Languages

Pages

Legal

Financial statements of

The Scarborough Hospital March 31, 2016

The Scarborough Hospital March 31, 2016 Table of contents Independent Auditor’s Report .................................................................................................... 1-2

Statement of revenue and expenses ............................................................................................ 3

Statement of changes in net assets .............................................................................................. 4

Statement of remeasurement gains .............................................................................................. 5

Statement of financial position ...................................................................................................... 6

Statement of cash flows ................................................................................................................ 7

Notes to the financial statements ............................................................................................. 8-20

Deloitte LLP 5140 Yonge Street Suite 1700 Toronto ON M2N 6L7 Canada Tel: 416-601-6150 Fax: 416-601-6151 www.deloitte.ca

Independent Auditor’s Report To the Board of Directors of The Scarborough Hospital We have audited the accompanying financial statements of The Scarborough Hospital, which comprise the statement of financial position as at March 31, 2016, the statements of revenue and expenses, changes in net assets, remeasurement gains and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with Canadian public sector accounting standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained in our audit is sufficient and appropriate to provide a basis for our audit opinion.

Page 2

Opinion In our opinion, the financial statements present fairly, in all material respects, the financial position of The Scarborough Hospital as at March 31, 2016 and the results of its operations, changes in its net assets, remeasurement gains and its cash flows for the year then ended in accordance with Canadian public sector accounting standards.

Chartered Professional Accountants Licensed Public Accountants June 7, 2016

Page 3

The Scarborough Hospital

Statement of revenue and expenses

Year ended March 31, 2016

(In thousands of dollars)

2016 2015 $ $

Revenue

Ministry of Health and Long-Term Care and Cancer Care Ontario 334,630 335,763

Other Ministry Community Programs 6,208 6,786

Patient revenues 25,811 27,263

Recoveries and other income 18,308 15,415

Medical Mall office building 2,125 1,952

Amortization of deferred capital contributions 5,479 4,822

392,561 392,001

Expenses

Salaries and wages 205,008 205,009

Employee benefits 51,356 51,970

Medical and surgical supplies 27,049 26,752

Drugs 26,664 23,229

Supplies and other expenses 56,594 58,099

Other Ministry Community Programs 6,384 6,997

Medical Mall office building 1,074 1,194

Amortization - building and equipment 14,597 14,960

Bad debt expense 2,214 1,840

Interest on long term debt 1,153 1,108

392,093 391,158

Excess of revenue over expenses 468 843

Page 4

The Scarborough Hospital

Statement of changes in net assets

As at March 31, 2016

(In thousands of dollars)

2016 2015

Invested in capital assets

Invested in joint venture

assets Unrestricted Total Total

$ $ $ $ $

Net assets, beginning of year 59,637 538 (45,462) 14,713 13,870

Excess of (expenses over revenue) -

revenue over expense (9,118) 3 9,583 468 843

Net change in net assets invested

in capital assets 11,750 - (11,750) - -

Net assets, end of year 62,269 541 (47,629) 15,181 14,713

Page 5

The Scarborough Hospital

Statement of remeasurement gains

As at March 31, 2016

(In thousands of dollars)

2016 2015 $ $

Accumulated remeasurement gains, beginning of year 1,548 1,464

Unrealized gains attributable to

Derivatives – interest rate swap 428 84

Accumulated remeasurement gains, end of year 1,976 1,548

Page 6

The Scarborough Hospital Statement of financial position As at March 31, 2016 (In thousands of dollars)

2016 2015 $ $

Assets Current assets

Cash and short term investments - 7,359 Accounts receivable (Note 3) 12,382 11,412 Inventories 2,460 2,319 Prepaid expenses 3,523 2,171 Current portion of long-term receivable (Note 4) 688 703

19,053 23,964

Long-term receivable (Note 4) - 631 Investment in joint ventures (Note 5) 541 538 Restricted cash (Note 6) 2,353 - Capital assets (Note 7) 176,314 175,919

198,261 201,052

Liabilities Current liabilities

Bank indebtedness (Note 8) 3,587 - Short term indebtedness (Note 9) 1,500 1,500 Accounts payable and accrued liabilities (Note 10) 44,311 49,560 Current portion of long-term debt (Note 11) 3,716 3,429 Current portion of capital lease obligation (Note 12) 715 1,064 Deferred contributions 3,561 4,498

