Languages

Pages

Legal

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 1/61

Modelling the FX Skewodelling the FX Skew

Dherminder Kainth and Nagulan SaravanamuttuDherminder Kainth and Nagulan Saravanamuttu

QuaRC, Royal Bank of ScotlandQuaRC, Royal Bank of Scotland

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 2/61

Overview

o FX Markets

o Possible Models and Calibration

o Variance Swaps

o Extensions

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 3/61

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 4/61

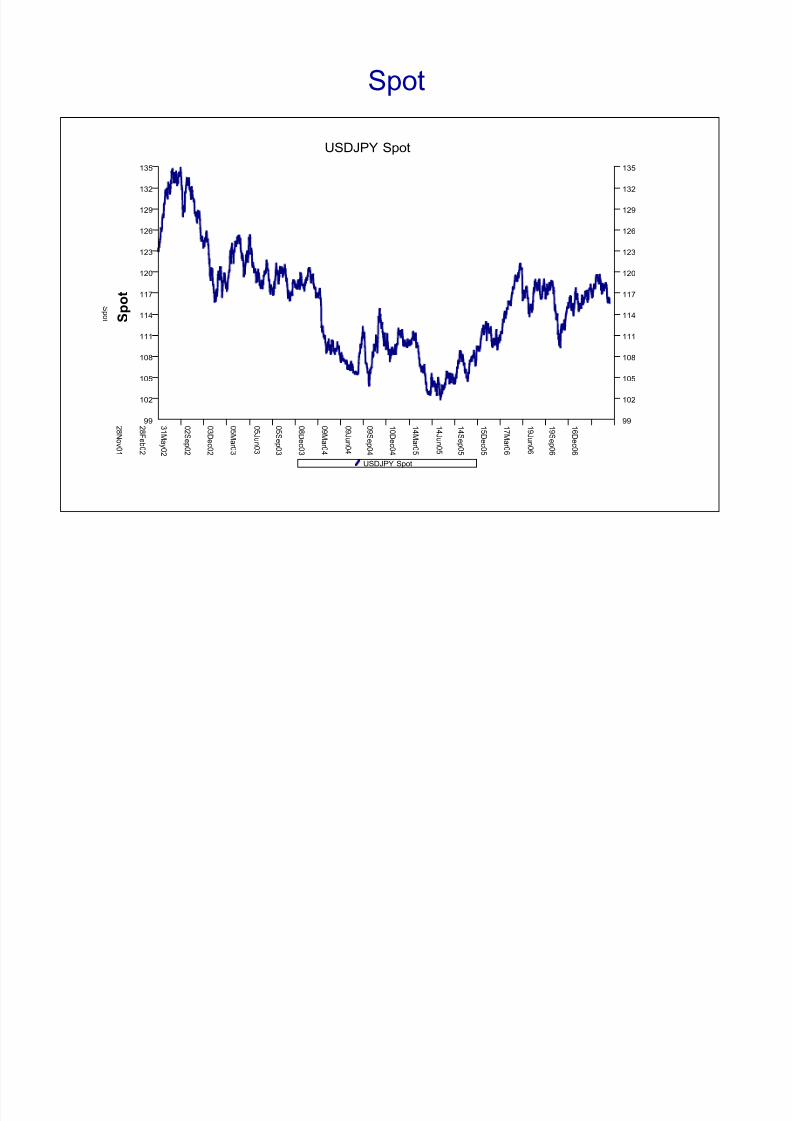

Spot

USDJPY Spot

USDJPY Spot

S p o t

99

102

105

108

111

114

117

120

123

126

129

132

135

99

102

105

108

111

114

117

120

123

126

129

132

135

2 8 N ov 0 1

2 8 F e b 0 2

3 1 M a y 0 2

0 2 S e p 0 2

0 3 D e c 0 2

0 5 M ar 0 3

0 5 J un 0 3

0 5 S e p 0 3

0 8 D e c 0 3

0 9 M ar 0 4

0 9 J un 0 4

0 9 S e p 0 4

1 0 D e c 0 4

1 4 M ar 0 5

1 4 J un 0 5

1 4 S e p 0 5

1 5 D e c 0 5

1 7 M ar 0 6

1 9 J un 0 6

1 9 S e p 0 6

1 6 D e c 0 6

S p o t

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 5/61

Volatility

USDJPY 1M Historic Volatility

4

5

6

7

8

9

10

11

12

13

14

15

16

17

4

5

6

7

8

9

10

11

12

13

14

15

16

17

2 8 N ov 0 1

2 8 F e b 0 2

3 1 M a y 0 2

0 2 S e p 0 2

0 3 D e c 0 2

0 5 M ar 0 3

0 5 J un 0 3

0 5 S e p 0 3

0 8 D e c 0 3

0 9 M ar 0 4

0 9 J un 0 4

0 9 S e p 0 4

1 0 D e c 0 4

1 4 M ar 0 5

1 4 J un 0 5

1 4 S e p 0 5

1 5 D e c 0 5

1 7 M ar 0 6

1 9 J un 0 6

1 9 S e p 0 6

1 4 D e c 0 6

V o l a t i l i t y

