Languages

Pages

Legal

Funding Op*ons for Life Science Companies May 6, 2014

The Panel Jeremy Halpern Partner, Nu@er McClennen & Fish jhalpern@[email protected] @startupboston

Yumin Choi Partner, HLM Venture Partners [email protected] @yuminvc

Paul Hartung President and CEO, Cognotpix, Inc PHartung@cognop*x.com

Funding the Company

Assuming you plan to be a “high growth” company…

What are your funding op*ons?

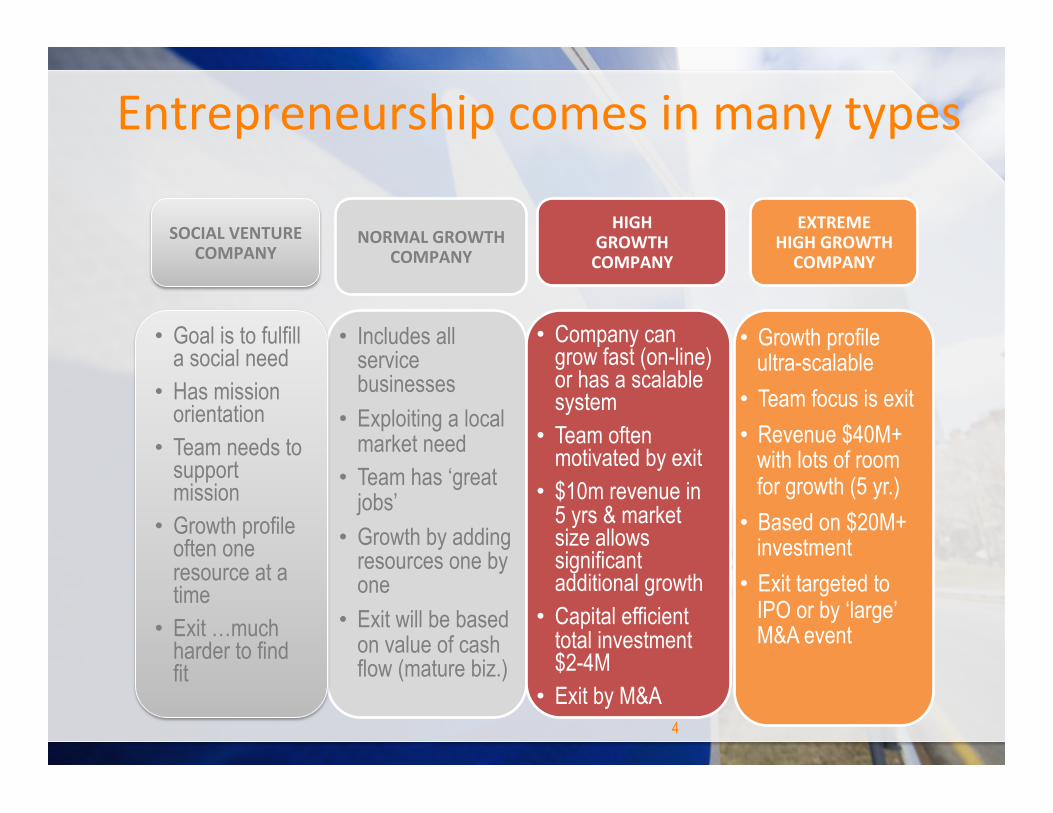

Entrepreneurship comes in many types

4

NORMAL GROWTH COMPANY

HIGH GROWTH COMPANY

EXTREME HIGH GROWTH COMPANY

SOCIAL VENTURE COMPANY

• Includes all service businesses

• Exploiting a local market need

• Team has ‘great jobs’

• Growth by adding resources one by one

• Exit will be based on value of cash flow (mature biz.)

• Growth profile ultra-scalable

• Team focus is exit • Revenue $40M+

with lots of room for growth (5 yr.)