57,390 60,051

Legal defence fund (Note 15 B) 1,567 431 Long-term debt (Note 11) 12,240 14,103 Long-term capital lease obligation (Note 12) 833 1,547 Deferred capital contributions (Note 13) 96,541 96,139 Employee future benefits (Note 14) 10,637 10,196 Derivatives - interest rate swap (Note 19) 1,896 2,324

181,104 184,791

Contingent liabilities and guarantees (Note 15)

Net assets Invested in capital assets (Note 16) 62,269 59,637 Invested in joint ventures (Note 5) 541 538 Unrestricted (47,629) (45,462)

15,181 14,713

Remeasurement gains 1,976 1,548 198,261 201,052

Page 7

The Scarborough Hospital

Statement of cash flows

As at March 31, 2016

(In thousands of dollars)

2016 2015 $ $

Operating activities

Excess of revenue over expenses 468 843

Payment of employee future benefits (603) (566)

Items not affecting cash

Amortization of capital assets 14,597 14,960

Amortization of deferred capital contributions (5,479) (4,822)

Employee future benefit expense 1,044 1,114

Joint venture income (3) 3

Market value adjustment - derivative 428 84

Legal defence provision 1,136 431

11,588 12,047

Changes in non-cash working items (Note 20) (8,649) 7,098

2,939 19,145

Financing activities

Receipt of long-term debt 1,595 1,926

Repayment of long-term debt (3,171) (3,439)

Receipt of long-term receivable 646 644

Increase (decrease) in derivative liability (428) (84)

Legal defence claims fund (2,353) -

(3,711) (953)

Capital activities

Acquisition of capital assets (14,992) (21,011)

Receipt of deferred capital contributions 5,881 10,480

Repayment of capital lease (1,063) (1,025)

(10,174) (11,556)

Net change in cash (10,946) 6,636

Cash, beginning of year 7,359 723

(Bank indebtedness) cash , end of year (3,587) 7,359

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 8

1. Description of business

Upon approval by the Health Services Restructuring Commission and the Ministry of Health and Long-Term Care (“Ministry”), The Scarborough Hospital (the “Hospital”) was formed on September 8, 1999 through the amalgamation under subsection 113(3) of the Corporations Act (Ontario) of the Scarborough General Hospital and the Salvation Army Scarborough Grace Hospital.

The Hospital is a multi-location acute care community general hospital. It is classified as a registered charity under the Income Tax Act (Canada) and, as such, is not subject to income tax provided certain disbursement requirements are met.

The financial statements do not include the assets, liabilities and operations of The Scarborough Hospital Foundation (the “Foundation”). Revenues generated by the Foundation may be donated to the Hospital upon approval by its board.

The Hospital signed a 2015-16 Hospital Service Accountability Agreement with the Central East Local Health Integration Network (“LHIN”) which included a balanced total margin target. Any excess of expenses over revenue is the responsibility of the Hospital and must be funded from other sources, including capital funds.

2. Summary of significant accounting policies

Financial statement presentation

The financial statements have been prepared in accordance with Canadian public sector accounting standards for government not-for-profit organizations, using the deferral method of reporting contributions.

Description of funds

Funds invested in capital assets represent the net book value of the Hospital’s capital assets, less any related debt and unamortized capital grants.

Unrestricted funds represent the excess of revenue over expenses (expenses over revenue) accumulated from the ongoing operations of the Hospital since its inception.

Revenue recognition

Under the Health Insurance Act and Regulations thereto, the Corporation is primarily funded by the Province of Ontario. Operating grants are recorded as revenue in the year to which they relate.

Operating contributions are recognized as revenue when received or receivable if the amounts to be received can be reasonably estimated and collection is reasonably assured. Capital contributions externally restricted for the purchase of capital assets are deferred and amortized into revenue on a straight-line basis at a rate corresponding with the amortization rate of the related capital assets.

Revenue from other agencies, patients, special programs and other sources is recognized when the service is provided.

To the extent which the Ministry or LHIN funding has been received with the stipulated requirement that the Hospital provide specific services and these services have not yet been provided, the funding is deferred until such time as the services are performed and the monies spent. In the event that the services are not performed in accordance with the funding requirements, the funds received in excess of monies spent could be recovered by the Ministry or LHIN.

Investment income is recorded as revenue in the statement of revenue and expenses.

