Languages

Pages

Legal

A crash course in financial management for startup businesses Presented by:

Matt H. Evans SCORE Mentor

Finance 101 for Startups Outline

• Module 1 – How Accounting Works

• Module 2 – Reading the Financial Statements

• Module 3 – Analyzing the Financial Statements

• Module 4 – Additional Financial Analysis

• Module 5 – Evaluating Long Term Investments

• Module 6 – Advanced Concepts in Finance

• Module 7 – Business Analysis

1

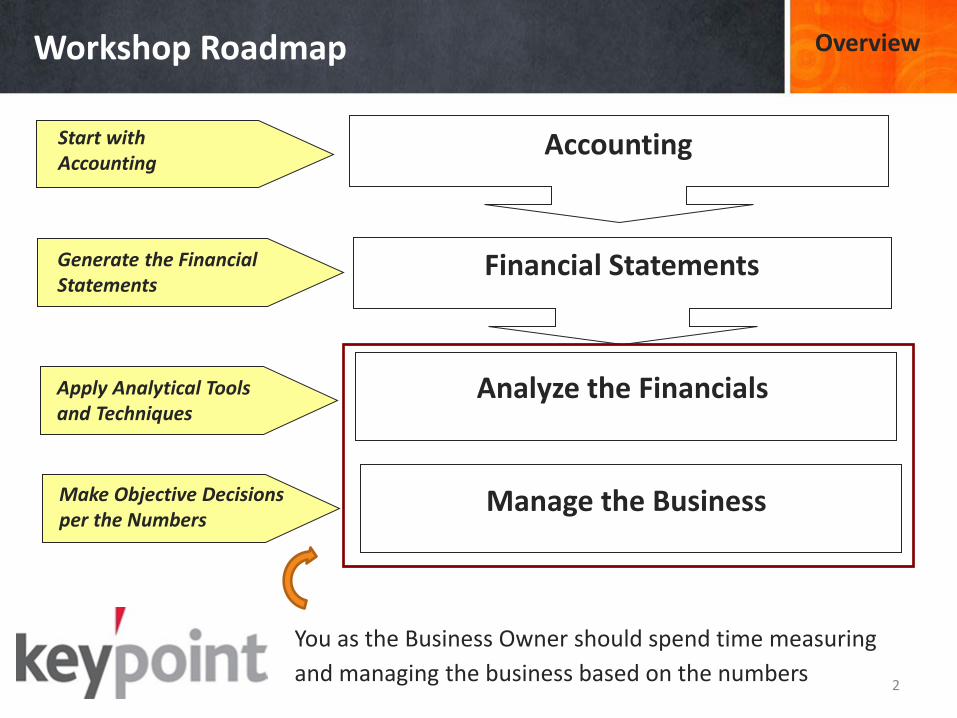

Workshop Roadmap Overview

2

Accounting

Financial Statements

Analyze the Financials

Start with Accounting

Generate the Financial Statements

Apply Analytical Tools and Techniques

Make Objective Decisions per the Numbers

Manage the Business

You as the Business Owner should spend time measuring

and managing the business based on the numbers

Module 1 How Accounting Works

3

Overview of how the accounting process works at

a detail transaction level

Think in Terms of Your Check Book Module 1

4

• All transactions pass through your Check Book

• All transactions must be recorded

• Businesses have a wide range of transactions:

- Customers buy your products or services = Cash Inflows

- Vendors and Employees must be paid = Cash Outflows

Cash Inflows

(Deposits)

Cash Outflows

(Checks)

Accrual Accounting is Preferred Module 1

5

Most transactions are cash basis (pass through your cash account), but . . .

• Accrual Accounting recognizes revenues when earned before you collect the cash – Accounts Receivable Account

• Accrual Accounting recognizes expenses when incurred before you make payment – Accounts Payable Account

• Cash Basis – Only post transactions when they go in and out of your Check Book

• Tracking – Make sure you can control and track the money you owe others in the future and collect all money owed to you (customers pay on time when due).

Simple Cash Basis Accounting Module 1

6

Simple Spreadsheet for Cash Basis Accounting

Year:

Date Description Name Amount Category RefRevenues: (Cash Collected from Sales to Customers)

2/8/2018 Sold 18 bars soap at Eastern Market Various Walk By Traffic 54.00$ Sales Revenue

2/17/2018 Sold 20 bars soap to Rosa Ela Shop Rosa Ela Shop in College Prk 40.00$ Sales Revenue

2/22/2018 Sold 22 bars soap at Dupont Circle Various Walk By Traffic 66.00$ Sales Revenue

Feb-18 Online Orders of Soap - Etsy Various per Etsy 22.00$ Sales Revenue

TOTAL REVENUES 182.00$

Expenses: (Cash Paid for all business related expenses)1/6/2018 Soap Materials Sarah's Craft House (110.09)$ Materials Expense

1/15/2018 Booth Materials for Markets M-Displays Inc (75.00)$ Marketing Expense

1/22/2018 Promotion Flyers Office Max (36.55)$ Marketing Expense

2/6/2018 License Fee to County DC Dept of Cons / Reg Affairs (115.00)$ Legal Expenses

TOTAL EXPENSES (336.64)$

PROFIT OR (LOSS) (154.64)$

How the Accounting Model Works Module 1

Businesses invest in assets two ways: Liabilities and

Equity. Assets exist for one single reason: To Generate

Revenues

1. Assets – Resources of the Business

2. Liabilities – Obligations

3. Equity – Investments by Owners

4. Revenues – Inflows from Sales

5. Expenses – Outflows for Costs

Balance Sheet

Income Statement

The Accounting Model can be summarized through two equations: Assets = Liabilities + Equity Revenues – Expenses = Profit or (Loss)

7

Chart of Accounts – Capture the Transactions Module 1

Chart of Accounts is the structure by which all

transactions are categorized and reported by the business

Cash Money in the bank

Accounts Receivable Amounts owed to the company for sales

Inventory Pants, Shirts, Hats, Shoes, Socks, Belts, etc.

Prepaid Expenses Amounts paid in advance

Furniture and Fixtures Storefront assets such as tables, racks, chairs, etc.

Machinery and Equipment Property used to manufacture clothing (Sewing Machines)

Accounts Payable Amounts that must be paid to vendors / suppliers

Loans Payable Amounts due to banks

Long Term Debt Amounts due to investors or bank against long term assets

Owners Capital Account Amount invested by the owner of the business

Retained Earnings Profits held by the business for reinvesting

Sales Revenue Amount of revenues from selling products / services

Cost of Goods Sold Cost of inventory that has been sold

Administrative Expense Cost of office support personnel

Selling and Marketing Expense Advertising, Sales Commissions, Trade Show Displays, etc.

Utility Expense Gas, Water & Electric expenses

Depreciation Expense Expense a portion of the cost of a long term asset

Assets

Liabilities

Equity

Revenues

Expenses

8

Most Transactions Go Thru the Cash Account Module 1

9

1-6-2014 Purchase office supplies

1-1-2014 Beginning Balance

Account Title: Cash

1-16-2014 Run Bi Weekly Payroll

1-12-2014 Deposit payment from customer

1-26-2014 Pay Monthly Electric Bill

1-22-2014 Insurance Premium Paid

$ 4,220.55

$ 142.20

1-31-2014 Ending Balance

$ 3,600.00

$ 2,640.00

$ 265.00

$ 516.30

$ 4,257.05

Debit (Left) Credit (Right)

Let’s walk through a few accounting entries as it relates to the Cash Account

The balance as of a cut off date is what gets reported

on the Financial Statements

Accounting is Dual (Two Sides)

10

Module 1

Balance Sheet

Assets offset by Liab +Equity

Income Statement Revenues offset by Expenses

The Accounting Process Module 1

11

Accounting

System

Financial

Statements

End of Period

Accrual Entries

Transactions

(Mostly Cash Basis)

Post to General

Ledger Accounts

Accounting is a very iterative process that captures transactions (inputs)

to generate Financial Statements (outputs)

Balance

Sheet

Income

Statement

Economic Activity of the

Business

Recap Important Points Module 1

12

1. Most transactions pass through the Cash Account. Make sure you post all transactions that go through your Business Bank Account.

2. You must classify all transactions according to how you want to report financial results. Chart of Accounts

3. Accounts capture transactions. There are five major groups of accounts: Assets, Liabilities, Equity, Revenues, and Expenses

4. The five groups of accounts is the basis for presenting the financial statements of a business: Balance Sheet and Income Statement.

