Languages

Pages

Legal

This report is solely for the use of Zinnov client and Zinnov personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organization without prior written approval from Zinnov

Global R&D Benchmarking December , 2010

Global R&D spending has declined/ decreased; however, this decline is much lower than the decline in net sales, indicating the strategic importance of R&D

Source: Zinnov analysis of global top 1000 R&D spenders 2

468

511

549

538

420

440

460

480

500

520

540

560

2006-07 2007-08 2008-09 2009-10

Global R&D Investments Growth Trends, 2006-10 (USD Billion)

14,134

15,336

16,684

14,953

12,500

13,000

13,500

14,000

14,500

15,000

15,500

16,000

16,500

17,000

2006-07 2007-08 2008-09 2009-10

Global Net Sales Trends, 2006-10 (USD Billion)

Companies like Nokia, Sony, Daimler, Panasonic and Robert Bosch, have only slightly reduced their R&D spending even though net sales has taken a big hit in the last year

Analysis of top R&D spenders across verticals reveals that in R&D spending in the latest quarter (Sep 2010) went up by an average of 11% compared to last year

Source: Zinnov analysis of global top 1000 R&D spenders

14.1%

30.5%

15.4%

30.3%

9.7%

0%

5%

10%

15%

20%

25%

30%

35%

0-10 11-50 51-100 101-500 501-1000

Contribution of Top R&D Investors in the Total Global 1,000 R&D Spend

Company

Name

2009-2010

Rank

2008-2009

Rank

Change

2006-2007

Rank

Change

Toyota Motor 1 0 0

Roche 2 +2 +6

Microsoft 3 -1 +3

Volkswagen 4 -1 +6

Pfizer 5 -1 -3

Novartis 6 +4 +12

Nokia 7 0 +10

Johnson & Johnson

8 0 -3

Sanofi-Aventis 9 +2 0

Samsung Electronics

10 +5 +10

Siemens 11 +3 +5

General Motors 12 -7 -5

Honda Motor 13 0 +2

Daimler 14 -2 -11

GlaxoSmithKline 15 +6 -1

The Top 500 R&D spenders account for close to 90% of the total corporate R&D spending in the world; only three of the top 10 R&D spenders in 2009-10 were from North America

Companies marked in Red have shown continuous decrease in rank in last four years. The Scenario is opposite for companies marked in Green.

North America (NA) and Europe (EU) account for the majority of investments, but considering the PPP conversion, APAC contribution is significantly higher

Note: Average values have been taken for PPP analysis

Source: Zinnov analysis of global top 1000 R&D spenders; UN Statistical Data on PPP Conversion 4

Split of Top 1000 Companies by Geography

Split of R&D Investment of Top 1000 Companies by Geography

APAC 10%

EU 33%

Japan 20%

NA 35%

ROW 2%

Country

PPP

Conversion

(Local

Currency)

PPP

Conversion

(USD) Country

PPP

Conversion

(Local

Currency)

PPP

Conversion

(USD)

US 1.00 1.00 UK 0.65 1.08

Canada 1.23 1.17 Korea 872.00 0.76

France 0.93 1.38 China 4.09 0.57

Germany 0.89 1.33 Japan 134.34 1.49

Spain 0.79 1.18 India 16.54 0.36

` APAC 6.2%

APAC 12.5%

EU 35.5%

EU 32.5%

Japan 22.3%

Japan 17.0%

NA 34.7%

NA 36.4%

ROW 1.2%

ROW 2.8%

w/o PPP At PPP

0

50000

100000

150000

200000

250000

APAC EU Japan NA Others

Sum of R&D 2008-2009

Sum of R&D 2009-2010

Arrow indicates whether R&D as a % of sales increased or decreased compared o last year`

R&D investments in year 2008-2009 and 2009-2010 split by Geography

2.1%

13.2%

0.1%

5.1%

7.3%

Companies in the APAC region continued to increase their R&D investments against the prevailing trend of reducing R&D spending followed by companies in other geographies

Source: Zinnov analysis of global top 1000 R&D spenders

This presentation will be focused towards the highlighted verticals below, which account for more than 63% of the total R&D investments in the top 1,000 list

Note: *Others include Pharmaceutical, Biotechnology, Media & Entertainment, Energy and others

