Languages

Pages

Legal

Deferred Tax Project Team 7

Marcus Wong | Randy Lennard Cheong Adwyna Yeong | Choo Zi Lin | Kumari Sonam

Tornado Ltd

(“TL”)

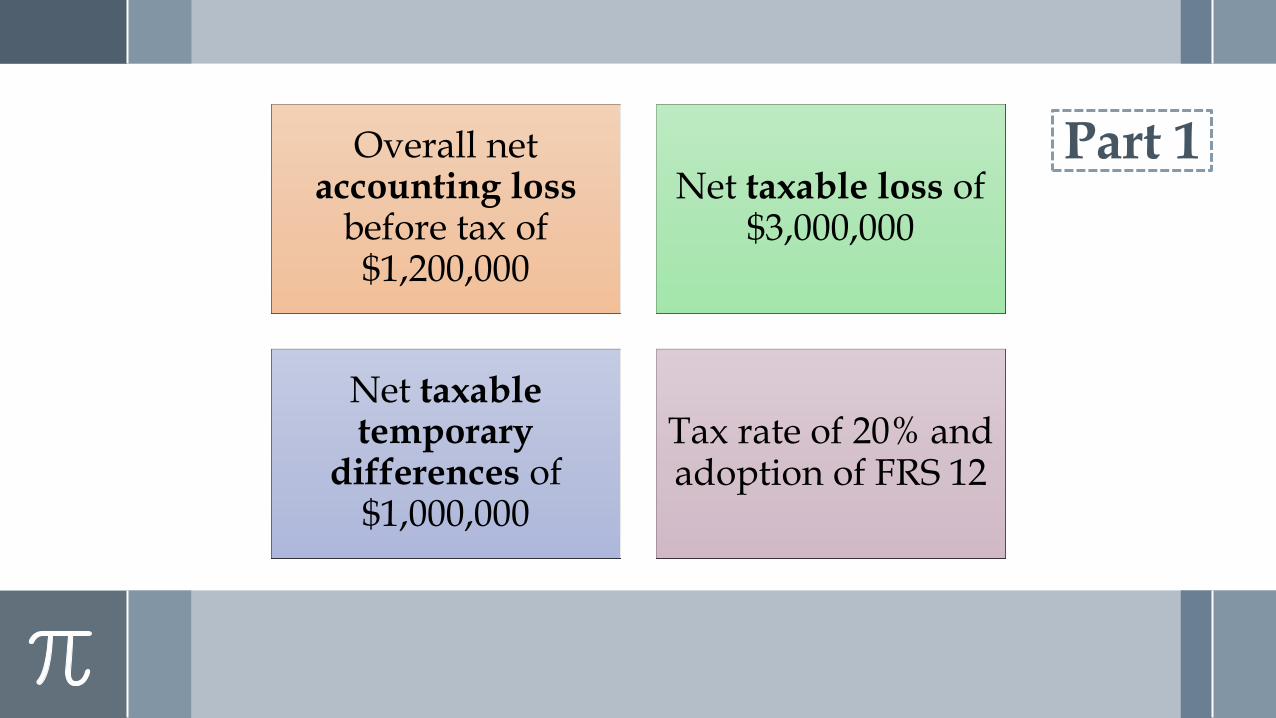

Part 1

Overall net accounting loss

before tax of $1,200,000

Net taxable loss of $3,000,000

Net taxable temporary

differences of $1,000,000

Tax rate of 20% and adoption of FRS 12

Part 1

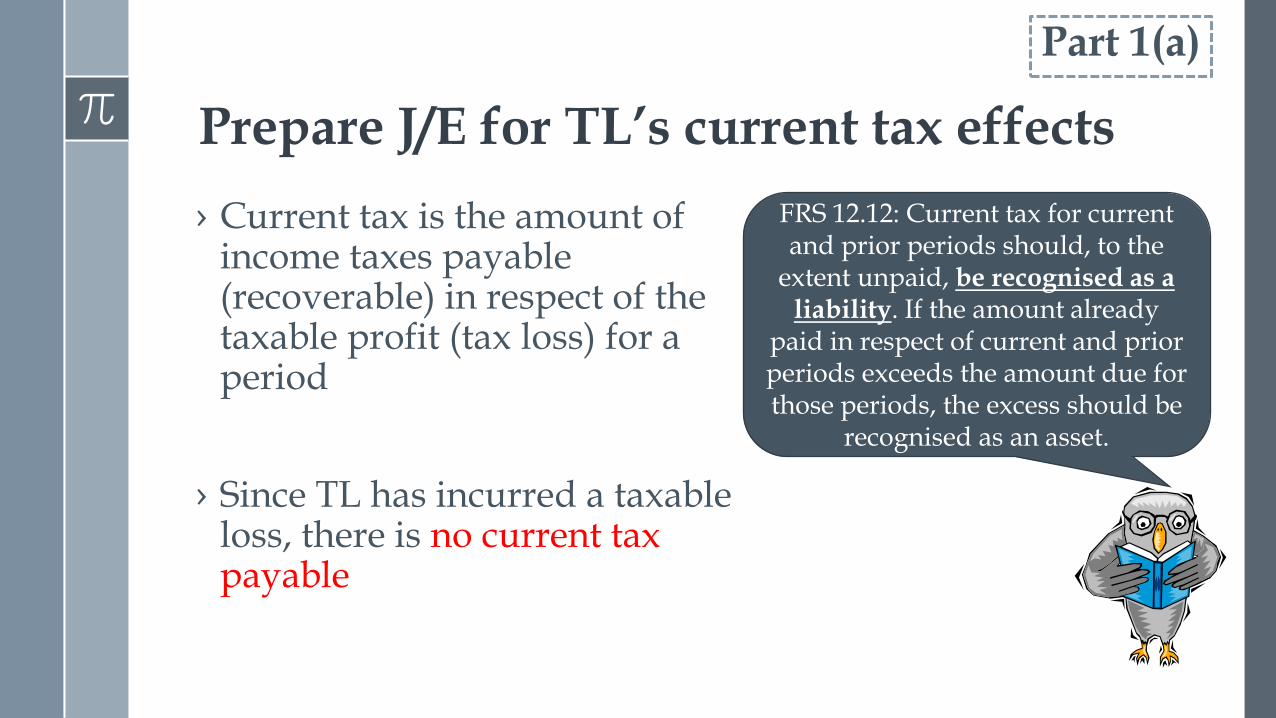

Prepare J/E for TL’s current tax effects

FRS 12.12: Current tax for current and prior periods should, to the

extent unpaid, be recognised as a liability. If the amount already

paid in respect of current and prior periods exceeds the amount due for those periods, the excess should be

recognised as an asset.

› Current tax is the amount of income taxes payable (recoverable) in respect of the taxable profit (tax loss) for a period

› Since TL has incurred a taxable loss, there is no current tax payable

Part 1(a)

Date Particulars Debit Credit

31/12/20x1 Tax Receivable (20%*3,000,000)

600,000

Tax Income 600,000

To record current tax receivable

Part 1(a)

Prepare J/E for TL’s current tax effects

› As per FRS 12, since tax losses are allowed to be carried forward to subsequent years, TL would have tax savings upon utilisation of the losses c/f

It is probable that there will be future taxable profits. Explain how TL should

account for its unused tax loss

› Recognition Probable flow of future taxable profits

No indication of history of losses (cannot apply FRS 12.35)

A DTL to be recognised immediately on the TTD of $1,000,000

A DTA must be recognised

But to what extent?

Part 1(b)

FRS 12.34: A deferred tax asset should be recognised for the carryforward of unused tax losses … to the extent that it is probable that future taxable profit will be available against which the unused tax losses … can be utilised.

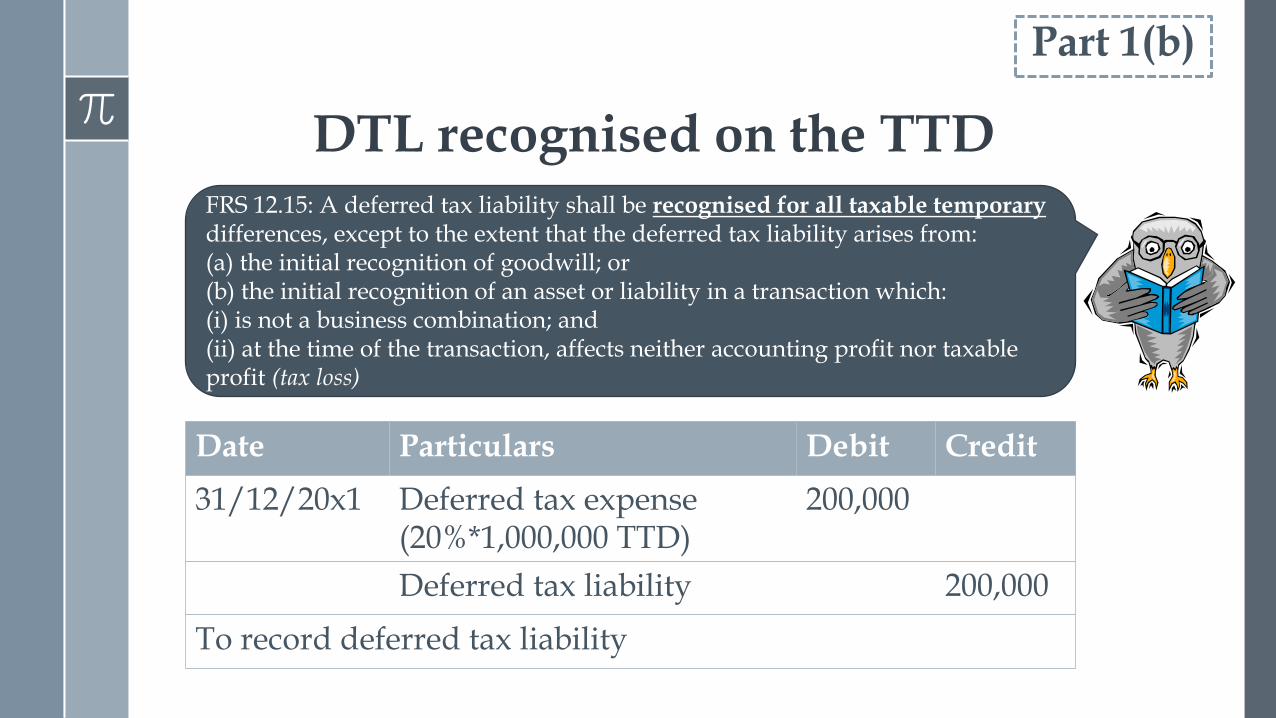

DTL recognised on the TTD FRS 12.15: A deferred tax liability shall be recognised for all taxable temporary differences, except to the extent that the deferred tax liability arises from: (a) the initial recognition of goodwill; or (b) the initial recognition of an asset or liability in a transaction which: (i) is not a business combination; and (ii) at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss)

Date Particulars Debit Credit

31/12/20x1 Deferred tax expense (20%*1,000,000 TTD)

200,000

Deferred tax liability 200,000

To record deferred tax liability

Part 1(b)

Recognition of DTA

Part 1(b)

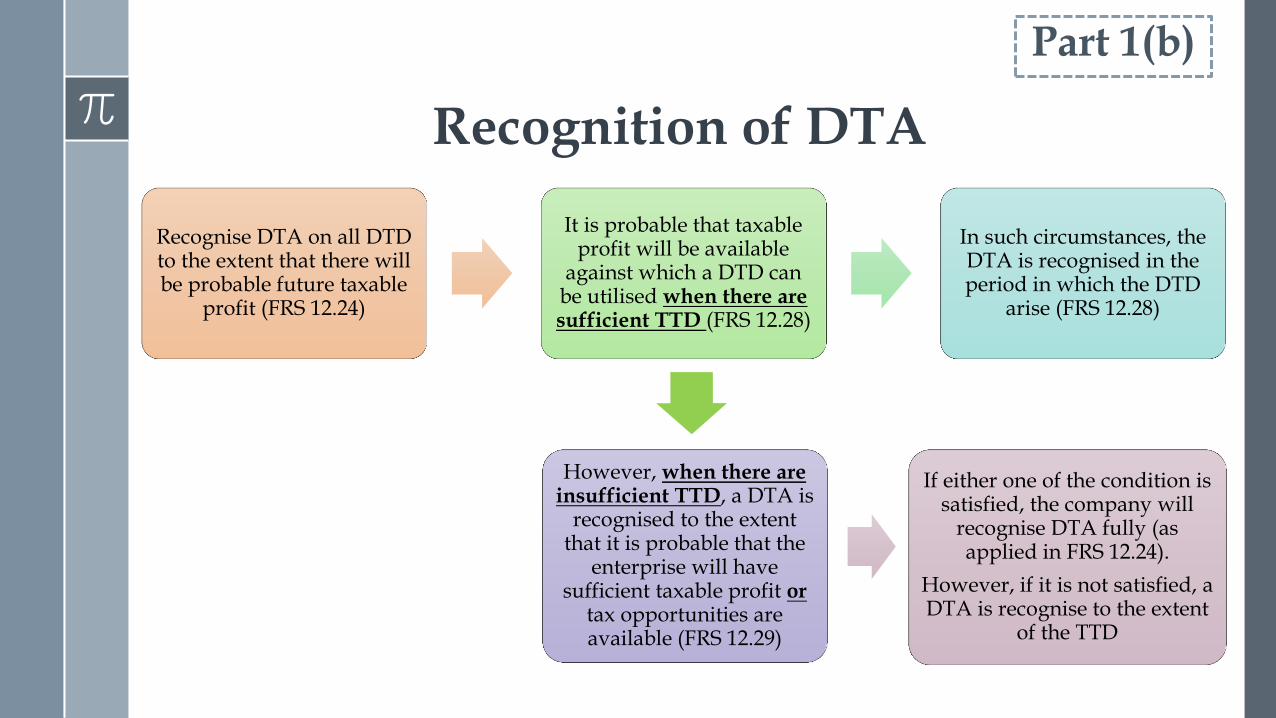

Recognise DTA on all DTD to the extent that there will be probable future taxable

profit (FRS 12.24)

It is probable that taxable profit will be available

against which a DTD can be utilised when there are sufficient TTD (FRS 12.28)

In such circumstances, the DTA is recognised in the period in which the DTD

arise (FRS 12.28)

However, when there are insufficient TTD, a DTA is

recognised to the extent that it is probable that the

enterprise will have sufficient taxable profit or

tax opportunities are available (FRS 12.29)

If either one of the condition is satisfied, the company will

recognise DTA fully (as applied in FRS 12.24).

However, if it is not satisfied, a DTA is recognise to the extent

of the TTD

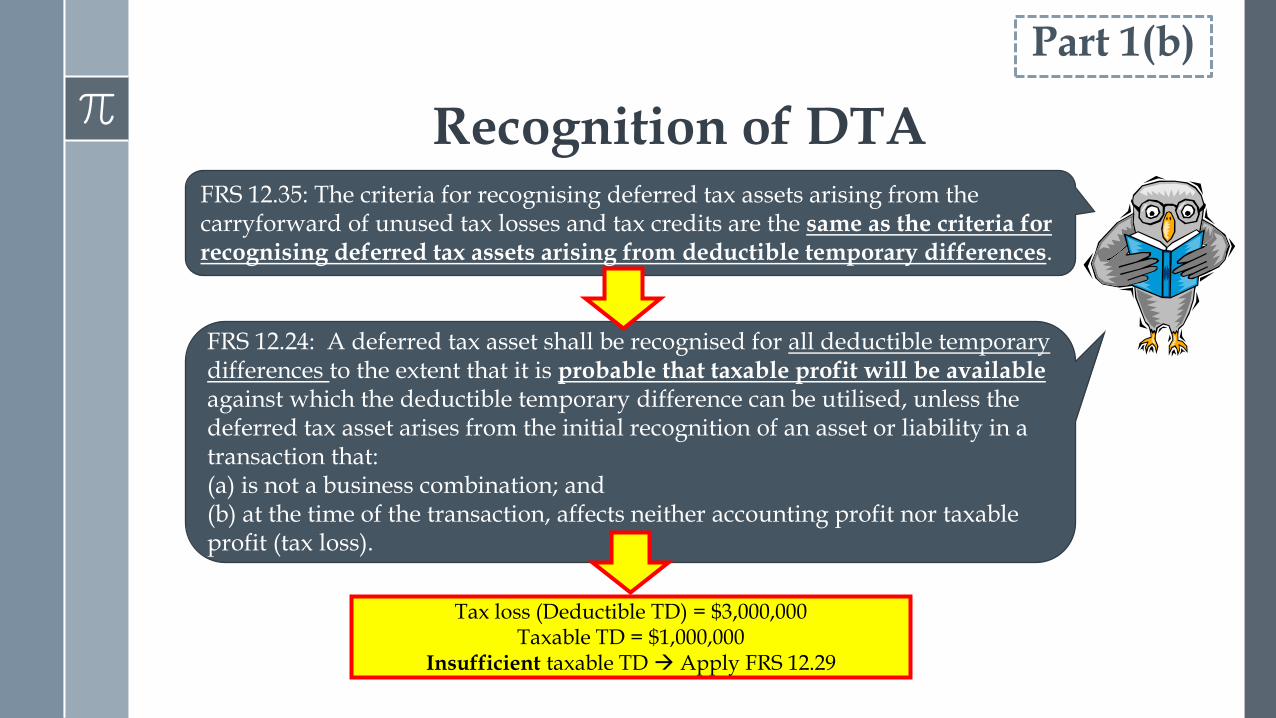

Recognition of DTA FRS 12.35: The criteria for recognising deferred tax assets arising from the carryforward of unused tax losses and tax credits are the same as the criteria for recognising deferred tax assets arising from deductible temporary differences.

