Languages

Pages

Legal

GASB UpdateCalifornia Society of Municipal Finance Officers

February 21, 2013Michelle Czerkawski, GASB Project Manager

The views expressed in this presentation are those of the speaker. Official positions of the GASB are determined only after extensive due process and

deliberation.

Session AgendaBoard appointmentsRecently issued Statements

◦Review of effective dates◦Statements effective for 2013 FYEs—

key provisions◦Statements effective for post-2013

FYEs—brief overviewCurrent-agenda projects

3

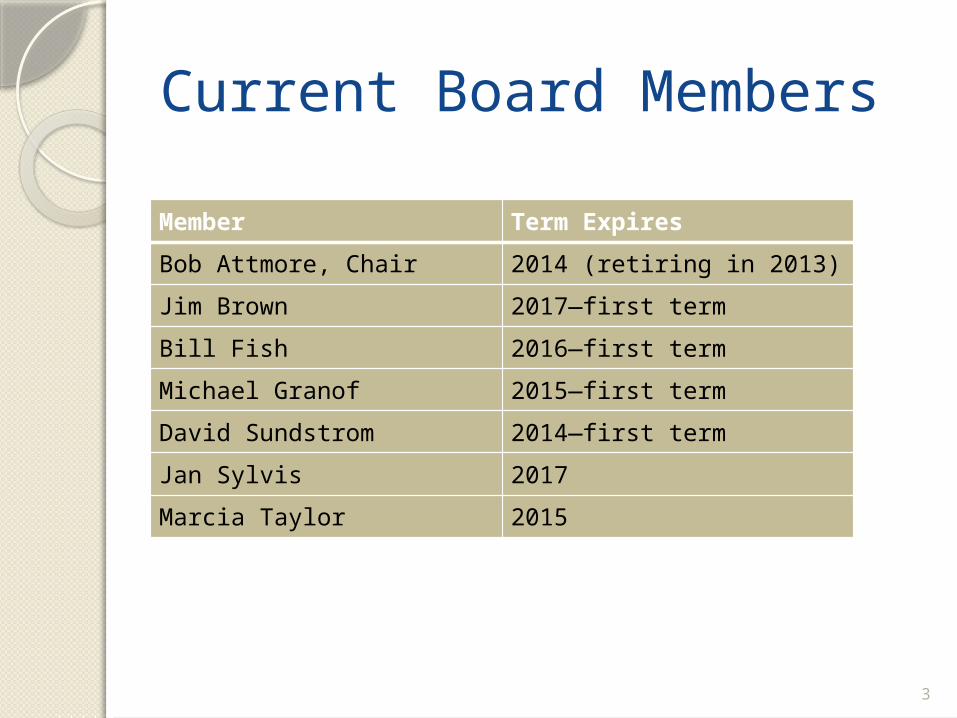

Current Board Members

Member Term Expires

Bob Attmore, Chair 2014 (retiring in 2013)

Jim Brown 2017—first term

Bill Fish 2016—first term

Michael Granof 2015—first term

David Sundstrom 2014—first term

Jan Sylvis 2017

Marcia Taylor 2015

RECENTLY ISSUED STATEMENTS

5

Effective Dates—FYE June 30 2013

◦ Statement 60—Service Concession Arrangements◦ Statement 61—Financial Reporting Entity◦ Statement 62—Codification of AICPA & FASB ◦ Statement 63—Deferrals Presentation

2014◦ Statement 65—Assets & Liabilities—Reclassification &

Recognition◦ Statement 66—Technical Corrections◦ Statement 67—Pension Plans

2015◦ Statement 68—Pension Accounting for Employers &

Nonemployer Contributing Entities◦ Statement 69—Government Combinations & Disposals of

Government Operations

Service Concession Arrangements (SCAs)

2013 FYEs: Statement 60

Effective for Periods Beginning after December 15, 2011

7

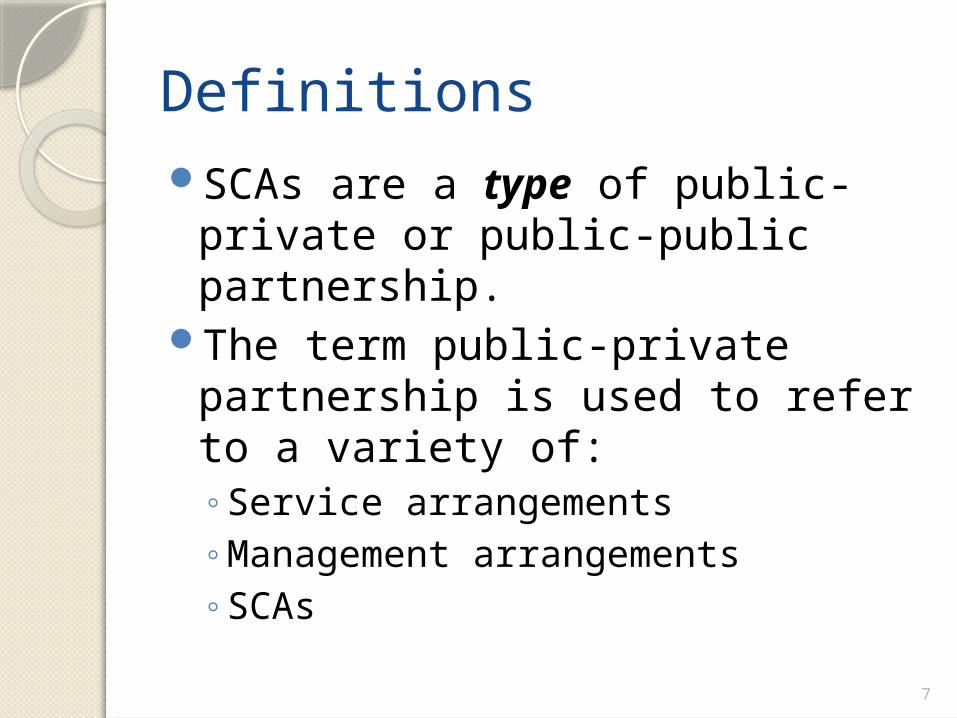

DefinitionsSCAs are a type of public-private

or public-public partnership. The term public-private

partnership is used to refer to a variety of:◦Service arrangements◦Management arrangements ◦SCAs