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 6/61

European Implied Volatility Surface

• Implied volatility smile defined in terms of deltas

• Quotes available

‒ Delta-neutral straddle ⇒ Level

‒ Risk Reversal = (25-delta call ‒ 25-delta put) ⇒Skew

‒ Butterfly = (25-delta call + 25-delta put ‒ 2ATM) ⇒Kurtosis

• Also get 10-delta quotes

• Can infer five implied volatility points per expiry

‒ ATM

‒ 10 delta call and 10 delta put ‒ 25 delta call and 25 delta put

• Interpolate using, for example, SABR or Gatheral

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 7/61

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 8/61

Implied Volatility Smiles

6

6.5

7

7.5

8

8.5

9

9.5

10

10.5

11

10C 25C ATM 25P 10P

delta

I m p l i e d V o l a t i

l i t y 1M

1Y

2Y

6

6.5

7

7.5

8

8.5

9

9.5

10

10.5

11

10C 25C ATM 25P 10P

delta

I m p l i e d V o l a t i l i t y 1M

1Y

2Y

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 9/61

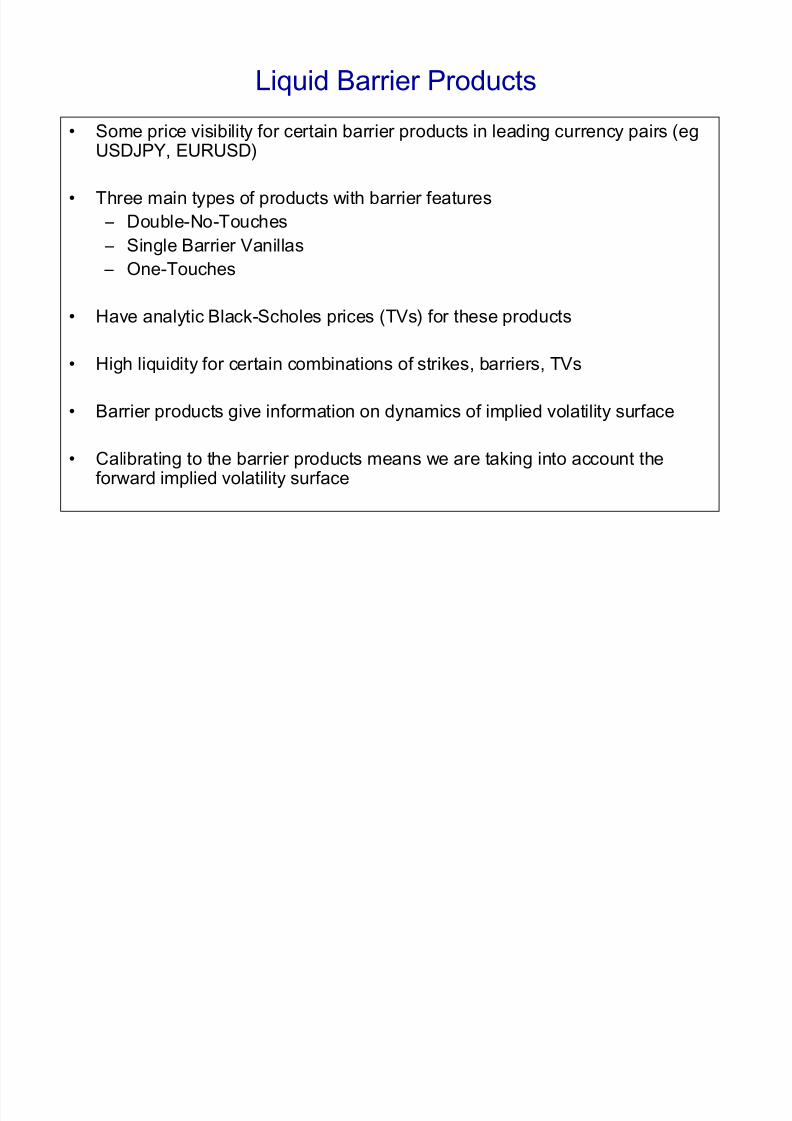

Liquid Barrier Products

• Some price visibility for certain barrier products in leading currency pairs (egUSDJPY, EURUSD)

• Three main types of products with barrier features

‒ Double-No-Touches

‒ Single Barrier Vanillas

‒ One-Touches

• Have analytic Black-Scholes prices (TVs) for these products

• High liquidity for certain combinations of strikes, barriers, TVs

• Barrier products give information on dynamics of implied volatility surface

• Calibrating to the barrier products means we are taking into account theforward implied volatility surface

