![mRrj izns'k izks&iqvj i;ZVu fodkl ifj;kstuk · lgHkkxh lEHkkfor i;kZoj.kh;] lkekftd rFkk lk¡Ld`frd vk'kadkvksa ,oa ifj;kstuk ds dqizHkkok dk irk yxkdj ifj;kstuk dh lajpuk ls fØ;kUo;u](https://static.fdocuments.us/doc/165x107/5ba9ecb909d3f2cf6d8b57d9/mrrj-iznsk-izksiqvj-izvu-fodkl-ifjkstuk-lghkkxh-lehkkfor-ikzojkh-lkekftd.jpg)

Languages

Pages

Legal

CORPORATE PLAN 2017-26

Kolkata Airport

fuxfer ;kstuk

AIRPORTS AUTHORITY OF INDIAHkkjrh; foekuiŸku izkf/kdj.k

AAI's Vision till 2026 is:

“To be the principal aviation services provider in the country, AAI shall

adopt and facilitate the use of contemporary air navigation services;

upgrade and develop airport infrastructure;

support improving air connectivity at unserved and under-served airports;

have a restructured organization;

focusonprofitableoperationsatmajorairportsthroughcontinuing efforts on cost reduction and enhancing non-aeronautical revenue.”

2026 rd Hkkfoçk dk /;s; ns'k esa foeku lsok,a miyC/k djkus gsrq çeq[k lsok çnkrk cuuk gS vkSj blds fy, Hkk-fo-çk- fuEufyf[kr dk;Z djsxk%&

foeku fnDpkyu dh ledkyhu lsokvksa ds ç;ksx dks viukuk ,oa mls lqxe cukuk(

gokbZvM~Mksa ls lacaf/kr cqfu;knh lqfo/kkvksa dks mUur djuk rFkk mudk fodkl djuk(

mi;ksx esa u yk, tk jgs rFkk de mi;ksx esa yk, tk jgs gokbZvM~Mksa ij foekuksa dk çpkyu c<+kus gsrq lgk;rk çnku djuk(

laxBu dh iqulaZjpuk(

ykxr esa deh ykus ,oa xSj&oSekfud jktLo dks c<+kus ds fy, fujarj ç;kl djrs gq, bl vksj /;ku dsafær djuk fd çeq[k gokbZvM~Mksa ij çpkyuksa ls ykHk çkIr gksA

mR—"V] lqjf{kr vkSj xzkgd vuqdwy gokbZvM~Mk ,oa foeku fnDpkyu lsok,¡ miyC/k djkrs gq, Hkkjr ds LFkkbZ foekuu usVodZ dh cqfu;kn cuuk vkSj mlds ek/;e ls mu {ks=ksa esa vkfFkZd of̀) ds fy, mRçsjd ds :i esa dk;Z djuk] tg‚a ge lsok,aW çnku djrs gSa A

“To be the foundation of an enduring Indian aviation network, providing high quality, safe and customer-oriented airport and air navigation services, thereby acting as a catalyst for economic growth in the areas we serve”.

MISSION

VISION

mís';

/;s;

AAI Corporate Plan 2017-264

ContentsForeword by Chairman, AAI 12Preface by Member Planning, AAI 14

1. Introduction 171.1. Background 171.2. Corporate Plan 2017-26: The Context 171.3. Objective and Approach 181.4. This Document 192. Internal Assessment 212.1. AAI’s Mandate and Services Provided 212.2. Resource Assessment 262.3. AAI’s Performance 312.4. Summary of Internal Assessment 393. External Assessment 413.1 PEST Framework 413.2. Summary of External Assessment 534. Market Assessment 554.1. Existing Market Constituents 564.2. Allied Services 684.3. Understanding and Managing Customer Expectations 775. SWOT Analysis 815.1. Key Strengths 815.2. Key Weaknesses 835.3. Major Opportunities 845.4. Major Threats 855.5. Summarizing the SWOT 866. Setting the Vision and Mission 896.1. Setting the Mission Statement 896.2. Setting the Vision Statement 907. Corporate Agenda: Priorities, Action Areas and Strategies 957.1. Introduction 957.2. Framework 957.3. Priorities for AAI 967.4. Action Areas for the Plan Period 997.5. Strategies 1008. Corporate Plan Monitoring and Review 1198.1. Corporate Plan Monitoring and Review 1198.2. Summary 123

AAI Corporate Plan 2017-26 5

List of ExhibitsExhibit 1: Overarching framework for preparation of Corporate Plan for AAI 19Exhibit 2: Framework for conducting internal assessment 21Exhibit 3: AAI's Mandate and Services being offered 22Exhibit 4: AAI initiatives to modernize air traffic services in India 25Exhibit 5: City-side developments to be undertaken by AAI (under DPR stage) 27Exhibit 6: Airports under AAI: operational vs. non-operational 27Exhibit 7: Average terminal capacity utilization for AAI and other airports 28Exhibit 8: Organizational pyramid, AAI 29Exhibit 9: Organizational structure for AAI 30Exhibit 10: Revenue sources for AAI 32Exhibit 11: Revenue mix for AAI (2008-16) 33Exhibit 12: Composition of expenses (2008-16) 33Exhibit 13: Expected funding sources for proposed capital expenditure over 2016-20 34Exhibit 14: Contribution to PBT by profitable airports under AAI in 2015-16 35Exhibit 15: Growth trend of passenger traffic in India 36Exhibit 16: Airports operating beyond capacity 37Exhibit 17: PEST framework for external assessment 41Exhibit 18: Implications of the NCAP, 2016, for AAI 43Exhibit 19: Unutilized / Under-utilized AAI airports 44Exhibit 20: Growth in domestic air passenger traffic and India’s economy 47Exhibit 21: Projected growth in key drivers of air passenger growth 49Exhibit 22: Framework for internal assessment 55Exhibit 23: Approach to market analysis 56Exhibit 24: Growth of passenger traffic in India 57Exhibit 25: Growth of domestic and international traffic 58Exhibit 26: Correlation between growth of domestic traffic and GDP 59Exhibit 27: Passenger growth forecast 60Exhibit 28: Additional capacity and investment requirement 61Exhibit 29: Evolution of airport ownership in India 62Exhibit 30: Traffic distribution between AAI and PPP airports 63Exhibit 31: International and Domestic cargo growth 64Exhibit 32: International and Domestic cargo growth 65Exhibit 33: Sector wise growth in air cargo 66Exhibit 34: NTDPC forecast for cargo infrastructure growth 67Exhibit 35: Potential disciplines for international consulting for AAI 69

AAI Corporate Plan 2017-266

Exhibit 36: Assessment for international consulting business 71Exhibit 37: Airports with MRO facilities 72Exhibit 38: Evolution of Ground Handling policy in India 74Exhibit 39: Porter's assessment for ground handling business 75Exhibit 40: Assessment for in-flight catering business 77Exhibit 41: Land available at select airports 82Exhibit 42: Comparison of non-aeronautical revenues of AAI with a comparable private

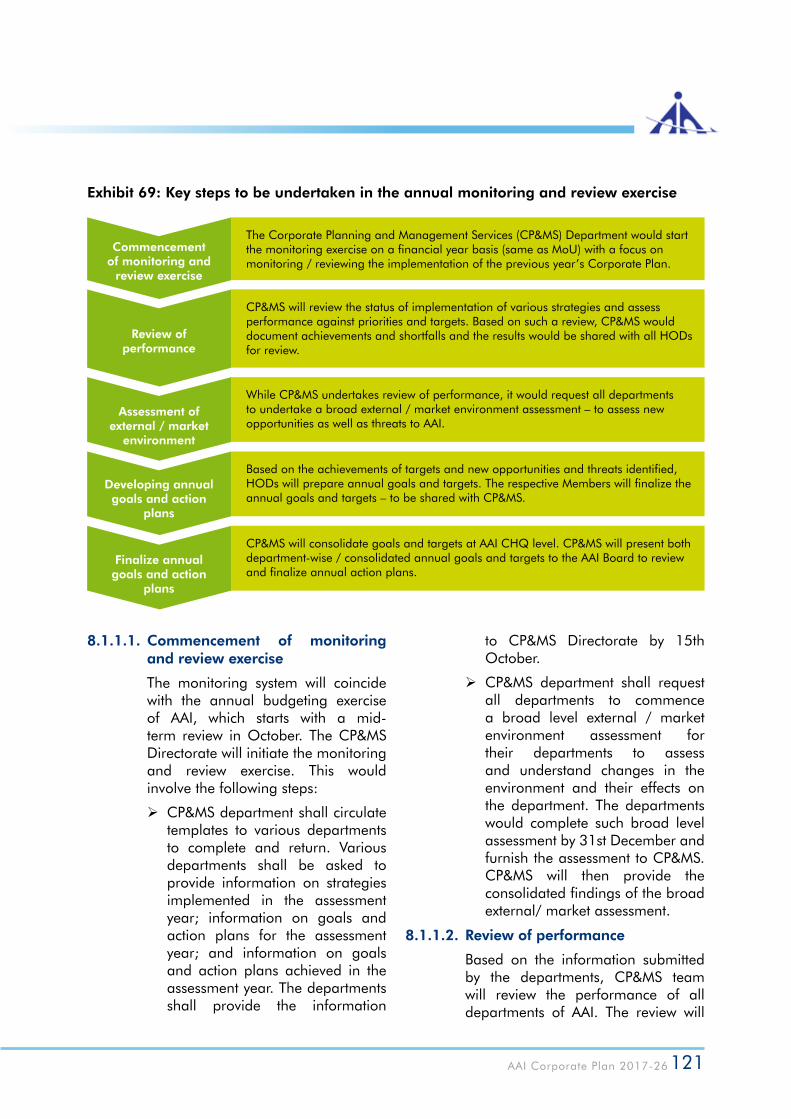

airport 83Exhibit 43: Summary of SWOT analysis for AAI 87Exhibit 44: Framework of review mechanism 89Exhibit 45: Framework for preparation identifying vision statements 91Exhibit 46: Key inputs for vision 92Exhibit 47: Framework for setting priorities 95Exhibit 48: Action Plans for the plan period 99Exhibit 49: Phases for implementation of ATFM 100Exhibit 50: Approach for infrastructure planning 101Exhibit 51: Focus on airport marketing 102Exhibit 52: Usage of social media by airports 103Exhibit 53: Potential Social Media Platforms for AAI 104Exhibit 54: Strategy on new greenfield airports 105Exhibit 55: Development Models for Fuel Farms 107Exhibit 56: Approach to provide value added services 108Exhibit 57: Options to improve energy efficiency 109Exhibit 58: Strategies to develop green airports 110Exhibit 59: Strategies/Plan for SMS implementation level 3-4 111Exhibit 60: Strategies to increase non-aeronautical revenue from terminals 112Exhibit 61: Strategy for city-side development 113Exhibit 62: Potential development options to be assessed 114Exhibit 63: Possible development models 114Exhibit 64: Three step approach to MRO business 115Exhibit 65: Examples of MRO business (Representative list) 116Exhibit 66: Modes of entering international consulting business 116Exhibit 67: Strategy for brand building 117Exhibit 68: Corporate Planning Monitoring and Review framework 120Exhibit 69: Key steps to be undertaken in the annual monitoring and review exercise 121Exhibit 70: Steps for revising strategies by AAI 123

