Languages

Pages

Legal

2nd Quarter 2016

Financial Report

Island Offshore Shipholding LP

27 of September 2016

The businessIsland Offshore Shipholding, L.P. (the “Company” or “Island Offshore”) is the parent company in the Island Offshore

group (the “Group”). The Group has 28 vessels in operation within the vessel segments PSV, AHTS, Well Stimulation

(WS), Subsea Construction (SCV) and Light Well Intervention (LWI). The fleet operates in Norway, UK, Holland, India,

West Africa and Gulf of Mexico.

The fleet is modern and versatile and Island Offshore has taken a leading position in attractive market segments. The

Group is privately owned.

Contract awards Island Champion: Team Marine

Island Valiant: KD Marine

Island Vanguard: NCA

Island Constructor: Erin Energy, Shell, BP UK

Island Condor: Perenco

Island Crown: VBMS/Vattenfall

Fleet changesSale of Island Patriot, May 2016

Fleet The fleet comprises 28 vessels in operation including the Island Champion which is leased back on bareboat. The vessel

Island Patriot was sold in May 2016 but is still operated by Island Offshore Management AS.

At present 5 PSV vessels are in lay-up. As long as both spot and term day rates remain unsustainable, additional lay-

ups will be considered to reduce operational cost and mitigate reduced cash inflow. The PSV fleet is particularly exposed

upon expiry of existing contracts. Accordingly, we expect the number of vessels in lay-up to increase through the winter

months.

Island Offshore currently has 6 vessels in the spot market; 2 PSVs , 2 AHTS and 2 SCVs . Vessels are tendered for term

work globally.

1

2nd Quarter Financial Report 2016

Main events 2016:

Type Vessels in operation

Vessels under construction

TOTAL

PSV 15 0 15

AHTS 2 1 3

SCV 4 0 4

RLWI 4 0 4

STIM 3 0 3

THD 0 1 1

TOTAL 28 2 30

Vessel Type/Design Yard

Island Victory DWIV, UT 797 CX Vard Brevik

Island Navigator THDV, UT 777 Kawasaki Heavy Industries

Income Statement

Fleet revenue totals NOK 566 mill in Q2-16, up from NOK 419 million in Q1-16, but lower than the same quarter last

year. Fleet utilization in Q2 was 67% including vessels in lay-up (YTD 65%). Utilization thus revenue from the LWI fleet

increased significantly in Q2 following commencement of term contracts. Bareboat day rate for one of the units was

re-negotiated in Q2 thus revenue for this unit is reduced accordingly. Due to increased spot exposure and declining

average rates, both AHTS and PSV revenue declined compared to Q1-16 and the equivalent period last year.

EBITDA in Q2-16 totals NOK 207 mill versus NOK 133 mill in Q1-16 thus a significant improvement. All segments

reported year to date a positive EBITDA contribution despite challenging market conditions. WS EBITDA includes

a sales gain of NOK 35 mill from the sale of Island Patriot; adjusted for this gain WS profitability is stable across

quarters. The LWI vessels made a significant contribution to EBITDA in Q2-16 due to commencement of campaigns.

The EBITDA margin increased to 41% in Q2-16, which is up from 34% in Q1-16, mainly due to increased vessel

activity, especially LWI.

Focus continues to be on developing market opportunities and cost reductions to mitigate declining revenue. Salary

cuts and manning reductions have been implemented both onshore and offshore, and further cost reduction initiatives

will be introduced. We expect the PSVs currently in lay-up to remain out of the market, but explore potential

conversion and modification opportunities for these vessels.

The book value of the fleet at 31.12.2015 was written down by NOK 268 mill based on impairment analysis. The

analysis has not been revised as of 30.6.2016, however updated fair value appraisals obtained from independent ship

brokers indicate an average value reduction of 9,4% in the fleet.

Q2-16 profit before tax is NOK 13 mill and includes unrealized FX loss of NOK 12 mill related to conversion of ship

mortgages in USD.

Quarterly Financial Report

2

- Comments

Q2 2015 Q2 2016 YTD Q2 2015 YTD Q2 2016

NOK mill

Revenue 694 566 1.237 985

Net subcontractors -91 -68 -107 -97

Total operating revenue 603 499 1.130 889

Operating expenses 333 292 660 548

EBITDA 271 207 471 340

Depreciation 89 91 170 181

Impairment provision 0 0 0 0

EBIT 182 117 301 159

Unrealized foreign exchange gain+/losses- on USD ship mortages

42 -12 -69 86

Net other foreign exchange gain+/losses- -5 -12 -2 -36

Net financial interests & other financial items -98 -79 -200 -174Profit before tax 121 13 30 34

3

Photo: Sondre Solvang

Photo: Sondre Solvang

NOK mill 31.12.2015 30.06.2016Ships 9.773 9.441New building contracts 131 139Other financial assets 764 756Deferred tax asset 34 34Total Fixed Assets 10.702 10.368

