Languages

Pages

Legal

1 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Global Consumer Trends and Key Consumer Targets in Alcoholic

Beverages

Sample Pages

Reference Code: CS0608IS

Publication Date: January 2015

2 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Reasons to buy this report

‘Global Consumer Trends and Key Consumer Targets in Alcoholic Beverages’ provides a comprehensive overview of the

alcoholic beverage landscape, analyzing the regulatory and consumer drivers to identify the best opportunities and

strategies.

Consumer attitudes to drinks The report offers a breakdown of consumers’ view of the

health proposition of five different drinks categories –

carbonated drinks, fruit juice, dairy drinks, bottled water,

and tea and coffee – as well as highlighting which common

drinks ingredients consumers are concerned about.

Future outlook The report provides insight to highlight the "so what?"

implications behind the data, and analysis of how the

need states of consumers within the industry will evolve in

the short-to-medium term future.

Recommended actions Strategic recommendations of how to capitalize on the

evolving consumer landscape are offered, allowing

product and marketing strategies to be better aligned with

the leading trends in the market.

Product innovation examples Examples are provided of innovative international and

country-specific functional drinks product development

within five drinks categories, with analysis of how these

products effectively target the most pertinent consumer

need states.

Identify key consumer targets Key demographic groups driving beverage consumption are

identified. Canadean’s unique consumer data sizes the

percentage of beverage markets that are driven by specific

need states, by age and gender.

Market sizing Beverage market value and volumes are given for leading

countries across the globe. The report highlights which

countries and categories are driving growth and where

growth is stalling.

3 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Executive Summary: Market Context

Both volume and value growth are being driven by emerging economies such as China and India

Across the alcoholic beverages market there is high growth in all

categories in China, which is also the largest Beer market in terms

of volume. India is also a rapidly expanding market, presenting an

attractive opportunity for investment, with largest for cast growth

across the Beer and Spirits sectors.

In Wine, the US and Europe still account for the largest market

share, yet these developing markets are becoming stagnant, with

some high-consumption countries such as France where the overall

volume of Wine consumed is declining.

Speciality Spirits are the most popular global Spiri ts, followed by

Whiskey and Vodka. Much of the Speciali ty Spirits market is driven

by emerging markets where local and regional alcoholic beverages

remain popular.

In value terms, Spirits is the most valuable market, followed by Beer

and then Wine, with Spirits and Beer both forecast high levels of

growth in the US and China, presenting opportunities for

manufacturers to target these expanding markets.

4 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Older males are driving the alcoholic beverages market as women are under-consuming across all categories

Men are driving the alcoholic beverage market, and over-

consuming in every category, more so in Beer & Cider and Spirits.

In Beer, it is older consumers who are over-consuming,

specifically men, and marketers should provide products

formulated specifically to encourage consumption among aging

consumer who are more concerned in regards to health into later

life.

Across the Wine market i t is again older consumers who are

driving the market, and as health is more influential in the Wine

category marketers must focus on promoting the beneficial

aspects of consumption to reassure aging consumers, particularly

in emerging economies with high growth and rapidly again

populations. The gender spli t is more even, highlighting

opportunities to target both men and women.

In Spirits it is consumers aged 25-44 who are driving growth, as

they seek products offering superior experiences and enjoyment,

as older consumers limit consumption of stronger alcohol. It is

men who over-consume Spirits, yet there are growing numbers of

female consumers, particularly in emerging economies.

Executive Summary: Consumer Demographics

5 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Health is becoming increasingly influential across emerging markets Focusing on providing healthier options is essential for growth in

emerging markets. Consumers in China are highly influenced by

health across all alcoholic beverage categories and it is vital that

manufactures respond to the demand for better for you products.

As Wine becomes more popular in Brazi l, consumers, particularly

women, are seeking Wines which promote better health. Marketers

can target this burgeoning market by highlighting the beneficial

aspects of consumption and the link between antioxidants in Red Wine

and overall health.

In more developed markets Health remains a niche motivator of

consumption. However, as consumers become more health-conscious

globally, manufacturers of Beer and Spirits should be prepared to

innovate and provide products meeting the growing desire for healthier

options.

Ultimately, the Health trend will become increasingly influential in

both developed and emerging markets. In these emerging markets

manufactures should focus on better for you options. In more

developed markets, though health is growing in importance, other

concerns will always remain more vital, such as indulgence and value.

