Languages

Pages

Legal

—KPMG Business School

TEI HoustonCross-Border Tax IssuesHouston, TexasMay 1, 2017

Global Transfer Pricing:Controversy Update

Anjit BajwaMark HorowitzKPMG LLP

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

2

Agenda— Trends in IRS Transfer Pricing Enforcement Personnel and policy changes at Large Business and Int’l (LB&I) Examination trends regarding transfer pricing issues

— Trends in US Advance Pricing Agreements (APAs) and Mutual Agreement Procedures

— Transfer Pricing Litigation

— Global Controversy Environment

Trends in US Transfer Pricing Enforcement

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

4

LB&I Structure – 2017

Tina MeauxAssistant Deputy Commissioner -

Compliance Integration

Combined MAP/APA Team

Rosemary SeretiDeputy Commissioner

Theodore SetzerAssistant Deputy Commissioner -

International

Sharon PorterDirector -

Treaty and Transfer Pricing Operations

Douglas O’DonnellLB&I Commissioner

Jennifer BestDFO – Transfer Pricing

Practice

Deborah PalacheckDirector – Treaty Administration

John HughesActing Director –

APMA

TAIT, EOI, JITSIC

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

5

TTPO Structure – 2017

Combined MAP/APA Team

Sharon PorterDirector -

Treaty and Transfer Pricing Operations

Jennifer BestDFO – Transfer Pricing

Practice

Deborah PalacheckDirector – Treaty Administration

John HughesActing Director –

APMA

TAIT, EOI, JITSIC

Shah MobedTPP North

Matt HartmanTPP East

Nancy BronsonTPP West

Deborah Dickson

TPP SouthTPO IPNs

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

6

LB&I Future State Initiatives— Shift to a centralized issue-focused enforcement strategy Replaces current decentralized case selection model Publication 5125, LB&I Examination Process (LEP) replaced Quality

Examination Process• Provides examination framework for new issue-focused approach• Effective May 1, 2016

— Treaty activities and the Transfer Pricing Practice merged to form TTPO All field economists reassigned to TPP International examiners added to TPP

— IRS Transfer Pricing Audit Roadmap (the Roadmap) Provides recommended audit steps for IRS transfer pricing examiners Released February, 2014

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

7

Current TP Enforcement — Case selection currently occurs in the field – continual

audits are common— Transfer pricing specialists typically are brought onto a

case mid-cycle to conduct risk assessment Leads to tight audit timelines (statute extensions?) Transfer pricing issues may not be fully developed Unfocused audit plans lead to “any and all” and unnecessary

IDRs Productive communication between the IRS and taxpayers

suffers— “Acting” managers and transfer pricing specialists working

remotely are common – decision maker difficult to identify

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

8

The Roadmap— The Roadmap is organized around the planning, execution, and

resolution audit phases The Roadmap is not a template (“one size does not fit all”) The Roadmap provides insight into what to expect during a transfer

pricing examination— Describes audit tasks and steps to consider/complete in a well-

developed transfer pricing case — IRS is emphasizing increased transparency and communications

in its transfer pricing enforcement activities

Caution . . . IRS audit teams are not always transparent

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

9

The Roadmap— Key themes Upfront planning is essential to a transfer pricing exam The success of a transfer pricing case hinges on the facts

• Use of the Acknowledge of the Facts IDR being re-assessed• Examiners are instructed to consider all relevant facts, including those

weighing in the taxpayer’s favor, before issuing a NOPA The 24 month notional examination model is retained

• Illustrates how transfer pricing audit steps and phases are sequenced• The Roadmap is clear that a complex transfer pricing case may

take 2 – 3 years or longer to thoroughly develop

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

10

IRS Audit Campaigns— Issue-focused audit strategy hinges on a centralized approach

to tax issue selection: data analysis and “campaign” proposals submitted by the field

— The issue-focused strategy is expected to yield resource efficiencies Examiners are assigned to a campaign once a tax issue is identified

for exam Campaigns may span multiple taxpayers or industries

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

11

IRS Audit Campaigns— Initial tranche of 13 campaigns released January 31, 2017

include Offshore Voluntary Disclosure Program Mid-market tax-free repatriation structures Form 1120-F non-filers Inbound distributors

— Will centralized campaigns represent a “national” position where outcomes are predetermined? What authority will field audit teams possess? Will functional, legal, and economic analysis be conducted?