Part 1(b)

FRS 12.24: A deferred tax asset shall be recognised for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilised, unless the deferred tax asset arises from the initial recognition of an asset or liability in a transaction that: (a) is not a business combination; and (b) at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

Tax loss (Deductible TD) = $3,000,000 Taxable TD = $1,000,000

Insufficient taxable TD Apply FRS 12.29

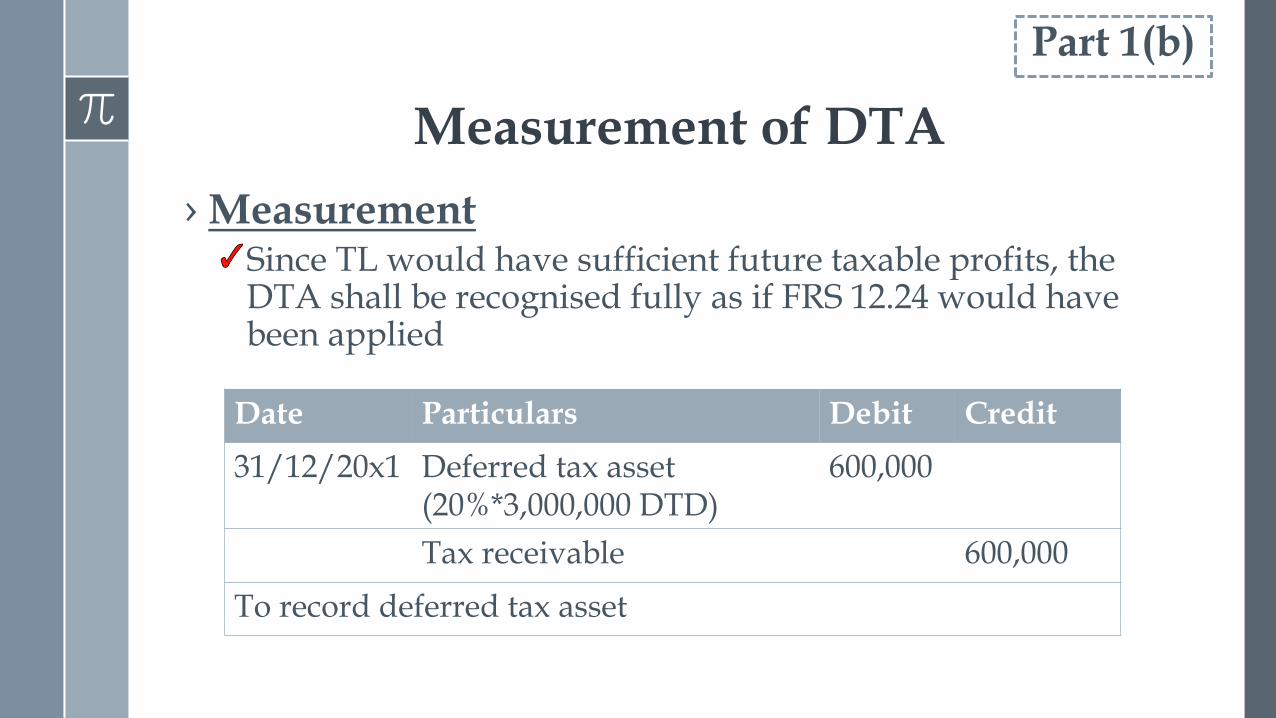

Measurement of DTA

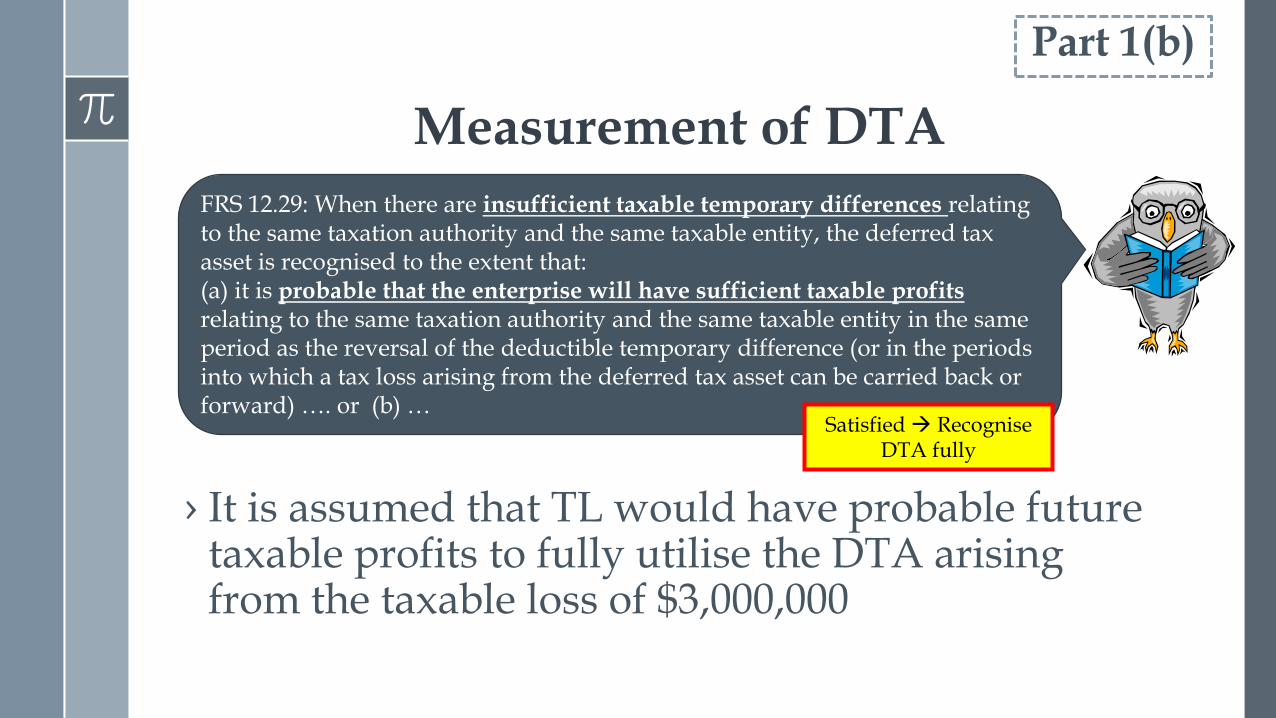

› It is assumed that TL would have probable future taxable profits to fully utilise the DTA arising from the taxable loss of $3,000,000

Part 1(b)

FRS 12.29: When there are insufficient taxable temporary differences relating to the same taxation authority and the same taxable entity, the deferred tax asset is recognised to the extent that: (a) it is probable that the enterprise will have sufficient taxable profits relating to the same taxation authority and the same taxable entity in the same period as the reversal of the deductible temporary difference (or in the periods into which a tax loss arising from the deferred tax asset can be carried back or forward) …. or (b) …

Satisfied Recognise DTA fully

Measurement of DTA

› Measurement Since TL would have sufficient future taxable profits, the DTA shall be recognised fully as if FRS 12.24 would have been applied

Part 1(b)

Date Particulars Debit Credit

31/12/20x1 Deferred tax asset (20%*3,000,000 DTD)

600,000

Tax receivable 600,000

To record deferred tax asset

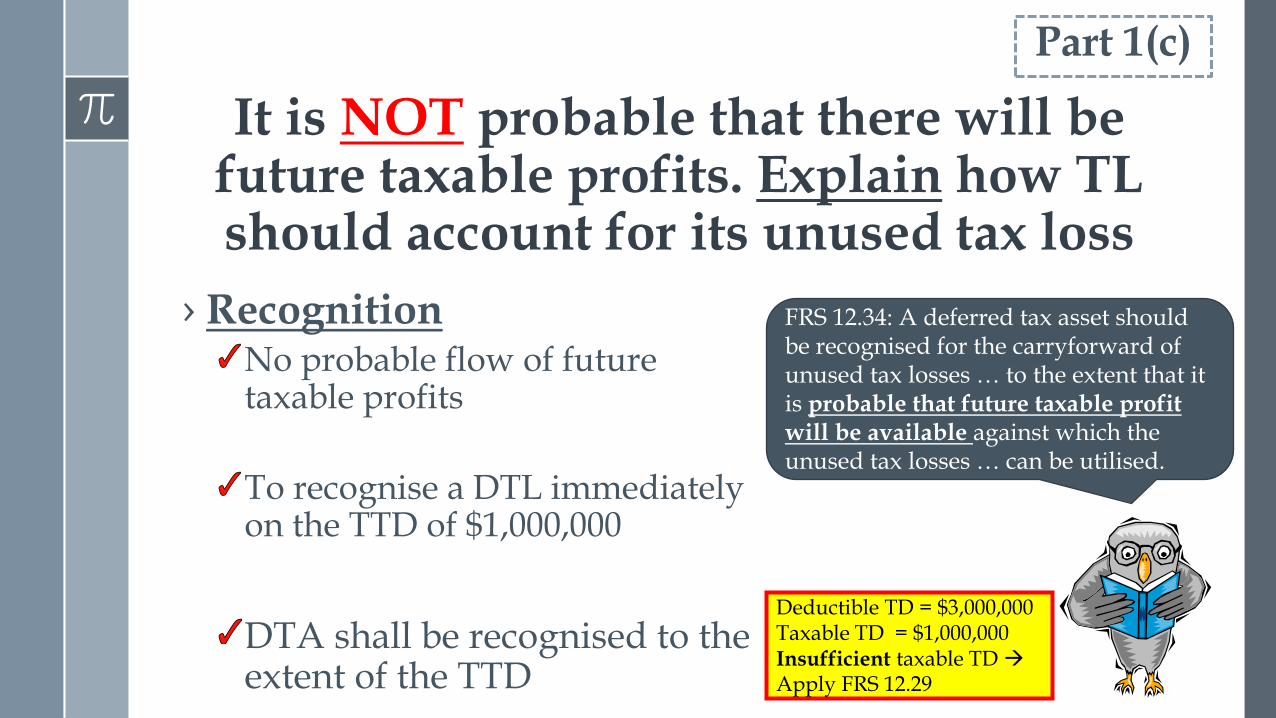

It is NOT probable that there will be future taxable profits. Explain how TL should account for its unused tax loss

› Recognition No probable flow of future taxable profits

To recognise a DTL immediately on the TTD of $1,000,000

DTA shall be recognised to the extent of the TTD

Part 1(c)

FRS 12.34: A deferred tax asset should be recognised for the carryforward of unused tax losses … to the extent that it is probable that future taxable profit will be available against which the unused tax losses … can be utilised.

Deductible TD = $3,000,000 Taxable TD = $1,000,000 Insufficient taxable TD Apply FRS 12.29

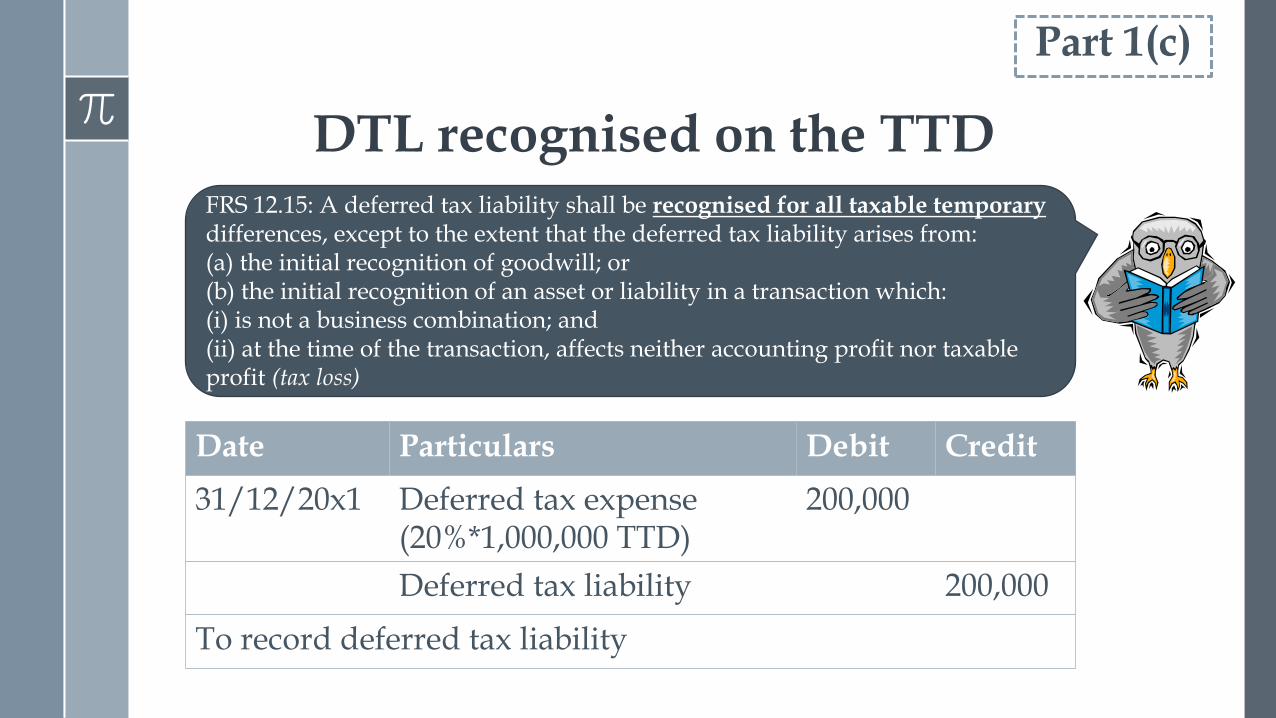

DTL recognised on the TTD FRS 12.15: A deferred tax liability shall be recognised for all taxable temporary differences, except to the extent that the deferred tax liability arises from: (a) the initial recognition of goodwill; or (b) the initial recognition of an asset or liability in a transaction which: (i) is not a business combination; and (ii) at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss)

Date Particulars Debit Credit

31/12/20x1 Deferred tax expense (20%*1,000,000 TTD)

200,000

Deferred tax liability 200,000

To record deferred tax liability

Part 1(c)

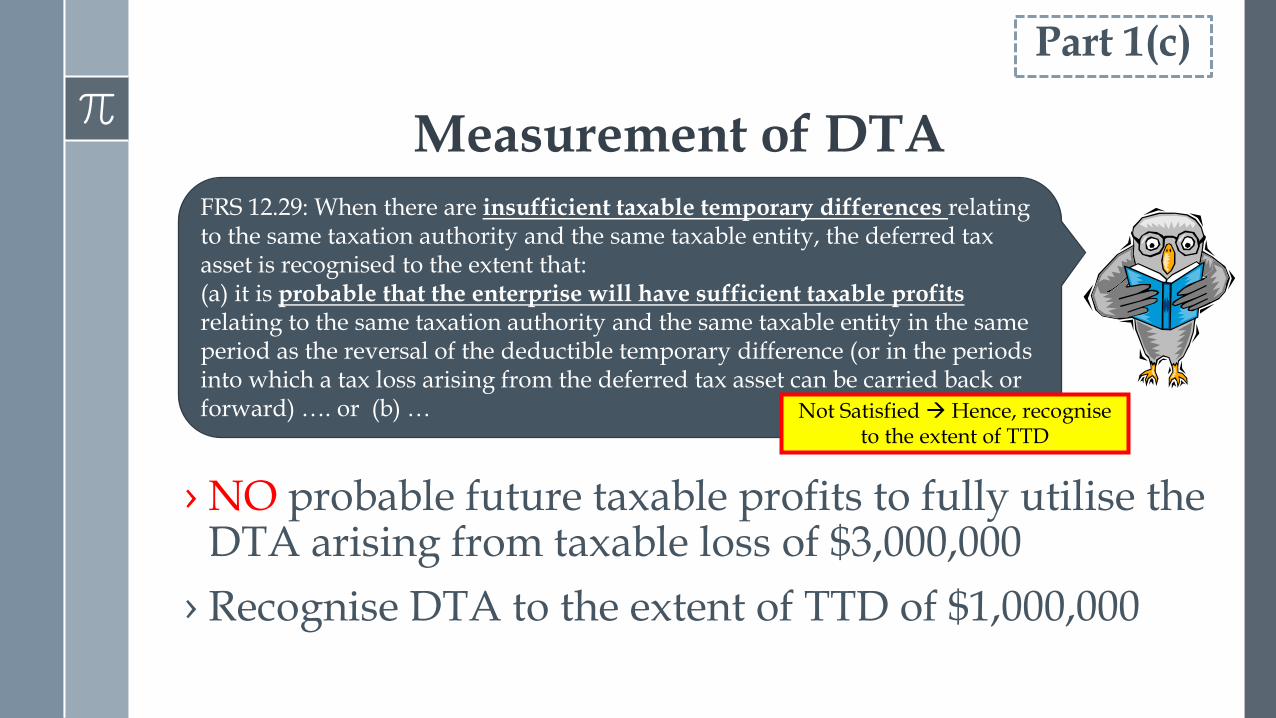

Measurement of DTA

› NO probable future taxable profits to fully utilise the DTA arising from taxable loss of $3,000,000