Executive Summary: Health in Alcoholic Beverages

6 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Recreating the on-trade experience is vital to drive at-home consumption

One of the main inhibitors of on-trade consumption is price,

highlighting the necessity to manufacturers of providing lower-priced

offerings to encourage a greater number of consumers to drink

outside of the home.

The biggest challenge faced by off-trade manufacturers and retailers

is to drive the number of consumers drinking in the home. By

recreating the on-trade experience – through improving quality,

memorable positioning, and ensuring that at-home options do not

compromise on the social aspect of drinking – manufacturers can

encourage higher levels of off-trade consumption.

Many consumers are also hesitant to try new drinks out of the home

due to scepticism over taste, and manufacturers' must overcome

these consumer perceptions by promoting the indulgence of new

flavors. Craft offerings are also increasingly popular, and marketers

should ensure that any such products are marketed around the

quality of ingredients and formulation and how this relates to a more

enjoyable overall experience.

Of consumers who rarely sample new drinks out of the home, many

state that there are no new offerings they enjoyed, highlighting

opportunities to encourage consumption through more diverse

ranges of flavors.

Executive Summary: Defending Share of Throat

7 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Targeting new audiences and occasions

Targeting new audiences and demographics is vital to sustain

and promote growth across the alcoholic beverages market.

Manufacturers must innovate with products that meet evolving

consumer needs such as the growing desire for more indulgent

offerings across the Beer & Cider market.

Manufacturers can also increase consumption by targeting new

occasions via food pairings. By positioning specifically

formulated Beer products to compliment food occasions,

marketers can encourage consumers to choose Beer over Wine

for eating with a meal.

Increasing the number of premium gifting occasions can also be

successful in driving market growth, as can increasing the level

of connection consumers fell to a brand. As the craft movement

is becoming more popular, consumers want products with more

careful formulation and smaller-scale production. Leveraging the

connection to less mass-produced options and exclusivity of

such brands will appeal to consumers seeking innovative and

novel alcoholic beverage options.

Fusion flavors will also become increasingly popular as

consumers seek more unusual and novel tastes, sampling new

and exciting experiences through alcohol.

Executive Summary: Recommended Actions

8 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Contents

Introduction & Overview

Market Context – Market Volume

Market Context – Market Value

Consumer Demographics

Consumer Analysis – Beer & Cider

Consumer Analysis – Wine

Consumer Analysis – Spirits

Health in Alcoholic Beverages

Defending Share of Throat – Lessons for the On-Trade & Off-Trade

Recommended Actions

Appendix

9 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

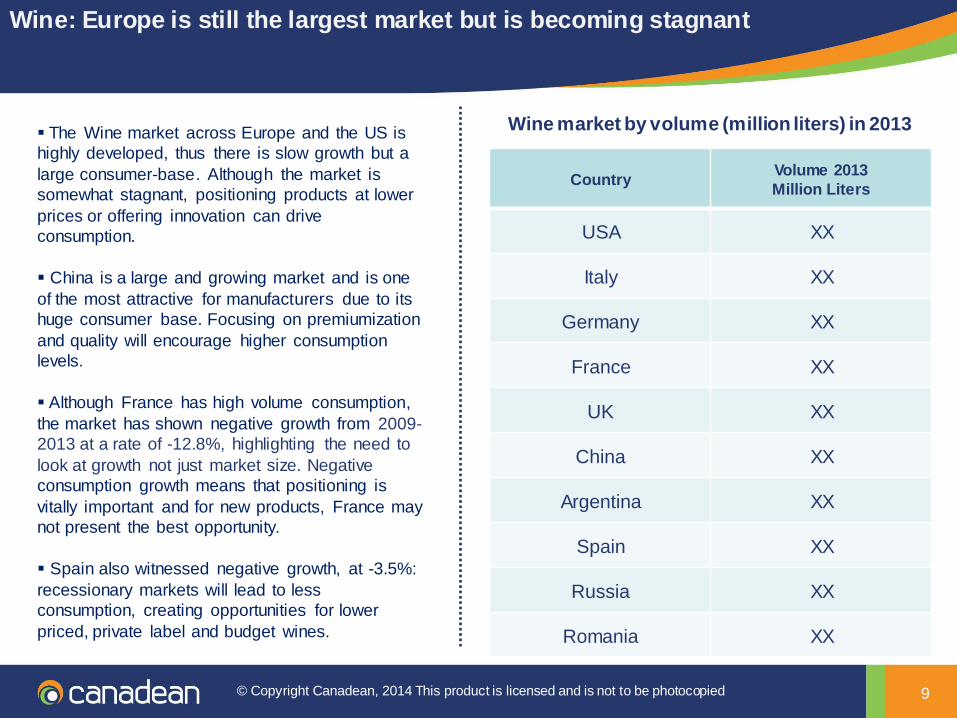

Wine: Europe is still the largest market but is becoming stagnant

The Wine market across Europe and the US is

highly developed, thus there is slow growth but a

large consumer-base. Although the market is

somewhat stagnant, positioning products at lower

prices or offering innovation can drive

consumption.