AAI Corporate Plan 2017-26 7

List of AnnexuresAnnexure 1: List of expansion works planned by AAI 125Annexure 2: Cargo handling capacity and volume handled by AAI airports 130Annexure 3: Airports selected for City side development 131Annexure 4: Stakeholder consultation 132Annexure 5: Questionnaires used for feedback on Mission and Vision statements 133Annexure 6: Vision statements of international airports 134Annexure 7: Action plans provided by select Directorates of AAI 135Annexure 8: Potential coverage of MIS for AAI 145Annexure 9: City side development by international airports 146

AAI Corporate Plan 2017-268

List of AbbreviationsAbbreviations Expansions

AAI Airports Authority of IndiaAAICLAS AAI Cargo Logistics and Allied Services Company LtdACI Airports Council InternationalACLPB Air Cargo Logistics Promotion BoardACS Air Cargo Community SystemADS Automatic Dependent SurveillanceADS-B Automatic Dependence Surveillance – BroadcastAEO Authorized Economic OperatorAERA Airports Economic Regulatory Authority of IndiaAIATSL Air India Air Transport Services LimitedAIESL Air India Engineering Services LimitedAIMS Airport Information Management SystemAISATS Air India SATS Airport Services Private LimitedANSP Air Navigation Service ProviderANS Air Navigation ServicesAOCC Airport Operation Control CentreAODB Airport Operational Data Base (AODB)ASBU Aviation System Block UpgradesASEAN Association of Southeast Asian NationsASMGCS Advanced Surface Movement Ground Control SystemsASQ Airport Service QualityATC Air Traffic ControlATF Aviation Turbine FuelATFM Air Traffic Flow Management SystemATFMSG Air Traffic Flow Management Steering GroupATM Air Traffic ManagementATS Air Traffic ServicesAVSEC Aviation SecurityBCAS Bureau of Civil Aviation SecurityBIAL Bangalore International Airport LimitedBSF Border Security ForcesCAG Changi Airport GroupCAGR Compound Annual Growth RateCAPA Centre for Asia Pacific Aviation

AAI Corporate Plan 2017-26 9

C-ATFM Centralized Air Traffic Flow ManagementCATC Civil Aviation Training CollegeCBP Customs and Border ProtectionCE Civil EnclaveCHQ Central HeadquartersCNS Communications, Navigation and SurveillanceCP & MS Corporate Planning & Management ServicesCPC Centre for Perishable CargoCSI Customer Satisfaction IndexCUDCT Common User Domestic Air Cargo TerminalsDAEP Dubai Aviation Engineering ProjectsDGCA Directorate General of Civil Aviation of IndiaDIAL Delhi International Airport LimitedDPR Detailed Project Report DRDO Defence Research and Development OrganisationDVOR Doppler VHF Omni Directional RangeECIL Electronics Corporation of India LimitedE & M Electrical & MechanicalEPoS Electronic Point of SaleF & B Food and BeverageFIDS Flight Information Display SystemFIU Flight Inspection UnitFTC Fire Training CollegeFSC Full Service CarrierGoI Government of IndiaGAGAN GPS Aided GEO Augmented NavigationGBAS Ground-Based Augmentation SystemGDP Gross Domestic ProductGH Ground HandlingGHA Ground Handling AgenciesGHIAL GMR Hyderabad International Airport LimitedGRIHA Green Rating for Integrated Habitat AssessmentG2G Government – to – GovernmentHOD Heads of DepartmentHR Human ResourcesIAA Indian Aviation AcademyIAAI International Airports Authority of IndiaIAF Indian Airforce

AAI Corporate Plan 2017-2610

IATA International Air Transport AssociationIBEF India Brand Equity FoundationICAO International Civil Aviation OrganizationIFS Instant Feedback SystemILS Instrument Landing SystemIMF International Monetary FundINR Indian RupeeINSPIRE Indian Ocean Strategic Partnership to Reduce EmissionsIP Internet ProtocolISMS Information Security Management SystemISRO Indian Space Research OrganisationI.T Information TechnologyJV Joint VentureJVC Joint Venture CompanyKPI Key performance IndicatorsLCC Low Cost CarrierLED Light Emitting DiodeMAG Minimum Annual Guarantee MGAE MAS GMR Aerospace Engineering Company LimitedMGAT MAS - GMR Aero Technic LtdMIAL Mumbai International Airport LimitedMIS Management Information SystemMMT Million Metric TonneMoCA Ministry of Civil AviationMoEF Ministry of Environment and ForestsMoU Memorandum of UnderstandingMPPA Million Passengers Per AnnumMRO Maintenance and Repair OrganizationsMT Metric TonnesNAA National Airports AuthorityNCAP National Civil Aviation PolicyNOCAS No Objection Certificate Application SystemNTDPC National Transport Development Policy CommitteeOECD Organisation for Economic Co-operation and DevelopmentO & M Operations and ManagementPBN Performance Based NavigationPBT Profit Before TaxPEST Political, Economic, Social and Technological

AAI Corporate Plan 2017-26 11

PPP Public Private PartnershipsPMC Project management consultancyRBI Reserve Bank of IndiaRCS Regional Connectivity SchemeR&D Research and DevelopmentRFID Radio Frequency IdentificationRNFC Route Navigation Facilities ChargesSAARC South Asian Association for Regional CooperationSATCOM Satellite CommunicationsSARP Standards, Recommended Practices and ProceduresSBAS Satellite based Augmentation SystemSCA Scheduled Commuter AirlinesSEZ Special Economic ZoneSID Standard Instrument DeparturesSMS Safety Management SystemSOW Statement of WorkSPV Special Purpose VehicleSRM Safety Risk ManagementSSP State Safety ProgrammeSTAR Standard Terminal Arrival RoutesSWOT Strength, Weakness, Opportunity, ThreatTMI Traffic Management InitiativesTNLC Terminal Navigational Landing ChargesUAE United Arab EmiratesUN United NationsUSD US DollarVFR Visual Flight RulesVHF Very High Frequency

AAI Corporate Plan 2017-2612

Foreword by Chairman, AAI

I’m pleased to provide some introductory thoughts to this document, which arrives at an important turning point in history of Indian Aviation, especially at a time when Government of India has released the new National Civil Aviation Policy 2016 (NCAP), as also, when India is going through a phase of high economic growth and is poised to be the 3rd largest aviation market in the world in near future.

In today’s world, airports are operating in a competitive environment and it has become critical to adjust its business strategies inthe ever-evolving aviation scenario to ensure sustainable growth in the future. Airports Authority of India (AAI) is very conscious of its responsibilities and is making sincere endeavour to sustain and propel the growth story in the aviation sector, which is experiencing drastic changes since the recent past. While AAI’s traditional businesses are growing at a healthy rate, there is potential for AAI to foray into new businesses and new markets which complement the existing businesses. International aviation business fosters rapid growth to meet huge demands of relatively higher standards. As such, organisations are pushed to expand and invest in the best tools and technologies to keep up, and Corporate Planning is one such tool. Corporate Plan is of

paramount importance to an organization as it dictates the shared philosophy, practices and culture of an organization and its employees. An organization without a system of a Corporate Plan is often regarded as a body without a soul or conscience. Deciding which type of Corporate Plan is the best for any organisation can be a challenging task.

Since its inception in 1995, AAI has been already participating in globally accepted benchmarking programmes to assess our own standing and understand the areas for improvement in future. It is in this context that AAI has undertaken the preparation of this Corporate Plan document to communicate with its stakeholders. This Corporate Plan, developed for the period 2017 to 2026 is in

AAI Corporate Plan 2017-26 13

harmony with the NCAP and presents the Vision and Mission statements that AAI envisages for itself along with the targets and strategies to meet them during the next 10 years. The Corporate Plan of AAI is a strategic plan, which places greater emphasis on using internal resources and streamlining operations to achieve expected goals. It has been structured by first introducing a grand overall vision ofgrowth and development, then laying out a plan of action on a microscopic level to meet its end goal. It consists of a vision statement, mission statement, strength, weakness, opportunity, threat (SWOT) analysis, market assessment, identifying available resources and then listing objectives and strategies to be used tomeetthoseobjectives

OurCorporatePlan isambitious. Itdefineshow we will be successful within a challenging and changing aviation environment. The plan has been devised to enrich the experience of our stakeholders, and has been developed with their involvement and support through an extensive consultation programme that has also engaged with our internal and external stakeholders, as also, influencers. AAI has exciting aspirations as it moves into a new era of development. This plan, which will guide our workoverthenextfewyears,capturesfivekeypriorities – NCAP, RCS, AAICLAS, UAH & MRO that will enhance our reputation and position on a global platform. Our culture of support andcollaborationwillbenefitthecommunitiesin which we operate and address global challenges. This document is only the start of

the strategic planning process. Throughout the next few months, we will engage to specify the detail of the projectwork thatwill deliver ourvision and feed into an operating plan. We will ensure that we have appropriate supporting strategies for each of our priorities. We will review our plan on an annual basis to ensure that we respond appropriately to external and internal drivers. Our performance is on an upwardtrajectoryandwehaveinvestedinbothcurrent and future research leaders to continue improvement. We want to position ourselves as one of the leading global air service provider in afiercelycompetitiveenvironment.