› Recognise DTA to the extent of TTD of $1,000,000

Part 1(c)

FRS 12.29: When there are insufficient taxable temporary differences relating to the same taxation authority and the same taxable entity, the deferred tax asset is recognised to the extent that: (a) it is probable that the enterprise will have sufficient taxable profits relating to the same taxation authority and the same taxable entity in the same period as the reversal of the deductible temporary difference (or in the periods into which a tax loss arising from the deferred tax asset can be carried back or forward) …. or (b) … Not Satisfied Hence, recognise

to the extent of TTD

DTA recognised to the extent of the TTD

Date Particulars Debit Credit

31/12/20x1 Deferred tax asset (20% x 1,000,000, restricted)*

200,000

Tax receivable 200,000

To record deferred tax asset

*The net effect of recognising DTA to the extent of the TTD is nil

Part 1(c)

› TTD of $1,000,000 < DTD (taxable loss) of $3,000,000

› As at 31 December 20x1, there is an unrecognised DTA of $400,000 [20%*(3,000,000-1,000,000)] To be disclosed separately under FRS 12.81(e)

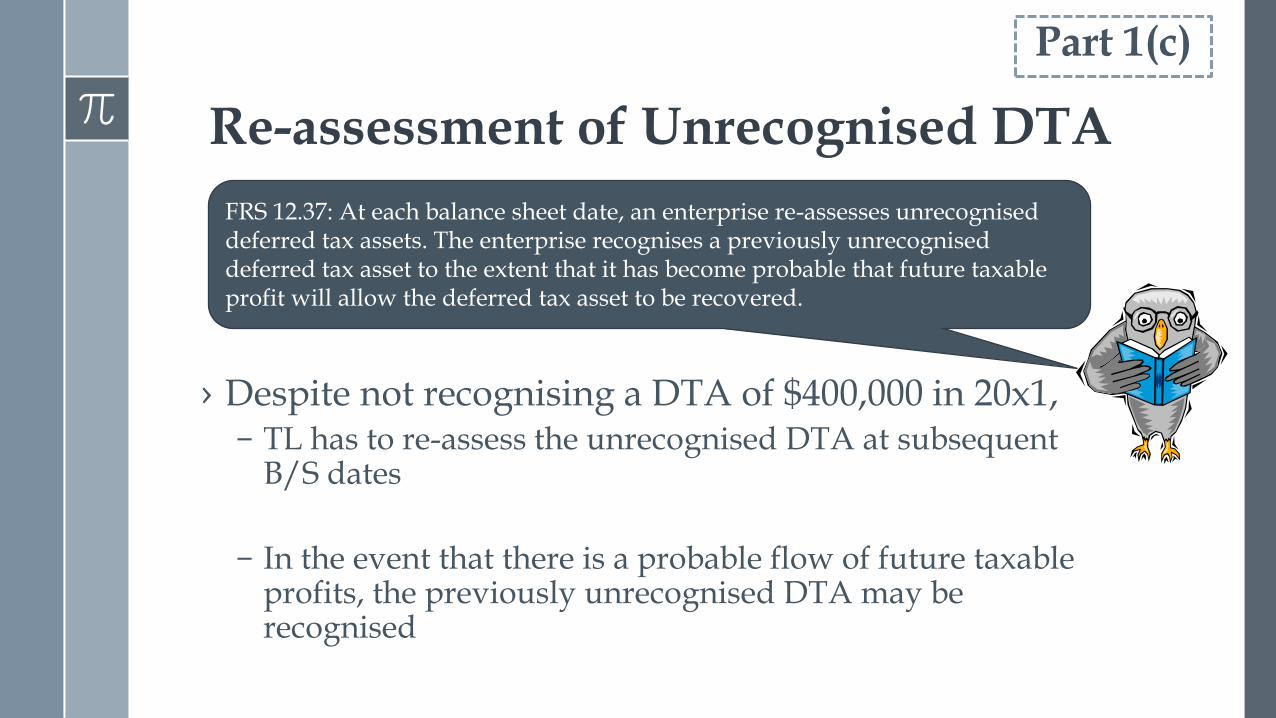

Re-assessment of Unrecognised DTA

› Despite not recognising a DTA of $400,000 in 20x1, – TL has to re-assess the unrecognised DTA at subsequent

B/S dates

– In the event that there is a probable flow of future taxable profits, the previously unrecognised DTA may be recognised

FRS 12.37: At each balance sheet date, an enterprise re-assesses unrecognised deferred tax assets. The enterprise recognises a previously unrecognised deferred tax asset to the extent that it has become probable that future taxable profit will allow the deferred tax asset to be recovered.

Part 1(c)

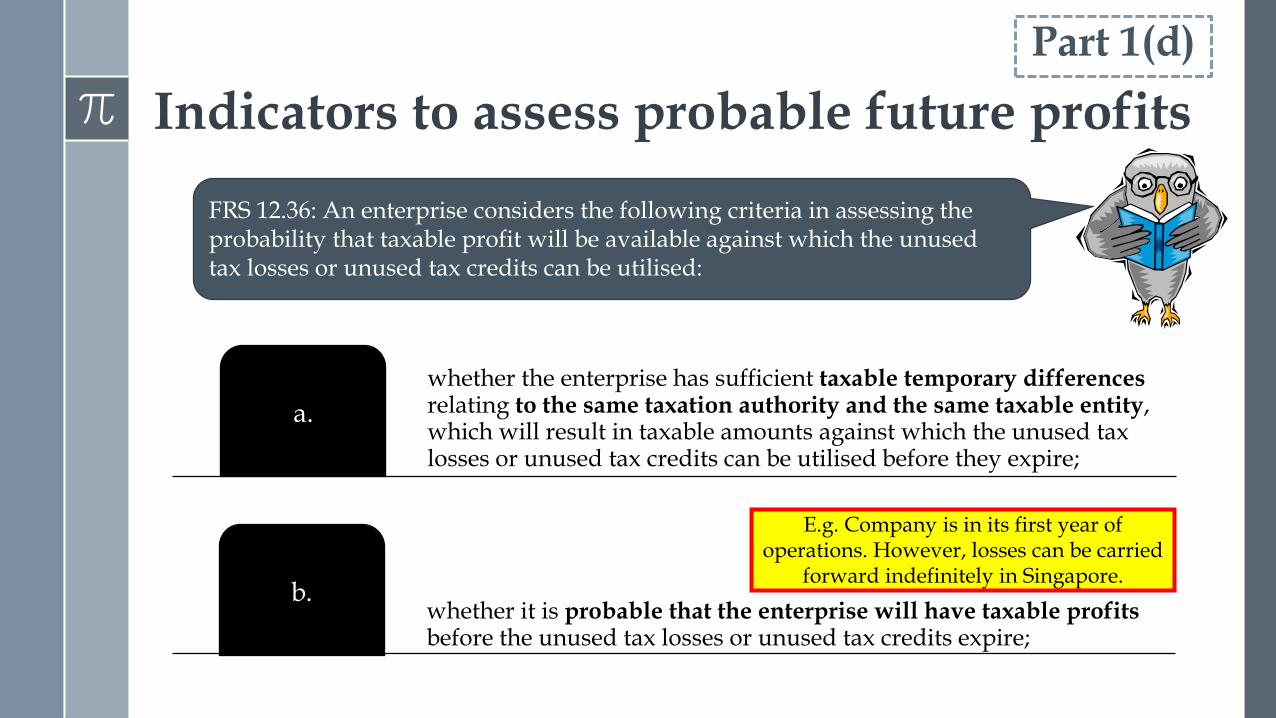

Indicators to assess probable future profits

FRS 12.36: An enterprise considers the following criteria in assessing the probability that taxable profit will be available against which the unused tax losses or unused tax credits can be utilised:

whether the enterprise has sufficient taxable temporary differences relating to the same taxation authority and the same taxable entity, which will result in taxable amounts against which the unused tax losses or unused tax credits can be utilised before they expire;

a.

whether it is probable that the enterprise will have taxable profits before the unused tax losses or unused tax credits expire;

b.

Part 1(d)

E.g. Company is in its first year of operations. However, losses can be carried

forward indefinitely in Singapore.

Indicators to assess probable future profits

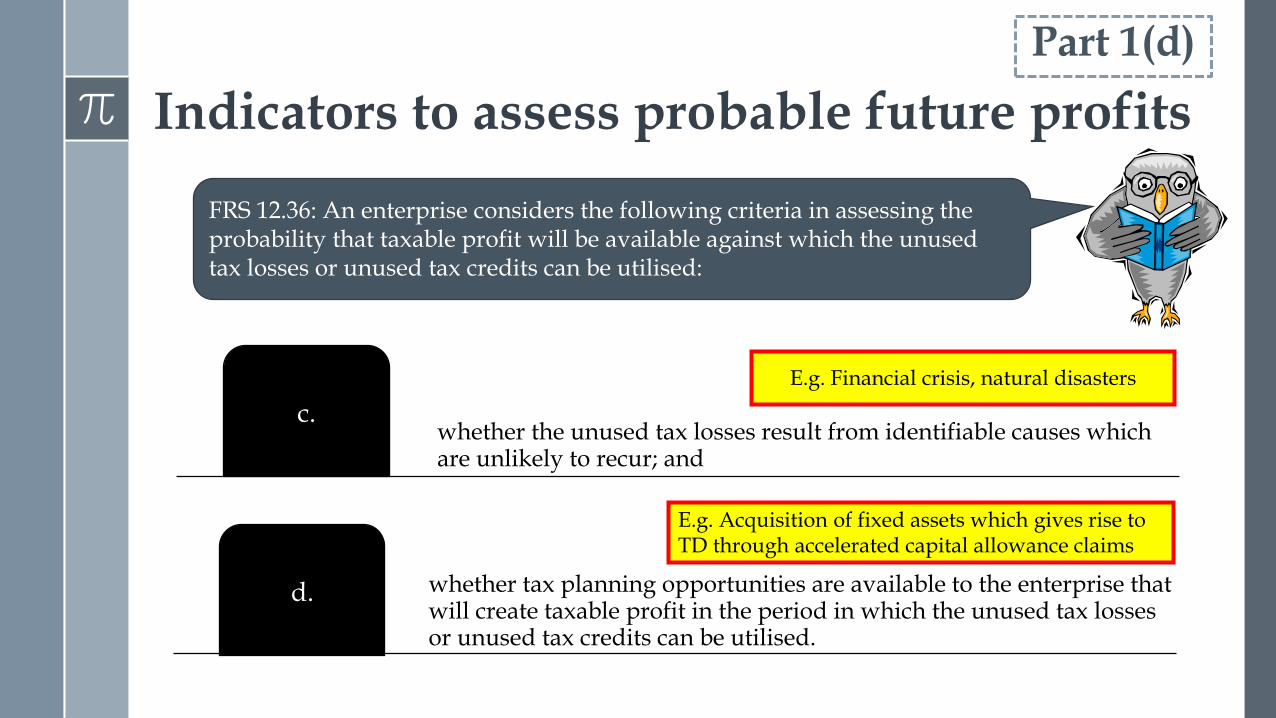

FRS 12.36: An enterprise considers the following criteria in assessing the probability that taxable profit will be available against which the unused tax losses or unused tax credits can be utilised:

whether the unused tax losses result from identifiable causes which are unlikely to recur; and

c.

whether tax planning opportunities are available to the enterprise that will create taxable profit in the period in which the unused tax losses or unused tax credits can be utilised.

d.

Part 1(d)

E.g. Acquisition of fixed assets which gives rise to TD through accelerated capital allowance claims

E.g. Financial crisis, natural disasters

Tax planning opportunities

Part 1(d)

e.g.

FRS 12.30: Tax planning opportunities are actions that the enterprise would take in order to create or increase taxable

income in a particular period before the expiry of a tax loss or tax credit carry forward.

Electing to have interest income

on either a received or

receivable basis,

Deferring the claim for certain deductions from taxable profits,

Selling or leasing back assets which have appreciated but the tax base

has not been adjusted to reflect the appreciation,

Selling of an asset that generates non-taxable

income in order to purchase

another investment that

generates taxable income

Hurricane Ltd

(“HL”)

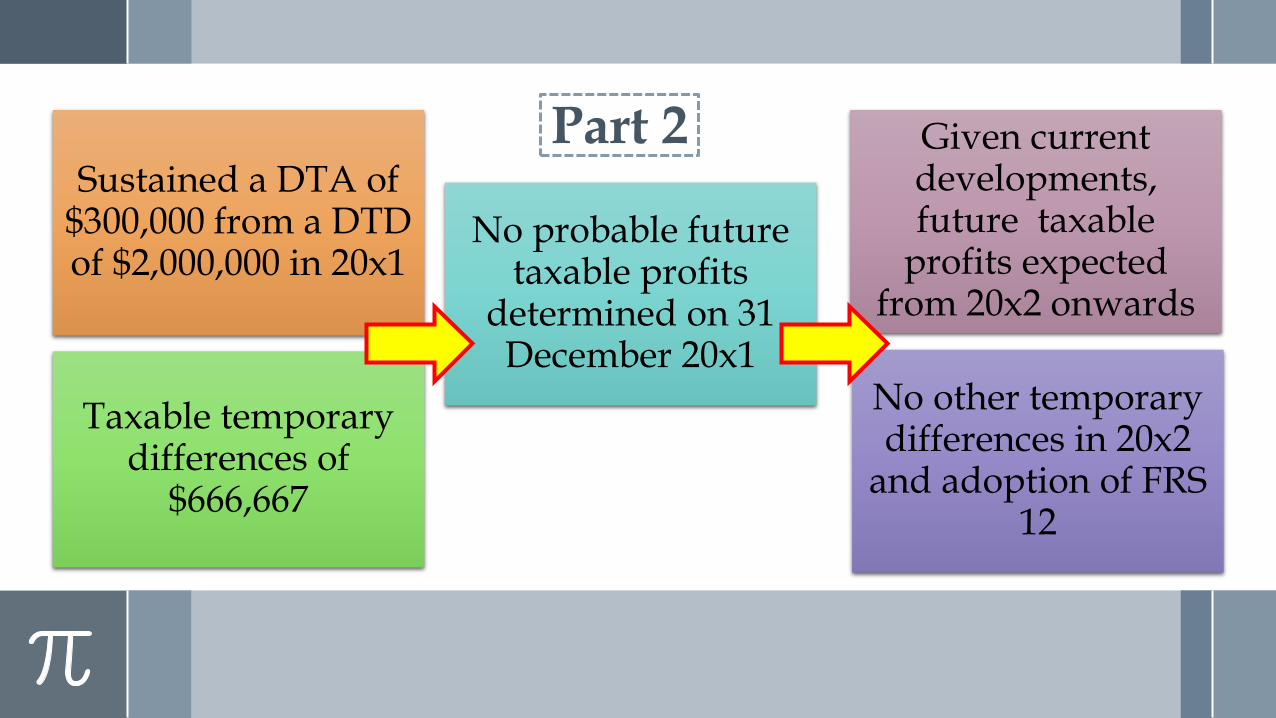

Part 2

Sustained a DTA of $300,000 from a DTD of $2,000,000 in 20x1

Taxable temporary differences of

$666,667

No probable future taxable profits

determined on 31 December 20x1

No other temporary differences in 20x2

and adoption of FRS 12

Given current developments, future taxable

profits expected from 20x2 onwards

Part 2

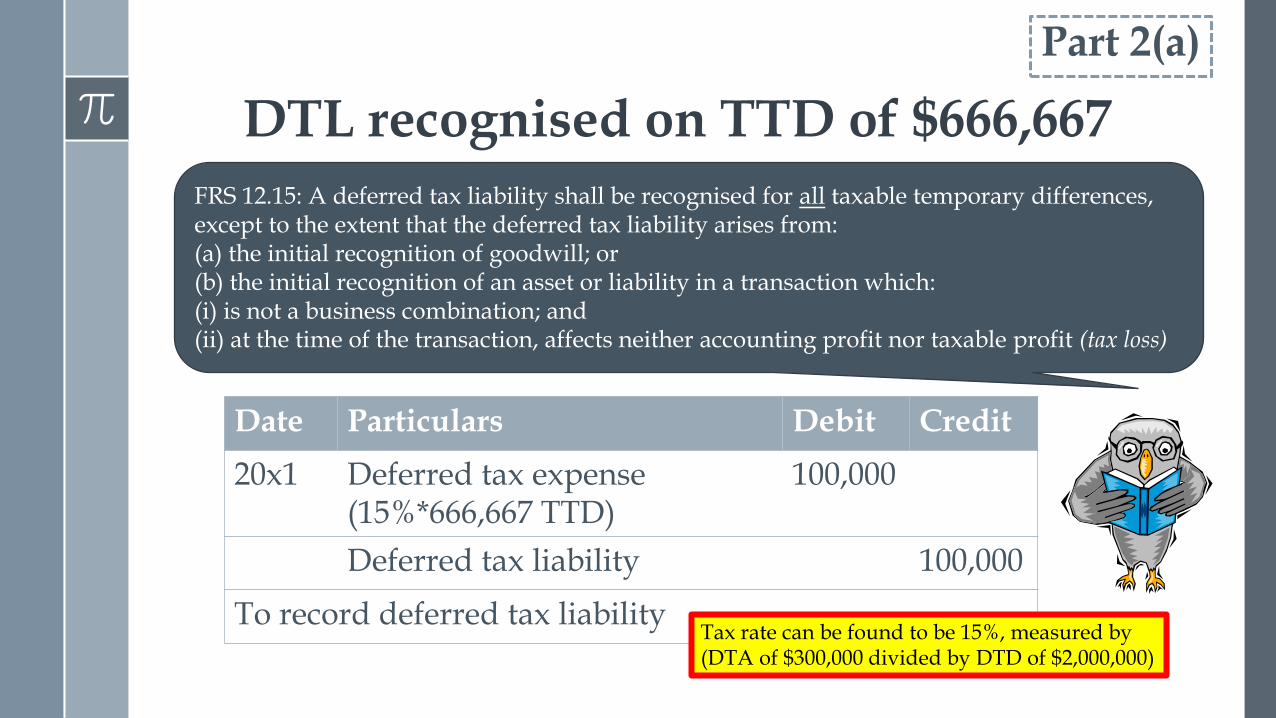

DTL recognised on TTD of $666,667

FRS 12.15: A deferred tax liability shall be recognised for all taxable temporary differences, except to the extent that the deferred tax liability arises from: (a) the initial recognition of goodwill; or (b) the initial recognition of an asset or liability in a transaction which: (i) is not a business combination; and (ii) at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss)