China is a large and growing market and is one

of the most attractive for manufacturers due to its

huge consumer base. Focusing on premiumization

and quality will encourage higher consumption

levels.

Although France has high volume consumption,

the market has shown negative growth from 2009-

2013 at a rate of -12.8%, highlighting the need to

look at growth not just market size. Negative

consumption growth means that positioning is

vitally important and for new products, France may

not present the best opportunity.

Spain also witnessed negative growth, at -3.5%:

recessionary markets will lead to less

consumption, creating opportunities for lower

priced, private label and budget wines.

Country Volume 2013

Million Liters

USA XX

Italy XX

Germany XX

France XX

UK XX

China XX

Argentina XX

Spain XX

Russia XX

Romania XX

Wine market by volume (million liters) in 2013

10 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Manufacturers should target Older Young Adults and Pre-Mid-Lifers with

more premium offerings

Older Young Adults are over consuming Spirits by XX%, and manufacturers should focus on targeting the growing

desire among this demographic for Spirits which meet their individual taste preferences.

As Individualism is a big concern among 25-34 year olds, marketers can leverage not only the demand for new and

innovative flavors, but the desire to connect to a brand through exclusivity, and less mass-produced and generic

offerings in Spirits, particularly in developed markets.

Early Young Adults

Older Young Adults

Pre-Mid Lifers Mid-Lifers Older

Consumers

XX XX XX XX XX

Across the alcoholic beverages market, Older Consumers are an attractive target for manufacturers. Due to the large

overall size of the demographic, and with life-expectancy rising globally, encouraging consumption among aging

consumers into later life is increasingly important.

In the Beer market, manufacturers must do more to target under-consuming younger demographics, promoting value

through focusing on lower-cost options.

In Wine, marketers can focus on emphasising the social aspects of drinking with friends in both on-trade and off-

trade environments

In Spirits, manufacturers should focus on healthier formulations to appeal to Mid-Life and Older Consumers

concerned with health and quality to encourage higher consumption among a demographic with more disposable

income

Global Spirits over and under-consumption by age-group, 2013

11 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Changing Lifestages is driving the Lager market while Indulgence is most

influential in Beer & Ale and Cider

Lager: 1. Changing Lifestages XX%

2. Better Value for Money XX% 3. Indulgence XX%

Beer & Ale: 1. Indulgence XX%

2. Personal Space & Time XX% 3. Better Value for Money XX%

Cider: 1. Indulgence XX%

2. Personal Space & Time XX% 3. Experience Seeking XX%

Lager is by far the most popular category in the Beer market, and Changing Lifestages are driving consumption

across this sector, as consumers seek products which meet their lifestage needs. This includes more premium options

for consumers with higher disposable income levels who desire quality products to reflect their connoisseurship. Aging

consumers will seek lower calorie options due to health concerns over consumption into later li fe, and manufacturers

should respond by altering formulation to provide better for you options.

Though Beer & Ale and Cider are smaller categories overall, the craft movement and increasing variety of Ciders is

driving rapid growth in these markets. Indulgence is by far the most influential motivator as consumers seek products

which offer the best tastes and flavors, in two markets which have a vastly diverse range of options. Flavored Cider and

innovative formulations in Beer & Ale are driving the market with novel combinations of indulgent tastes, which are

becoming more popular among women and driving occasions in an under-consuming demographic.

12 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Manufacturers must diversify their approaches due to differing consumer

needs across the Spirits market

Brandy:

Changing Lifestages XX%

Indulgence XX%

Manufacturers should focus on providing a

variety of indulgent products to meet the lifestage

needs of consumers.

Marketers should promote Indulgence to

encourage consumption among a younger

demographic who are less likely to opt for

Brandy.

Tequila:

Fun & Enjoyment XX%

Indulgence XX%

As Tequila is often consumed as a shot,

manufacturers can leverage the Fun & Enjoyment

associated with drinking with friends.

Drinking Tequila straight is becoming more

popular, and marketers should promote more

indulgent tastes and innovate to provide smoother,

less harsh flavors to encourage consumption.

