Languages

Pages

Legal

© LogicEase Solutions Inc.TOTAL Compliance™ Webinar Series

How to Prepare for How to Prepare for FHA and State ExaminationsFHA and State Examinations

October 14, 2008

Dial In No.: 1 (616) 883-8055Access Code: 692-552-126Help Desk No.: 1 (866) 212-3273 option 3

2

Welcome to TodayWelcome to Today’’s Webinars WebinarModerator: Jason Roth

Senior Vice PresidentComplianceEase

Speakers: Darlin McRoyalPresidentThe Darlin Company, Inc.

Shannon O'TooleDirector of Quality AssuranceU.S. Dept. of Housing and Urban Development (HUD)

Chuck CrossVice PresidentConference of State Bank Supervisors (CSBS)

3

Discussion TopicsDiscussion TopicsHow industry can prepare for examinationsHow US Dept. of HUD examines FHA lendersHow State regulators are modernizing examsQ & A - Send questions to the speakers by entering them on the Question and Answer box on the right panel…

4

Darlin McRoyalDarlin McRoyalMore than thirty years in the financial services industry Focus on risk management, credit and compliance, systems and product development, mortgage banking operations, project management and systems analysisExtensive experience in Federal and State laws and regulationsParticular expertise in Government/Agency guidelines and regulation: FHA, VA, Ginnie Mae, Fannie Mae, Freddie Mac

5

Shannon O'TooleShannon O'TooleDirector of Quality Assurance for HUD Santa Ana Homeownership CenterPreviously Dept. Head of REO for FDIC and RTC Appeared before U.S. Congress to advise on Government Lien RecoveriesDeveloped pilot programs for U.S. and CA State TreasuriesProject Manager for FEMA’s Inspector General’s office, auditing Congressional grants for earthquake retrofittingDeveloped programs for CA Department of Insurance, examining fraud, waste and abuse

6

Chuck CrossChuck CrossVice President for Mortgage Regulatory Policy for the Conference of State Bank Supervisors (CSBS)Oversees development of examination protocols and coordinated multi-state supervisionFormerly of Washington DFI Div. of Consumer ServicesServed as President for the American Association of Residential Mortgage Regulators (AARMR)Former subject matter expert and instructor for National White Collar Crime CenterCertified Fraud Examiner

Are You Prepared?Are You Prepared?

Darlin McRoyalDarlin McRoyal

8

Don’t Wait Until the Audit to Find Out!Read and understand the rules beforeobtaining license and/or FHA authority Post all licenses and other notices (HUD, State, Federal, HMDA, etc.)

9

Check Check Hiring and for transferring individual licenses, if applicable. Provide timely notification of changes and terminations; file required reports and pay feesCompensation – FHA requires W2 employees, as do many StatesRequirements for disclosures, fees, other charges, advertising and record retention

10

PerformPerformBackground and reference checks as required and document the employee file. For FHA, also check CAIVRS and the government listsQuality control and compliance reviews (manual, automated or both); and check systems periodically to assure that tests are being performed accuratelyBranch, broker (if applicable) and other third party reviewsManagement reporting and follow up

11

Maintain Maintain Files with State and/or FHA correspondence, approvals, licenses,updates, audits and responseFiles of consumer complaints and resolutionLists of investors, lenders, brokers and vendors; keep copies ofall contracts and agreementsCopies of all advertising (including websites), format, dates advertised and the marketing area. Assure that all advertising meets Federal and State requirementsUniform file stacking order; include rate sheets, invoices, reconciliation and disbursements. Assure that all files contain legible copies of all documents and disclosuresSample loan disclosures and documents (tested versions, including changes/updates)Quality control and compliance, internal audit, investor/agency;other due diligence reports