While concentrating on development, AAI is committed to ensure safety, security and sustainability. Several measures have been adopted and strategies deployed which have a greater probability of success as the same is based on a better understanding of the direction the economy will take. This Corporate Plan brings together in one document the key work which Airports Authority will be doing in the next 10 years in meeting stakeholders’ expectations and making air travel a delight for passengers.

I would like to thank all my fellow Board Members and colleagues, as also, Deloitte Touche Tohmatsu India LLP for their persistent effortsinfinalizingtheCorporatePlandocument.

Dr. Guruprasad Mohapatra, IASChairman, AAI

AAI Corporate Plan 2017-2614

Preface by Member Planning, AAI

The corporate plan of Airports Authority of India (AAI) for the period from 2017 to 2026 has taken its shape at the right time, when our prestigious organisation is blossoming, with the scope to excel in its current scheme of functioning. The coherent latitude is seconded earnestly by tremendous growth in Civil Aviation Sector in India, with the combination of ever increasing traffic demand, mainstay support from theGovernment of India and concentrated efforts of the stakeholders. At the national level, aviation business has been amajor driver ofgrowth and development in the last 10 years. Civil aviation industry has ushered into an era of expansion and connectivity driven by factors such as Low Cost Careers, modern airports, Foreign Direct Investment (FDI), advanced Information Technology interventions with growing emphasis on regional connectivity, as part of New Civil Aviation Policy (NCAP)-2016.

As a responsible industry stakeholder, AAI is engaging & collaborating with policy makers to implement the various policies of the Government efficiently, with an objectiveto boost India's civil aviation sector. In this currenttransformationalphase,clearlydefinedstrategic action plans, optimal utilisation of internal resources, streamlined operations and performance evaluation parameters are the definite ways to achieve the envisaged goalsover short, medium & long term.

I am happy to present the "Corporate Plan" of AAI on behalf of our Corporate planning & Management Services Department. The plan which would be supporting the NCAP provides for special focus on resource assessments (both internal and external) and market

For an organisation to be competitive, it needs to achieve goals;To achieve its goals, we need strategic plans

AAI Corporate Plan 2017-26 15

assessment.Abriefintroductoryofthesubjectarea of Corporate Plan is provided with SWOT analysis on the strengths and opportunities which may go in favour of implementation of Corporate Plan vis-à-vis the probable key weaknesses and major threats, which mightprove to be challenging. The plan also analyses dimensions involving current & future issues and primary determinants of evaluating performance in a comprehensive way, relating to various steps for realizing the Corporate Plan.Theplanalsoclearlydefinesthespecificaction stages that must be taken-up to achieve thedesiredobjectivesandwhichcan,aswellbeused as markers to check on a periodic basis todeterminewhetherornotsufficientprogressis being made. The objectives set forth areflexible allowing for mid-course amendments and adjustments as the time progresses, sothatwelearnfromourfirstsuchproactiveandqualitative step.

I must appreciate the enormous efforts put in, both by my colleagues in AAI and by M/s. Deloitte TT India, in framing the modalities, in surveying applicable action areas for the Plan period and in bringing out a workable formulation and implementation of policies. I also take this opportunity to thank the Chairman, AAI and the Board Members for their guidance and help, from time to time, in completing the Corporate Plan.

Now in executing the Corporate Plan, we have to identify issues that surround the key question as to who manages and monitors the Plan and how the plan is communicated

and supported and how committed are we in implementing the plan to take our organisation forward. I am happy that we are moving in a positive direction to make this Plan a success, teaming-upinanefficientmannerinachievingthe common goal of 'excellence'

S.RahejaMember (Planning)

Chennai Airport

Amritsar Airport

AAI Corporate Plan 2017-26 17

1. Introduction1.1. Background

The Airports Authority of India (AAI) was constituted by an Act of Parliament and came into being on 1st April 1995 by merging the erstwhile National Airports Authority (NAA) and International Airports Authority of India (IAAI). The merger brought into existence a single organization entrusted with the responsibility for creating, upgrading, maintaining, and managing civil aviation infrastructure both on the ground and in air space in the country.

AAI manages 125 airports, which include 21 international airports (3 civil enclaves), 8 customs airports (4 civil enclaves), 77 domestic airports, and 19 domestic civil enclaves at defence airfields and provides air navigation services for over 2.8 million square nautical miles of air space. In terms of administrative control, AAI has divided its airports under five regions, namely Northern, Eastern, Western, Southern and the North-East.

AAI’s functions are as follows1: ¾ Design, development, operation and maintenance of international and domestic airports and civil enclaves.

¾ Construction, modification and management of passenger terminals.

¾ Development and management of cargo terminals at international and domestic airports.

¾ Provision of passenger facilities and information systems at the passenger terminals at airports.

¾ Expansion and strengthening of operational areas, viz., runways, aprons, taxiway, etc.

¾ Control and management of the

Indian airspace extending beyond the territorial limits of the country, as accepted by International Civil Aviation Organization (ICAO).

¾ Provision of visual aids. ¾ Provision of communication and navigation aids, viz., instrument landing system (ILS), doppler VHF omni directional range (DVOR), radar etc.

1.2. Corporate Plan 2017-26: The Context

As mentioned above, since its inception in 1995, the Airports Authority of India (AAI) has been at the helm of affairs in the development of airport infrastructure and management and control of airport operations and air navigation services in India. Over the past two decades, AAI has been at the forefront of modernizing and developing airside & terminal side infrastructure, air navigation services, and improving its services at airports to deliver a better travel experience to passengers. These measures have resulted in improved air safety and passenger satisfaction as is reflected in passenger experience survey results.

There have been remarkable changes in the Indian aviation sector since the inception of the AAI. Various policy measures in the late 1990s, such as the repeal of the Air Corporation Act, Open Skies Policy & and the promotion of foreign direct investment in aviation and airport infrastructure allowed the flow of private investments in aviation in the form of the emergence and active participation of new airlines. Other factors such as economic growth and the influx of foreign tourists also supported

1http://www.aai.aero

AAI Corporate Plan 2017-2618

the aviation industry by keeping demand buoyant. The emergence of the low cost carrier (LCC) model, which followed an established trend in western countries, also boosted demand. Passenger traffic grew by ~2.6 times at a compound annual growth rate (CAGR) of 11.6% over the last decade, creating an acute need for further capacity development. Although the spurt in air traffic brought new opportunities for AAI, it also posed a major challenge in terms of expanding ground infrastructure and air navigation services.

The period from 2007-16 also witnessed private sector participation in airport infrastructure development and management in India, with the re-structuring of two major AAI airports at Delhi and Mumbai. Few green field airports, like at Bangalore and Hyderabad, were also developed with funding from private sector. Besides, several state governments, like those in Maharashtra, Goa, Telangana, etc., are planning to develop primary / second airports in certain cities to cater to growing air traffic. In 2008, the Airport Economic Regulatory Authority (AERA) was constituted through the Airport Economic Regulatory Authority of India Act, 2008. The Authority was given the mandate to regulate tariff and other charges for the aeronautical services rendered at major airports and also to monitor performance standards at major airports.

The Indian aviation industry is likely to face challenges arising from the rapid growth and global integration of the Indian economy and from policy and regulatory changes. In a bid to inform stakeholders within and outside the organization of its priorities and proposed future strategies over the next decade, AAI has undertaken the preparation of this Corporate Plan document.

The preparation of the Corporate Plan for the period 2017-26 involved the following:

¾ Information gathering and analyses:• Internal assessment• External &market assessment

¾ Identification of key strengths and weaknesses

¾ Review of Mission Statement and development of the Vision Statement

¾ Development of priorities, action areas and strategies

1.3. Objective and Approach

While the Corporate Plan document presents the organization’s priorities and proposed strategies as a culmination of the present exercise, management activity around Corporate Planning would need to be institutionalized in the context of a changing business environment to ensure its relevance in coming years.

Operational strategies and plans formulated for 10 years would tend to be ineffective as planning tools because they are likely to be based on present expectations of possible changes in the business environment. Institutionalizing corporate planning by setting up a separate corporate planning unit with a well-defined framework within AAI will provide insights into the organization’s strengths, weaknesses, opportunities and threats in a dynamic and rapidly changing business environment and enable AAI to plan and respond effectively.

Aligned to this requirement, a multi-tiered approach is required beginning with an assessment of environmental trends and analyses of the organization’s strengths and weaknesses, development of a statement of the organization’s mission and vision for the future, and identification of priorities and strategies to achieve the identified vision.

AAI Corporate Plan 2017-26 19

This framework is shown in Exhibit 1.

Exhibit 1: Overarching framework for preparation of Corporate Plan for AAI

A SWOT analysis and the drawing up of a vision statement takes time when done once in ten years. A periodic review should be taken at shorter intervals if there are major changes in the organization or the business environment.

AAI accordingly envisages moving away from a static corporate planning

towards adopting a dynamic planning model which can respond to the evolving Indian aviation sector.

1.4. This Document

The various sections of this Corporate Plan document address the following key areas:

Section Number Content Page Number2 Internal Assessment 213 External Assessment 414 Market Assessment 555 SWOT Analyses 816 Setting the Vision and Mission 897 Corporate Agenda: Priorities and Strategies 958 Corporate Plan Monitoring and Review 119

InternetAssessment

SWOT

Mission

Vision

Priorities & Targets

Strategies

Management Aspirations

Aspirations of other Airport Authorities

ExternalAssessment

MarketAssessment

MultipleManagementWorkshops

SeconderyResearch

Dehradun Airpot

Indore Airport

AAI Corporate Plan 2017-26 21

2. Internal AssessmentThe internal assessment undertaken as part of preparation of this Corporate Plan document has focused on three key aspects – understanding of the mandate and services delivered by AAI, analysing resources available with AAI to discharge its mandate, and analysing AAI’s performance on certain parameters. To do so, AAI has used primary data collected by

itself, data from other/secondary sources, and from interaction and consultation within the organisation and with stakeholders outside the organisation.

The focus of this assessment was to identify AAI’s potential strengths / areas of comparative advantage as well as potential weaknesses / areas of vulnerability.

Exhibit 2: Framework for conducting internal assessment

2.1. AAI’s Mandate and Services Provided

As per the provisions of the AAI Act, the gamut of services to be provided by AAI

are summarized along with the extent to which AAI is currently providing these services.