8

Scope Transferor conveys to operator right & related

obligation to provide public services through the operation of a capital asset in exchange for significant consideration◦ Examples: Up-front payment, installment payments, new

facility, improvements to existing facility Operator collects & is compensated from fees from

third parties Transferor determines /has the ability to modify or

approve:◦ What services the operator is required to provide◦ To whom the operator is required to provide the services◦ Prices or rates that can be charged for the services

Transferor entitled to significant residual interest in the service utility of the facility at end of the arrangement

9

Facilities Associated with SCAs

If new & purchased/constructed by operator or existing that has been improved by the operator◦Transferor reports:

New facility or improvement—capital asset at fair value when placed in operation

Any contractual obligations—liabilities, with deferred inflow of resources

10

Upfront or Installment PaymentsTransferor reports:

◦Up-front payment or present value of installment payments—asset

◦Any contractual obligations—liabilities, with deferred inflow of resources

◦Revenue as deferred inflow of resources is reduced Systematic & rational manner Over term of the arrangement Beginning when facility is placed into

operation

11

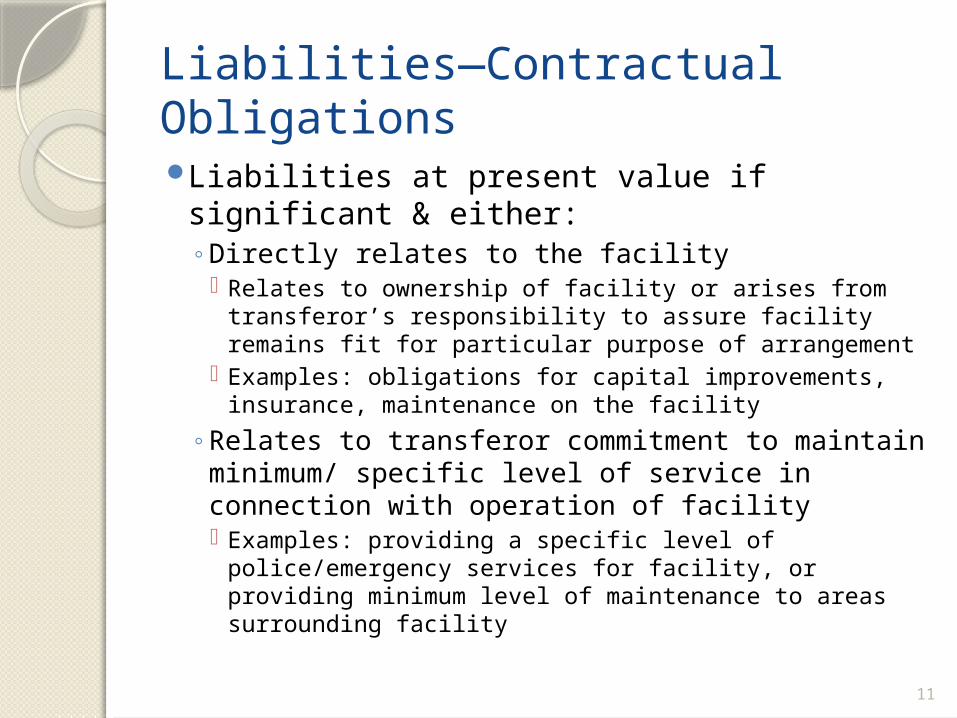

Liabilities—Contractual ObligationsLiabilities at present value if significant &

either:◦Directly relates to the facility

Relates to ownership of facility or arises from transferor’s responsibility to assure facility remains fit for particular purpose of arrangement

Examples: obligations for capital improvements, insurance, maintenance on the facility

◦Relates to transferor commitment to maintain minimum/ specific level of service in connection with operation of facility Examples: providing a specific level of

police/emergency services for facility, or providing minimum level of maintenance to areas surrounding facility