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 10/61

Double-No-Touches

• Pays one if barriers not breached through lifetime of product

• Upper and lower barriers determined by TV and UL=S2

• High liquidity for certain values of TV : 35%, 10%

time

0 T

F X

r a t e

U

L

S

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 11/61

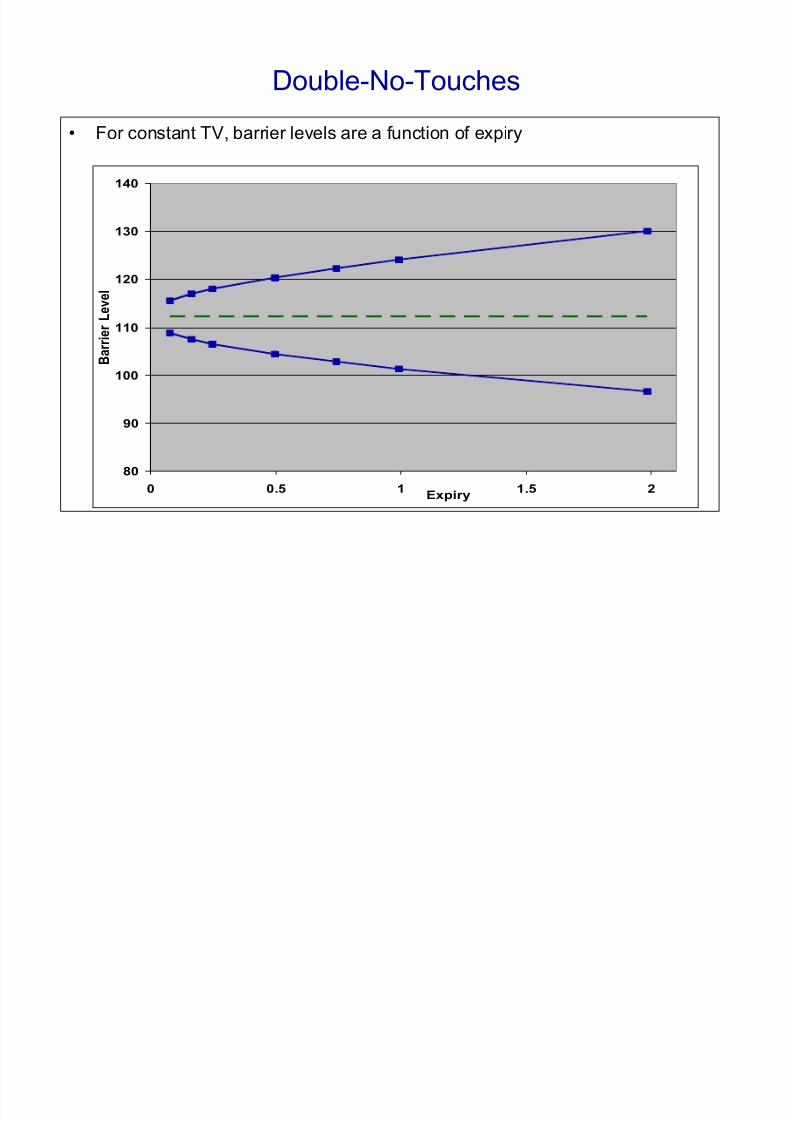

Double-No-Touches

• For constant TV, barrier levels are a function of expiry

80

90

100

110

120

130

140

0 0.5 1 1.5 2Expiry

B a r r i e r L e v e l

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 12/61

Single Barrier Vanilla Payoffs

• Single barrier product which pays off a call or put depending on whether barrier is breached throughout life of product

• Three aspects

‒ Final payoff (Call or Put)

‒ Pay if barrier breached or pay if it is not breached (Knock-in or Knock-out)

‒ Barrier higher or lower than spot (Up or Down)

• Leads to eight different types of product

• Significant amount of value apportioned to final smile (depending on

strike/barrier combination)

• Not as liquid as DNTs

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 13/61

One-Touches

• Single barrier product which pays one when barrier is breached

• Pay off can be in domestic or foreign currency

• There is some price visibility for one-touches in the leading currency markets

• Not as liquid as DNTs

• Price depends on forward skew

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 14/61

Replicating Portfolio

60 70 80 90 100 110 12060 70 80 90 100 110 12060 70 80 90 100 110 12060 70 80 90 100 110 120