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 9

2. Summary of significant accounting policies (continued)

Financial instruments

All financial instruments reported on the Statement of financial position for the year ended March 31, 2016 are measured as follows:

Cash and short term investments Fair value Bank indebtedness Fair value Short-term indebtedness Amortized cost Accounts receivable Amortized cost Long-term receivable Amortized cost Accounts payable and accrued liabilities Amortized cost Long-term debt Amortized cost Derivatives – Interest rate swap Fair value

Contributed services

Due to the difficulty in determining their fair value, contributed services are not recognized in the financial statements.

Investment in joint ventures

The investment in joint venture is accounted for using the modified equity method.

Capital assets

Capital assets are recorded at cost and amortized on a straight-line basis over their estimated useful lives using the following rates:

Buildings and building improvements 10-50 years Furniture and equipment 5-20 years Computer equipment 3-5 years

Construction in progress

Construction in progress represents expenditures incurred for projects currently underway. Upon completion, the relating construction in progress will be transferred to the appropriate capital asset category and amortization will commence.

Capital contributions

Building and equipment grants received by the Hospital are deferred and amortized on a straight-line basis at a rate corresponding to the amortization rate for the related building or equipment purchased.

Employee benefit plans

The Hospital is an employer member of the Healthcare of Ontario Pension Plan, which is a multi-employer, defined benefit pension plan. The Hospital has adopted defined contribution plan accounting principles for this Plan because insufficient information is available to apply defined benefit plan accounting principles.

The Hospital accrues its obligations for employee benefit plans. The cost of non-pension post-retirement and post-employment benefits earned by employees is actuarially determined using the projected benefit method prorated on service and management’s best estimate of retirement ages of employees and expected heath care costs. Actuarial gains or losses are amortized over the average remaining service period of the active employees. The average remaining service period for active employees is 13 years. Future cost escalation affects the amount of employee future benefits. The accrued benefit obligation related to employee benefits is discounted using current interest rates based on the Hospital’s cost of borrowing.

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 10

2. Summary of significant accounting policies (continued)

Employee benefit plans (continued)

Adjustments arising from plan amendments are recognized in the year that the plan amendments occur. Actuarial gains or losses are amortized over the average remaining service period of the active employees.

Use of estimates

The preparation of financial statements in accordance with Canadian public sector accounting standards requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the statement of financial position date and the reported amounts of revenues and expenses for the year then ended. Actual results may differ from such estimates.

In particular, the amount of revenue recognized from the Ministry and the LHIN requires some estimation. The Hospital has entered into accountability agreements that set out the rights and obligations of the parties in respect of funding provided to the Hospital by the Ministry and the LHIN. The accountability agreements set out certain performance standards and obligations that establish acceptable results for the Hospital’s performance in a number of areas.

If the Hospital does not meet its performance standards or obligations, the Ministry and the LHIN have the right to adjust funding received. Neither the Ministry nor the LHIN are required to communicate certain funding adjustments until after submission of year end data. Since this data is not submitted until after the completion of the financial statements, the amount of the Ministry/LHIN funding received during a year may be increased or decreased subsequent to year end. The amount of revenue recognized in these financial statements represents management’s best estimates of amounts that have been earned during the year.

Other accounts that include significant estimates are accounts receivable, useful lives of capital assets, accounts payable and accrued liabilities, legal defense provision, employee future benefits and derivatives.

3. Accounts receivable

2016 2015$ $

Ministry of Health and Long-Term Care 3,964 3,441Patients’ accounts 7,364 5,884Other 3,607 4,024 14,935 13,349Less: allowance for doubtful accounts 2,553 1,937 12,382 11,412

4. Long-term receivable

During fiscal 2013, the Hospital paid a total refundable membership of $2,580 to Plexxus to finance its transitional cash requirements in fiscal years 2012 and 2013 as it proceeded with the implementation of the Integrated Technology Solution (ITS) project. Accrued interest of $58 during the year (2015 - $58) is included in the balance. Plexxus has been refunding the membership fee in four annual installments $703 (includes $58 interest) commencing on April 1, 2013 and concluding on April 1, 2016. The Hospital received the third installment of $703 (2015 - $703) during the year.

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 11

5. Investment in joint ventures

In 1997 the Hospital, (through its predecessor organizations) together with North York General Hospital formed an incorporated joint venture for the purpose of providing non-emergency laboratory services to the hospitals. In fiscal 2008, Michael Garron Hospital (formerly Toronto East General Hospital joined the joint venture. The joint venture is equally owned through common shares by the three hospitals as at the reporting date. The Hospital owns one third of the common shares as at the reporting date and contributed 44% of the joint venture revenues. There are no significant differences between the accounting policies of the Hospital and those of the joint venture. The investment represents the investment in common shares of the joint venture using the modified equity method and non-voting preferred shares in the amount of $166.