12

The Financial Reporting Entity—Omnibus

2013 FYEs:Statement 61

Effective for Periods Beginning after June 15, 2012

13

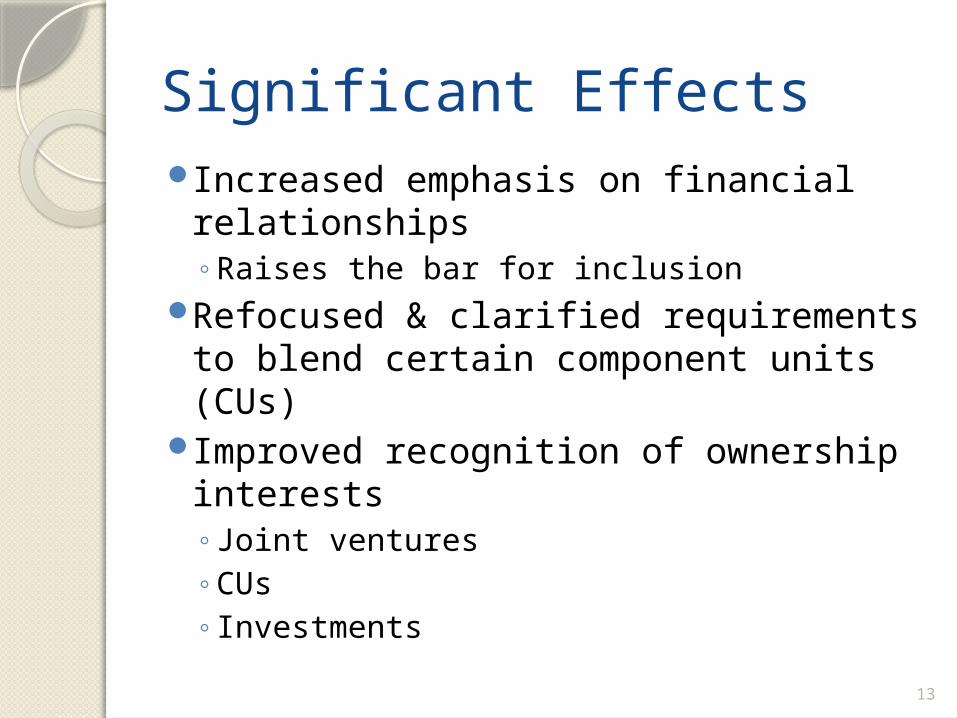

Significant EffectsIncreased emphasis on financial

relationships◦Raises the bar for inclusion

Refocused & clarified requirements to blend certain component units (CUs)

Improved recognition of ownership interests◦Joint ventures◦CUs◦Investments

14

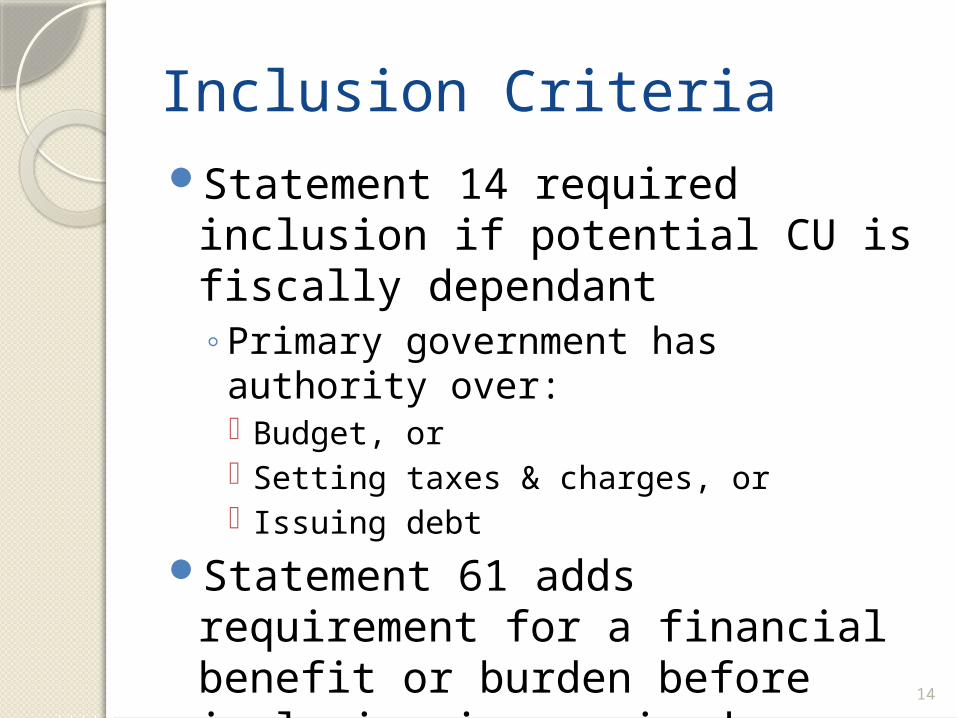

Inclusion CriteriaStatement 14 required inclusion

if potential CU is fiscally dependant◦Primary government has authority

over: Budget, or Setting taxes & charges, or Issuing debt

Statement 61 adds requirement for a financial benefit or burden before inclusion is required

15

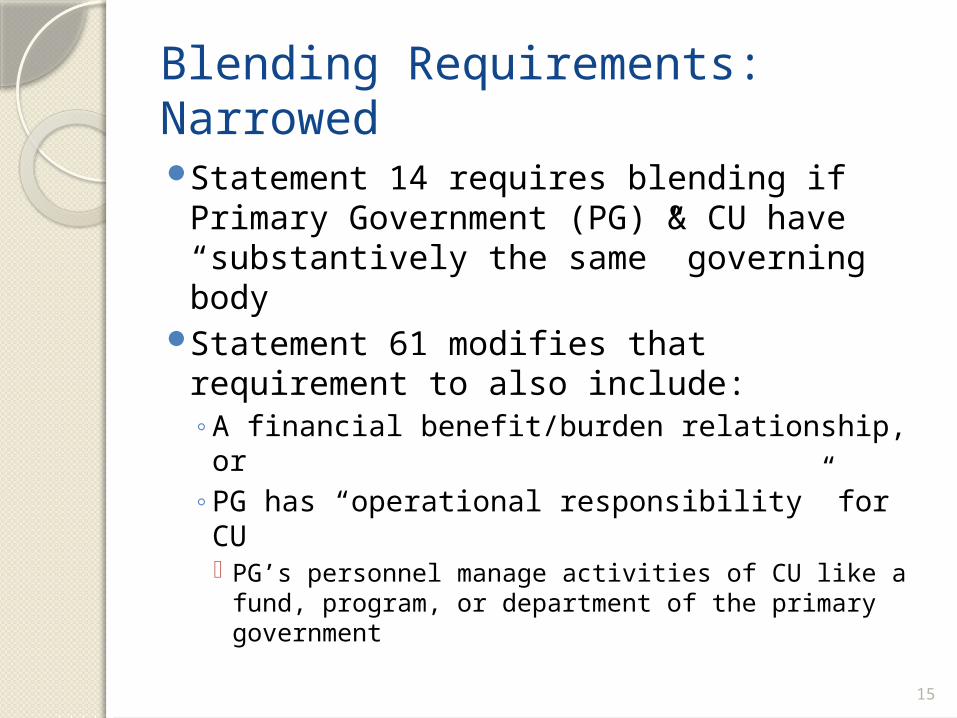

Blending Requirements: NarrowedStatement 14 requires blending if

Primary Government (PG) & CU have “substantively the same” governing body

Statement 61 modifies that requirement to also include:◦A financial benefit/burden relationship, or◦PG has “operational responsibility” for CU

