![Slip Op. 13-94 UNITED STATES COURT OF … STATES COURT OF INTERNATIONAL TRADE ALCAN FOOD PACKAGING (SHELBYVILLE), ... the first retort pouch rations ... of the thickness, [[ ]] ...](https://static.fdocuments.us/doc/165x107/5ac28ca47f8b9a1c768e1f00/slip-op-13-94-united-states-court-of-states-court-of-international-trade-alcan.jpg)

Languages

Pages

Legal

European Plastic PackagingM&A update

Spring 2012

The plastic packagingindustry in Europe is valuedat €€38 billion annually,accounts for a quarter ofglobal supply and generatednearly half of all M&Atransactions in the sector.

This report highlights boththe opportunities andchallenges for Europeancompanies in the sector.

The key observations fromour research:

Over the past three years almost half of all global M&A deals in the plasticpackaging sector took place in Europe,attracting both trade acquirers andfinancial investors.

Whilst some segments of the industry,such as flexible food packaging, aredominated by a few large players theEuropean industry as a whole remainshighly fragmented. We expectconsolidation trends to continue.

Private equity firms have beensignificant investors. The commontheme has been for private equity firms

to grow initial ‘platform’ investmentsthrough bolt-on acquisitions, takingadvantage of operational synergies.

Cross-border deals accounted for 40%of all transactions in 2011. Much of thisis attributable to the global sourcingrequirements of major customers.

Typical acquisition multiples haveremained at between 5x and 7x EBITDAover the past three years. Howeverhigher acquisition multiples have beenpaid for some companies, particularlythose offering niche products.

Europe dominatesglobal M&A activity

Highly fragmentedindustry creating

consolidationopportunities

European plastic packaging on theroad to consolidation

“Plastic packaging is becominga global affair, innovation isongoing as companies strive tosatisfy demanding customersand end users. These factorsare driving consolidation”Jean-Pierre Brice, Partner

Cross-border dealsare a major feature

of M&A

UK 3.76m t (6.6%)

France7.53m t (13.3%)

Benelux 11.30m t (20%)

Other European6.44m t (11.3%)

Italy4.90m t (8.7%)

Germany22.67m t (40.1%)

Production Consumer Demand Recovery

Electrical & Electronic (6.0%)

Automotive (8.0%)

Construction (21.0%)

Other (26.0%)

Packaging (39.0%)

Food51%

Beverage18%

Cosmetics5%

Healthcare6%

Other20%

PS 4.7%

PUR 6.7%

PET 8.6%

LDPE 11.5%

HDPE 17.9%

PVC 11.3%

PP 18.6%

Other 20.7%

Recycling and Energyrecovery 66%

Disposed to Landfill 34%

Conversion

57 million tonnesProduced

46 million tonnesConverted

PS (Polystyrene) e.g. DVD casesPUR (Polyurethane) e.g. Phone casesPET (Polyethylene terephthalate) e.g. Plastic bottlesPVC (Polyvinyl chloride) e.g. Blister packsPP (Polypropylene) e.g. StationeryPE (Polyethylene) e.g. Plastic film

Plastic Types

End Market

Industry trendsPackaging is the largest user ofplastics in Europe, representing 39%of the overall 46 million tonnes usedin plastic conversion (see Figure 1).

Although there are some downsides toplastic packaging (e.g. raw materialfluctuations) it also holds many inherentadvantages over other packaging materialsincluding flexibility, cost and its ability toadjust to new innovations and technologies.Plastic now accounts for the largest shareof the packaging market followed by paper.

Rigid packaging accounts for around 60%of total production volume. The currentgrowth in demand for rigid packaging islargely being driven by the beverage andpersonal care markets.

Flexible packaging is being boosted fromsectors like perishable and conveniencefoods, healthcare, and industrials.

Whilst the development in end user marketsis crucial to the industry’s performancethere are a number of other importantconsiderations:

The softening in recycled plastic pricesevidenced in H2 2011, partly as a resultof weakening export markets, is likely toreverse this year as exports start torecover (see Figure 2). A similar trend in virgin prices is also likely.