PerformanceUnder this head,

the financial and operational performance of

AAI over the past few years has been

analysed

Mandate and Services

Under this head, an assessment of the

current service portfolio has been undertaken

- airport services; ATC/CNS services; cargo

operations

ResourcesUnder this head, an

assessment of resources has been undertaken - physical resources,

manpower and organizational

resources

AAI Corporate Plan 2017-2622

Exhibit 3: AAI's Mandate and Services being offered

Mandate as per AAI Act Services being provided currently

Manage airports, civil enclaves and aeronautical communication sta-tions

Yes

Provide air traffic service and air transport service at any airport and civil enclaves

Yes

Plan, develop, construct and maintain runways, taxiways, aprons and terminals and ancillary buildings at airports and civil enclaves

Yes

Plan, procure, install and maintain navigational aids, communication equipment, beacons and ground aids at airports and at such locations as may be considered necessary for safe navigation and operation of aircraft

Yes

Provide air safety services and search and rescue facilities in co-ordina-tion with other agencies

Yes

Establish schools or institutions or centres for the training of its officers and employees in regard to any matter connected with the purposes of this Act

Yes

Construct residential buildings for its employees YesEstablish and maintain hotels, restaurants and restrooms at or near the airports

Partially – only at select airports

Establish warehouses and cargo complexes at airports for the storage or processing of goods

Partially – only at select airports

Arrange for postal, money exchange, insurance and telephone facili-ties for the use of passengers and other persons at airports and civil enclaves

Yes

Develop and provide consultancy, construction or management ser-vices, and undertake operations in India and abroad in relation to airports, air navigation services, ground aids and safety services or any facilities thereat

Yes. Consultancy has been limited in scope.

Allow for airport operations on public private partnerships (PPP) basis Yes

Source: Based on stakeholder consultations and AAI (Amendment) Act 2003

The extent and coverage of AAI’s provision of these services varies across its airports – primarily with respect to the nature of services and traffic quantum at a given airport. Therefore, while AAI provides air navigation services across all airports, its services around establishing and operating warehouses and cargo complexes are limited to certain airports.

2.1.1. Airport development, operations and management

AAI undertakes structural design of passenger and cargo terminals, aircraft hangars, runways and other pavements, technical buildings for installation of airport ground aids etc. through its Civil Engineering Department. A separate wing under the Civil Engineering Department looks after maintenance requirements

AAI Corporate Plan 2017-26 23

/ civil engineering aspects of airport operations and management. AAI also has a specialized department of electrical engineering looking after electrical and mechanical (E&M) services for airport terminal buildings and airfield lighting works.

2.1.1.1. Passenger facilities AAI is currently in the process of

expanding terminal buildings at

several existing airports, including Jaipur, Dehradun, Srinagar, Lucknow, Chennai, Vijayawada, Surat, Vadodara, etc. The list of ongoing expansion works at existing AAI airports is presented in Annexure 1 of this document. Recently, AAI appointed project management consultants to improve efficiency in development works across 14 airports.

2.1.1.2. Cargo facilities AAI has the mandate to develop

and manage air cargo terminals at international and domestic airports in India under the provisions of the AAI (Amendment) Act 2003 and Airports Authority of India (Storage and processing of Cargo, Courier and Express Goods and Postal Mail) Regulations 2003. AAI also acts as a custodian of import cargo under section 45 of Customs Act 1962. AAI has developed several common user cargo terminals both for international and domestic cargo.

AAI’s cargo business has been administered through a departmental structure within the overall AAI administration. Over the years, 115,000 sq. m of warehouse capacity was developed across the country with an estimated cargo handling capacity of 1,600,000 MT2. Depending on the size of operations, either an airport has a separate cargo department or the cargo function is managed as part of the commercial activities of the airport.

AAI currently manages3 international air cargo terminals at eight airports viz., Kolkata, Chennai, Amritsar, Guwahati, Coimbatore, Trichy, Lucknow and Mangalore and domestic cargo operations at four airports, namely Port Blair, Jaipur, Coimbatore and Lucknow. Cargo facilities at certain other airports are being managed through outsourced agencies/state government organizations on an O&M basis. AAI is also in the advanced stages of commissioning international air cargo handling facilities at Madurai and Visakhapatnam airports.

AAI had appointed a consultant to advise it on its air cargo business plan. The consultant had recommended that AAI separate its cargo department from the main organization by corporatizing the department. Based on these recommendations, AAI has decided to form a 100% AAI owned Cargo Subsidiary - AAI Cargo Logistics and Allied Services Company Limited (AAICLAS) in August 2016. AAICLAS will undertake all the activities that were previously carried

Over the years, AAI has gained significant expertise in planning, designing and developing airports. AAI has successfully completed the modernization of airports in both tier I and tier II cities. AAI’s expertise in development works have been used by other government enterprises like Air India, Bureau of Civil Aviation security (BCAS), Border Security Forces (BSF), Defence Research and Development Organisation (DRDO), etc., in the form of deposit works.

2Source: Air Cargo Business Plan for AAI, 2016 3Source: Air Cargo Business Plan for AAI, 2016

AAI Corporate Plan 2017-2624

out by the Cargo Department of AAI and it is envisioned that it will becomes the foremost integrated logistics network in India. AAICLAS would provide cargo handling and related value added services at airports in India and or abroad including ground handling services, documentation, transport services for carriage of bonded & non-bonded cargo and screening services. It will promote, represent, organize, undertake, establish, conduct, handle, arrange, own, operate, participate, facilitate, sponsor, encourage, and provide the business as Cargo Terminal Operator, Free Trade Zone, Air Freight Station and Inland container depot for cargo and passengers.

2.1.2. Air Navigation Services AAI provides air navigation services

(ANS) across all civil airports in India. AAI manages Indian air space measuring over 2.8 million square nautical miles, which includes a land area measuring 1.05 million square nautical miles and oceanic airspace measuring 1.75 million square nautical miles, extending beyond the territorial air space into the Arabian Sea, Indian Ocean and Bay of Bengal.4 Air navigation services are also provided by AAI at joint venture airports (e.g. Delhi, Mumbai, Nagpur), green field airports (e.g., Bengaluru, Hyderabad and Cochin), state government airports (e.g., Lengpui) and private airports (e.g., Mundra, and Durgapur) as per the terms and conditions of communications, navigation and surveillance (CNS)/ air traffic management (ATM) agreements between AAI and the concerned airport operators.

AAI has laid major emphasis on developing communication, navigation and surveillance (CNS) infrastructure in the country. The emphasis has been on providing reliable and efficient ground

based equipment and the adoption of satellite based communication, navigation and surveillance systems. AAI has a dedicated team to deliver the ANS and air traffic services (ATS), respectively.

2.1.2.1. Communication, Navigation & Surveillance (Planning)

The CNS Planning Department within AAI is responsible for planning, procuring and commissioning all CNS facilities and support systems for air navigation based on short- term and long-term requirements. To meet the guidelines laid down by ICAO and to further the CNS ATM transition plans for SATCOM based air traffic management, the CNS Planning Department had undertaken the following initiatives:

¾ Installed automatic dependent surveillance (ADS) at Chennai, Kolkata, Delhi and Mumbai airports and successfully tested for operations

¾ Implemented a dedicated SatCom network in 80 airports all over India to support data and voice communication, including remote controlled air ground VHF communication to provide VHF coverage over the entire Indian air space, networking of radars and ATS data communications

¾ Taken up an area augmentation system using GPS Aided GEO Augmented Navigation (GAGAN), a space based augmentation systems for airspace, which has been developed in collaboration with Indian Space Research Organisation (ISRO)

2.1.2.2. Air Traffic Management (ATM)

This department is responsible for managing air traffic within the country. AAI envisages further upgrade of the ATM infrastructure in the country both in terms of conditional provision of automation systems and upgrade of

4Source: AAI Annual Report 2014-15

AAI Corporate Plan 2017-26 25

Exhibit 4: AAI initiatives to modernize air traffic services in India

Location Initiatives for improving ATS

Mumbai, New Delhi • The upgrade of automation systems to (Auto Track-Ill) with new air traffic controller assistance features such as arrival manager, depar-ture manager etc. at Mumbai and New Delhi airports

• Advanced surface movement ground control systems (ASMGCS) to improve efficient handling of aerodrome traffic (at Mumbai and New Delhi airports)

• Automatic dependent surveillance to enhance the surveillance of suitably equipped aircraft over the entire flight information region (at Mumbai and New Delhi airports)

Hyderabad, Bangalore

• Advanced integrated automation systems that integrate state-of-the-art radars, flight data processors, air situation display, advanced surface movement ground radars, have been installed by SELEX Integreti for providing effective air traffic management

Chennai, Kolkata • An ATS modernization project is underway for replacing old radars, surveillance systems by the latest state-of-the-art technology on par with Mumbai/Delhi to provide a common platform for integration of entire systems over Indian airspace, which will effectively increase air traffic capacity and bring synergy in ATS operations

Nagpur/ Vara-nasi/ Ahmedabad/ Trivandrum/ Mangalore

• Integration of radar with flight data processors has been completed by Electronics Corporation of India (ECIL) in collaboration with AAI for providing indigenous automation solutions for effective air traffic management within the designated airspace

• Initiatives to enhance the standards of ATS

Mumbai, Chennai • Established a number of ATS connector routes in airspace to facili-tate performance based navigation (PBN) operations

Delhi, Mumbai, Ahmedabad and Chennai

• Introduced PBN, standard instrument departures (SIDs) and standard terminal arrival routes (STARs) to reduce delays to aircraft

Source: AAI website5

5Source: http://www.aai.aero/public_notices/aaisite_test/airtraffic_management.jsp

technology, which also involves shifting from ground based navigation to satellite based navigation. AAI has taken

several initiatives to modernize air traffic services in the country, as summarized in Exhibit 4:

2.1.2.3. Flight Inspection Unit The Flight Inspection Unit (FIU)

of AAI is a critical resource of the CNS department. It is responsible for conducting flight checks and calibration of CNS facilities installed

by AAI throughout the country as well as at some Indian Air Force and Indian Navy bases. The calibrations are required to be done on a regular basis, so that the equipment may be certified for use. Considering the vast

AAI Corporate Plan 2017-2626

geographical reach of the country and the range of installed CNS equipment to be tested, the FIU is an important service to ensure flight safety. The need for expanded FIU operations is critical given the increase in the number of airports, and the expansion of existing facilities, e.g., extended or new runways. Currently, the FIU has three fully equipped aircraft, one B-300 and two Do-228s, to undertake flight inspections with support crew. The unit suffers from a shortage of flight crew with only one captain and three co-pilots. This is an important resource that needs to be augmented in this plan period.