• Based on $20M+ investment

• Exit targeted to IPO or by ‘large’ M&A event

• Goal is to fulfill a social need

• Has mission orientation

• Team needs to support mission

• Growth profile often one resource at a time

• Exit …much harder to find fit

• Company can grow fast (on-line) or has a scalable system

• Team often motivated by exit

• $10m revenue in 5 yrs & market size allows significant additional growth

• Capital efficient total investment$2-4M

• Exit by M&A

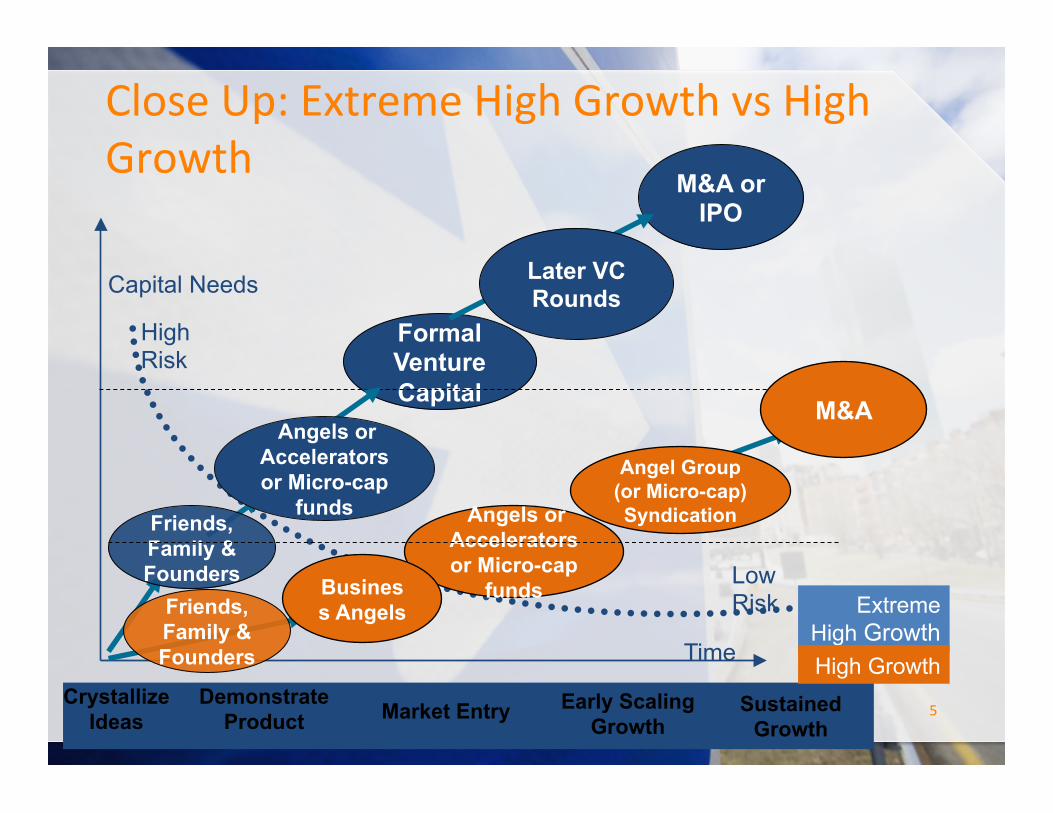

Close Up: Extreme High Growth vs High Growth

5

Capital Needs

Time

High Risk

Low Risk

Formal Venture Capital

M&A or IPO

Crystallize Ideas

Demonstrate Product

Early Scaling Growth

Sustained Growth

Angel Group (or Micro-cap) Syndication

Angels or Accelerators or Micro-cap

funds Angels or Accelerators or Micro-cap

funds Business Angels

Market Entry

M&A

Later VC Rounds

Extreme High Growth High Growth

Friends, Family & Founders

Friends, Family & Founders

High Growth Company Characteris*cs • Disrup*ve Innova*on with Strong value proposi*on

– Correla*on between Large Unmet Need : Solu*on • High Margin Product (Ra*o of Revenue : COGS)