SpotKB

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 15/61

Replicating Portfolio

60 70 80 90 100 110 12060 70 80 90 100 110 120

SpotKB

u < T

T

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 16/61

60 70 80 90 100 110 120

Replicating Portfolio

60 70 80 90 100 110 12060 70 80 90 100 110 120

SpotKB

u < T

T

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 17/61

One-Touches

• For Normal dynamics with zero interest rates

• Price of One-Touch is probability of breaching barrier

• Static replication of One-Touch with Digitals

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 18/61

One-Touches

• Log-Normal dynamics

• Barrier is breached at time

• Can still statically replicate One-Touch

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 19/61

One-Touches

• Introduce skew

• Using same static hedge

• Price of One-Touch depends on skew

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 20/61

Model Skew

• Model Skew : (Model Price ‒ TV)

• Plotting model skew vs TV gives an indication of effect of model-implied smile

dynamics

• Can also consider market-implied skew which eliminates effect of particular

market conditions (eg interest rates)

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 21/61

Possible Models and Calibration

o Local Volatility

o Heston

o Piecewise-Constant Heston

o Stochastic Correlation

o Double-Heston

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 22/61

Local Volatility

• Local volatility process

• Ito-Tanaka implies

• Dupires formula

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 23/61

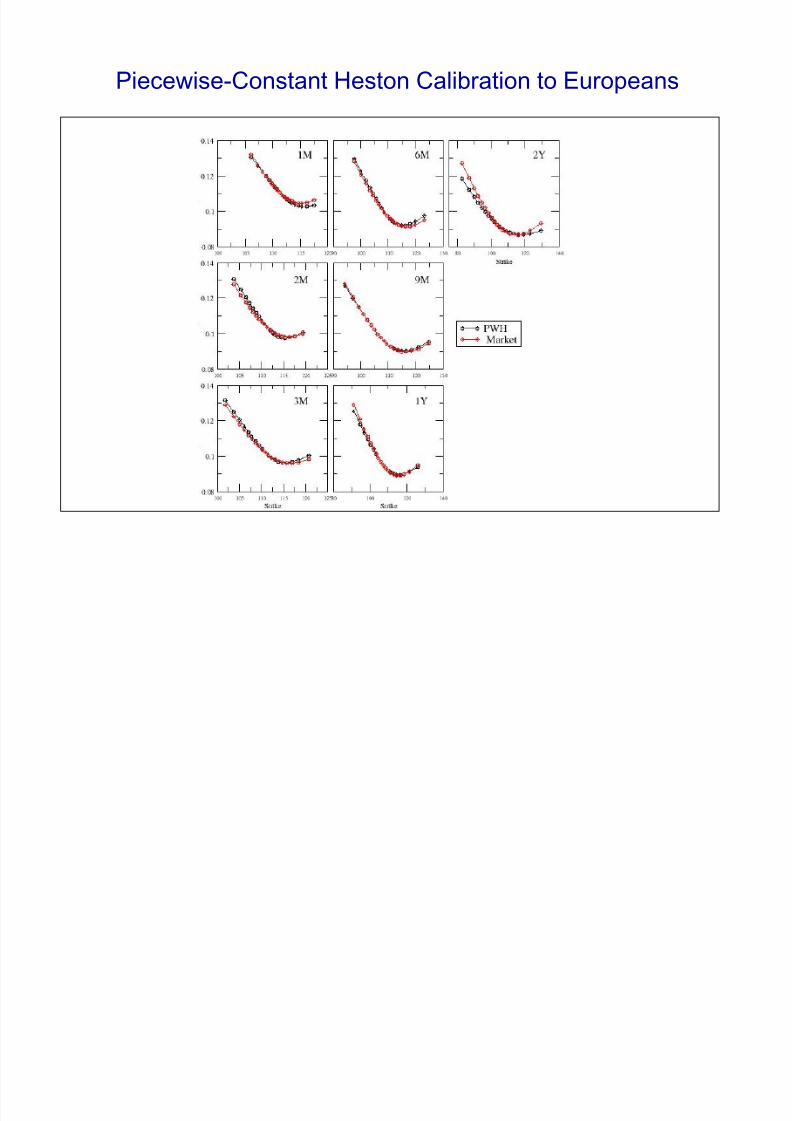

Local Volatility Calibration to Europeans

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 24/61

Local Volatility

• Gives exact calibration to the European volatility surface by construction

• Volatility is deterministic, not stochastic

• implies spot perfectly correlated to volatility

• Forward skew is rapidly time-decaying

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 25/61

Local Volatility Smile Dynamics

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

75 85 95 105 115 125Strike

I m p l i e d V o l a t

i l i t y

Original

Shifted

ΔS

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 26/61

Heston Model

• Heston process

• Five time-homogenous parameters

• Will not go to zero if

• Pseudo-analytic pricing of Europeans

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 27/61