2.1.3. Consulting AAI provides consulting services

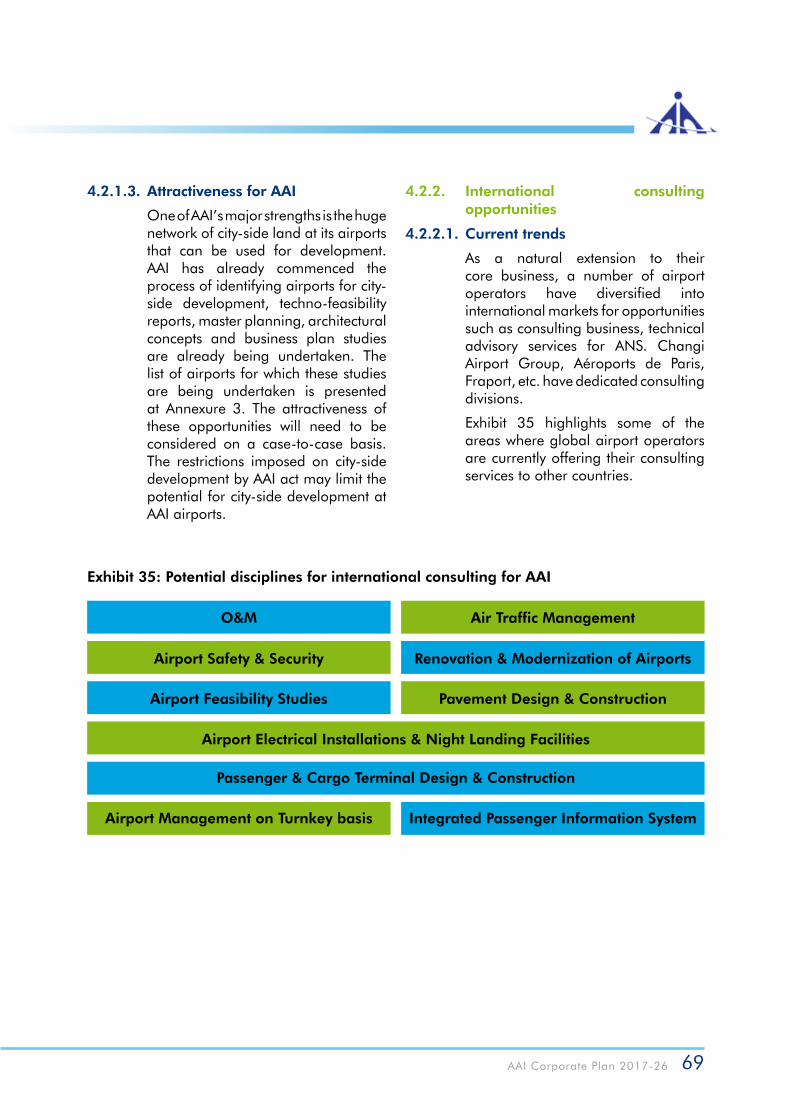

across various domains of airport development and operations. AAI has undertaken consultancy and construction projects in India and abroad. Over the years, AAI has developed a large number of specialists in almost every aspect of airport planning, construction, maintenance and operations. The consultancy division of AAI can co-ordinate and provide inputs leveraging the skills of airport planners, designers, aviation ground equipment specialists, and civil, electrical, and electronics engineers besides specialists in navigational aids, communications, air traffic control, air traffic management, airport terminal operations, air safety, security and audit functions. The expertise available within AAI can be used to provide consulting services across the following areas:

¾ Airport feasibility studies - site selection/technical feasibility

¾ Airport development services - concept to commissioning service for green field airports

¾ Airport commercial viability studies/airport audit services

¾ Airport master planning ¾ Designing, evaluating and constructing passenger terminals/air cargo terminals.

¾ Planning, installation, operation and maintenance of radars, navigational-aids, visual & non-visual landing aids and communication facilities.

¾ Air space and air traffic management, air route re-structuring

¾ Airport management on turnkey basis.

¾ Computerization ¾ Training ¾ Flight calibration of airport ground facilities

2.2. Resource Assessment

AAI’s resources can be categorized as ¾ Physical – tangible assets owned and deployed to provide various services: for example, passenger and cargo terminals, land holdings etc.; and

¾ Manpower and organization.

2.2.1. Physical Resources From the perspective of a corporate

planning exercise, the key physical resources AAI considered were ones that could have a substantial impact on its ability to deliver services over the long term.

Land assets AAI has substantial land assets across

its airports and has the potential to leverage its land holdings for city-side development. Exhibit 5 shows land identified across various airports for potential city-side development in different phases. Currently, AAI is in the process of undertaking feasibility studies and preparing detailed project reports (DPRs) for city-side development at these airports. Besides, AAI has engaged consultants

AAI Corporate Plan 2017-26 27

6Source: AAI presentation to MoCA titled ‘Planning of works – an overview’, 2016

Exhibit 5: City-side developments to be undertaken by AAI (under DPR stage)

Exhibit 6: Airports under AAI: operational vs. non-operational

Airport Land Identified (in Acres)

Airport Land Identified (in

Acres)

Airport Land Identified (in Acres)

Phase I Phase II Phase II

Lucknow 217 Hyderabad Planning Stage Guwahati 46

Raipur 80 Trivandrum 2 Gaya 62

Tirupati 117 Bengaluru Planning Stage Patna 10.5

Kolkata 105 Visakhapatnam Planning Stage Phase III

Varanasi 60 Coimbatore Planning Stage Trichy Planning Stage

Bhubanesh-war

80 Ahmedabad Planning Stage Bhopal 2.5

Jaipur 40 Indore Planning Stage Dehradun 2.4

Amritsar 60 Chandigarh 30 Madurai Planning Stage

Source: AAI presentation to MoCA titled ‘Planning of works – an overview’, 2016

Source: AAI

2.2.1.1. Airside and Terminal Assets

AAI operates a large network of airports, consisting of 21 international airports (3 civil enclaves), 8 customs

airports (4 civil enclaves), 77 domestic airports and 19 domestic civil enclaves. Of these, some of its domestic airports are non-operational.

20

10

19

466

2 2 3

7 7

45

8

1 1 1 00 0 0 0 0 0 0 0 00 0

9

15

12

0Domestic

Operational Non-Operational

DomesticInternational InternationalCustom Custom

North East North East West South

to assess the potential to develop multi-level car parking facilities at

Chennai, Kozhikode, Jaipur, Amritsar, Ahmedabad and Pune.6

AAI Corporate Plan 2017-2628

AAI is in a position to leverage its assets to cater to air traffic growth in the country as well as to enhance regional air connectivity in the country in future, including through potential operationalization of its non-operational airports.

However, it will need to continue to focus on appropriate expansion of airside infrastructure to be able to sustain traffic growth at existing operational airports as well as rehabilitate / upgrade infrastructure at some of its non-operational airports to be able to cater to regional operations in the future.

Based on data as well as interactions with stakeholders, it is evident that enhanced airside infrastructure would be required at a number of airports to cater to future traffic / growth requirements.

For instance, Chennai Airport has a displaced threshold for the runway 12-30 and Kolkata Airport has parallel runways with separation of approximately 200m, which is not adequate for simultaneous operations. Besides, AAI operates 26 civil enclaves that are generally not amenable for flexible capacity expansion to cater to traffic growth. This has resulted in some state governments taking up green field airport development projects (for instance Mopa and Bhogapuram in Goa and Andhra Pradesh respectively).

In terms of passenger terminals, AAI’s average terminal capacity utilization, as presented in Exhibit 7, is ~68% of the available capacity. While high utilization levels are typically preferred from an efficiency / profitability perspective,7 AAI needs to ensure that capacity planning and enhancements are in sync with expected traffic growth rates across airports.

Exhibit 7: Average terminal capacity utilization for AAI and other airports

AAI

70%

0%10%20%30%40%50%60%70%80%90%

100%

81% 68% 92%69% 78% 66% 86%

Terminal Capacity Utilization in the IndianAirport Sector

JV/Pvt./SG Delhi (DIAL) Mumbai (MIAL)

2014-15 2015-16(Till Jan)

7A comparative analysis with other airports in the country shows that some of these airports are operating at higher utilization levels.

AAI Corporate Plan 2017-26 29

AAI’s cargo terminals, under its departmental control, have a current utilization level of ~17%. A list of AAI managed airports with their cargo holding capacities and volume of cargo handled in 2015-16 is presented in Annexure 2.

2.2.2. Manpower and Organisational Resources

2.2.2.1. Manpower – Numbers and Key Issues

AAI's employee strength exceeds 17,000 personnel across various grades and functions. Its employees are predominantly organized by major job functions within a largely function-based organizational structure. As shown in Exhibit 8, ~44% of the employees are in the lower management to top management (executive) cadre.

AAI employees have experience in the areas of airport planning, engineering development, ANS, airport operations,

Exhibit 8: Organizational pyramid, AAI

and other support functions such as finance and human resources.

While AAI has an advantage in terms of the wide variety of professional experience among its employees across key areas, most departments within AAI reported manpower shortage. However, as the HR Strategic Plan 2013-17 noted, manpower cost is the highest proportion of AAI’s revenue expenditure and effective management of human resources is required.

An employees’ satisfaction survey, cited in the HR Strategic Plan 2013-17 indicated satisfaction with aspects like compensation and facilities extended; however, the satisfaction scores indicated that aspects such as ‘working style of management’, working conditions/environment, etc., which affect efficiency and productivity, needed to be addressed.

2.2.2.2. Training

The share of training expenses as a percentage of AAI’s gross expenses have reduced from ~2% in 2007-08 to <0.1% in 2014-15 (in absolute terms, training expenses have fallen from Rs 21 crore in FY07 to Rs 2 crore in FY15), indicating a potential gap in this area. Stakeholder interactions during the preparation of the Corporate Plan also identified this as a key focus area. In this context, the HR Strategic Plan 2013-17 noted that there was need to take up skill development as a planned effort in line with AAI’s requirements and that employees needed to be enabled – especially at the non-executive level – to take up higher responsibilities before elevation.