Date Particulars Debit Credit

20x1 Deferred tax expense (15%*666,667 TTD)

100,000

Deferred tax liability 100,000

To record deferred tax liability

Part 2(a)

Tax rate can be found to be 15%, measured by (DTA of $300,000 divided by DTD of $2,000,000)

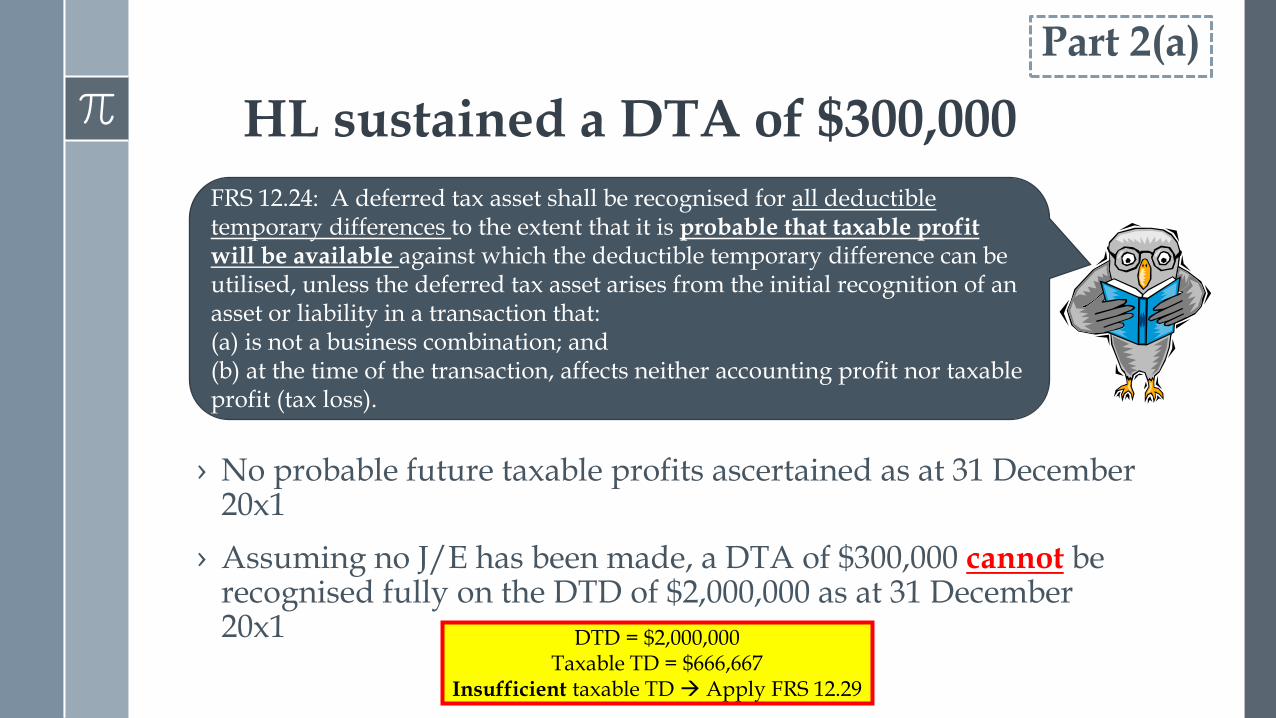

HL sustained a DTA of $300,000

FRS 12.24: A deferred tax asset shall be recognised for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilised, unless the deferred tax asset arises from the initial recognition of an asset or liability in a transaction that: (a) is not a business combination; and (b) at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

› No probable future taxable profits ascertained as at 31 December 20x1

› Assuming no J/E has been made, a DTA of $300,000 cannot be recognised fully on the DTD of $2,000,000 as at 31 December 20x1

Part 2(a)

DTD = $2,000,000 Taxable TD = $666,667

Insufficient taxable TD Apply FRS 12.29

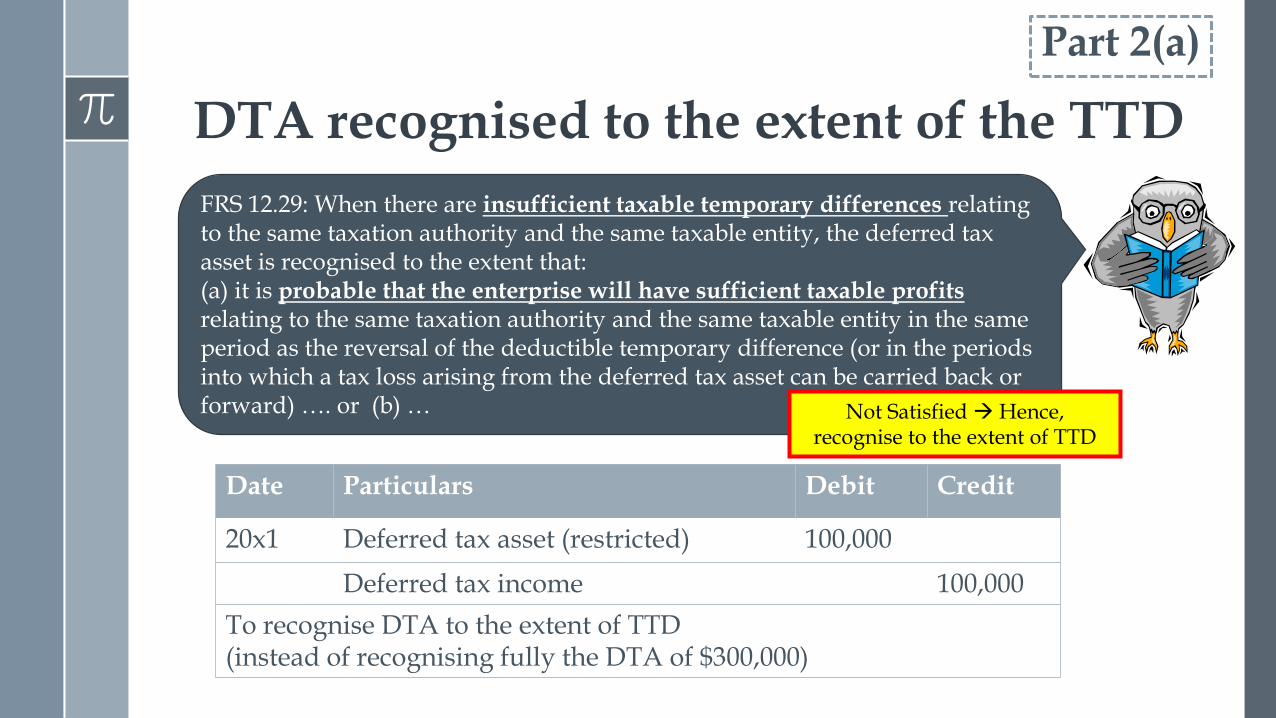

DTA recognised to the extent of the TTD

Date Particulars Debit Credit

20x1 Deferred tax asset (restricted) 100,000

Deferred tax income 100,000

To recognise DTA to the extent of TTD (instead of recognising fully the DTA of $300,000)

Part 2(a)

FRS 12.29: When there are insufficient taxable temporary differences relating to the same taxation authority and the same taxable entity, the deferred tax asset is recognised to the extent that: (a) it is probable that the enterprise will have sufficient taxable profits relating to the same taxation authority and the same taxable entity in the same period as the reversal of the deductible temporary difference (or in the periods into which a tax loss arising from the deferred tax asset can be carried back or forward) …. or (b) … Not Satisfied Hence,

recognise to the extent of TTD

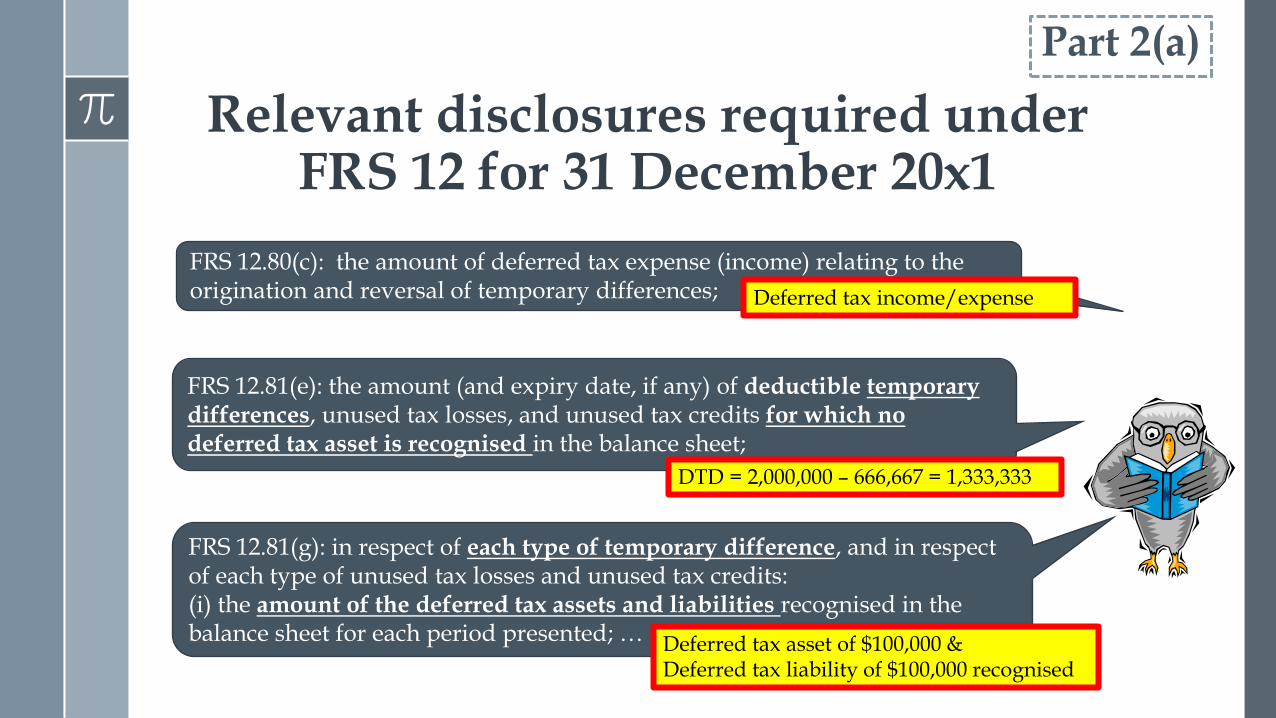

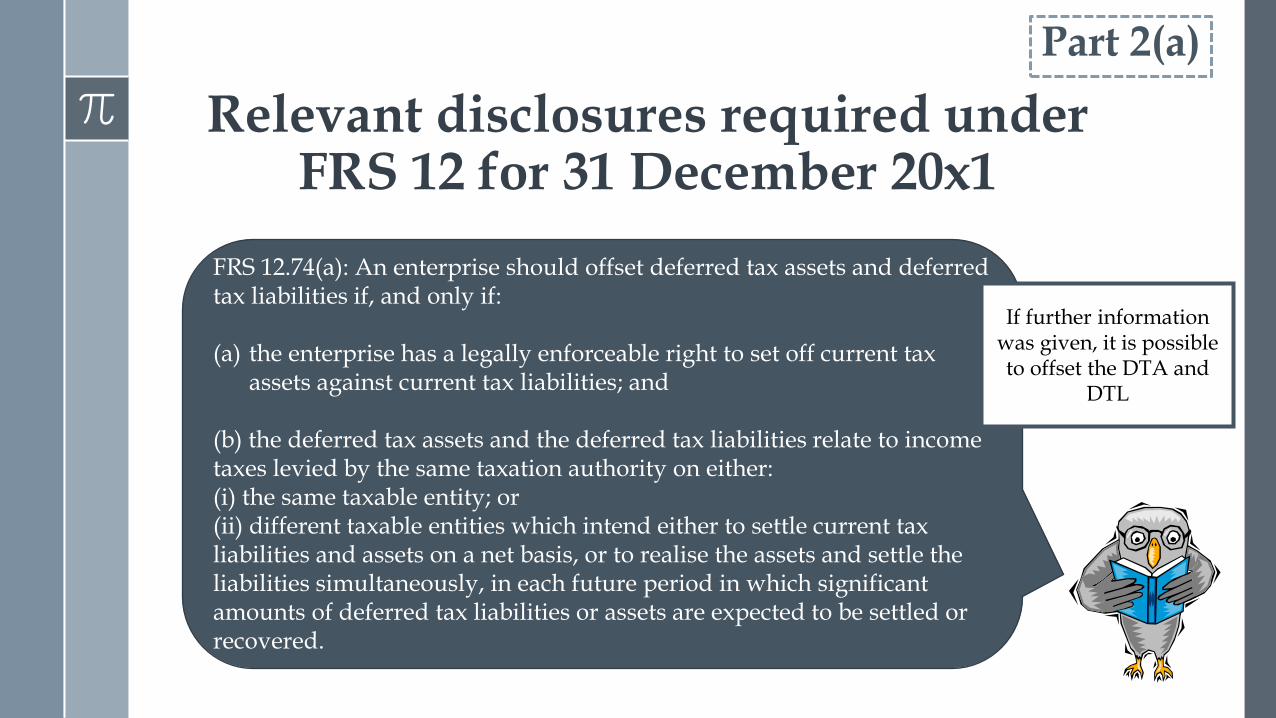

Relevant disclosures required under FRS 12 for 31 December 20x1

Part 2(a)

FRS 12.81(e): the amount (and expiry date, if any) of deductible temporary differences, unused tax losses, and unused tax credits for which no deferred tax asset is recognised in the balance sheet;

FRS 12.81(g): in respect of each type of temporary difference, and in respect of each type of unused tax losses and unused tax credits: (i) the amount of the deferred tax assets and liabilities recognised in the balance sheet for each period presented; …

FRS 12.80(c): the amount of deferred tax expense (income) relating to the origination and reversal of temporary differences;