Heston Characteristic Function

• Pricing of European options

• Fourier inversion

• Characteristic function form

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 28/61

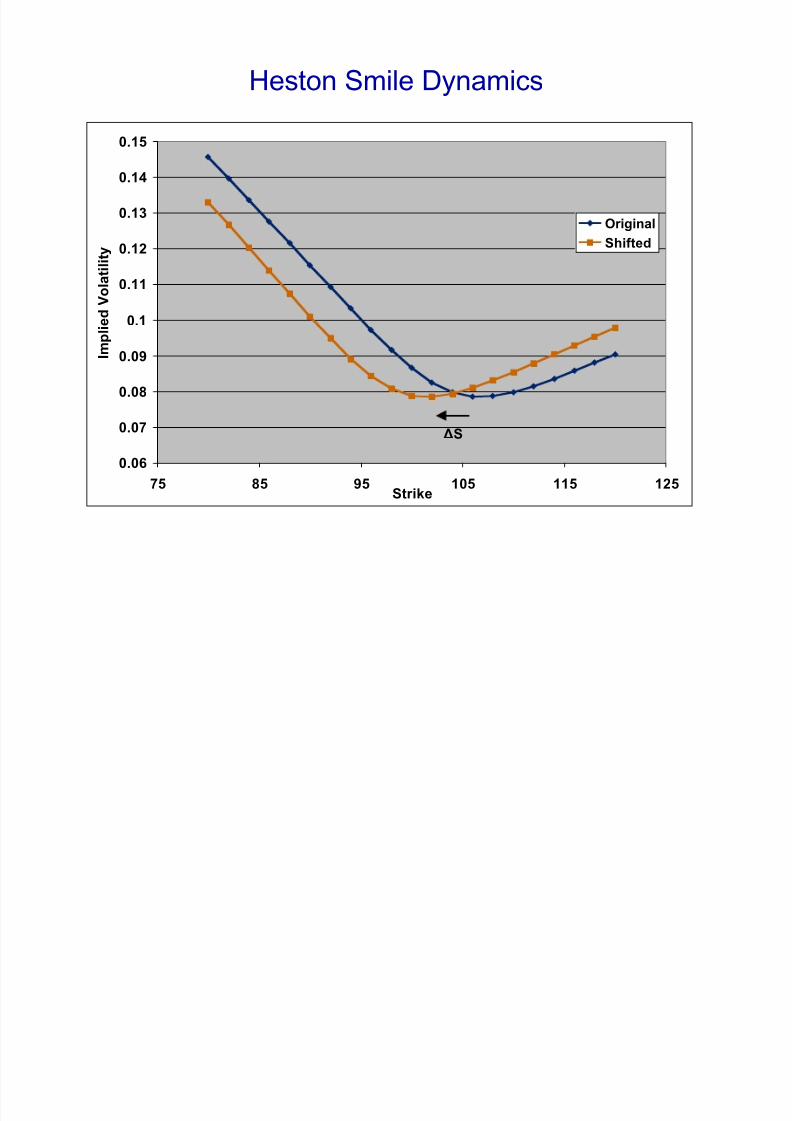

Heston Smile Dynamics

0.06

0.07

0.08

0.09

0.1

0.11

0.12

0.13

0.14

0.15

75 85 95 105 115 125Strike

I m p l i e d V o l a

t i l i t y

Original

Shifted

ΔS

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 29/61

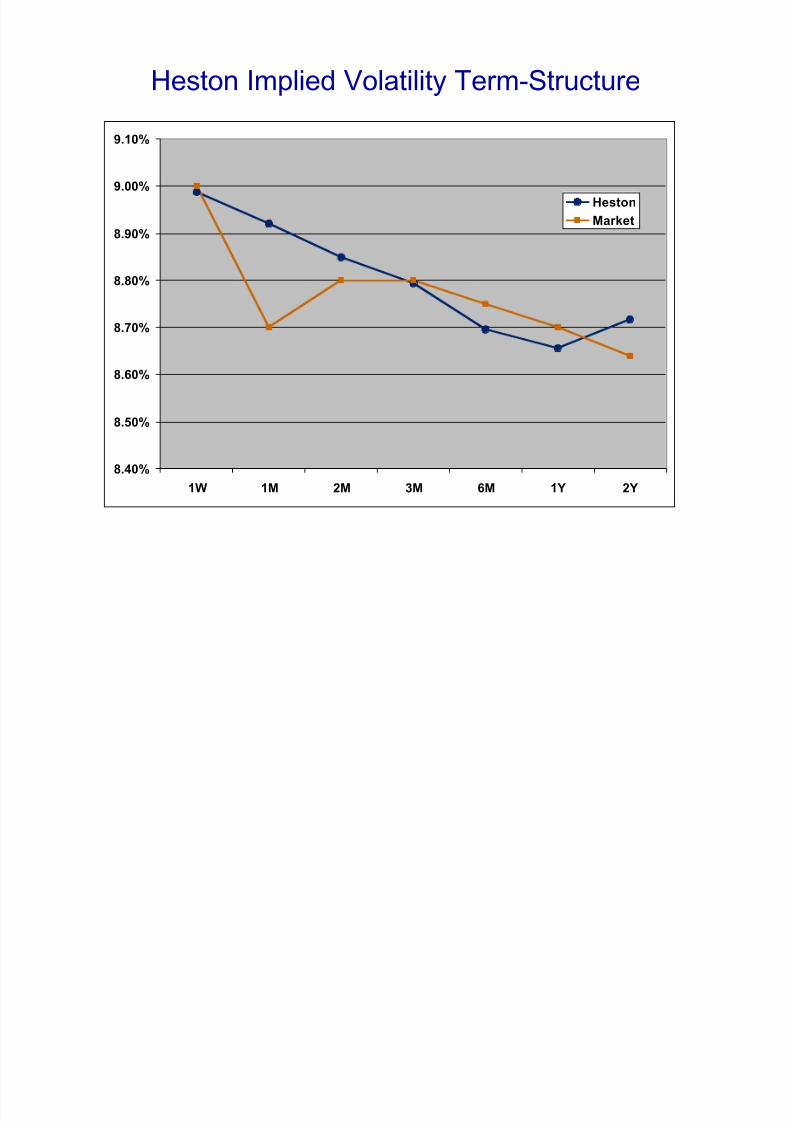

Heston Implied Volatility Term-Structure

8.40%

8.50%

8.60%

8.70%

8.80%

8.90%

9.00%

9.10%

1W 1M 2M 3M 6M 1Y 2Y

Heston

Market

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 30/61

Implied Volatility Term Structures

6

6.5

7

7.5

8

8.5

9

1W 1M 2M 3M 6M 1Y 2Y 3Y 4Y 5Y

USDJPY

EURUSD

AUDJPY

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 31/61

Piecewise-Constant Heston Model

• Process

• Form of reversion level

• Calibrate reversion level to ATM volatility term-structure

time0 1W 1M 3M2M

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 32/61

Piecewise-Constant Heston Characteristic Function

• Characteristic function

• Functions satisfy following ODEs (see Mikhailov and Nogel)