PG’s personnel manage activities of CU like a fund, program, or department of the primary government

16

Blending Requirements: BroadenedInclude CUs whose total debt

outstanding is expected to be repaid entirely or almost entirely by revenues of the PG◦Even if the CU provides services to

constituents or other governments, rather than exclusively or almost exclusively to the PG

17

Note DisclosuresClarifies that current disclosures

require:◦Rationale for including each CU◦Whether CU is discretely presented,

blended, or included as a fiduciary fund

No new disclosuresPractical consideration—can

aggregate similar CUs for disclosure

18

Codification of Pre-November 30, 1989 FASB and AICPA Pronouncements

2013 FYEs: Statement 62

Effective for Periods Beginning after December 15, 2011

19

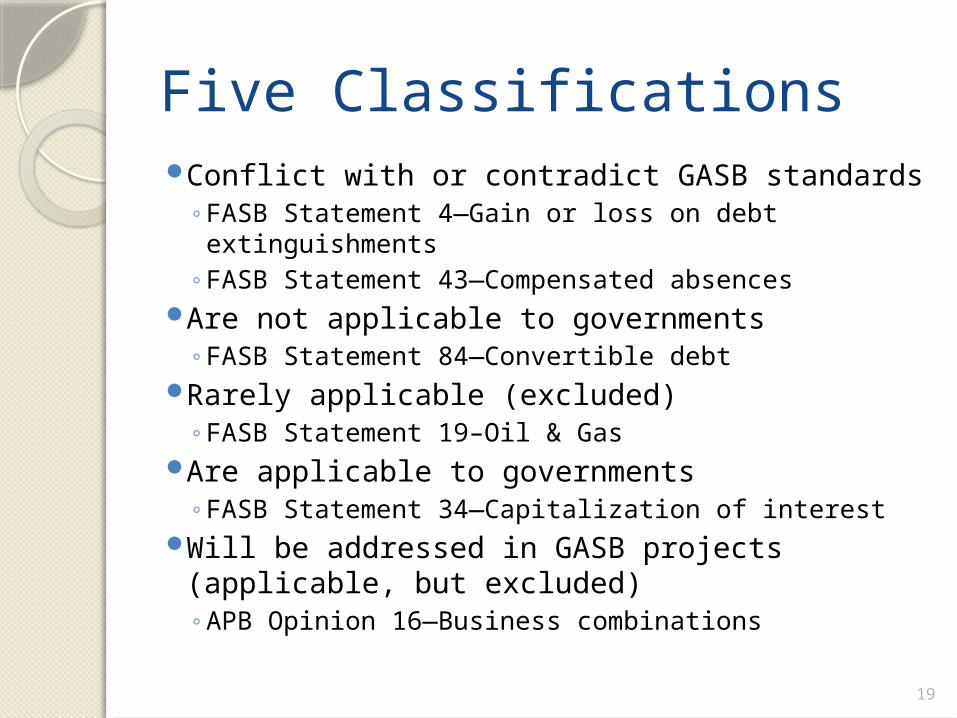

Five ClassificationsConflict with or contradict GASB standards

◦ FASB Statement 4—Gain or loss on debt extinguishments

◦ FASB Statement 43—Compensated absencesAre not applicable to governments

◦ FASB Statement 84—Convertible debtRarely applicable (excluded)

◦ FASB Statement 19–Oil & GasAre applicable to governments

◦ FASB Statement 34—Capitalization of interestWill be addressed in GASB projects (applicable,

but excluded)◦ APB Opinion 16—Business combinations

20

Basic GuidanceStatement 20 is superseded

◦All applicable pre-11/30/89 standards are contained in the GASB’s codification

◦All potentially applicable post-11/30/89 non-GASB standards will be “other accounting literature”

Guidance on 29 topics is brought into the GASB literature

21

Significant TopicsSpecial & extraordinary items (APB Opinion 30)Comparative financial statements (ARB 43)Related parties (FASBS 57)Prior-period adjustments (FASBS 16 & APB

Opinion 9)Accounting changes & error corrections (APB

Opinion 20 & FASBI 20)Contingencies (FASBS 5 & FASBI 14)Extinguishments of debt (APB Opinion 26 &

FASBS 76)Inventory (ARB 43)Leases (FASBS 13, 22, 98 & FASBI 23, 26, 27)

22

Specialized TopicsSales of real estate (FASBS 66)Real estate projects (FASBS 67)Research & development arrangements

(FASBS 68)Broadcasters (FASBS 63)Cable television systems (FASBS 51)Insurance enterprises (FASBS 60)Lending activities (FASBS 91)Mortgage banking activities (FASBS 65)Regulated operations (FASBS 71, 90, 101)

23

Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position

2013 FYEs: Statement 63

Effective for Periods Beginning after December 15, 2011

24

BackgroundConcepts Statement 4—five

elements in a statement of financial position ◦Assets◦Liabilities◦Deferred outflows of resources◦Deferred inflows of resources◦Net position