12

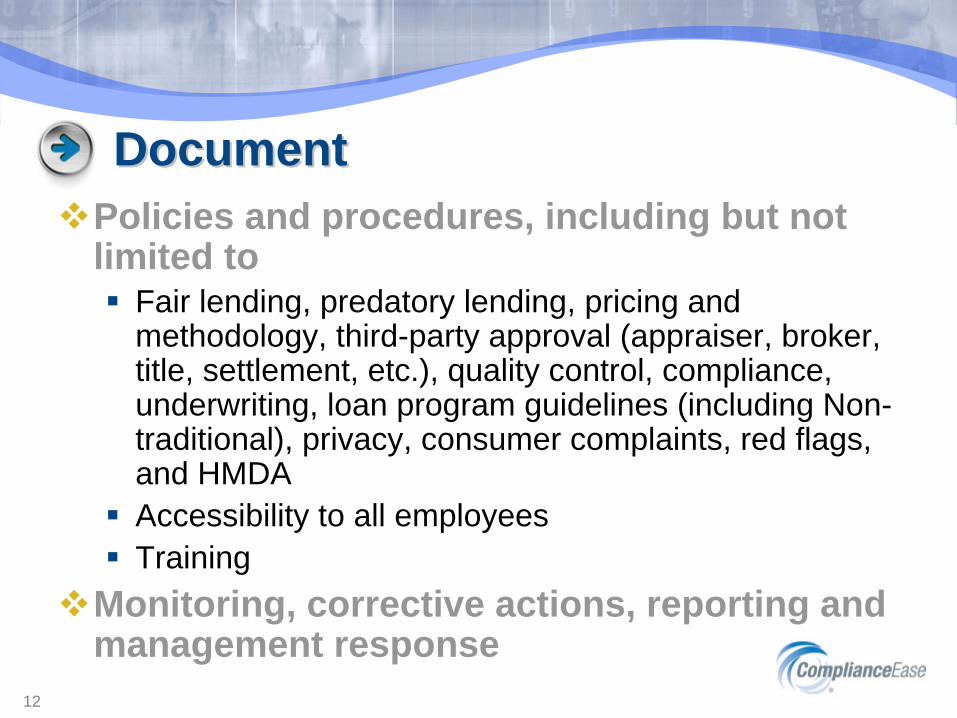

Document Document Policies and procedures, including but not limited to

Fair lending, predatory lending, pricing and methodology, third-party approval (appraiser, broker, title, settlement, etc.), quality control, compliance, underwriting, loan program guidelines (including Non-traditional), privacy, consumer complaints, red flags, and HMDAAccessibility to all employeesTraining

Monitoring, corrective actions, reporting and management response

13

BeforeBefore the Examthe ExamAsk questions, know the rules, and be cooperative. During an examination, try to clear all questions and provide any missing documentation while the examiner is performing the review

14

Systems and Data Systems and Data Not all systems are created equal. Prior to the examination, you may need to gather information from various areas, both systematically and manually Ensure that you can provide accurate data such as borrower name and property address, occupancy, loan originator, loan number, loan program and documentation type, term, lien position, interest rate, fees, APR, funding and closing dates, and other party information (appraiser, settlement, title, broker, lender, etc.)

15

Loan Files Loan Files –– locate all files locate all files Funded/closed, and Withdrawn/cancelled/deniedState and/or FHA required stacking order –legible Final HUD-1, application (initial/final), disclosures and documents, title policy, invoices, rate sheets, compliance tests, evidence of refundsSignatures, dates, evidence of timely disclosure

16

Policies and Procedures Policies and Procedures Are they current and in writing?

17

Other DocumentationOther DocumentationMay be requested

Recent balance sheets and financialsTrust accounting documentationBank statements and reconciliation Cancelled checksWarehouse bank and investor information Third party/vendor lists Employees (evidence of background checks and compensation)Originator contracts Investor and secondary market agreements Loan documents and disclosures, and more You may also be asked for foreclosure, delinquency and servicinginformation

18

FHAFHAWill also review

UnderwritingFHA Connection data (accuracy)MIP and timely payment of premiumsInsuring NOR’s (Notice of Reject)Neighborhood Watch/Credit Watch delinquency/default,EPD (early payment default)other documentation required in lender file but not submitted for insuring file (i.e. new construction, condo)

FHA does not permit net branches or dual employment

FHA ExaminationsFHA Examinations

Shannon O'TooleShannon O'Toole

20

Compliance and MonitoringCompliance and MonitoringRisk Factors

Compare ratiosNational, regional, zip code comparisonsEarly defaults and claimsProcessing and underwriting referralsHigh risk programsLate mortgage insurance premiums VolumeIndustry referrals, tips, OIG, FBIRoutine and sampleDelinquent or incomplete Lender Data Reporting

21

Neighborhood WatchNeighborhood Watch

22

Mortgagee NotificationMortgagee NotificationThe “Love Letter” as some of my monitors refer to it, is our notification to the mortgagee that they have been selected for a review