EU legislation is significantly impactingon recycling volumes. The updateddirective on Packaging and PackagingWaste coupled with the rising rawmaterial prices are increasinginvestment in closed loop processes.

European Plastic Packaging M&A update

Figure 1: Plastic packaging market structure

Raw material costslikely to rise in 2012

Source: Mergers Alliance, Plastics Europe MRG, Rexam

2

Figure 1: Plastic packaging market structure

European Plastic Packaging M&A update

PET Glass Metal Others

0

5

10

15

20

25

30

35

40

2004 2009 2014

Figure 3: Share of total beveragepacking (%)

Source: Euro monitor, BPI

Whilst around half of all consumergoods are packaged in plastic, thisamounts to just 17% of all packagingweight, a reduction of 28% in the last10 years. The significant investmentrequired to achieve these returns is afurther contributor to the consolidationin the sector.

The rigid food and beverage packagingmarket is forecast to increase inimportance, with growth rates forecastat 3.7% over the next three years, twice the industry average.

PET is experiencing significant growth in volume in the consumer markets.PET’s functional and light weightcharacteristics should ensure steadygrowth (see Figure 3). It is alsoincreasingly replacing segments that have traditionally been dominatedby other materials for example glassbeer bottles.

Certain European consumer companiesare moving towards sustainablepackaging, with the bioplastics segmentin particular experiencing increaseddemand. Cleaning products brandEcover recently announced that all of its packaging will be made from plantbased plastic made from sugarcane.

The emerging markets of EasternEurope, Asia and South America haveall benefited from significant investmentfrom larger international suppliers asopportunities for growth are sought.Evidence of this is seen in AMCOR’sgrowth in these regions of 18% p.a.between 2000 and 2011. RPC Groupand Constantia Flexibles are activelyseeking mid-market opportunities inthese emerging markets. To remaincompetitive European manufacturersneed to ensure they are present in these regions.

Environmental factorsinfluencing packaging

materials

Emerging markets aretarget regions for

multinationals

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

PET

HPDE Blow moulding standard

HPDE Injection moulding grade

Figure 2: Polymer price €€ pertonne

Source: Mergers Alliance

3

-100.00%

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Mar-20

02

Aug-20

02

Jan-2

003

May-20

03

Oct-20

03

Mar-20

04

Aug-20

04

Jan-2

005

Jun-2

005

Oct-20

05

Mar-20

06

Aug-20

06

Jan-2

007

Jun-2

007

Oct-20

07

Mar-20

08

Aug-20

08

Jan-2

009

Jun-2

009

Nov-20

09

Mar-20

10

Aug-20

10

Jan-2

011

Jun-2

011

Nov-20

11

Mergers Alliance Index MSCI World Industrial Index

Figure 4: Plastic packaging composite valuation index

Source: Capital IQ

Mergers Alliance Index: Amcor, Rexam, DS Smith, Huhtamaki Oyj, MacFarlane Group, British Polythene Industries, Resilux NV, RPC Group, La Seda de Barcelona

Current valuationsThe past decade has seen plasticpackaging valuations slightly exceed ortrack wider industrial market indices, areflection of the defensive nature of the

companies in our index, which haverobust earnings and dividend policies.

The global recession put downwardpressure on valuations, however ourresearch has shown a marginal recoveryover the last 12 months.

4

PET recoversPET imports into Europe from Asiaincreased dramatically in 2009 toreach 0.9 million tonnes, a historicalhigh. Asian companies were able toescalate their exports at highlycompetitive prices due to their higherproduction efficiency and the lowercosts of local raw materials.

This, along with slowing demand in Europe, meant that PET pricesplunged – 33% below the current price level. The EU initiated anti-dumping laws to counteract the lowimport prices and protect Europeancompanies.

These quasi protectionist measureswere effective in bringing down PETimports to around 0.5 million tonnes in 2011 with prices regaining much of the lost ground.