5. Financial Statements are prepared as of a cut off date (such as March 31st) presenting the balances as of this date.

Comprehensive Example – Accounting Entries Module 1

13

Let’s go through a startup business and see how accounting transactions get posted over time Three phases take place over time when starting a business: 1. Fund the Business – Financing Transactions 2. Acquire the Right Mix of Assets to Generate Revenues –

Investment Transactions 3. Generate Revenues and Expenses – Operating Transactions

Someone in your business must be responsible for

posting accounting transactions on a regular basis

Accounting Software Programs

14

Module 1

Using software programs can help automate the entire process including invoicing, creating financial reports, etc. Here are some very inexpensive programs for small businesses that are highly rated:

Quick Books > https://quickbooks.intuit.com/ Fresh Books > https://www.freshbooks.com/ Wave > https://www.waveapps.com/ Billy > https://billyapp.com/ Zip Books > https://zipbooks.com/ Express Accounts > https://www.nchsoftware.com/accounting/index.html KashFlow > https://www.kashflow.com/ GoDaddy Accounting > https://www.godaddy.com/email/online-bookkeeping Clear Books > https://www.clearbooks.co.uk/ Less Accounting > https://lessaccounting.com/ Zoho Books > https://www.zoho.com/us/books/ Xero > https://www.xero.com/us/

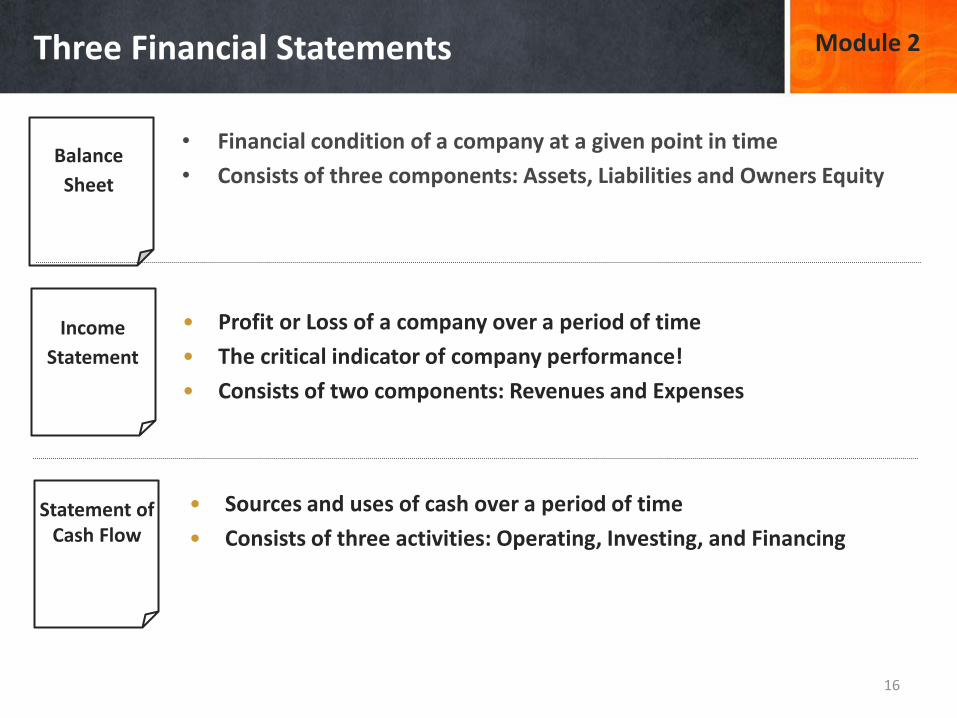

Module 2 Financial Statements

15

Read and understand the three financial

statements associated with your business

Three Financial Statements Module 2

• Financial condition of a company at a given point in time

• Consists of three components: Assets, Liabilities and Owners Equity

• Profit or Loss of a company over a period of time

• The critical indicator of company performance!

• Consists of two components: Revenues and Expenses

• Sources and uses of cash over a period of time

• Consists of three activities: Operating, Investing, and Financing

Income

Statement

Statement of Cash Flow

Balance

Sheet

16

Overview of the Balance Sheet

17

Module 2

The Balance Sheet is prepared as of a Cut Off Date and what-ever the balances are in the Accounts gets compiled and reported under key categories: Current Assets, Long Term Assets, Current Liabilities, Long Term Liabilities and Owners Equity

Balance Sheet – Key Financial Points (Red) Module 2

These accounts should Turnover in the Current Year

18

Long term investments in the business should generate positive returns (Module 5)

Current Assets

Cash 850

Receivables 2,300

Inventories 6,600

Prepaid Insurance 400

Total Current Assets 10,150

Long Term Assets

Furniture and Fixtures 1,950

Vehicle 12,400

Special Equipment 6,450

Intangible - Patent 1,200

Total Long Term Assets 22,000

Total Assets 32,150

Pay attention to key concepts (such as Turnover)as you read and compare the Balance Sheet

Balance Sheet – More Key Points (Red) Module 2

Sufficient Liquidity: Total Current Liabilities should be less than Total Current Assets

19

Be careful – High debt level equates to a high risk of default. Too much debt (Total Liabilities) – Unable to Borrow Money

Currrent Liabilities

Accounts Payable 1,760

Salaries Payable 1,500

Short Term Loan Payable 3,500

Total Current Liabilities 6,760

Long Term Liabilities

Bank Loan on Vehicle 9,800

Total Long Term Liabilities 9,800

Total Liabilities 16,560

Equity

Owners Capital Account 14,690

Retained Earnings 1,100

Owners Withdrawal (200)

Total Equity 15,590

Total Liabilities + Equity 32,150

Income Statement – Covers a Period of Time

20

Module 2

For the entire year

Income Statement – Key Points Module 2

Operating Expenses

Non-Operating Expenses

Non-Operating line items add “noise” to Income

Statements – they can be both revenue and expense 21

Sales Revenues 6,800

Cost of Goods Sold 2,600

Gross Profit 4,200

Selling and Marketing Expenses 1,824

Rent and Utilities 2,600

Administrative Support Expenses 750

Other Operating Expenses 300

Operating Income (1,274)

Interest Expense 81

Special Legal Fee 300

Net Income (1,655)

TOP LINE

BOTTOM LINE

Distinguish Operating vs. Non Operating when presenting the Income Statement

Reporting Cash Flows – Three Categories Module 2

22

Operating Activities

• Cash received from customers

• Payments made to vendors and employees

• Tax payments, rent payments, utilities, etc.

Investment Activities • Invest in Real Estate

• Sell Off Equipment

Financing Activities • Secure Long Term Financing (Loan)

• Distribute Income to Owners

For financial reporting purposes, cash flows have three categories:

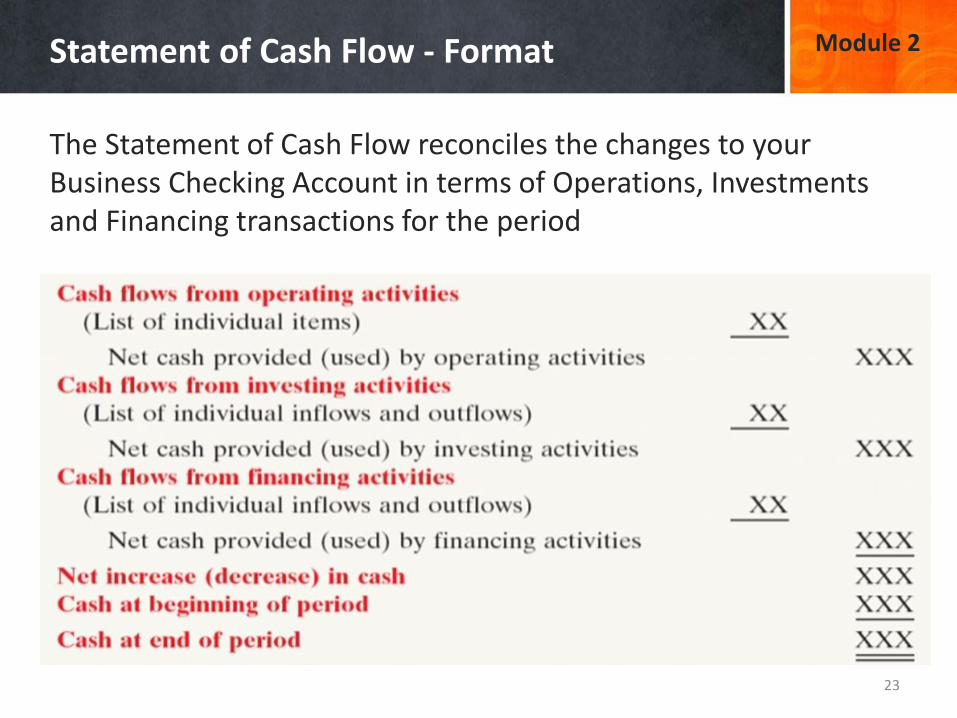

Statement of Cash Flow - Format

23

The Statement of Cash Flow reconciles the changes to your Business Checking Account in terms of Operations, Investments and Financing transactions for the period

Module 2

Statement of Cash Flow – Key Point (Red) Module 2

You eventually want your business to be cash flow positive from its operations so you can avoid having to finance the business from yourself or lenders

24

Exercise 1 – Generate Financial Statements Module 2

25

Close out the accounting period and generate the Balance Sheet per the balances that are outstanding in the various general ledger accounts Two handouts – Financial Statement Template and Account Activity for the Period

Sales is the most important enabler for producing

favorable financial results. You must spend time and

effort on acquiring customers – selling!