23

HUD Will RequestHUD Will RequestQuality control reviews and reports to management for the past 12 monthsA list of all employees and positions to include terminated employeesFunding LogLoan files where a repurchase request has been made for the last 12 monthsAny FHA loan for which payments are being made to investor for early payment defaultsWill probably select additional files upon arrival from Funding LogProvide the date, time and point of contacts for HUD (we are generally flexible)

24

Examination ActivitiesExamination ActivitiesOn-site

Opening interviewMonitor reviews selected files

Off-siteConduct face-to-face and telephone interview with borrowers and other partiesReverify employment, source of funds, gift, mortgage, rent and alternative credit informationPrepare the Report (Findings Letter or Referral)Address final report to President, CEO or designee

25

Lender Quality Control PlansLender Quality Control Plans

26

Data AnalysisData AnalysisCase # LO Appraiser Seller Default Units

1 Valdez Barney Kopple 2 32 Smith King Jones 33 Valdez Barney Kopple 14 Smith King Rogers 4 25 Valdez Barney Garcia 46 Valdez Barney Burnett 07 Wegman Reed Muncie 28 Johnson Lacey Martin 5 49 Legg Hergert Kane 710 Valdez Barney Andre 411 Lombardi Nichols Garcia, M 212 Bonorden Edmunds Hunsaker 013 Smith King Bacon 6 214 Flemming Johnson Martinez 215 Nichols Barney Dale 0

27

ReverificationsReverifications

28

ReverificationsReverificationsEmploymentGift lettersDeposits from acceptable sourcesBank statementsFunds from acceptable sourcesBudget lettersCredit reportsCareful examination of HUD-1’s

29

OperationsOperationsW-2 EmployeesVerifications of Licenses, dual employmentNo third party originatorsNo non-approved FHA entity participationRegistered branchesRegistered relationships

Correspondent/ Sponsor/Principal/Agent Licenses

30

Common FindingsCommon FindingsOrigination

Insufficient funds to closeImproperly documented giftNon-exclusive employees originating loansInaccurate HUD-1 line item documentation issuesProhibited branch arrangementsLack of or inadequate QC plan and reviews

ServicingFailure to review loan for, or document, loss mitigation actionsFailure to report or inaccurate SFDMS reportingUnrealistic forbearance203k Release IssuesInadequate QC reviews

31

Close Out MeetingClose Out MeetingDiscuss findingsResolve findingsImprove operations/proceduresDevelop remedial actionsAdvise of further investigations Findings letter to follow

32

QAD Findings LetterQAD Findings LetterThe violations that were found during the review are listed below and in the

Attachment to this letter:

Finding No. 1: Lender failed to adopt, implement and maintain a QC Plan in compliance with HUD/FHA requirements. Lender’s QC Plan is deficient in several elements required by HUD Handbook 4060.1 REV-2, Chapter 7.

Finding No. 2: Lender failed to document the transfer of gift funds in accordance with HUD/FHA requirements. HUD-1 Settlement Statement

reflects that the source of funds to close were from a non profit organiziation, but the file did not include a copy of the wire transfer of the gift funds. Refer to HUD Handbook 4155.1 REV-5, paragraph 2-10C the FHA TOTAL Mortgage

Scorecard User Guide and Mortgagee Letters 04-28 and 04-47.

Finding No. 3: Lender failed to ensure that its employees underwrote FHA insured loans. Refer to Handbook 4060.1 REV-2, paragraph 2-9G.

Please provide your response to this office within 60 days from the date of this letter.

33

What is Next?What is Next?Mortgagee Board ReferralState Regulator ReferralInspector General Referral

34

Corrective ActionsCorrective ActionsSuspensionLimited Denial of Participation (LDP) in HUD programsDebarment from future participation in HUD programsCivil money penaltiesLoss mitigation

35

Ongoing CommunicationOngoing CommunicationLender responseOpen communicationApplication of RemediesFollow up

State ExaminationsState Examinations

Chuck CrossChuck Cross

37

A Responsive State SystemA Responsive State System

RESPONSE(INITIATIVE OR PROCEDURE)

IMPLEMENTATION

IDENTIFIED NEED

38

Major Examination InitiativesMajor Examination InitiativesModel Examination Guidelines (MEGs) for the implementation of Guidance and StatementNationwide Cooperative Protocol and Agreement for Mortgage SupervisionFed/State Pilot Examination projectDevelopment and implementation of examination software

39

Model Examination Guidelines (MEGs)Model Examination Guidelines (MEGs)