Differs from composition required by Statement 34

25

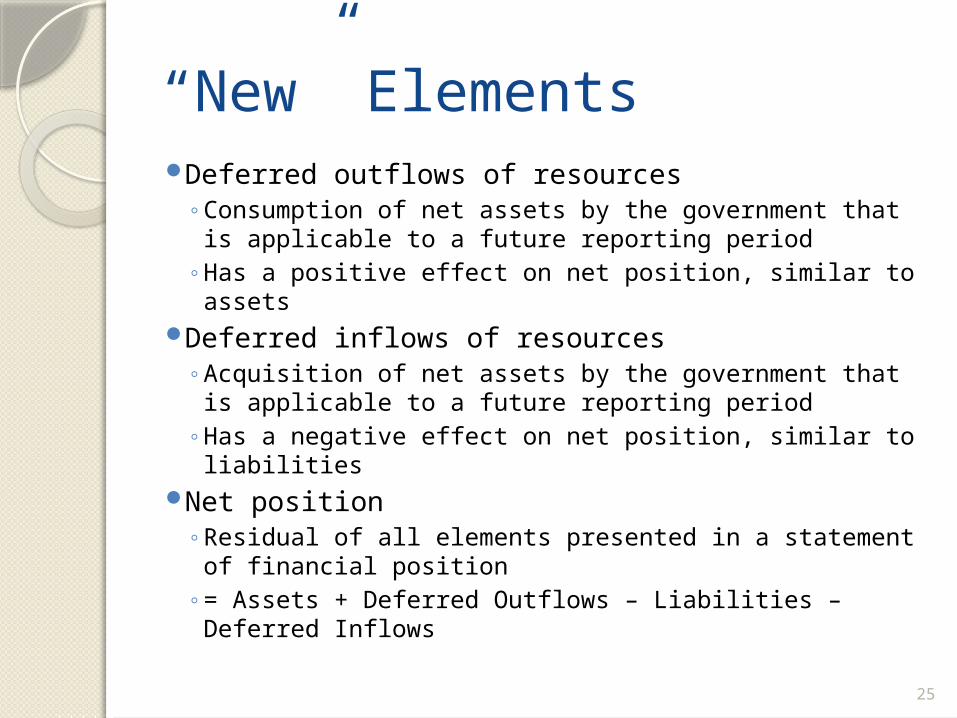

“New” ElementsDeferred outflows of resources

◦ Consumption of net assets by the government that is applicable to a future reporting period

◦ Has a positive effect on net position, similar to assetsDeferred inflows of resources

◦ Acquisition of net assets by the government that is applicable to a future reporting period

◦ Has a negative effect on net position, similar to liabilities

Net position◦ Residual of all elements presented in a statement of

financial position ◦ = Assets + Deferred Outflows – Liabilities – Deferred

Inflows

26

Display RequirementsDeferred outflows of resources reported in a

separate section following assetsDeferred inflows of resources reported in a

separate section following liabilitiesNet position components

◦ Resemble net asset components under Statement 34 Net investment in capital assets Restricted Unrestricted

◦ Include the effects of deferred outflows & deferred inflows of resources

Governmental funds continue to report fund balance

27

Deferred Outflows/Inflows of ResourcesPrior standards

◦Statement 53—Derivative Instruments

◦Statement 60—Service Concession Arrangements

Post-issuance standards◦Statement 65—Items Previously

Reported as Assets & Liabilities◦Statement 68—Pensions◦Statement 69—Government

Combinations

28

Items Previously Reported as Assets and Liabilities

Later FYEs:Statement 65

Effective for Periods Beginning after December 15, 2012

29

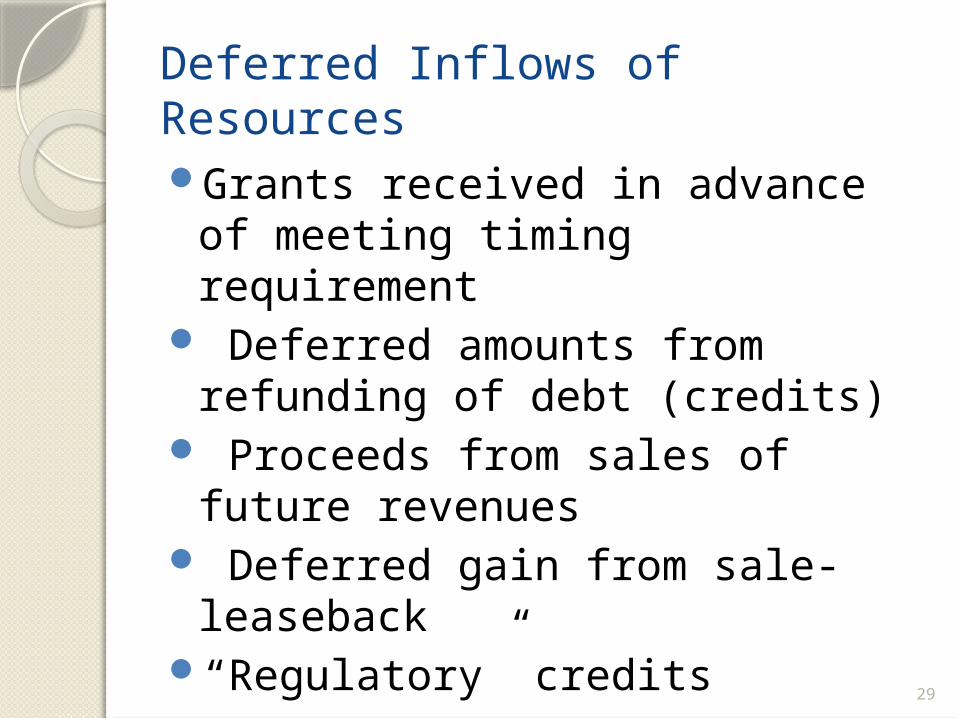

Deferred Inflows of Resources

Grants received in advance of meeting timing requirement

Deferred amounts from refunding of debt (credits)

Proceeds from sales of future revenues

Deferred gain from sale-leaseback

“Regulatory” credits

30

Deferred Outflows of Resources

Grant paid in advance of meeting timing requirement

Deferred amounts from refunding of debt (debits)

Cost to acquire rights to future revenues (intra-entity)