Some Important Tax Information

26

Due Dates for 2019 Estimated Quarterly Tax Payments:

Q1: Monday, April 15, 2019 (January – March) Q2: Monday, June 17, 2019 (April – May) Q3: Monday, September 16, 2019 (June – August) Q4: Wednesday, January 15, 2020 (September – December)

Module 2

1. Profits are subject to taxation 2. Most businesses are pass through entities (such as LLC) – Profits

pass through to the Owners who get taxed on the Profits 3. Three forms of taxation on Profits to the Owner(s):

1. State Income Tax (personal tax rate) 2. Federal Income Tax (personal tax rate) 3. Self Employment Tax (12.4% social security + 2.9% medicare)

Some Useful Links – Learning Related

27

Module 2

My Own Online Short Courses: https://exinfm.com/training/ Accounting in One Hour > http://inanhour.com/ Learn Accounting Online > https://www.accountingcoach.com/ Accounting Library > http://www.businessbookmall.com/Accounting%20Internet%20Library.htm Simple Accounting Studies > http://www.simplestudies.com/ Financial Tutorial > http://www.almaris.com/fact/fact-contents.htm Principles of Accounting Online > https://www.principlesofaccounting.com/ Understanding Financial Statements > http://bizzer.com/images/Financial/index.html Take the Fundability Quiz > https://www.businessloans.com/fundability/ How Contributions and Distributions Work for an LLC > https://www.thebalancesmb.com/llc-member-capital-contributions-398638

28

Take a Break

Module 3 Analyze the Financials

29

Apply analytical techniques to your financial

statements to better assess where you stand

Financial Terminology Module 3

30

Cash Flow – The amount of cash receipts and disbursements that flows in and out of the business over time. We want more cash coming in then cash going out.

Debt – Liabilities such as Loans, Mortgages, Bonds, and Commercial Paper (large public corporations). High debt levels equates to high risk.

Equity – The amount of funds invested by owners of the business + profits that are retained by the business for future growth.

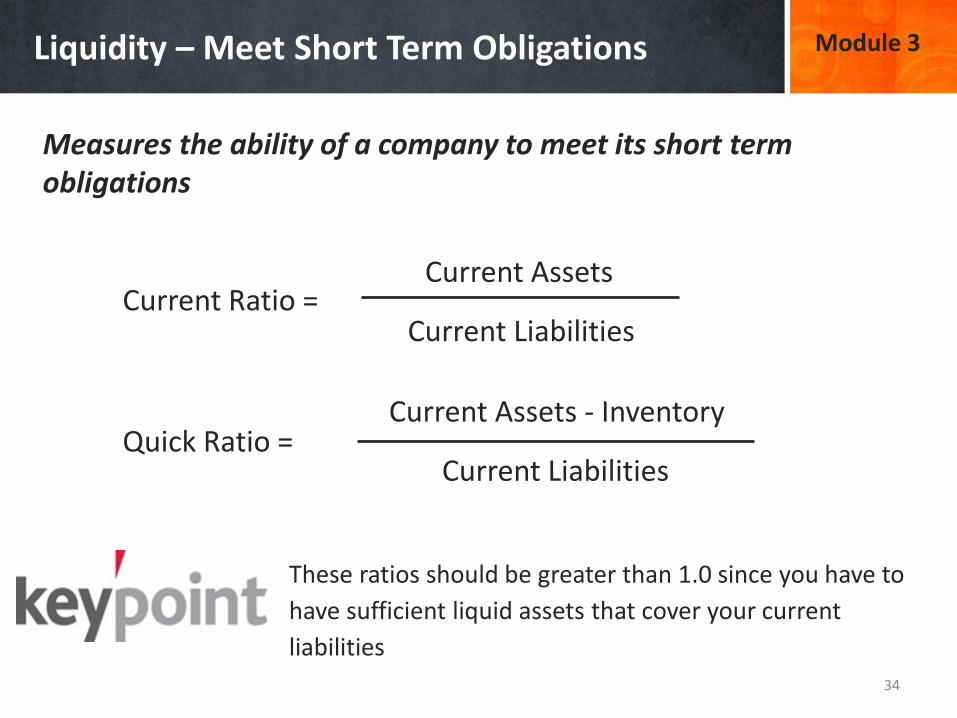

Liquidity – The ability of a company to convert assets into cash for meeting short-term obligations. It is important to have sufficient liquidity to meet your short term obligations.

Leverage – How a company finances its assets; debt vs. equity

Earnings = Net Income = Profits – The residual income remaining after all expenses.

Rate of Return – How much return does the investment generate for the business; residual income after all costs. It is important for long term assets to generate positive returns.

Turn Over – The ability of a company to turn over and convert an asset into something else, such as sales or cash. It is important to turn over current assets into cash.

Working Capital – The funds available to the business within the current operating cycle, expressed as current assets in excess of current liabilities.

Every business owner should be financially smart. This will require an understanding of some important concepts such as:

Important Concept - Turnover Module 3

Any asset that is “current” needs to turnover – the shorter the cycle the better which in turn reduces the need to finance the current operations of the business. Try and collect the money at the Point of Sale – No Need to Collect Money

Accounts

Receivable (Send a bill to the customer)

Cash

Inventory - Appliances

Sale on Credit

Eventually everything will flow through your cash account!

31

Three Useful Analytical Techniques Module 3

32

Ratio Analysis • Divide one number by another number • Easy to benchmark and understand performance Horizontal Analysis • Track Trends over Time • Key Trends include Sales Revenues, Net Income, Debt Levels Vertical Analysis • Track Relationships (between accounts) over Time • Monitor proportion of debt and equity to assets – too much debt equates to

higher risk • Monitor proportion of non-operating expenses to operating expenses – most

of your costs should be operating with minimal non-operating expenses

Analyze a set of financial statements:

Four Types of Ratios Module 3

33

Liquidity Ability to meet short-term

obligations of the business

Leverage Degree to which assets are

financed by debt

Asset Management Management’s ability to manage

assets

Profitability Degree of profitability generated

You need both a Balance Sheet and Income Statement

in order to calculate ratios

Ratios help you measure the following:

Liquidity – Meet Short Term Obligations Module 3

34

Measures the ability of a company to meet its short term obligations

Current Ratio =

Quick Ratio =

Current Assets

Current Liabilities

Current Assets - Inventory

Current Liabilities

These ratios should be greater than 1.0 since you have to

have sufficient liquid assets that cover your current

liabilities

Liquidity Ratio Calculations

35

Module 3

Assets

Cash $ 5,600

Accounts Receivable 12,400

Inventory 39,000

Total Current Assets 57,000

Plant and Equipment 145,000

Real Estate Holdings 55,000

Total Non-Current Assets 200,000

Total Assets 257,000

Liabilities

Accounts Payable 11,500

Long Term Loans Payable 73,000

Total Liabilities 84,500

Equity

Owners Capital 110,000

Retained Earnings 62,500

Total Equity 172,500

Current Ratio

$ 57,000 / $ 11,500 = 5

We have 5 times the current assets that we have in current liabilities

Quick Ratio

( 57,000 - 39,000) / 11,500 = 1.5

Our current liabilities are covered 1.5 times by highly liquid assets

Asset Management Ratios Module 3

36

Use Ratios to measure how well a company manages its current assets

Accounts Receivable Turnover

Sales

Accounts

Receivable

Days Held in Accounts Receivable

A / R Turnover

365 Days

Inventory Turnover

Cost of Goods Sold

Inventory Days Held in Inventory

365 Days

Inventory Turnover

Inventory Ratio Calculations

37

Module 3

Revenues

Sales Revenues $ 620,000

Investment Revenues 115,000

Total Revenues 735,000

Expenses

Cost of Goods Sold 380,000

Assets

Cash $ 5,600

Accounts Receivable 12,400

Inventory 39,000

Total Current Assets 57,000

Inventory Turnover

$ 380,000 / $ 39,000 = 9.7

How often does Inventory turn over during the year?

Number of Days Held in Inventory

365 / 9.7 = 37 days

How many days does it take to convert Inventory into Accounts Receivable?