In the event of the liquidation, dissolution or winding up of the joint venture, the holders of the Class A preferred shares are entitled to receive from the assets of the joint venture, a sum equivalent to all Class A preferred shares held, before any amount to be paid to other parties.

During 2011, the Hospital entered into a joint venture agreement with Professional Respiratory Home Care Service Corp. to form Scarborough ProResp Inc. The investment represents $260 Class A preferred shares and 50% of the equity interest in the form of 50 Class A common shares. The investment represents the investment in commons shares of the joint venture using the modified equity method and non-voting preferred shares in the amount of $260. The Hospital has a Management Services Agreement with Scarborough ProResp Inc. to provide supervisory and management services in return for a management fee. During the year management fees of $139 (2015 - $139) were included in the statement of revenue and expenses as other income.

The following discloses the Hospital’s share of the following financial statement elements:

2016Shared Hospital

Laboratories ProResp$ $

Shareholder’s equity 15 361Revenues 1,211 656Expenses 1,214 577Dividends paid 73Cash flow from operating (21) 115Cash flow from investing (8) (10)Cash flow from financing (1) (59)

2015

Shared Hospital Laboratories ProResp

$ $ Shareholder’s equity 18 355Revenues 1,185 635Expenses 1,189 562Dividends paid - 72Cash flow from operating (104) 144Cash flow from investing (1) (38)Cash flow from financing (1) (72)

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 12

6. Restricted Cash

Effective January 1, 2015, the Hospital entered into an agreement with Health Care Insurance Reciprocal of Canada (“HIROC”) whereby the cost of investigating and defending any litigation claims would be borne by the Hospital. To fund the expected payments, the Hospital transferred funds to an operating account managed by HIROC Management Ltd. as the Hospital’s appointed agent. The cash balance of $2,353 at March 31, 2016 (2015 - $nil) is restricted for these payments.

7. Capital assets

2016 2015

CostAccumulated amortization

Net book value

Net book value

$ $ $ $

Land 967 - 967 967Buildings and building improvements 256,807 104,874 151,933 149,318Furniture and equipment 173,327 159,626 13,701 14,678Computer equipment 36,125 31,016 5,109 5,828Construction in progress 4,604 - 4,604 5,128

471,830 295,516 176,314 175,919

8. Bank indebtedness

The Hospital has an operating line of credit with its financial institution to assist in managing the day to day cash flows of the Hospital. As of March 31, 2016 the available line of credit was $30,000 (2015 - $30,000). As of March 31, 2016, the Hospital has drawn $3,587 (2015 - $nil). The line of credit bears interest at a rate of prime less 0.25% and is payable on demand.

9. Short term indebtedness

The Hospital has a credit facility with the Foundation. Amounts borrowed from the Foundation are due on demand and bear interest at prime less 0.50%. As of March 31, 2016, $1,500 (2015 - $1,500) has been borrowed.

10. Accounts payable and accrued liabilities

2016 2015$ $

Trade payables 16,807 22,695Salaries and benefits 25,410 24,753Accrued liabilities 2,050 1,652Others 44 460 44,311 49,560

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 13

11. Long-term debt

The non-revolving term loan facility, originally entered into in February 2009 for $14,000, relates to the construction of the West Wing. This facility is repayable in 120 monthly payments through January 2019. It bears a floating interest rate based on variable banker’s acceptance rates, which ranged from 0.743% to 0.988% (2015 - 0.976% to 1.30%) during the year. Effective October 2, 2006, an interest rate swap modified the floating interest rate on the loan to a fixed rate of 7.96%.

The non-revolving term loan facility, originally entered into in May 2005 for $5,000, relates to the construction of the Head Start component of the West Wing. This facility was repayable in 120 monthly payments through May 2015. It bears a floating interest rate based on variable banker’s acceptance rates, which ranged from 0.868% to 0.986% (2015 - 0.976% to 1.30%) during the year. Effective October 2, 2006, an interest rate swap modified the floating interest rate on the loan to a fixed rate of 6.707%. The loan was fully repaid at March 31, 2016

The non-revolving 10-year demand loan facility, originally entered into in April 2003 for $7,000, relates to the purchase of the Medical Mall office building. This facility is repayable in 300 monthly payments through April 2028. It bears a floating interest rate based on variable banker’s acceptance rates, which ranged from 0.743% to 0.988% (2015 - 0.976% to 1.30%) during the year. Effective April 1, 2003, an interest rate swap modified the floating interest rate on the loan to a fixed rate of 6.66%. The Hospital or the financial institution may elect to terminate the facility on April 1, 2018 or April 1, 2023.