Deferred loss from sale-leaseback

31

Outflows of ResourcesDebt issuance costs (other than

insurance) Initial costs incurred by lessor in

an operating lease Acquisition costs for risk pools Loan origination costs

32

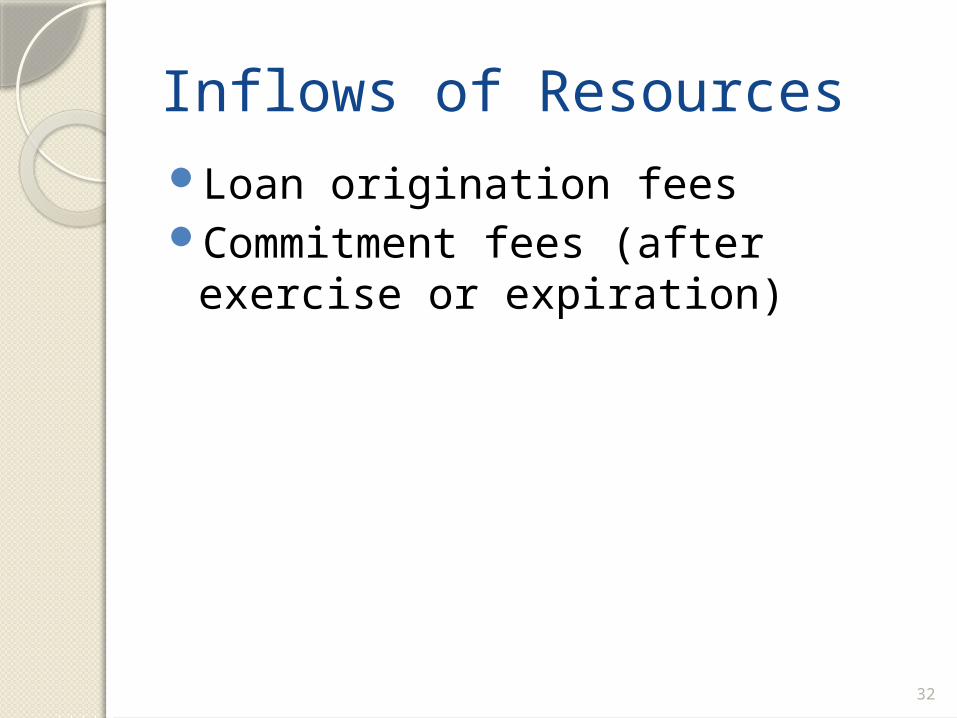

Inflows of ResourcesLoan origination feesCommitment fees (after exercise

or expiration)