Board, ED,GM

Top

JGM, DGM, AGM, Senior Manager

Manager Assistant. Manager, Junior Executive

MiddleManagement

LowerManagement

Non-Executive

9,690 (56%)

5,030 (29%)

2,474 (14%)

184 (1%)

AAI Corporate Plan 2017-2630

2.2.2.3. Organizational Structure

HR Strategic Plan 2013-17 noted:

“After the merger of two erstwhile organizations i.e. IAAI and NAA, the organization continued to function with two separate and parallel divisions for over 18 years. The pace to merge

various functions and bringing a unified structure was very slow. Even at this stage, the unified structure is yet to emerge. In order to bring out an optimum organization structure, the pending issues related to merger are required to be addressed and resolved at a faster pace.”

AAI has recently taken up an Organizational Restructuring and Capability Enhancement study to facilitate and expedite achievement of desired results on various initiatives that the Authority is in the process of

undertaking. The key objectives of the study have been articulated as follows:

a. Providing of world class infrastructure and services to the users of airports

b. Tapping the potential from the city side land areas of airports

It accordingly noted a key action plan item as follows:

“To realize an optimum organization structure, a three-step activity will be carried out i.e. restructuring, rationalization and redeployment. Restructuring will involve the study of existing organization structure and

bring out an alternative structure in line with emerging priorities. Rationalization will involve assessment of manpower requirement based on the existing level of activity. This will be followed by redeployment of personnel as per the plan evolved.”

Exhibit 9: Organizational structure for AAI

Source: AAI website

Given the diversity of various activities / businesses at airports requiring specialized skills, airport companies across the world respond by identifying separate teams and executives who can lead such teams. For Example: Changi Airports Group has dedi-cated teams focusing on:

• International endeavours led by an Executive Vice President

• Airside Concessions led by a Senior Vice President

• Landside Concessions led by a Senior Vice President

Chairman

Aviation safety Company Secretary

Member ANS Member Finance

Member Planning

Member OperationsVigilanceMember HR

AAI Corporate Plan 2017-26 31

c. Increasing commercial revenue by restructuring existing infrastructure and by creation of additional infrastructure

d. Creating air cargo infrastructure and facilities for taking air cargo volumes to new heights

e. Excelling in airport performance and building airport’s image, especially in the Asia and Asia Pacific region

The first phase of the study focuses on the following:a. Developing an in-depth

understanding of the organizational priorities and objectives as well as the current organizational structure to outline the key objectives for the new organizational design

b. Defining roles, responsibilities and key performance indicators (KPIs) for the new organizational structure

c. Diagnosing internal capability issues that need to be addressed on a priority basis.

The first phase of this study has been completed and the consultant has already submitted its report. The consultant has already commenced the second phase in which it will develop a time bound capability building programme with detailed roles and responsibilities, key performance indicators (KPI) outline etc., for capacity deficient areas/unit/functions.

2.2.2.4. Management Information System (MIS)

As can be seen, AAI’s is focusing on identifying KPIs for the new organizational structure. Hence, it will be necessary to develop an institutional framework for the development and co-ordination of a robust Management Information System (MIS) for AAI’s top management.

An updated MIS will enable the top management to focus and monitor progress on a number of aspects:

¾ Operations – Improve passenger experience by increasing efficiencies across touch points through regular monitoring and analytics

¾ Finance – Enhance profitability through better controls

¾ Commercial – Increase non-aeronautical revenues through better utilization of retail space within the airport terminal, car park, advertisement and other rentals

¾ Airline Marketing – Identify trends and opportunities to attract more airlines at airports

¾ Infrastructure – Monitor projects as well as proactively maintain assets for better efficiency and serviceability

¾ Environment and Sustainability – Improve safe and energy efficient business operations

¾ Business development – Identify and develop opportunity pipeline within India / overseas

¾ Engineering – Track and improve maintenance activities at the airports

2.3. AAI’s Performance

AAI’s financial and operational performance is discussed in detail below.

2.3.1. Financial Performance

2.3.1.1. Revenues

AAI’s revenues can be broadly categorized into aeronautical, non-aeronautical, cargo, airport lease revenues and others from allied services such as consultancy projects. Sub-heads under each of these revenue categories are highlighted in Exhibit 10:

AAI Corporate Plan 2017-2632

Exhibit 10: Revenue sources for AAI

Source: AAI Financial Statements

As shown in Exhibit 11, AAI’s aeronautical revenues have doubled between 2008 and 2016, contributing more than 50% of AAI’s overall revenues. However, aeronautical revenues are dominated by ANS charges (route navigation facilities charges and terminal navigational landing charges), which have approximately 24.1% share in the overall revenues of AAI.

Non-aeronautical revenues for AAI come from commercial operations at airports like retail, F&B, car parking, other concessions and rentals in terminals and city side premises. As shown in Exhibit 11, non-aeronautical

revenues contributed (on an average) about 10% of total revenues for AAI between 2008 and 2016.

Lease revenues from major airports like Mumbai and Delhi accounted for ~31% of AAI’s revenues in 2016. As tariffs at these airports are regulated by the Airports Economic Regulatory Authority of India (AERA) with reference to traffic growth and investment plans of these airports, AAI has no control over this revenue stream.

The contribution of cargo revenues to AAI’s total revenues was hitherto marginal at about 2%. The overall revenue mix for AAI over 2008, 2012 and 2016 is shown in Exhibit 11.

AAI revenues

Aeronautical Revenues

Non-Aeronautical revenues

OthersCargo revenues

Airport lease revenues

Airport Services• LPH Charges• PSF• UDF• Other airport

services• Service hours

extension• Ground

handling• Oil

Throughput• Royalty on

CUTE

ANS• RNFC charges• TNLC charges Rent & services

• Non-residential buildings

• Hangars• Land rent• Other services• Light, power &

water

Trading concessions

Other airport services• Admission fee

Commercial Passes• Car Parking• Other

Self Operated and outsourced cargo terminals

Consultancy

MIAL Airport

DIAL Airport

AAI Corporate Plan 2017-26 33

Exhibit 11: Revenue mix for AAI (2008-16)

Exhibit 12: Composition of expenses (2008-16)

Source: AAI Annual Reports

Source: AAI Annual Reports

2.3.1.2. Expenses

AAI’s key expense categories include employee costs (comprising employee salaries, allowances and contributions to provident fund), operating expenses including aviation security, administrative expenses, financing

costs and depreciation.

As shown in Exhibit 12, employee costs for AAI have increased by about 12 percentage points between 2008 and 2016, contributing to about 49% of total expenses.

Revenue Mix for AAI (INR Crore)

Cost Mix for AAI (INR Crore)

Reve

nu

eC

ost

s

0

0

1000

2000

3000

4000

5000

6000

7000

8000

2000

2008 2012 2016

4000

6000

8000

10000

36%

37%46%

49%

18%

20%

13%

26%

23%

29%22%

36% 24%

27%

11%

31%

22%

13%

21%

24%

17%10%

10%

4%1%

2%

2%

2,469

2008 2012 2016

2,469

4,378

7,127

4%

4%4%

5%2%

9%4,273

5,879

10,824

Others Cargo Airport Lease Non-Aero Aero ANSOthers Cargo Airport Lease Non-Aero Aero ANS

Gross expensesAdministrative & Other expensesOperating expenses

Finance CostsDepreciationEmployee Benefits

AAI Corporate Plan 2017-2634

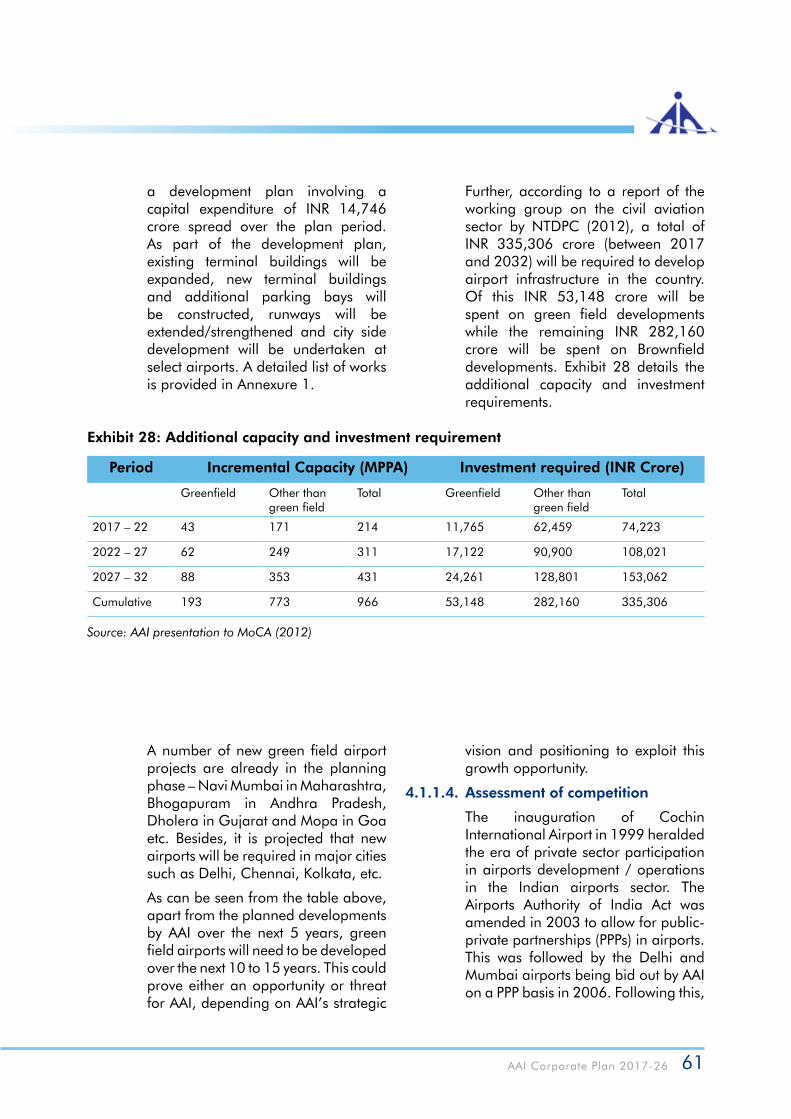

AAI plans to fund the creation of airport infrastructure and ANS equipment worth Rs. 14,746 crore and Rs. 2,646 crore respectively also over the next

five years. The key sources of funding this proposed capital expenditure have been shown in Exhibit 13.