— IRS has not provided information as to how campaign implementation will occur

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

12

IRS Transfer Pricing Audit Trends— Intensive transfer pricing exam processes are being

observed Earlier involvement of outside experts Transfer pricing orientations focusing on profitability analysis

and tax planning Site visits Functional interviews of taxpayer personnel

— Overly broad and unfocused IDRs continue to be issued “Any and all” IDRs Unfocused IDRs unrelated to audit hypothesis

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

13

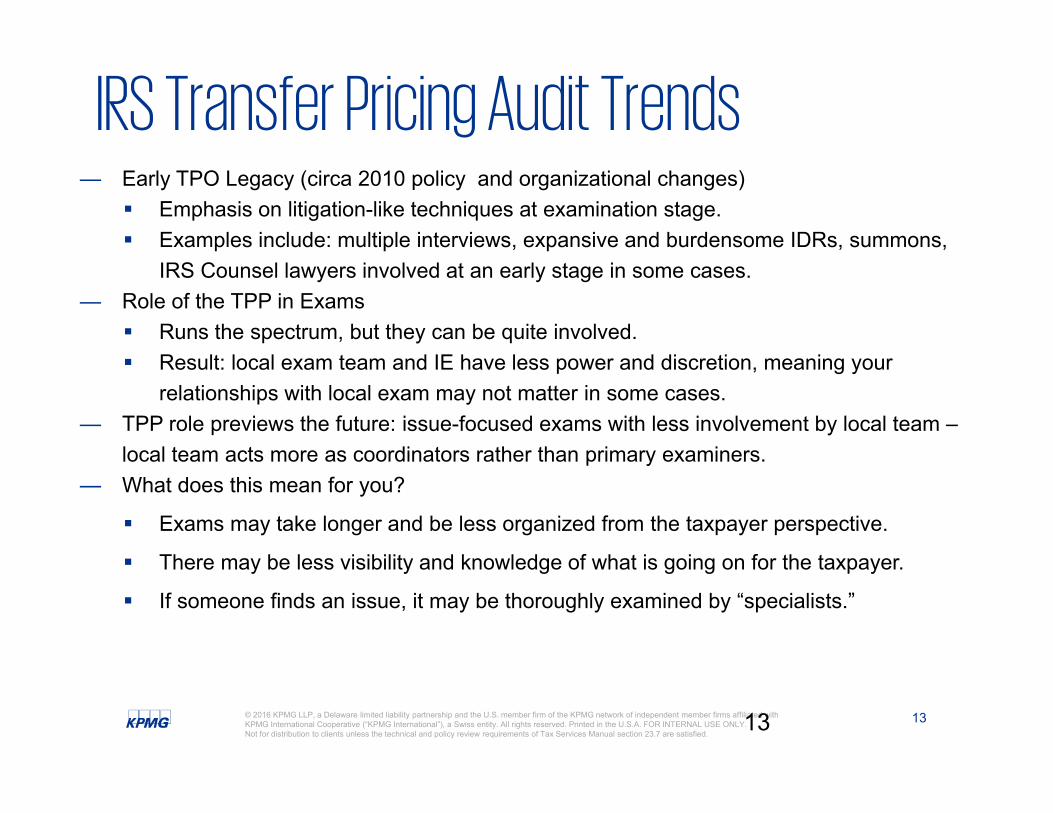

IRS Transfer Pricing Audit Trends— Early TPO Legacy (circa 2010 policy and organizational changes)

Emphasis on litigation-like techniques at examination stage. Examples include: multiple interviews, expansive and burdensome IDRs, summons,

IRS Counsel lawyers involved at an early stage in some cases.— Role of the TPP in Exams

Runs the spectrum, but they can be quite involved. Result: local exam team and IE have less power and discretion, meaning your

relationships with local exam may not matter in some cases.— TPP role previews the future: issue-focused exams with less involvement by local team –

local team acts more as coordinators rather than primary examiners.— What does this mean for you?