Measuring Risk (Debt Levels) Module 3

38

Measure the degree to which the company is leveraged in terms of debt and equity

Debt to Equity

Debt to Assets

Total Liabilities

Owners Equity

Total Liabilities

Total Assets

Greater than 100% means company is using more debt than equity – more risk to the company

Greater than 50% means the company is using more debt than equity – more risk to the company

Leverage Ratio Calculations

39

Module 3

Proportion of Debt (Total Liabilities) to Equity in Funding the Business: Debt / Equity or $ 1,000 / $ 500 = 2 (you have 2 times more debt vs. equity) Proportion of Debt used to finance the assets of the business: Debt / Assets = $ 1,000 / $ 1,500 = .67% of financing of assets is in the form of debt (.33% is equity – owner)

Calculate Your Margins Module 3

40

Profit Margin

Net Income

Sales

Operating Margin Sales

Operating Income

Return on Assets

Net Income

Total Assets (1)

Gross Margin

Gross Profit

Sales

(1) Average balances for the year are often used

Know your margins – every industry has an approximate

margin it should generate

Use Ratios to measure profitability and benchmark to your respective industry

Profitability Ratio Calculations

41

Module 3

Gross Margin = $ 98,841 / $ 524,359 = 19% Operating Margin = $ 26,765 / $ 524,359 = 5% Profit Margin = $ 20,166 / $ 524,359 = 4%

Horizontal - Track Your Historical Trends Module 3

42

Another easy way to read and understand financial results is to

look at trends from period to period

2004 2005 2006

Sales Revenues $ 120,000 $ 135,000 $ 146,000

Operating Expenses $ 68,000 $ 73,000 $ 78,000

Net Income $ 22,000 $ 26,000 $ 29,000

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

2004 2005 2006

Sales Revenues

Operating

Expenses

Net IncomeIt can be easier to read trends when you show it graphically

More Examples of Horizontal Analysis

43

Module 3

How are the numbers tracking / trending over time?

Vertical Analysis – Income Statement Module 3

44

Express the balances as a percentage of Total Revenues to size up the breakdown of all line items on the Income Statement

%

Revenues Breakdown

Sales Revenues 4,000.00$ 100%

Total Revenues 4,000.00

ExpensesCost of Goods Sold 1,320.00 33%

Office Supply Expense 680.90 17%

Depreciation Expense 458.33 11%

Interest Expense 278.96 7%

Tax Expense 312.50 8%

Total Expenses 3,050.69 76%

Net Income 949.31$ 24%

Vertical Analysis – Balance Sheet Module 3

45

Percentage Breakdown of all assets

Assets %

Current Assets Breakdown

Cash 32,714.60$ 32%

Accounts Receivable -$ 0%

Inventory 9,680.00$ 9%

Total Current Assets 42,394.60 41%

Long Term Assets

Furniture & Fixtures 6,104.50 6%

Warehouse Facility 55,000.00$

Less Accumulated Depreciaiton 458.33$

Net Warehouse Facility 54,541.67 53%

Total Long Term Assets 60,646.17 59%

Total Assets 103,040.77 100%

Minimize and Turnover

Generate a Return

Vertical Analysis – Balance Sheet Module 3

46

Percentage Breakdown of all liabilities and equity

Liabilities

Current Liabilities

Accounts Payable 591.46 1%

Mortgage Payable - Current 305.81 0%

Total Current Liabilities 897.27 1%

Long Term Liabilities

Mortgage Payable 51,194.19 50%

Total Long Term Liabilities 51,194.19 50%

Total Liabilities 52,091.46 51%

EquityCapital Account 50,000.00 49%

Retained Earnings 949.31 1%

Total Equity 50,949.31 49%

Total Liab + Equity 103,040.77 100%

A Simple Example of Vertical Analysis

47

Module 3

Easy to read the breakdown of relationships within the financial statement when expressed as percentages

Total Sales Revenues = 100% Income Statement Total Assets = 100% Balance Sheet

Benchmark Your Performance Module 3

48

Per the Arlington Public Library, two sources that can help you benchmark are:

RMA (Risk Management Association) Annual Statement Studies – Financial Ratios

2017 Almanac of Business and Industrial Financial Ratios, 48th Edition

1. Know your NAICS Code: 448110 = Men’s Clothing Retail 448120 = Women’s Clothing Retail 448140 = Family Clothing Retail 448150 = Clothing Accessories 448210 = Shoes Retail 448310 = Jewelry Retail 2. Know your size by total assets and total sales

1. Know your Industry Code: 315215 = Clothing Manufacturing 448115 = Clothing Retail Store 2. Know your size by total assets and total sales

http://www.bizstats.com/

Here are some online sources:

https://www.sba.gov/tools/sizeup

NOTE: Exercise 2 will show how to use both of these benchmark sources

Benchmark Your Results

49

Module 3

Do not get too internal when reviewing financial results – compare yourself to your respective industry and / or competition . . . .

Exercise 2 – Calculate Ratios

50

Module 3

Calculate two ratios per the Balance Sheet on this slide: Current Ratio = Current Assets / Current Liabilities Debt / Equity Ratio = Total Liabilities / Total Equity

Exercise 2 – Continued (Benchmark It)

51

Module 3

Now let’s benchmark our calculations – refer to handout: 1. NAICS Code = 448120 2. Size of Business = Under $ 500,000 in Assets

Ratio Your Company (prior slide)

Industry Average

Current Ratio

Debt to Equity

Recognize that key thresholds may apply when you apply for a bank loan: Current Ratio below 2.0 – May not qualify for a bank loan Debt to Equity Ratio above 4:1 – May not quality for a bank loan

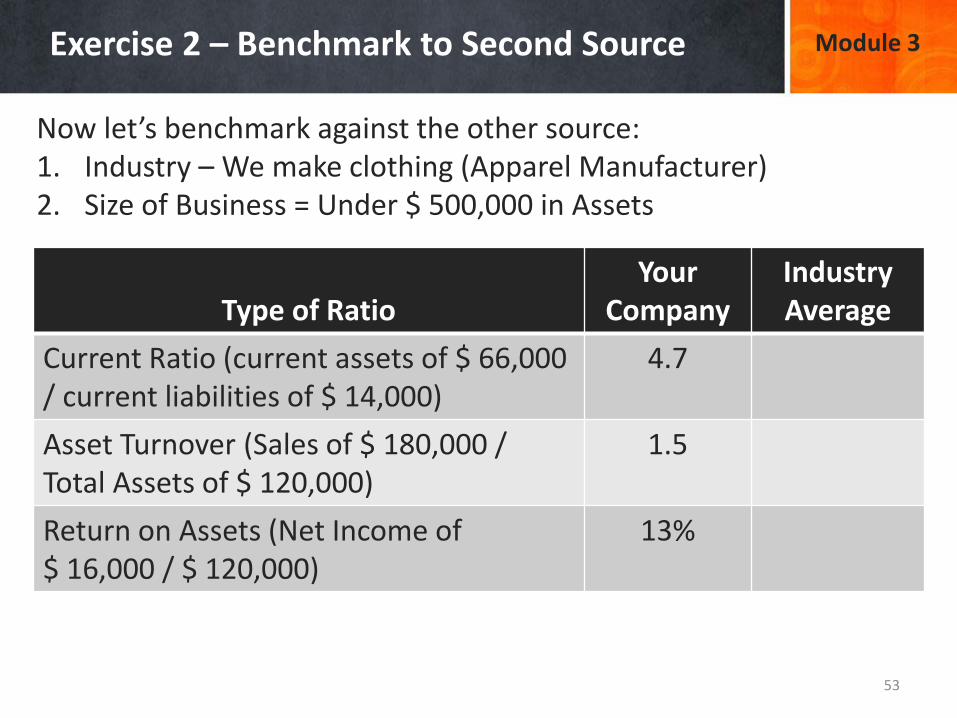

Exercise 2 – Benchmark to Second Source

53

Module 3

Now let’s benchmark against the other source: 1. Industry – We make clothing (Apparel Manufacturer) 2. Size of Business = Under $ 500,000 in Assets

Type of Ratio

Your Company

Industry Average

Current Ratio (current assets of $ 66,000 / current liabilities of $ 14,000)

4.7

Asset Turnover (Sales of $ 180,000 / Total Assets of $ 120,000)

1.5

Return on Assets (Net Income of $ 16,000 / $ 120,000)

13%

54

Recap – Morning Sessions

1. Must have an accounting process to create financial statements 2. Review financial statements at least quarterly – tax payments 3. Current Assets must turnover and go through Cash quickly! 4. Most businesses need a Gross Margin of 40% or higher 5. Three techniques to analyze financial statements:

1. Ratios – One number in relation to another number per the financials

2. Horizontal – Trends over Time 3. Vertical – Percentage breakdown of financials that can be

benchmarked

Breakeven Analysis, Return on Investment, Valuation, Ratio Models, Analyzing the Business

After Lunch:

Module 4 Additional Analysis

55

Additional concepts related to financial analysis

Important Relationships – Income Statement Module 4

56

Sales Revenues (1,645 units sold x $ 26.00 Sales Price) . . . . . . . . . . . . . $ 42,770 Less Direct Cost (1,645 units sold x $ 18.00 Unit Cost) . . . . . . . . . . . . . . . 29,610 Gross Profit or Margin . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,160 Less Indirect Cost: Sales and Marketing Expenses . . . . . . . . . . . . . . . . . . . . . . . . . . 2,350 Administrative Salaries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,450 Rent and Utilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,780 Insurance and Legal Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,200 Depreciation Expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 900 Other Miscellaneous Expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . 760 Profit or (Loss) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2,720

Direct Cost varies with sales whereas Indirect Cost tend to

be fixed – same month to month regardless of what you

sell. Direct Cost tend to be Variable whereas Indirect Cost

tend to be Fixed

Cost Analysis Module 4

Sales Volume

Cost Variable

Fixed

Variable Cost – Varies or changes with changes in sales. Includes production labor, raw materials and various discretionary items such as advertising.