The non-revolving demand loan facility, originally entered into in March 2012 for $3,563, relates to the purchase of CT scan equipment. This facility is repayable in 60 monthly payments through March 2017. It bears a fixed interest rate of 3.40%.

In fiscal 2014, the Hospital entered into a capital energy agreement with Ameresco Canada Inc. and Manulife to commence work on capital and energy measures at the Hospital. The terms of the agreement require the Hospital to obtain a loan which bears fixed interest of 4.75% and is repayable in monthly payments commencing June 2015 through May 2025.

2016 2015 $ $

CIBC - non-revolving term loan facility (West Wing) 5,146 6,703 CIBC - non-revolving term loan facility (West Wing Head Start) - 114 CIBC - non-revolving demand loan facility (Medical Mall office building) 4,619 4,868 CIBC - non-revolving demand loan facility (CT scan equipment) 765 1,503 Manulife - Energy Savings Agreement 5,426 4,344 15,956 17,532 Less: current portion 3,716 3,429 12,240 14,103

Principal payments required in each of the next five fiscal years and beyond are as follows:

$ 2017 3,7162018 2,6072019 2,4212020 8372021 884Thereafter 5,491 15,956

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 14

12. Obligations under capital leases

In December 2011, the Hospital entered into a capital lease agreement for MRI equipment with Macquarie Equipment Finance Ltd. for $3,518 payable quarterly. The agreement expires September 2016 and provides an option to purchase the equipment from the Lessor at the expiration of the Base Term by payment to the Lessor of $1.00. The applicable rate used by the Lessor in pricing the lease is 3.40%.

In November 2013, the Hospital entered into a capital lease agreement for endoscope equipment with Olympus Canada Inc. Medical Systems Group for $1,343 payable monthly. The agreement expires October 2019 and provides an option to purchase the equipment from the Lessor at the expiration of the Base Term by payment to the Lessor of $131. The applicable rate used by Lessor in pricing the lease is 5.0%.

In March 2013, the Hospital entered into a capital lease agreement for SAN and Meditech server with Macquarie Equipment Finance Ltd. for $602 payable monthly. The agreement expires February 2018 and provides an option to purchase the equipment from the Lessor at the expiration of the Base Term by payment to the Lessor of $1.00. The applicable rate used by Lessor in pricing the lease is 3.89%.

The future minimum lease payments required under the capital lease agreements are as follows:

$ Total minimum lease payments 1,548Less: current portion 715Long-term portion 833

Principal payments due in the next 4 years are as follows:

$ 2017 7152018 3362019 2262020 271 1,548

13. Deferred capital contributions

2016 2015$ $

Balance, beginning of year 96,139 90,481Capital contributions received during the year 5,881 10,480Amortization for the year (5,479) (4,822)Balance, end of year 96,541 96,139

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 15

14. Employee future benefits

The Hospital provides certain post-employment benefits to some of its employees. The most recent actuarial valuation for the Hospital was performed March 31, 2015.

At March 31, the Hospital’s liability associated with the benefit plan is as follows:

2016 2015$ $

Accrued benefit liability, beginning of year 10,196 9,648Current service cost 621 606Interest cost 343 434Amortization of actuarial gains 80 74Benefits paid (603) (566) 10,637 10,196 Accrued benefit liability, end of year 11,098 11,091Unamortized actuarial gains (461) (895) 10,637 10,196

The significant actuarial assumptions adopted in estimating the Hospital’s accrued benefit obligations are as follows:

2016 2015 % %

Discount rate to determine accrued benefit obligation 3.0% 4.0% Extended healthcare cost escalations, decreasing by 0.25% per annum to an ultimate rate of 4.75% thereafter 7.5% 7.5% Expected average remaining service life of employees 13 13

Included in the statement of revenue and expenses is an amount of $1,044 (2015 - $1,114) regarding employee future benefits. This amount is comprised of:

2016 2015$ $

Current service costs 621 606Amortization of actuarial gains 80 74Interest on obligation 343 434 1,044 1,114

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 16

15. Contingent liabilities and guarantees

A. Due to the nature of its operations, the Hospital is periodically subject to lawsuits in which the Hospital is a defendant, as well as grievances filed by its various unions. Management accrues liabilities for claims against the Hospital when a liability is likely to be incurred and the amount of the claim can be reasonably estimated.