DTD = 2,000,000 – 666,667 = 1,333,333

Deferred tax asset of $100,000 & Deferred tax liability of $100,000 recognised

Deferred tax income/expense

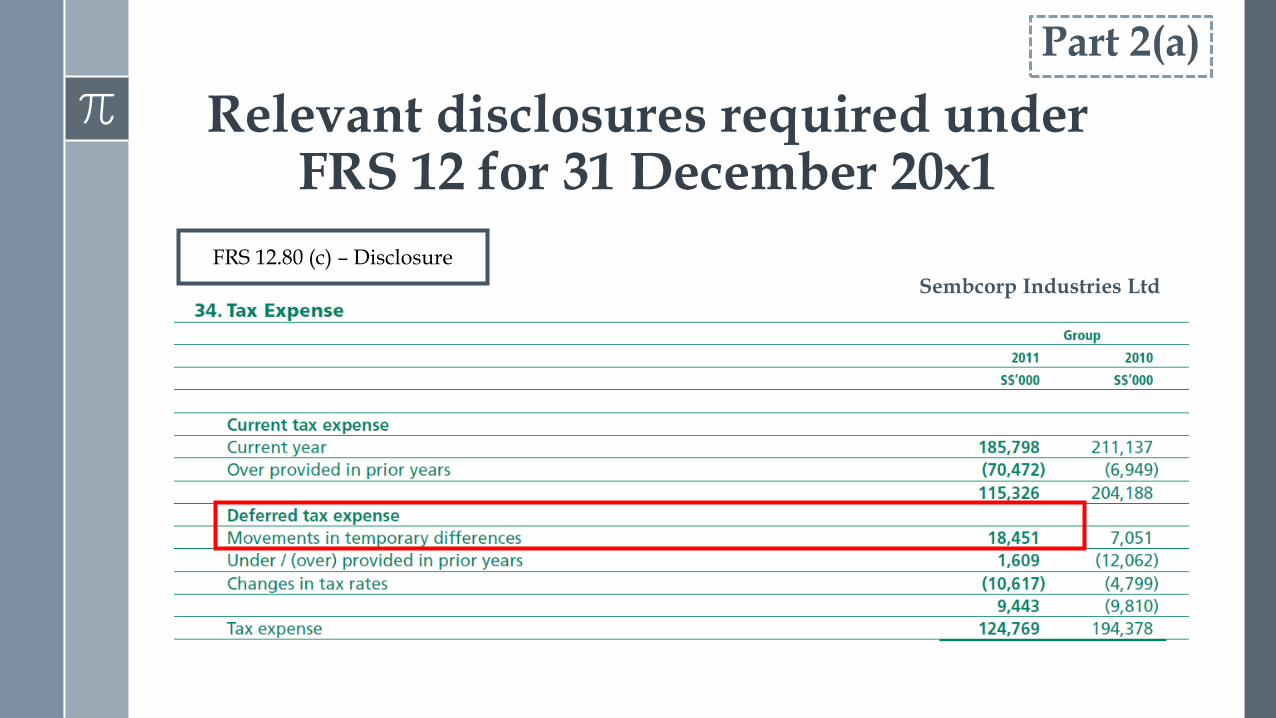

Relevant disclosures required under FRS 12 for 31 December 20x1

Part 2(a)

FRS 12.80 (c) – Disclosure

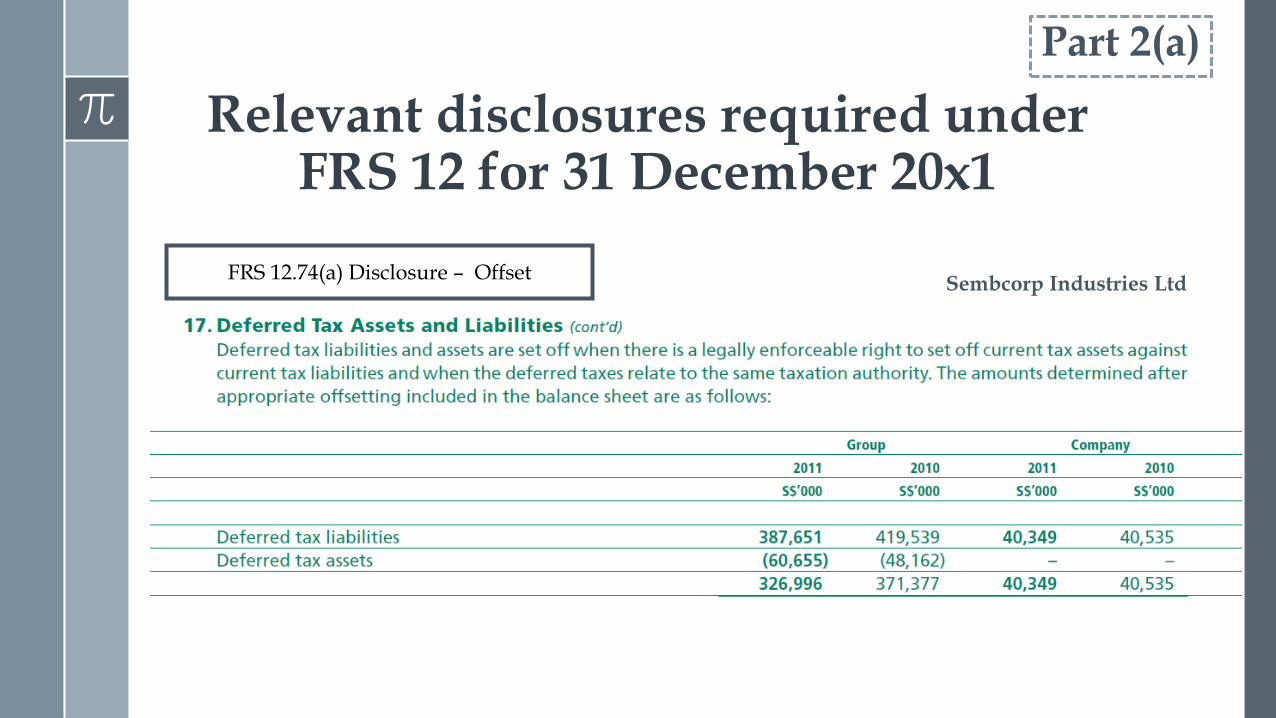

Sembcorp Industries Ltd

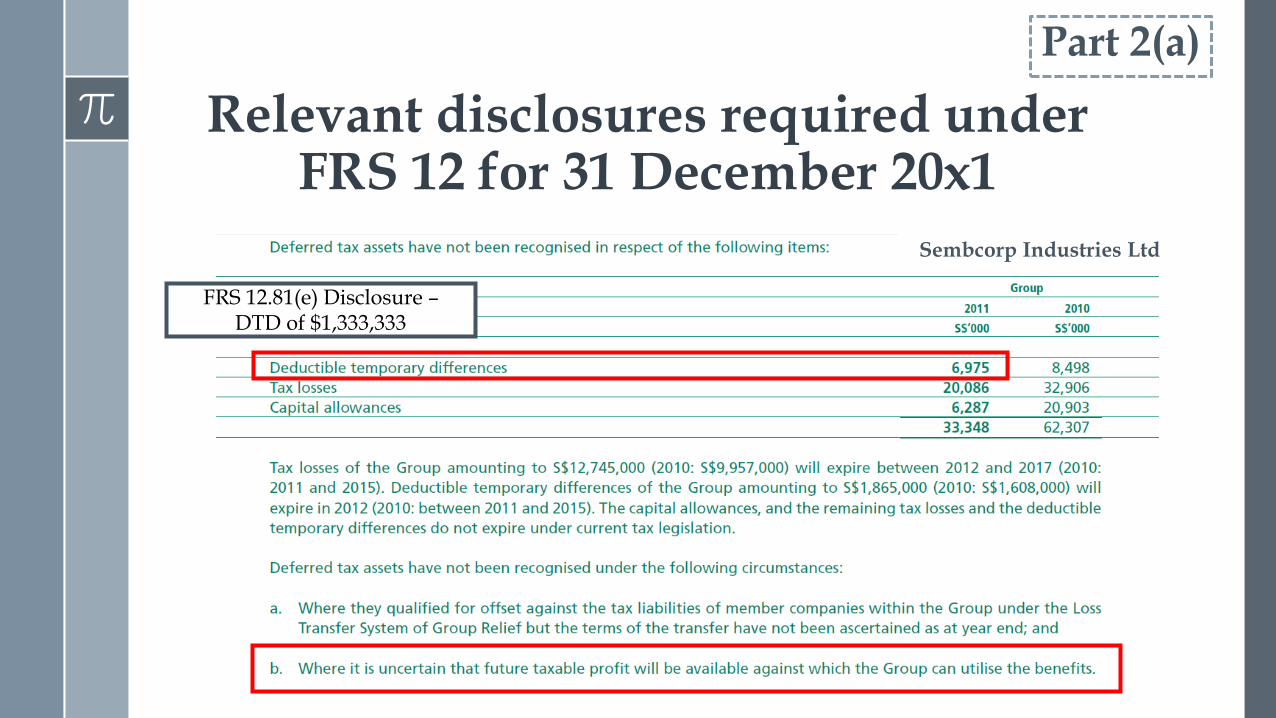

Relevant disclosures required under FRS 12 for 31 December 20x1

Part 2(a)

Sembcorp Industries Ltd

FRS 12.81(e) Disclosure – DTD of $1,333,333

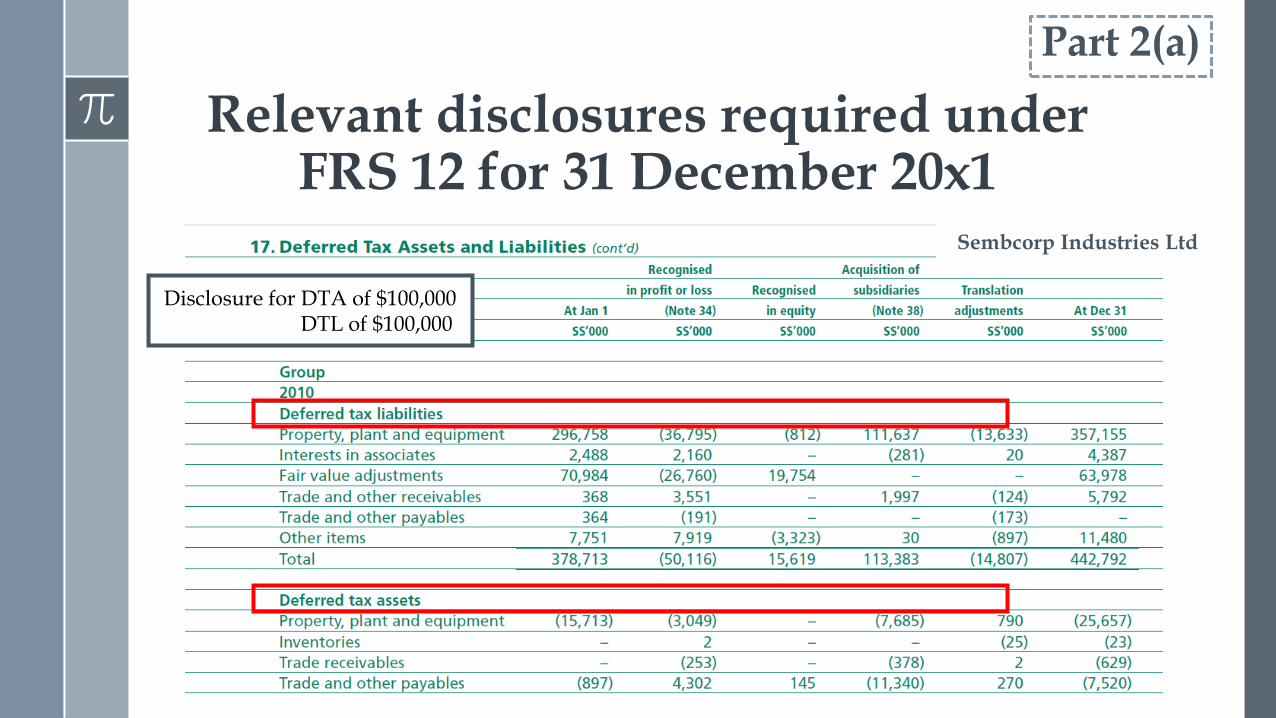

Relevant disclosures required under FRS 12 for 31 December 20x1

Part 2(a)

Disclosure for DTA of $100,000 DTL of $100,000

Sembcorp Industries Ltd

Relevant disclosures required under FRS 12 for 31 December 20x1

Part 2(a)

FRS 12.74(a): An enterprise should offset deferred tax assets and deferred tax liabilities if, and only if: (a) the enterprise has a legally enforceable right to set off current tax

assets against current tax liabilities; and (b) the deferred tax assets and the deferred tax liabilities relate to income taxes levied by the same taxation authority on either: (i) the same taxable entity; or (ii) different taxable entities which intend either to settle current tax liabilities and assets on a net basis, or to realise the assets and settle the liabilities simultaneously, in each future period in which significant amounts of deferred tax liabilities or assets are expected to be settled or recovered.

If further information was given, it is possible to offset the DTA and

DTL

Relevant disclosures required under FRS 12 for 31 December 20x1

Part 2(a)

Sembcorp Industries Ltd FRS 12.74(a) Disclosure – Offset

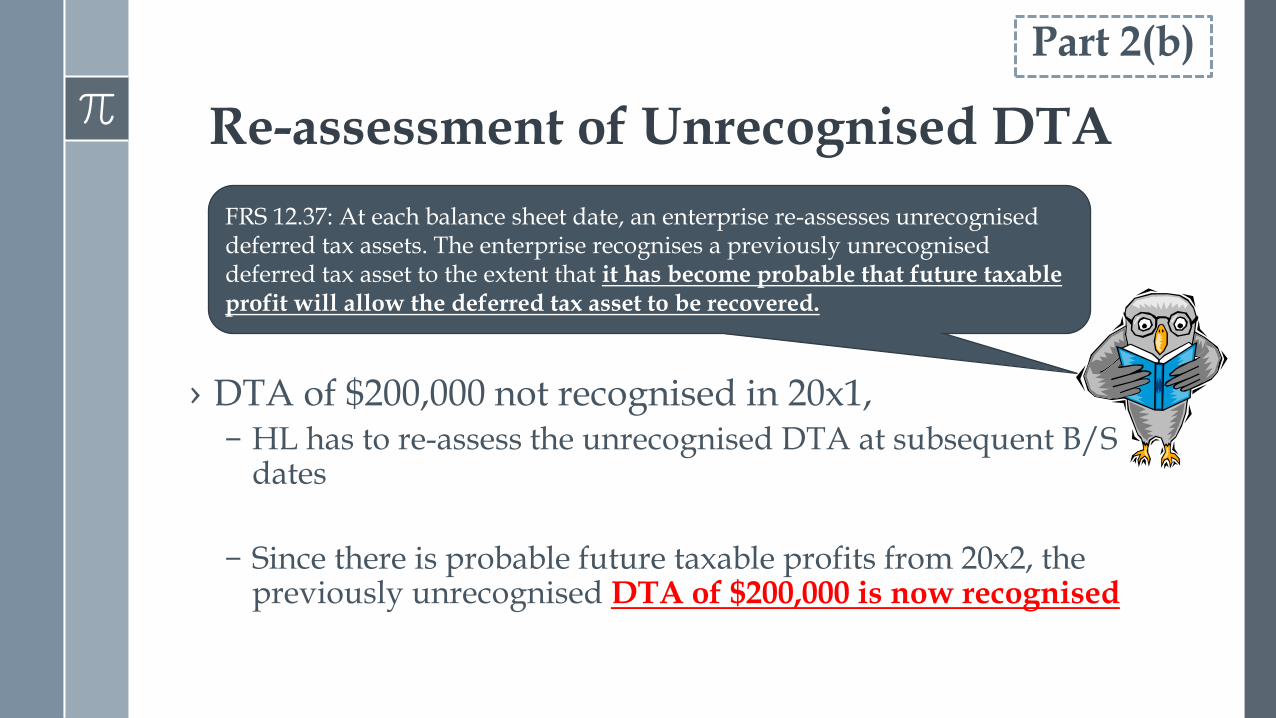

Discuss implications of current development on HL’s DTA. Suggest any

relevant J/E to effect the implication, if any

› In the previous FY ending 31 Dec 20x1, only $100,000 of DTA was recognised

› DTA of $200,000 was not recognized since there were no probable future taxable profits

› In 20x2, the following events would occur:-

Re-assessment of Unrecognised DTA as at 31

December 20x2

New production

process

Future taxable

profits from 20x2

Previously unrecognised DTA

of $200,000 to be recognised in 20x2

Part 2(b)

› DTA of $200,000 not recognised in 20x1, – HL has to re-assess the unrecognised DTA at subsequent B/S

dates

– Since there is probable future taxable profits from 20x2, the previously unrecognised DTA of $200,000 is now recognised

FRS 12.37: At each balance sheet date, an enterprise re-assesses unrecognised deferred tax assets. The enterprise recognises a previously unrecognised deferred tax asset to the extent that it has become probable that future taxable profit will allow the deferred tax asset to be recovered.