– Some*mes Massive Volume Products where innova*on is incremental

• High Rate of Revenue Growth over sustained period • Scalable (Fixed cost is a low percent of Revenue) • No major barriers to con*nued growth (ex. blocking IP; geography;

regulatory) • Repeatable sales and distribu*on model with many credit worthy

customers • Large Total Addressable Market (TAM) • Defensible innova*on able to withstand compe**on and changing

condi*ons • [Capital efficient]

6

Return on Equity Return on Debt Income High Return

NON PROFIT ORGANIZATION

Capital Source View

7

Debt- Pay it back Fixed Amounts

Equity – Ownership stake % of Future Value

Charity $$

Impact / Tax Write off

NORMAL GROWTH COMPANY

HIGH GROWTH

(COMPANY)

EXTREME HIGH GROWTH (COMPANY)

Risk / Return

SOCIAL VENTURE COMPANY

Match Funding Sources

8

NORMAL GROWTH COMPANY

HIGH GROWTH COMPANY

EXTREME HIGH GROWTH COMPANY

SOCIAL VENTURE COMPANY

• Friends family, founders

• Debt Bank and other

• (Future) Crowd funding (portal style)

Early on • Accelerators • Individual Angels • Micro Cap VCs • Seed from VC Later stages • Venture Funds • Strategic VCs • Angel

Syndication

• Friends family, founders

• Charity$$ • Crowds (Kick-

starter) • Impact Angels • (Future)

Crowd funding (portal style)

• Angels • Angel Groups • Angel Group

Syndication • Angel List • Micro-cap Funds • (Future) Crowd

funding (portal style)

• Increasingly Strategic Corporate VCs

Non-‐Equity Sources • Accelerators (some) • Kickstarter type dona5ons

• Pre-‐orders from end-‐customers • Credit from vendors • Strategic VCs • Strategic NREs • Distribu5on Contracts Common Theme: Providing early cash in exchange for a beHer commercial opportunity

9

Equity Sources • Accelerators (some) • Friends & Family Common Theme: Suppor5ng success of the entrepreneur; business terms vary

• Portal Funding • Early Angels • Super Angels • Angel Groups • Micro VC • Tradi5onal VC (1st Round)

Common Theme: All are looking for – sale (or IPO) of the Company at 4-‐10 x original investment – Capital gains treatment on all sale proceeds – Preferen5al treatment on subop5mal exit versus the founders

10

Sources of Equity Capital Must have exits for equity model to work!!

– 2011 US IPOs -‐ $36B – 2011 US M&A -‐ $57B – 2011 US Private Equity -‐$35B

• Exit sources extremely variable … health of economy • All exits: indica*ve of future cash flow or market control

Idea Stage • Friends family, founders

• Grants • Crowds (Kick-‐ starter)

Demonstrate Product & Market Interest • Accelerators • Individual Angels • Angel Groups • Accelerators • Micro Cap VCs

Market Entry & Early Growth • Crowdfunding (portal style) • Angel Groups • Angel Group SyndicaSon • Angel List • Micro-‐cap Funds

Early Scaling Growth • Most Venture Funds

• Angel SyndicaSon

Repeatable Growth • Most Venture Funds

• Strategic VCs • Angel SyndicaSon

• Private Equity

High Growth Capital by Stage &Amount

12

Venture Stage

Investment Size

Friends & Family

Vendors

Angels

Traditional VC

Angel Groups

Corporate Venturing

Grants

Customers

Crowdfunding

Portal Funding

AngelList

Micro VC

Equipment Financing

Founder

Capital Sources: Size & Cost

Investment Size

Investment “Cost”

Traditional VC

Micro VC

Equipment Financing

Angel Groups Angels

AngelList

Corporate / Strategic Venture

Customers

Portal Funding

Vendors

Founder Friends & Family

Crowdfunding

Grants

Venture Debt Bank

Loans

Personal Loans

Private Equity

So What is Equity Anyway?