B. On July 1, 1987, a group of health care organizations (“subscribers”) formed HIROC. HIROC is registered as a Reciprocal pursuant to provincial Insurance Acts, which permit persons to exchange with other persons reciprocal contracts of indemnity insurance. HIROC facilitates the provision of liability insurance coverage to health care organizations in the provinces of Ontario, Manitoba, Saskatchewan and Newfoundland. Subscribers pay annual premiums, which are actuarially determined, and are subject to assessment for losses in excess of such premiums, if any, experienced by the group of subscribers for the years in which they were a subscriber. No such assessments have been made to March 31, 2016.

Effective January 1, 2015, the Hospital entered into an agreement with HIROC to provide indemnity insurance, however, the cost of investigating and defending any ligation claims would be borne by the Hospital. The Hospital has appointed HIROC Management Limited (HML) to act as agent for the Hospital for such claims defence costs in accordance with an Agency Agreement. To fund the expected payments, the Hospital transferred funds to an operating account managed by HIROC Management Ltd. as the Hospital’s appointed agent. Costs associated with claims arising prior to January 1, 2015 will be borne by HIROC. Costs of defending claims that arise subsequent to January 1, 2015 are based on claims defence costs incurred by HIROC in the past. The provision at March 31, 2016 is $1,567 (2015 - $431) and the related claims defence expense of $1,357 is included in the statement of revenue and expenses.

C. In the normal course of business, the Hospital enters into agreements that meet the definition

of a guarantee. The Hospital’s primary guarantees are as follows:

a) The Hospital has provided indemnities under lease agreements for the use of various operating facilities. Under the terms of these agreements the Hospital agrees to indemnify the counterparties for various items including, but not limited to, all liabilities, losses, suits, and damages arising during, on or after the term of the agreement. The maximum amount of any potential future payment cannot be reasonably estimated.

b) Indemnity has been provided to all directors and or officers of the Hospital for various items including, but not limited to, all costs to settle suits or actions due to association with the Hospital, subject to certain restrictions. The Hospital has purchased errors and omissions insurance to mitigate the cost of any potential future suits or actions. The term of the indemnification is not explicitly defined, but is limited to the period over which the indemnified party served as a director or officer of the Hospital. The maximum amount of any potential future payment cannot be reasonably estimated.

c) The Hospital has entered into agreements that include indemnities in favour of third parties. These indemnification agreements may require the Hospital to compensate counterparties for losses incurred by the counterparties as a result of breaches in representation and regulations or as a result of litigation claims or statutory sanctions that may be suffered by the counterparty as a consequence of the transaction. The terms of these indemnities are not explicitly defined and the maximum amount of any potential reimbursement cannot be reasonably estimated.

Historically, the Hospital has not made any significant payments under such or similar indemnification agreements and, therefore, no amount has been accrued in the statement of financial position with respect to these agreements.

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 17

16. Net assets invested in capital assets

2016 2015$ $

Capital assets (Note 6) 176,314 175,919Adjusted for amounts financed by

Long-term debt (Note 11) (15,956) (17,532)Deferred capital contributions (Note 13) (96,541) (96,139)Obligations under capital lease (Note 12) (1,548) (2,611)

62,269 59,637

17. Pension plan

Substantially all of the employees of the Hospital are members of the Healthcare of Ontario Pension Plan (“the Plan”), a multi-employer defined benefit plan. Contributions to the Plan made during the year by the Hospital on behalf of its employees amounted to $14,911 (2015 - $14,682) and are included in the statement of revenue and expenses.

18. Related party transactions

During the year, contributions were received from The Scarborough Hospital Foundation (“the Foundation”) in the amount of $ 5,304 (2015 - $5,361). At March 31, 2016, $106 (2015 - $347) was due from the Foundation and included in accounts receivable. The Hospital also has related party transactions with joint ventures as disclosed in Note 5. The Hospital is a member of Plexxus, Booth Centennial Healthcare Linen Services, and Hospital Diagnostic Imaging Repository Services, who provide various services to the Hospital at market value.