Exams may take longer and be less organized from the taxpayer perspective.

There may be less visibility and knowledge of what is going on for the taxpayer.

If someone finds an issue, it may be thoroughly examined by “specialists.”

13

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

14

IRS Transfer Pricing Audit Trends— I/C agreements are being reviewed Are the terms firm or easily modifiable? Is the conduct of the parties consistent with the terms? Identifying obligations/risks assigned to each party

— Trend toward applying consistent IRS audit positions across taxpayers and industries

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

15

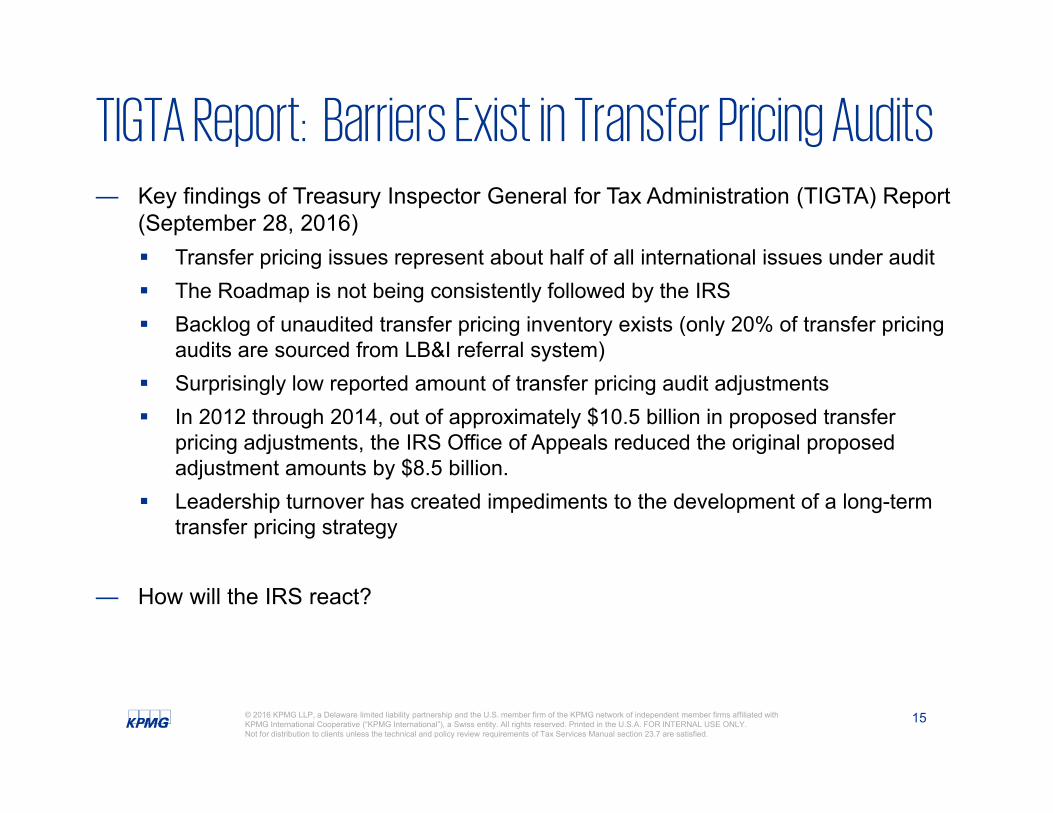

TIGTA Report: Barriers Exist in Transfer Pricing Audits— Key findings of Treasury Inspector General for Tax Administration (TIGTA) Report

(September 28, 2016) Transfer pricing issues represent about half of all international issues under audit The Roadmap is not being consistently followed by the IRS Backlog of unaudited transfer pricing inventory exists (only 20% of transfer pricing

audits are sourced from LB&I referral system) Surprisingly low reported amount of transfer pricing audit adjustments In 2012 through 2014, out of approximately $10.5 billion in proposed transfer

pricing adjustments, the IRS Office of Appeals reduced the original proposed adjustment amounts by $8.5 billion.