Part 2(b)

Re-assessment of Unrecognised DTA

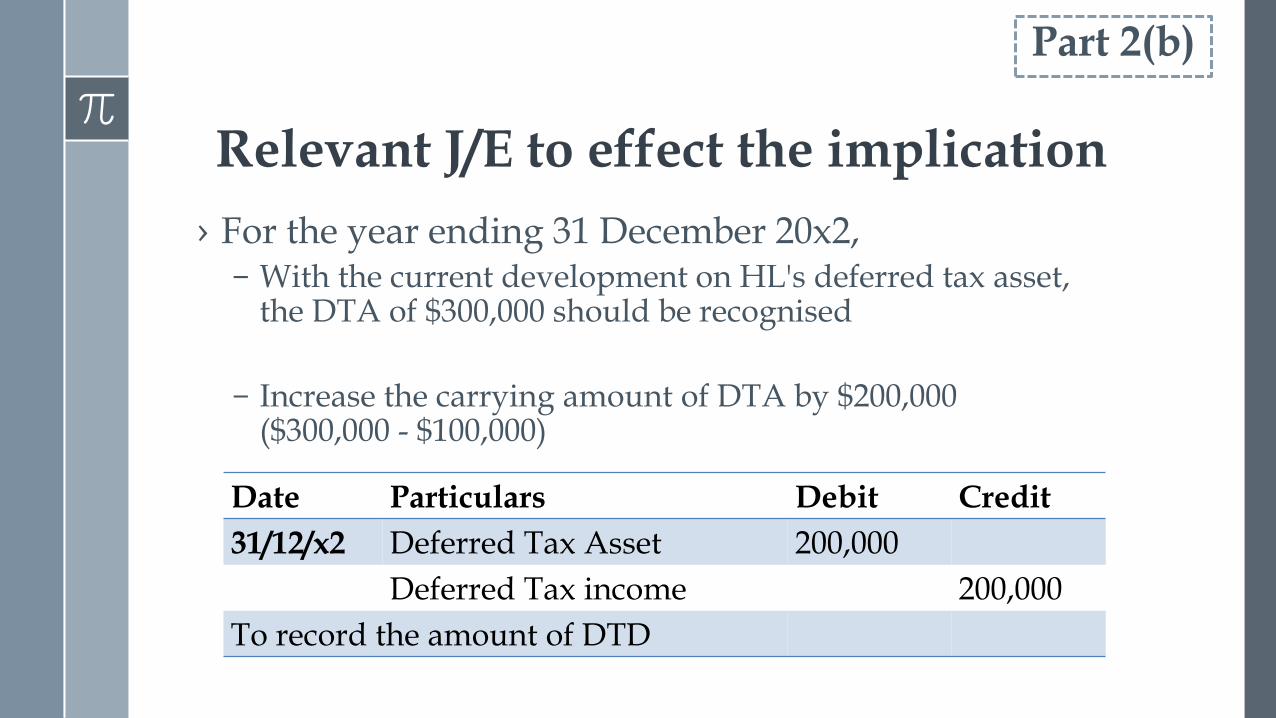

Relevant J/E to effect the implication

› For the year ending 31 December 20x2, – With the current development on HL's deferred tax asset,

the DTA of $300,000 should be recognised

– Increase the carrying amount of DTA by $200,000 ($300,000 - $100,000)

Date Particulars Debit Credit

31/12/x2 Deferred Tax Asset 200,000

Deferred Tax income 200,000

To record the amount of DTD

Part 2(b)

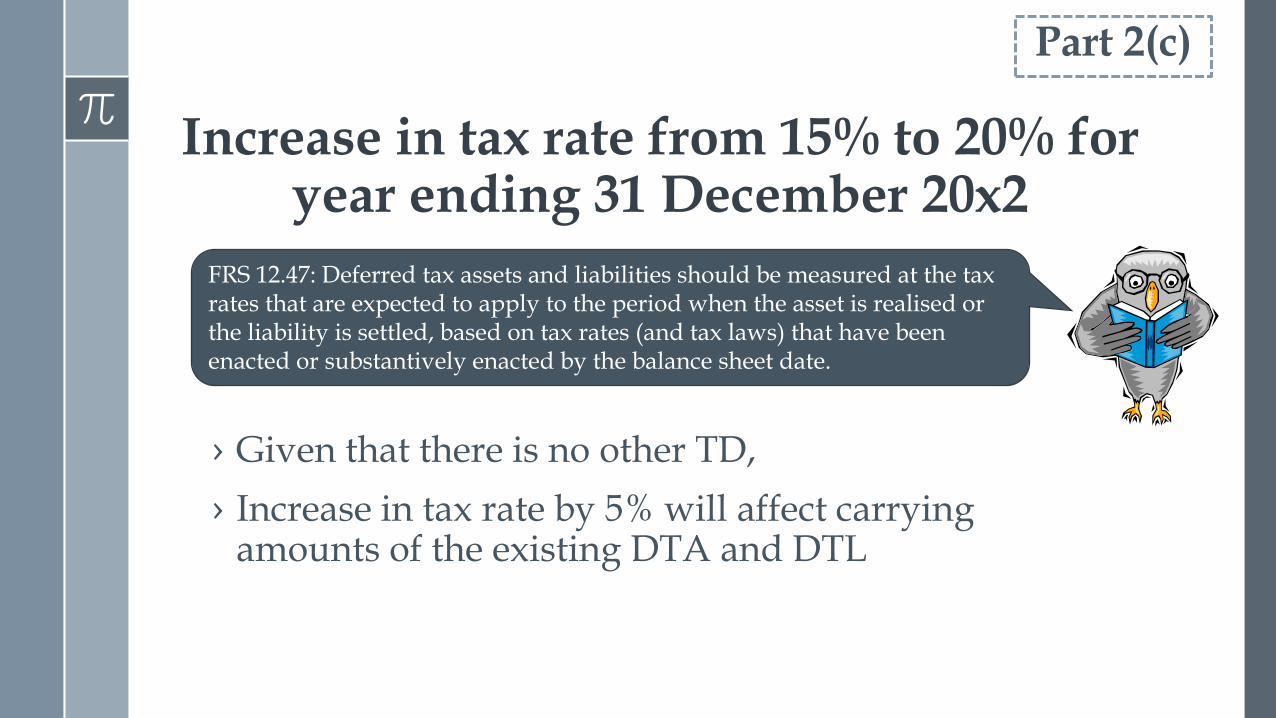

Increase in tax rate from 15% to 20% for year ending 31 December 20x2

FRS 12.47: Deferred tax assets and liabilities should be measured at the tax rates that are expected to apply to the period when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted by the balance sheet date.

Part 2(c)

› Given that there is no other TD,

› Increase in tax rate by 5% will affect carrying amounts of the existing DTA and DTL

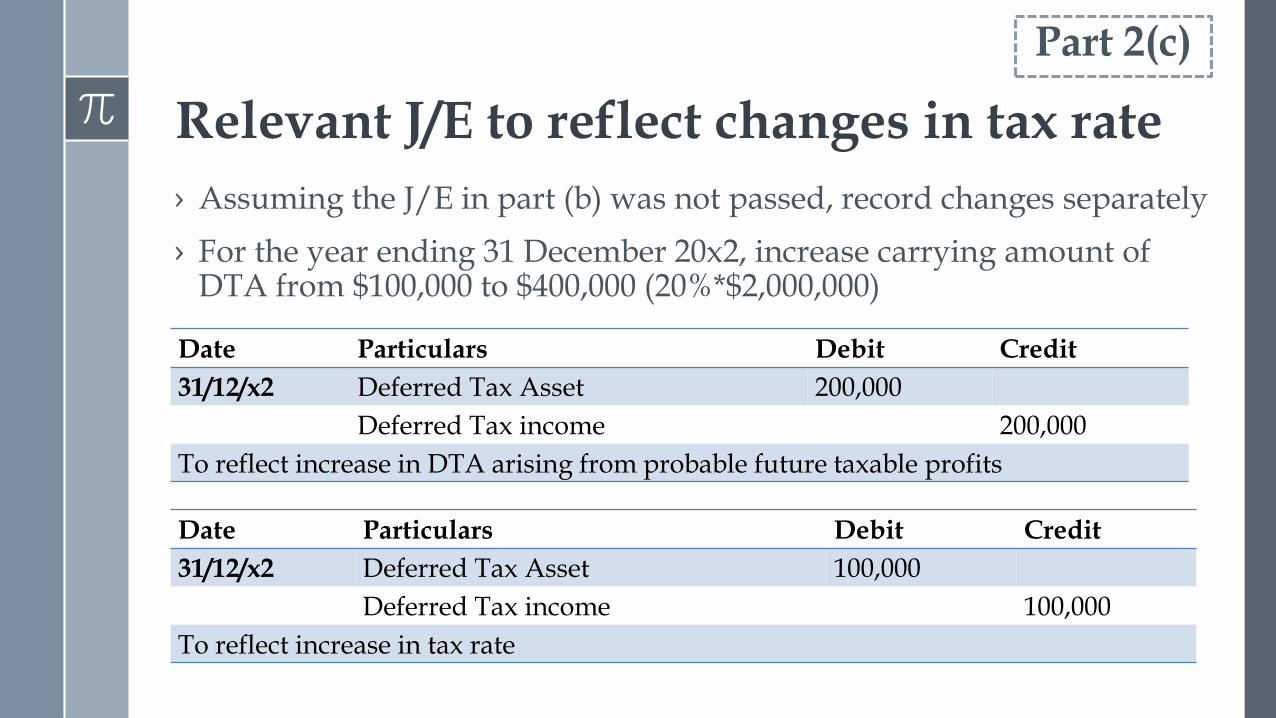

Relevant J/E to reflect changes in tax rate

› Assuming the J/E in part (b) was not passed, record changes separately

› For the year ending 31 December 20x2, increase carrying amount of DTA from $100,000 to $400,000 (20%*$2,000,000)

Part 2(c)

Date Particulars Debit Credit

31/12/x2 Deferred Tax Asset 200,000

Deferred Tax income 200,000

To reflect increase in DTA arising from probable future taxable profits

Date Particulars Debit Credit

31/12/x2 Deferred Tax Asset 100,000

Deferred Tax income 100,000

To reflect increase in tax rate

Relevant J/E to reflect changes in tax rate

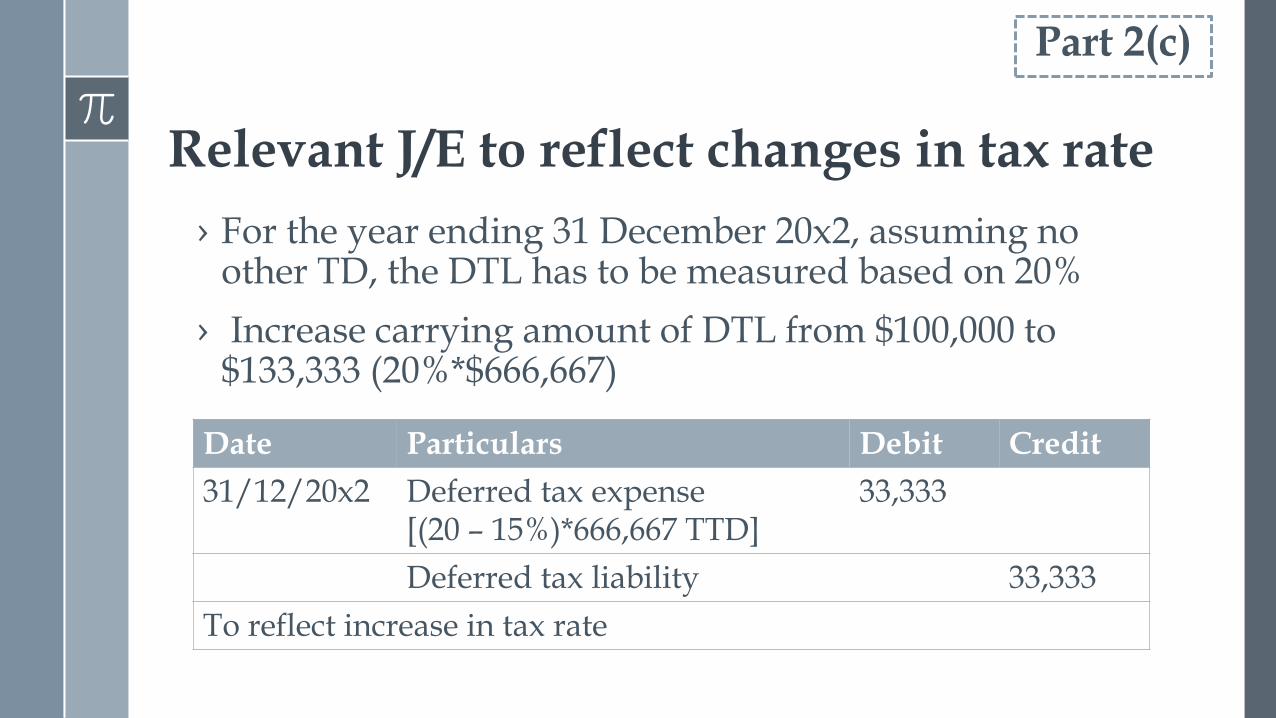

› For the year ending 31 December 20x2, assuming no other TD, the DTL has to be measured based on 20%

› Increase carrying amount of DTL from $100,000 to $133,333 (20%*$666,667)

Part 2(c)

Date Particulars Debit Credit

31/12/20x2 Deferred tax expense [(20 – 15%)*666,667 TTD]

33,333

Deferred tax liability 33,333

To reflect increase in tax rate

Cyclone Ltd

(“CL”)

Part 3

On 1/1/20x1, acquired a freehold

land at $105m

On 31/12/20x1, the land was revalued

to $95m

Profit on sale taxed at 17% and other income taxed at

20%

Land is under FRS 16 PPE Revaluation

Model and adoption of FRS 12

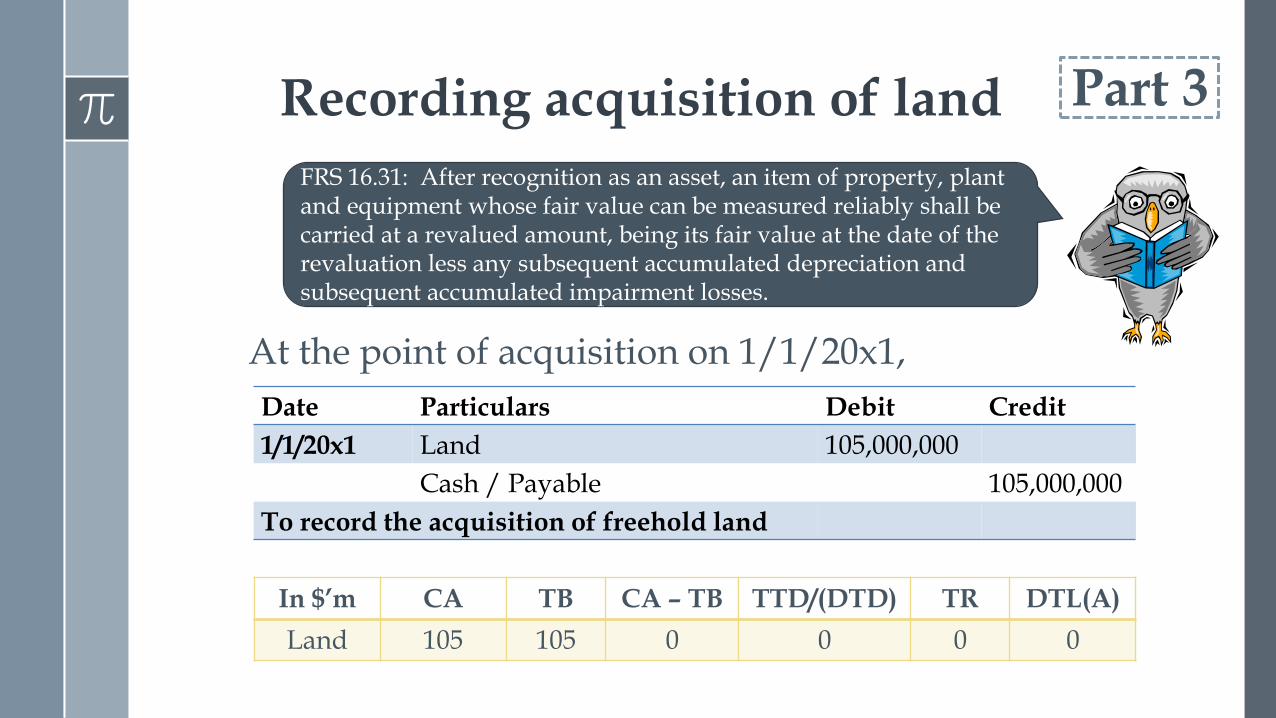

Part 3

At the point of acquisition on 1/1/20x1,

In $’m CA TB CA – TB TTD/(DTD) TR DTL(A)

Land 105 105 0 0 0 0

Date Particulars Debit Credit

1/1/20x1 Land 105,000,000

Cash / Payable 105,000,000

To record the acquisition of freehold land

FRS 16.31: After recognition as an asset, an item of property, plant and equipment whose fair value can be measured reliably shall be carried at a revalued amount, being its fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses.