Gin:

Individualism XX%

Indulgence XX%

The popularity of Gin is increasing, particularly

among a younger demographic, as manufacturers

have attempted to reinvent the image of the drink.

Consumers are seeking Gin which reflects their

individual taste preferences and will seek the latest

innovative flavors in a burgeoning category which

has the potential for large growth.

Rum:

Indulgence XX%

Fun & Enjoyment XX%

Rum is most often consumed with a mixer, and

consumers seek the most indulgent flavors and

drinks combinations.

Consumers are also concerned with Fun &

Enjoyment, and marketers can promote the

enjoyable and social aspect of consumption with

friends, to encourage sales.

13 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Health is becoming increasingly influential across the alcoholic beverages

market

Although the alcohol market in general will never be a category

driven by the desire for health and wellness, there are many

markets and many sectors where the desire for healthier options is

driving growth. The following section will look at the growing

influence of Health across the alcohol market as a whole, and

analyze which consumers present the most attractive opportunities

for marketers.

By fully understanding which demographics are driven by the desire

healthier options, and through identifying the countries where these

products are most popular, manufacturers can develop entry

strategies around more healthy options.

However, many consumers will not be influenced by Health, and it is

important the manufacturers identify the key areas for growth,

without wasting time and investment on consumers who are

unconcerned with better for you alcohol options.

14 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Lessons for the off-trade: Memorable positioning and a recreation of the

on-trade experience will drive off-trade sales

To further drive sales in off-trade alcohol retail, manufacturers need to ensure that they stay aware of the latest

developments in the on-trade market, and also innovate to encourage a higher number of occasions. By providing

consumers novel products which offer both value and experience, marketers and manufacturers can encourage

consumption in the home, and take share of throat away from bars.

The Austin Brewery Peacemaker offers a 99 can pack of Beer. Despite its seemingly novel positioning, it

actually meets many of the most essential consumer needs.

• Firstly, the essence of the ‘bulk-buy’ offers value to consumers seeking lower-priced alcohol, and here the

product is much cheaper than buying eighteen 6-packs of beer, saving consumers money

• Secondly, whi le initial transportation may be difficult, the sheer number of cans offers convenience as it

means less return trips to the supermarket, and the long shelf-life means that the product is unlikely to spoil.

• Thirdly, it is positioned to encourage social drinking, aimed at younger consumers for parties and gatherings

with friends, whi le the product itself is memorable due its positioning, and this recall and exposure increases

brand loyalty.

15 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Focusing on new flavors and craft offerings will drive out-of-home

consumption

Off-trade marketers looking to increase

out-of-home consumption should focus on

providing new and exciting flavors to

consumers.

Craft offerings are also becoming

increasingly popular, and focusing on

smaller-scale production and connection to

a brand will encourage consumers to try

more new offerings out of the home and

lead to brand loyalty.

On-trade manufacturers seeking to gain

share of throat from on-trade offerings

should focus on recreating the on-trade

experience while offering better value.

Many consumers feel that drinking on-

trade is too expensive but do not want to

sacrifice the social aspects of drinking with

friends. Thus marketers should promote

their products as offering value without

compromising on experience.

16 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Action Points: New ways to target female drinkers

Traditionally, the alcoholic beverage market has

looked to target females through feminine packaging –

usually pink - and sweeter, less harsh flavours. Whilst

women are not always adverse to these colourings

and flavors, a growing number think that such

positioning is outdated and stereotypical.

This does not necessari ly mean that women are

opposed to buying brands offering more ‘feminine’

products, however it does indicate that more subtle

approaches are needed in order to find maximum

success.

As such, manufacturers need to adopt a more

sophisticated approach to targeting females by

combining female-friendly product aspects such as

sweet and fruit-based flavours with more empowering

traits such as promoting strength and independency.

Positioning around social drinking will also help

encourage consumption – for example, moving away

from traditional advertising of women drinking wine at

home and cocktails in bars – as well as showing a

greater number of women drinking beer.

Red Stripe ‘Burst’ is a Rasberry Beer

from Diageo is positioned towards

younger consumers from both

genders. However, the sweet flavor

means it is positioned primarily

towards younger females to

encourage consumption and

acquaint them with the malt flavor

found in classic Red Stripe – creating

brand loyalty and a predilection for

the malt taste of the manufacturer’s

flagship beer.

Vallure Vodka is positioned as a

premium, luxury product, without

employing traditional gender tropes.