Source: Zinnov analysis of global top 1000 R&D spenders 6

Split of Top 1000 Companies by Vertical

R&D Investment of Top 1,000 Investors

Automotive USD 86.5 Bn

Consumer Electronics

USD 59.4 Bn

Industrial USD 58.8 Bn

Semiconductors USD 29.8 Bn

Vertical

Software/Internet USD 38.4 Bn

Total USD 538.5

Bn

11%

10.9%

5.5%

7.1%

8.7%

Aerospace & Defense

USD 20.2 Bn 3.8%

Telecom & Networking

USD 46.8 Bn

16.1%

Others USD 198.5

Bn 36.9% Aerospace &

Defense 3.3%

Automotive 7.3%

Computer Hardware/ Consumer Electronics

5.4%

Industrial 20.0%

Others 44.6%

Semiconductor

7.5%

Software/ Internet

6.0%

Telecom & Networking

5.9%

0

20000

40000

60000

80000

100000

120000

Aerospace & defence Automotive Computerhardware/Consumer

Electronics

Industrial Semiconductors Software/Internet Telecom &Networking

R&D in 2008-2009

R&D in 2009-2010

R&D investments in year 2009-2010 and 2008-2009 split by Vertical

Source: Zinnov analysis of global top 1000 R&D spenders

-11.6%

-7.4 %

-3.9%

However, almost all verticals witnessed a decrease in absolute R&D investments with Automotive, Semiconductors and Telecom showing the maximum percentage decrease

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

0 10 20 30 40 50 60 70 80 90 100

During the recent economic downturn companies in most verticals continued to spend the similar percentage of revenue on their R&D activities

Source: Zinnov analysis of global top 1000 R&D spenders 8

Total Vertical R&D Investments (USD Billion)

1. Size of the Bubble Represents the relative Total Net Sales of the Industry Vertical

2. Arrow indicates whether R&D as a % of sales increased or decreased compared o last year

Total R&D Investments as Percentage of Net Sales (Top 1,000 R&D Spenders) , 2009 -2010

R&

D I

nve

stm

en

ts a

s P

erc

en

tage

of

Ne

t Sa

les

Semiconductors

Software

Telecom & Networking

Industrial

Consumer Electronics / Computer Hardware Automotive

Aerospace & Defense

Distribution of R&D Investments Top 1000 Companies in Software Vertical by Geography

North American companies are the largest contributor towards software product/ internet R&D with Europe coming a distant second

Source: Zinnov analysis of global top 1000 R&D spenders 9

29

11

2

7

8

1

3

NA EU APAC ROW

1 - 500 Mn 500 Mn - 1 Bn 1 - 10 Bn 10 Bn+

44

12

2 3

Distribution of Top 1000 Companies in Software Vertical by Geography and Revenue Ranges (USD)

Company Geography

Microsoft North America

IBM North America

Oracle North America

Google North America

SAP Europe

APAC 0.6% EU

11.6%

NA 87.4%

ROW 0.4%

3

2 2

Arrows indicate the change in number of companies from year 2006-07 to 2009-10

Distribution of R&D Investments Top 1000 Companies in Industrial Vertical by Geography

Majority of the companies in the Industrial vertical are small/medium sized contributing aggressively towards R&D investments; companies from APAC are on the rise in this vertical

Source: Zinnov analysis of global top 1000 R&D spenders 10

39

71

23

39

3

6

5

6

3

3

2

NA EU APAC Japan ROW

1 - 500 Mn 500 Mn - 1 Bn 1 - 10 Bn

3

48

79

23

47

Distribution of Top 1000 Companies in Industrial Vertical by Geography and Revenue Ranges (USD)

APAC 6.7%

EU 40.2%

Japan 22.7%

NA 30.0%

ROW 0.4%

Company Geography

Siemens Europe

General Electric North America

Honeywell North America

Schneider Europe

Mitsubishi Heavy Japan

9

6

7

2

4

Arrows indicate the change in number of companies from year 2006-07 to 2009-10

Distribution of R&D Investments Top 1000 Companies in Semiconductor Vertical by Geography

North America accounts for more than 65% of total R&D spend in Semiconductor vertical with significant contribution from APAC & EU geographies

Source: Zinnov analysis of global top 1000 R&D spenders 11

35

1

12 9

1

5

2

3

1

4

2

NA EU APAC Japan ROW

1 - 500 Mn 500 Mn - 1 Bn 1 - 10 Bn 10 Bn+

44

5

15

9

Distribution of Top 1000 Companies in Semiconductor Vertical by Geography and Revenue Ranges (USD)