33

Technical Corrections—2012

Later FYEs: Statement 66

Effective for Periods Beginning after December 15, 2012

34

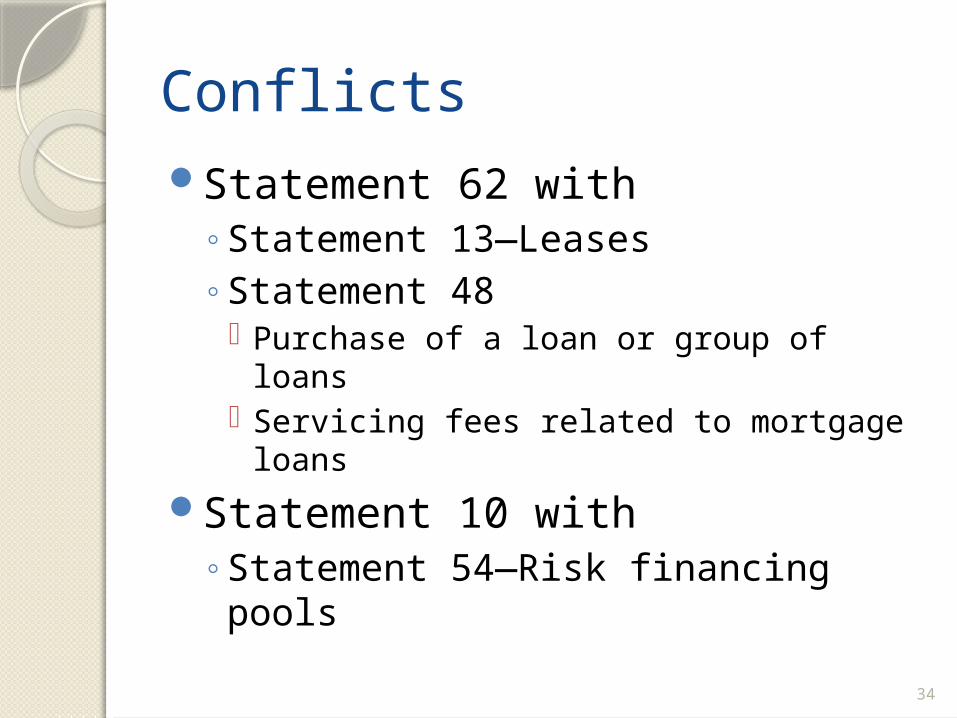

ConflictsStatement 62 with

◦Statement 13—Leases◦Statement 48

Purchase of a loan or group of loans Servicing fees related to mortgage loans

Statement 10 with◦Statement 54—Risk financing pools

35

Financial Reporting for Pension Plans

Later FYEs:Statement 67

Effective for Fiscal Years Beginning after June 15, 2013

36

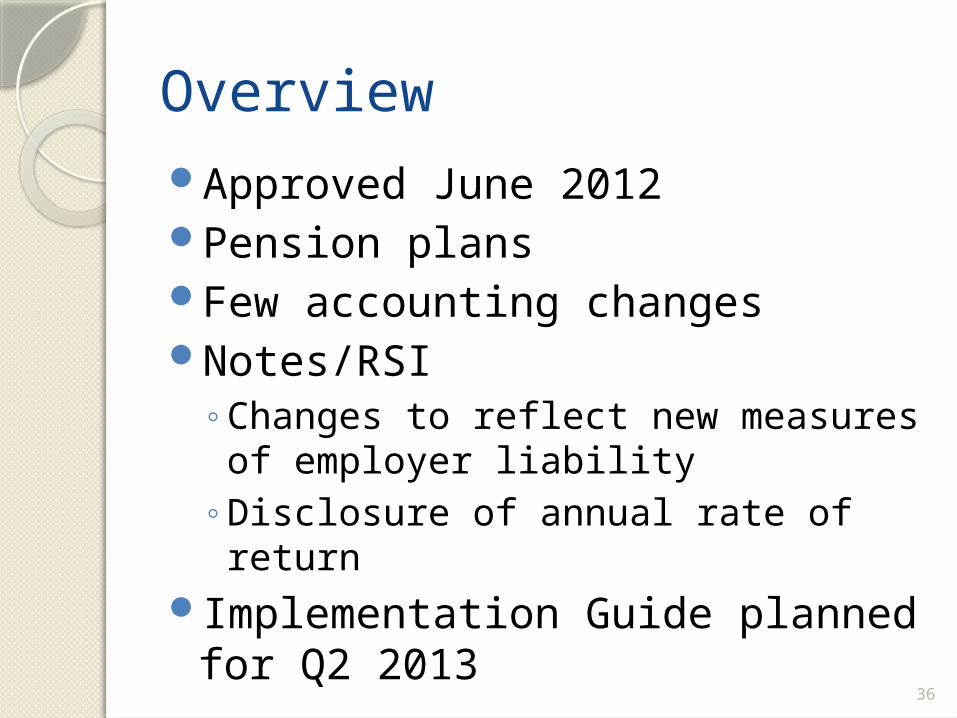

OverviewApproved June 2012Pension plansFew accounting changesNotes/RSI

◦Changes to reflect new measures of employer liability

◦Disclosure of annual rate of return Implementation Guide planned

for Q2 2013

37

Accounting and Financial Reporting for Pensions

Later FYEs:Statement 68

Effective for Fiscal Years Beginning after June 15, 2014

38

OverviewApproved June 2012Employer reporting & certain

governmental nonemployer contributing entities

Changes in liability & expense recognition◦Break with funding measures◦Similar recognition for all types of employers

(single, agent, cost-sharing)Notes disclosure/RSI changesAdditional implementation guidance

planned for Q1 2014

Government Combinations and Disposals of Government Operations

Later FYEs: Statement 69

Effective for Transactions Occurring in Financial Reporting Periods Beginning after December 15, 2013

40

ScopeCombinations in which no

consideration is provided◦Government mergers◦Transfers of operations

Combinations in which consideration is provided◦Government acquisitions

Disposal of government operations

41

Mergers & Transfers of OperationsAssets & liabilities at carrying values

◦Presumption of GAAPReporting

◦Mergers New entity Continuing entity

◦Transfers of operationsAdjustments

◦Accounting principles, policies, & estimates◦Capital asset impairment◦Transaction eliminations

42

AcquisitionsAssets (& liabilities) at acquisition

value◦Recognition based on GAAP applicable to

state & local governments◦Market-based entry price measurements◦Exceptions

Difference between consideration given and net position acquired◦“Goodwill”—deferred outflow of resources◦Contribution received or reduction of non-

current assets

43

Note Disclosures—All CombinationsGeneral information

◦Brief description of the combination & identification of the entities involved

◦Date of the combination◦Primary reasons for the combination

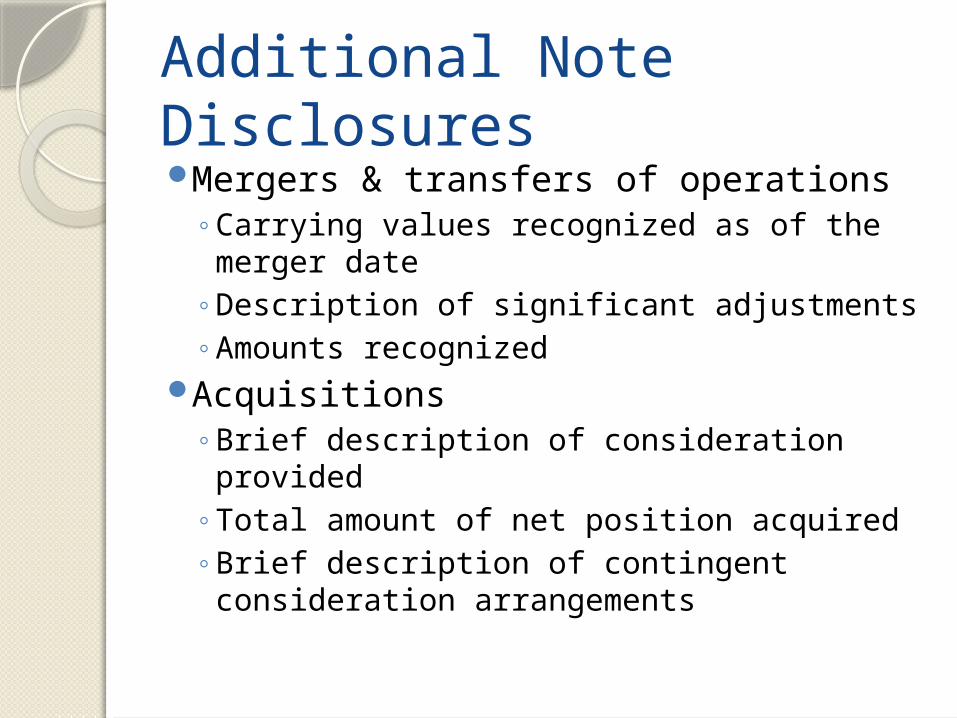

Additional Note DisclosuresMergers & transfers of operations

◦Carrying values recognized as of the merger date

◦Description of significant adjustments◦Amounts recognized

Acquisitions◦Brief description of consideration

provided◦Total amount of net position acquired◦Brief description of contingent

consideration arrangements

45

Disposals of Government OperationsIncludes all disposals of operations

(transfers or sales)◦Gains & losses reported as special items

Costs associated with disposals of government operations◦Consider only costs directly associated with