Part 3 Recording acquisition of land

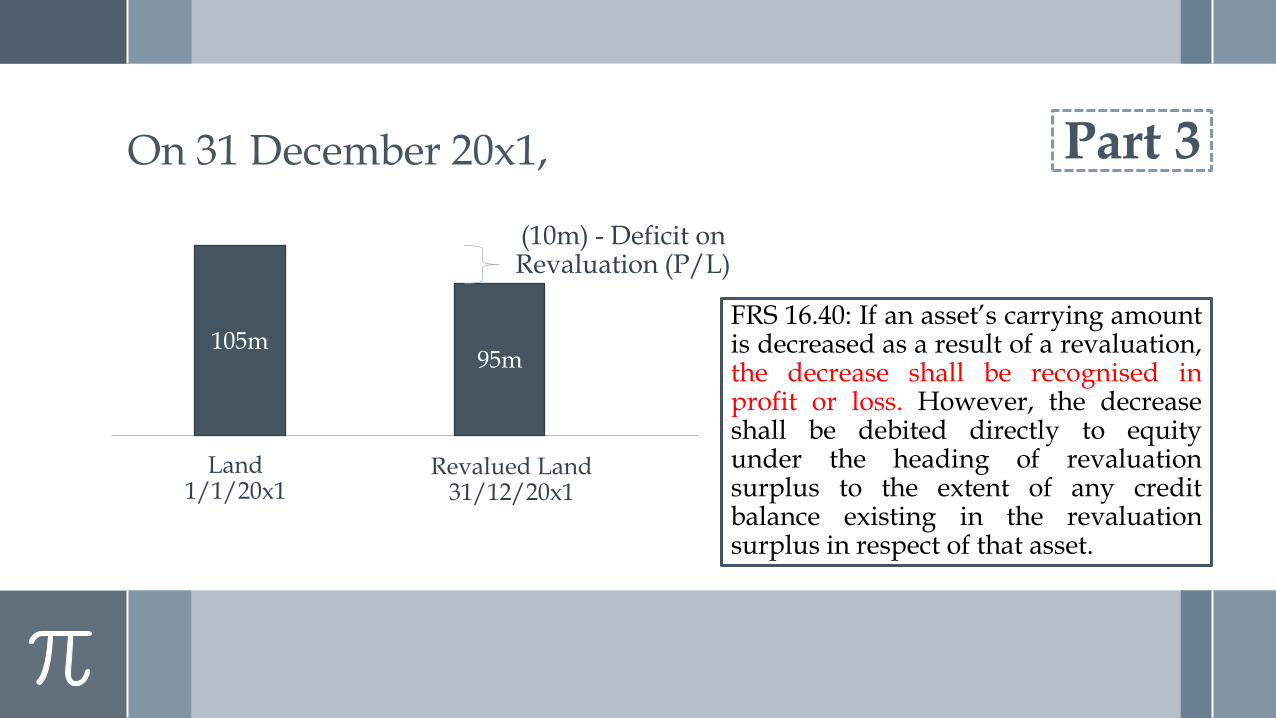

Part 3

105m 95m

Land 1/1/20x1

Revalued Land 31/12/20x1

(10m) - Deficit on Revaluation (P/L)

On 31 December 20x1,

FRS 16.40: If an asset’s carrying amount is decreased as a result of a revaluation, the decrease shall be recognised in profit or loss. However, the decrease shall be debited directly to equity under the heading of revaluation surplus to the extent of any credit balance existing in the revaluation surplus in respect of that asset.

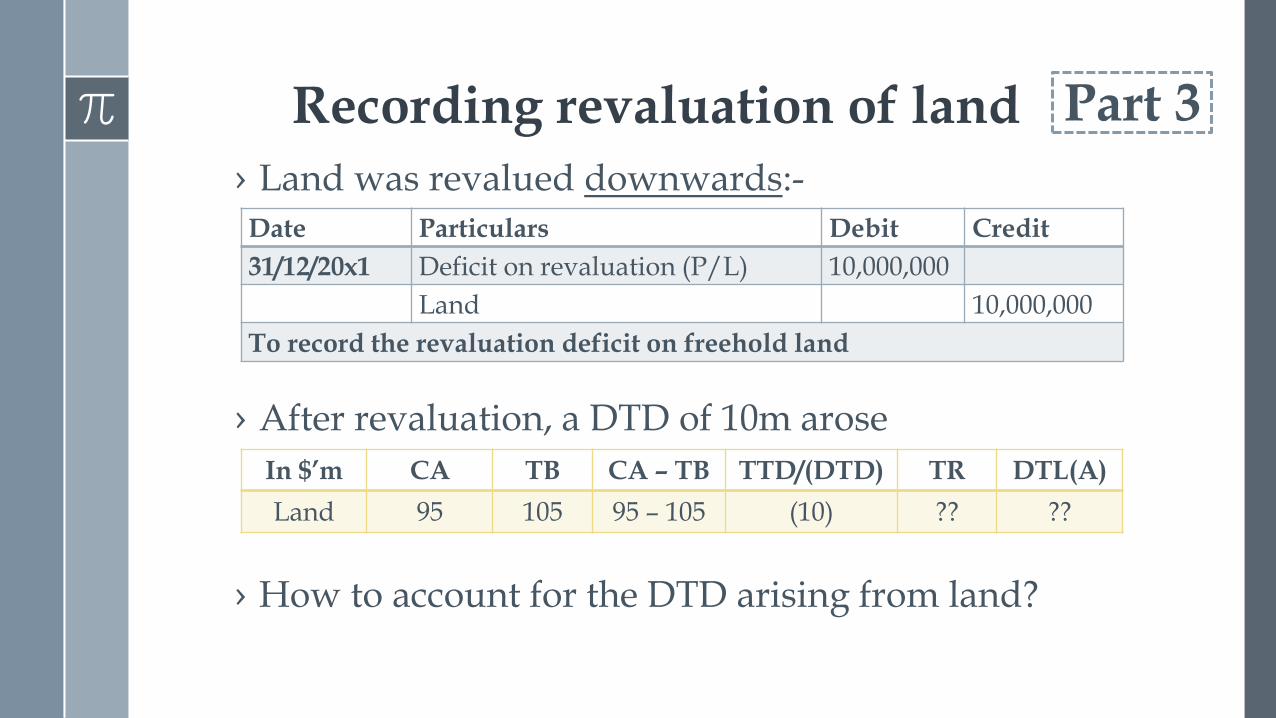

› Land was revalued downwards:-

› After revaluation, a DTD of 10m arose

› How to account for the DTD arising from land?

Date Particulars Debit Credit

31/12/20x1 Deficit on revaluation (P/L) 10,000,000

Land 10,000,000

To record the revaluation deficit on freehold land

Part 3

In $’m CA TB CA – TB TTD/(DTD) TR DTL(A)

Land 95 105 95 – 105 (10) ?? ??

Recording revaluation of land

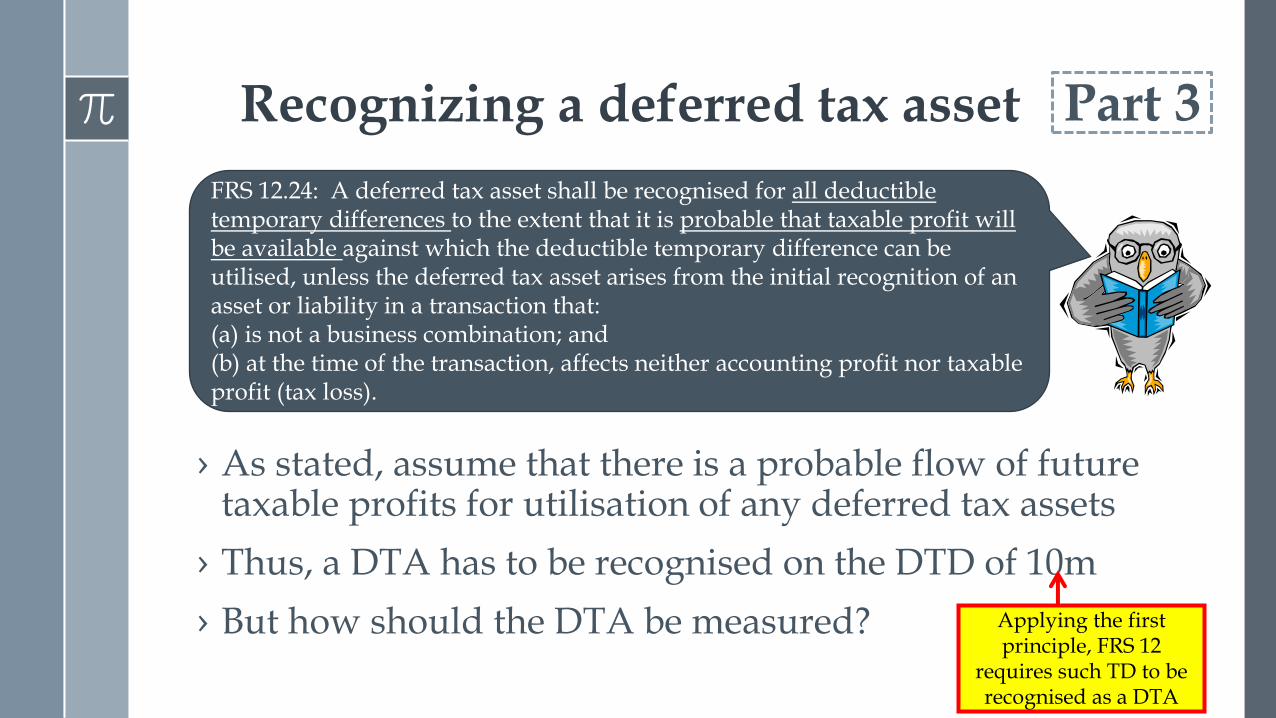

Recognizing a deferred tax asset

FRS 12.24: A deferred tax asset shall be recognised for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilised, unless the deferred tax asset arises from the initial recognition of an asset or liability in a transaction that: (a) is not a business combination; and (b) at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

› As stated, assume that there is a probable flow of future taxable profits for utilisation of any deferred tax assets

› Thus, a DTA has to be recognised on the DTD of 10m

› But how should the DTA be measured?

Part 3

Applying the first principle, FRS 12

requires such TD to be recognised as a DTA

Basis of tax rate to be used

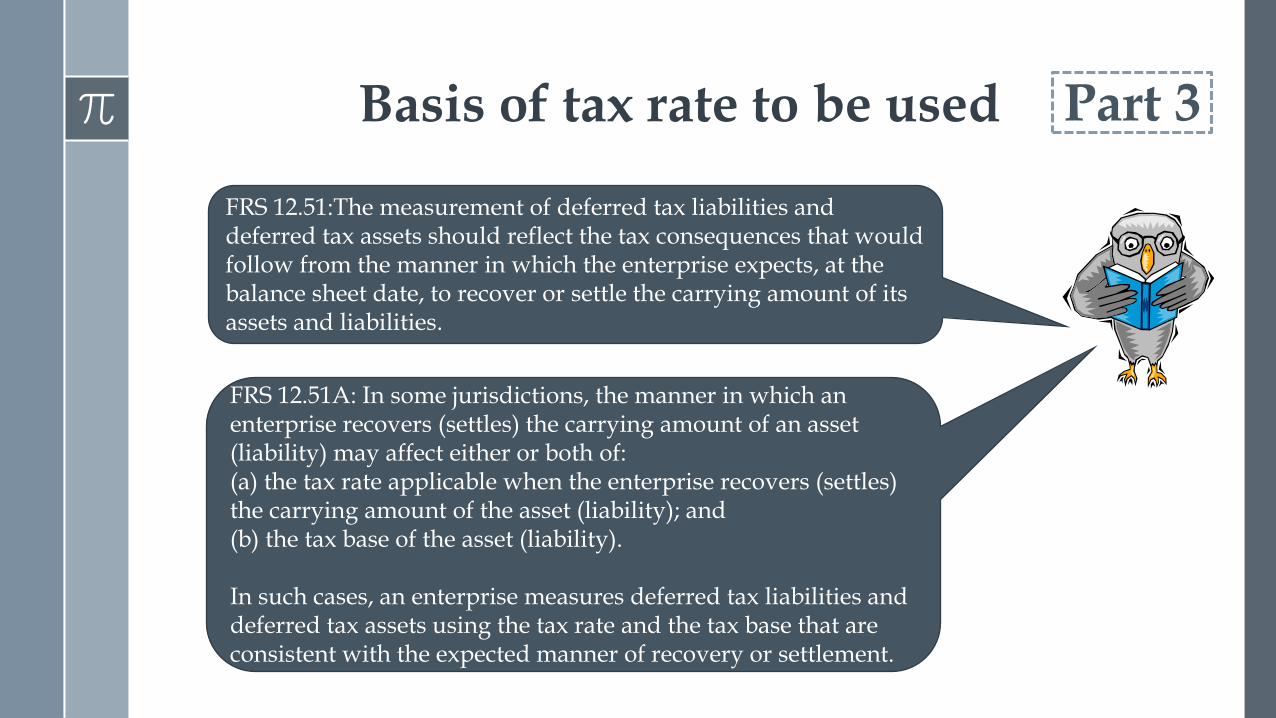

FRS 12.51A: In some jurisdictions, the manner in which an enterprise recovers (settles) the carrying amount of an asset (liability) may affect either or both of: (a) the tax rate applicable when the enterprise recovers (settles) the carrying amount of the asset (liability); and (b) the tax base of the asset (liability). In such cases, an enterprise measures deferred tax liabilities and deferred tax assets using the tax rate and the tax base that are consistent with the expected manner of recovery or settlement.

FRS 12.51:The measurement of deferred tax liabilities and deferred tax assets should reflect the tax consequences that would follow from the manner in which the enterprise expects, at the balance sheet date, to recover or settle the carrying amount of its assets and liabilities.

Part 3

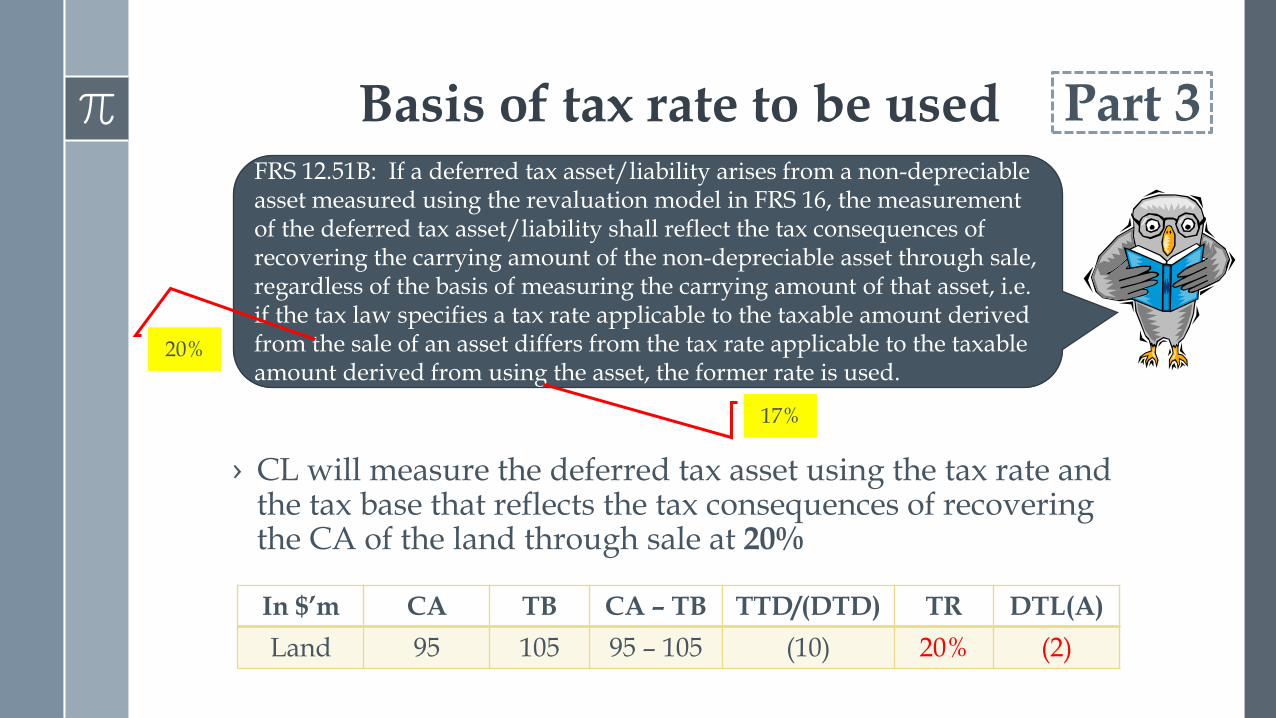

› CL will measure the deferred tax asset using the tax rate and the tax base that reflects the tax consequences of recovering the CA of the land through sale at 20%

FRS 12.51B: If a deferred tax asset/liability arises from a non-depreciable asset measured using the revaluation model in FRS 16, the measurement of the deferred tax asset/liability shall reflect the tax consequences of recovering the carrying amount of the non-depreciable asset through sale, regardless of the basis of measuring the carrying amount of that asset, i.e. if the tax law specifies a tax rate applicable to the taxable amount derived from the sale of an asset differs from the tax rate applicable to the taxable amount derived from using the asset, the former rate is used.