Leadership turnover has created impediments to the development of a long-term transfer pricing strategy

— How will the IRS react?

Trends in US Advance Pricing Agreements/ Mutual Agreement

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

17

APMA structure – 2017Acting Director, APMA

John Hughes

Assistant Director Peter Rock

Team 11Chuck LarsonEconomists

Team 1Vacant

Team 6Vacant

Team 2Russell KwiatEconomists

Team 7Keith Doce

(Acting)

Team 3Judith Cohen

Team 4Mark Dunshee

(Acting)

Team 5Burton Mader

Team 8Gregory Spring

Team 9Patricia Fouts

Team 12Ho Jin LeeEconomists

Team 10Dennis Bracken

Assistant Director Vacant

Assistant Director Vacant

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

18

IRS APA StatisticsFISCAL YEAR

FILED(uni-, bi-, and multilateral)

EXECUTED(uni-, bi-, and multilateral)

Year End Inventory

2012 126 140 391

2013 111 145 331

2014 108 101 336

2015 183 110 410

2016 98 86 398

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

19

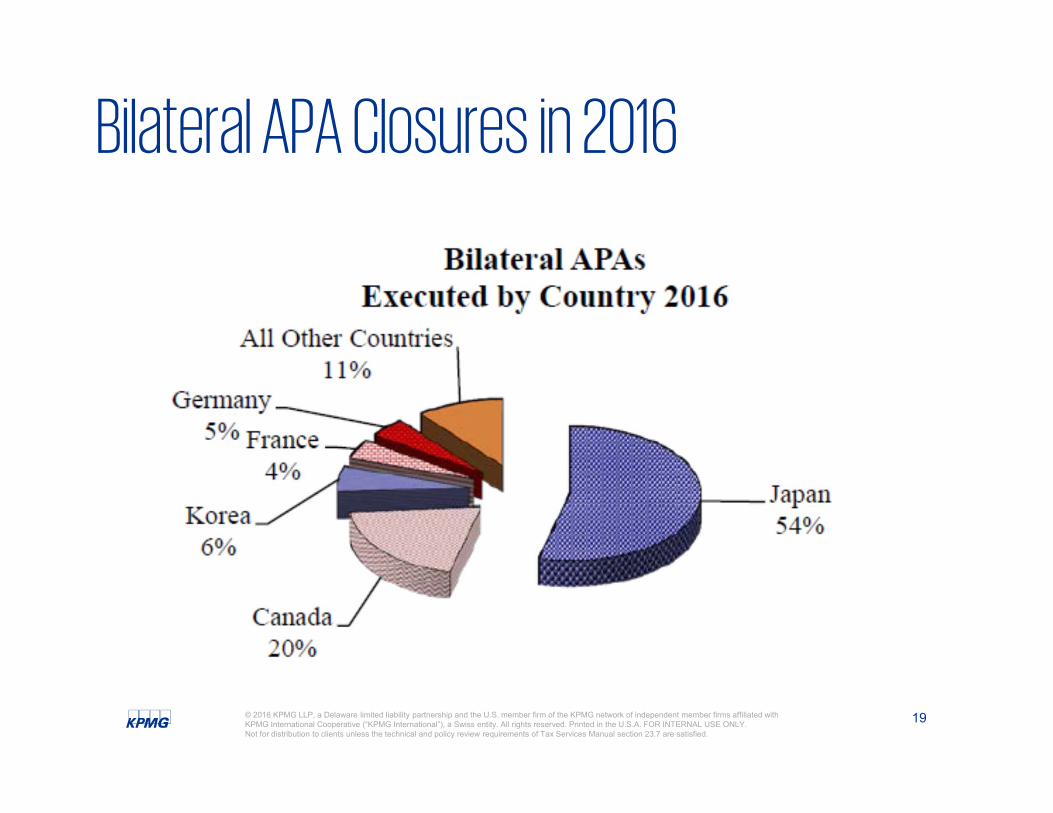

Bilateral APA Closures in 2016

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

20

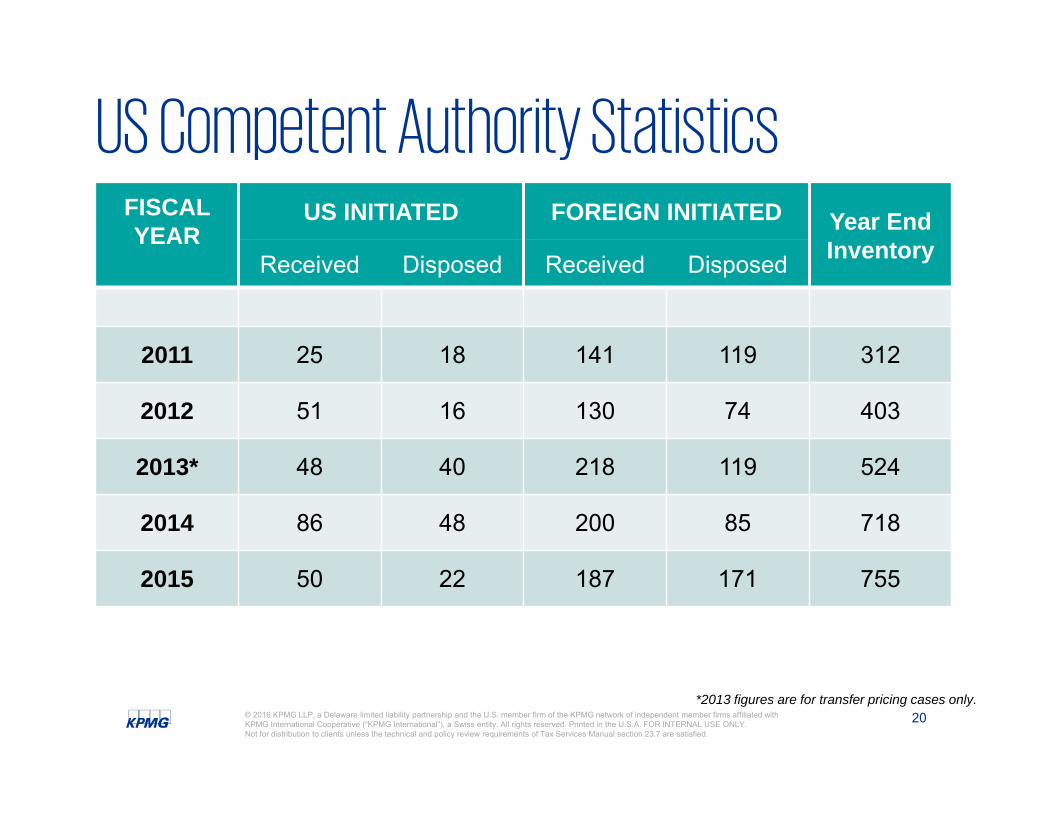

US Competent Authority StatisticsFISCAL YEAR

US INITIATED FOREIGN INITIATED Year End InventoryReceived Disposed Received Disposed

2011 25 18 141 119 312

2012 51 16 130 74 403

2013* 48 40 218 119 524

2014 86 48 200 85 718

2015 50 22 187 171 755

*2013 figures are for transfer pricing cases only.

Transfer Pricing Litigation

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

22

Litigation – Court Cases— Medtronic, Inc. v. Commissioner, T.C. Memo. 2016-112 (2016);— Guidant/Boston Scientific;— United States v. Microsoft, W.D. Wash., No. 2:15-cv-00102;— Coca-Cola Co. v. Commissioner , T.C., No. 031183-15;— Facebook, Inc. v. Commissioner;— Eaton Corp. v. Commissioner, T.C., No. 5576-12;— And others….

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

23

Litigation – Court Cases— In Amazon, Inc. v. Commissioner, 148 T.C. No. 8, T.C., No. 31197-12, 3/23/17, the

Taxpayer faced a determination that it had undervalued the intangible property transferred as part of a CSA by over $3 billion.

— In making its adjustment, IRS utilized a discounted cash flow analysis as the best method and rejected the taxpayer’s CUT method. The IRS also assumed that the transferred intangibles had an indefinite useful life.