The strong prestige image and use of

premium cosmetics influenced gold

packaging targets women in subtler

way than using stereotypical

feminine colours and design, offering

females a more gender neutral

alcohol option.

17 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

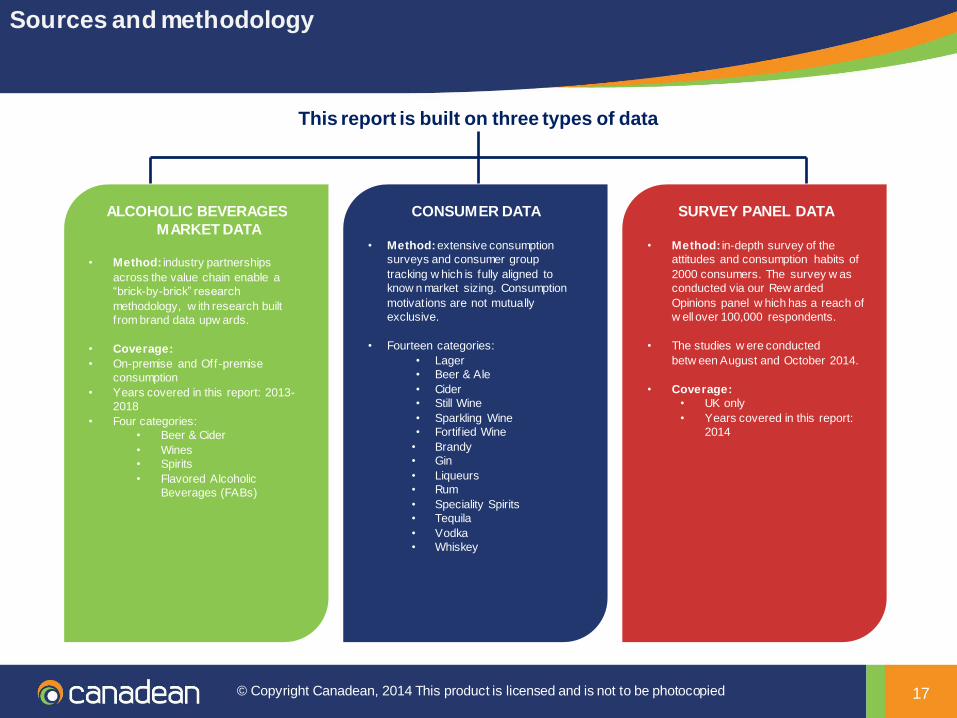

Sources and methodology

This report is built on three types of data

ALCOHOLIC BEVERAGES

MARKET DATA • Method: industry partnerships

across the value chain enable a

“brick-by-brick” research

methodology, w ith research built

from brand data upw ards.

• Coverage:

• On-premise and Off-premise

consumption

• Years covered in this report: 2013-

2018

• Four categories:

• Beer & Cider

• Wines

• Spirits

• Flavored Alcoholic

Beverages (FABs)

SURVEY PANEL DATA

• Method: in-depth survey of the

attitudes and consumption habits of

2000 consumers. The survey w as

conducted via our Rew arded

Opinions panel w hich has a reach of

w ell over 100,000 respondents.

• The studies w ere conducted

betw een August and October 2014.

• Coverage:

• UK only

• Years covered in this report:

2014

CONSUMER DATA

• Method: extensive consumption

surveys and consumer group

tracking w hich is fully aligned to

know n market sizing. Consumption

motivations are not mutually

exclusive.

• Fourteen categories:

