $197 $248 $294 $323 $347 $349

Adjusted Operating Income $175,790 $174,981 $203,585 $215,253 $325,083 $431,634

After Tax Adjusted Operating Income $108,990 $101,489 $122,130 $129,131 $195,050 $258,937

Average Total Debt and Capital Leases $225,170 $341,899 $616,704 $735,676 $1,017,084 $1,071,477

Common Equity $199,368 $286,499 $249,384 $302,141 $407,234 $378,703

Average Capitalized Operating Leases 3 $789,047 $790,180 $691,486 $759,747 $744,957 $778,653

Remove Average Excess Cash ($90,295) ($64,407) ($115,173) ($122,710) ($179,626) ($209,288)

Average Invested Capital $1,123,290 $1,354,171 $1,442,401 $1,674,855 $1,989,649 $1,965,544

Pre-Tax ROIC 15.6% 12.9% 14.1% 12.9% 16.3% 22.0%

After-Tax ROIC 9.7% 7.5% 8.5% 7.7% 9.8% 13.2%

Notes: 1 All unrestricted cash removed from invested capital, except for working capital required to operate the business, defined as unrestricted cash equal to 15% of TTM total revenue 2 Assumes 25 years useful life of aircraft and 10% salvage value 3 Average capitalized operating leases equals TTM rent multiplied by 7

Top Related