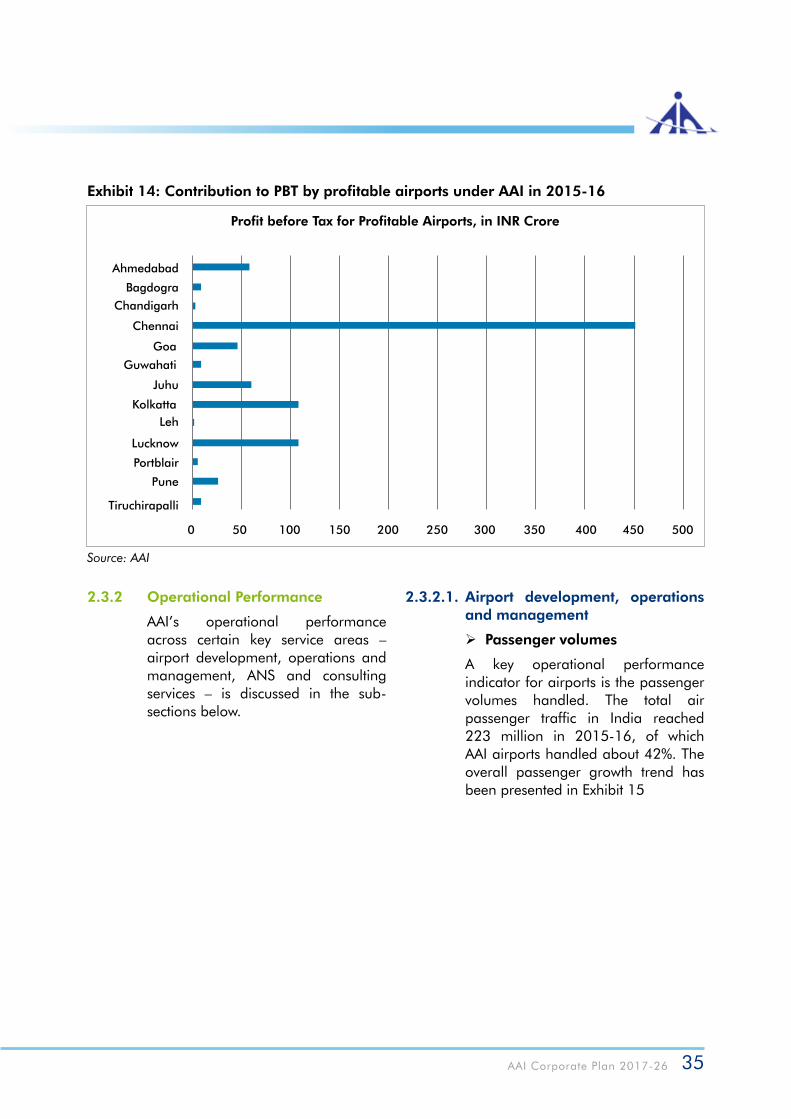

2.3.1.3. Profitability

Only 13 out of 80 operational AAI airports have profitable operations. Kolkata and Chennai Airports are the most profitable airports for AAI, contributing approximately Rs 559 crore to profit before tax (PBT).

Ahmedabad, Bagdogra, Chandigarh, Goa, Guwahati, Juhu, Leh, Lucknow, Port Blair, Pune and Tiruchirapalli Airports are the other profitable airports contributing approximately Rs. 302 crore to PBT.

Exhibit 13: Expected funding sources for proposed capital expenditure over 2016-20

Source: AAI

in INR Crore

Year FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 Total

Opening Cash Balance

2,827 4,493 3,503 746 67 11,636

Internal Re-sources

3,903 2,319 2,323 2,917 3,105 14,568

Accretion to Debtors

(350) (350) (350) (350) (350) (1,750)

NEC Grant 21 76 100 100 100 397

Govt. Bud. Support

81 100 100 90 70 442

CAPEX for Engg / IT works

(1,486) (2,056) (3,919) (4,218) (3,068) (14,746)

Capex for ANS Equip-ment

(271) (284) (734) (578) (779) (2,646)

Term Loans/Borrowings

68 15 158 1,360 1,000 2,600

Bond Repay-ment

(300) (810) (435) 0 0 (1,545)

Closing Cash Balance

4,493 3,503 746 67 146 8954

AAI Corporate Plan 2017-26 35

2.3.2 Operational Performance

AAI’s operational performance across certain key service areas – airport development, operations and management, ANS and consulting services – is discussed in the sub-sections below.

Exhibit 14: Contribution to PBT by profitable airports under AAI in 2015-16

Source: AAI

Profit before Tax for Profitable Airports, in INR Crore

Ahmedabad

Bagdogra

Chandigarh

Chennai

Goa

Guwahati

KolkattaLeh

Lucknow

Portblair

Pune

Tiruchirapalli

Juhu

0 50 100 150 200 250 300 350 400 450 500

2.3.2.1. Airport development, operations and management

¾ Passenger volumes

A key operational performance indicator for airports is the passenger volumes handled. The total air passenger traffic in India reached 223 million in 2015-16, of which AAI airports handled about 42%. The overall passenger growth trend has been presented in Exhibit 15

AAI Corporate Plan 2017-2636

Exhibit 15: Growth trend of passenger traffic in India

Source: AAI data

¾ Passenger satisfaction

Passenger satisfaction is a key parameter of operational performance. AAI has enrolled eleven of its airports in the international passenger satisfaction measurement exercise carried out by Airports Council International (ACI). ACI conducts the “Airport Service Quality (ASQ)” survey annually covering more than thirty parameters that affect passenger experience during their journey – from the time they enter the terminal building to the time they board the flight. Currently, ASQ surveys indicate an average rating of 4.31 out of 5 for the 11 AAI airports that participate in the survey. In 2015, Jaipur and Lucknow airports ranked first and second respectively in the ASQ ratings for airports in the 2-5 million passengers category globally. On the lines as the ASQ survey, AAI also conducts the Customer Satisfaction Index (CSI) survey, at 53 airports that have scheduled operations, to ascertain passenger satisfaction levels.

Along with monitoring passenger satisfaction scores, AAI will need to leverage user feedback (including

online user-generated feedback) to effect continuous improvement in various services.

¾ Cargo volumes

Indian airports handled 2.70 million metric tonnes (MMT) of cargo in 2015-16. Of this, AAI airports handled only 0.79 MMT. Even though AAI has a large number of airports under its management, the bulk of the air cargo is handled at private/joint venture (JV) airports. This can partly be attributed to the fact that private/JV airports are located in large metro cities – catering to buoyant local catchments.

¾ Capacity enhancement

AAI’s last plan period saw economic growth, privatization of major airports and the entry of low cost carriers in the Indian aviation sector. This led to a spurt in passenger numbers, necessitating capacity expansion. AAI undertook a large capital expenditure programme to develop infrastructure across the country. Under this programme, 35 non-metro airports were identified for development to meet future demand. AAI was successful in meeting its

Growth of Passenger traffic in India, 2008-16

2008 2009 2010 2011

Pass

enge

rs in

mill

ions

2012 2013 2014 2015 2016

250

200

150

100

50

0

AAI Traffic PPP Traffic Total Traffic

AAI Corporate Plan 2017-26 37

Source: AAI estimates, presented to MoCA

capacity enhancement targets and has completed development/expansion of 32 airports by the end of its last plan period (2007-2016).

Going forward, designing and planning of terminals will require inputs from all departments, including operations and commercial, to ensure passenger comfort and optimum space utilization to generate non-aeronautical revenues at airports.

Further, as shown in Exhibit 16, of the 20 airports where AAI has planned capacity additions, ten airports are

already operating at traffic levels in excess of their existing design capacities. This has led to situations where new capacity addition by airlines has to be deferred due to terminal congestion. In order to pro-actively cater to growing traffic, it will be important to ensure that planning and development of additional infrastructure / capacities is undertaken in a manner that ensures that growth is not hindered by capacity constraints. This is critical since AAI aspires to build an enduring aviation network to connect businesses and people.

¾ Safety and security

Passenger safety and security are among AAI’s prime concerns. AAI complies with the regulations set by the Directorate General of Civil Aviation of India (DGCA) in matters of aviation safety and by the Bureau of Civil Aviation Security (BCAS) in matters of aviation security.

AAI has taken steps in the past to improve safety at its airports and in the air. The ANS strategic plan, 2014, highlights the steps taken to improve

safety. DGCA, the safety regulator, is a member of ICAO’s State Safety Programme (SSP). In order to manage the SSP and to implement a safety management system (SMS), a special division has been formed by the DGCA.

The SMS identifies safety hazards, ensures implementation of corrective measures to maintain agreed levels of safety, monitors and assesses the efficacy of safety measures and improves SMS on a continuous basis.

Exhibit 16: Airports operating beyond capacity

Airport CurrentCapacity(MPPA)

CurrentDemand(MPPA)

Airport CurrentCapacity(MPPA)

CurrentDemand(MPPA)

Calicut 1.71 2.58 Agartala 0.5 0.88

Guwahati 1.6 2.23 Dehradun 0.4 0.47

Jaipur 2.07 2.20 Mangalore 1.0 1.31

Lucknow 2.18 2.54 Trichy 0.5 1.19

Pune 2.24 4.19

Srinagar 2.00 2.04

AAI Corporate Plan 2017-2638

Following the setting up of the SMS implementation department by the DGCA, AAI in 2005 developed its first Corporate Safety Management System Manual for ANS operations. The manual was subsequently revised and the latest version (2013) was accepted by the DGCA.

AAI has also developed safety performance indicators to monitor and improve safety performance. The main areas of focus are a reduction in bird strike incidents, reduction in separation minima infringement, reduction in runway incursion/excursion and reduction in flight level bursts.

Although AAI takes all necessary steps to ensure passenger safety and security, there have been some instances in the recent past where minor and major incidents were reported. Cases of animal intrusion were reported at Jabalpur, Nagpur and Surat airports, in some cases leading to damage to aircraft. In 2015, an airline bus crashed into an aircraft at Kolkata Airport. There was also an aerobridge related incident in Chennai in 2015.

Given the priority attached to safety and security, AAI intends to initiate measures to eliminate the recurrence of such events.