2008 2009 2010 20110

200

400

600

800

1000

Impo

rts

Imports

European PET imports (k tonnes)

Source: PCI, BPI and Bloomberg.

Valuations reflectconsistent earnings

performance

Europe alert tointernationalcompetition

European Plastic Packaging M&A update

5

European Plastic Packaging M&A update

Figure 5: Top 15 global plastic packaging companies

Amcor Ltd. Australia Global (Australia, 6,916 9,932 990 6.1% 7.2x 10.0% 2.4% Dominate European flexible market. (ASX:AMC) the United States,

and Singapore)

Rexam plc United Global (US, 4,050 5,567 838 3.4% 7.2x 15.1% 4.2% Recently announced the sale of its(LSE:REX) Kingdom Brazil, Europe) plastic lid-making division to Berry Plastics

for €267m.

Bemis Company, Inc. United Global 2,530 4,096 494 5.5% 7.4x 12.1% 2.5% Acquired Finnish based Huhtamaki Oyj's(NYSE:BMS) States (sub-companies South American operations in 2009.

in 13 countries)

Berry Plastics United Global (US, Private 3,494 493 5.6% na 14.1% 12.4% Recently acquired Linpac PackagingCorporation States Brazil, Germany) Filmco from Linpac for €15m.

Sonoco Products Co. United Global 2,409 3,444 423 6.8% 8.1x 12.3% 4.8% Has been acquiring across the supply (NYSE:SON) States (US, UK, China) chain in North America with deal value

totalling €508m.

DS Smith plc United Europe (UK, 1,255 3,218 270 7.4% 4.9x 8.4% 9.6% Planning integration of SCA. May divest(LSE:SMDS) Kingdom France, Belgium) plastic operations.

Alpla-Werke Alwin Austria Global Private 2,900 na 16.1% na na na Has not engaged in M&A of late, hasLehner GmbH est focused instead on greenfield & Co. KG investments.

Silgan Holdings Inc. United Americas, 2,173 2,593 353 8.9% 8.1x 13.6% 6.0% European acquisitions have been(NasdaqGS:SLGN) States Europe, Asia confined to metal packaging companies

of late.

Graham Packaging United US, Europe, Private 2,127 394 8.3% na 18.5% 5.6% In 2010 it acquired China Roots Packaging,Holdings Company States China its first manufacturing facility in China.

Huhtamaki Oyj Finland Global (Europe, 973 2,064 203 2.5% 6.7x 9.9% -1.0% Sold its European rigid plastic consumer(HLSE:HUH1V) US, Australasia) goods operations to Sun Capital for €52m.

Constantia Austria Global (Europe, 1,838 1,838 297 3.9% na 16.1% 4.3% Recently acquired Asas in Turkey andPackaging AG US, China) Alcan's food packaging operations in

Spain.

AptarGroup, Inc. United US, France 2,642 1,780 322 8.6% 8.5x 18.1% 6.0% Acquired India based plastic packaging(NYSE:ATR) States company T.K.H. Plastics for €14m.

FP Corp. Japan Global 880 1,285 194 6.8% 6.3x 15.1% 6.3% Has been active in acquiring packaging(OSE:7947) companies in Japan and China.

Linpac Group United Global Private 1,231 108 -0.4% na 8.7% 5.2% Has been divesting its non-core operationsLimited Kingdom to both trade and financial buyers of late.

RPC Group plc United Europe 1200 1,105 122 9.4% 8.3x 11.1% 23.6% After its acquisition of Superfos Industries(LSE:RPC) Kingdom it is known to be seeking further

acquisitions in Europe.

EBITDA EBITDA, Countries of 3 Yr Margin 3 Yr CAGROperation Market Cap Revenue LTM EBITDA Revenue % % [LTM]

Name HQ Country (Primary) (€) Million (€) Million (€) Million CAGR EV/EBITDA [LTM] (%) Rigid Flexible Comments

Companies with disclosed revenue only

Source: Mergers Alliance, Capital IQ

Trade buyer activityOver 100 transactions were completedin the past 18 months. Deal volume for2011 equalled the deal volume for 2010and surpassed the lows of therecession.