19. Financial instruments and risk management

Risk management

The Hospital, through its financial assets, including financial instruments and liabilities has exposure to credit risk and interest rate risk.

Interest rate risk

Interest rate risk arises from the possibility that changes in interest rates will affect the value of debt held by the Hospital. The Hospital has mitigated this risk by entering into interest rate swaps.

Credit risk

The Hospital’s principal financial assets are short term investments and accounts receivable which are subject to credit risk. The carrying amounts of financial assets on the statement of financial position represent the Hospital’s maximum credit exposure at the statement of financial position date.

The Hospital’s credit risk is primarily attributable to its patient receivables. The amounts disclosed in the statement of financial position are net of allowance for doubtful accounts, estimated by the management of the Hospital based on previous experience and its assessment of the current economic environment. The credit risk on short-term investments is limited because the counterparties are banks with high credit-ratings assigned by national credit-rating agencies.

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 18

19. Financial instruments and risk management (continued)

Fair value

Fair value represents the amount that would be exchanged in an arm’s length transaction between willing parties who are under no compulsion to act and is best evidenced by a quoted market price, if one exists. The Hospital’s fair values are management’s estimates and are generally determined using market conditions at a specific point in time and may not reflect future fair values. The determinations are subjective in nature, involving uncertainties and the exercise of significant judgment.

The fair value of short term indebtedness, accounts receivable, accounts payable and accrued liabilities approximate their carrying values due to their short-term maturity.

The fair value of short-term investments is based on cost plus accrued interest which approximates fair value due to their short term maturity.

The fair value of long term debt approximates its carrying value due to interest rate swaps which have been entered on each debt instrument that account for the change in market values relative to the fixed rates.

Fair value of derivative financial instruments

The Hospital has entered into three derivative financial instrument transactions. Descriptions of the current derivative financial instruments are as follow:

A. A non-revolving term loan facility for the construction of the West Wing in the amount of $14,000 was originally obtained in February 2009. The notional value of this loan is $5,146 at March 31, 2016 (2015 - $6,703). The Hospital entered into an interest rate swap arrangement to modify the rate of the loan from a variable banker’s acceptance rate ranging from 0.743% to 0.988% (2015 - 0.976% to 1.30%) to a fixed rate of 7.96%. The start date of the interest rate swap was January 2, 2009 with a maturity date of January 2, 2019. The fair value of the interest rate swap at March 31, 2016 is $497 (2015 - $867).

B. A non-revolving demand loan facility for the financing of the Medical Mall office building in the amount of $7,000 was originally obtained in April 2003. The notional value of this loan is $4,619 at March 31, 2016 (2015 - $4,868). The Hospital has entered into an interest rate swap arrangement to modify the rate of the loan from a variable banker’s acceptance rate ranging from 0.743% to 0.988% (2015 - 0.976% to 1.30%) to a fixed rate of 6.66%. The start date of the interest rate swap was April 1, 2003 with a maturity date of April 3, 2028. The fair value of the interest rate swap is $1,399 at March 31, 2016 (2015 - $1,456). The Hospital also had the option to reduce the notional amount of the loan by $150 commencing April 1, 2004 and annually thereafter. The Hospital sold the option on November 10, 2011 and received proceeds of $530 which were recorded in the statement of remeasurement gains. The Hospital or the financial institution may elect to terminate the facility on April 1, 2018 or April 1, 2023.