disposalDisclosures

◦Description of the circumstances leading to the discontinuation

◦Operations revenues, expense, & non-operating items

46

CURRENT AGENDA PROJECTS

47

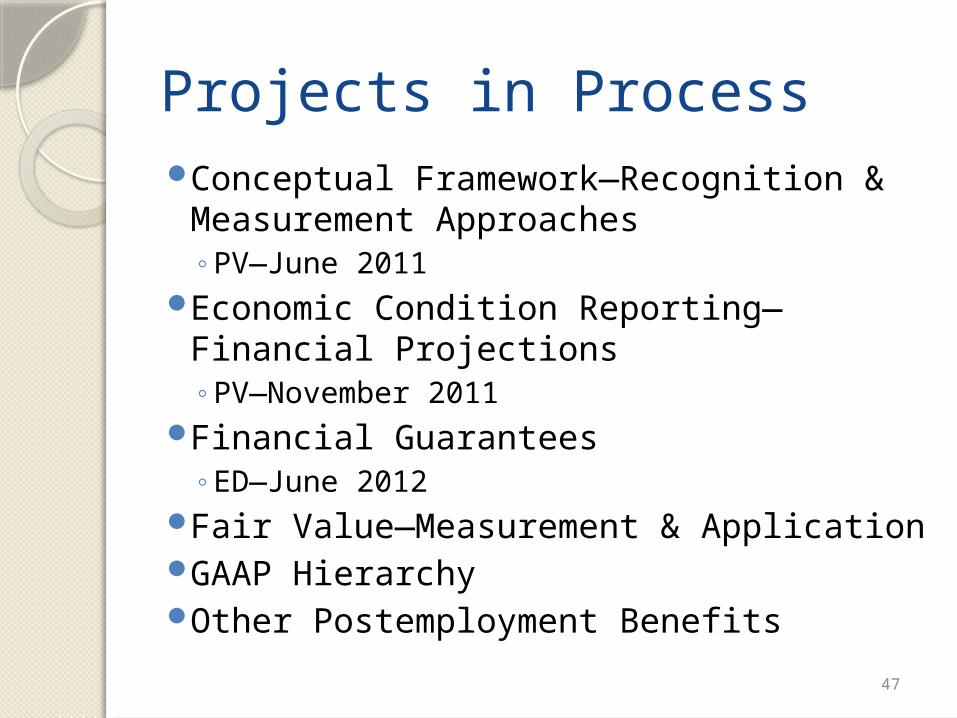

Projects in ProcessConceptual Framework—Recognition &

Measurement Approaches ◦PV—June 2011

Economic Condition Reporting—Financial Projections◦PV—November 2011

Financial Guarantees◦ED—June 2012

Fair Value—Measurement & ApplicationGAAP HierarchyOther Postemployment Benefits

48

RESEARCH AGENDA PROJECTS

49

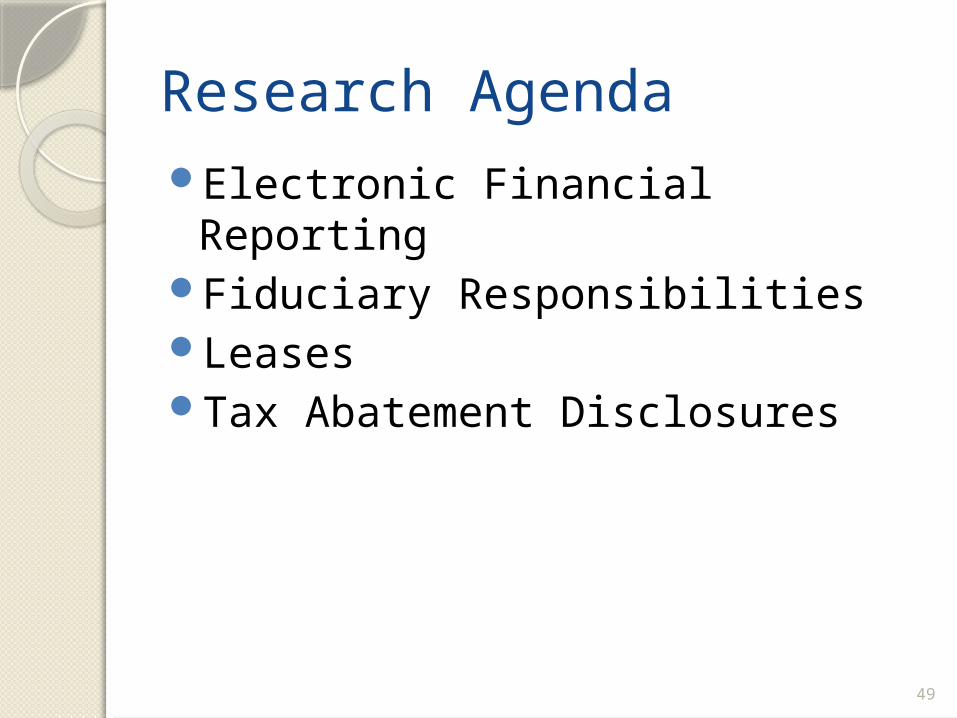

Research AgendaElectronic Financial ReportingFiduciary ResponsibilitiesLeasesTax Abatement Disclosures

50

FOR ADDITIONAL INFORMATION/RESOURCES:

WWW.GASB.ORG

Top Related