Genesis was in the 2006 Guidance on Nontraditional Mortgage Product Risks and the 2007 Subprime Lending StatementThe need was an interpretive tool and guide for examiners and financial institutions to use in complying with the Guidance and Statement

40

MEGs ConceptMEGs ConceptA “top down” versus “bottom up” approach to examinations

Policies, practices and business cultureManagement, management, management

A template of questions triggering examiners to “think” and “respond” to an institution’s compliance, consumer protection and safety and soundness risk

Compare management intentions to institution performance

41

Goals of MEGsGoals of MEGsCreate efficiency in examination process

Lenders know what is expected of themExaminers have standard methodology to follow

Guidelines are available to the industryInstitutions can use guidelines and available technology in-house as self-regulationEnables management to prepare for new exam process

Drive uniformity, standardization, and objectiveness in examinations

42

Modular DesignModular DesignModule 1 – Instructions and ScopingModule 2 – Examiner ChecklistModule 3 – Company InformationModule 4 – Management QuestionnaireModule 5 – Examination SoftwareModule 6 – Report Writing and Follow-Through

43

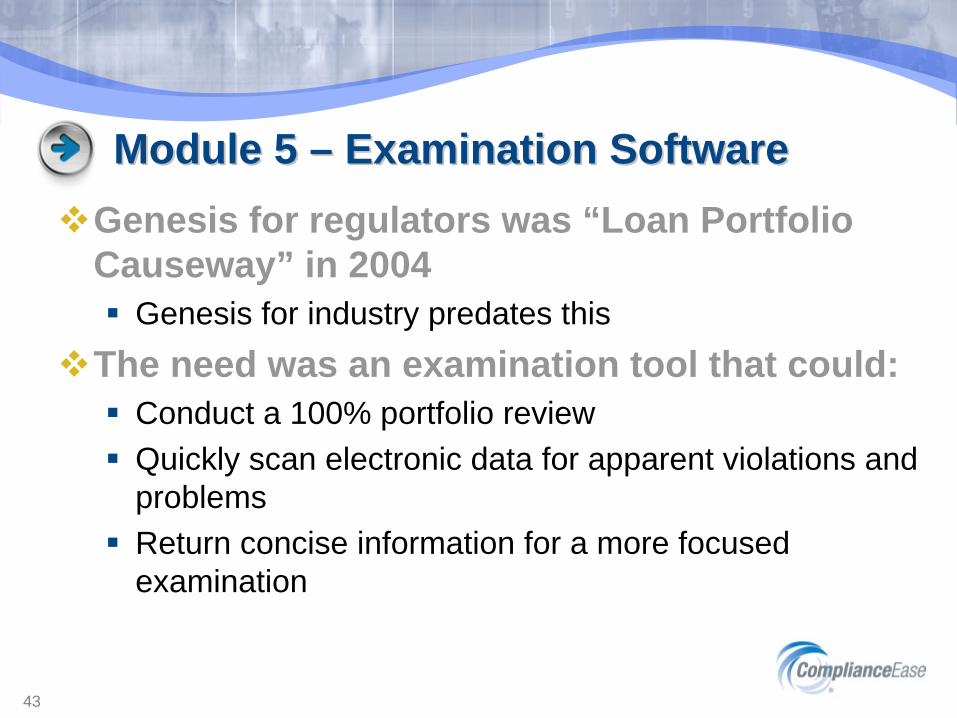

Module 5 Module 5 –– Examination SoftwareExamination SoftwareGenesis for regulators was “Loan Portfolio Causeway” in 2004

Genesis for industry predates this The need was an examination tool that could:

Conduct a 100% portfolio reviewQuickly scan electronic data for apparent violations and problemsReturn concise information for a more focused examination

44

Evaluation and Implementation Evaluation and Implementation CSBS began vetting vendor products in 200714 states tested 3 vendors over an 8 month periodIn the end, the states chose ComplianceEase’s ComplianceAnalyzer® & RegulatorConnect™ solutionsCSBS signed up in May 2008, AARMR in Sept 2008State-by-state implementation commenced in JuneTarget to have all 50 states and DC implemented by end of 2009

45

How It Works How It Works –– Data SubmissionData SubmissionInstitutions respond to the state’s Entry Letter by uploading transaction level data through a secure portal called RegulatorConnect.orgThe examiner retrieves the data and uploads to ComplianceAnalyzer software