Fixed Cost – Remains the same regardless of activity levels. Tends to be long-term commitments or non-discretionary items such as Rent, Insurance, Interest, Depreciation and Senior Management Salaries.

A scalable business is one where you increase the volume sold and you see lower marginal cost. If your sales grow and your total cost continue to go up, you do not have a scalable business

57

Know Your Breakeven Point Module 4

Simple Concept: How much business do I have to do to breakeven (recover all of my costs)?

Breakeven Volume = Fixed Costs / (Sales Price – Variable Cost per Unit)

Breakeven Sales Amount = Fixed Costs / Contribution Margin Ratio

Contribution Margin Ratio = (Sales Price – Variable Cost) / Sales Price

EXAMPLE: Sales Price = $ 45.00 per shirt | Materials = $ 6.00 per shirt + Labor = $ 9 per shirt + Variable Overhead = $ 3 per shirt = Total Variable Cost per Unit of $ 18.00

$ 70,470 of costs are incurred no matter how much you sell

Breakeven Units = $ 70,470 / ($ 45.00 - $ 18.00) = 2,610 shirts must be sold

Contribution Margin = $ 27.00 / $ 45.00 = 60%

Breakeven Revenues = $ 70,470 / .60 = $ 117,450 (2,610 units x $ 45.00)

58

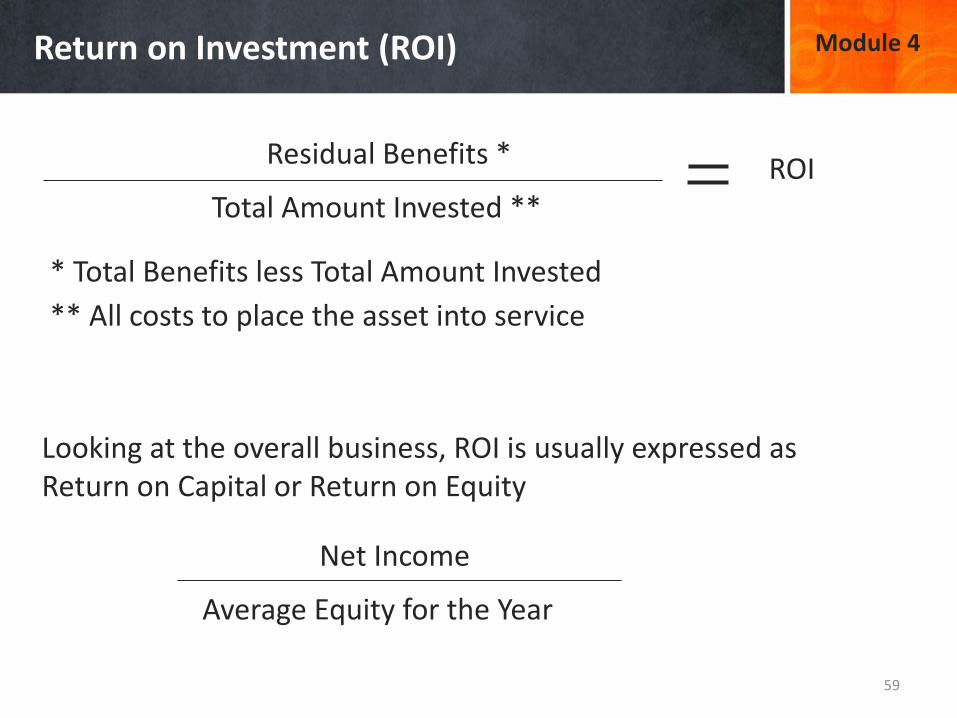

Return on Investment (ROI) Module 4

59

Residual Benefits *

Total Amount Invested **

Looking at the overall business, ROI is usually expressed as Return on Capital or Return on Equity

ROI

Net Income

Average Equity for the Year

* Total Benefits less Total Amount Invested

** All costs to place the asset into service

Quantify the Future Benefits Module 4

Organizational Benefits Builds company reputation Creates new customer opportunities Fosters company vision and mission Improves market position relative to competitors Improves the ability to serve customers Increases competitiveness Financial Benefits Creates additional/new revenue Creates cost savings through tax avoidance Enables cost avoidance Faster return on investments Increases cash flow Increases profitability of existing products/services Increases revenue of existing sources Increases stock price/shareholder value Lowers cost of production Lowers cost of servicing

Operational Benefits Decreases employee work loads for undesirable work Eliminates non-value added activities Improves employee morale / team spirit Improves internal communication Improves use of workspace Reduces cycle time Reduces cycle time of production/process Reduces external inputs to processes Reduces person-hours Reduces process steps

Information Technology Benefits Decreases maintenance/support costs Improves application/system performance Improves application/system utilization rate Increases efficiency of support activities Increases productivity through automation Reduces paper documentation requirements Strengthens application/system security

Identifying costs (outflows) is fairly straight-forward. Trying to quantify the benefits (inflows) can be very challenging. Examples of benefits include:

60

Simple Example of ROI Module 4

61

Proposed new marketing program cost $ 200,000. It will give the company much more exposure to new potential customers. Past programs have proven to increase a company’s revenues by 5% over a three year period. What is the Rate of Return for this investment?

Step 1 - Quantify the Benefits: Estimated Annual Revenues (next 3 years) are $ 1,600,000 x 5% = $ 80,000 benefits per year x 3 years = $ 240,000 Total Benefits (NOTE: Conservative Estimates are best used on the Benefit Side – Subjective and prone to error) Step 2 – Quantify all of the Costs: Total investment cost is up front, one time fee of $ 200,000 Step 3 – Calculate the ROI: Total Benefits of $ 240,000 - $ 200,000 costs = $ 40,000 residual benefits divided by $ 200,000 = 20% ROI

Returns Must Exceed Cost of Capital Module 4

62

All businesses have a cost of financing the business:

1. Cost of Debt – Interest Payments on Loans

2. Cost of Equity – Owners expect to get a return on what they’ve invested into the business

Cost of Capital = Cost of Debt + Cost of Equity

Cost of Capital Create Value

Destroy Value

Returns on Investment (ROI)

10%

12%

14%

16%

8%

6%

Exercise 3 – What is the ROI? Module 4

63

You are thinking about investing in a new vehicle to improve sales delivery for your food business. The initial investment required is $ 23,450 and you do expect some operating cost each year of about $ 3,150 per year for paying the driver, insurance, gas, and repairs. You have estimated that the delivery of food could really boost your sales each year over the next 5 years as follows: Year 1 - Increase in Sales $5,000 Year 2 - Increase in Sales $7,500 Year 3 - Increase in Sales $9,500 Year 4 - Increase in Sales $11,000 Year 5 - Increase in Sales $10,000

Add up all the money you have to pay out – Day 1 investment + all the cost each year. Compare to the total benefits (Sales). What is the residual benefit? Divide the Residual Benefit by the Total Investment = Return on Investment

Module 5 Evaluating Long Term

Investments

64

How to evaluate the economics of a long term

investment

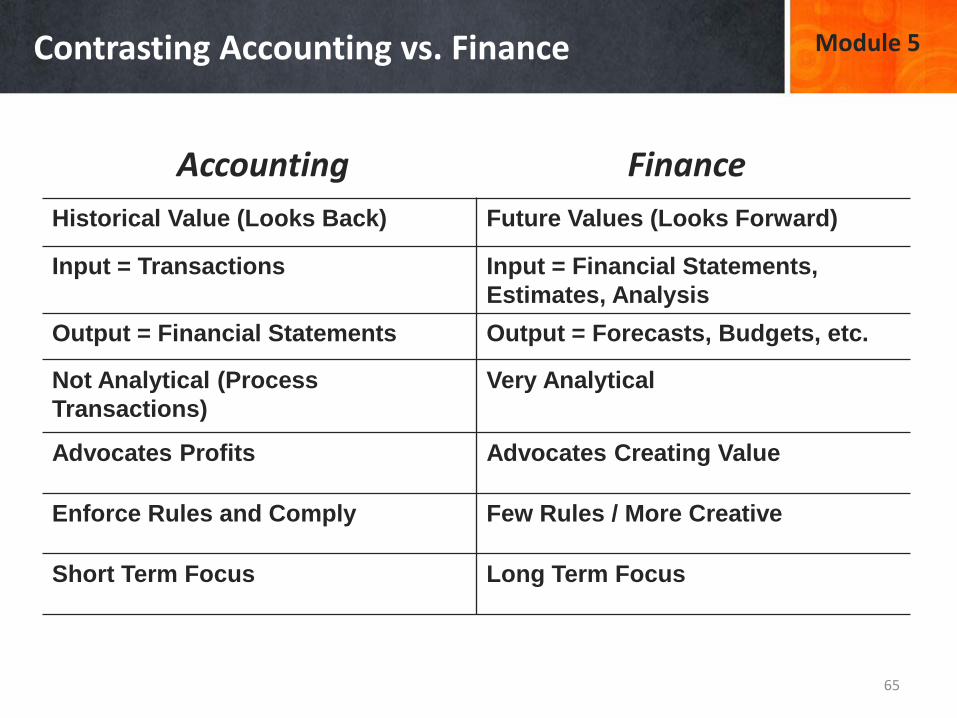

Contrasting Accounting vs. Finance Module 5

65

Accounting Finance

Historical Value (Looks Back) Future Values (Looks Forward)

Input = Transactions Input = Financial Statements,

Estimates, Analysis

Output = Financial Statements Output = Forecasts, Budgets, etc.