APAC 12.1%

EU 12.9%

Japan 6.9%

NA 65.1%

ROW 3.0%

Company Geography

Intel North America

STMicroelectronics Europe

Advanced Micro Devices North America

Broadcom North America

Texas Instruments North America

2

6

1

1

1

Arrows indicate the change in number of companies from year 2006-07

Distribution of R&D Investments Top 1000 Companies in Consumer Electronics/ Hardware Vertical by Geography

Consumer Electronics/ Computer Hardware companies are majorly concentrated in the Japan and Asia-Pacific region

Source: Zinnov analysis of global top 1000 R&D spenders 12

10

7

9

2 2

2

1

1

2

1

2

9

NA EU APAC Japan ROW

1 - 500 Mn 500 Mn - 1 Bn 1 - 10 Bn 10 Bn+

3

6

14

8

12

17

Distribution of Top 1000 Companies in Consumer Electronics/ Computer Hardware Vertical by Geography and Revenue Ranges

(USD)

APAC 18.3%

EU 6.2%

Japan 60.7%

NA 12.7%

ROW 2.1%

0.0%

Company Geography

Samsung Electronics APAC

Panasonic Japan

Sony Japan

Hitachi Japan

Toshiba Japan

Arrows indicate the change in number of companies from year 2006-07

2

1

1

Distribution of R&D Investments Top 1000 Companies in Telecom & Networking Vertical by Geography

Telecom & Networking vertical witnesses significant contributions from all sizes of the companies, though mainly in North America & Europe

Source: Zinnov analysis of global top 1000 R&D spenders 13

21

12

6

2

4

1

1

3

7

2

1

NA EU APAC Japan

1 - 500 Mn 500 Mn - 1 Bn 1 - 10 Bn 10 Bn+

28

20

9

3

Distribution of Top 1000 Companies in Telecom & Networking Vertical by Geography and Revenue Ranges (USD)

APAC 10.9%

EU 46.2%

Japan 6.9%

NA 35.9%

Company Geography

Nokia Europe

Cisco Systems North America

Alcatel-Lucent Europe

Ericsson Europe

Motorola North America

1

1

2

Arrows indicate the change in number of companies from year 2006-07 to 2009-10

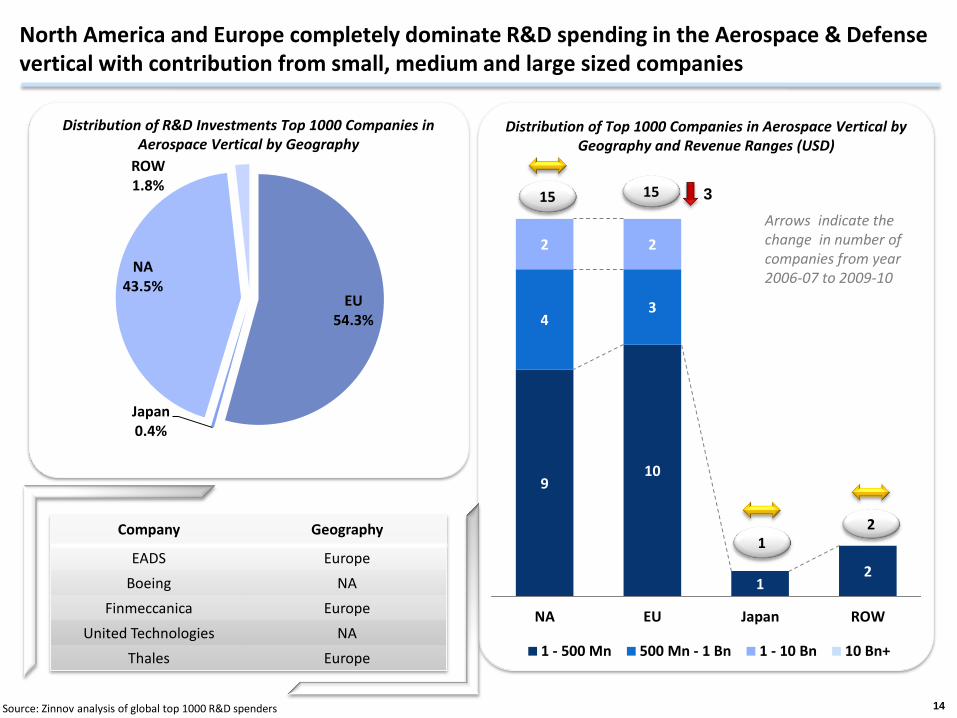

Distribution of R&D Investments Top 1000 Companies in Aerospace Vertical by Geography