Employs rules engine of laws, regulations, and calculations (e.g. APR, Truth-in-Lending, Sec. 32, etc.)Identifies apparent violations of law and regulation or highlights potential trouble areas

46

How It Works How It Works –– Audit ReportsAudit Reports

A report of analytical findings is producedThe examiner reviews the findings and uses the information:

To identify the necessity of an onsite exam or to narrow or broaden the exam focusTo focus resources on potential problem areasTo assist in making recommendation

47

Benefits of Software Benefits of Software Time and cost savings for both regulators and industry

Companies with few exceptions may not even be examinedFacilitates offsite exams

The ability to do more with less100% file reviewChecking APRs or High Cost loan limitsSystem performs the legal research and “remembers”all of the laws and regs so the examiner doesn’t have to

48

49

MultiMulti--agency Examinationagency Examination

Genesis was the realization of a “fractured” or “segregated” system of regulationDevelop a better way of supervising in the modern regulatory worldNationwide Cooperative Protocol and Agreement

Focused on multi-state mortgage entities (MMEs)Creates an oversight board

4 Federal/State pilot examinations conducted in 2008

50

How Can Companies Prepare for the How Can Companies Prepare for the Future of State Exams? Future of State Exams?

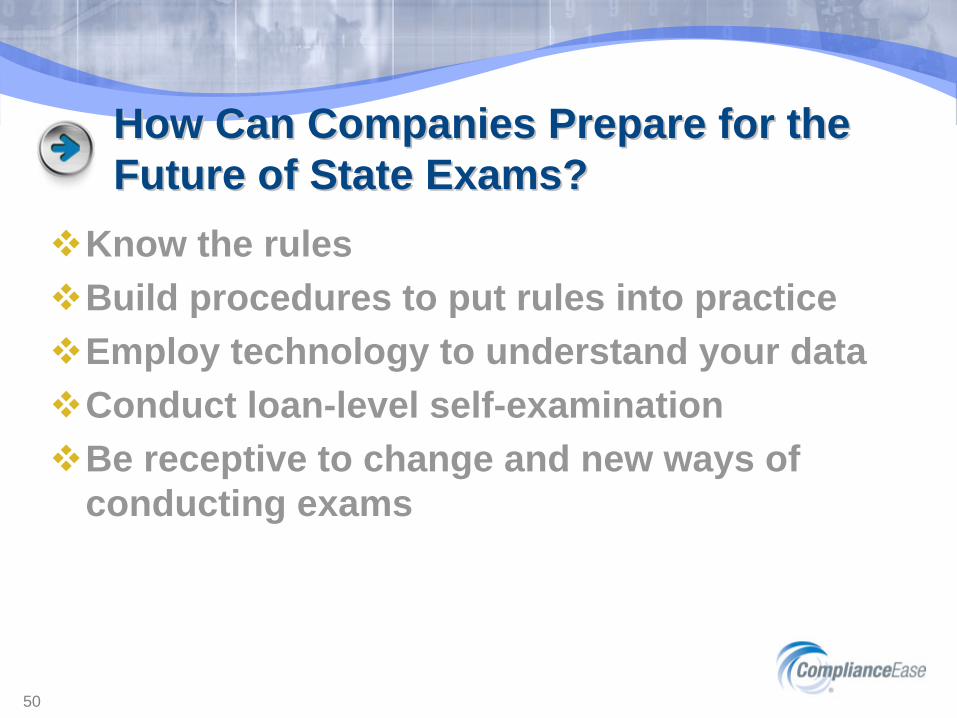

Know the rulesBuild procedures to put rules into practiceEmploy technology to understand your dataConduct loan-level self-examinationBe receptive to change and new ways of conducting exams

51

Q & AQ & ASend your questions to the Speakers by entering them on the Question and Answer box on the right panel…

52

Speaker ContactsSpeaker ContactsDarlin McRoyalThe DARLIN Company, [email protected]

Shannon O'TooleDepartment of HUD1.714.796.1200 Ext. 3614shannon.o'[email protected]

Chuck CrossConference of State Bank Supervisors (CSBS)[email protected]

53

Evaluation and Webinar ArchiveEvaluation and Webinar ArchiveAn Event Evaluation Email will be sent to you after this Webinar. Your feedback is very important for us to improve our future events.Archived Webinar will be ready for download on October 16th at ComplianceEase.com

© LogicEase Solutions Inc.

ComplianceEase.com

Thank You for Your Participation!Thank You for Your Participation!

Top Related