Part 3 Basis of tax rate to be used

17%

20%

In $’m CA TB CA – TB TTD/(DTD) TR DTL(A)

Land 95 105 95 – 105 (10) 20% (2)

- Journal entry required:-

Date Particulars Debit Credit

31/12/20x1 Deferred tax asset

(20%*10,000,000)

2,000,000

Deferred tax income (P/L) 2,000,000

To recognise a deferred tax asset on the deductible temporary

difference of $10,000,000

Recording deferred tax effects Part 3

Applying the second principle, since revaluation deficit is accounted for directly

in P/L, the deferred tax effect thereof should also be accounted for directly in P/L

Part 3

125m

95m

CL’s books

(20m) – Taxable Profit

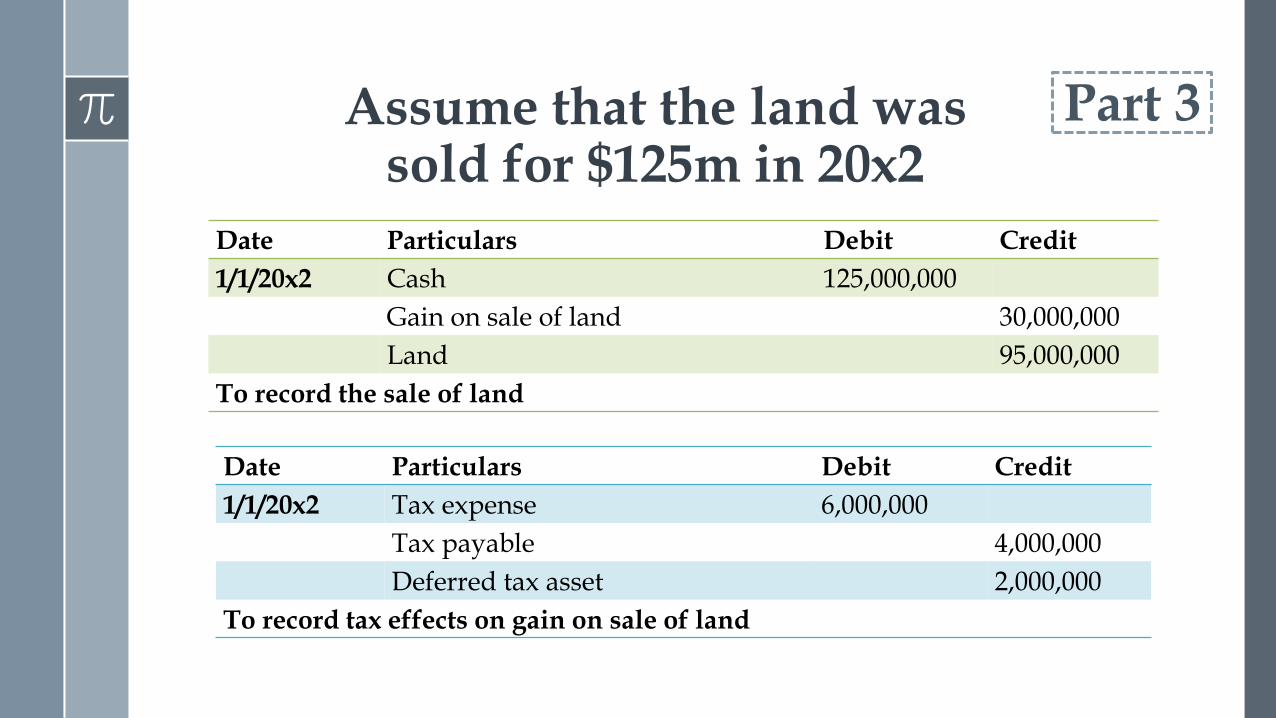

Assume that the land was sold for 125m in 20x2, attracting a tax rate of 20%

105m

IRAS’s books

(30m) – Acc Profit

Tax expense = 600,000 (20%*30,000,000)

Tax payable = 400,000 (20%*20,000,000)

Cash on sale

Date Particulars Debit Credit

1/1/20x2 Cash 125,000,000

Gain on sale of land 30,000,000

Land 95,000,000

To record the sale of land

Date Particulars Debit Credit

1/1/20x2 Tax expense 6,000,000

Tax payable 4,000,000

Deferred tax asset 2,000,000

To record tax effects on gain on sale of land

Assume that the land was sold for $125m in 20x2

Part 3

Theory

Part 4

Part 4

General recognition criteria

1) It must meet the definition of a financial statement element;

2) Probable inflow/outflow of future economic benefits

3) Cost or value can be reliably measured

Conceptual Framework

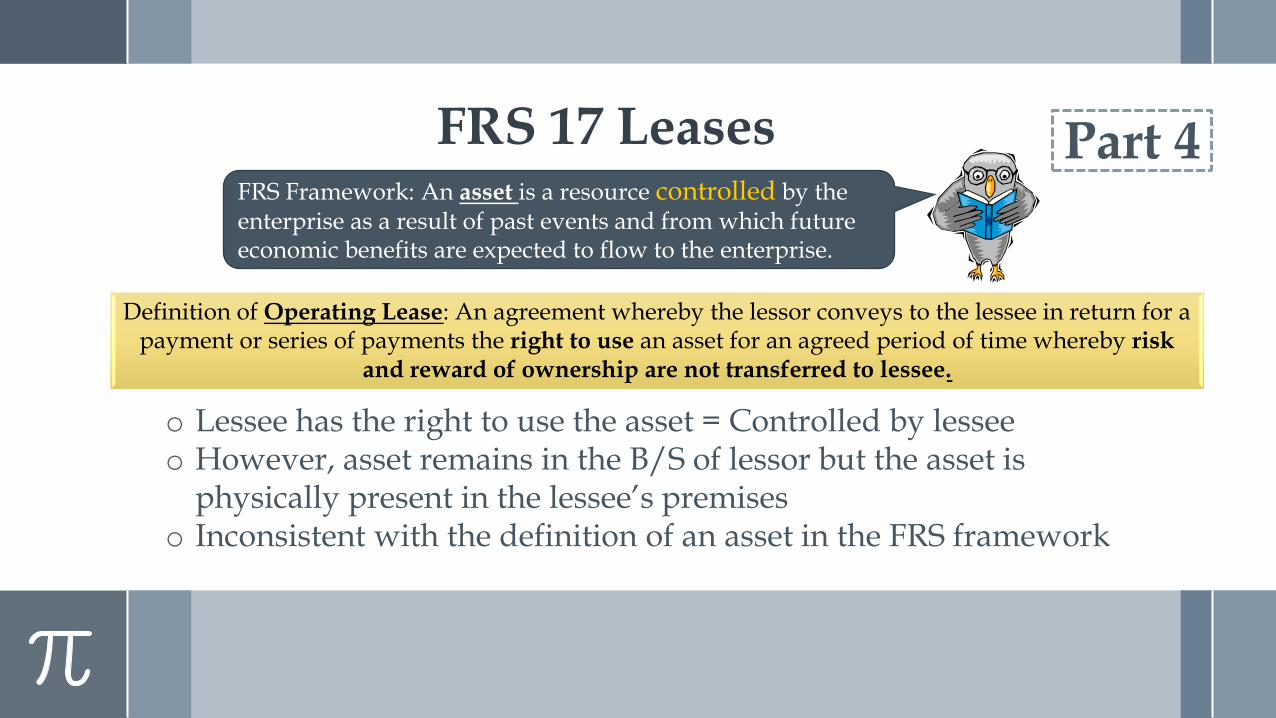

Part 4 FRS Framework: An asset is a resource controlled by the enterprise as a result of past events and from which future economic benefits are expected to flow to the enterprise.

Definition of Operating Lease: An agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of time whereby risk

and reward of ownership are not transferred to lessee.

o Lessee has the right to use the asset = Controlled by lessee o However, asset remains in the B/S of lessor but the asset is

physically present in the lessee’s premises o Inconsistent with the definition of an asset in the FRS framework

FRS 17 Leases

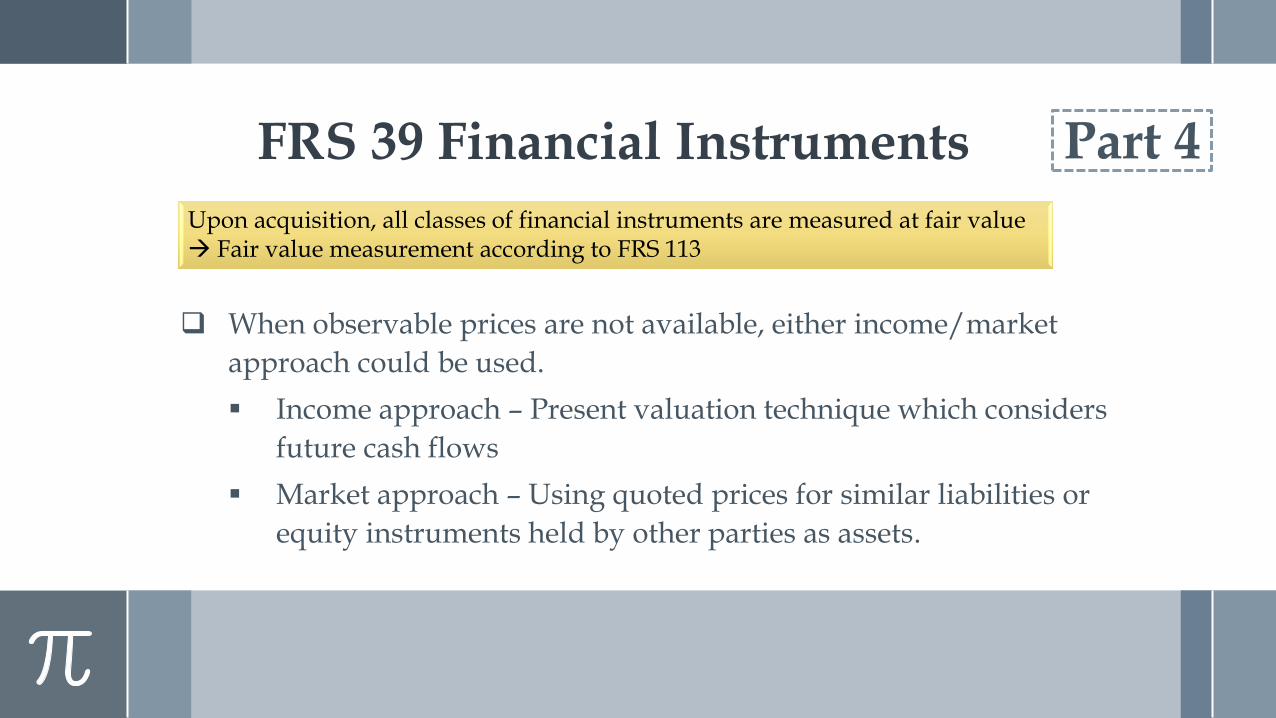

Part 4 FRS 39 Financial Instruments

When observable prices are not available, either income/market

approach could be used.

Income approach – Present valuation technique which considers

future cash flows

Market approach – Using quoted prices for similar liabilities or

equity instruments held by other parties as assets.

Upon acquisition, all classes of financial instruments are measured at fair value Fair value measurement according to FRS 113

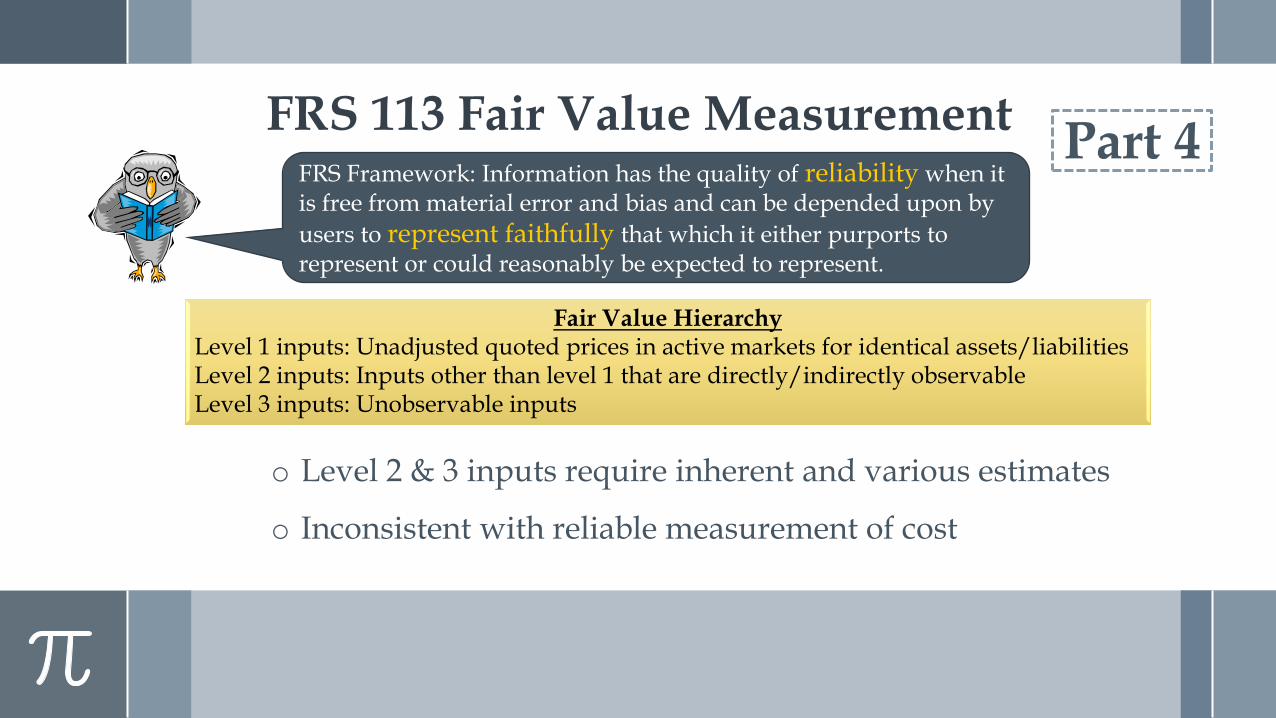

o Level 2 & 3 inputs require inherent and various estimates

o Inconsistent with reliable measurement of cost

Fair Value Hierarchy Level 1 inputs: Unadjusted quoted prices in active markets for identical assets/liabilities Level 2 inputs: Inputs other than level 1 that are directly/indirectly observable Level 3 inputs: Unobservable inputs

FRS Framework: Information has the quality of reliability when it is free from material error and bias and can be depended upon by

users to represent faithfully that which it either purports to represent or could reasonably be expected to represent.

FRS 113 Fair Value Measurement Part 4

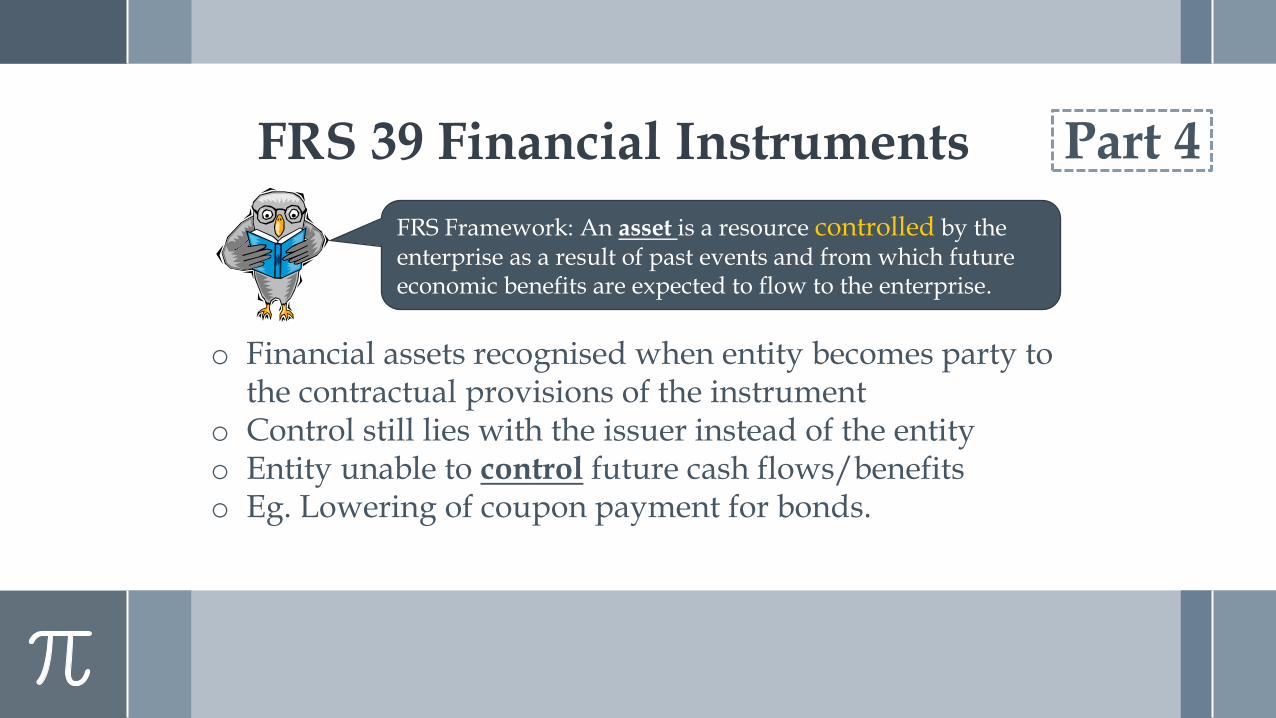

FRS Framework: An asset is a resource controlled by the enterprise as a result of past events and from which future economic benefits are expected to flow to the enterprise.

o Financial assets recognised when entity becomes party to the contractual provisions of the instrument

o Control still lies with the issuer instead of the entity o Entity unable to control future cash flows/benefits o Eg. Lowering of coupon payment for bonds.

Part 4 FRS 39 Financial Instruments

Part 4

Definition: Deferred tax liabilities are the amounts of income taxes payable in future periods in respect of taxable temporary differences.

o There is no legal obligation to pay the deferred tax expense

o Deferred tax liabilities are still recognized for accounting purposes

o Inconsistent with definition in framework

FRS Framework: A liability is a present obligation of the enterprise arising from past events, the settlement of which is expected to result in an outflow from the enterprise of resources embodying economic benefits.

FRS 12 Deferred Tax

Top Related