The common theme over the past twoyears has been for the medium to largesized companies to buy up smaller playersto achieve their growth initiatives.

The ‘serial acquirers’ in Europe have oftenbeen the bigger companies, such as RPCand Constantia Packaging (PE owned),seeking to strengthen their position in theproduction and technology chain, growmarket share, ‘follow’ their clientsgeographically and react to the ‘bulking’trends of the larger global players (seeFigure 6).

M&A activity demonstrates two key themes;the consolidation taking place withinEurope; and the opportunities arising fromdistressed situations as a result of thepressures of operating in these markets.

The largest deal of the past four yearsinvolving a European target wascompleted by an Australian buyer.Amcor, the world's largest manufacturerof plastic bottles, purchased Alcan’sflexible packaging business in 2010 for€1.5bn giving Amcor c. 25% marketshare and further consolidating flexiblepackaging in Europe.

Highly acquisitive, Amcor has alsobought smaller mid-market companiessuch as Italian based B-Pack Due(€45m).

European flexible companies havereacted to Amcor’s increasingdominance by making acquisitions of their own, with Constantia being oneof the more prominent buyers. Theyacquired Asas in Turkey (sales of €63m)and Alcan’s food packaging operationsin Logrono and Burgos, Spain.

In rigid plastic packaging RPC Grouphas also employed M&A to meet theirgrowth ambitions. During the past four

years they have made threeacquisitions: Superfos Industries;DM Plast; and MOB SAS.

The acquisition of Denmark basedSuperfos for €240m gives RPC accessto a variety of markets including EasternEurope and Scandinavia. RPC is knownto be seeking further acquisitions toexpand its pan-European operations.

The most high profile distressed salesoccurred in 2009, including CanalCorporation (formerly ChesapeakeCorp) and Budelpack, and failure stilloccasionally occurs in the small to midsized market. LIR Packaging, whichproduces cosmetic product packagingand Sedis, the French confectioneryand pastry packager have both recentlyannounced insolvency proceedings.This creates opportunities for ‘value’and turnaround acquirers.

Analysis of plastic packaging industrydeals over the last decade shows thatthe majority (58%) of acquisitions aremade of direct competitors. Of the othertargets: 13% are distributors; 13%printing companies; 8% competitors indifferent sectors (majority being paperpackaging); and 8% are of othercompanies (e.g. recycling plants). Thisshows clear consolidation strategiesand that moves into more peripheralsectors are less common.

6

Majority ofacquisitions are ofdirect competitors

“Superfos was a significantacquisition for RPC and wasconsistent with our currentstrategy of growing the businessorganically and through acquisition”Jamie Pike, Chairman at RPC

AMCOR dominatesflexible markets

European Plastic Packaging M&A update

7

Date Target Description Plastic Type (Target) BuyerDeal Value (€’m)

Jan-12 SCA Packaging (BE) Plastics and paper consumer goods packaging Flexible and Rigid DS Smith (UK) 1,650

Jan-12 Geka (Ger) Cosmetics packaging Rigid 3i (UK) ND

Jan-12 Linpac Allibert (UK) Plastic returnable transit packaging Rigid One Equity Partners

LLC (USA) ND

Oct-11 Johnsen & Jorgensen Group (UK)

Plastic and glass packaging Flexible and Rigid Pont Packaging

(NL) ND

Aug-11 Interpack (UK) Plastic packaging distributor Rigid Coral Products

plc (UK) 5

Aug-11 Pack2Pack (BE) Industrial packagingmanufacturer Rigid Greif Inc (USA) ND

Aug-11 ASAS (Tur) Plastic products manufacture Flexible Constantia packaging

AG (Aut)ND

Jul-11 Medisize Corporation (Fin) Pharmaceutical primary packaging Flexible and Rigid Phillips Plastics