• and independent of

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 33/61

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 34/61

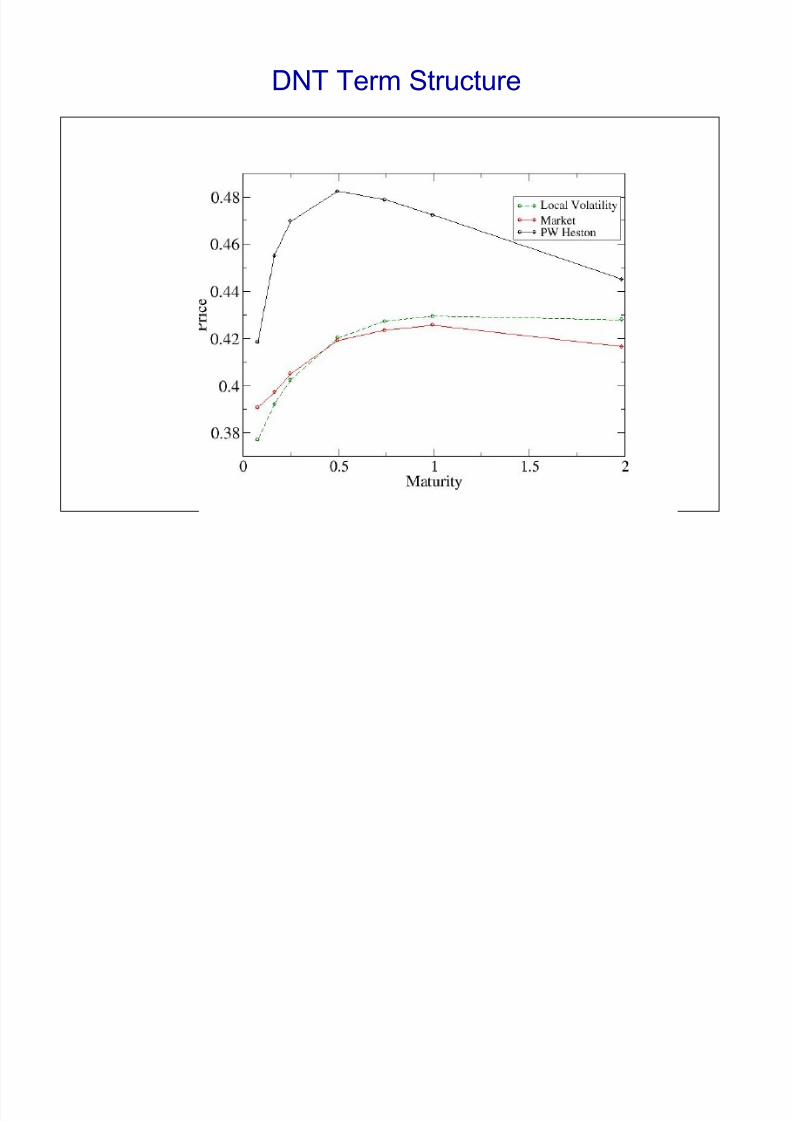

DNT Term Structure

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 35/61

Stochastic Volatility/Local Volatility

• Possible to combine the effects of stochastic volatility and local volatility

• Usually parameterise the local volatility multiplier, eg Blacher

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 36/61

Stochastic Risk-Reversals

• USDJPY 6 month 25-delta risk-reversals

USDJPY (JPY call) 6M 25 Delta Risk Reversal

Ri s k R ev er s al

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

0 8 N ov 0 4

2 1 N ov 0 5

2 6 N ov 0 6

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 37/61

Stochastic Correlation Model

• Introduce stochastic correlation explicitly but what process to use?

• Process has to have certain characteristics:

‒ Has to be bound between +1 and -1

‒ Should be mean-reverting

• Jacobi process

• Conditions for not breaching bounds

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 38/61

Stochastic Correlation Model

• Transform Jacobi process using

• Leads to process for correlation

• Conditions

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 39/61

Stochastic Correlation Model

• Use the stochastic correlation process with Heston volatility process

• Correlation structure

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 40/61

Stochastic Correlation Calibration to Europeans and DNTs

Loss Function : 14.3

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 41/61

Stochastic Correlation Calibration to Europeans and DNTs

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 42/61

Multi-Scale Volatility Processes

• Market seems to display more than one volatility process in its underlying

dynamics

• In particular, two time-scales, one fast and one slow

• Models put forward where there exist multiple time-scales over which volatility

reverts

• For example, have volatility mean-revert quickly to a level which itself is

slowly mean-reverting (Balland)

• Can also have two independent mean-reverting volatility processes with

different reversion rates

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 43/61

Double-Heston Model

• Double-Heston process

• Correlation structure

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 44/61

Double-Heston Model

• Stochastic volatility-of-volatility

• Stochastic correlation

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 45/61

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 46/61

Double-Heston Parameters

• Two distinct volatility processes

‒ One is slow mean-reverting to a high volatility ‒ Other is fast mean-reverting to a low volatility

‒ Critically, correlation parameters are both high in magnitude and of

opposite signs

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 47/61

Double-Heston Calibration to Europeans and DNTs

Loss Function : 4.30

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 48/61

Double-Heston Calibration to Europeans and DNTs

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 49/61

One-Touches

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 50/61

One-Touches

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 51/61

Variance Swaps

o Product Definition

o Process Definitions

o Variance Swap Term-Structure

o Model Implied Term-Structures

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 52/61

Variance Swap Definition

• Quadratic variation

• Variance swap price

• Price process

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 53/61

Variance Process Definitions

• Define the forward variance

• Define the short variance process

• We already have models for describing

‒ Heston

‒ Double-Heston ‒ Double Mean-Reverting Heston (Buehler)

‒ Black-Scholes

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 54/61

Variance Swap Term Structure

• Heston form for variance swap term structure

• Double-Heston

• Note the independence of the variance swap term-structure to the correlationand volatility-of-volatility parameters