• Lager

• Beer & Ale

• Cider

• Still Wine

• Sparkling Wine

• Fortif ied Wine

• Brandy

• Gin

• Liqueurs

• Rum

• Speciality Spirits

• Tequila

• Vodka

• Whiskey

18 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

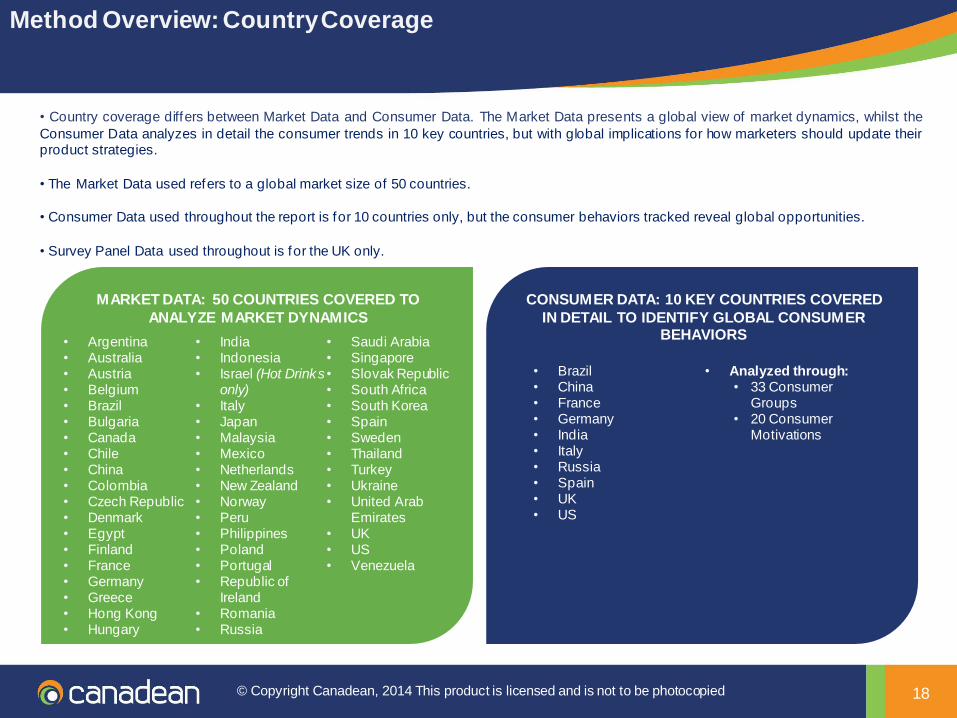

Method Overview: Country Coverage

• Country coverage differs between Market Data and Consumer Data. The Market Data presents a global view of market dynamics, whilst the

Consumer Data analyzes in detail the consumer trends in 10 key countries, but with global implications for how marketers should update their product strategies.

• The Market Data used refers to a global market size of 50 countries.

• Consumer Data used throughout the report is for 10 countries only, but the consumer behaviors tracked reveal global opportunities.

• Survey Panel Data used throughout is for the UK only.

MARKET DATA: 50 COUNTRIES COVERED TO

ANALYZE MARKET DYNAMICS

CONSUMER DATA: 10 KEY COUNTRIES COVERED

IN DETAIL TO IDENTIFY GLOBAL CONSUMER BEHAVIORS

• Argentina • Australia • Austria • Belgium • Brazil • Bulgaria • Canada • Chile • China • Colombia • Czech Republic • Denmark • Egypt • Finland • France • Germany • Greece • Hong Kong • Hungary

• India • Indonesia • Israel (Hot Drinks

only) • Italy • Japan • Malaysia • Mexico • Netherlands • New Zealand • Norway • Peru • Philippines • Poland • Portugal • Republic of

Ireland • Romania • Russia

• Saudi Arabia • Singapore • Slovak Republic • South Africa • South Korea • Spain • Sweden • Thailand • Turkey • Ukraine • United Arab

Emirates • UK • US • Venezuela

• Brazil • China • France • Germany • India • Italy • Russia • Spain • UK • US

• Analyzed through: • 33 Consumer

Groups • 20 Consumer

Motivations

19 © Copyright Canadean, 2014 This product is licensed and is not to be photocopied

Related reports

The Future of Functional Food & Drinks - successful product positioning and claims This report segments the functional food and drinks market by health claim and

consumer age groups, and studies the future of four key trends in the market: probiotics,

glucose control, performance muscle and prevention muscle, and cognitive performance

in adults. Key ingredients are identified in each of these areas. Finally, the future of the

functional food and drinks market is considered.

Identifying new opportunities in the Soft and Hot Drink markets and responding to evolving consumer need states Consumer behavior is evolving rapidly and this will open up new opportunities in both

Soft Drinks and Hot Drinks markets. This includes a more holistic understanding of

health and the role drinks can play in meeting these needs, the continuing influence

consumers’ busy lives have in changing consumption habits, the ongoing key role taste

will play in consumer choices, and the changing consumer perceptions towards sugar

and artificial sweeteners.

What next for Health in Food? Consumer Lifestyles, Nutrition, Food Labelling & Product Choice Disease-related, demographic, and desire-led drivers are making health of growing

importance to food marketers. However, barriers such as cost, habits, and confusion

over how to eat healthily are limiting consumer’s ability to act on these drivers. After

exploring these drivers and barriers, this report focuses on the health solutions available

to consumers, the best practice case studies and the actions food marketers need to

take to make the most of the increased focus on health.

Top Related