Corporation (USA) 100

Jul-11Rexam Plc, Beverage and Speciality Closures Business (UK)

Beverage plastic packaging Rigid Berry Plastics

Corporation (USA) 251

May-11 Sterilin (UK) Life sciences plastic packaging Flexible and Rigid Thermo Fisher

Scientific, Inc (USA) ND

May-11 Pannunion Packaging Ltd (Hun)

Production of plastic packaging materials Rigid Sun Capital

Partners (USA) 36

Apr-11 Atlantis-Pak Co Ltd (Rus) Flexible plastic packaging for meat products Flexible Agrokom Group (Rus) 73

Apr-11 Britton Group (UK)

Flexible packaging group, plastic and other materials Flexible Sun European

Partners, LLP (UK) 101

Dec-10 CFS B.V. (NL) Packaging equipment Flexible and Rigid GEA Group AG (Ger) 435

Dec-10 Superfos Industries (Den)

Injection moulded rigid packaging Rigid RPC Group plc (UK) 240

Dec-10 Nampak Cartons (now Contego Packaging) (UK)

HDPE packaging for food and drink Rigid Platinum Equity

(USA) 77

Aug-10 Bilcare Research (Ger) Pharmaceutical packaging Flexible and Rigid Bilcare GmbH (Ger) 100

Jul-10 Albéa (Fra) Cosmetics and personal care packaging company Flexible and Rigid Sun European

Partners, LLP (UK) 110

Jan-10 CV Flexible Packaging (Ger) Flexible packaging Flexible Packaging and Technology Ltd (UK) ND

Jan-10 Kalle (Ger) Plastic sausage casings Flexible Silver FleetCapital (UK) 213

Nov-09 Petainer (Swe) Eco PET packaging Rigid Next Wave Ventures WHEB VENTURE (UK) 18

Oct-09 Constantia Packaging AG (Aut)

Packaging holding company Flexible One Equity Partners

LLC (USA) 1,104

Aug-09 Majority of Alcan Packaging Businesses (Sui)

Plastic, aluminium and packaging Flexible and Rigid Amcor Ltd (Aus) 1,497

Figure 6: Selected European plastic packaging deals

Source: Capital IQ, Corpfin

European Plastic Packaging M&A update

Plastic packaging atarget sector for someprivate equity houses

Private equityinvestmentSince 2009 a fifth of all Europeanplastic packaging deals have hadprivate equity participation. A largeproportion of higher value deals havebeen completed by financial investors.

Global private equity investment inEurope has been broad and has had animpact in consolidating both the rigidand flexible market. The most activefirms include One Equity Partners, ABTraction, Sun Capital and PlatinumEquity. Deal values have ranged from€10m to over €1bn.

Although their focus has been primarilyon consumer goods (FMCG) there hasbeen rising involvement in industrial andcommercial end markets.

There are two models in evidence in the mid-market:

PE employ buy and build strategies(building up established companiesthrough smaller bolt-on’s) to createvalue for their ‘mature’ companies.

Sun Capital for example has assembleda large portfolio of European plasticpackaging businesses having madeseven mid-market acquisitions inEurope since 2007. Their portfolio nowincludes Kobusch-Sengewald GmbH,Unterland, Britton Flexibles, BettsGlobal, Albéa and Acorn SAS.

By combining existing affiliated portfoliocompanies Sun Capital has created apan-European flexible packagingspecialist, Britton Group, and a pan-European rigid packaging specialist,PACCOR. Annual turnover of thecombined businesses will beapproximately €680m.

8

Private equity firmshave backed buy &

build strategies

Retail Ready Packaging (RRP) orshelf-ready packaging is designed tobe easily placed on the shelf withoutthe need for unpacking or repackingand is typically made up of rigidplastic, fibreboard or corrugatedboard.

RRP is recognised as delivering higher efficiency in the supply chainand this segment is expected to growsignificantly across continental Europewith a tonnage CAGR of 6%.