• Stock = right to residual economic interests upon sale/liquida*on + stockholder vo*ng rights (usually limited to Board of Directors and Sale of the Company)

• Preferred Stock = right to be paid before Common Stock Par*cipa*ng = original investment PLUS a pro rata share of remainder Non-‐Par*cipa*ng = original investment OR a pro rata share

• Common Stock = whatever is let ater all other creditors and preferred stockholders are paid

• Dividend = a right to an addi*onal amount upon liquida*on measured as a func*on of *me x percentage of original investment . Ex. 6.0% per annum

• OpSons / Warrants = Contracts allowing holder to purchase an amount of stock in the future at a pre-‐determined price

• Control Rights = Statutory and Contractual

14

Equity Type Comparisons

15

Solo Angel Super Angel Angel Group MicroVC VC

Valua*ons High rela*ve to stage

High rela*ve to stage

Low rela*ve to stage

Low rela*ve to stage

Medium

Type -‐ Likely (less likely)

Common (Warrants)

Conv Note (Preferred)

Preferred (Conv Note)

Preferred (Conv Note)

Preferred

Board Seat Maybe 1 or none 1-‐2 of 5 +/-‐ Observer

1 of 5 +/-‐ Observer

1-‐2 of 5 +/-‐ Observer

Audited Financials

No No No (reviewed) Yes Yes

Nega*ve Covenants

No Some*mes Yes Yes Yes

Preemp*ve Rights

No Some*mes Yes Yes Yes

Ver*cal Exper*se

Some*mes Rarely Some Usually Always

Equity Type Comparisons

16

Solo Angel Super Angel Angel Group MicroVC VC

Exit Horizon (from $ in)

7 years 5 years 4 years 5 -‐7 years 4-‐5 years

Exit Range $20m+ $40m+ $50m+ $100m+ $250m+

Structure of an Equity Deal • Company and Investors agree on a “pre-‐money valua*on” (PM) which leads to a price per share

• Investors put in $X • Investors then own: X / (X + PM) of the company

Example: PM = $1M X = $0.5M Investors own 0.5/1.5 = 33% Remember: New issuance NOT transfer

17

Understand the Funding Path • We’re talking about 1st funding here • What is the probable complete funding picture?

– This is only funding – Another small round then probable small exit – Big money needed before exit

• Each funding event should occur at an “inflec5on point” – Hopefully at a point where risk is removed – Increased PM = so-‐called “up round”

18

Understand the Funding Path, cont.

• What if things aren’t going so well? – Flat or decreased PM = so-‐called “down round”

• More money coming in without increased PM means everyone gets diluted, but…

• Depending on anS-‐diluSon provision entrepreneur may carry more burden than the investors

19

What about Conver*ble Debt? • Many seed-‐stage companies use an instrument called Conver5ble Debt. Huh?

• Conver5ble debt is not tradi5onal bank debt • Converts exist for two major reasons

– Investors and Entrepreneurs find it hard to agree on a PM valua5on

– Some5mes quicker and cheaper to document than equity deals (but not really)

20

Conver*ble Debt provides Op*onality

• ConverSble Debt = unsecured debt obliga*on of the Company that may be converted into equity of the Company.

• Conversion Trigger = Qualified Financing usually at some

minimum amount of funds (ex. $500,000)

• If Notes stays as Debt = Get back principal and interest ahead of other equity (behind other creditors typically)

• If Notes Convert = Convert amount of debt and interest into equity at the valua*on in the next round

• ater applica*on of a Discount (oten 5 – 20%) • subject to a maximum valua*on amount (the “Cap”)