C. During the year, $428 in derivative gain (2015 - $84 gain) was included in the statement of remeasurement gains.

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 19

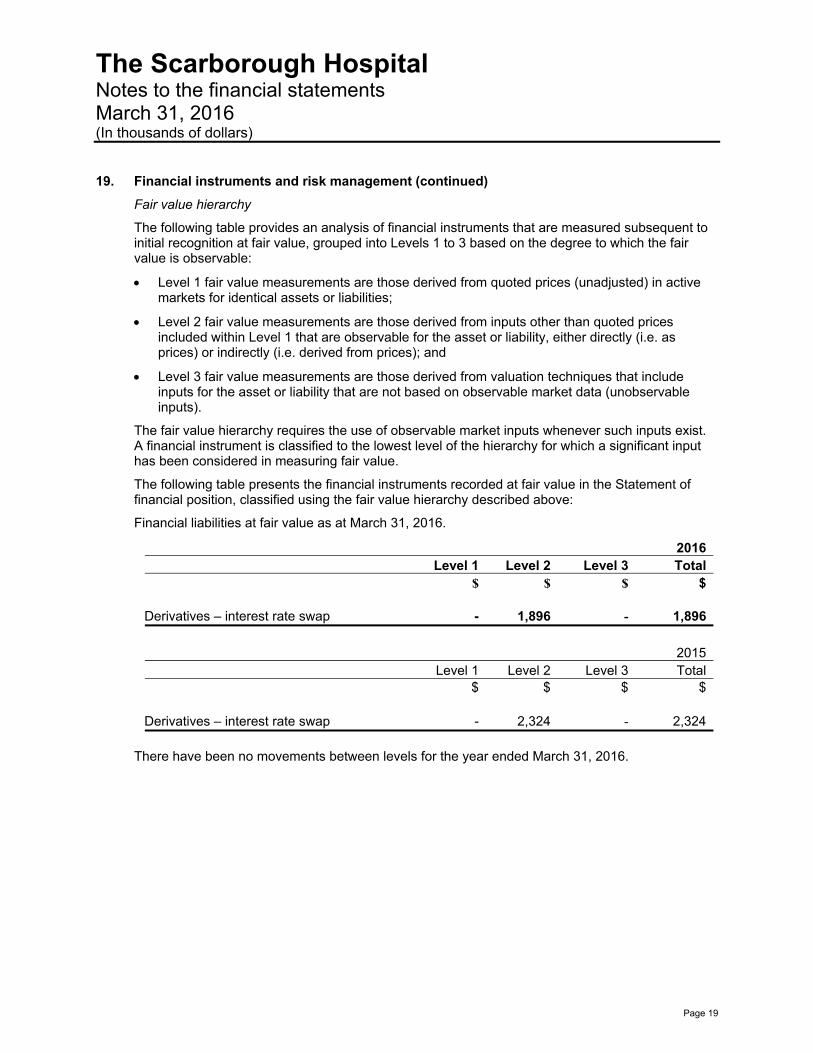

19. Financial instruments and risk management (continued)

Fair value hierarchy

The following table provides an analysis of financial instruments that are measured subsequent to initial recognition at fair value, grouped into Levels 1 to 3 based on the degree to which the fair value is observable:

Level 1 fair value measurements are those derived from quoted prices (unadjusted) in active markets for identical assets or liabilities;

Level 2 fair value measurements are those derived from inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices); and

Level 3 fair value measurements are those derived from valuation techniques that include inputs for the asset or liability that are not based on observable market data (unobservable inputs).

The fair value hierarchy requires the use of observable market inputs whenever such inputs exist. A financial instrument is classified to the lowest level of the hierarchy for which a significant input has been considered in measuring fair value.

The following table presents the financial instruments recorded at fair value in the Statement of financial position, classified using the fair value hierarchy described above:

Financial liabilities at fair value as at March 31, 2016.

2016 Level 1 Level 2 Level 3 Total $ $ $ $

Derivatives – interest rate swap - 1,896 - 1,896

2015

Level 1 Level 2 Level 3 Total $ $ $ $

Derivatives – interest rate swap - 2,324 - 2,324

There have been no movements between levels for the year ended March 31, 2016.

The Scarborough Hospital Notes to the financial statements March 31, 2016 (In thousands of dollars)

Page 20

20. Changes in non-cash working capital items

2016 2015 $ $

Accounts receivable (970) 1,169Inventories (141) 886Prepaid expenses (1,352) 94Accounts payable and accrued liabilities (5,249) 7,178 Deferred contributions (937) (2,229)

(8,649) 7,098

21. Integration of The Scarborough Hospital

On April 26, 2016, the Minister of Health and Long-Term Care, supported the implementation of allrecommendations from the final report of the Scarborough/West Durham Expert Panel related tohospital governance, service delivery and planning to give patients better access to care in thecommunity.

The Expert Panel recommended the creation of an integrated hospital system under onecorporation and one Board of Directors to oversee the three Scarborough hospital sites; specificallythe General and Birchmount sites of The Scarborough Hospital and the Centenary site of RougeValley Health System, and the development of a single master plan.

To oversee the integration efforts, the Minister appointed a special advisor to the Minister to workwith the three hospitals affected by the announcement; The Scarborough Hospital, Rouge ValleyHealth System, and Lakeridge Health for a period that will not exceed one year and ending no laterthan June 30, 2017.

22. Comparative figures

Certain comparative numbers have been reclassified to conform to the current year presentation.

Top Related