While the UK and German marketsalready have high penetration rates,most of continental Europe is still arelatively immature market and iswhere most of the growth will take place.

‘Retail Ready Packaging’

RRP penetration by country

Red: High penetration of RRPGreen: Medium penetration of RRPBlue: Developing RRP

Source: igd.com

RRP a key target formultinationals

European Plastic Packaging M&A update

9

PE firms are also focusing on nicheplastic packaging companies.

Good examples of this included theNext Wave Ventures and WHEBVentures acquisition of Swedish ecofriendly PET specialists Petainer for€18m and Silver Fleet Capital’sacquisition of Germany based Kalle, an innovator and producer of flexibleplastic sausage casings (€213m). Thegrowth strategy for both these privateequity funds is to invest in companiesthat offer innovative and value addingsolutions.

Financial buyers have also been keenlyfocused on the plastic packagingmachinery segment with a notableinterest in the Italian market. Activityincluded PE house IGI SGR acquiringItalian based plastic film machineryspecialists Gruppo Fabbri for €40m in2011. Meanwhile the Chinese-EuropeanPE fund Mandarin Capital Partnersacquired a minority stake in one of theleading global manufacturers ofmachines for plastic packaging,Industria Macchine Automatiche, for €30m.

Private equitytargeting machinery

segment

Prospects for M&Aand the industryThe whole plastics packaging industryis closely linked to economic growthand consumer confidence.

As much of Europe is still being affected bysovereign debt issues it is inevitable that theindustry’s growth prospects in the near termwill be affected. Nevertheless, the fact thatthe sector exhibits a low level of demandvolatility should ensure steady growth inthe medium term.

Looking ahead, the high growth indemand for both rigid and flexibleplastic packaging – as FMCGcompanies look for the more versatileoptions to glass and metal – willencourage acquisitions as businessesseek to meet customer’s demands.

In the flexible market, Amcor/Alcan’sindustry dominance will continue todrive consolidation as companiesacquire to compete.

As well as the traditional markets weexpect a new wave of acquisitions in Eastern Europe where flexiblepackaging is experiencing an average 6.2% sales growth.

The increasing demand for recycled and biodegradable products as well a focus on the afterlife of a packageshould also encourage verticalintegration by firms looking to expand their product portfolio.