2.3.2.2. Air Navigation Services

¾ Technology at AAI Airports

New technologies have been introduced recently at various levels in Air Navigation Services. Essentially they have been towards increasing capacity, safety, and providing for savings in flight time and fuel costs to airlines, in addressing issues related to air space use, and towards introducing

environmental sustainability measures and cost control at airport facilities. However, the introduction of new technologies to directly address passenger satisfaction services is not in the forefront of the technological introductions.

In the CNS and ATC disciplines, the introduction of technologies that link the primary and secondary radars through ATC automation systems are a major benefit to tower and area controllers. Further the introduction of automatic dependence surveillance – broadcast (ADS-B) at 21 airports has resulted in improved surveillance using GPS technology to determine the location and airspeed and other aircraft related data.

The indigenous GAGAN system, once commissioned in the next few years during this Corporate Plan period, will further enhance the surveillance capability of aircraft in Indian controlled airspace and in neighbouring countries. This will be a further step ahead in improving air traffic management procedures.

AAI has taken steps to increase and improve communication data links with aircraft and between airports and will attempt to expand these links to neighbouring countries too.

To improve and enhance co-ordination between airport operators, airlines, ATC and other major service providers at the airports, Airport Operations Control Centres have been introduced at 10 airports and more are on the way. The airport operation control centre (AOCC) is key in providing a real-time co-ordinated, collaborative decision making platform to key service providing stakeholders, the airlines

AAI Corporate Plan 2017-26 39

and airport operators, enabling safe airport operations and enhancing its capacity utilization. This service needs to be expanded to all airports as traffic volumes grow. The level of the airport operational data base (AODB) to be introduced varies depending on the volume of traffic to be handled. Discussions with users indicate that AODB should atleast be introduced at airports as they approach an annual load of 5 million passengers or about 150 movements per day.

¾ Air Traffic Flow Management System

The air traffic flow management system (ATFM) system is a forward looking technology application by which a real-time link of all the surveillance and navigation systems will show aircraft operating throughout the Indian airspace on a large screen display at AAI’s air traffic management (ATM) centre. Along with the aircraft and routes, etc., the display will present weather systems and concentrations of flight operations throughout the airspace. The data available will enable guidance to be provided to controllers throughout the country. It will allow flexible routing of flights and improve on-time performance and safety, besides helping maximize utilisation of airspace capacity.

2.3.2.3. Consulting services

AAI has in the past carried out consulting assignments for various state governments and private operators. A majority of these assignments were pre-feasibility studies or techno-economic feasibility studies for new airport projects. In some cases, AAI has offered services to develop new

infrastructure at existing airports or airstrips.

For the year 2014-15, the total revenue earned from consulting services was INR 52 lakh. For the year 2015-16, the revenue from consulting services jumped to INR 4 crore. The revenue earned from these services is modest but AAI can increase revenue from consulting if it actively looks out for opportunities in India and abroad.

2.4. Summary of Internal Assessment

Based on the internal assessment outlined in this section, certain strengths and weaknesses have been identified. These have been presented in section 5 along with opportunities and threats identified that are based on external and market assessments.

AAI Corporate Plan 2017-2640

Srinagar Airport

Bhopal Airport

Ahmedabad Airport

AAI Corporate Plan 2017-26 41

3. External AssessmentThe objective of undertaking an external assessment as part of the Corporate Plan was to identify / assess possible changes and trends in the environment external to the AAI that could have an impact on it over the plan period. To ensure that the exercise is meaningful, the focus has been to identify only those changes that could have a significant impact on the AAI and which could present opportunities

or threats to AAI’s working / growth in the future.

3.1. Policy and Regulatory, Economic, Social, Technology (PEST) Framework

The various factors / trends that could affect AAI have been outlined under certain broad categories as shown in Exhibit 17.

Exhibit 17: PEST framework for external assessment

Economic &

Industrial growth

Tariff Regulation

Environment & Safety

Trends in Air Transportation

NCAP

Social

Technology

Policy & Regulatory

Economic

EXTERNAL ASSESSMENT

AAI Corporate Plan 2017-2642

3.1.1. Policy and Regulatory

Policies and regulations are an integral part of an aviation industry’s ecosystem and can significantly influence its evolution.

The National Civil Aviation Policy (NCAP), recently issued by the Ministry of Civil Aviation, Government of India, is a comprehensive policy blueprint that will have a significant bearing on the functioning of airports in general and of AAI in particular.

As mentioned earlier, the Corporate Planning exercise should have a mechanism to review any future changes in policies and regulations that may affect the aviation sector in the country in general and AAI in particular.

An important aspect to be considered is the fact that AAI revenues from airport leases (Delhi International Airport Limited and Mumbai International Airport Limited) and its own major

airports are dependent on tariff determination by the Airports Economic Regulatory Authority of India (AERA). Further, tariffs for non-major airports, most of which are AAI airports, continue to be determined by the Ministry of Civil Aviation (MoCA). As can be expected in a regulated infrastructure sector, economic regulation has a major bearing on AAI’s financial outlook. Agencies like the Directorate General of Civil Aviation (DGCA) and Bureau of Civil Aviation Security (BCAS) also regulate aspects of AAI’s operations.

3.1.1.1. National Civil Aviation Policy, 2016

The National Civil Aviation Policy (NCAP), 2016, aims to provide a thrust to the sector and envisions the creation of an ecosystem that enables 50 crore domestic ticketing and 20 crore international ticketing by 2027. The NCAP has attempted to address a whole host of issues with implications for AAI.

AAI Corporate Plan 2017-26 43

Exhibit 18: Implications of the NCAP, 2016, for AAI

Source: National Civil Aviation Policy, 2016

Key Features of the NCAP that impact AAI

Cargo MRO OperationsRegional Connectivity Airline Operations

• RCS aims to tap potential markets within India; revive unviable airtstrips / developing 'no frills' airports; effective April 1, 2016

• Separate fund set up to enhance financial support

• State support in providing free land and multi-modal hinterland connectivity

• Provides tax rebates; airport charges exemptions; excise duty exemption on ATF (from RCS airports for RCS routes); utility concessions

• Air Cargo Logistics Promotion Board (ACLPB) formed earlier; to submit detailed action plan to reduce dwell time of "air cargo in truck" and shift to paperless processing

• Encourages development of cargo village near airports

• Provision of space on 10 year lease to operators of express cargo and freighters

• Implementation of advanced air cargo information system by Apr 2016 to improve efficiency/faster processing

• Modification of 5/20 rule to ease commencement of international operations for airlines

• Single-window system for all aviation related transaction queries and complaints

• Promotes growth of airlines through ease of regulations such as no airport charges on airlines having operations under the RCS scheme, Permission to Scheduled Commuter operators to have code share agreements with other airlines

• Tools and tool kits used by MRO have been exempted from customs duty.

• Provision of adequate land for MRO services providers in all future airports with potential for MRO services

• Allows import of unserviceable parts by MROs for providing exchange/advance exchange

• Allows foreign aircraft to stay for up to 6 months for maintenance

• Airport royalty and additional charges will not be levied on MRO service providers for 5 years

Boost to traffic

Increase in Efficiency

OPPORTUNITY

Propels MRO business

Boost to traffic

Cost of infra for airstrip

THREAT

New Airlines and Routes

Boost to traffic

OPPORTUNITY

Airport royalty loss

OPPORTUNITY

AAI Corporate Plan 2017-2644

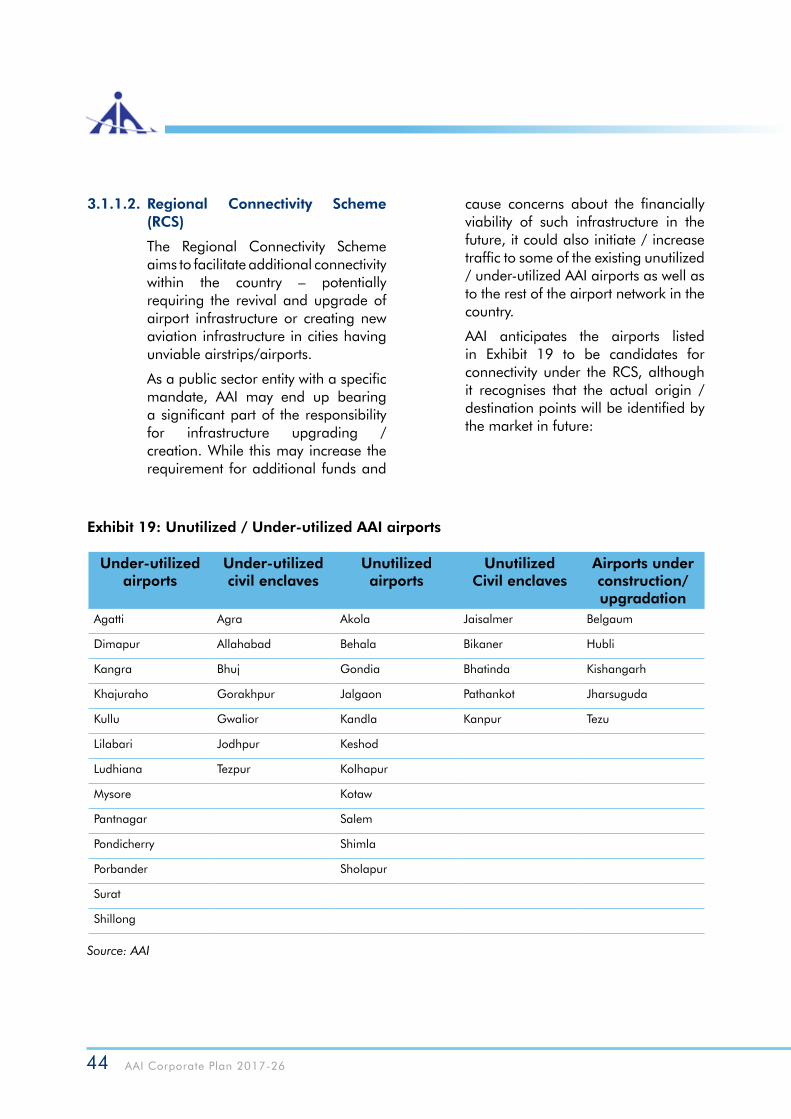

3.1.1.2. Regional Connectivity Scheme (RCS)

The Regional Connectivity Scheme aims to facilitate additional connectivity within the country – potentially requiring the revival and upgrade of airport infrastructure or creating new aviation infrastructure in cities having unviable airstrips/airports.