North America and Europe completely dominate R&D spending in the Aerospace & Defense vertical with contribution from small, medium and large sized companies

Source: Zinnov analysis of global top 1000 R&D spenders 14

9 10

1 2

4 3

2 2

NA EU Japan ROW

1 - 500 Mn 500 Mn - 1 Bn 1 - 10 Bn 10 Bn+

2

15 15

1

Distribution of Top 1000 Companies in Aerospace Vertical by Geography and Revenue Ranges (USD)

EU 54.3%

Japan 0.4%

NA 43.5%

ROW 1.8%

Company Geography

EADS Europe

Boeing NA

Finmeccanica Europe

United Technologies NA

Thales Europe

3

Arrows indicate the change in number of companies from year 2006-07 to 2009-10

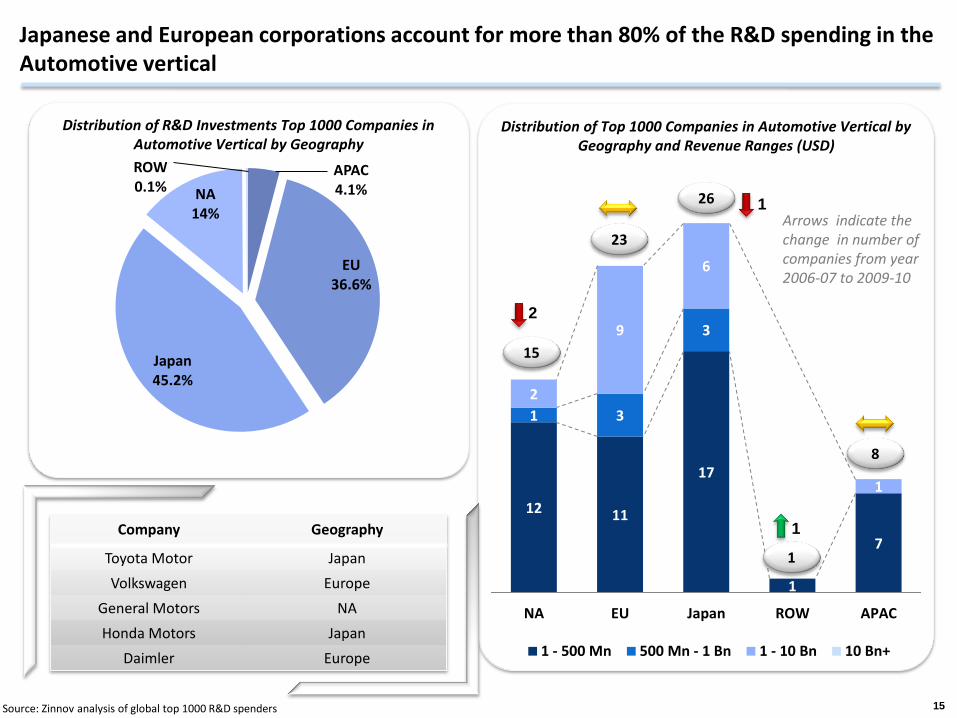

Distribution of R&D Investments Top 1000 Companies in Automotive Vertical by Geography

Japanese and European corporations account for more than 80% of the R&D spending in the Automotive vertical

Source: Zinnov analysis of global top 1000 R&D spenders 15

12 11

17

1

7

1 3

3

2

9

6

1

NA EU Japan ROW APAC

1 - 500 Mn 500 Mn - 1 Bn 1 - 10 Bn 10 Bn+

8

15

23

1

Distribution of Top 1000 Companies in Automotive Vertical by Geography and Revenue Ranges (USD)

APAC 4.1%

EU 36.6%

Japan 45.2%

NA 14%

ROW 0.1%

0.0%

Company Geography

Toyota Motor Japan

Volkswagen Europe

General Motors NA

Honda Motors Japan

Daimler Europe

26

2

1

1

Arrows indicate the change in number of companies from year 2006-07 to 2009-10

Thank You

69 "Prathiba Complex", 4th 'A' Cross, Koramangala Ind. Layout, 5th Block, Koramangala Bangalore – 560095 Phone: +91-80-41127925/6

575 N. Pastoria Ave Suite J Sunnyvale CA – 94085 Phone: +1-408-716-8432

21, Waterway Ave, Suite 300 The Woodlands TX – 77380 Phone: +1-281-362-2773

@zinnov

Top Related