Adaptability drivinggrowth in plastic

packaging

European Plastic Packaging M&A update

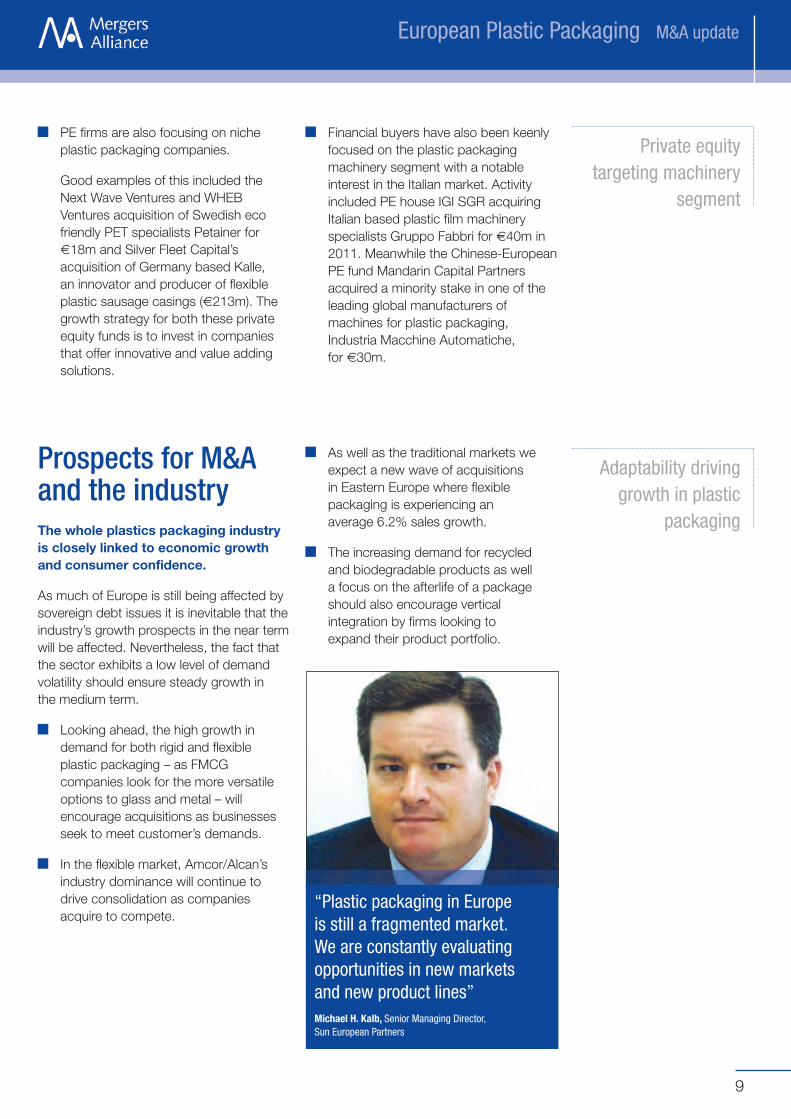

“Plastic packaging in Europeis still a fragmented market.We are constantly evaluatingopportunities in new marketsand new product lines”Michael H. Kalb, Senior Managing Director, Sun European Partners

The ten largest transactions comprisedc.73% of the total value over the pastfour years. If you exclude these largerdeals, average deal size has beenbelow the €50m marker indicating thatthe mid-market has experienced themost activity. Due to the still fragmentednature of the market we expect thistrend to continue.

We expect that some of the larger dealsin the future will be in the form of the bigdiversified players divesting either partor all of their plastic packagingoperations. This is likely to includeRexam’s personal care plasticpackaging business and DS Smith’sentire plastic division.

Almost half of all transactions werecross-border in 2011. The steady rise incross-border activity since 2009 is likelyto continue as companies look to buildscale, lower transport costs, increasemarket share and expand theirgeographical footprint.

Specifically, we expect Europeanplayers to buy other Europeancompanies as they seek to consolidatethe market and cover any ‘blind spots’while US players will look to takeadvantage of the challenging macroconditions in Europe, surveyingcompanies with high potential.

ContactsSpecialist advice on call…For information on sector trends, valuations and corporate finance advice in plastic packaging

Leonardo AntunesManaging Director, Brazil

Telephone: +5521 3873 8000Email: [email protected]

Bart JonkmanManaging Partner, Netherlands

Telephone: +31 73 623 8774Email: [email protected]

Jean-Pierre BricePartner, France

Telephone: +33 148 246 300Email: [email protected]

Piotr OlejniczakDirector, Poland

Telephone: +48 22 236 9200Email: [email protected]

Ervin SchellenbergManaging Partner, Germany

Telephone: +49 611 205 4810Email: [email protected]

David WolfeSenior Partner, Russia

Telephone: +7 495 937 5855Email: [email protected]

Ankur GuptaManager, India

Telephone: +91 11 4617 0860Email: [email protected]

Igor GorostiagaPartner, Spain

Telephone: +34 944 352 311Email: [email protected]

Piero ManaresiPartner, Italy

Telephone: +39 051 59 47 309Email: [email protected]

Richard SandersPartner, United Kingdom

Telephone: +44 121 654 5000 Email: [email protected]

Owen HultmanExecutive Vice President, Japan

Telephone: +81 3 6895 5521Email: [email protected]

Doug UsiferManaging Director, USA

Telephone: +1 (802) 658 7733Email: [email protected]

10

European Plastic Packaging M&A update

11

Country focus M&ABenelux:

European cross-border transactions have beencommonplace of late, and includes notable transatlanticinterest in the Benelux region. US-Benelux deals includedGreif, Inc acquiring industrial packaging specialistsLigtermoet and Alpha Plastics acquiring PET specialistsSmartPET.