Inventory, stock 32 30Debtors 785 933Bank, cash 271 184Total Current Assets 1.088 1.146Total Assets 11.791 11.515

Total paid-in equity 596 696Other equity 1.864 1.900Total Equity 2.460 2.596

Deferred tax 118 118Total Provisions 118 118

Liabilities to financial institutions 7.378 6.962Other long term liabilities 1.427 1.407Total Long Term Liabilities 8.805 8.369Trade creditors 239 230Other Short Term Liabilities 168 201Total Short Term Liabilities 407 431

Total Liabilities 9.328 8.919Total Equity and Liabilities 11.791 11.515

Balance Sheet

4

Fixed asset additions in 2016 comprise planned

maintenance activities. Sale of the Island Patriot was

recorded in May 2016 thus reducing fleet book value at

30.6.2016. Book value of the fleet was written-down

by NOK 268 mill at 31.12.2015 based on impairment

analysis; please refer to comment above regarding

changes in market prices.

The cash balance is NOK 184 mill as at 30.6.2016 thus

down from NOK 271 mill at 31.12.2015. Net working

capital has increased in Q2 following increased vessel

activity and sales/AR.

Net interest bearing debt is NOK 7.023 mill at 30.6.2016

adjusted for CIRR loans/deposits and shareholder loans.

This corresponds to a gearing ratio of 8,22 (NIBD/12M

rolling EBITDA). The Company has obtained acceptance

of ease on financial covenants, hereto debt service and

gearing ratio covenants.

The book value of the equity is NOK 2.596 mill, which

equals a book equity ratio of 24,1%, adjusted for CIRR

loans/deposits. VAE is estimated to NOK 3.156 mill equal

to a ratio of 27,9% at 30.6.2016 based on broker’s value

appraisals of the fleet. In the bank loan agreements

the VAE ratio covenant is 30% and thus the Company

has requested waivers with the financial institutions

regarding this.

Balance Sheet and Cash Flow

4

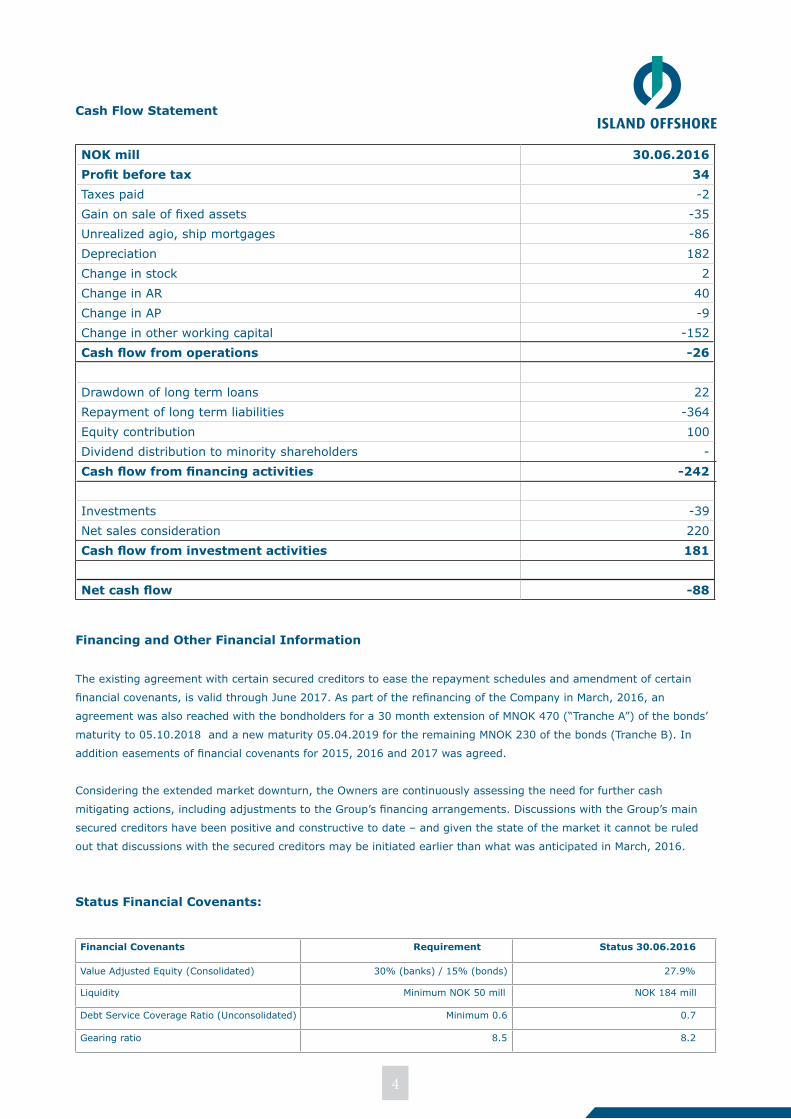

Cash Flow Statement

NOK mill 30.06.2016Profit before tax 34Taxes paid -2Gain on sale of fixed assets -35Unrealized agio, ship mortgages -86Depreciation 182Change in stock 2Change in AR 40Change in AP -9Change in other working capital -152Cash flow from operations -26