21

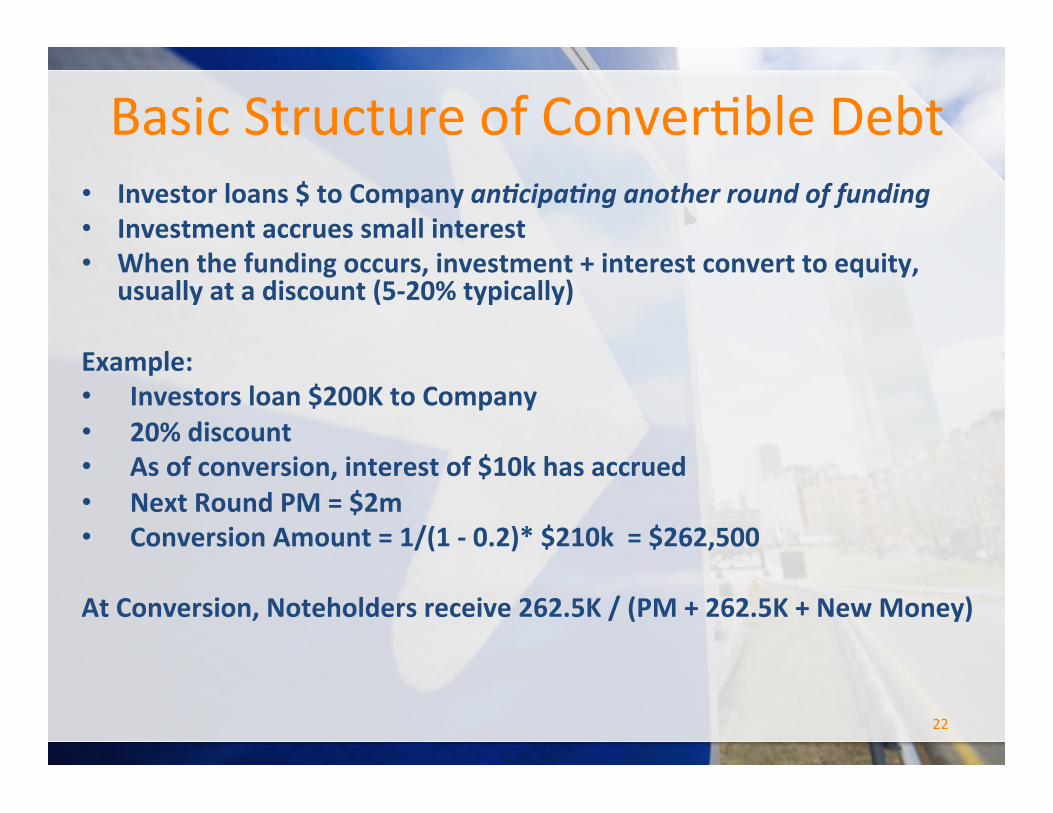

Basic Structure of Conver*ble Debt • Investor loans $ to Company an5cipa5ng another round of funding • Investment accrues small interest • When the funding occurs, investment + interest convert to equity,

usually at a discount (5-‐20% typically)

Example: • Investors loan $200K to Company • 20% discount • As of conversion, interest of $10k has accrued • Next Round PM = $2m • Conversion Amount = 1/(1 -‐ 0.2)* $210k = $262,500 At Conversion, Noteholders receive 262.5K / (PM + 262.5K + New Money)

22

Conver*ble Debt – Complica*ons! • When does the debt convert? • What happens if PM of next round is huge? • Does the investor have any say in things? • What if there is an equity investment that doesn’t trigger conversion?

• What happens if it never converts? • What happens if Company gets bought?

23

Conver*ble Debt – Solu*ons? • Caps and Floors

– May defeat purpose with signaling

• Default conversion price and security at maturity

• Quick sale preferences (ex. 2x) • Governance provisions • Careful agenSon to conversion condiSons

24

Conver*ble Debt – Worse than Equity?

• MulSple liquidaSon preference (circa 2008) – Ex. $500k of Notes with cap at $2m PM – Next Round at $6m PM – Issue Noteholders 3x number of shares – 3x shares equals 3x liquidaSon preference!!

• Without a floor, effecSvely Full Ratchet AnS-‐diluSon

• Preference Overhang – In prior example Noteholders bought $262,500 of preference for $200,000.

– All other Series A Holders bought 1:1 preference

• Not Just a Price Adjustment 25

www.TheCapitalNetwork.org

Top Related