France:M&A activity has evolved around companies looking toincrease their product offering or increase their marketshare. Regardless of their intentions, companies havebeen reluctant to overpay for fixed assets.

Germany/Austria/Switzerland:Private equity investment has been broad over the past18 months. Deals include cosmetics packaging firmGeka acquired by 3i and Bayern LB’s PE division’sacquisition of a majority stake in Rebhan for anundisclosed amount.

Italy:In one of the more notable trade deals of 2011 high densitypolyethylene specialists Fustiplast was acquired by Dutchindustrial packaging company Greif International Holding BV.Fustiplast generated revenues of €472m in 2010.

Poland:Although transactions have stalled recently we expectthe high growth domestic plastic packaging market toencourage an upswing in M&A activity over the next18 months.

Spain:Despite a highly fragmented market in Spain, M&Aactivity has been moderate and outbound deals fewand far between. Distressed macro-conditions andcredit restrictions have contributed to this. There arehowever opportunities to consolidate the market forthose with strong balance sheets.

United Kingdom:Over a third of all privately owned plasticpackaging companies in the UK are ownedby owners/managers approaching retirement.We expect them to drive M&A activity.

FranceGermanyItalyNetherlandsSpainUKPolandRest of Europe

12%

10%

8%

4%

14%18%

4%

30%

Plastic packaging companies by country (%)

Source: Capital IQ

56%

44%

60%

40%

64%

36%

63%

37%

75%

25%

77%

23%

INBOUND INBOUND

INBOUNDINBOUND INBOUND

INBOUND

OUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUND

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

56%

44%

60%

40%

64%

36%

63%

37%

75%

25%

77%

23%

INBOUND INBOUND

INBOUNDINBOUND INBOUND

INBOUND

OUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUND

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

56%

44%

60%

40%

64%

36%

63%

37%

75%

25%

77%

23%

INBOUND INBOUND

INBOUNDINBOUND INBOUND

INBOUND

OUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUND

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

56%

44%

60%

40%

64%

36%

63%

37%

75%

25%

77%

23%

INBOUND INBOUND

INBOUNDINBOUND INBOUND

INBOUND

OUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUND

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

56%

44%

60%

40%

64%

36%

63%

37%

75%

25%

77%

23%

INBOUND INBOUND

INBOUNDINBOUND INBOUND

INBOUND

OUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUND

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

56%

44%

60%

40%

64%

36%

63%

37%

75%

25%

77%

23%

INBOUND INBOUND

INBOUNDINBOUND INBOUND

INBOUND

OUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUND

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

56%

44%

60%

40%

64%

36%

63%

37%

75%

25%

77%

23%

INBOUND INBOUND

INBOUNDINBOUND INBOUND

INBOUND

OUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUNDOUTBOUND

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

M&AActivity

European Plastic Packaging M&A update

Report edited by Andre Johnston, with special thanks to Stefan Cooksammy

Contact Us...

Australia

Austria

Belgium

Brazil

Bulgaria

Canada

China

Colombia

Czech Republic

Denmark

Finland

France

Germany

India

Italy

Japan

Luxembourg

Mexico

Netherlands

Norway

Poland

Russia

Singapore

South Africa

Spain

Sweden

Switzerland

Turkey

UK

USA

Internationalcorporate finance

Over 250 transaction professionals based acrossevery key economic location around the world

42 office locations, covering the Americas, Europe,Middle East, Africa, Asia and Australasia

Dedicated industry sector teams, with proven track records and experience

Your local senior corporate finance advisor willalways be your point of contact, connecting you to our partnership

Mergers Alliance is a group of award winning corporate financespecialists who provide high quality advice to organisations who requireinternational reach for their M&A strategies.

Global coverage

Stas MichaelBusiness Manager

Direct Line: +44 (0) 20 7881 2990E: [email protected]

www.mergers-alliance.com

Top Related