Drawdown of long term loans 22Repayment of long term liabilities -364Equity contribution 100 Dividend distribution to minority shareholders -Cash flow from financing activities -242

Investments -39Net sales consideration 220Cash flow from investment activities 181

Net cash flow -88

The existing agreement with certain secured creditors to ease the repayment schedules and amendment of certain

financial covenants, is valid through June 2017. As part of the refinancing of the Company in March, 2016, an

agreement was also reached with the bondholders for a 30 month extension of MNOK 470 (“Tranche A”) of the bonds’

maturity to 05.10.2018 and a new maturity 05.04.2019 for the remaining MNOK 230 of the bonds (Tranche B). In

addition easements of financial covenants for 2015, 2016 and 2017 was agreed.

Considering the extended market downturn, the Owners are continuously assessing the need for further cash

mitigating actions, including adjustments to the Group’s financing arrangements. Discussions with the Group’s main

secured creditors have been positive and constructive to date – and given the state of the market it cannot be ruled

out that discussions with the secured creditors may be initiated earlier than what was anticipated in March, 2016.

Financing and Other Financial Information

Status Financial Covenants:

Financial Covenants Requirement Status 30.06.2016

Value Adjusted Equity (Consolidated) 30% (banks) / 15% (bonds) 27.9%

Liquidity Minimum NOK 50 mill NOK 184 mill

Debt Service Coverage Ratio (Unconsolidated) Minimum 0.6 0.7

Gearing ratio 8.5 8.2

5

Debt maturity profile Group:

The NOK 700 million bond is repayable in two tranches, first in October 2018 with NOK 470 mill and subsequently the

buy-back amount of NOK 230 mill in April 2019. Annual loan installments are adjusted for balloon payments year by

year.

Outstanding capital expenditures Group:

The Group’s future capital expenditure commitments mainly comprise the two new building contracts with delivery

in April 2018 and January 2019 respectively. The Island Navigator, to be delivered from Kawasaki Heavy Industries,

is fully financed. Take out financing for Island Victory, to be delivered from Vard Brevik, is progressing as planned.

Remaining capital expenditure constitutes estimated periodical maintenance activities.

The significant demand/supply imbalance continues to depress the global PSV and AHTS markets despite the increasing

number of vessels in lay-up. We do not see any signs of a restored market, and expect the PSV market to be poor in the

next few years. The AHTS market offers short periods with acceptable day rates and utilization. Overall, the market state

is weak also for this vessel type.

Our strategy remains firm with focus on securing long-term commitment with strategically preferred clients, in addition to

exploring opportunities to develop new and improved services.

The fleet order backlog excluding charterer’s options totals NOK 3,7 billion at 30.6.2016. Contract coverage for the

remainder of 2016 is 54% based on contract days; 32% in 2017.

One LWI vessel is contracted to a US end-client through a related party entity . The end-customer has recently (Q3/16)

terminated the charter contract, however the contract with the related party entity is continued albeit at a reduced rate.

The full implications for the Group’s future earnings are not yet determined, however the parties are collaborating to secure

future employment for the vessel. The order back log has been adjusted to reflect the agreed day rate.

Market Outlook & Order Backlog

7

Contract coverage by vessel:

6

Health, Safety and the Environment

Island Offshore shall endeavor to promote and maintain a safe and healthy working environment offshore and

onshore. This includes considering health and safety factors in the design, construction and operation of all vessels

and equipment. We are committed to increasing the level of safety involvement and awareness among all employees.

Key performance targets are set, validated and monitored in a QHSE plan. The personnel injury frequency remains

low but further improvement is required to facilitate the zero incident objective. Sick leave for offshore personnel has

stabilized in Q2-16 but the ambition remains to reduce sick leave beyond current levels. CO2 emission from the fleet

has been reduced by 19% in 2016, however reduction is partly explained by lower vessel activity and lay-up.

We continue with the main focus areas:

• Reductions in emissions by use of alternative fuels, reduction in fuel consumption and cleaning of exhaust

• Selection and handling of chemicals

• Waste management

• Handling of environmentally harmful substances from marine and subsea operations

Photo: Sondre Solvang

Investor relations:

Mr. Henning Sundet, Chief Financial Officer: [email protected], +47 913 65 735

*This financial report represents the consolidated financial statements for the Island Offshore Shipholding LP Group. The report is prepared on the basis of Generally Accepted Accounting Principles in Norway and has not been audited.

Top Related