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 55/61

Double-Heston Term Structures

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 56/61

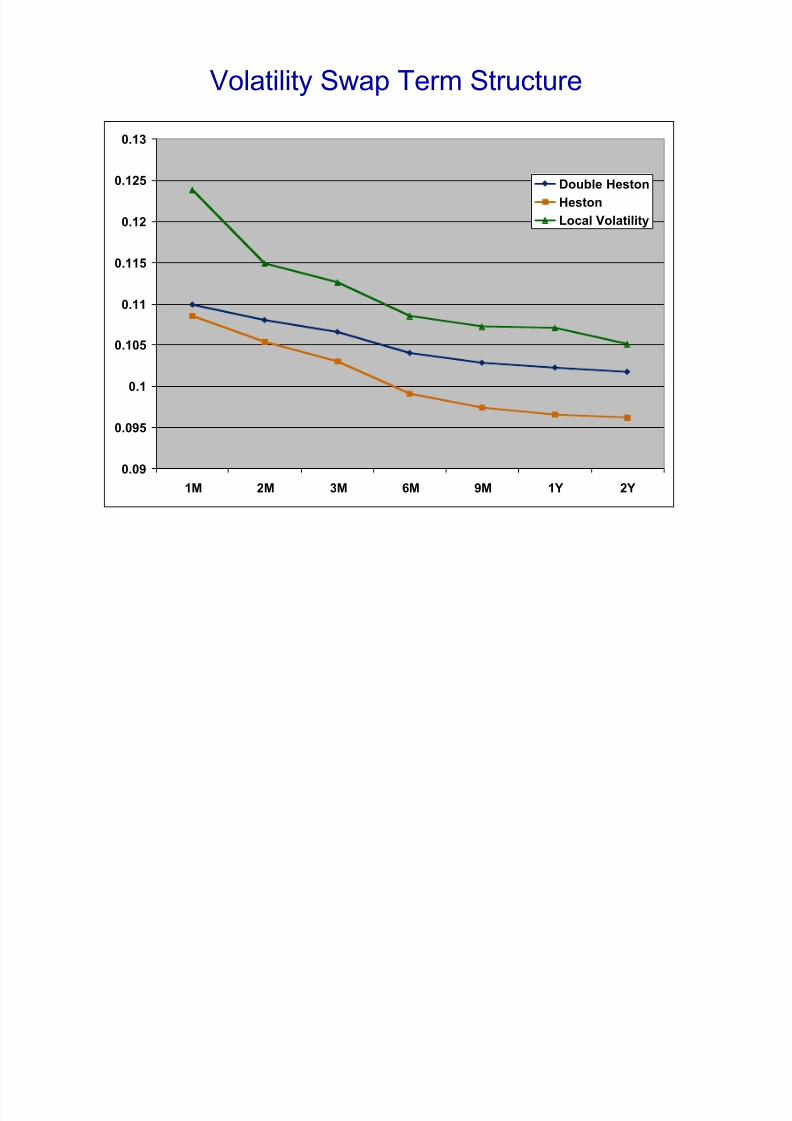

Volatility Swap Term Structure

0.09

0.095

0.1

0.105

0.11

0.115

0.12

0.125

0.13

1M 2M 3M 6M 9M 1Y 2Y

Double Heston

Heston

Local Volatility

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 57/61

Extensions

o Stochastic Interest Rates

o Multi-Heston

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 58/61

Stochastic Interest Rates

• Long-dated FX products are exposed to interest rate risk

• Need a dual-currency model which preserves smile features of FX vanillas

• Andreasens four-factor model

‒ Hull-White process for each short rate

‒ Heston stochastic volatility for FX rate ‒ Short rates uncorrelated to Heston volatility process

‒ Pseudo-analytic pricing of Europeans

‒ Can incorporate Double-Heston process for volatility and maintain rapid

calibration to vanillas

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 59/61

Multi-Heston Process

• Can always extend Double-Heston to Multi-Heston with any number of

uncorrelated Heston processes

• Maintain pseudo-analytic European pricing

• In fact, using three Heston processes does not significantly improve on the

Double-Heston fits to Europeans and DNTs

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 60/61

Summary

• FX markets exhibit certain properties such as stochastic risk-reversals and

multiple modes of volatility reversion

• Barrier products show liquidity - especially DNTs - and their prices are linked

to the forward smile

• The Double-Heston model captures the features of the market and recoversEuropeans and DNTs through calibration

• It also prices One-Touches to within bid/offer spread of SV/LV and exhibits

the required flexibility for modelling the variance swap curve

• Advantages are that it is relatively simple model with pseudo-analyticEuropean prices, and barrier products can be priced on a grid

8/8/2019 FXSkew2

http://slidepdf.com/reader/full/fxskew2 61/61

References

• D. Bates : Post-87 Crash Fears in S&P 500 Futures Options, National Bureau of

Economic Research, Working Paper 5894, 1997• S. Heston : A Closed-Form Solution for Options with Stochastic Volatility with

Applications to Bond and Currency Options, Review of Financial Studies, 1993

• H. Buehler : Volatility Markets ‒ Consistent Modelling, Hedging and PracticalImplementation, PhD Thesis, 2006

• M. Joshi : The Concepts and Practice of Mathematical Finance, Cambridge, 2003

• J. Andreasen : Closed Form Pricing of FX Options under Stochastic Rates andVolatility, ICBI, May 2006

• P. Balland : Forward Smile, ICBI, May 2006• S. Mikhailov and U. Nogel : Hestons Stochastic Volatility, Model Implementation,

Calibration and Some Extensions, Wilmott, 2005

• A. Chebanier : Skew Dynamics in FX, QuantCongress, 2006

• P. Carr and L. Wu : Stochastic Skew in Currency Options, 2004

• P. Hagan, D. Kumar, A. Lesniewski and D. Woodward : Managing Smile Risk,Wilmott, 2002

• J. Gatheral : A Parsimonious Arbitrage-Free Implied Volatility Parameterization with

Application the Valuation of Volatility Derivatives, Global Derivatives & RiskManagement, 2004

• [email protected], [email protected]

• www.quarchome.org

Top Related