— The Court held in the Taxpayer’s favor for the following reasons: DCF analysis failed to restrict valuation to the ‘pre-existing intangible property’ Rejected akin to a sale approach Useful life of the intangible property at issue was not indefinite

— Tax Court relied upon a transactional CUT method, with adjustments, rather than using a profit-based approach in reaching its conclusions

Global Controversy Environment

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

25

BEPS backgroundThe changing landscape

Increased political focus on perceived tax avoidance by multinationals

Governments under extreme fiscal pressure as a consequence of the global economic crisis

The G20 was concerned that current international tax rules and frameworks were/remain inadequate

The G20 was applying political support/pressure to push for change

The OECD response to growing pressure was to release the Base Erosion and Profit Shifting (BEPS) report

There is a drive to develop a tax system that is fit for purpose for today’s multinationals and digital age

Transfer pricing is at the heart of the debate

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

26

■ Objective: Risk Assessment■ Approach: Provides an overview of the multinational group and

businessMaster file

■ Objective: Appropriate considerations in setting transfer prices■ Approach: Provides additional detail on the operations and

transactions relevant to that jurisdictionLocal file

■ Objective: Prioritization of Audit Issues■ Approach: Provides summary data by jurisdiction including

revenue, income, taxes, and indicators of economic activity

Country-By-Country(CbyC) Report

BEPS Action 13 guidanceThree-tired approach for documentation

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

27

Confidentiality and audit readiness issues• Treaty protection for CbyC• Treaty disclosure (bilateral, multi-lateral)

- How widely available will CbyC information be, and will it eventually become public?

• Separate European transparency initiative for CbyC like data- In today’s world, any public information is available for

everyone• Only local protections for Master File• What approach for Master File? Minimal compliance versus

detailed explanation?

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

28

Historically, MNEs Have: Used contracts to move assets and

risks to principal companies Moved the economic responsibility for,

and key benefits from, important local functions to principal companies

Limited local returns

The OECD and Other Key G20 Countries Pushed to: Increase the importance attached

to people and local functions Focus on key decision makers and

where they are located Limit profits associated with

“naked” contractual rights

Risks

Assets Functions

Key Themes in Chapter I of OECD Transfer Pricing Guidelines

Contractual arrangements and actual conduct should be considered

Need to look at the location of decision-makers and the decisions they have made, especially with respect to risk

Transfer Pricing Generally Focuses on:

Actions 8 – 10: Focus on people & functions

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

29

Identify economically significant risks with specificity1

Identify contractual assumption of the specific risk2

Functional analysis. Establish conduct and which enterprises perform control functions and risk mitigation functions and have the financial capacity to assume the risk

3

Is the contractual assumption consistent with the conduct? Do the entities follow the contractual terms and does the party assuming risk exercise control and have the financial capacity to assume risk?

4

If the party assuming the risk does not control the risk or does not have the financial capacity to assume the risk, then allocate the risk to the group company having most control and having the financial capacity to assume the risk

5

Price the accurately delineated transaction taking into account the financial and other consequences of risk assumption, as appropriately allocated6

Six-step analytical risk framework

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

30

Understanding DEMPE Functions Existing “IP” models did not always include an analysis of the parties responsible for: Legal ownership Funding [economic ownership]

Many “IP” planning strategies did not clearly define “IP”. Often it means, “anything” leading to profits above “routine” or “normal” profits. Model was applied for all industries, from high tech to consumer goods, in a similar way

A review of DEMPE functions may require changes to the allocation of profits in the value chain

New emphasis on control: people with the relevant knowledge to make decisions

What is DEMPE? Development, Enhancement, Maintenance, Protection and Exploitation

What questions do you have?

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A. FOR INTERNAL USE ONLY.Not for distribution to clients unless the technical and policy review requirements of Tax Services Manual section 23.7 are satisfied.

32

Speakers

Mark HorowitzPrincipal

Economic & Valuation Services(713) 319-2840

Anjit Bajwa, Ph.D.Principal

Economic & Valuation Services(713) 319-3759

Thank you

© 2016 KPMG LLP, a Delaware limited liability partnership and the US member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia

Top Related