Not Analytical (Process

Transactions)

Very Analytical

Advocates Profits Advocates Creating Value

Enforce Rules and Comply Few Rules / More Creative

Short Term Focus Long Term Focus

What is the Value Today? Module 5

66

Accounting

Historical

Values

Constant Dollars –

does not change

over time

Why the differences in value (Accounting vs. Finance)?

1. Risk – I promise to pay you $ 100,000 five years from now!

2. Inflation - $ 100,000 five years from now will lose purchasing power!

3. Opportunity Cost – If you had $ 100,000 now (not five years from now), you could do something with it – lost opportunity!

Finance

Present

Values

What is the value

today?

Future

Values

What is the value

tomorrow?

67

Three Economic Criteria Module 5

Three important economic indicators in finance for evaluating long term investments:

1. Return on Investment – We discussed this earlier > Investors must earn a rate higher than the cost of capital; otherwise the investment is not attractive.

2. Net Present Value – Discount the cash flows of both the costs and the benefits of the investment. The more positive the value, the more attractive the investment.

3. Discounted Payback Period – How long does it take for the investor to recover his investment. The shorter the payback, the more attractive the investment.

68

Simple Example of Discounting Module 5

Three Important Steps:

1. Identify the cash inflows (benefits) and cash outflows (costs) over the useful life of the investment

2. Identify your cost of capital

3. Discount the cash inflows and outflows using your cost of capital

i = 8% Year 1 Year 2 Year 3 Totals

Inflows $ 120,000 $ 84,000 $ 36,000 $ 240,000

Outflows $ (200,000) $ - 0 - $ - 0 - $ (200,000)

Difference $ (80,000) $ 84,000 $ 36,000 $ 40,000

Discount .9259 .8573 .7938

Present Value $ ( 74,072) $ 72,013 $ 28,576 $ 26,517

Net Present Value

69

Discounted Pay Back Period Module 5

A simple economic indicator – when will I recover all of my costs?

Net

Present Cumulative

Year Value Value

1 (74,072)$ (74,072)$

2 72,013$ (2,059)$

3 28,576$ 26,517$

You reach pay back in Year 3 for this investment

Per the Previous Slide

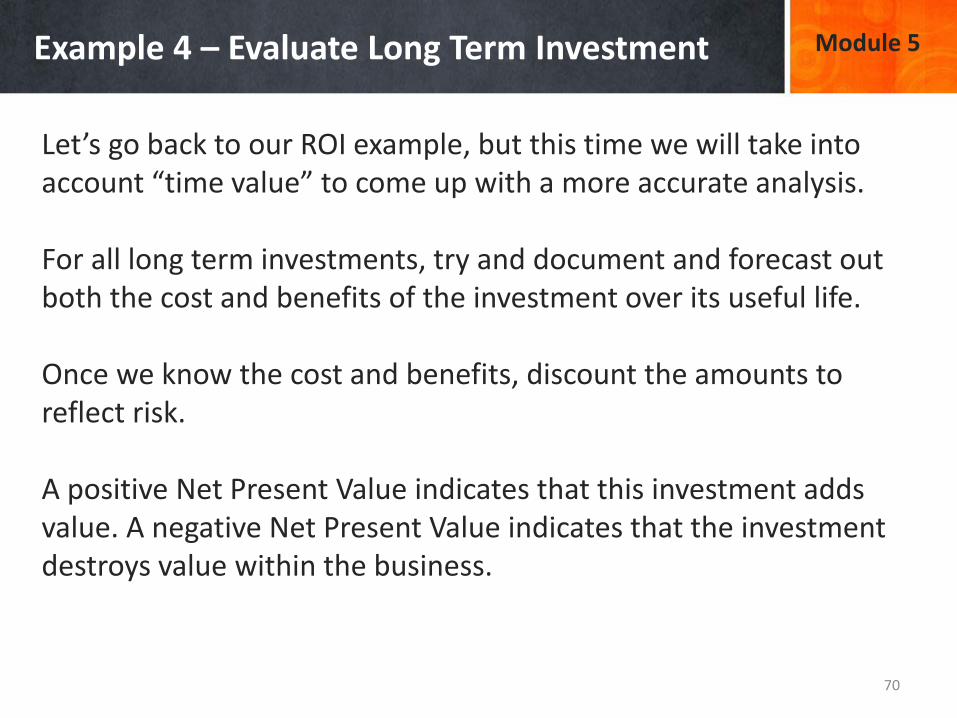

Example 4 – Evaluate Long Term Investment Module 5

70

Let’s go back to our ROI example, but this time we will take into account “time value” to come up with a more accurate analysis. For all long term investments, try and document and forecast out both the cost and benefits of the investment over its useful life. Once we know the cost and benefits, discount the amounts to reflect risk. A positive Net Present Value indicates that this investment adds value. A negative Net Present Value indicates that the investment destroys value within the business.

71

Take a Break

Module 6 Some Advanced Concepts

72

A few advanced concepts related to financial

management

Manage Your Cash Flow Module 6

73

1. Put Emphasis on Selling – Sales cures all and you must capture

customers and convert them into sales to generate cash flow.

2. Forecast your cash inflows and outflows based on past history or what

you expect to incur month to month

3. Be aggressive in collecting money owed to you

4. Be aggressive in reducing your cash expenses:

a. Labor – Use temporary or part-time workers unless you can justify

full time employees

b. Office – Use your home or shared office spaces as opposed to a

formal expensive office

c. Purchases – Buy used as opposed to new and purchase only

minimum quantities until you can justify larger quantities

d. Insurance – Don’t over-insure the business, accept the risk until you

can afford complete insurance coverage

e. Bootstrap – Use free resources as much as possible such as social

media for marketing

Working Capital for Day to Day Operations Module 6

74

2016

Days in Receivables (per slide 25) 51

Days in Inventory (per slide 26) 59

Operating Cycle in Days 110

Less Accounts Payable (1) -33

Days to be Financed 77

(1) Days in Accounts Payables = 365 / Accts Payable Turnover

Accounts Payable Turnover = Total Purchases / Avg A/P Balance

A/R Held 1 Day (1/365 x Credit Sales for Year) 5,917$

Inv Held 1 Day (1/365 x Cost of Goods Sold for Yr) 22,575$

A/P Held 1 Day (1/365 x Purchases for Year) 3,150$

Most businesses cannot cover normal operating cycles. They must cover the short fall through high enough margins. In this example, if the company can turn the inventory over faster from 59 days to 55, this equates to $ 90,300 of more cash on hand for current operations ( 4 days x $ 22,575)

Working Capital represents the current funds to cover day to day operations and it comes from the excess of Current Assets over Current Liabilities

75

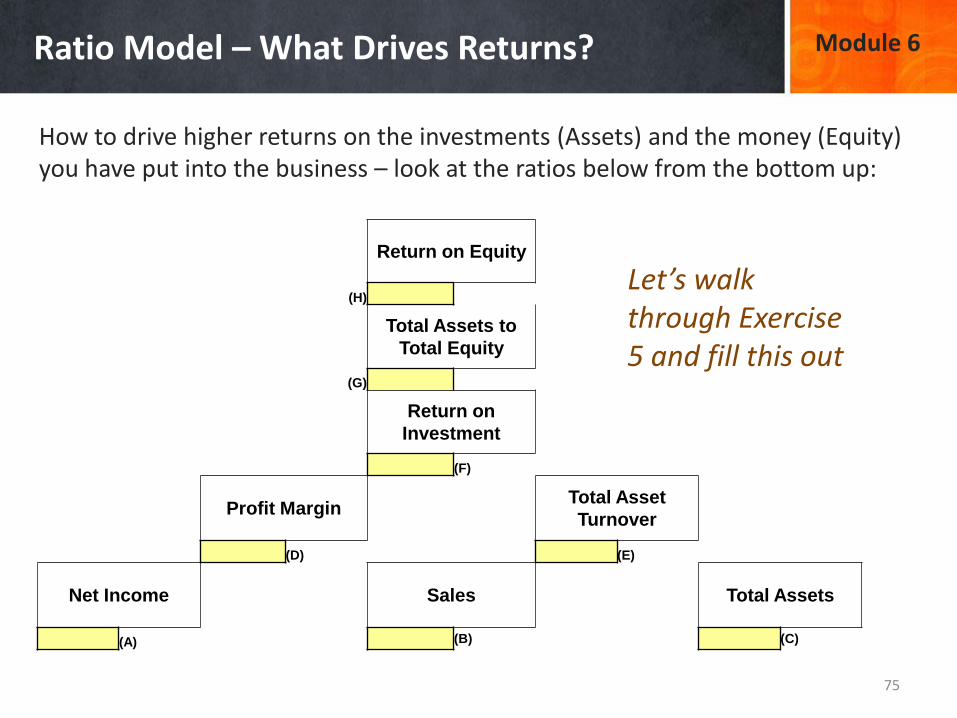

Ratio Model – What Drives Returns? Module 6

How to drive higher returns on the investments (Assets) and the money (Equity) you have put into the business – look at the ratios below from the bottom up:

Return on Equity

(H)

Total Assets to

Total Equity

(G)

Return on

Investment

(F)

Profit Margin Total Asset

Turnover

(D) (E)

Net Income Sales Total Assets

(A) (B) (C)

Let’s walk through Exercise 5 and fill this out

76

Ratio Model – Sustainable Growth Module 6

77

Ratio Model – Financial Distress Module 6

Very predictive of financial distress and bankruptcy:

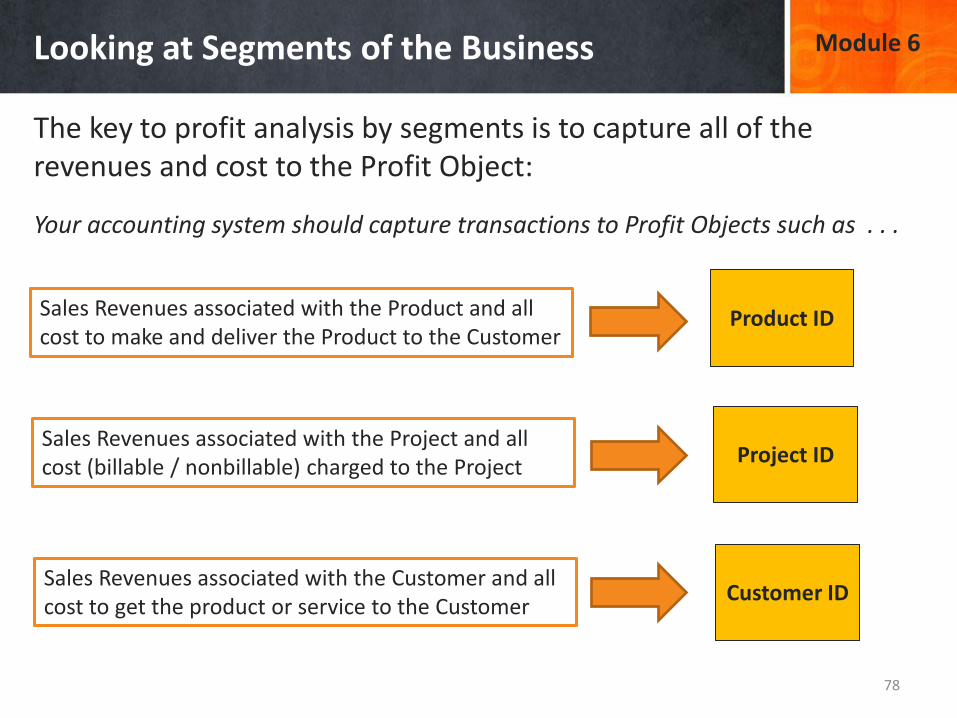

Looking at Segments of the Business Module 6

78

The key to profit analysis by segments is to capture all of the revenues and cost to the Profit Object:

Product ID

Project ID

Customer ID

Sales Revenues associated with the Product and all cost to make and deliver the Product to the Customer

Sales Revenues associated with the Project and all cost (billable / nonbillable) charged to the Project

Sales Revenues associated with the Customer and all cost to get the product or service to the Customer

Your accounting system should capture transactions to Profit Objects such as . . .

Financial Performance by Segments Module 4

Store A Store B Store C Store D

Sales 100% 100% 100% 100%

Cost of Goods Sold 46% 51% 42% 55%

Gross Margin 54% 49% 58% 45%

Operating Expenses 34% 27% 36% 31%

Operating Margin 20% 22% 22% 14%

Non Operating Expenses 7% 7% 9% 11%

Profit Margin 13% 15% 13% 3%

Your accounting system should be able to generate statements by location

You should be able to slice / dice sales a number of ways (product, customer, etc.)

Quarterly Sales Summarized by Type

Customer Type 2016-Q1 2016-Q2 2016-Q3 2016-Q4

Young Women (under 30) 1,159$ 1,089$ 965$ 1,105$

Young Men (under 30) 905$ 1,106$ 875$ 982$

Mid Women (31 - 55) 2,605$ 2,560$ 2,678$ 2,811$

Mid Men (31 - 55) 1,230$ 1,289$ 1,246$ 1,328$

Older Women (> 55) 633$ 606$ 584$ 621$

Older Men (>55) 455$ 460$ 403$ 479$ 79

Cost Reduction thru Process Improvement Module 6

80

Traditional approach to Cost Control – by General Ledger:

Better approach is to improve the Process!

General Ledger Account Balances

Year End Expense Accounts

Account Description Balance

4001 Cost of Goods Sold * 3,166,401.50

4003 Marketing & Promotion 377,560.00

4005 Salary Expense 474,906.82

4006 Payroll Tax Expense 86,089.15

4007 Equipment Maintenance 36,450.92

4009 Rent & Lease Expense 19,807.65

4011 Utilities Expense 11,050.86

4012 Insurance Expense 7,650.00

4014 Product Warranty Expense 6,672.00

4015 Depreciation Expense 22,880.00

4016 Interest Expense 26,404.20

4017 Tax Expense 101,678.89

Total Expenses 4,337,551.99

* consists of direct materials + direct labor + allocation of overhead

• Eliminate non-value added type activities (“Re” type activities)

• Compress hand-off’s in workflows

• Look for delays, wait times, waste, defects, holding inventory, etc.

• Too many manual processes – invest in technologies

• Look at how people spend their time – should be spent servicing an internal or external customer

Valuations – What is Your Business Worth?

81

Module 6

Most small businesses get valued based on the Operating Cash Flow – commonly calculated off the Income Statement as follows . . . . . . . .

Earnings or Net Income $ 1,850

Interest Expense (1) + 300

Taxes (1) + 420

Depreciation (2) + 160

Amortization (2) + 70

Earnings Before Interest Taxes

Depreciation Amortization or EBITDA

$ 2,800

(1)Not directly related to the actual operations of the business

(2)Not an actual disbursement of cash

Add Back

Valuations – Apply a Multiple

82

Module 6

Sales ($millions)

5 150 500 1,000

Small Lower Middle Upper Large

Businesses M I d d l e M a r k e t Companies

2-3x 4-7x 8-9x 10-11x >12x

5.4MM 300,000 2,000

Depending upon the size of the business (Total Annual Sales Revenues), the multiple will vary as applied to the Benefit Stream (EBITDA) and this is what your business is worth

Exercise 4 - Valuation

83

Module 6

Referring to the Income Statement to the right and with the assumption that a business of your size and your industry typically sells for 4 times its EBITDA number, what is your business worth?

Intellectual Capital

84

Module 6

Increasingly, the value or worth of a business is driven by assets that do not show up on the Balance Sheet – Intellectual Capital:

Keys to Growing Intellectual Capital (IC)

85

Module 6

Three major areas of Intellectual Capital that touch most businesses. Three M Rule: Measure, Manage, and Maximize your IC

Major IC

Category

IC Description Measure to Grow

(Appreciate IC)

Human Capital Value of a business that is

contained in the skills, abilities

and talents of its people.

Level of Competency,

Level of Experience,

Advanced Certifications

Organizational

Capital

Value of a business that is

contained in the processes,

systems, patents, trademarks,

reputation, innovation, etc.

Process Turn Around

Times, % of Innovative

Ideas Implemented, # of

Patents Licensed, etc.

Relational Capital Value of a business contained in

its relationships with customers,

suppliers, other businesses,

government, etc.

Customer Retention

Rate, Satisfaction

Surveys, Supply Chain

Metrics with Vendors,

Broader View of Metrics

86

Module 6

Measurement Area => Customer Service (Price, Delivery, Support, Satisfaction). Metric Examples => Price comparisons to competition, number of on-time deliveries, response times, customer complaints, number of product returns, customer survey results, service awards, etc.) Measurement Area => Internal Operations (Efficiency, Costs, Production, Inventories). Metric Examples => Cycle times, inventory turnovers, defect rates, plant utilization, targets met, unit cost compared to competition, overhead trends, etc. Measurement Area => Innovation (New Products, Technology, R & D). Metric Examples => Number of new products, number of patents, new technologies adopted, system improvements implemented, etc. Measurement Area => Financial (Profitability, Growth, Value). Metric Examples => Sales Growth Rate, Gross Margin, Operating Cash Flow, Return on Equity, Return on Investments in Assets

Measure the Non Financial Parts of the Business - Critical to driving Financial Results. This allows you to be more pro-active on performance issues:

Metrics for Different Business Models

87

Module 6

Recap and Key Points

88

Module 6

1. Once you understand Ratios, you can leverage this approach through Ratio Models to gain key insights on how to run the business. a. How many days do I have to finance the business? b. What is a sustainable growth rate for the business? c. Is this business bankrupt?

2. Segment your Customers, Products, Projects – What segment is the most and least profitable?

3. Cut cost through elimination of work, not the workers. Time is what drives cost – how can we do this with less effort?

4. All business owners should have some grounding in how their business gets Valued. This is your basis for Retirement!

5. Intellectual Capital is now critical to increasing the value of most businesses

89

Module 7 Business Analysis

Solving Business Problems Module 7

90

What are the most important issues? Pareto Analysis

How does my industry work?

What is our current situation?

What performance areas are weak?

Porter’s Five Forces

SWOT

Benchmarking

How well do we manage our products / services? Boston Growth Matrix

GE Business Screen How well do we manage our different businesses?

What is causing this problem? Root Cause Analysis

There are a wide range of analytical models that you can use to solve key business questions. Here are some examples:

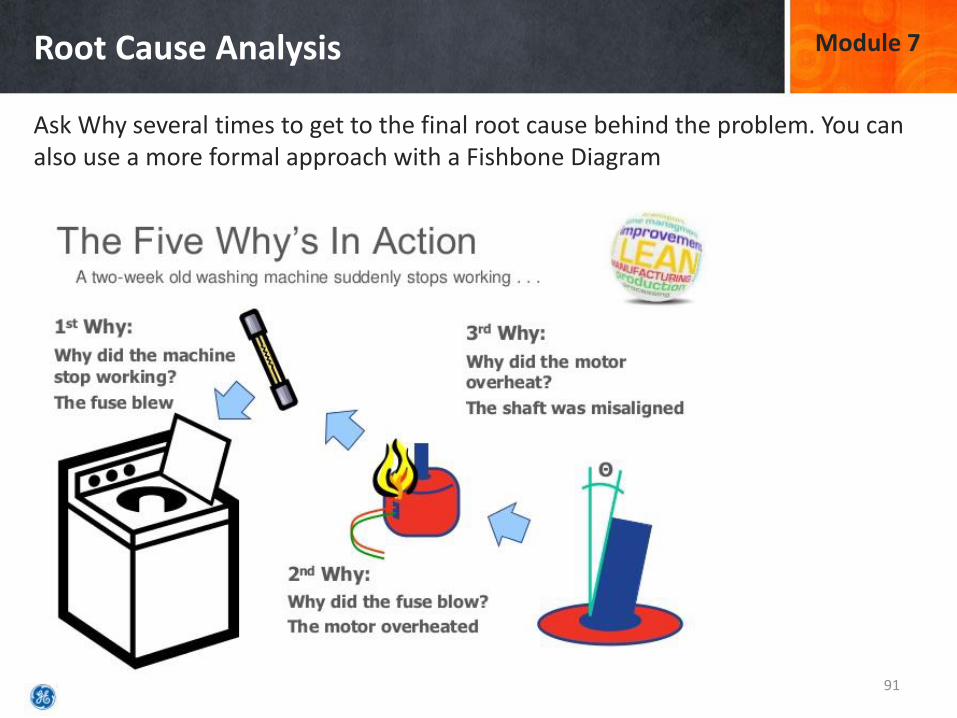

Root Cause Analysis Module 7

91

Ask Why several times to get to the final root cause behind the problem. You can also use a more formal approach with a Fishbone Diagram

Example of Root Cause Analysis

92

https://www.youtube.com/watch?v=BEQvq99PZwo

Module 7

The Jefferson Memorial shows how you might have to go through root cause analysis more than once to finally get to the source of your problem:

Most Popular Analytical Model - SWOT Module 7

93

Internal Assessment of the organization, its people, services, competencies, etc.

External Assessment of direct and indirect forces, social, economic, political, etc.

Client has a global infrastructure to

service all types of customers

Strengths Weaknesses

Services are in high demand in most

parts of the world

Client has limited resources for

expanding its global reach

Key processes are not very cost competitive

when compared to other service providers

Untapped demand exists in almost half

of the World

New Technologies make it possible to

expand service reach

Other clients are investing in newer

technologies

Some clients are entering into strategic

partnerships to expand their global

footprint

Threats Opportunities

It is important to periodically assess your current situation. This is best done using the SWOT Model

A very good instructional video: https://www.youtube.com/watch?v=I_6AVRGLXGA

Industry Analysis – Porter’s Five Forces Module 7

94

If you want to fully understand your industry, look at five different forces that define your industry:

Example – Porter’s Five Forces Module 7

95

McDonald’s (MCD) and the Fast Food Industry might look like this:

Categorize Your Products – Boston Matrix Module 7

96

1. Stars – Products with high growth rates and strong market position. Want to invest heavily and grow these aggressively.

2. Question Marks – Products with high growth rates, but market share is small. Invest heavily, but monitor closely to see if you can secure solid market share. Goal is to move these to the Star category.

3. Cash Cows – Products are mature and not growing, but they have a very secure and steady market. Invest modestly to sustain.

4. Dogs – Products with low market share and very low growth. Hard to sustain – Unless you can grow and improve, you should divest and remove these products.

Not all products or service lines are the same. You should regularly review each on its own and see which ones to keep and which ones to discontinue. Boston Consulting Group has a four quadrant matrix that many companies use.

Example – Boston Matrix Module 7

97

Pareto Analysis – 80 / 20 Rule Module 7

98

Categories

Causes, Products, Mfg. Lines, Operators Machines, Defect Types, etc. D

ow

nti

me,

Err

ors

,

# o

f E

mp

loy

ees,

etc

.

Allocate your limited resources to the few items that represent the largest portion of the entire population

Spend your time and resources where it matters the most. Pareto Analysis forces you to apply a measure to a set of objects, helping you understand where to focus

Example of Pareto Analysis

99

Module 7

Where should we allocate our limited school budget in accordance with complaints submitted?

3 complaints (broken branches, fans not working and bad atmosphere) make up 57% of total complaints

Multiple Choice Question

100

Module 7

Every year, it is recommended that every business do an assessment where it stands and renew its strategy for the up coming year. Which of the following analytical models would you apply to address this task?

a. Porter’s Five Forces b. Root Cause Analysis c. SWOT Analysis d. Pareto Analysis

Recap – Business Analysis

101

Module 7

1. Be Proactive – Solve your problems BEFORE it shows up on the financial statements. This requires a very analytical approach to running the business.

2. Three Step Process: 1. Define the Problem 2. Select the right Analytical Model 3. Apply the Analytical Model

3. Non Financial Parts (Customer, Processes, etc.) drive financial results. Don’t just measure financial results – measure your non financial parts. Examples: 1. Customer Satisfaction Survey 2. Process Efficiency 3. Product Quality 4. Employee Turnover Rate

Wrap Up

102

Summarize Key Points

103

1. Someone must keep the books – you must do accounting to understand if you are losing or making money.

2. Generate and review your financial statements on a monthly or quarterly basis

3. Analyze the financial statements with ratios, horizontal and vertical analysis – be analytical in how you look at numbers

4. Current Assets must turn over and go through cash 5. Long Term Assets must generate a Return greater than the cost to finance the

investment 6. Benchmark the financials to evaluate your financial performance according to

your industry (NAICS) code 7. Evaluate your long term investments – does it generate benefits greater than

the cost and if the life cycle is several years, consider discounting at the cost of financing or required return to see what the investment is worth to the business. This is what big companies do when they make major investment decisions.

Summarize Key Points - continued

104

8. You can leverage the use of ratios within certain models to help manage key financial goals

9. It is helpful to assess profits by key segments of the business such as products, customers, locations, etc.

10. Business owners should ultimately try and increase the value of the business. Value is determined based on a benefit stream such as EBITDA with a multiple applied.

11. Increasingly it is the Intellectual Capital of the business that drives performance and value.

12. You can solve a wide range of business problems through the application of analytical models such as SWOT, Pareto Analysis, and Root Cause Analysis.

Some More Useful Links (More Advanced)

105

Finance and Accounting Seminars > https://www.seminarinformation.com/search.cfm?tp=7 Teach Me Finance > http://www.teachmefinance.com/ Finance World > http://web.utk.edu/~jwachowi/wacho_world.html Study Finance > http://www.studyfinance.com/ Principles of Finance > http://educ.jmu.edu//%7Edrakepp/principles/

106

DC SCORE Mentors with a Financial Background: Matt H. Evans – Silver Spring Library | Phone: 240-773-9420 [email protected] Len Briskman – Rockville Library | Phone: 240-777-0001 [email protected] Diane Starkey – Wheaton Library | Phone: 240-777-0678 [email protected] Mariann Zylstra – Gaithersburg, MD | Phone: 240-618-9263 [email protected] Mike Kipp – Ashburn, VA | Phone: 202-619-1000 [email protected]